Abstract

Southwest China’s Yunnan province is evolving into one of the world’s largest hydro-power-producing regions. It already rivals the world’s largest hydro-producing nations. However, five of Yunnan’s six basins are international and therefore its hydropower development is of great academic and geopolitical interest. While the implementation of large projects on Yunnan’s three large rivers (Jinsha, Mekong and Nu) is relatively well studied, hydropower development outside these three main streams is hardly known. Here, we identified 128 large hydropower projects (≥50 MW) having a capacity of 16.5 GW, along with another 16.4 GW of other types of power generation, neither of which has been discussed in the academic literature yet. The paper utilizes a powershed approach to study the rapid hydropower development underway in Yunnan, both in its implication and challenges (at basin and administrative level) as well as in its trade-offs within the broader electricity context. Yunnan’s power generation and consumption patterns are characterized by diverging interests of local/provincial usage and export utilization. Within the province, the largest (hydro-) power users are energy/electricity intensive industries, which themselves have strong impacts on land use changes. Yunnan is also evolving as a major power exporter, already in 2013 exporting about one-third of its generated electricity mainly to Guangdong’s Pearl River Delta. We see a need for a critical revision of those existing generation and consumption paradigms, which includes a rethinking of major development modes, both in terms of future hydropower generation and utilization projects as well as export obligations.

1. Introduction

At the turn of the new millennium, the United States and the EU together produced almost half of the world’s electricity (45.7% or 6979 TWh) [1], with China following by a wide margin (8.9% or 1359 TWh) [2]. By 2013, only a few years later, the situation had totally changed. China quadrupled its electricity output and is now, by far, the world’s largest generator (5347 TWh or 23.2%), while the combined output of the USA and the EU remained basically stable (7515 TWh) and their combined global share dropped to 32.5% [2]; (Figure 1). A similar rapid increase, but from a much lower level, is recorded for other emerging countries, especially in Asia. This development coincides with a growing global debate about the transformation of the energy and power sectors. This discourse is faced with the challenge of finding a balance between economic growth, preservation of the environment, reduction of carbon emissions, political and economic viability, technical and political feasibility and social acceptance.

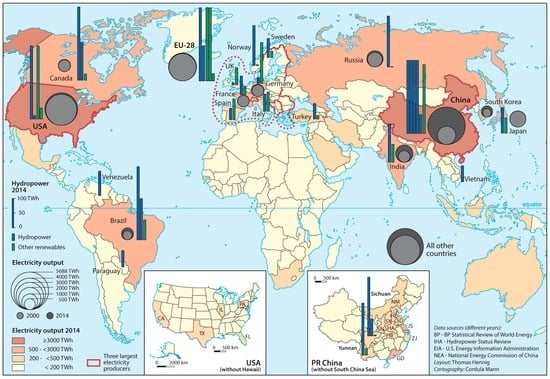

Figure 1.

Yunnan in the global setting. Global electricity production (by nation, and in comparison to Chinese provinces and US states) and global hydropower production and production of other renewables (both in 2014) of the world’s largest hydroelectricity producers (only production ≥50 TWh).

If the three largest producers (China, the United States and EU-28) are not seen as monolithic blocks, but rather considered as smaller entities (provinces, federal states or countries), huge regional disparities appear. For instance, some Chinese provinces (e.g., Jiangsu, Guangdong, Shandong) show an electricity demand comparable to that of France, Germany, Canada and Brazil—countries that are all among the ten largest electricity producers and consumers worldwide. Other Chinese provinces have a lower demand, but are large producers and therefore electricity exporters [3]. In that setting, especially provinces from China’s southwest emerge as major producers and exporters of hydroelectricity. This region has the world’s largest hydropower (HP) potential under development, concentrated especially in Sichuan Province, Yunnan Province, and the Tibet Autonomous Region (TAR), each of which currently has about 100 GW HP under development. HP development is already advanced in Sichuan (64.5 GW) and Yunnan (51.3 GW) while the exploitation of Tibet’s gigantic HP resources is just in the early stages [4]. As a comparison, the currently (2014) installed capacity in each of the two provinces is larger than in most other powerful HP nations such as India, Russia, Norway, and Switzerland. However, the major differences between the Yunnan and Sichuan cases are the drainage basins and related geopolitical implications. While Sichuan is almost exclusively drained by the domestic Yangtze basin (with a smaller region also by the domestic Yellow River basin), Yunnan shares a long international border with three other countries. Beside the Yangtze basin, it is therefore additionally drained by five transnational basins (Lancang-Mekong, Nu-Salween, Yuan-Red River, Dulong-Ayeyarwaddy [5] and Nanpan/Beipan-headwaters of Pearl River).

Yunnan is, for all its six basins, an upstream province and large upstream hydropower investments generally have pronounced downstream effects. Some scholars have argued that the level of vulnerability is fairly low for the upstream sections that lie within Yunnan, while the downstream influence is more substantial [6]. Others [7] further argue that upstream–downstream relations in the Mekong basin are not really clear-cut in a nation concept, but rather should be better differentiated between a powerful elite versus a large mass of rural poor.

The massive hydropower development along Yunnan’s large streams, especially the (few) multi-seasonal reservoirs, holds geopolitical implications, including up- and downstream conflicts, differing perspectives on basin development, national and international (hydro-) electricity import/export obligations, and different governance and legal contexts. Yunnan’s unique geographic and geopolitical setting makes it a key site for academic inquiry into large-scale HP development.

Yunnan’s power capacity at the end of 2014 was 69.3 GW [8], which is comparable to larger national economies such as Italy, Spain, Iran, and Turkey. Compared to its southeast Asian neighbors, it is even larger than those of Thailand, Vietnam or Malaysia. It is only logical, therefore, to put a special focus on the electricity and HP development of Yunnan. Yunnan’s potential to become one of the largest HP generating regions worldwide was first brought into academic discourse by He and Chen [9] and Magee [10]. Since then, a large number of subsequent studies have followed, most of them addressing either selected river sections of Yunnan’s three major rivers, or characterized by major challenges:

- Most studies on Yunnan’s large-scale hydropower development have focused on the high-profile and large HP projects along the province’s three major rivers: the Lancang-Mekong [11,12,13,14,15], the Nu-Salween [16,17,18,19] and the Jinsha-Upper Yangtze [20]. Outside those three rivers, not much is known about Yunnan’s HP development or the development of its power sector in general.

- The situation of poor data quality is similar regarding the HP development of Yunnan’s transnational basins. Studies focusing on those basins provide occasionally detailed data about HP development in downstream countries, but there is an astonishing lack of data for the Yunnan/China side of the basin [7,21,22,23,24,25]. Failure to appreciate the scale of Yunnan’s massive HP development efforts, however, results, at times, in surprising and unsatisfactory conclusions, e.g., [26,27].

- While for the transnational Mekong basin there exists a relatively wide range of studies (though most also suffering from insufficient HP data for the Chinese section), there are almost no comparable studies for the other three transnational basins with a similarly high hydropower potential, leading us to regard them as data-poor basins [6,28,29].

Despite Yunnan’s huge relevance for global hydropower development, there are only limited hydropower data available (including general generation data as well as consumption data), both at the province- and basin-scale. Besides, even though China is located in the upstream regions of most international rivers in continental Asia, China has not signed international conventions or formal agreements on international waters, nor fully participated in transboundary river commissions, all of which further impedes transparency and data availability. Instead, China has tended to prefer bilateral cooperation with its downstream neighboring countries. Thus while China continues to remain on the sidelines of the Mekong River Commission, in early 2016 the country launched its own new initiative, the Lancang-Mekong Cooperation, ostensibly intended to be a platform for the six riparian countries to discuss regional cooperation beyond water issues in the Lancang-Mekong basin. Yet, bottom-up approaches to utilizing and managing transboundary waters often prove difficult in terms of sharing data on hydrology, environmental issues, water resources engineering, and the like. This is true even within one basin that lies entirely within one nation-state; it is no surprise, then, that it should be even more difficult across national boundaries.

This article aims to fill that void, and contribute to discussions of the water–energy nexus in the region, by highlighting the HP development underway in Yunnan and the tight interconnection between electricity-intensive industries and stress on water resources. The basic concept of the water–energy nexus takes on different manifestations depending on the context, scale and geography in which it is examined [30,31,32,33]. For this paper, we analyze and discuss various interdependencies among water, hydropower, and energy-intensive industries in the context of electricity exports. The geographic scale of our analysis is primarily provincial, though we hasten to note that the ways Yunnan Province is embedded in new geographies of electricity production and distribution across southern China and Mainland southeast Asia fundamentally shape the nature of water–energy–industry interdependencies in the region.

The article addresses the following research questions. First, what is the status quo of Yunnan’s HP development within its entire power generation picture? Second, how does Yunnan’s HP development fit within a broader electricity context (electricity consumption, import/export, power transmission)? Finally, what are the major challenges related to Yunnan’s large HP implementation?

The paper first provides a brief overview of the study region and the powershed approach. Section 3 provides detailed and, to the best of our knowledge, novel data and analysis regarding Yunnan’s hydropower development, as well as its other power generation types, while also describing Yunnan’s consumption pattern (both local demand and power export). Section 4 describes and discusses important implications and challenges related to Yunnan’s hydropower development. This includes a brief historical overview of that development; a discussion of the development rights for large and mid-sized HP cascades in various river basins (the latter with focus on Yunnan’s Ayeyarwady basin); the role of the Clean Development Mechanism (CDM); and challenges and utilization conflicts of Yunnan’s Power Grid. Section 5 concludes with some policy suggestions.

2. Materials and Methods

2.1. Data Procurement

The study is based on extensive fieldwork in Yunnan from 2005 to 2016. It considers all commissioned large HP (LHP) projects in Yunnan (≥50 MW) and all HP data for the Chinese Nu and Ayeyarwady basins (≥1 MW). The data were obtained from different government agencies (e.g., Development and Reform Commission, Bureau of Water Resources, etc.) or from yearbooks [4,8]; additionally, media reports and web documents were collected (e.g., CDM project design documents). Altogether, we identified 128 LHP stations outside Yunnan’s three main rivers, including those under construction. For all those LHP projects we compiled a comprehensive database [34] and geovisualized them in thematic maps.

Over the decade we conducted more than 50 open-ended, in-depth interviews with HP stake-holders and expert observers. These included interviews with government representatives at county, prefecture, and provincial levels (e.g., Development and Reform Commission, Energy Bureau, hydropower planning commission, water resource department, forest department, environmental protection bureau.); academics familiar with Yunnan’s HP development; individuals from the power sector (e.g., representatives of HP stations, China Southern Power Grid (CSPG), Yunnan Power Grid (YPG); and individuals involved in energy-intensive industries. Further, we visited, during multiple field campaigns, more than 100 HP stations of Yunnan, both small and large ones. In those field visits we additionally had many talks with persons affected by local HP development (e.g., HP owners and employees, village heads, resettled or other affected villagers) and conducted some surveys. We mapped HP structure and river diversion, collected additional HP-related data and in one case conducted a first fish species inventory. The information was used for geovisualizing results in thematic maps and for conducting basic multivariate analyses.

2.2. The Powershed Approach

The recent boom in global dam activities is of great scholarly interest. We recognize that each HP project, large or small, is characterized by specific peculiarities that cannot be generalized. Nevertheless, due to long traditions in HP construction, on a general level, the financial calculus as well as the ecological, environmental and social impacts of large HP projects are well known and documented [35,36,37,38,39,40].

In recent years, in the context of climate change and the attendant national mitigating strategies, HP development is often analyzed in the context of national energy policies. Scholars have undertaken country-based studies in China [41,42,43,44], and India [45,46,47,48], Turkey [49,50] for example. Yet such macro-level policy approaches rarely consider regional/local dam activities and their consequences, and often neglect the electricity demand side. Still other studies model worldwide dam activities and their impacts on a global scale [26,27,51,52,53]. Not surprisingly, the quality of those models depends very much on the global dam data. Asia is particularly problematic; it is the region with the world’s fastest growth of dam construction, yet the data quality is often very poor.

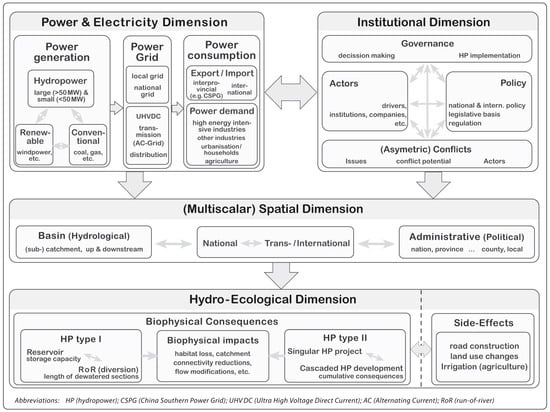

For our study, we use the frame of the powershed approach first introduced by Magee [10]. This approach serves as a lens for understanding scalar politics of electricity (both in generation and consumption) in a dynamic and process-oriented sense. We refine Magee’s initial framework here to focus more sharply on power relationships—comprising both the conductors that carry electricity from generator to user, as well as the political-economic dynamics among institutions related to that infrastructure. We also examine the trade-offs between (hydro) power generation and other uses of waterways. In doing so, we hope to enrich our spatiotemporal and empirical understanding of Yunnan’s significant large-scale HP development. Figure 2 builds on Magee’s initial concept to better conceptualize the complex interplay of Yunnan’s rapid HP development and the overall electricity development (generation, transmission, and consumption); the environmental implications of hydropower; and the institutional arrangements (from actors, politics, policy and governance to asymmetric conflicts). This framework facilitates such a multi-dimensional analysis of HP development and its various trade-offs and consequences. Since not all the dimensions of HP can be equally measured in one paper, we emphasize here the power and electricity dimension (see top left of Figure 2). The approach provides a richer understanding of development trajectories and helps to highlight often neglected and less studied trade-offs, such as the spatial dimension, cumulative implications of multiple projects, or the parallel development of hydropower and energy-intensive industries, as is occurring in rural western Yunnan.

Figure 2.

Modified conceptual map of Magee’s powershed approach [10].

2.3. Study Area

Yunnan province, roughly ten percent larger than Germany, covers 394,100 km2 and shares a 4060 km-long border with Southeast Asia (Myanmar, Laos and Vietnam). The landlocked province has for a long time been seen by the country’s eastern leadership as geographically peripheral and socio-economically marginal. However, its geopolitical location makes it China’s gateway towards Southeast Asia and India (via Myanmar), both in transportation infrastructure development as well as (transboundary) HP development. Yunnan has a population of 47 million. About one-third of the population belongs to various ethnic groups, making it the most culturally diverse province of China.

Yunnan’s topography is primarily mountainous in character. Basins comprise only seven percent of the area, but the majority of the population lives in those basins. Yunnan’s geologic and geographic diversity, combined with a climatic setting that ranges from tropical to alpine, has led to a unique diversity of ecosystems. It is part of two of the world’s major biodiversity hotspots and several important ecoregions [54]. Yunnan hosts about half of China’s biodiversity, which is also reflected in the fact that about 6.3% of its territory lies within protected areas on the national or provincial level. The province has over 600 rivers forming six large river basins, of which five are transnational. Yunnan’s varied topography, hydrology, and climate combine to yield one of the largest HP potentials worldwide.

3. Yunnan’s Power Sector

Yunnan’s power sector is currently one of the largest HP generators and a major electricity exporter (Figure 3). Yet a decade ago, Yunnan’s HP generation was only 10% of today’s figure and the province routinely suffered power shortages. Further, it was only in 2008 that Yunnan shifted to HP as the major source of power generation. This rapid growth of HP, both small and large, has created a considerable oversupply during the rainy season, resulting in grid congestion and power curtailment (i.e., periods when grid assets are inadequate for transmitting all the available electricity supply, requiring certain generators to be shut down or idled). Such conditions, not surprisingly, can yield financial losses for the generators. It was mainly for this reason that, in 2014, Yunnan was selected by China’s National Energy Commission as a pilot area for allowing direct power purchase and sale between electricity generators and large power users (e.g., smelters); but only from 2016 will such arrangements be permitted across the province.

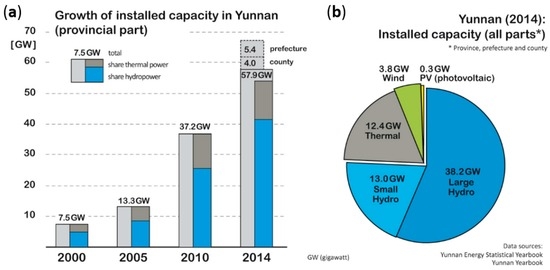

Figure 3.

(a) Growth of Yunnan’s power sector and (b) its sectoral and administrative shares in 2014.

As noted above, data on Yunnan’s power sector are limited, often difficult to obtain, and may vary considerably depending on the source. Hence, different statistics are referenced in the academic literature and often they jump between different statistical sources which results sometimes in ‘odd’ time series. Contradictory data affect both electricity generation and utilization as well as installed capacity. The reasons are multiple. Often, data refer only to provincial statistics and neglect the local level (prefecture or county). For 2013, this difference amounts to 9.2 GW, mainly hydropower; hence data for Yunnan’s 2013 capacity range between 51.1 GW and 62.3 GW. Other reasons for varying data include an inconsistent differentiation between small and large HP and, especially for the megaprojects, disparities between reported and actual commissioned turbines (installed capacity). Also, some data for megaprojects on the Jinsha River, which for a stretch forms the border between Yunnan and neighboring Sichuan Province, include the Sichuan share of generation in the Yunnan data. Additionally, Yunnan’s provincial data can be further categorized into three groups: national plants which primarily serve power export (5 × LHP and 2 × thermal power), provincial plants (49 × hydropower, 9 × coal and 8 × wind power plants) and those under joint management between provincial-level and local-level entities (106 × hydropower and most other renewables).

3.1. Overview of Yunnan’s Power Portfolio

3.1.1. Small and Large Hydropower

Yunnan’s theoretical HP potential is far above 100 GW and its economic and technically feasible HP potential is estimated between 96 and 104 GW. The province’s three largest rivers, Jinsha, Mekong and Nu, hold 85.6% of Yunnan’s economic and technically feasible HP potential, estimated at 82 GW installed capacity or 403 TWh [55] of annual output [56]. Our current knowledge about Yunnan’s HP development is almost exclusively based on these three rivers. In 2015, there were 12 existing HP stations only along the Jinsha and Mekong with another ten under construction or partly commissioned (Table 1).

Table 1.

Brief overview of hydropower stations along Yunnan’s three largest rivers.

In 2014, Yunnan had an installed HP capacity of 51.3 GW and HP generation of 177 TWh [4]. Both figures are larger than their equivalents of most other HP-rich nations such as Russia, India or Norway. The core of it is produced in the above relatively well studied river cascades. We identified another 128 LHP projects (≥50 MW), including those under construction, but excluding those still in the planning phase. The 128 LHP projects have a cumulative capacity of 16.5 GW, roughly equal to the HP capacity of countries such as Venezuela, Sweden or Switzerland. However, these projects are virtually absent from the academic literature. According to Chinese classification, they can be further differentiated between six projects of large size (≥300 MW) and the remaining 122 of moderate size (between 50 and 300 MW). Yunnan’s presently largest HP project outside its three main rivers is Daying-4 (875 MW) within the Ayeyarwady basin. This tiny catchment has, together with the much larger Yangtze and Red River Basins, the largest number of HP projects >100 MW (Figure 4).

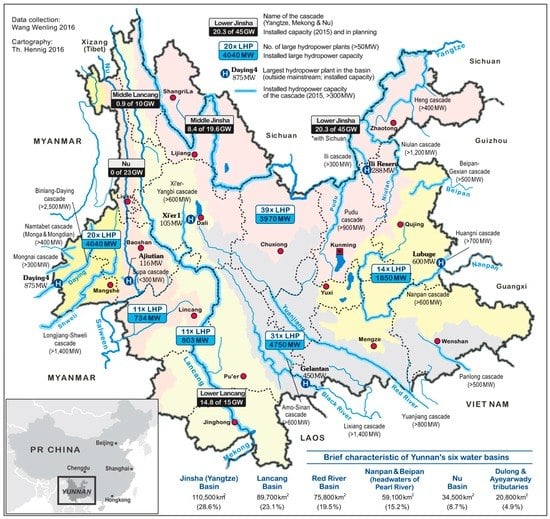

Figure 4.

Overview of Yunnan’s large hydropower development in its six river basins.

Compared to LHP, the contribution of small HP (SHP) is often neglected, mostly due to difficulty in accessing relevant data. However, in 2014, Yunnan’s installed SHP capacity was some 13.1 GW, which is equal to 25.6% of Yunnan’s HP capacity. The SHP figure alone is far larger than that of many other HP-rich nations, and comparable to the entire HP capacity of Austria or Vietnam. Yunnan’s SHP sector comprises more than 1600 SHP stations with installed capacities ranging from 0.5 MW to 50 MW [57]. Further, there are still thousands of micro-HP projects with installed capacities <500 kW which primarily serve rural electrification, but their number is gradually decreasing. Yunnan’s installed SHP capacity is ranked first among all Chinese provinces and it can be considered as the region (province) with the world’s largest installed SHP capacity. Since 2000, Yunnan’s SHP capacity has quadrupled, and since 2010, despite yearly variations, its electricity output has exceeded 20 TWh annually [41]. Despite these impressive figures there are many problems and challenges related to SHP. About one-third of them are located in remote areas which still have a semi-autonomous grid with only limited connectivity to the Yunnan Power Grid (YPG). In the flood season, SHP generation is routinely curtailed due to limited transmission capacity, causing considerable losses in electricity output and the revenues that would have been derived from that output. Already in 2010, the SHP loss was 1.7 TWh. In other areas that are better incorporated into the YPG, the situation is less tense due to improved management of various sources (“dispatch”) in ways that reduce or avoid grid congestion and overloads. The second major challenge related to the rapid SHP development lies in its omni-presence approach (due to the popularity of the cascade concept among HP developers). It causes a fragmentation of almost all its subcatchments, mainly by alternating damming and dewatering (drying up) of long river sections. Some scientists assess that the negative ecological impacts, compared to the limited electricity output, are larger than those of large dams [58].

3.1.2. Thermal Power

After HP, Yunnan’s thermal power sector, at 12.4 GW of installed capacity, is the province’s second-largest electricity producer, whereas before 2008 it was the largest. The old coal-fired power plants, built in the 1950s, underwent several expansions and capacity upgrades until 2012; among them is also Xuanwei, Yunnan’s first coal-fired plant. Since 2000, Yunnan’s thermal power sector has seen numerous older, smaller plants (<250 MW) decommissioned under the guise of pollution abate-ment. Thus, while six of the province’s current 11 thermal plants trace their history to the last century, 10.8 GW of new thermal power has been newly built. Currently there are no new coal-fired plants under consideration; only enlargements of existing plants are being discussed. Yunnan’s thermal electricity production is relatively stable around 58 TWh per year, but thermal power’s relative share decreased to 27% as of 2013. All of the newly constructed or modernized power plants employ subcritical boiler technology, whereas the five largest use supercritical technology. Two national plants (Diandong-I + II) support electricity export to Guangdong, while the other nine plants feed into the provincial grid (Table 2).

Table 2.

Other large power plants of Yunnan (≥50 MW), except hydropower.

Yunnan has no major oil and gas reserves. In 2013, a high-profile and geopolitically important oil-and gas pipeline was completed. It starts in Myanmar’s Arakan state (Kyaukphu) and goes via Dehong and Dali to Anning, near Yunnan’s capital Kunming. The gas pipeline will facilitate gas imports from Myanmar and the Andaman Sea and Indian Ocean, and has since been expanded to the neighboring province of Guizhou. In that context there are plans for three gas power plants in Yunnan.

3.1.3. Other Renewables

Beside HP, wind power is the fastest-growing renewable energy source in Yunnan, but installed capacity remains at a low level compared to that of HP. The province’s first two wind farms were established in 2008. By late 2014 Yunnan had an installed wind power capacity of 3780 MW [8], twelfth-highest among all Chinese provinces. During the dry season, with its limited HP generation, wind power is an important complement to support network stability, yet it often contributes to network congestion (overloading) during the rainy season when hydropower output is at its peak.

Recent years show a rapid increase in wind power; in 2014 alone Yunnan installed an additional capacity of 1590 MW distributed over 25 wind farms. However, the growth is less than expected, mainly due to price. The tariff for Yunnan’s in-province wind power is CNY 0.34/kWh, making it more expensive than hydro- and thermal power [59]. Currently, Yunnan has 80 wind farms, of which 70 feed into YPG and ten support prefecture-level local grids. Due to tax and permitting reasons, 51 of those 70 wind farms have an installed capacity just below 50 MW (48–49.5 MW). The largest number of windfarms are found in northwest Yunnan, especially in Dali prefecture. Northwest Yunnan is a global biodiversity hotspot and most of its wind farms are developed around the timberline ecotone (>3500 m), which is ecologically vulnerable to human interventions. The large-scale localized deforestation within those parks (including related infrastructure development) contributes significantly to habitat fragmentation and is seen very critically among conservationists. A proposed wind farm from Yunnan’s largest power generator, Hydrolancang, failed due to intensive local protests, led by monks. The wind farm had been planned for Mount Jizushan, one of Asia’s most sacred mountains. In 2015, 50 wind farms in Yunnan were registered as CDM projects, with almost half (22) in Dali prefecture. Of those, 41 have installed capacities between 48 and 49.5 MW, thereby allowing them to avoid province-level scrutiny and approval. In contrast to HP, most wind farms that have applied for CDM are built and operated by state-owned companies.

Other renewables play only a minor role in Yunnan. The installed capacity of photovoltaic (PV) is 266 MW (less than 10 percent of the province’s wind capacity), with the largest solar array situated in Shilin (166 MW), and two others in Chuxiong. Yunnan’s first biogas plants came online in 2014; at the time of writing, seven plants have a combined capacity of 105 MW.

3.2. Yunnan’s Electricity Demand and Its Challenges

Yunnan’s rapidly growing HP generation is mainly driven by two complementary yet competing interests: its domestic demand and its export obligations. Relevant for both is Yunnan’s provincial grid which is part of CSPG, the smaller one of China’s two national grids. Beside Yunnan, it also consists of the provincial grids of Guangdong, Guangxi, Guizhou and Hainan. YPG is in charge of 16 prefectures, of which four still have a semi-autonomous grid with only limited connectivity to YPG. Those four peripheral prefectures exclusively depend on HP for their electricity generation, especially SHP. The major challenge of those grids is that they, compared to their huge HP generation capacity, lack sufficient transmission capability to deliver and transmit power. Often, those regional grids are only connected to YPG by one or two 110 kV or 220 kV lines, which have limited transmission capacity compared to larger facilities. Especially during the flood seasons it results in major network congestions. The general principle of limited transmission capacity is also valid for the entire province.

In 2013, Yunnan’s electricity generation was 216.8 TWh of which the provincial grid provided 174.5 TWh and the regional and local grids produced 42.3 TWh [8]. In 2013 alone, it increased by 40 TWh, primarily due to newly added hydroelectricity assets. Yunnan’s electricity generation is almost entirely produced within the province, with only a small part imported from two HP plants in neighboring Myanmar; but between 2011 and 2013 the Myanmar share decreased from 2.42 to 1.88 TWh. The import from other adjoining provinces is negligible (0.4 TWh). In 2013, 67.3% of Yunnan’s grid-fed electricity was consumed within the province while 22.7% was exported, mainly to energy hungry Guangdong. One of Yunnan’s key challenges is the wastage of hydroelectricity, mainly due to network congestions during the monsoon season. The loss of potential electricity generation, especially from the recent Jinsha dams, doubled in the past four years and reached 20 TWh in 2014 [60].

3.2.1. Yunnan’s Electricity Export

Already in the late 1980s, Chinese policymakers conceptualized the West–East electricity transfer to support the rapid economic development of eastern and southern coastal regions. Yunnan’s first transfer started with the construction of the Lubuge dam (600 MW) in the early 1990s, a period when Yunnan was still a power deficit region. Around the turn of the century, as the economic disparities between eastern and western (or coastal and inland) China became clearer, the rhetoric of addressing that disparity crystallized in the Western Development Campaign (xibu dakaifa) [61]. Much has been written about the strengths and weaknesses of the campaign, with some arguing that it simply legitimized longstanding patterns of western resource extraction to support eastern development, and others countering that it indeed represented a good-faith effort by central planners to address the “backward” (luohou) [62] nature of western regions. Most relevant to our discussion is the fact that xibu dakaifa legitimized a handful of other policies specifically related to Yunnan’s electricity generation and transmission. The names of some of those policies, most notably Send Western Electricity East (xidian dongsong) and Send Yunnan electricity to Guangdong (Dian dian song Yue), clearly reveal the geographies of power, both electrical and political, in which Yunnan is implicated.

By 2013, those new geographies of hydroelectric dams and long-distance transmission lines had enabled an aggregated electricity transfer of 350 TWh, of which 154 TWh refer only to the last three years (2011–2013). Since 2008, the yearly transfers have exceeded 20 TWh annually, reaching 70.8 TWh in 2013 (Figure 5). Yunnan’s electricity export obligations are growing much faster than its provincial demand. Currently, about 85% of Yunnan’s power exports go to Guangdong province, especially the Pearl River Delta. Guangdong, with a population of 104 million people, is one of the world’s largest manufacturing hubs. Until 2012 it was China’s largest electricity consumer, but has since been overtaken by eastern China’s Jiangsu province, another major industrial hub. In 2013, Guangdong had an electricity demand of 483 TWh, but an electricity generation of only 365 TWh which caused an electricity deficit of 118 TWh [4]. Guangdong (and CSPG) has compensated for this fast-growing deficit mainly by importing HP from other provinces, especially Yunnan and Guizhou, via dedicated long-distance ultra-high-voltage-direct-current (UHVDC) transmission lines. Thus, in 2014, more than 11% of Guangdong’s power consumption was met with generation from Yunnan. The latest power agreement (2015) between Yunnan and Guangdong calls for an annual transfer of 88.2 TWh. As a result of the new transmission lines between the two provinces, the powerful National Development and Reform Commission (NDRC) cut the prices for Guangdong’s hydro-imports from Yunnan to 0.45 ¥/kWh which is lower than the import price of other provinces and even 0.22 ¥/kWh lower than Guangdong’s benchmark retail price [59]. Yunnan’s electricity exports are not constantly transmitted over the year. They are based on the monthly (hydro-) electricity output, which, due to limited storage and reservoir capacity, varies significantly between wet and dry seasons. In only three month of the rainy season (July to September), Yunnan produces about 40% of its annual hydroelectricity but consumes only 24%. It is the key period for electricity export and it corresponds to the peak demand in Guangdong [63]. In step with these seasonal variations, Yunnan’s monthly export obligations can surpass 10 TWh during the rainy season and fall below 3 TWh in the dry season.

Figure 5.

Nuozhadu, the largest hydropower project in terms of installed capacity (5850 MW) and storage reservoir along the Mekong, and one of the key projects for Yunnan’s electricity transfer to Guangdong (Photo: He Daming).

Yunnan’s power exports are based on two different approaches, the UHVDC point-to-point transmission and the traditional grid exports. In the latter, power stations feed into YPG and their electricity is transmitted via the neighboring provincial grids to the load center. Hence both, decision making for power plant construction (including problems and benefits) as well as electricity management takes place within the province. Currently, Yunnan has two major 500 kV export corridors. One passes via Qujing (Yunnan), Guizhou and Guangxi to Guangdong. It mainly includes hydroelectricity from the Jinsha and Mekong basins and thermal power from two plants in Qujing. The other YPG corridor started in 2009 and mainly transmits hydroelectricity to Guangdong from Yunnan’s Ayeyarwady and Red River basins. Interestingly, the SHP clusters in both basins also support the electricity export to Pearl River Delta, even though SHP has long been hailed as a solution for meeting local electricity needs in rural Yunnan where grid connections were tenuous or nonexistent.

Compared to the traditional grid exports, the UHVDC trunk transmission is now dominating the export sector. It is based on a small number of very large HP stations along the Jinsha and Mekong. Its hydroelectric output is not fed into the YPG; instead from the nearby converter it is directly sent to the demand region in the Pearl River delta (point-to-point), and only from there is it fed into Guangdong’s grid. Hence, YPG does not have any rights of management nor any financial benefits (e.g., taxes) and the decision-making is exclusively done by CSPG and/or the national government. The local financial benefit is, in most cases, limited to the compulsory fee per kWh of generated electricity, which officially flows back to the local government. The world’s first UHVDC transmission line capable of handling more than 5 GW of power started operation in 2009, between Chuxiong (Yunnan) and Guangdong. Later, two other UHVDC-lines were built between Guangdong and Nuozhuadu (5 GW) and Xiluodu (6.4 GW) and two more are underway. The related power struggle about the utilization of that electricity is described in Section 4.5 (Figure 6).

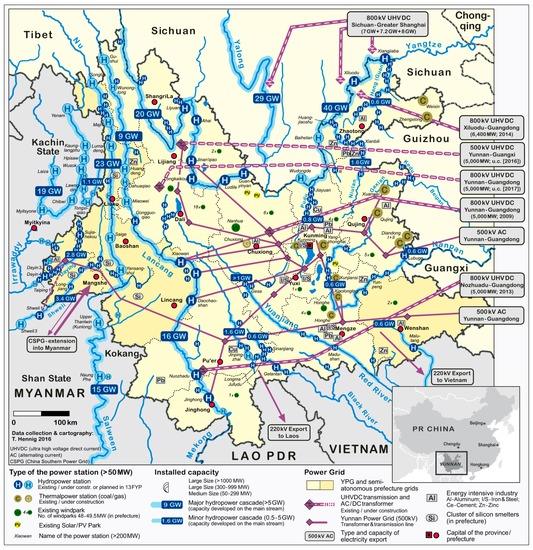

Figure 6.

Status quo of Yunnan’s power sector in 2015.

Yunnan is also a major exporter of hydroelectricity to its neighboring countries. Since 2004, it has been transferring electricity to northern Vietnam, in 2013 3.2 TWh. This trade has earned YPG more than $1.5 billion in the past decade [8]. While, in the beginning, Yunnan’s hydro exports to Vietnam were seen as necessary, especially during peak demand periods, they are now criticized as non-beneficial to Vietnam [64]. With the completion of large projects in Vietnam the export rate will likely drop in future. Already, since 2001, Yunnan supports Lao PDR’s border areas, which are still not connected to the Lao national grid. Even though this cross-border transmission is still small (0.3 TWh in 2013), it will almost certainly grow in the future. The cross-border transmission is similar in areas along Myanmar’s border, but electricity sales from Yunnan to Myanmar declined following the completion of two LHPs in Myanmar, which now primarily export electricity to Yunnan. The long-delayed UHVDC-transmission line from Yunnan’s Mekong dams (e.g., Jinghong) to Thailand will start its operation only in 2017. The reasons for that long delay are mainly related to the withdrawal of Thai financiers.

3.2.2. Demand within Yunnan

In 2013, Yunnan’s provincial demand (146 TWh) was still almost double its electricity exports (70.8 TWh). Between 2008 and 2013 Yunnan’s electricity export grew by 350%, while the provincial consumption ‘only’ doubled over the same period [8]. In terms of GDP (gross domestic product), Yunnan is one of the poorest provinces of China, but its own electricity demand is comparable to its neighboring and nearby countries (Vietnam: 130.1 TWh and Thailand: 164.8 TWh). Yunnan is rich in many minerals; some deposits are the largest in China. Spurred by this rich cache of mineral deposits, the metallurgical and chemical industries with their high electricity demand have interests intertwined with those of HP developers and have thus become a critical engine for local economic growth, including job creation and local government tax revenue [65]. In 2013, Yunnan’s energy-intensive industries (processing and manufacturing) consumed 112.3 TWh, which corresponds to 76.9% of the provincial consumption. It is only slightly higher than China’s average (73.5%) but it is much higher compared to other industrialized countries (e.g., Japan 29.7%). In contrast, Yunnan’s residential utilization is only 18.3 TWh (12.5%).

4. Discussion of Yunnan’s Large-Scale Hydropower Development

4.1. Yunnan’s Hydropower Development and Policy

China’s first HP project was built in 1912 in Shilongba (0.48 MW), near Yunnan’s capital city Kunming, and in 1946 another station was built along the Xi’er river near Dali (0.4 MW). With the establishment of the People’s Republic of China in 1949, despite its huge potential, Yunnan’s HP development increased only modestly due to the strict financial limitations. Up to the mid-1980s (hydro-) power generation and investments were an absolute state monopoly, first exclusively held by the central government, and later shared by the provinces. In that period Yunnan was either too poor or too remote to invest in large HP projects; therefore only a few projects of moderate size came up in the 1970s, like the cascades on the rivers Xi’er in Dali (now 255 MW) and Yili in Qujing (now 321 MW) as well as Lüshui in Honghe (now 92 MW). In 1985 Yunnan’s installed HP capacity was merely 679 MW, only about one-third of the province’s total capacity, which was still dominated by small and old thermal power plants.

In response to increasing power shortages and low electrification rates, the first reforms of the power sector were implemented in the 1980s. They resulted in an important milestone for Yunnan’s small and large HP development. In 1982 China launched its first round of rural electrification. During that pilot program, 1600 MW of SHP capacity was installed in 109 Chinese counties. This success resulted in China’s main strategy of rural electrification through SHP exploitation, and led to a specific SHP development model with distinct Chinese characteristics [66,67]. Dehong prefecture of Yunnan’s Ayeyarwady basin was China’s second region to successfully complete its rural electrification in 1995. However, it was not until 2012, with the rural electrification of the upper Nu valley, that the entirety of Yunnan finally became electrified.

With the gradual opening of the generation market throughout the 1980s and 1990s, the provincial and local power bureaus became operating entities [68]. Consequently, a larger number of moderate-sized (between 1 MW and 100 MW) HP stations were established and regional grids were developed parallel to the provincial and national grid. Furthermore, in the 1990s, due to the acute power shortage, Yunnan experimentally committed funds to develop expensive but much needed LHP projects. Manwan (now 1670 MW), completed in 1995 on the main stream of the Mekong, was the first LHP plant co-financed by the central and provincial government. Lubuge (600 MW) was China’s first HP project co-financed (20%) by the World Bank (including Australia and Norway). It became the symbol of China’s reform policy related to the water sector. In addition, finally, Dachaoshan (1350 MW), completed in 2003, became the first LHP project exclusively funded by Yunnan and its different province-owned corporations [69].

Yunnan’s actual dam boom really began in the new millennium and only subsequently did HP become the main source of electricity production. It is also a consequence of the rapidly increasing electricity demand in China’s coastal provinces and the reform of the power sector in 2004. The opening of the power market had two major implications. For smaller rivers and SHP projects the development rights were mainly given to private entrepreneurs (especially from coastal China). The development rights of the major rivers had traditionally belonged to the central and provincial governments, hence the six major state-owned power corporations are the major developers along the large rivers with their huge HP potential. Among them Hydrolancang, the Yunnan branch of Huaneng, plays the most important role.

4.2. Development Rights of Yunnan’s Large Hydropower Cascades

Since 1949, HP development of China’s large streams has been under control of the central government, which, traditionally, used to license development rights to the provinces. In Yunnan’s context, the development rights for the Jinsha, which forms a provincial border to Sichuan, were given to both provinces. However, in the mid-1990s, due to financial weakness and insufficient engineering expertise of the two provinces, the development authority for its proposed cascades was given to large power corporations [70] in which the central government owns a majority share of the stock. Although the basic development concepts of these cascades are well known, the reality of development rights within single cascades is more complex than previously thought, which was resulted in some repeated misunderstandings. Only two of Yunnan’s large cascades (Lower Jinsha and Lancang) are being exclusively developed by one company. The situation is more complex in the two other large cascades (Middle Jinsha and proposed Nujiang), where the development rights belong to a company with different large shareholders (Table 1), which are mainly state-owned power companies, Yunnan province and the private developer Hanergy. Therefore in both cascades, individual projects will be developed by different companies. Most notably, Jin’anqiao is China’s first large privately owned HP station (Hanergy holds 80% of its shares) and Nujiang’s proposed two largest projects, Songta and Maji, are set to be built and owned by Datang and Huadian , respectively (two of the Big Five state-owned power companies).

Another striking issue in the development of those cascades is the ongoing power struggle between electricity demand and environmental concerns. The basis for most of Yunnan’s large HP development is the Comprehensive Utilization Plan of the Yangtze River, which has seen several revisions. Only in the latest revision of 2009 were environmental concerns seriously considered, but this revision has not been approved yet by the State Council [71]. In consequence, most projects of the Jinsha cascade were not built according to the modified 2009 plan, which especially affects site selection and storage capacities (two topics that received much more careful attention in the 2009 revision). Nevertheless, in 2004, the controversial Tiger Leaping Gorge dam/reservoir was stopped (at the original location). Additionally, three projects were temporarily halted due to violating legal procedures. In 2006, the Jinsha was diverted at the Jin’anqiao site to allow for construction to begin, despite not having received final NDRC approval. In 2009, Ludila and Longkaikou were completed without submitting their EIA (Environmental Impact Assessment) reports [71]. However, now all three projects are completely finished. Similar to the Jinsha dams, Hydrolancang started construction of dams in the upper Mekong cascade without governmental approval. Additionally, the Guonian dam in Deqin was cancelled due to its potential impacts to the core area of the National Nature Reserve (Three Parallel Rivers).

The development of the proposed Nu river cascade (23 GW) has been put on hold since 2004, initially for failing to comply fully with the then newly implemented Environmental Impact Assessment Law. After that halt, the cascade was modified, with plans now calling for development to proceed in two phases. Already, in 2013, the NDRC decided to develop Stage 1 in the concept of one major reservoir plus four smaller (though still large) projects. Details such as installed capacity and reservoir size, however, have not been given with any certainty so far. We wish to emphasize, however, that in contrast to several poorly researched reports, no HP project per se on the Nu is presently under construction, although intensive preparations [72] have been underway at these sites for more than a decade. Further, northwestern Yunnan is extremely remote and mountainous, and Songta and Maji, sites of two major dams, still have insufficient road access, which does not allow any major construction. However, a new and wide road within the narrow canyon is currently under construction.

Comparing the current HP implementation along Yunnan’s Jinsha and Lancang rivers allows a crucial conclusion. If a LHP cascade or a longer river section is developed and owned by the same company (not in the sense of the ‘general’ multi-shareholder development company), it enables a coordinated management approach which could potentially mitigate negative environmental impacts for a larger part of the watershed, including some of the tributaries. That is, modifications to dam construction and operation parameters (e.g., dam height, number, precise location, and output) are easier to implement if they occur within one company than if they require coordination across several companies. Such a coordinated approach, which already includes proposed future projects, also enables the project developer to minimize social implications. In contrast, a fragmented ownership situation results merely in a project-based focus which will likely have more serious environmental and social costs.

4.3. Development Rights and Implementation Challenges of Yunnan’s Mid-Sized Hydropower Cascades

In contrast to Yunnan’s three large rivers, HP cascades on tributaries are only of moderate size. The largest of those cascades can be found within China’s Ayeyarwady and Red River basins. The development rights for these mid-sized HP cascades are quite diverse. It is striking that the development rights (except Lixian, Heng and Pudu cascades) rarely belong to one company, which again are mostly structured as shareholding corporations. In addition, China’s Big Five companies are present in many singular projects, often later purchased from private investors. Besides, so-called dianneng’s [73] (“local” electric power companies) are well present in many mid- or small-sized HP cascades. They are especially strong in their former regional nuclei and in projects from the first wave of HP development from the late 1990s and early 2000s. Hence, most of Yunnan’s mid-sized HP cascades are developed by many different companies, often in a mix of state-owned, province-owned and private shareholders. Especially in the late 1990s and early 2000s, development rights were given to different entities which were not financially strong enough to undertake development of the entire subcatchment.

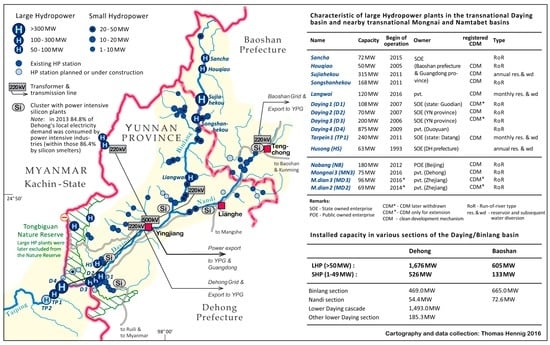

Additionally, some of the most lucrative mid-sized projects are located near international borders with Myanmar and Vietnam, where they are often embedded in complex implementation patterns. This may be briefly illustrated by the example of the transnational Daying River (Figure 7), which is only a 246 km-long tributary (MQ: 178 m3/s) of the Ayeyarwady, but which holds the largest HP potential outside Yunnan’s three largest rivers. That potential, estimated at 2.6 GW, has been developed in two cascades of 16 dams, of which ten are LHPs. Only one reservoir has an annual storage capacity; all other dams are of diversion type without major storage potential. The projects are shared by China and Myanmar, including two Chinese prefectures; hence three different power grids. All projects, except the most downstream dam in Myanmar, are finished and almost all support (either entirely or partially) electricity transfer to Guangdong (including the project in Myanmar). Only the five upstream projects belong to the same developer, while all the others are held by different private-, province- or state-owned entities. The complex HP approval system can be best illustrated for the downstream cascade, consisting of six dams and forming the border between China and Myanmar. Additionally, this section also comprises the former core area of Tongbiguan Nature Reserve which shows characteristics of the northern tropical margins and is famous for its unique biological diversity blending Indian and Chinese fauna and making it to one of the key biodiversity hotspots in Yunnan [74].

Figure 7.

Hydropower development in the transnational Daying Basin. It exemplifies the combination of large and small hydropower as well as a highly fragmented ownership and complex grid structure. It further exemplifies large hydropower development in a transnational context of protected areas, such as Tongbiguan Nature Reserve, one of China’s largest biodiversity hotspots.

It is here that Daying-4 (875 MW) is located [75], currently the largest HP project within the entire Ayeyarwady basin and the largest outside Yunnan’s three large rivers. The run-of-river [76] project is privately owned by Duoyuan company and diverts the river over a distance of 17 km where it forms an international watercourse (as a boundary river) with Myanmar; during the dry season this section totally dries up due to the dewatering caused by Daying-4’s diversion. For this reason, Daying-4 was formerly not approved by Yunnan’s Environmental Bureau. In order to legitimize the project, the affected area was excised (discursively, at least) from the Tongbiguan Nature Reserve and is now called the experimental zone of Tongbiguan. Further, the affected site in Myanmar is not controlled yet by Myanmar’s national government, but only by the Kachin Independent Organization/Army.

Daying-4 is, in essence, only accredited by the local militia. Directly downstream is Darpein1 and both dams form the nucleus for YPG’s 500 kV transmission line going to Guangdong (see above). Even though Darpein1 lies within Myanmar, officially only 7.8% free power is fed into Myanmar’s power grid, hence the project almost exclusively supports YPG and electricity transfer to Guangdong [77]. Ironically, it is also Myanmar’s first HP project that successfully applied for and received CDM funding. In contrast to neighboring Daying-4, it was approved by Myanmar’s central government (the former military junta), but not by the local Kachin. In 2011, the Kachin were in dispute with the Chinese company Datang over the extremely poor contractual terms of the project. On June 14, 2011, a violent incident around Darpein1 triggered a military offensive by the Tatmadaw, Myanmar’s army. In combination with other reasons, a tenuous 11-year-old cease-fire was broken and the new Kachin war broke out. This civil war displaced as many as 100,000 civilians and left over 1000 people dead [77].

The experience of HP-implementation along the Daying River is similar to that along the main rivers. The fragmentation of ownership involving so many companies results in a merely project-based focus, with companies seeking simply to maximize HP generation (and thus revenues) of each station, while almost totally neglecting a coordinated watershed-wide planning approach (at least of sub-catchments).

4.4. The Role of CDM

One of the major drivers of Yunnan’s recent HP development outside the three large rivers is the Clean Development Mechanism (CDM), which was introduced by the Kyoto Protocol and has developed into one of the most important carbon market instruments. Although the market, due to low prices, does not give any relevant incentives for mitigation anymore, Yunnan has globally (beside Sichuan) the largest number of HP projects in the CDM pipeline. We identified for Yunnan 300 CDM-registered HP projects (∑11.40 GW), as some are bundled projects the actual figure is higher. These are far more HP projects than entire countries such as Vietnam (200; 6.23 GW), India (166; 5.89 GW), or Brazil (94; 11.97 GW), ranked globally as number two to four respectively, have as registered in the CDM pipeline.

Of Yunnan’s three largest rivers, there is only one HP project among them that received CDM support, Mekong’s Gongguoqiao (900 MW). Among Yunnan’s other rivers, however, more than half of the 128 LHP projects are in the CDM pipeline and 54 of them are already registered (7.22 GW). Focusing on the six basins, the largest number of CDM projects is also within the largest basin (Jinsha). However, more importantly, the remote Nu and Ayeyarwady basins, which share only 13.6% of Yunnan’s territory, together hold more than one-third (34.3%) of Yunnan’s HP projects currently in the CDM pipeline. The incentives for CDM are also expressed in the fact, that among all of the 235 HP projects of the two basins built after 2006, 57% applied for CDM. Analyzing the CDM data presents many challenges. In many cases wrong coordinates are given, which frustrates efforts to find true locations for the projects (especially in the border areas). Often the data given in the Project Design Documents does not match the current HP data (MW) of the project. In other cases, the same project might exist under different names in the CDM pipeline.

4.5. Utilization Conflicts and Limitations of the Grid

Yunnan’s fast-paced HP development results, at times, in various disputes or conflicts which must be carefully handled by Chinese authorities. These tensions can be classified into three different groups: environmental issues, socio-economic disputes (mainly due to dislocation), and conflicts about utilization of electricity.

At several places disputes arise over local utilization demand versus export demand. Such disputes may manifest either around individual or cascaded HP projects, or about the utilization in semi-autonomous grids having limited or no connectivity to the YPG. Jin’anqiao on the middle Jinsha cascade, for example, became famous for its continuing power struggle between provincial and national governments about electricity utilization, distribution and grid tariffs. While Jin’anqiao, together with the Mekong’s Xiaowan dam, are feeding the Chuxiong UHVDC converter, the utilization of the other (later) dams remains controversial. Whereas the central government wants to build more UHVDC lines, some local governments are keen to utilize the electricity in Yunnan. This is especially true of the Lijiang government, which wanted to build a huge aluminum smelter close to the Three Parallel Rivers UNESCO World Heritage Site. Beijing disagreed with this idea due to serious environmental constraints. Due to this disagreement, only in 2013 were the HP projects integrated into the 500 kV YPG network. In the interim, e.g., the Ahai dam ran idle for one year, causing a loss of more than 8 TWh. Even after the connection of this and other dams into YPG, especially during the flood season only a small part of the potential electricity generation can be fed into the grid and therefore still a huge loss is incurred by many plants over the rainy season. Currently CSPG is building a UHVDC line to Guangxi (3.2 GW, 500 kV) which should be completed in 2016 (much later than scheduled). Hence, Guangxi gains a higher relevance for Yunnan’s power exports (in 2013 it took in only 3 TWh from Yunnan). Additionally, in 2016 CSPG started work on another huge UHVDC line from Jianchuan/Dali to Shenzhen. From 2017 it will transmit 20 TWh annually to Shenzhen, roughly 25% of the city’s consumption.

Yunnan has an electricity demand similar to neighboring states such as Thailand or Vietnam. This huge demand is not primarily caused by its manufacturing strengths (as is the case, for instance, in Guangdong), but by the huge demand of highly electricity-intensive processing industries. They can be classified into three groups. The first group comprises a relatively small group of mostly centralized plants with large output volumes. They are mainly located near mines or larger HP plants on the Yunnan plateau. Examples are the aluminum industry which consumed in 2013 18.9 TWh, the chemical and fertilizer industry (18.6 TWh) or the zinc smelters. Currently, Yunnan’s western prefectures which have high HP outputs but peripheral location are vying to attract such plants. The second group comprises a large number of plants spread all over the province. Its largest consumer is the cement industry; in 2013, about 100 cement plants consumed 8.9 TWh. The third group comprises a large number of mostly small silicon smelters producing metallurgical-grade silicon. They are primarily concentrated in the remote Ayeyarwady and Nu watersheds with its mainly prefectural grids having only a very limited connectivity to YPG but a huge electricity surplus, especially during the rainy season. In 2013, about 57 producing smelters consumed about 6 TWh (another 13 plants have temporarily stopped production). The development paradigm of those prefectural grids prioritizes local electricity-intensive industries, especially silicon purification. However, this causes serious environmental ramifications such as disposal of toxic by-products and a huge charcoal demand. This latter, of course, is a major driver of Yunnan’s deforestation and the related conversion of forests to forest plantations. In 2013, alone silicon plants within Yunnan’s Ayeyarwady and Nu basins had a charcoal demand of 300,000 t [77].

5. Conclusions

Our paper provides a detailed overview of the status quo of Yunnan’s current HP development. In 2014, Yunnan had an installed HP capacity of 51.3 GW and HP generation of 177 TWh. Even though Yunnan, in terms of GDP, is one of the poorest provinces of China, its installed hydropower capacity rivals that of emerging national economies such as Vietnam, Turkey, and Iran. Our goal here is to bring to light the extent of Yunnan’s HP outside the well-known and well-studied cascades on the Jinsha and Mekong. We identified 128 large hydropower projects (≥50 MW) having a capacity of 16.5 GW, along with another 16.4 GW of other types of power generation already developed or underway, the majority of which have heretofore not been subjected to academic scrutiny.

Utilizing a powershed approach places the focus not only on the individual dams themselves, but also on the sites to which the power from those dams’ flows, be they nearby electricity-intensive industrial sites such as silica and aluminum smelters, or faraway urban and industrial centers in Guangdong. It allows Yunnan’s HP development to be seen as a complex affair involving both private enterprises and state or province actors, serving both local and export needs. Rather than looking simply at drivers, governance, or implementation, we have attempted to examine Yunnan’s HP development in a more holistic way that also comprises the greater context of other generating alternatives. More importantly, we have sought to understand the utilization patterns, both in terms of export demands as well as provincial consumption patterns.

Yunnan’s (hydro-) power export is rapidly growing, but it still accounts for merely one-third of the province’s power generation. While some of that generating capacity is slated to respond to existing or anticipated electricity demand within Yunnan or for the export market, we suspect that a large proportion of it is being developed purely for speculative reasons based on the existence of more-or-less suitable sites and flow volumes, and concern that restrictions on developing new hydropower will only get tighter in the future. We therefore see a need for a critical revision of existing electricity generation and consumption paradigms in China, including dispatch rules, development modes prioritizing energy-intensive industries alongside new HP development, and the extent to which future HP construction and generation will be shaped by local projects versus export obligations. This includes a fundamental reassessment of the value of such indicators of development as “per capita electricity consumption” and “total installed capacity,” indicators whose value decreases as efficiency gains render equivalent energy services from less electricity. Similarly, devoting greater efforts to improving the energy (and hence water-) efficiency of energy-intensive industries, in parallel with diversifying Yunnan’s industrial base, could not only help slow the growth in electricity and water demand, but would also accord well with the energy efficiency goals set in the 13th Five Year Plan promulgated in early 2016.

As we noted in the paper, current transnational basin-wide research is, for the most part, limited to the Mekong. Yet, the approaches developed and lessons drawn need to be applied to Yunnan’s other four transnational basins, including more joint scientific research and information sharing [11,77]. Part of the reason for the relative lack of attention to HP development in basins such as the Ayeyarwaddy is the difficulty in accessing relevant data, no small challenge in rural China, especially in subjects and geographic areas considered politically sensitive [78]. Yet, absence of evidence must not be understood as evidence of absence; as we have shown, the scale of present and expected future HP development, not to mention related energy-intensive industry such as non-ferrous metals smelting, has few precedents. There is a pressing need for a better understanding of HP development in Yunnan’s six river basins, including the smaller projects and more tributaries and sub-catchments, which can have a rather high cumulative generating capacity, not to mention impacts [77]. Similarly, this should include both local consumption patterns of energy intensive industries as well as their environmental and socio-economic implications. Such studies should include both quantitative and qualitative analyses and assessments of downstream impacts of hydropower (dam) development. This will require better coordination (implementation governance) and management of hydropower development in transboundary catchments, and in and around protected areas, along with far greater data transparency than currently exists.

It is also important, given the extent and rapidity of HP development in Yunnan and surrounding areas, that careful reviews of individual large projects be conducted by disinterested parties with expertise in understanding the social, environmental, and geopolitical impacts of HP development. Moreover, the numerous smaller or mid-sized projects in or around sensitive and protected areas need to be carefully reexamined. These projects often have negligible benefit in terms of additional installed capacity (and may be even more marginal in terms of actual output), yet they can bring major environmental degradation. The Chinese central government recently took a first promising step by banning all SHP projects in the Nu basin; it remains to be seen how lasting this ban is, and whether or not it will result in the type of fundamental reassessment we call for here. Our study indicates that if a cascade or a longer river section is developed and owned by the same company, it enables a more coordinated management approach which could potentially mitigate negative environmental impacts for a larger part of the watershed, including some of the tributaries.

Finally, in times of emerging discussions about a global grid and China’s ongoing desire to exploit huge HP reserves in countries neighboring Yunnan (especially Myanmar and Laos), one of the greatest barriers to greater cooperation on infrastructure and other issues in the region is the widely shared distrust of China’s long-term interests [79]. Yet, such distrust could perhaps be somewhat mitigated if the Chinese government and state-backed power and infrastructure companies not only backed power projects across the region, but would also prioritize new transmission projects. From a technological perspective, better interconnectivity between China’s existing grid and the national grids gradually being developed in neighboring countries would help alleviate some of the problems with “spilled” electricity and grid congestion within Yunnan. From a broader socio-cultural perspective, they could also help build trust, ease energy poverty, and pave the way, or rather, light the way, to greater collaboration on infrastructure and communications across southeast and south Asia.

Acknowledgments

Research funding has been provided by MOST (Ministry of Science and Technology of China, project No. 2016YFA0601603), NSFC (Natural Science Foundation of China, project No. U1202232) and by the DFG (German Research Foundation, HE 5951/2-1 and 4-1). Further, Asian International River Center provided support for fieldwork and data collection.

Author Contributions

Thomas Hennig led the research project this study is based on, but all authors undertook certain parts of the fieldwork and contributed to this article. Thomas Hennig coordinated the writing process of this article and was in charge of the cartography. Darrin Magee, besides editing of this paper, especially contributed to the sections Conclusions, Powershed Approach and Yunnan’s electricity demand. Daming He and Wenling Wang contributed in various parts of the sections Results and Discussions and supports data collection.

Conflicts of Interest

The authors declare no conflict of interest.

References and Notes

- To reduce the impact of inter-annual variations, the figure is the mean of three subsequent years (e.g., for 2000 it is the mean of 1999, 2000 and 2001).

- BP. BP Statistical Review of World Energy 2015; BP p.l.c.: London, UK, 2015. [Google Scholar]

- In this paper, electricity exports refer to electricity sent out of a province, regardless of whether the destination is another province in the same country (such as Guangdong, a major load center in southern China), or a different country altogether.

- China Electric Power Yearbook; China Electric Power Press: Beijing, China, 2013/2014.

- Also frequently spelled Irrawaddy.

- Kattelus, M.; Kummu, M.; Keskinen, M.; Salmivaara, A.; Varis, O. China’s southbound transboundary river basins: A case of asymmetry. Water Int. 2015, 40, 113–138. [Google Scholar] [CrossRef]

- Kuenzer, C.I.; Campbell, I.; Roch, M.; Leinenkugel, P.; Tuan, V.; Dech, S. Understanding the impact of hydropower developments in the context of upstream–downstream relations in the Mekong river basin. Sustain. Sci. 2013, 8, 565–584. [Google Scholar] [CrossRef]

- Yunnan Energy Statistical Yearbook; Yunnan Science and Technology Press: Kunming, China, 2012–2014.

- He, D.M.; Chen, L.H. The impact of hydropower cascade development in the Lancang-Mekong Basin, Yunnan. Mekong Update Dialogue 2002, 53, 2–4. [Google Scholar]

- Magee, D. Powershed politics: Yunnan hydropower under great western development. China Q. 2006, 185, 23–41. [Google Scholar] [CrossRef]

- Fan, H.; He, D.M.; Wang, W.L. Environmental consequences of damming the mainstream Lancang-Mekong River: A review. Earth-Sci. Rev. 2015, 16, 77–91. [Google Scholar] [CrossRef]

- Galipeau, B.; Ingman, M.; Tilt, B. Dam-induced displacement and agricultural livelihoods in China’s Mekong basin. Human Ecol. 2013, 41, 437–446. [Google Scholar] [CrossRef]

- Grumbine, R.E.; Dore, J.; Xu, J. Mekong hydropower. Drivers of change and governance challenges. Front. Ecol. Environ. 2012, 10, 91–98. [Google Scholar] [CrossRef]

- Magee, D. The Dragon upstream. China’s Role in the Lancang-Mekong Development. In Politics and Development in a Transboundary Watershed: The Case of the Lower Mekong Basin; Öjendal, J., Hansson, S., Hellberg, S., Eds.; Springer: Berlin, Germany, 2012; pp. 171–193. [Google Scholar]

- Orr, S.; Pittock, J.; Dumaresq, D. Dams on the Mekong River: Lost fish protein and the implications for land and water resources. Glob. Environ. Chang. 2012, 22, 925–932. [Google Scholar] [CrossRef]

- Tullos, D.D.; Foster-Moore, E.; Magge, D.; Tilt, B.; Wolf, A.T.; Gassert, F.; Kibler, K. Biophysical, socioeconomic, and geopolitical vulnerabilities to hydropower development on the Nu River, China. Ecol. Soc. 2013, 18, 260–272. [Google Scholar] [CrossRef]

- Brown, P.H.; Xu, K. Hydropower development and resettlement policy on China’s Nu River. J. Contemp. Chin. 2010, 19, 777–797. [Google Scholar] [CrossRef]

- Feng, Y.; He, D.; Li, Y. Ecological changes and the drivers in the Nu river basin, upper Salween. Water Int. 2010, 35, 786–799. [Google Scholar] [CrossRef]

- Grumbine, R.E. Where the Dragon Meets the Angry River: Nature and Power in China; Island Press: Washington, DC, USA, 2010. [Google Scholar]

- Tang, X.; Zhou, J. A future role for cascade hydropower in the electricity system of China. Energy Policy 2012, 51, 358–363. [Google Scholar] [CrossRef]

- Winemiller, K.O.; McIntyre, P.B.; Castello, L.; Fluet-Chouinard, E.; Giarrizzo, T.; Nam, S.; Baird, I.G.; Darwall, W.; Lujan, N.K.; Harrison, I.; et al. Balancing hydropower and biodiversity in the Amazon, Congo, and Mekong. Science 2016, 351, 128–129. [Google Scholar] [CrossRef] [PubMed]

- Suhardiman, D.; Giordano, M. Legal Plurality: An Analysis of Power Interplay in Mekong Hydropower. Ann. Assoc. Am. Geogr. 2014, 104, 973–988. [Google Scholar] [CrossRef]

- Hecht, J.; Guillaume, L. The effects of hydropower dams on the hydrology of the Mekong Basin. In CGIAR Research Program on Water, Land and Ecosystems (WLE); State of Knowledge Series 5; CGIAR Research Program on Water, Land and Ecosystems (WLE): Vientiane, Lao, 2014. [Google Scholar]

- Pearce-Smith, S. The impact of continued Mekong basin hydropower development on local livelihoods. Cons. J. Sustain. Dev. 2012, 7, 73–86. [Google Scholar] [CrossRef]

- Johnston, R.; Kammu, M. Water resources models in the Mekong basin: A review. Water Resour. Manag. 2012, 26, 429–455. [Google Scholar] [CrossRef]

- Grill, G.; Lehner, B.; Lumsdon, A.E.; MacDonald, G.K.; Zarfl, C.; Liermann, C.R. An index-based framework for assessing patterns and trends in river fragmentation and flow regulation by global dams at multiple scales. Environ. Res. Lett. 2015, 10, 55–60. [Google Scholar] [CrossRef]

- Zarfl, C.; Lumsdon, A.E.; Berlekamp, J.; Tydecks, L.; Tockner, K. A global boom in hydropower dam construction. Aquat. Sci. 2014, 77, 161–170. [Google Scholar] [CrossRef]

- Salmivaraa, A.; Kummu, M.; Keskinnen, M.; Varis, O. Using global datasets to create environmental profiles for data-poor regions: A case from Irrawaddy and Salween river basins. J. Environ. Manag. 2013, 5, 897–911. [Google Scholar] [CrossRef] [PubMed]

- Kattelus, M.; Rahaman, M.M.; Varis, O. Hydropower development in Myanmar and its implications on regional energy cooperation. Int. J. Sustain. Soc. 2015, 7, 42–66. [Google Scholar] [CrossRef]

- Keskinnen, M.; Guillaume, J.H.A.; Kattelus, M.; Porkka, M.; Räsänen, T.A.; Varis, O. The water-energy-food nexus and the transboundary context: Insights from large Asian Rivers. Water 2016, 8, 193. [Google Scholar] [CrossRef]

- Matthews, N.; Motta, S. Chinese state-owned enterprise investment in Mekong hydropower: Political and economic drivers and their implications across the water, energy, food nexus. Water 2015, 7, 6269–6284. [Google Scholar] [CrossRef]

- Middleton, C.; Allouche, J.; Gyawali, D.; Allan, S. The rise and implications of the water-energy-food nexus in Southeast Asia through an environmental justice lens. Water Altern. 2015, 8, 627–654. [Google Scholar]

- Hussey, K.; Pittock, J. The energy-water nexus: Managing the links between energy and water for a sustainable future. Ecol. Soc. 2012, 17, 293–303. [Google Scholar] [CrossRef]

- The database includes the following information: HP name, location, capacity (MW), no. of turbines, annual output (GWh), capacity factor (%], hydraulic head (m), average water flow (m3/s), HP type, dam height (m), storage/reservoir size (m3), grid connectivity (kV), year of commission, present/previous owner, and whether the project was CDM-funded or had applied for CDM funding.

- World Commission on Dams (WCD). Dams and Development: A New Framework for Decision-Making; Earthscan: London, UK, 2010. [Google Scholar]

- Tullos, D.D.; Tilt, B.; Liermann, C.R. Introduction to the special issue: Understanding and linking the biophysical, socioeconomic and geopolitical effects of dams. J. Environ. Manag. 2009, 90, S203–S207. [Google Scholar] [CrossRef] [PubMed]

- Poff, N.L.; Hart, D.D. How dams vary and why it matters for the emerging science of dam removal. Bioscience 2002, 52, 659–668. [Google Scholar] [CrossRef]

- Scudder, T. The Future of Large Dams: Dealing with Social, Environmental, Institutional and Political Costs; Earthscan: Sterling, VA, USA, 2005. [Google Scholar]

- Nilsson, C.; Reidy, C.A.; Dynesius, M.; Revenga, C. Fragmentation and flow regulation of the world’s large river systems. Science 2005, 308, 405–408. [Google Scholar] [CrossRef] [PubMed]

- Morgan, K.B.; Sardelic, D.N.; Waretini, A.F. The Three Gorges Project: How sustainable? J. Hydrol. 2012, 460/461, 1–12. [Google Scholar] [CrossRef]

- Cheng, C.; Liu, B.; Chau, K.W.; Li, G.; Liao, S. China’s small hydropower and its dispatching management. Renew. Sustain. Energy Rev. 2015, 42, 43–55. [Google Scholar] [CrossRef]

- Li, Y.; Li, Y.B.; Ji, P.F.; Yang, Y. The status quo analysis and policy suggestions on promoting China’s hydropower development. Renew. Sustain. Energy Rev. 2015, 51, 1071–1079. [Google Scholar] [CrossRef]

- Liu, J.G.; Zang, C.F.; Tian, S.Y.; Liu, J.G.; Yang, H.; Jia, S.F.; You, L.Z.; Liu, B.; Zhang, M. Water conservancy projects in China: Achievements, challenges and way forward. Global Environ. Chang. 2013, 23, 633–643. [Google Scholar] [CrossRef]

- Magee, D. Dams in East Asia: Controlling water but creating problems. In Routledge Handbook of East Asia and the Environment; Harris, P., Graeme, L., Eds.; Routledge: Oxford, UK, 2014. [Google Scholar]

- Hennig, T. Energy, hydropower and geopolitics: Northeast India and its neighbors. Asien 2015, 134, 121–142. [Google Scholar]

- Choudhuri, N. Towards responsible hydropower development through contentious multi-stakeholder negotiations: The case of India. In Evolution of Dam Policies; Scheunemann, W., Hensengerth, O., Eds.; Springer: Berlin, Germany, 2014; pp. 95–129. [Google Scholar]

- Grumbine, R.E.; Pandit, R.K. Threats from India’s Himalaya dams. Science 2013, 339, 36–37. [Google Scholar] [CrossRef] [PubMed]

- Sharma, N.K.; Tiwari, P.K.; Sood, Y.R. A comprehensive analysis of strategies, policies and development of hydropower in India: Special emphasis on small hydropower. Renew. Sustain. Energy Rev. 2013, 18, 460–470. [Google Scholar] [CrossRef]

- Kankal, M.; Bayram, A.; Uzlu, E.; Satilmiş, U. Assessment of hydropower and multi-dam power projects in Turkey. Renew. Energy 2014, 68, 118–133. [Google Scholar] [CrossRef]

- Melikoglu, M. Hydropower in Turkey: Analysis in the view of Vision 2023. Renew. Sustain. Energy Rev. 2013, 25, 503–510. [Google Scholar] [CrossRef]

- Liermann, C.R.; Nilsson, C.; Robertson, J.; Ng, R.Y. Implications of dam obstruction for global freshwater fish diversity. Bioscience 2012, 62, 539–548. [Google Scholar]

- Hamududu, B.; Killingtveit, A. Assessing climate change impacts on global hydropower. Energies 2012, 5, 305–322. [Google Scholar] [CrossRef]

- Lehner, B.; Liermann, C.R.; Revenga, C.; Vörösmarty, C.; Fekete, B.; Crouzet, P.; Döll, P.; Endejan, M.; Frenken, K.; Magome, J.; et al. High-resolution mapping of the world’s reservoirs and dams for sustainable river-flow management. Front. Ecol. Environ. 2011, 9, 494–502. [Google Scholar] [CrossRef]

- Xu, J.; Wilkes, A. Biodiversity impact analysis in northwest Yunnan, southwest China. Biodivers. Conserv. 2004, 13, 959–983. [Google Scholar] [CrossRef]

- Li, L. Sixty Years of Yunnan Water Resources and Hydropower; Yunnan Water Resources Department: Kunming, China, 2009. (In Chinese) [Google Scholar]