FinTech 2026, 5(2), 54; https://doi.org/10.3390/fintech5020054 - 11 Jun 2026

Abstract

Generative artificial intelligence (GAI) is increasingly embedded in personal finance, yet little is known about how models make recommendations using financial information and demographic cues. This study audits three frontier GAI models, GPT 5.5, Gemini 3.1 Pro, and Claude Opus 4.7, using a

[...] Read more.

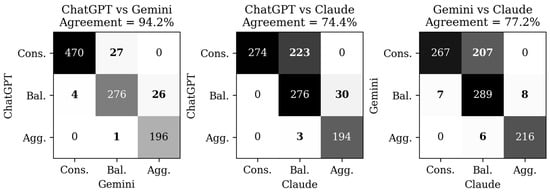

Generative artificial intelligence (GAI) is increasingly embedded in personal finance, yet little is known about how models make recommendations using financial information and demographic cues. This study audits three frontier GAI models, GPT 5.5, Gemini 3.1 Pro, and Claude Opus 4.7, using a conjoint experiment in which each model evaluated the same hypothetical investor profiles and selected among standardized conservative, balanced, and aggressive portfolios. Investor profiles systematically varied attributes, including risk tolerance, time horizon, goal type, income, and age, gender, ethnicity, marital status, and employment type. Ordered logistic regressions and matched-profile comparisons show that all three models base recommendations primarily on financial attributes, especially risk tolerance and time horizon. Age and marital status shift recommendations towards conservatism in all models, conversely only Claude conditions on gender and employment type. Ethnicity exerts no detectable influence on the recommendations of ChatGPT or Claude, but is a small, statistically significant predictor for Gemini, with non-White profiles receiving slightly more conservative recommendations than otherwise identical White profiles. Overall, we find that the models are not interchangeable: they differ significantly in overall risk appetite and in how they translate risk tolerance, time horizon, goal type, and age into portfolio choices, with economically meaningful differences in predicted recommendations for identical clients. These findings suggest that contemporary GAI investment advice is driven mainly by financially relevant attributes, but that demographic sensitivity may appear in model-specific and statistically nuanced ways, alongside a distinct form of platform risk arising from model-specific advisory logic.

Full article

(This article belongs to the Topic Artificial Intelligence Applications in Financial Technology, 2nd Edition)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}