Improving the Performance of Entities in the Mining Industry by Optimizing Green Business Processes and Emission Inventories

,

,

Abstract

:1. Introduction

2. Materials

2.1. Business Process Management (BPM) and Green Business Process Management (GBPM)

2.2. Criteria for Assessing the Performance of Green Business Processes

3. Methods

4. Results

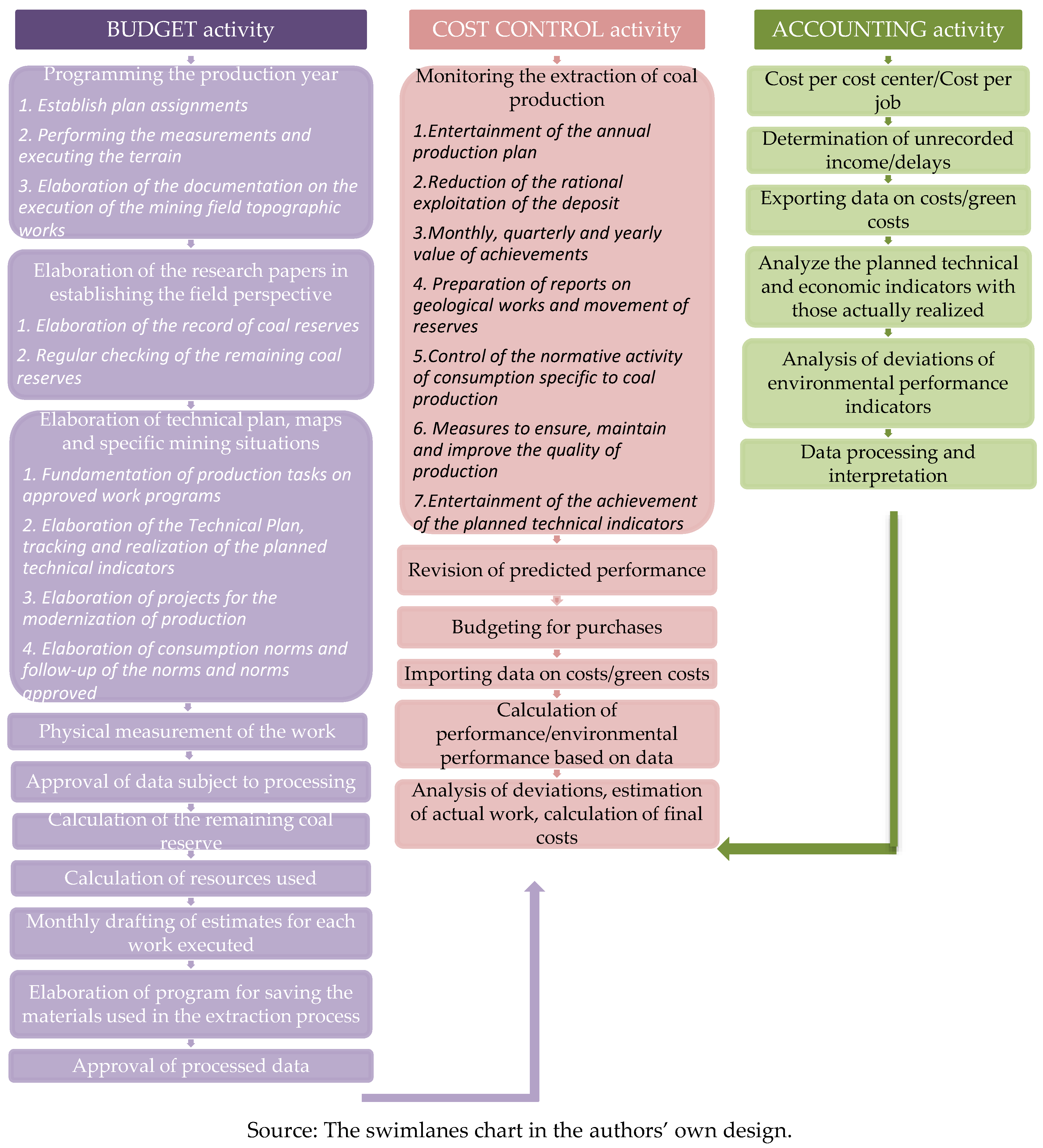

4.1. Presentation of Business Processes Before Optimization

4.2. Business Process Analysis

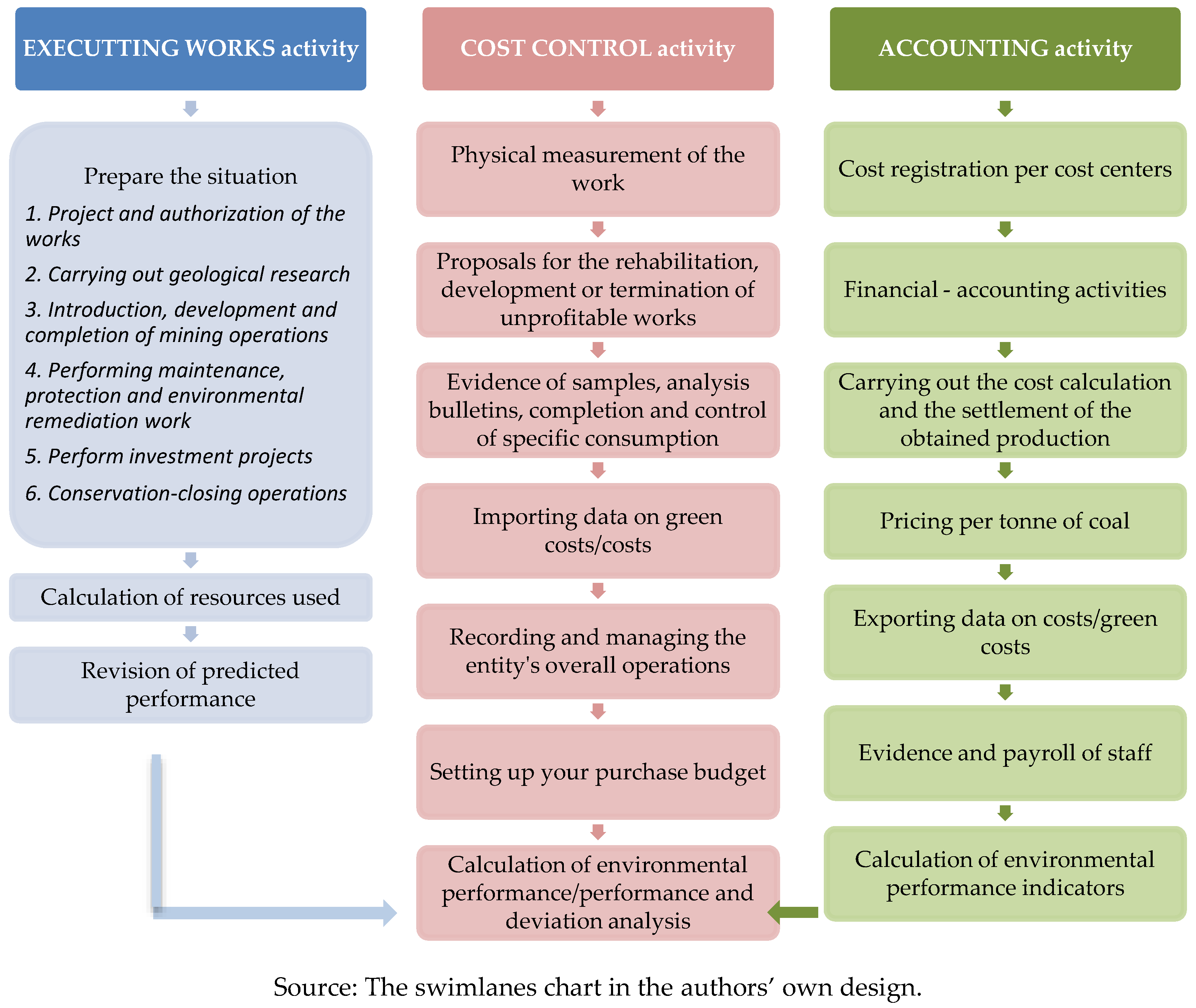

4.3. Presentation of Business Processes After Optimization

5. Discussions

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Galarraga, I.; Gonzalez-Eguino, M.; Rübbelke, D.T.G. Environmental Economics, Climate Change Policy and Beyond: A Tribute to Anil Markandya. Environ. Res. Econ. 2016, 63, 219–224. [Google Scholar] [CrossRef]

- Bréchet, T.; Meunier, G. Are clean technology and environmental quality conflicting policy goals? Resour. Energy Econ. 2014, 38, 61–83. [Google Scholar] [CrossRef] [Green Version]

- Brekke, K.A.; Johansson-Stenman, O. The behavioural economics of climate change. Oxf. Rev. Econ. Policy 2008, 24, 280–297. [Google Scholar] [CrossRef] [Green Version]

- Guest, R. Optimal Pollution Abatement under ‘Sustainable’ and Other Social Time Preferences. Environ. Res. Econ. 2014, 58, 373–390. [Google Scholar] [CrossRef]

- Stoever, J.; Weche, J.P. Environmental Regulation and Sustainable Competitiveness: Evaluating the Role of Firm-Level Green Investments in the Context of the Porter Hypothesis. Environ. Resour. Econ. 2018, 70, 429. [Google Scholar] [CrossRef]

- Combes Motel, P.; Choumert, J.; Minea, A.; Sterner, T. Explorations in the Environment–Development Dilemma. Environ. Resour. Econ. 2014, 57, 479. [Google Scholar] [CrossRef]

- Rosemann, M.; de Bruin, T. Towards a Business Process Management Maturity Model. In Proceedings of the Thirteenth European Conference on Information Systems, Regensburg, Germany, 26–28 May 2005. [Google Scholar]

- Hasan, S.N.M.S.; Kusin, F.M.; Jusop, S.; Yusuff, F.M. Potential of soil, sludge and sediment for mineral carbonation process in selinsing gold mine, Malaysia. Minerals 2018, 8, 257. [Google Scholar] [CrossRef]

- Prior, T.; Giurco, D.; Mudd, G.M.; Mason, L.; Behrisch, J. Resource depletion, peak minerals and the implications for sustainable resource management. Glob. Environ. Chang. 2012, 22, 577–587. [Google Scholar] [CrossRef]

- Ana Karla, M. Genetic Process Mining; CIP-Data Library Technische Universität Eindhoven: Eindhoven, The Netherlands, 2006. [Google Scholar]

- Van der Aalst, W.M.P. Decision Support Based on Process Mining. In Handbook on Decision Support Systems 1; Burstein, F., Holsapple, C.W., Eds.; Basic Themes; Springer: Berlin/Heidelberg, Germany, 2008; pp. 637–657. [Google Scholar]

- Nowak, A.; Leymann, F.; Schumm, D.; Wetzstein, B. An Architecture and Methodology for a Four-Phased Approach to Green Business Process Reengineering. In Information and Communication on Technology for the Fight against Global Warming ICT-GLOW 2011; Kranzlmüller, D., Toja, A.M., Eds.; Lecture Notes in Computer Science; Springer: Berlin/Heidelberg, Germany, 2011; Volume 6868, pp. 150–164. [Google Scholar]

- Pinggera, J.; Zugal, S.; Weidlich, M.; Fahland, D.; Weber, B.; Mendling, J.; Reijers, H. Tracing the Process of Process Modeling with Modeling Phase Diagrams. In Proceeding of the Business Process Management Workshops; Springer: Berlin/Heidelberg, Germany, 2012; pp. 370–382. [Google Scholar]

- Weske, M. Business Process Management-Concepts, Languages, Architectures, 2nd ed.; Springer: Berlin/Heidelberg, Germany, 2012. [Google Scholar]

- Ahlers, D.; Krogstie, J.; Driscoll, P.; Lundli, H.E.; Loveland, S.J.; Rothballer, C.; Wyckmans, A. A workflow Analysis of Greenhouse Gas (GHG) Emission Inventory Methods for Trondheim Municipality; CTT Deliverable; Technical report; NTNU: Trondheim, Norway, 2015. [Google Scholar]

- Thaler, T.; Maurer, D.; De Angelis, V.; Fettke, P.; Loos, P. Mining the Usability of Business Process Modeling Tools: Concept and Case Study. In Proceedings of the Industry Track at the 13th International Conference on Business Process Management, Innsbruck, Austria, 31 August–3 September 2015. [Google Scholar]

- Larsch, S.; Betz, S.; Duboc, L.; Magdaleno, A.M.; Bomfim, C. Integrating Sustainability Aspects in Business Process Management. In Business Process Management Workshops (BPM 2016); Dumas, M., Fantinato, M., Eds.; Lecture Notes in Business Information Processing; Springer: Cham, Switzerland, 2016; Volume 281, pp. 403–415. [Google Scholar]

- Vom Brocke, J.; Mendling, J. Business Process Management Cases: Digital Innovation and Business Transformation in Practice (Management for Professionals), 1st ed.; Springer: Berlin/Heidelberg, Germany, 2018. [Google Scholar]

- Couckuyt, D.; Van Looy, A. Green BPM as a Business-Oriented Discipline: A Systematic Mapping Study and Research Agenda. Sustainability 2019, 11, 4200. [Google Scholar] [CrossRef]

- Opitz, N.; Krüp, H.; Kolbe, L.M. Green Business Process Management—A Definition and Research Framework. In Proceedings of the 47th Hawaii International Conference on System Sciences (HICSS), Waikoloa, HI, USA, 6–9 January 2014; pp. 3808–3817. [Google Scholar]

- World Commission on Environment and Development. Our Common Future; Oxford University Press: Oxford, UK; New York, NY, USA, 1987. [Google Scholar]

- Reiter, M.; Fettke, P.; Loos, P. Towards Green Business Process Management: Concept and Implementation of an Artifact to Reduce the Energy Consumption of Business Processes. In Proceedings of the 2014 47th Hawaii International Conference on System Sciences (HICSS), Waikoloa, HI, USA, 6–9 January 2014; pp. 885–894. [Google Scholar]

- Hammer, M. What is Business Process Management? In Handbook on Business Process Management 1: Introduction, Methods and Information Systems; vom Brocke, J., Rosemann, M., Eds.; Springer: Berlin/Heidelberg, Germany, 2010; pp. 88–101. [Google Scholar]

- Li, S.; Wang, Y. Dynamic Performance Assessment of Primary Frequency Modulation for a Power Control System Based on MATLAB. Processes 2019, 7, 11. [Google Scholar] [CrossRef]

- Remenyi, D.; Money, A.H.; Bannister, F. The Effective Measurement and Management of IT Costs and Benefits, 3rd ed.; Elsevier: Amsterdam, The Netherlands, 2007. [Google Scholar]

- Hatayama, H.; Tahara, K.; Daigo, I. Worth of metal gleaning in mining and recycling for mineral conservation. Miner. Eng. 2014, 76, 58–64. [Google Scholar] [CrossRef]

- Seidel, S.; Recker, J.; vom Brocke, J. (Eds.) Green Business Process Management; Springer: New York, NY, USA, 2012; pp. 3–13. [Google Scholar]

- Nowak, A.; Leymann, F.; Schumm, D. The differences and commonalities between green and conventional business process management. In Proceedings of the 2011 IEEE Ninth International Conference on Dependable, Autonomic and Secure Computing, Sydney, Australia, 12–14 December 2011; pp. 569–576. [Google Scholar]

- Lubbecke, P.; Reiter, M.; Fettke, P.; Loos, P. Simulation-based Decision Support for the Reduction of the Energy Consumption of Complex Business Processes. In Proceedings of the 48th Hawaii International Conference on System Sciences, 5–8 January 2015. [Google Scholar]

- Zambon, I.; Egidi, G.; Rinaldi, F.; Cividino, S. Applied Research towards Industry 4.0: Opportunities for SMEs. Processes 2019, 7, 344. [Google Scholar] [CrossRef]

- Lottermoser, B.G. Mine Wastes: Characterization, Treatment and Environmental Impacts; Springer: Berlin/Heidelberg, Germany, 2010. [Google Scholar]

- Hitch, M.; Ballantyne, S.M.; Hindle, S.R. Revaluing mine waste rock for carbon capture and storage. Int. J. Min. Reclam. Environ. 2010, 24, 64–79. [Google Scholar] [CrossRef] [Green Version]

- McCutcheon, J.; Turvey, C.C.; Wilson, S.A.; Hamilton, J.L.; Southam, G. Experimental deployment of microbial mineral carbonation at an asbestos mine: Potential applications to carbon storage and tailings stabilization. Minerals 2017, 7, 191. [Google Scholar] [CrossRef]

- Nowak, A.; Leymann, F.; Schleicher, D.; Schumm, D.; Wagner, S. Green business process patterns. In Proceedings of the 18th Conference on Pattern Languages of Programs (PLoP ’11), Portland, OR, USA, 21–23 October 2011. [Google Scholar]

- Moran, C.J.; Kunz, N.C. Sustainability as it pertains to minerals and energy supply and demand: A new interpretative perspective for assessing progress. J. Clean. Prod. 2014, 84, 16–26. [Google Scholar] [CrossRef]

- Lundgren, T.; Zhou, W. Firm performance and the role of environmental management. J. Environ. Manag. 2017, 203, 330–341. [Google Scholar] [CrossRef]

- Färe, R.; Grosskopf, S. Modeling undesirable factors in efficiency evaluation: Comment. Eur. J. Oper. Res. 2004, 157, 242–245. [Google Scholar] [CrossRef]

- Lan, Y.C. Reengineering a Green Business. Int. Interdiscip. Stud. 2012, 2, 1–11. [Google Scholar]

- Fu, J. Two-stage data envelopment analysis with undesirable intermediate measures: An application to air quality improvement in China. Cent. Eur. J Oper. Res. 2018, 26, 861. [Google Scholar] [CrossRef]

- Maciel, J.C. The Core Capabilities of Green Business Process Management—A Literature Review. In Proceedings of the 13th International Conference on Wirtschaftsinformatik, St. Gallen, Switzerland, 12–15 February 2017; pp. 1526–1537. [Google Scholar]

- Recker, J.; Rosemann, M.; Hjalmarsson, A.; Lind, M. Modeling and analyzing the carbon footprint of business processes. In Green Business Process Management: Towards the Sustainable Enterprise; Vom Brocke, J., Seidel, S., Recker, J.C., Eds.; Springer: Heidelberg/Berlin, Germany; Dordrecht, The Netherlands; London, UK; New York, NY, USA, 2012; pp. 93–109. [Google Scholar]

- Perez, F.; Sanchez, L.E. Assessing the evolution of sustainability reporting in the mining sector. Environ. Manag. 2009, 43, 949–961. [Google Scholar] [CrossRef]

- Pernici, B.; Aiello, M.; vom Brocke, J.; Donnellan, B.; Gelenbe, E.; Kretsis, M. What IS Can Do for Environmental Sustainability: A Report from CAiSE’11 Panel on Green and Sustainable IS. In Proceedings of the 23rd International Conference on Advanced Information Systems Engineering (CAiSE’11), London, UK, 20–24 June 2011. [Google Scholar]

- Meyer, J.; Teuteberg, F. Nachhaltiges Geschäftsprozessmanagement—Status Quo und Forschungsagenda. In Tagungsband der Multikonferenz der Wirtschaftsinformatik (MKWI); Mattfeld, D., Robra-Bissantz, S., Eds.; Institut für Wirtschaftsinformatik: Braunschweig, Germany, 2012; pp. 1515–1530. [Google Scholar]

- Yeomans, J.S. Efficient generation of alternative perspectives in public environmental policy formulation: Applying co-evolutionary simulation–optimization to municipal solid waste management. Cent. Eur. J. Oper. Res. 2011, 19, 391. [Google Scholar] [CrossRef]

- Rada, E.C.; Zatelli, C.; Cioca, L.I.; Torretta, V. Selective Collection Quality Index for Municipal Solid Waste Management. Sustainability 2018, 10, 257. [Google Scholar] [CrossRef]

- Recker, J. Green, Greener, BPM? BPTrends 2011, 7, 1–8. [Google Scholar]

- Pavlovčič-Prešeren, P.; Stopar, B.; Sterle, O. Application of different radial basis function networks in the illegal waste dump-surface modelling. Cent. Eur. J. Oper. Res. 2019, 27, 783–795. [Google Scholar] [CrossRef]

- Rozman, T.; Draghici, A.; Riel, A. Achieving Sustainable Development by Integrating It into the Business Process Management System. In Systems, Software and Services Process Improvement; European Conference on Software Process Improvement EuroSPI; Springer: New York, NY, USA, 2015; pp. 247–259. [Google Scholar]

- Houy, C.; Reiter, M.; Fettke, P.; Loos, P.; Hoesch-Klohe, K.; Ghose, A. Advancing business process technology for humanity: Opportunities and challenges of green BPM for sustainable business activities. In Green Business Process Management; Springer-Verlag: Berlin/Heidelberg, Germany, 2012; pp. 75–92. [Google Scholar]

- Wesumperuma, A.; Ginige, A.; Ginige, J.; Hol, A. Green activity based management (ABM) for organisations. In Proceedings of the 24th Australasian Conference on Information Systems (ACIS), Melbourne, Australia, 4–6 December 2013; pp. 1–11. [Google Scholar]

- Zhu, X.; Zhu, G.; vanden Broucke, S.; Recker, J. On Merging Business Process Management and Geographic Information Systems: Modeling and Execution of Ecological Concerns. In Geo-Informatics in Resource Management and Sustainable Ecosystem; Springer: New York, NY, USA, 2015; pp. 486–496. [Google Scholar]

- Ghose, A.; Hoesch-Klohe, K.; Hinsche, L.; Le, L.S. Green business process management: A research agenda. Australas. J. Inf. Syst. 2010, 16, 103–117. [Google Scholar] [CrossRef]

- Mars, P. Learning Algorithms: Theory and Applications in Signal Processing, Control and Communications; CRC Press: Boca Raton, FL, USA, 2018. [Google Scholar]

- Opitz, N.; Erek, K.; Langkau, T.; Kolbe, L.; Zarnekow, R. Kick-starting Green Business Process Management—Suitable Modeling Languages and Key Processes for Green Perfomance Mesaurement. In Proceedings of the AMCIS 2012 Proceedings, Seattle, WA, USA, 9–12 August 2012. [Google Scholar]

- Watson, R.T.; Howells, J.; Boudreau, M.C. Energy Informatics: Initial Thoughts on Data and Process Management. In Green Business Process Management; Springer: New York, NY, USA, 2012; pp. 147–159. [Google Scholar]

- Lazarevic, D.; Buclet, N.; Brandt, N. The application of life cycle thinking in the context of European waste policy. J. Clean. Prod. 2012, 29, 199–207. [Google Scholar] [CrossRef]

- Houy, C.; Reiter, M.; Fettke, P.; Loos, P. Towards Green BPM—Sustainability and Resource Efficiency through Business Process Management. In Proceedings of the 8th International Conference on Business Process Management—BPM Workshops, Hoboken, NJ, USA, 13–16 September 2010; pp. 501–510. [Google Scholar]

- Rojanschi, V.; Grigore, F.; Ciomoş, V. Guide to Environmental Assessor and Auditor; Economic Publishing House: Bucharest, Romania, 2008. [Google Scholar]

- Yuan, Z.; Bi, J.; Yuichi, M. The circular economy: A new development strategy in China. J. Ind. Ecol. 2014, 10, 4–8. [Google Scholar] [CrossRef]

- Fodor, D. The influence of the mining industry on the environment. AGIR Bull. 2006, 3, 2–13. [Google Scholar]

- Wesumperuma, A.; Ginige, J.A.; Ginige, A.; Hol, A. A framework for multi-dimensional business process optimization for GHG emission mitigation. In Proceedings of the Australasian Conference on Information Systems (ACIS 2011): Identifying the Information Systems Discipline, Sydney, Australia, 30 November–2 December 2011. [Google Scholar]

- Martinescu Oprea, D.-M.; Căpuşneanu, S. Concentrations and annual scheme of particular matter in Slatina municipality area. Rom. Stat. Rev. 2010, 9, 31–34. [Google Scholar]

- Radulescu, C. Pollutant Emissions. Methods for Reducing Them; Bibliotheca Publishing House: Targoviste, Romania, 2008. [Google Scholar]

- Norgate, T.E.; Haque, N. Energy and greenhouse gas impacts of mining and mineral processing operations. J. Clean. Prod. 2010, 18, 266–274. [Google Scholar] [CrossRef]

- Popescu, M.; Popescu, M. Applied Ecology; Matrix Rom Publishing House: Bucharest, Romania, 2000. [Google Scholar]

- Environmental Protection Agency 2017. Available online: http://apmhd.anpm.ro/web/apm-hunedoara/acasa (accessed on 14 November 2018).

- Petrakis, E.; Xepapadeas, A. Location decisions of a polluting firm and the time consistency of environmental policy. Resour. Energy Econ. 2003, 25, 197–214. [Google Scholar] [CrossRef]

- Canton, J.; Soubeyran, A.; Stahn, H. Environmental Taxation and Vertical Cournot Oligopolies: How Eco-industries Matter. Environ. Resour. Econ. 2008, 40, 369. [Google Scholar] [CrossRef]

- Pactwa, K.; Wozniak, J. Environmental reporting policy of the mining industry leaders in Poland. Resour. Policy 2017, 53, 201–207. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Questions | Category of Respondents | ||||

|---|---|---|---|---|---|

| Specialists | Management | ||||

| Yes | No | Yes | No | ||

| (1) Does green business process management help make your business more efficient? | 132 | 31 | 39 | 7 | |

| (2) What is the modern method for determining pollutant emissions used in your company? | |||||

| (a) Emission inventory method * | 89 | 74 | 34 | 12 | |

| (b) Emission annotations ** | 92 | 71 | 28 | 18 | |

| (c) Activity-Based Emissions (ABE) *** | 67 | 96 | 25 | 21 | |

| (3) What are the cost and performance benefits for your company? | |||||

| (a) Reduction of operational environmental costs | 101 | 62 | 30 | 16 | |

| (b) Increase in profit | 98 | 65 | 28 | 18 | |

| (c) Reliable information | 83 | 80 | 27 | 19 | |

| Process Type | Activities | Operations | Level of Competence | Employees | Costs (Thousands RON) |

|---|---|---|---|---|---|

| Execution of mining works | Budgeting | Programming the production year | Management | 3 | 25,286 |

| Elaboration of the research papers in establishing the field perspective | Technical | 5 | 45,578 | ||

| Elaboration of technical plan, maps and specific mining situations | Technical | 5 | 188,905 | ||

| Physical measurement of the work | Technical | 1 | 13,777 | ||

| Approval of data subject to processing | Technical | 1 | 21,987 | ||

| Calculation of the remaining coal reserve | Technical | 1 | 21,247 | ||

| Calculation of resources used | Technical | 1 | 21,875 | ||

| Monthly drafting of estimates for each work executed | Technical | 1 | 12,569 | ||

| Elaboration of program for saving the materials used in the extraction process | Technical | 3 | 14,862 | ||

| Approval of processed data | Technical | 1 | 12,245 | ||

| 22 | 378,331 | ||||

| Business Process: Cost of the Mining Work | |||||||

|---|---|---|---|---|---|---|---|

| Budget Activity | Costs (Thousands RON) | Differences (Thousands RON) | |||||

| Before Optimization | After Optimization | ||||||

| 2016 | 2016 | 2017 | 2018 | 2016 | 2017 | 2018 | |

| Programming the production year | 25,286 | 25,286 | 24,156 | 23,965 | 0 | −1.13 | −0.191 |

| Elaboration of the research papers in establishing the field perspective | 45,578 | 45,578 | 44,775 | 43,902 | 0 | −0.803 | −0.873 |

| Elaboration of technical plan, maps and specific mining situations | 188,905 | 188,905 | 187,883 | 187,275 | 0 | −1.022 | −0.608 |

| Physical measurement of the work | 13,777 | 13,777 | 13,226 | 13,158 | 0 | −0.551 | −0.068 |

| Approval of data subject to processing | 21,987 | 0 | 0 | 0 | −21,987 | 0 | 0 |

| Calculation of the remaining coal reserve | 21,247 | 0 | 0 | 0 | −21,247 | 0 | 0 |

| Calculation of resources used | 21,875 | 21,875 | 20,173 | 20,156 | 0 | −1.702 | −0.017 |

| Monthly drafting of estimates for each work executed | 12,569 | 12,569 | 11,906 | 11,298 | 0 | −0.663 | −0.608 |

| Elaboration of program for saving the materials used in the extraction process | 14,862 | 0 | 0 | 0 | −14,862 | 0 | 0 |

| Approval of processed data | 12,245 | 12,245 | 11,964 | 11,875 | 0 | −0.281 | −0.089 |

| Total | 378,331 | 320,235 | 314,083 | 311,629 | −58,096 | −6.152 | −2.454 |

| Suspensions (mg/mc)—Short-Term Average (30 min) | ||||

|---|---|---|---|---|

| Control Point | Sterile Transport Stream | Charging Coal in Wagons | Fan Station | Car Transport |

| September 2016 | 0.16 | 0.13 | 0.08 | 0.08 |

| September 2017 | 0.13 | 0.11 | 0.00 | 0.11 |

| September 2018 | 0.11 | 0.09 | 0.00 | 0.08 |

| September monthly average | 0.13 | 0.11 | 0.02 | 0.09 |

| Allowed limit value | 0.50 | 0.50 | 0.50 | 0.50 |

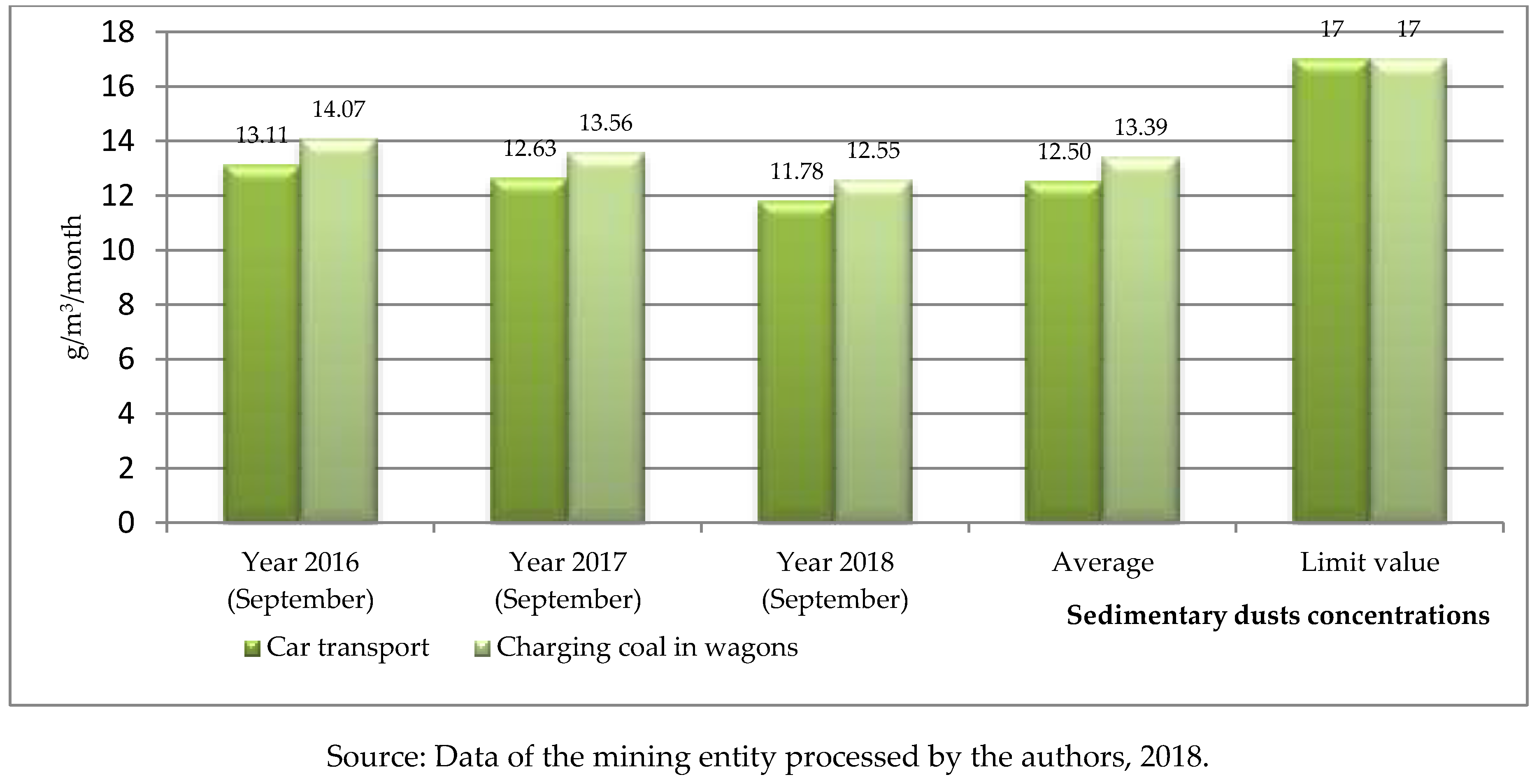

| Sedimentary Dusts (g/m2)—Monthly Average Determination | ||

|---|---|---|

| Control Point | Car Transport | Charging Coal in Wagons |

| September 2016 | 13.11 | 14.07 |

| September 2017 | 12.63 | 13.56 |

| September 2018 | 11.78 | 12.55 |

| September monthly average | 12.50 | 13.39 |

| Allowed limit value | 17.00 | 17.00 |

| Indicator | M.U. | Year | Deviations | |||

|---|---|---|---|---|---|---|

| 2016 | 2017 | 2018 | 2016/2017 | 2017/2018 | ||

| Electricity produced | MWh | 1,842,437 | 1,422,566 | 1,516,271 | −419,871 | +93,705 |

| Delivered electricity | MWh | 1,658,411 | 1,281,964 | 1,356,904 | −376,447 | +74,940 |

| Sold electricity | MWh | 1,733,959 | 1,409,925 | 1,607,235 | −324,034 | +197,310 |

| Purchased and resold energy | MWh | 85,409 | 130,346 | 140,468 | +44,937 | +10,122 |

| Thermal energy produced | Gcal | 337,783 | 266,978 | 315,475 | −70,805 | +48,497 |

| Thermal energy delivered | Gcal | 155,504 | 103,074 | 121,346 | −52,430 | +18,272 |

| Coal delivered to power plants | Gcal | 3,272,701 | 2,622,120 | 2,878,206 | −650,581 | +256,086 |

| Gross margin on sales (gross sales profit/ turnover), where: | − | −0.316 | −0.212 | 0.297 | −0.104 | +0.084 |

| 1. Income from the sale of electricity | Thousands RON | 491,537,172 | 375,085,877 | 383,996,256 | −116,451,295 | +8,910,379 |

| 2. Income from the sale of heat, from which: | Thousands RON | 19,478,253 | 16,892,749 | 18,425,690 | −2,585,504 | +1,532,941 |

| -Thermal energy subsidy according to O36/2006 | Thousands RON | 1,365,986 | 1,336,193 | 1,287,798 | −29,793 | −48,395 |

| 3. Other Income | Thousands RON | 14,769,321 | 12,095,950 | 14,167,489 | −2,673,371 | +2,071,539 |

| Total | Thousands RON | 525,784,746 | 404,074,576 | 416,589,435 | −121,710,170 | +12,514,859 |

| Profit (loss) | Thousands RON | −1,661,612 | −858,352 | +1,235,337 | −803,260 | +376,985 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oncioiu, I.; Căpuşneanu, S.; Oprea Constantin, D.-M.; Türkeș, M.C.; Topor, D.I.; Bîlcan, F.R.; Petrescu, A.G. Improving the Performance of Entities in the Mining Industry by Optimizing Green Business Processes and Emission Inventories. Processes 2019, 7, 543. https://doi.org/10.3390/pr7080543

Oncioiu I, Căpuşneanu S, Oprea Constantin D-M, Türkeș MC, Topor DI, Bîlcan FR, Petrescu AG. Improving the Performance of Entities in the Mining Industry by Optimizing Green Business Processes and Emission Inventories. Processes. 2019; 7(8):543. https://doi.org/10.3390/pr7080543

Chicago/Turabian StyleOncioiu, Ionica, Sorinel Căpuşneanu, Dana-Maria Oprea Constantin, Mirela Cătălina Türkeș, Dan Ioan Topor, Florentina Raluca Bîlcan, and Anca Gabriela Petrescu. 2019. "Improving the Performance of Entities in the Mining Industry by Optimizing Green Business Processes and Emission Inventories" Processes 7, no. 8: 543. https://doi.org/10.3390/pr7080543