Aligning the Economic Value of Companion Diagnostics and Stratified Medicines

Abstract

:1. Introduction

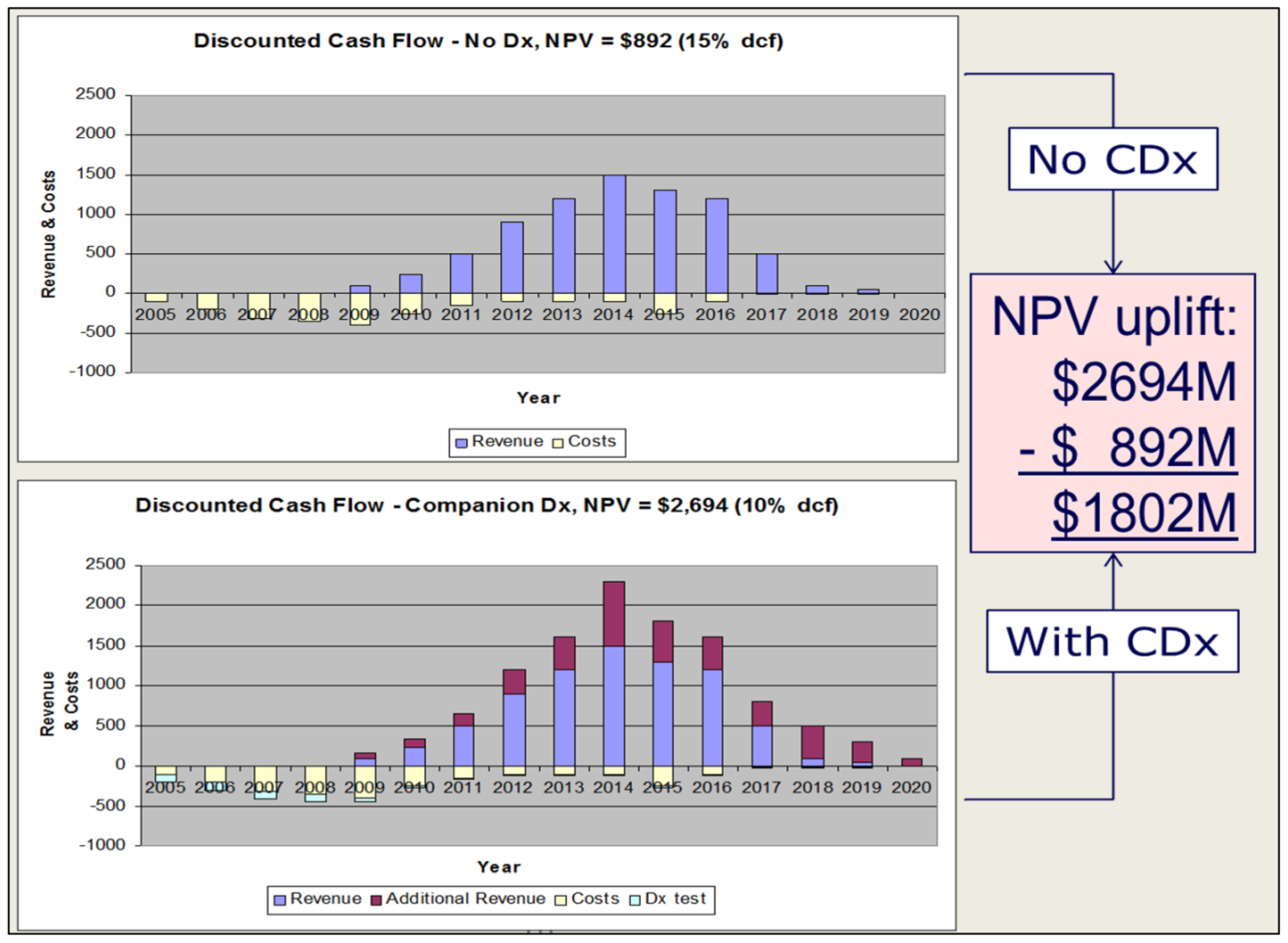

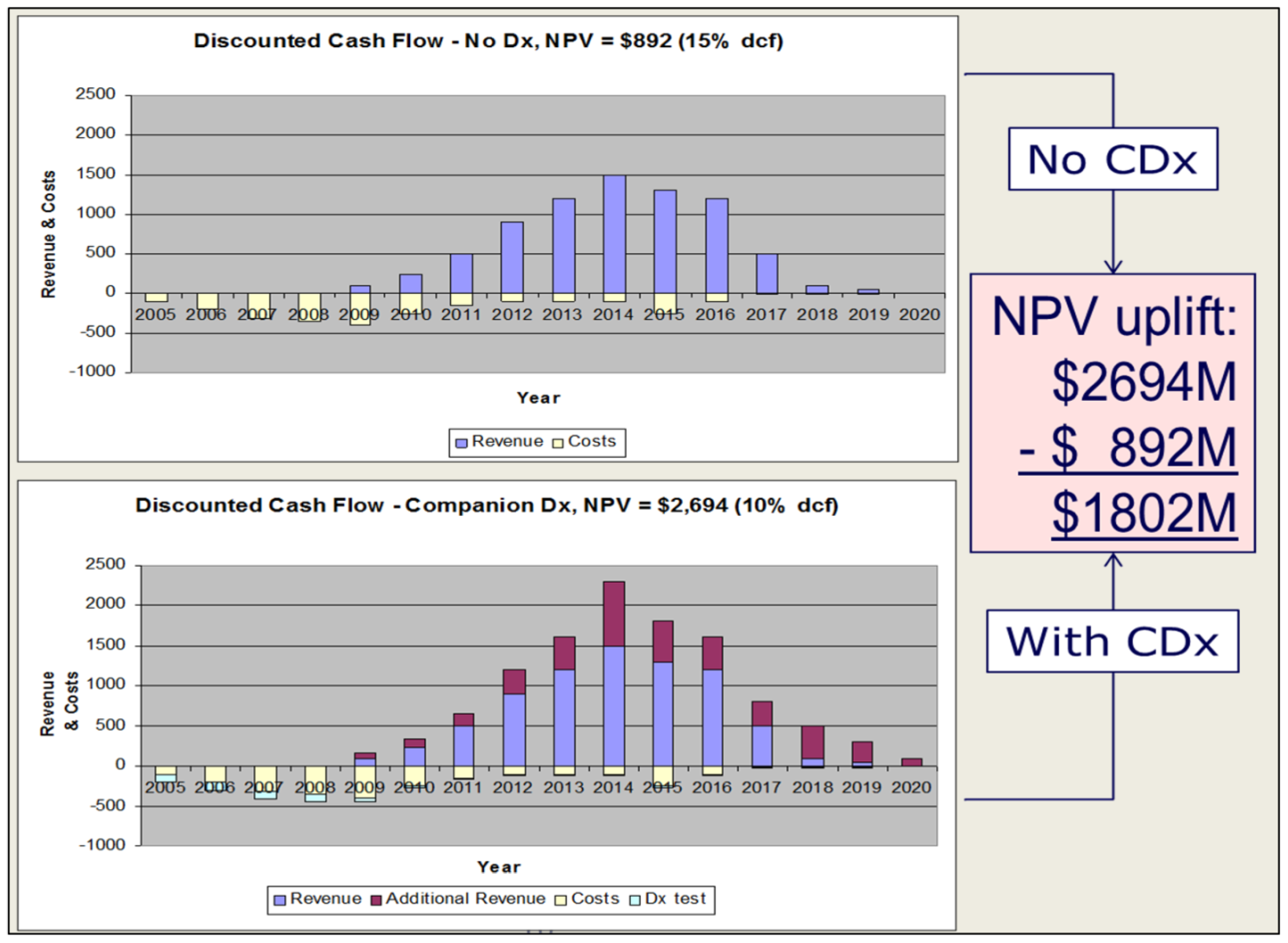

2. Relationship Economics and Relationship Structure

3. Impact on Regulation, Pricing and Reimbursement

{kind=link}

{kind=link}

| Targeted Therapy | Annual Price | Companion Diagnostic | Test Price | Model | Value |

|---|---|---|---|---|---|

| Xalkori (critozinib, Pfizer) | $115,200 | Vysis ALK Break Apart In Situ Hybridisation FISH Probe Kit (Abbott Molecular) | $1,500 | Rescue (ALK positivity ~7%) | TBD |

| Zelboraf (vemurafenib, Plexxikon / Diiachi-Sankyo/ Roche) | $56,400 | Cobas 4800 BRAF V600 Mutation Test (Roche Molecular) | $120-$150 | Co-development (BRAF V600E mutation ~40%) | $144M ($213M*) |

| Herceptin (trastuzumab, Genentech / Roche) | $70,000 | HercepTest (Dako) | $500 | Rescue (HER-2 expression score 3+ ~ 10%) | $620M* |

4. Beyond UK NICE, Health Technology Assessment in Germany

5. Conclusions

Acknowledgments

Conflict of Interest

References

- Walker, I.; Newell, H. Do molecularly targeted agents in oncology have reduced attrition rates? Nat. Rev. Drug Discov. 2009, 8, 15–16. [Google Scholar] [CrossRef]

- Trusheim, M.R.; Berndt, E.R.; Douglas, F.L. Stratified medicine: Strategic and economic implications of combining drugs and clinical biomarkers. Nat. Rev. Drug Discov. 2007, 6, 287–293. [Google Scholar]

- Blair, E.D. Predictive tests and personalised medicine. Drug Discov. World (Autumn) 2009, 22, 27–31. [Google Scholar]

- Gilham, I. Theranostics: An emerging tool in drug discovery and commercialisation. Drug Discov. World (Autumn) 2002, 6, 24–32. [Google Scholar]

- Trusheim, M.R.; Burgess, B.; Hu, S.X.; Long, T.; Averbuch, S.D.; Flynn, A.A.; Lieftucht, A.; Mazumder, A.; Milloy, J.; Shaw, P.M.; et al. Quantifying factors for the success of stratified medicine. Nat. Rev. Drug Discov. 2011, 10, 817–833. [Google Scholar] [CrossRef]

- Agarwal, A. Overlooked Opportunities. Available online: http://www.pharmexec.com/pharmexec/article/articleDetail.jsp?id=574630&pageID=1&sk=&date (accessed on 20 August 2012).

- Blair, E.D. Assessing the value-adding impact of diagnostic-type tests on drug development and marketing. Mol. Diagn. Ther. 2008, 12, 331–337. [Google Scholar] [CrossRef]

- Hughes, B. The comparative effectiveness challenge. Nat. Rev. Drug Discov. 2009, 8, 261–263. [Google Scholar] [CrossRef]

- Hughes, B. Novel risk-sharing scheme puts the spotlight on biomarkers. Nat. Rev. Drug Discov. 2007, 6, 945. [Google Scholar]

- Blair, E.D.; Blakemore, J.A. Drug-diagnostic co-development: How to harness the value. Drug Discov. Today 2011, 16, 902–905. [Google Scholar] [CrossRef]

- Allen, D.; Alves, L.; Caruncho, G.; Chin, D.; Cohn, D.; Damle, B.; Dracos, B.; Friend, S.; Ha, J.; Kadar, A.; et al. The new science of personalized medicine. Available online: http://www.PWC.com (accessed on 20 August 2012).

- Davis, J.C.; Furstenthal, L.; Desai, A.A.; Norris, T.; Sutaria, S.; Fleming, E.; Ma, P. The microeconomics of personalized medicine: Today’s challenge and tomorrow’s promise. Nat. Rev. Drug Discov. 2009, 8, 279–286. [Google Scholar]

- Personalized Medicine Coalition. The Case for Personalized Medicine 3rd ed. Available online: http://www.personalizedmedicinecoalition.org/ (accessed on 20 August 2012).

- Espicom Healthcare Intelligence. The World Pharmaceutical Markets Fact Book. 2011. Available online: http://www.marketresearch.com/Espicom-Healthcare-Intelligence-v1129/Pharmaceutical-Fact-Book-6485983/ (accessed on 20 August 2012).

- EAC Diagnostics Industry Study. 2011. Available online: http://www.eacorp.com (accessed on 20 August 2012).

- Blair, E.D. Molecular diagnostics and personalized medicine: Value-assessed opportunities for multiple stakeholders. Pers. Med. 2010, 7, 143–161. [Google Scholar] [CrossRef]

- Pfizer invests in Monogram. Available online: http://www.fiercebiotech.com/story/pfizer-to-invest-25m-in-monogram-biosciences/2006-05-08 (accessed on 20 August 2012).

- Mansfield, E.; Leptak, C. Draft Guidance for Industry and FDA Staff—In Vitro Companion Diagnostic Devices. Available online: http://www.fda.gov/medicaldevices/deviceregulationandguidance/guidancedocuments/ucm262292.htm (accessed on 20 August 2012).

- Chapman, P.B.; Hauschild, A.; Robert, C.; Haanen, J.B.; Ascierto, P.; Larkin, J.; Dummer, R.; Garbe, C.; Testori, A.; Maio, M.; et al. Improved survival with vemurafenib in melanoma with BRAF V600E mutation. N. Engl. J. Med. 2011, 364, 2507–2516. [Google Scholar]

- Goodman, M. Xalkori and the Art of Modern Drug Development. In Vivo 2012. Article No. 2012800030. [Google Scholar]

- Food and Drug Administration. FY2011 Innovative Drug Approvals. Available online: http://www.fda.gov/AboutFDA/ReportsManualsForms/Reports/ucm276385.htm (accessed on 20 August 2012).

- European Medicines Agency. Qualification of novel methodologies for medicine development: Guidance to applicants. Available online: http://www.ema.europa.eu/ema/index.jsp?curl=pages/regulation/document_listing/document_listing_000319.jsp&mid=WC0b01ac0580022bb0 (accessed on 20 August 2012).

- Stynen, D. Revision of Europe’s IVD Directive 98/79/EC—Lessons and results from the Public Consultation document. IVD Technology, 20 July 2011. [Google Scholar]

- Maverick, N.Y. My take on the Crizotinib / xalkori FDA approval. Available online: http://pharmastrategyblog.com/2011/08/my-take-on-the-crizotinibxalkori-fda-approval.html/ (accessed on 20 August 2012).

- Herper, M. Gene Test for Pfizer Cancer Drug to Cost $1,500 per Patient. Available online: http://www.forbes.com/sites/matthewherper/2011/08/29/gene-test-for-pfizer-cancer-drug-to-cost-1500-per-patient/ (accessed on 20 August 2012).

- Sauter, G.; Lee, J.A.; Slamon, D.J.; Press, M.F. Reply to V. Arena. et al. J. Clin. Oncol. 2010, 28, e85–e88. [Google Scholar] [CrossRef]

- Crino, L.; Kim, D.; Riely, G.J.; Janne, P.A.; Blackhall, F.H.; Camidge, D.R.; Hirsh, V.; Mok, T.; Solomon, B.J.; Park, K.; et al. Initial phase II results with crizotinib in advanced ALK-positive non-small cell lung cancer (NSCLC): PROFILE 1005. J. Clin. Oncol. 2011, 29 (Suppl.). Abstract 7514. [Google Scholar]

- Kwak, E.L.; Bang, Y.J.; Camidge, D.R.; Shaw, A.T.; Solomon, B.; Maki, R.G.; Ou, S.H.; Dezube, B.J.; Jänne, P.A.; Costa, D.B.; et al. Anaplastic lymphoma kinase inhibition in non-small-cell lung cancer. N. Engl. J. Med. 2010, 363, 1693–1703. [Google Scholar] [CrossRef]

- Camidge, D.R.; Bang, Y.; Kwak, E.L.; Shaw, A.T.; Iafrate, A.J.; Maki, R.G.; Solomon, B.J.; Ou, S.I.; Salgia, R.; Wilner, K.D.; et al. Progression-free survival (PFS) from a phase I study of crizotinib (PF 02341066) in patients with ALK-positive non-small cell lung cancer (NSCLC). J. Clin. Oncol. 2011, 29 (Suppl.). Abstract 2501. [Google Scholar]

- Crystal, A.S.; Shaw, A.T. New Targets in Advanced NSCLC: EML4-ALK. Clin. Adv. Hematol. Oncol. 2011, 9, 313–331. [Google Scholar]

- Jemal, A.; Siegel, R.; Xu, J.; Ward, E. Cancer statistics. Cancer J. Clin. 2010, 60, 277–300. [Google Scholar] [CrossRef]

- Taube, S.E.; Lively, T. Challenges in drug and biomarker co-development. Recent Results Cancer Res. 2012, 195, 229–239. [Google Scholar] [CrossRef]

- Cheng, S.; Koch, W.H.; Wu, L. Co-development of a companion diagnostic for targeted cancer therapy. Biotechnology 2012, 29, 682–688. [Google Scholar]

- COSMIC Database. Available online: http://www.sanger.ac.uk/genetics/CGP/cosmic/ (accessed on 20 August 2012).

- Yervoy vs. Zelboraf: Melanoma Drugs Battle for Market Share. Available online: http://seekingalpha.com/article/744721-yervoy-vs-zelboraf-melanoma-drugs-battle-for-market-share (accessed on 20 August 2012).

- Roche Half Year Results 2012. Available online: http://www.roche.com/investors/ir_agenda/halfyear-2012.htm (accessed on 20 August 2012).

- Roche / Plexxikon: vemurafenib set to impact melanoma market. Available online: http://www.datamonitor.com/store/News/rocheplexxikon_vemurafenib_set_to_impact_melanoma_market?productid=9F516C6D-E974-47E4-8060-11C464770B05 (accessed on 20 August 2012).

- Food and Drug Administration. FDA approves new treatment for a type of late-stage skin cancer. Available online: http://www.fda.gov/newsevents/newsroom/pressannouncements/ucm1193237.htm (accessed on 20 August 2012).

- Uproar as NICE rejects B-MS skin cancer drug Yervoy. Available online: http://www.pharmatimes.com/article/11-10-14/Uproar_as_NICE_rejects_B-MS_skin_cancer_drug_Yervoy.aspx (accessed on 20 August 2012).

- NICE consults on a new treatment for skin cancer. Available online: http://www.nice.org.uk/newsroom/pressreleases/VemurafenibForMelanomaACD.jsp (accessed on 20 August 2012).

- Atherly, A.J.; Camidge, D.R. The cost-effectiveness of screening lung cancer patients for targeted drug sensitivity markers. Br. J. Cancer 2012, 106, 1100–1106. [Google Scholar] [CrossRef]

- Miller, I.A.; Ashton-Chess, J.; Spolders, H.; Fert, V.; Ferrara, J.; Kroll, W.; Askaa, J.; Larcier, P.; Terry, P.F.; Bruinvels, A.; et al. Market access challenges in the EU for high medical value diagnostic tests. Pers. Med. 2011, 8, 137–148. [Google Scholar] [CrossRef]

- Gesetz zur Neuordnung des Arzneimittelmarktes in der gesetzlichen Krankenversicherung (Arzneimittelmarktneuordnungsgesetz – AMNOG). Available online: http://www.bgbl.de/Xaver/start.xav?startbk=Bundesanzeiger_BGBl&bk=Bundesanzeiger_BGBl&start=//*[@attr_id=%27bgbl110s2262.pdf%27] (accessed on 20 August 2012).

© 2012 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Blair, E.D.; Stratton, E.K.; Kaufmann, M. Aligning the Economic Value of Companion Diagnostics and Stratified Medicines. J. Pers. Med. 2012, 2, 257-266. https://doi.org/10.3390/jpm2040257

Blair ED, Stratton EK, Kaufmann M. Aligning the Economic Value of Companion Diagnostics and Stratified Medicines. Journal of Personalized Medicine. 2012; 2(4):257-266. https://doi.org/10.3390/jpm2040257

Chicago/Turabian StyleBlair, Edward D., Elyse K. Stratton, and Martina Kaufmann. 2012. "Aligning the Economic Value of Companion Diagnostics and Stratified Medicines" Journal of Personalized Medicine 2, no. 4: 257-266. https://doi.org/10.3390/jpm2040257

APA StyleBlair, E. D., Stratton, E. K., & Kaufmann, M. (2012). Aligning the Economic Value of Companion Diagnostics and Stratified Medicines. Journal of Personalized Medicine, 2(4), 257-266. https://doi.org/10.3390/jpm2040257