Towards a Balanced Sustainability Vision for the Coffee Industry

1

President of 4.0 Brands. Former President of oriGIn and former CMO of Federación Nacional de Cafeteros de Colombia, Bogotá 110221, Colombia

2

Department of Economics and Social Sciences, University of Natural Resources and Life Sciences (BOKU), Vienna, Feistmantelstraße 4, 1180 Vienna, Austria

*

Author to whom correspondence should be addressed.

Resources 2017, 6(2), 17; https://doi.org/10.3390/resources6020017

Submission received: 22 November 2016

/

Revised: 23 March 2017

/

Accepted: 24 March 2017

/

Published: 5 April 2017

(This article belongs to the Special Issue Sustainable Supply Chain Management)

{kind=link}

{kind=link}

{kind=link}

Abstract

:As one of the world’s most traded agricultural commodities, coffee constitutes a significant part of the overall economy and a major source of foreign revenue for many developing countries. Coffee also touches a large portion of the world’s population in the South, where it is mainly produced, and in the North, where it is primarily consumed. As a product frequently purchased by a significant share of worldwide consumers on a daily basis in social occasions, the coffee industry has earned a high profile that also attracts the interest of non-governmental organizations, governments, multilateral organizations and development specialists and has been an early adopter of Voluntary Sustainability Standards (VSS). Responding to the trend of increased interest on sustainability, it is therefore not surprising that coffee continues to be at the forefront of sustainability initiatives that transcend into other agricultural industries. Based on literature and authors’ experiences, this article reflects on the VSS evolution and considers a sustainability model that specifically incorporates producers’ local realities and deals with the complex scenario of sustainability challenges in producing regions. Agreeing on a joint sustainability approach with farmers’ effective involvement is necessary so that the industry as a whole (up and downstream value chain actors) can legitimately communicate its own sustainability priorities. This top-down/bottom-up approach could also lead to origin-based, actionable and focused sustainability key performance indicators, relevant for producers and consistent with the UN’s Sustainable Development Goals. The initiative also aims to provide a sustainability platform for single origin coffees and Geographical Indications (GIs) in accordance with growers’ own realities and regions, providing the credibility that consumers now expect from sustainability initiatives, additional differentiation options for origin coffees and economic upgrade opportunities for farmers.

1. Introduction

Coffee is a high profile product that touches a large portion of the world’s population. It is estimated that 25 million mostly small scale farmers, mainly located in subtropical and equatorial regions (Figure 1) [1], produce the beans that are part of the estimated well over 2.25 billion coffee cups consumed every day around the world. According to the US National Coffee Association, 76% of adult Americans consume coffee [2], while the European Coffee Federation asserts that consumers from that continent have the highest per capita consumption in the world [3]. As one of the most traded agricultural commodities internationally, it constitutes a significant part of the overall economy and a major source of foreign exchange revenue for many developing countries [1,4].

The last few decades have brought significant changes to the coffee industry. As a result of the abolishment of the economic clauses of the International Coffee Agreement (ICA) in 1989 [6,7,8] and the expanding supply of Brazil and Vietnam, an ensuing period of low and more volatile green (unroasted) coffee prices brought very difficult times to millions of producers in over 40 countries. At the beginning of the 21st century, coffee growers faced the lowest real prices on record for their beans during the “coffee crisis” period.

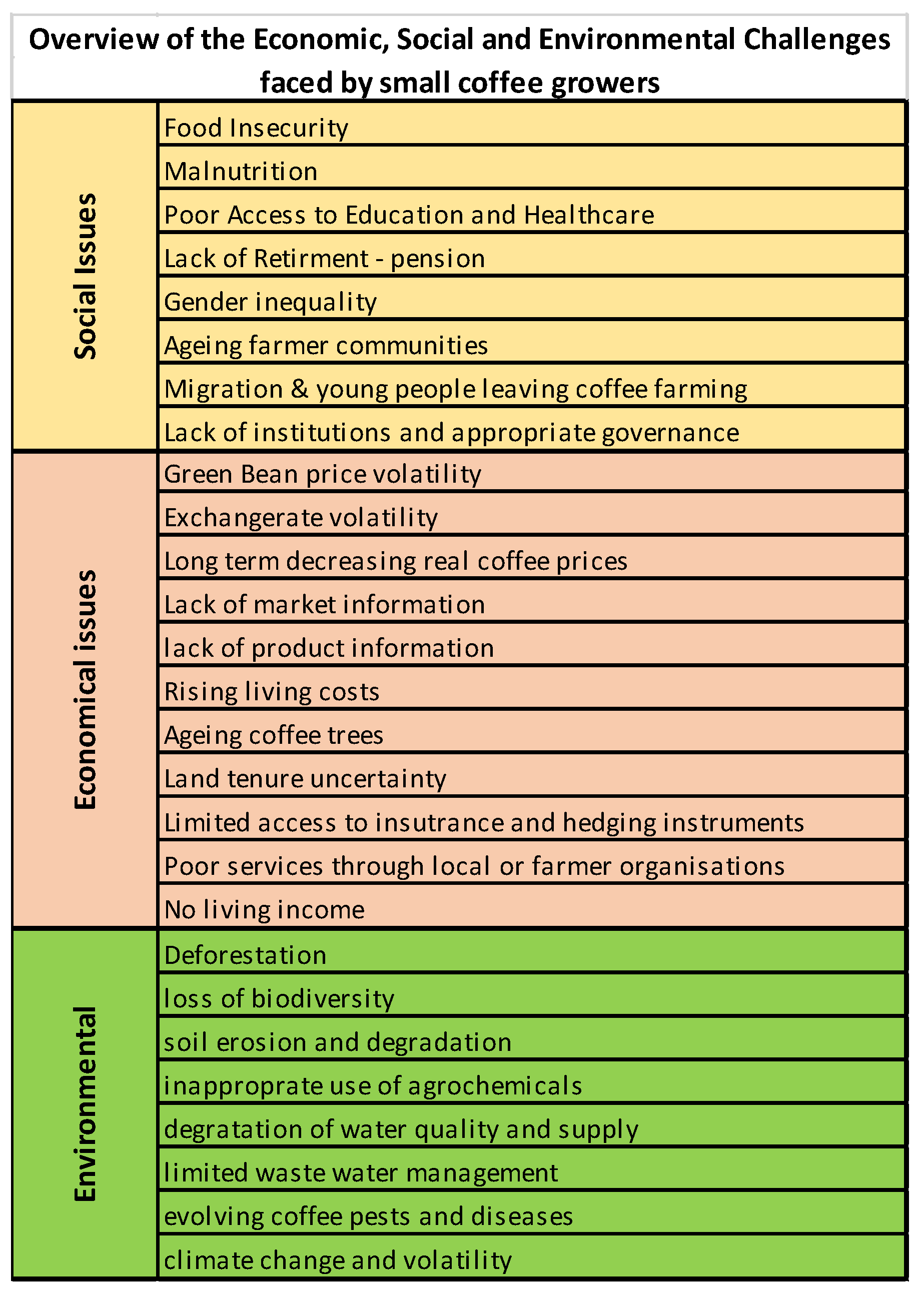

Low and volatile prices for green coffee are not the only challenges that growers face. They also have to contend with social issues such as food insecurity, ageing farmer communities, migration and young people leaving to the cities and the poor social and economic conditions of coffee harvesters; economic topics that include low productivity, ageing coffee trees, expensive fertilizers, lack of market information, poor direct market access; and environmental challenges such as soil erosion and degradation, changing climate conditions and poor waste water management among many other factors [1] (Figure 2). Most farmers also lack adequate institutional support from their local or national governments in the form of public goods [1,9]. The complexity of these challenges over the last few decades and the coffee crisis forced governments, grower organizations, development agencies and individual farmers to reevaluate their strategies and focus on higher priced beans [10].

From a demand perspective, major importing countries in the North saw in parallel significant changes in consuming patterns. The market liberalization gave way to a more dynamic and expanding specialty coffee segment that catered to more sophisticated consumers and was able to pay higher premiums over commercial coffees sold in traditional grocery distribution channels [6,11]. Well known gourmet and specialty brands became a major factor in altering demand patterns in a period of low prices, and pressure intensified on coffee brands to develop programs and initiatives to support coffee growing communities [12,13].

1.1. The Evolving Voluntary Sustainability Standards Landscape

To face the fierce competition and price fluctuations of commodity coffee, growers saw an opportunity to differentiate their beans and access higher prices through Voluntary Sustainability Standards (VSS) [14,15]. This option was particularly relevant during the coffee crisis, a period that brought significant social and economic challenges for most producing countries. The farmers’ difficulties were widely reported in the media and academic literature, generating increased scrutiny to high profile brands and prompting Non-Government Organisations (NGOs) and consumer advocates to press for the adoption of farmer support programs [11,16,17,18], among many others). Many of these brands shared these objectives and began their path to sustainability of their supply chain through different certification schemes that provided them with additional differentiation attributes and reduced their reputational risks [1,8,14,19,20,21,22].

The VSS model therefore arrived at the right time to the right industry. If one takes into account the number of producers, consumers, brands, coffee shop outlets and clients, as well as those that work in the farms and its different distribution and processing channels, it would be difficult to find a product with as many stakeholders. Thus, the high profile of the coffee industry, the fact that producing countries mainly sold green coffee at very low prices and the novel differentiation initiatives for gourmet coffee consumption created the ideal “breeding ground” for VSS to take hold and become a reference point to other industries. Currently, the most notable coffee VSS include Nespresso’s AAA, 4C Association, Starbucks C.A.F.E. Practices, Fairtrade, Organic, Rainforest Alliance and UTZ Certified. The coffee industry therefore became a leading example of VSS adoption in agriculture and some of these models were adopted in the banana, tea, cocoa or flower industries, to mention just a few examples.

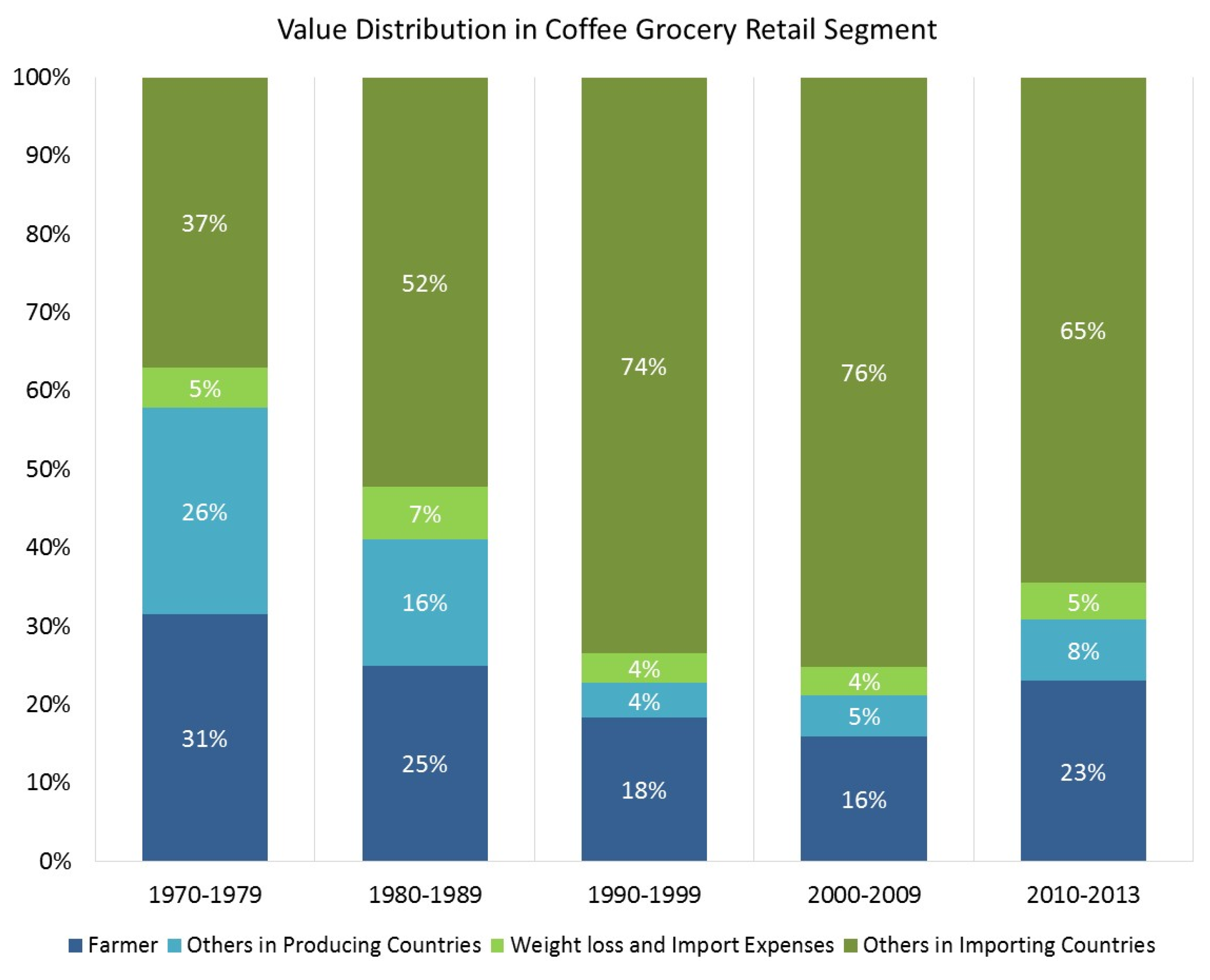

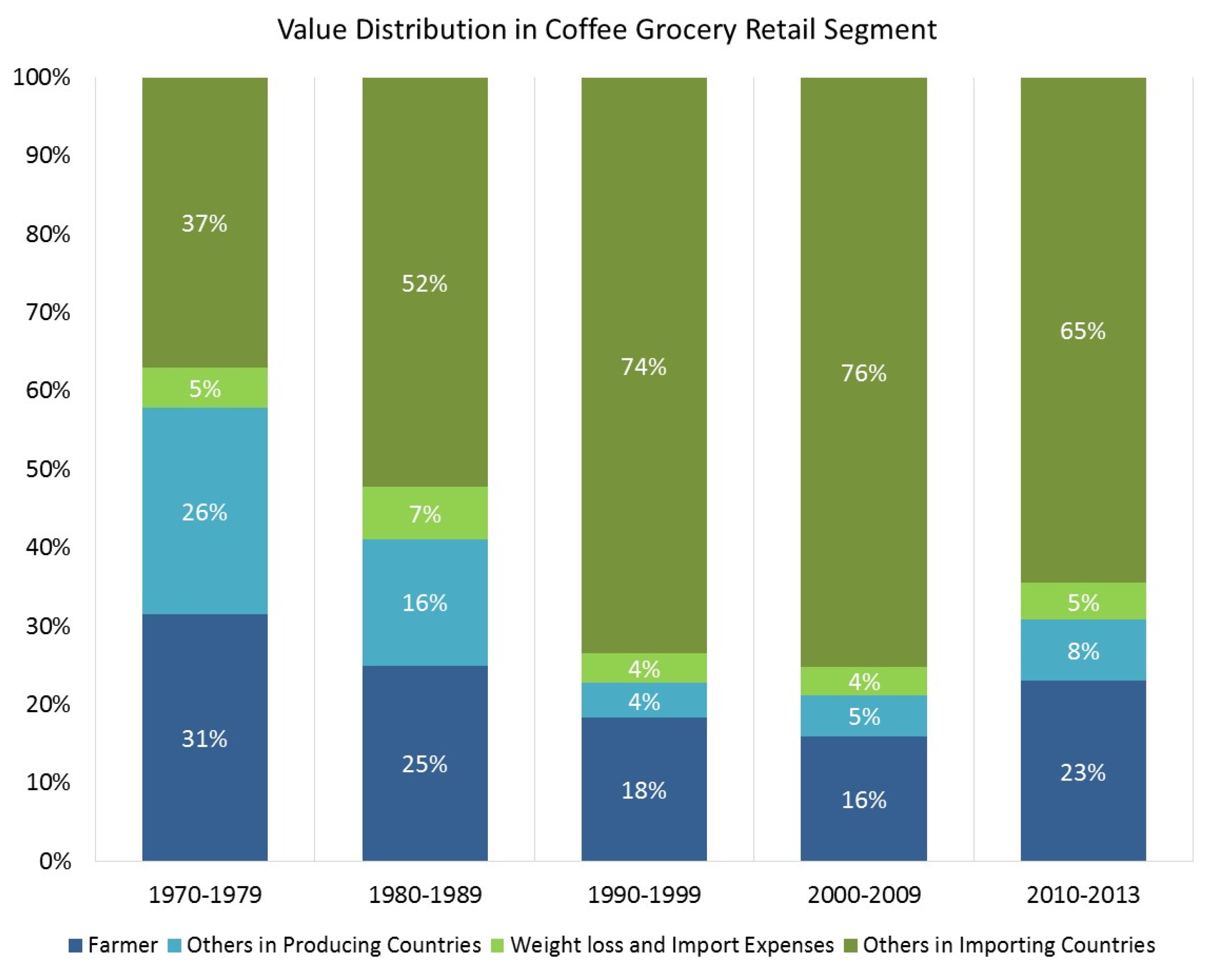

Despite these efforts, coffee growers have not been able to capture a higher portion of the coffee industry’s overall income, while international roasters and brand owners located in consuming countries have increased their revenue share of the industry in all consumer segments [23,24]. This is not only the case for the grocery retail segment (Figure 3) but more so in the higher end specialty out-of-home consumption segments. As explained by what has been termed as the coffee paradox, in many cases, what growers sell and what consumers get in specialty channels are different products [6]. The evolving specialty coffee industry has been able to position itself by selling higher quality coffees in more sophisticated environments, providing novel consumption occasions and satisfying more complex consumer needs for which consumers are willing to pay, which surpass the basic need for energy (caffeine fix) associated with coffee consumption of mainstream brands. Daviron and Ponte argue that, apart from the beans, coffee consumers mostly pay for the symbolic quality and in-person services reflected in the final price of specialty coffee sold at coffee shops or high-end stores. While coffee sold by the cup in specialized shops incurs higher costs other than the coffee itself, and, therefore, the additional revenue generated cannot automatically be considered a profit by the coffee shop operator, the new distribution channels clearly provided opportunities for value generation and appropriation for new brands in these novel segments. VSS also played a role in the positioning of these higher end brands. The symbolic quality to which Daviron and Ponte refer to not only includes the ambiance and consumption environment but also information that such brands provide to substantiate their higher prices. In this sense, VSS became a medium to provide assurance, communication, credibility and differentiation value to specialty brands.

In the meantime, the commercial non-gourmet brands selling to traditional distribution channels faced a growing concentration of grocery chains [25] and an increased competition of private label store brands. As VSS became more prevalent in specialty channels, mainstream brands also began to face significant stakeholder pressure to adopt VSS policies [26]. This resulted after a few years in a “mainstreamization” of VSS coffees and an expanded market with lower premiums for coffee growers. This competitive environment continued to exert pressure on the global coffee value chain, leaving limited possibilities for paying significant premiums for VSS compliant coffees and for farmers to achieve an economic upgrade other than by increasing productivity. Although it is arguable that achieving scale of VSS coffees is desirable, this came at the cost of reducing economic incentives for coffee farmers to adopt these standards and affecting the differentiating features that VSS provided to higher-end segments.

The adoption of VSS and the higher interest in quality coffee were key features of the expansion of the coffee industry in the last 30 years. Since 2011, the average annual growth rate in global coffee consumption has continued to increase at a rate of 2.5% per annum [5]. This process has taken place amid consolidation of major industrial players as major roasting mainstream brands controlling distribution channels continued to achieve a higher market share in many countries [27]. From the VSS coffees perspective, in 2013, sales of coffee complying with voluntary coffee standards grew to between 10% [28] and 15% of total coffee consumption [1]. Large coffee roasters (e.g., Nestlé, Starbucks, or Lavazza) have pledged to increase their offtake of VSS coffees. Although the sustainability plans for a major new player after the last wave of consolidation, JaconbsDouweEgberts, are still unclear, it would appear that there is still room for growth for the VSS coffee market [1].

These trends are also confronted with the mixed results of the benefits of VSS in producing regions. While in some cases they show monetary (e.g., price premiums, higher productivity), social (e.g., creation of growers’ organizations, knowledge) or environmental benefits [9], the result of available impact studies are not as conclusive [29]. Critical voices present VSS as strategies from the North limiting the local scope of decision making, imposing high transaction costs on growers and squeezing out small-holders not being able to comply with certification standards [9,14,30]. In the context of diverse types of growers, processors, consumers and a variety of standards, all having their own peculiarities, strengths, limitations and views on what is the best approach for scaling up, policy-makers, managers and organizations advocating for VSS coffees face difficult choices as to which path to pursue [21,31]. In addition, the presence of VSS in the mainstream segments has not significantly changed the competitive dynamics of major roasters selling in traditional channels. They continue to use their brands, economies of scale and distribution capacity as key competitive factors and have opted for VSS as a form of protection of brand reputation.

On the other hand, VSS mainstreamization has brought challenges to specialty coffee brands. As VSS symbols are used by mainstream brands, they lose their differentiating appeal for higher end coffees and reinforce the importance of the standard as opposed to the importance of the coffee origin. Coffee farmers appear to be trapped under these “differentiating from above” and “differentiating from the middle” efforts [32,33] established by brands and other actors in the value chain, which are viewed as top-down laid-out rules that do not allow for their own differentiation and long term economic upgrading. As many realize that these strategies do not necessarily bring growers long term benefits as VSS segments expand, they question whether VSS is an effective tool for their own financial sustainability. Clearly, they face difficult scenarios to achieve economic upgrade and profitability.

1.2. The Role of Geographical Indications

In this context, over the last 10 years, a new trend of sophisticated and independent coffee shops focusing on single origin and direct trade coffees began to influence the whole industry. The so called “third coffee wave” movement is skeptical of VSS coffees, favors direct origin contacts and developing partnerships with growing communities while finding very high quality coffees that can be sold together with the content of how they were found and procured.

In parallel, growers have also begun to use Geographical Indications (GIs) as a form of developing conditions to protect their coffee origin reputations and capture more value (e.g., Colombia (Café de Colombia, Café de Nariño), the Dominican Republic (Café Valdesia), Guinea (Ziama–Macenta coffee), Jamaica (Blue Mountain) or Mexico (Café Veracruz)). With GIs and other intellectual property tools such as certification marks, collective marks or trademarks (as in the case of Sidamo from Ethiopia), growers and processors are focusing on differentiating, protecting and labeling their coffee [34,35] with origin branding initiatives that can be classified as “differentiation from below” efforts [29,30,31,32,33].

The GI protection aims to avoid appropriation of geographical names by groups or users not linked to the area. There are cases in which large companies located outside of the production region might take advantage of the quality reputation of products originated in a given region and erode the benefits of origin production systems [36,37]. Well-known origins in different industries such as cheese, wines or spirits have used GIs as a measure to avoid unfair competition and free-riding of their quality reputation, empowering local producers to define the specific rules for using the origin label [38,39,40]. Thus, GIs are based on the principle that the equity and quality reputation associated with a given origin belongs primarily to the producers located in that region. Therefore, the implementation of GIs represent a bottom-up and differentiation from below effort, and an option for growers to protect their reputation and a possibility to provide symbolic value. GI recognition can also limit unfair competition, enforce quality standards and therefore provide conditions for long-term differentiation to access a higher value for origin products. Nevertheless, promoting and defending GIs are long-term efforts that, just like brands, require consistency and strategic planning. Clearly. GI protection does not always imply an increase in prices after registration, just like registering a trademark does not necessarily mean that it makes it automatically more valuable.

The third wave segment has given growers a possibility to accrue higher prices for high quality coffees in relation to the premiums provided by VSS compliant beans (There are several trade references to single coffees in the 3rd wave segment with or without VSS. Some useful sources https://www.allianceforcoffeeexcellence.org/en/, http://transparenttradecoffee.org/insights and http://www.pqc.coffee/serendipty.). The success of single origin coffees in this segment has created a renovated launch pad for GIs in the coffee category, influencing the product portfolio of other specialty and traditional segments that have also started to launch single origin coffees. Although the definition of single-origin coffees is not exactly laid out, these trends certainly constitute a new market opportunity for coffee GIs to provide transparency regarding the place of production or higher quality [41]. Whereas most mainstream brands used to base their portfolio on blends of different origins, they are now expected to have more product diversity.

However, GIs still lack a concrete sustainability platform. As it is clear that markets, consumers and above all local stakeholders expect more from brands and GIs in terms of sustainability, deciding on what GI sustainability strategy must be pursued is not an easy choice. On the one hand, VSS may offer ready off-the-shelve solutions to accommodate GI sustainability information needs with some degree of consumer awareness. On the other hand, adopting VSS for GIs may imply that origin branding initiatives abandon their bottom-up approach, giving priority to external stakeholder considerations over the expectations of local communities.

1.3. A Necessary Debate

Clearly the coffee industry is at a crucial moment to define the best sustainability strategy going forward. The time has come for revisiting, revaluating and improving coffee sustainability and differentiation models that can be more relevant to coffee origins. This implies additional responsibilities to coffee industry members to continuously improve the current tools to pursue an economic, social, governance and environmental sustainability for all actors in the supply chain.

This paper, based on literature review and previous work and experiences of the authors, attempts to enrich this debate. Our main objective is to present and discuss a path towards an inclusive sustainability agreement among supply chain actors that can provide economic upgrade opportunities for farmers. We also aim to further promote critical voices and increase the debate to find alternatives to the complex situation for the large portion of coffee farmers that still are far from profitable [42]. Our interest is not only to advocate for coffee growers to improve their social, economic, institutional and environmental conditions. We are conscious that their future also depends on the ability to enhance dialogue and create value for all industry members, so we aim for a balanced discussion that can lead to more focused and well prioritized sustainability investments and performance indicators, relevant to the largest possible number of farmers in producing countries.

Our next section discusses the recent developments and difficulties that VSS has faced over the last few decades. Afterwards, we review how the need to provide information on sustainability through different sustainability reporting frameworks is currently being satisfied by some market actors. We then discuss a proposed complementary sustainability model, and, finally, conclusions are drawn.

2. Voluntary Sustainability Standards and Value Chain Governance

The value chain analysis proposed by Gereffi [43,44] involves at least four dimensions: the input–output structure, the geographical coverage, the institutional framework under which value chain actors develop their activities and their governance structure. The input–output structure describes the stages of production. In the case of coffee, it deals with the harvesting, drying, exports, roasting and sales. The geographical dimension deals with the spatial component, where the stages of production are performed. The institutional framework surrounds the chains by regarding the local, domestic and international circumstances and policies around the commodity chain. The form of governance explains how the chain is controlled and coordinated (e.g., what stakeholders have a say in what decisions). These dimensions serve as a device to contextualize the debate about a possible sustainability agreement among supply chain coffee actors.

The coffee value chain has experienced significant changes in the last few decades, with an increased importance of out-of-home consumption and higher priced coffees that require different processes and, and as noted previously, more sophisticated environments where symbolic value can be conveyed. On the geographic front, clearly the coffee industry’s international impact has continued to grow, both in terms of production (with countries such as Vietnam, China and lately Myanmar as new sourcing regions), as well as in consumption by more East Europeans, Asiatic and producing country consumers. While these changes are clearly important, the more profound institutional changes that resulted from the collapse of the International Coffee Agreement (ICA) in 1989 have made a more significant impact to the coffee value chain. The absence of government intervention provided the conditions for private operators, civil society and third party certifiers to gain an increased influence in the coffee industry. Thus, the decreasing leverage of state-driven organizations dealing with transnational policies in the coffee sector resulted in key changes in the governance of the international coffee value chain [6,16,45,46].

As the coffee sector witnessed the emergence of VSS [15], other governance relations along the chain emerged for certain segments. In a form of a captive value chain governance [29,47], coffee growers received support to achieve VSS certifications, but they still depended on market demand and buyer’s decisions to acquire their certified coffees at varying premiums. As many product lines were still based on blends, the cost of switching suppliers of VSS coffees was still low for roasters. Despite these shortcomings, a process of adoption of VSS to counter the low coffee prices started in major producing countries, with varying degrees of success. However, the new governance conditions for these segments did not significantly alter the coffee farmer’s strategic ability to differentiate and capture more value [48]. Thus, like in most commodities under free market conditions, the coffee industry value chain is now mostly described as a market or buyer driven governance chain that limits the potential economic upgrade opportunities for farmers [49].

On the demand front, VSS were key to satisfying the needs of a more curious and responsible consumer that required “credence” or “clean” labels [29,32,50,51,52,53,54,55,56]. VSS labels provided end users with reasonable expectations of transparent labeling, complete information and compliance. These information needs are part of the wider trends affecting the food industry and the higher expectations of corporate responsibility. The implementation of these credence goods associated with certain characteristics related to quality or production processes, not verifiable through simple inspection or consumption [29,57], is another example of a top-down approach that required both consumer promotional programs and roaster acceptance to mobilize supply networks to ensure the supply of VSS coffees.

2.1. A Question of Impact

During the low price years, the valued-added markets based on VSS coffees seemed to be a promising tool for smallholders in developing regions, particularly for Organic and Fairtrade products [8,11,14,19,21,41,57,58,59,60,61]. These and other schemes were designed to offer an alternative to the conventional commodity market regime by challenging market competitiveness based solely on price [61] and by better valorizing local resources and internalizing social and environmental costs of production [61,62,63]. VSS also offered a medium to alleviate poverty by bringing higher prices for producers [8]. As credence labels, they are assumed to better connect producers and consumers, providing information about the place and the people involved in production, and the growing methods employed [14,41,62,64,65].

Certain evaluations have shown that VSS can provide benefits to growing communities. However, the case for a long-term positive impact expected by the implementation of different VSS for coffee growers with appropriate counterfactuals is still relatively weak and case-specific [7,9,29,48,66,67,68,69,70,71,72] and varies depending on the certification scheme or the institutional conditions or regions where they are implemented [29,73,74]. On the positive aspects for economic sustainability, increased productivity is often portrayed as a significant benefit in many recent studies. Impact assessments often fail to acknowledge national or regional agricultural policies that positively affect yields in a larger degree than VSS protocols. In addition, for a crop that has a high component of variable costs, yields per hectare are not the only factor to consider for a complete business case analysis of the required changes to achieve economic sustainability. In addition, increases in farm productivity also provide benefits to buyers, as that means a higher level of available supply and lower prices to them.

Impact by VSS can even be highly questioned. Some research has shown that certified producers do not necessarily significantly change their conditions after VSS implementation. Studies made in Nicaragua, for example, suggest that VSS farmers are more often found below the absolute poverty line than conventional producers. [11,66]. Other works question the sustainability standard approach, its ability to scale up and deliver benefits to both small and larger farmers and its impact in local institutions [75,76]. One could argue that some producers or some regions may be in a position to adapt to a particular VSS given their specific conditions, while, in some cases, other protocols, such as adding shade in an excessively wet area, will probably put them out of business.

A more comprehensive FAO study on the impact of VSS on smallholders and on market participation in developing countries also shows mixed results [9]. The study highlights a number of trends that are also valid for the coffee sector [9] (pp. 55–56): (i) self-selection: growers and exporters who have the means to make the initial investments are the first to join; the ability of exporters and growers to meet requirements set by voluntary standards largely depends on greater financial, environmental, physical and human capabilities at the farm level, which leads to exclusions of poorer growers; (ii) there is evidence that buyer preferences, pre-existing buyer–supplier relations and organizational structures of producers are selection mechanisms for the adoption of standards by small-scale growers; (iii) institutional contexts in which smallholders operate do matter; recent research pays attention to institutional contexts to comprehend how standards interact with pre-existing norms of production and trade. National institutions are needed to support growers’ compliance with standards, but the support for increasing growers’ participation in markets is still insufficient; (iv) compliance with standards and certification does increase costs but also farm-gate prices. The impact of standards is also contested because there are no common measurement methodologies and there is not statistically valid data for long-term impact assessments, a topic that has begun to be addressed lately [29,74,76]; while some studies find positive socio-economic effects for producers (e.g., [19,48,67,77,78,79]), others show that they do not necessarily achieve positive outcomes or show mixed results [9,29,30,80].

As pointed out by FAO, how coffee growers effectively participate in these value added-markets, capturing extra income in the long run for themselves, and how they share knowledge and expertise on sustainable and/or quality production, depends, to a greater extent, on formal institutions (e.g., national regulatory frameworks, national plans, assertive policies, functioning growers’ collective organizations, state support for extension services, access to credits and infrastructure) and informal institutions (e.g., forms of collaboration, cultural conventions such as degree of inclusiveness or exclusiveness, ability to adapt practices, ways of thinking and acting) [38,40,81,82].

In terms of VSS adoption, major producing countries and those relatively more developed provide better conditions for growers to attain VSS, whereas other countries in Africa or Asia face significant difficulties. Therefore, the supply of VSS coffees has concentrated in a few countries, with Brazil, Colombia and Vietnam accounting for 77% of the total [28].

2.2. Growing Pains: VSS Challenges

Contrary to the period when standards began to take hold during the coffee crisis years, current price premiums for given standards may vary or be non-existent, adding to grower uncertainties. No one can truly promise farmers that adopting these standards will mean a guaranteed market and significant premiums for the beans in the long term (a coffee tree can produce for 15 years or more). In addition, relative efforts across the chain may vary: the full extension of the farms has to be certified, leading to higher capital expenses for growers, although, in certain cases, buyers (e.g., roasters or brand owners) only have to buy a portion of certified coffees to be able to show consumers that the coffee sold under their brands complies with the respective VSS.

While in many cases the adoption of sustainability protocols has been positive for coffee growing communities, the first cohort of growers that reached them demonstrated that the ability of farmers to comply with such standards is limited without significant institutional support and capital investment [74]. Thus, a large number of coffee growers may not be in a position to obtain higher and significant premiums in the long term based on following sustainability protocols in countries lacking institutional support.

The mainstreamization of VSS has brought pressures for simplification or the implementation of less stringent standards to ensure adequate VSS supply for bigger brands, bringing its own challenges. Countries that have better institutional conditions, such as Colombia, face other types of challenges. Data from the Colombian Coffee Growers Federation show that by 2015 nearly 200 thousand coffee farmers operating in an aggregated area of 378 thousand hectares are working under one or more coffee VSS [83]. A similar effort is taking place in other large coffee producing countries, notably in Brazil and Vietnam [28]. This has resulted in an excess supply of “sustainable coffee” from a limited number of origins, making it more difficult for the model to expand. In fact, matching supply and demand of VSS coffee is perhaps the trickiest aspect of the current sustainability model. Demand does not necessarily surface when harvests are being collected, and when it does, it is satisfied by a portion of the certified farms. The world supply of sustainable coffee is estimated to be up to four times the demand [28], and, in Colombia alone, the supply of certain verification initiatives accounted for five times its demand in 2015. This means that the average premium for sustainable coffees has been reduced, or that there might not be premiums and willing VSS coffee buyers when a portion of the harvest comes to market, eliminating the financial incentives for growers to perform the required sustainability practices. In that sense, the scenario of “mainstream pushing out niche” for the VSS segment is clearly a source of discomfort from both the demand and supply standpoint [79], which can lead to an eventual watering down of the meaning of VSS for most consumers.

In addition, voluntary standards focus on the standard rather than on the origin of the coffee, favoring demand loyalty to the standard itself rather than to the coffee grower or his/her region of production. As the coffee origin and its exposure as an attribute of differentiation becomes less important than the sustainability standard in consumer communication, the farmers and their regions’ ability to differentiate and capture value through the symbolic quality and the origin information that enhances consumer’s willingness to pay is curtailed. Thus, the standards become a factor that contributes to the delocalization of production, and growers end up competing with other standard compliant coffees with lower premiums from regions or countries with different production costs and qualities. It is therefore not surprising that impact assessments of voluntary standards made so far show that the value added, when generated, mostly stays with other actors of the supply chain, including certifying agencies, while farmers obtain a limited participation in the resulting increased revenues [9,28,29,74].

Although it could be argued that the mainstreamization of VSS is one of the stages of the sustainable market transformation theory [84]. According to this concept, reaching a critical mass is the third stage that follows the inception and early mover phases, before regulations and institutions can lead to a truly sustainable industries. However, reaching the third (critical mass) phase requires a balanced representation of actors along the chain, implying shared priorities across a number of stakeholders, including governments, which is not part of what we have described as the mainstreamization of VSS. Furthermore, under current conditions, the incentives for a continuing expansion of demand and supply of VSS coffees are being reduced while the VSS model limits the upgrade opportunities for farmers by delocalizing production. It would appear that the current sustainability model is seen as a top-down (Northern) approach that does not necessarily provide the necessary stakeholder engagement consensus and the conditions to achieve and maintain this critical mass in a consistent manner.

2.3. The North and South Perspective

Voluntary sustainability protocols can also be viewed as well intentioned “private institutions” predominately designed in the North, which may limit the local scope of decision-making, impose high transaction costs on growers and squeeze out smallholders not being able to comply with the required standards [14,30].

These private institutions insert themselves in buyer-driven global value chains, and imply the use of transnational private governance arrangements and the implementation of standards for sustainable and quality production. Nevertheless, the validity of many of these initiatives is increasingly questioned since they are perceived as serving the interests and priorities set in consumer environments. Agricultural policy makers seem to agree that growers are not adequately consulted or are underrepresented in the process of defining priorities, which leads to an unbalanced standard definition process and low applicability to local realities [85,86,87]. In contrast with retail and processors, as well as NGOs and certifying agencies that have dedicated staff to sustainability areas, growers and their organizations are unable to attend or prepare for technical and sophisticated forums where standards are defined. As a result, decision makers often give excess weight to downstream industry, consumer or public opinion perceptions on farmer realities. When producers are consulted, they tend to have the chance to voice their opinion not on what priorities the standards should tackle but on the implementation of priorities already defined.

Studies show that: (i) the participation by Northern stakeholders is not balanced both quantitatively and qualitatively even if they encompass multi-stakeholder initiatives [88,89], and what dominates is the Northern discourse on sustainability and the formal scientific knowledge over local knowledge and growers’ preferences in the South [85,87,90]. This top-down criticism is reinforced by the static market driven governance conditions in most commodity supply chains that limit the ability of upstream actors to effectively interact with lead firms and value chain decision makers.

As a consequence of this imbalance and inconformity, groups of stakeholders who are excluded from the development of standards or perceive themselves in a disadvantaged situation regarding the outcomes of the standards are attempting to create (rival) VSS to affirm their own visions [91,92]. Some of these initiatives include the Trustea standard developed by the Indian tea industry, Flor Verde in the cut flower industry in Colombia [93], IScoffee from Indonesia, the Brazil’s Certifica Minas Café Standard [94] and Colombia’s recently launched initiative to develop its own sustainability standards [95].

Southern standard developments may be considered as counter-initiatives to existing global standards. However, it is still unclear how successful this bottom-up approach will be since: (i) they have only just emerged and the socio-economic impacts are not known yet; (ii) the implementation and enforcement of new regulations can be problematic in areas with weak institutional structures; (iii) they may get some relevance in national markets but lack the resources to be known internationally [85]. According to Hospes [91] (p. 11), there is a challenge to develop “new perspectives on state, scale and sovereignty over sustainability in a globalized, network society”.

More specifically, there is a need to establish the rules of the game in which producers in the South are not only standard-takers but also included in design of the rules [85,91]. The ability to reframe these initiatives with a sustainability value promise linked to single origin coffees or GIs is a possibility to be considered, but would in any case require the participation of both the growing and consuming industry. This would imply a bottom-up/top-down approach to satisfy the interests and needs of upstream and downstream industry players.

In summary, there is no straightforward evidence that VSS can significantly contribute to changing the coffee industry governance, and solving the large-scale challenges and the current inequality in the global coffee market explained by the coffee paradox. The impact assessment of the existent different initiatives varies significantly across regions and products. The success of a sustainability intervention depends on the particular context where it is applied [29,74,76] and its ability to significantly contribute to improving conditions at the scale required in growing regions is limited. In addition, the current top-down model faces complex challenges. From the demand side, the “sustainability of the sustainability model” in fact depends on the availability to continuously provide additional demand for VSS compliant coffees at higher prices.

From a supply side, the lack of incentives and the additional and significant funds that will be continuously required to support VSS adoption by small-scale growers, which are further below the standards than the first adopters [9,74], also question the current model’s ability to expand. In addition, apart from the possible lack of relevance of a given VSS for a producer or growing region, the current VSS model does not provide conditions for coffee growers’ economic upgrade and “differentiation from below” efforts associated with origin promotion. Finally, VSS might further shift power relations along the international value chain in favor of international stakeholders, exporters and better educated, bigger producers in developing countries to the detriment of smaller farmers, without significantly altering the market driven value chain governance.

3. Sustainability Reporting

There is an evolving consensus on the importance of environmental, social and economic sustainability for long-term brand and company performance [96,97,98,99,100,101,102]. Market research [2,103,104]—among others—shows that younger consumers around the world have become less influenced by traditional advertising and more thoughtful of their purchasing decisions. The evolving “reasons why” to buy a product or a service include, in many instances, the impact that such products have in the communities where they are produced, their environmental footprint and the labor practices used. These factors can be considered a new set of brand attributes or, depending on the industry and the product, a set of minimum expectations. In fact, more than half (55%) of global respondents of Nielsen’s corporate social responsibility survey say they are willing to pay extra for products and services from companies that are committed to positive social and environmental impact [104]. However, some consumers do not think that providing information is enough. Successful brands deliver higher return of investment if they are considered “meaningful” or “loved” by consumers, a condition that can only be obtained if they are trusted, and only if this condition is fulfilled can the information they convey become a positive and differentiating attribute [105,106].

In addition, corporations have the challenge of attracting and retaining talent. Millennials now account for over half of the workforce in many countries, and their set of values and expectations widely differs from previous generations. They are entrepreneurial, favor the underdog, and their job fulfillment also depends on their employer’s ability to inspire and provide social value [96,97,103,107].

Investors, on their part, are requiring more disclosure and becoming more demanding to companies and organizations [98]. In an era of high scrutiny and transparency, companies and brand values can be significantly affected by reputational risks. It takes time and can be very costly to recuperate consumer and regulator trust [108]. It is therefore not surprising that both retailers and large corporations have significantly evolved in evaluating the impact of their operations from an economic, social and environmental standpoint. Clearly, sustainability policies are now a tool to identify potential risks and competitive opportunities to deliver higher returns [99,100].

Companies dealing with raw material sourced overseas also have to contend with long and difficult-to-control supply chains. Industries such as coffee, minerals, diamonds, palm oil or sugar are continuously scrutinized for their social and environmental impact. The ability to know the supply chain actors and identify the specific origin of their products is not only an expectation by clients, retailers and consumers but also a possibility to differentiate and provide brand emotional value [109].

Clearly, large companies are becoming conscious that their organizations and brands have to take sustainability seriously and deliver a more complex set of benefits to clients and consumers. Sustainability and clarity of purpose are now a key to success for established companies [101,110] that need to compete for market share with newcomers that can sound more authentic and can more easily communicate their contribution to society [111]. In the coffee category, it is clear that these trends are reflected in consumer-oriented companies and brands. On the other hand, sustainability reports are less frequent in upstream and business-to-business environments with low visibility. Global sustainability reports published by coffee importers and exporters are difficult to find, even among major operators. Grower organizations exceptionally publish their own sustainability policies and indicators. In terms of reporting, there is clearly a lot to learn from “northern” actors to provide consistent updates on long-term sustainability initiatives and priorities.

3.1. A Question of Materiality

Sustainability reporting has been the result of the increasing pressure from stakeholders and the evolving material aspects that affect performance and surpass the financial topics traditionally presented in financial reporting. Reporting has also evolved. As more practitioners and interested parties became engaged in reviewing the sustainability policies, priorities and actions performed by companies, reporting frameworks and methodologies were required to provide transparency and credibility. Sustainability reports, in particular those developed under accepted sustainability reporting standards, require stakeholder consultation and a sustainability materiality assessment to identify the topics of priority for a company to be viable from an economic, social and environmental perspective [89]. Materiality is a term originally used by accounting regulators to establish standards for financial statement auditing. It has been defined in different ways by the US Supreme Court, the Financial Accounting Standards Board (FASB), the International Accounting Standards Board (IASB), the Securities and Exchange Commission (SEC), the World Business Council for Sustainable Development (WSBCSD), the Global Reporting Initiative (GRI), among many others. However, in practice, most coincide on the fact that the identification of material topics is a key factor to assess the current and future performance of an entity [112]. A material assessment on sustainability therefore identifies the sustainability topics that are considered a priority for the brand or company in question and its stakeholders [113,114].

There are different methods to identify and prioritize key sustainability topics. The Sustainable Accounting Standards Board (SASB) [115] and GRI have come up with tools that help companies identify material topics of interest for certain industries. This exercise must be complemented with an action plan to confront them, with their respective medium- and long-term objectives. Therefore, it is expected that companies belonging to the same industry will have similar sustainability materiality assessments, allowing the best possible comparison of views and initiatives among industry members. However, the set of priority issues and the degree of commitment to confront them can substantially vary between competitors in the same industry. This may reflect the degree of commitment to sustainability or an approach to sustainability that is merely considered as a way to respond to and/or appease their stakeholders. The resulting Key Performance Indicators (KPIs) on complex sustainability questions can also widely vary, both in their definition and in their objectives.

Over 5000 sustainability reports using GRI guidelines and standards were filed for calendar year 2015 [114], suggesting an increased commitment to follow these methodologies. Many of these companies are brand owners and retailers processing and distributing coffee as well as a number of agricultural products, whose stakeholders (in particular clients and shareholders) increasingly expect a clear commitment to continuous improvement in sustainable operations and practices. Others may file reports with the primary objective to reduce reputational risks and satisfy more demanding consumers. However, in an increasingly large number of cases, commitments regarding environmental, social and governance factors also play a role in accessing or maintaining a client base, in order to apply for public procurement contracts, to comply with regulations or to be in a position to adhere to fund management policies to invest in such companies.

One of the key features of the materiality assessment framework now used by thousands of companies and organizations around the world is deeper stakeholder consultations. The degree and depth of consultation still leans in favor of downstream players (clients or consumers) rather than upstream providers. In the case of the coffee value chain, the lack of institutions or relations with grower organizations imply that consultations are often limited to the next step up the chain for coffee brand owners, e.g., green coffee importers and occasionally exporters. Furthermore, the GRI methodology is not exempt from criticism because of its inclusive multi stakeholder process, which, according to some opponents, may lead to a sort of “paralysis by analysis” and less rapid advancements on a progressive agenda [116]. Thus, while the principle of consulting and identifying priorities with all stakeholders, including vendors, is of significant importance to global value chains, it may not be thoroughly exercised or may be limited to a few actors whose main operation is not in countries of origin.

3.2. Coffee Brand Reporting

The coffee industry is a notable example of a varying degree of depth of analysis in its different sustainability reports [117,118,119,120,121,122,123,124,125]. Most coffee brands acknowledge that a viable future for coffee growing is a key material area for the sustainability of their business. However, the degree of elaboration in the different action plans significantly varies. While some brands like Keurig [123] or Nestle [124] show more comprehensive approaches to the challenge of coffee growing sustainability, there are also cases where brand owners support a wide variety of low impact initiatives to support farmers that lack adequate impact assessments or focus.

In most instances, the sourcing sustainability policies result in the adoption of different VSS for the green coffee procured as raw material by different brands. Companies turn to their vendors and input providers to require them to adopt those standards for a portion of their total needs [1] exercising their market power [79] under a traditional top-down approach. It is therefore not surprising that, for many agricultural products, a significant number of these companies make public commitments to buy a portion of their raw materials with products complying with a particular VSS [1,28,126].

In a concentrated market like coffee, where seven companies account for nearly 50% of the world’s coffee grocery retail sales based on Euromonitor data and trade sources [1], these top-down policies have significant implications for over 25 million coffee producers around the world [9]. Producers learn the news from exporters and are then required to invest and change their practices in order to adopt the standards believed to be sustainable. In the meantime, exporters and importers adapt their processes and services to develop ways to ensure an adequate supply of VSS coffees. Unfortunately, this scenario, which could be described as “outsourcing sustainability to growers” does not give proper weight to grower’s interests and their own material topics.

3.3. A Top-Down/Bottom-Up Approach

Clearly, sustainability reporting has room for improvement to better reflect the interests and priorities of the farming community. From a coffee grower’s perspective, sustainability could be the most appropriate way (or manner) in which economic, social, governance and environmental conditions of supply chain actors (from coffee harvesters, growers, traders, coffee roasters and retailers) produce less gaps/disparities. Under this view, an emphasis on legitimate farmer governance, a topic seldom mentioned in brand sustainability reports, needs to be highlighted if farmer sustainability priorities are to be identified and validated. Furthermore, existing standards can play a positive role in many aspects but are more questionable when it comes to (sustained) economic-profitability of a long-term venture called coffee growing.

There are already efforts to bring the southern perspectives into sustainability frameworks that lead to KPIs and reporting by industry groups and VSS. The Sustainable Coffee Challenge [127] actively promotes knowledge and project sharing, while UTZ has adopted a more inclusive policy of farmer consultation at origin before its standards are formally implemented. The International Social and Environmental Accreditation and Labelling Alliance (ISEAL) [128,129] has brought different VSS and international stakeholders to reduce and simplify certification indicators. The Cocoa Action plan [130] has also acknowledged that coordination is needed to achieve more impact on consensus indicators in which origin governments participate. Likewise, the recently launched Global Coffee Platform [131] has producer representatives in their board of directors and calls for national and international platforms. However, these initiatives are still novel and lack a real bottom-up approach where growers from different countries and regions can provide their feedback on priorities and sustainability indicators.

Some companies are also conceiving positive developments to better incorporate coffee growers’ views. McCafé, under its Sustainability Improvement Platform (SIP) program, included a producer collaboration component designed to identify and validate farmer needs [120]. Farmer Brothers, a roaster based in California that is also a McCafe supplier, has developed its Direct Trade Verified Sustainable (DTVS) program, which includes adopting sustainability priorities and KPIs in collaboration with Committee on Sustainability Assessment (COSA) that are verified as relevant for coffee growers in the regions from where they source [121]. The resulting KPIs and progress reports would no doubt have more relevance and credibility for growers and consumers and for the industry as a whole.

In summary, successful coffee companies are publishing sustainability reports. The discipline of reporting and making sustainability materiality assessments is a significant step to getting the industry to use useful methodologies to determine the priority topics that the coffee industry needs to concentrate on for its long-term viability. These top-down experiences can be put to use for bottom-up efforts in an effort to engage coffee growing organizations to arrive at more meaningful sustainability initiatives that provide more benefits to farmers.

There are already efforts that lead to more quality reporting and consideration of coffee growers’ views that do not necessarily incorporate VSS. These more comprehensive efforts can increase consumer trust and relevance in coffee growing regions. A commonly agreed set of material aspects to achieve sustainability would provide legitimacy to the efforts of brands and origins, bring coherence to sustainability reporting and develop additional differentiation opportunities based on sustainability actions. This means that the equity of the brand, the retailer and the origin can work in tandem, as they share priorities and objectives.

Providing consumers and stakeholders with a consistent industry narrative and helping companies to report on their contribution to more impactful and significant sustainability KPIs would probably be the next stage of coffee sustainability reporting. Focusing on material priorities relevant to different origins is another key aspect of what we have termed a top-down/bottom-up sustainability vision. This approach will build on direct trade and relationship coffee trends that focus on individual farmer or community stories as a way to bring more authenticity and excitement to the coffee category.

4. Toward a New and Complementary Sustainability Model

The past few years have taught us that sustainability is an elusive target. The mainstreamization of VSS, while positive in many respects as it reaches a larger portion of the growing and consuming population, may not be in a position to continue to expand due to decreasing grower incentives and the substantial funds required for a new cohort of farms to comply with VSS requirements. Furthermore, and despite VSS coffees accounting for almost 40% of the world supply, the economic viability of coffee growing is still in question in many producing areas. In fact, a recent report [42] reminds the industry that coffee production is not profitable in several countries and the ability to expand production in a number of them may be put into question, whether they comply with VSS or not. This would imply that the economic upgrade opportunities for coffee farmers once foreseen when adopting VSS models tend to dissipate with time.

However, there have been positive developments that can bring new possibilities for the sustainability of the coffee industry. The expectation that industry members will be under constant “millennial” pressure would help to progressively increase the quality and consistency of brand sustainability reports. In addition, the launch of the UN’s Sustainable Development Goals (SDGs) may soon lead to concerted actions that could eventually call for industry realignment on sustainability priorities. It is expected that grower organizations, exporters and importers will also need to adopt consistent and coherent sustainability reporting standards rather than limit themselves to publish isolated corporate social responsibility initiatives. There are already individual companies and industry groups realizing the need to enlarge the “sustainability stakeholder consultation process” and involve coffee growing communities in defining priorities. In addition, there is a renovated interest for single origin coffees in the trendsetter segments of the market, which is filtering down to mainstream segments and giving opportunities for GIs to promote themselves as a high quality and sustainable coffee option. Clearly, we are at a critical junction to review the current coffee sustainability model and evaluate possibilities for improvement.

In this context, we believe that the conditions to develop an approach to sustainability that effectively involves farmers and their organizations in devising sustainability priorities have arrived. As the future of the coffee supply is in question due to lack of interest for growing coffee by younger potential coffee growers, upstream and downstream actors need to come to terms with sustainability objectives and metrics that are relevant to the specific conditions of origin regions and attend to consumers’ more demanding and credible information needs. Our proposed top-down/bottom-up approach should also provide a sustainability platform for single origin coffees and GIs, providing the credibility that consumers now expect from sustainability initiatives, and scalable differentiation from below and economic upgrade opportunities for farmers. In this section, we provide details of our model and how it can complement itself with the existing VSS frameworks.

4.1. The Need for a New Model

The few long-term VSS impact assessments available have shown that, under certain conditions and contexts, VSS produce positive impacts in coffee growing communities. However, their overall impact tends to be over-estimated while there is an increasing set of future challenges for coffee farming. As noted before, coffee growers now have to contend with higher risks associated with climate variability and climate change, which frequently mean more pest and disease incidences, significant price and income instability in the post ICA world, an ageing rural population, an ever concentrated demand that leads to a perennial income imbalance, the need to provide truthful information on supply chains, market access limitations for smaller growers—in some cases, due to VSS—demand and supply uncertainties, lower profitability and higher costs of production. These and other challenges are dynamic, and may affect different coffee growing communities in different ways at different times.

The coffee leaf rust pandemic that took place in Colombia, and in other Central and South American countries starting in 2009, showed how dynamic and far-encompassing these challenges can become. As hundreds of thousands of coffee farms became affected by the coffee rust fungus, many VSS certified producers found that they were very vulnerable to pests and diseases—more so than any sustainability standards could have anticipated. In fact, certain conditions recommended by standard setters made the situation worse [132,133,134]. The recent Brazilian drought and the increased prevalence of coffee berry borer in Colombia during dry periods have also shown cases in which producers with drastically reduced yields face difficult economic conditions while, at the same time, they are deemed sustainable according to certain standards [135]. Clearly, VSS do not necessarily adapt rapidly to an era of rapidly changing farming conditions.

The limitations of VSS may also be associated with the emphasis on far encompassing standards. Standards are defined as a “document, established by consensus and approved by a recognized body, that provides, for common and repeated use, rules, guidelines or characteristics for activities or their results, aimed at the achievement of the optimum degree of order in a given context” according to the definition of the International Organisation for Standarisation ISO/IEC Guide. When applied to coffee production and sustainability, a standard may become a tool that simplifies complex and evolving challenges for millions of coffee producers. There is no single difficulty, economic, environmental or social in nature that is not evolving. Different realities, no matter how much we try to simplify them in order to understand them, are very complex. The framework of defining standards and checklists to declare oneself “sustainable” when complying with an audit simplifies a clearly more intricate and complex reality.

The problems to simplify complexity involved in the standard setting processes are compounded with the lack of proper channels and institutions to gain knowledge and co-create with coffee farmers. The SDG framework provides an opportunity to develop an origin and/or region specific framework for sustainability. Relevant priorities and baselines can be defined with coffee growing communities so that sustainability KPIs and goals are defined taking into account local coffee grower specific challenges and realities. This implies an adoption of a continued improvement process for growers and regions on their path to sustainability, and dynamic sustainability reports that would show a commitment to sustainability rather than a declaration of being sustainable according to a given standard.

Furthermore, this sustainability concept and its KPIs will need to become region specific, acquiring more relevancy for local authorities and legitimacy among coffee farmer communities. The approach also favors public private partnerships on focused initiatives and programs with coffee industry actors. These characteristics are consistent with the critical mass phase of the sustainable market transformation theory. As pointed out in the previous section, current efforts under the Global Coffee Platform [131] and the sustainable Coffee Challenge [127] appear to work in this direction, although they still lack the region specific farmer community consultations implied in a bottom-up concept. The Direct Trade Verified Sustainable (DTVS) program developed by Farmer Brother and Cosa [121], while still not focused on single origins, as its main customers use blends, is a worthwhile initiative that explicitly incorporates grower consultation and validation of its sustainability initiatives.

One major obstacle to develop region specific sustainability KPIs is the ability and practicality to obtain farmer input. Most coffee growing regions still lack effective communication tools or strong farmer organizations to channel this consultation process. On the other hand, regions that have developed GIs usually have constituted more effective governance systems, which is a specific condition that they must comply with for being recognized as a GI in most legislations.

4.2. The Challenge of Effective Consultation

A number of initiatives that help identify coffee producer communities and regional priorities have been implemented under different frameworks. During the process that led to the application of Colombia’s Coffee Cultural Landscape (CCCL, the CCCL covers areas of 51 coffee growing municipalities in central Colombia) for inclusion into the UNESCO World Heritage List and the definition of its management plan [136,137], dozens of stakeholder engagement meetings took place. The initial management plan had KPIs that were regularly updated, for each of the exceptional values that were considered by UNESCO. Progress was reviewed in local and regional follow-up meetings and communication material was distributed to the region’s inhabitants [138]. As a result of these efforts, local and national authorities enacted policies to support these initiatives [139], give advice on implementing regulations and provide different materials to city councils that would support the conservation of the region [137]. Taking into account different experiences, a regional brand was launched to identify products originating from the region as well as tourism facilities that complied with certain standards [140,141,142]. More recently, after several years of implementing the original management plan for the landscape and evaluating its KPIs, a number of meetings and workshops took place with local stakeholders and a new and more comprehensive management plan is under consideration [143]. Both the previous and the new management plan focus on economic, environmental, social and cultural activities and can be described as a comprehensive sustainability policy [144].

Collective wisdom exercises based on appreciative enquiry methodologies have also been widely used for corporate strategic planning and community development workshops [145,146]. The Colombian Coffee Growers Federation has put to use these methodologies in a number of occasions to arrive at priorities and focus on strategies that would deliver a better return for coffee production [147]. This more comprehensive approach, which takes into account grower’s interests and priorities, aims for a more balanced set of objectives and responsibilities of actors in the industry and can result in KPIs and targets that are adapted at regional and local realities.

The Farmer Brother–Cosa approach is somewhat different. It incorporates a bottom-up approach, as it uses farmer surveys and follow-up instruments to validate the hypothesis on sustainability priorities detected on (top-down) previous work. As the world moves to sustainable platforms that can be adapted to national and local conditions, this framework can be useful for those regions with weak governance and institutions. Although there is no single and unique approach for farmer and community consultation, there are clearly a number of methodologies to obtain farmer feedback. Clearly, anecdotal evidence and indirect consultation though exporters and importers is not enough.

The legitimacy benefits of a top-down/bottom-up approach to sustainability go beyond legitimacy, relevance and origin specific equity. The co-creation of an industry materiality assessment can complement the traditional scientific knowledge, which often omits taking into account user knowledge and the ability for considering different conditions and contexts [148]. Thus, transferring the core meaning of transdisciplinarity [149] to the understanding of the challenges faced by coffee production and consumption implies the acknowledgement of the role of diverse actors (from growers to consumers) and their knowledge to jointly promote dialogue, understanding and definition of sustainability parameters and assessments.

4.3. Region Specific Sustainability KPIs and Global Priorities

The suggested coffee industry sustainability assessment can lead to a set of global material issues that also reflect local contexts and priorities both in the coffee growing and consuming environments, leading to common efforts, alliances and smarter resource allocation. Coffee industry members might adapt their CSR policies to actions that can impact a set of commonly agreed Coffee Industry Sustainability Performance Indicators.

These indicators, apart from complying with Specific, Measurable, Available, Relevant, Time-bound (SMART) criteria, can take into account global compact and Sustainable Development Goal (SDG) indicators and priorities, facilitating cooperation with multilateral and government agencies. They will also build on previous work done by VSS, the impact assessment work done by COSA and FAO’s Sustainability Assessment for Food and Agriculture (SAFA) indicators and tools [150]. More importantly, as the regional sustainability KPIs are shared with local growers and their organizations, they can be adopted by local governments, adapted to local coffee growing realities and communicated under the SDG platform. By focusing on key priorities and measuring their impact rather than investing resources in hundreds of initiatives that may or not be relevant to coffee growing local contexts, additional funds from non-industry stakeholders can be leveraged and scale can be achieved.

This implies the need to acknowledge that, in a complex world, not all indicators are necessarily positive and some may deteriorate under certain conditions. The challenge of sustainability is therefore not a pass/fail test, but the consistency of continuing work in prioritized sustainability material issues despite the fact that one does not control all possible variables that affect the business. The overall aim is that consumers and industry stakeholders must learn to value these long-term strategies and the commitment and efforts made by origin regions and brands.

Another advantage for region-specific KPIs has to do with impact assessment. Defining baselines, KPIs and sustainability evaluation criteria in specific regions are less complex than applying generic KPIs to several coffee growing sources with different conditions at once. The impact measurement results are therefore more transparent, less generic and more credible to consumers and region stakeholders.

4.4. Benefits for Origins

One additional and possibly substantial benefit in the long run for the proposed sustainability vision is that it can promote and complement the equity of the origin, providing differentiation from below and economic upgrade opportunities for farmers and regions that develop a meaningful sustainability track record. This would complement single origin coffee reputations and respond to consumer and marketing trends that define origin as a significant piece of information that consumers now demand. Growers have the additional incentive to develop GIs with sustainability indicators that connect with SDGs and provide both marketing content and relevant data for those industry sustainability reports that sell coffees from those origins. Under this vision, an Origin Sustainability Manifesto could be the base for long-term win-win partnerships and commitments for joint sustainability and marketing programs.

The proposed model requires that coffee growers themselves reflect (within their regions or national organizations) on their own material sustainability questions and develop their own sustainability reporting. This will necessarily require widespread consultation and transaction efforts at the local level through workshops and appreciative enquire exercises with producers themselves as well as a periodical revision of opportunities. The voice of a large majority of small farmers will have a platform bringing some equilibrium to the interests of large growers and exporters that are now benefiting more from the current sustainability standards regime.

GIs are uniquely well positioned for this consultation exercise thanks to their stronger governance and institutions. The equity of a given origin would not only be based on its availability, consistency and quality but on its commitment to sustainability, providing the conditions to launch sustainability manifestos for individual GIs, which can become useful tools for origin sustainability reports and for differentiating from below efforts. A region-specific and continuous-improvement approach to sustainability KPIs will also have the benefit of not forcing coffee growers into sustainability pass/fail corners that do not reflect different and evolving sustainability challenges.

For regions that have a quality reputation, the new framework will have expanded differentiation from below opportunities as the suggested process can also provide to them the necessary content to promote their own GIs with transparent sustainability KPIs. Thus, GIs can become a more robust and value added offering for single origin marketing, as it has attached credible information and valuable content that better meets the symbolic quality mentioned by Daviron and Ponte [6]. In other words, the system helps to develop the necessary loyalty to the origin and becomes a powerful incentive to promote a more complex and rewarding relationship with other actors in the value chain.

4.5. A Platform for Fruitful Dialogue

Another important benefit of this approach is that it might help industry players to understand and acknowledge the sustainability challenges that all members of the industry face, not only at the coffee producing level but also at the coffee manufacturing and consumption levels. Producers and other industry actors will look at sustainability in a more comprehensive way, acknowledging the difficulties, challenges and progress of other actors of the industry. This aims to enhance the way brands and other players communicate with consumers as an industry, building more credibility to the concrete actions that each member of the industry makes to improve on wider materiality questions.

Communicating to consumers and retailers with a consistent industry message can result in more visibility to the industry’s efforts, more focus on priorities that are relevant to coffee growers, more relevant impact assessments and progress indicators and more incentives to local communities to become actors in transforming their own realities. Once again, the coffee industry should be in a position to lead the way and show other industries how to achieve significant progress and provide the scale required for the needed industry transformations.

More importantly, the industry materiality assessment initiative does not undervalue or do away with the voluntary standards model. It can complement and enhance the current model where it is successful, aligning incentives to work and leveraging resources on similar programs and projects that have a direct impact on grower legitimate sustainability concerns.

In short, the proposed material assessment model and corresponding KPIs has at least the following benefits that enhance the current voluntary standard model:

- It is agreed upon and defined with the explicit participation of growers or a collective of growers, reflecting their own challenges and conditions, as well as their priorities in terms of social and natural capital and profitability concerns.

- It is inexorably linked to the origin where those growers live, therefore building upon and complementing the equity of the origin of their coffees. If a collective of growers or a given region demonstrates a firmer commitment to Sustainability KPIs that can be measured in a given geography or community/communities, the equity of such origin in consumer minds and industry buyers can correspondingly improve, as it will be more credible to consumers and stakeholders. In fact, this would lead to GIs in general adopting Sustainability KPIs to complement their own minimum quality policies.

- Assessing the impact and progress of sustainability indicators that are adapted to defined regions and origins is simpler and provides more ready feedback to reassess policies and evaluate benefits of sustainability investments.

- It reflects a complex reality where, at times, all KPIs may not be positive, without sacrificing the transparency and the commitment to improve upon them in the long term, gaining consumer’s trust.

- It has the benefit of scale, impacting a larger number of growers and not just those that can achieve the standards with less effort. Materiality questions aim to achieve widespread changes to a large number of farms and growers, not limiting itself to those that can more easily access a given certification standard or with the financing to be able to comply with them. This allows for forging alliances to invest resources in commonly agreed priorities rather than parceling available funds in limited initiatives.

- It does not work against the current voluntary standards model. On the contrary, it complements it, supplying a set of sustainability objectives for all coffee growers according to priorities defined by themselves, consulting consumer and industry expectations. At the same time, it does not do away with the existing certification and verification protocols, which aim for laudable objectives for those growers and industry members that see benefit in their use.

- It provides a platform to industry members to communicate to the farming communities their own sustainability challenges and efforts. At the coffee growing and supply chain levels, it allows them to use available resources more effectively with commonly agreed priorities. At industry and brand levels, it provides content and actions that allow communicating to clients and consumers with long-term strategies that include an effective and measurable impact.

- Clearly, there is a lot more work on developing a far encompassing sustainability model. However, as the coffee industry considers new paths for sustainability, we advocate for a framework of continuous improvement on clearly defined material topics that take into account the economic challenges of growers. The implied governance of the new model will require that farmer organizations from different regions of the world are able to participate in the co-definition of sustainability priorities that are relevant to their own realities and provide them with economic upgrade opportunities.

5. Conclusions