Communicating Sustainability: An Operational Model for Evaluating Corporate Websites

Abstract

:1. Introduction

2. Literature Review

- (1)

- Content related to the core business, which refers to activities that have a strong impact on the area of business and the competitiveness of an organization.

- (2)

- Content that impacts the value chain, i.e., initiatives that have a significant impact on business processes and activities.

- (3)

- Social content of generic interest, not significantly related to the core business of an organization but regarding generic philanthropic initiatives.

3. Research Design

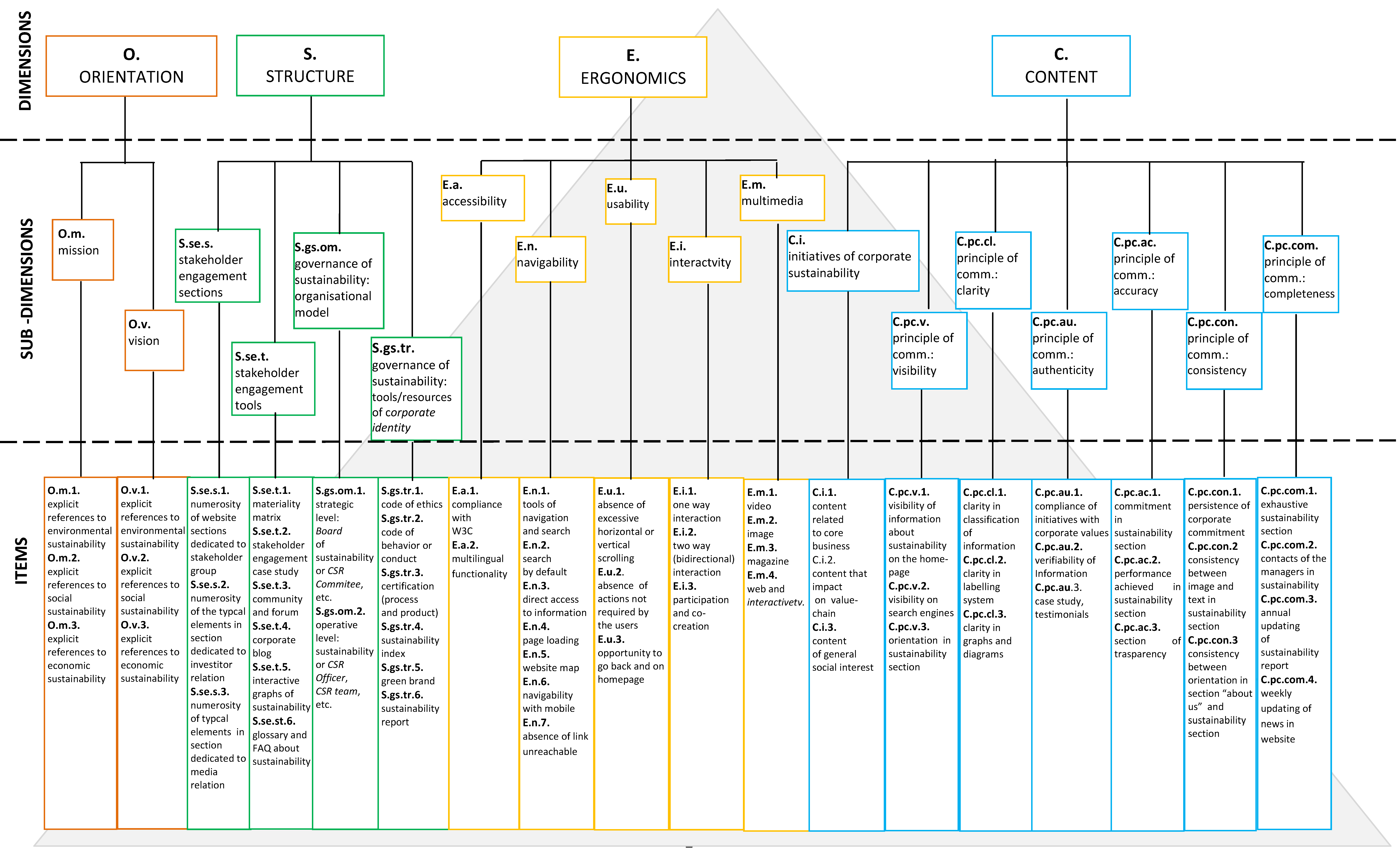

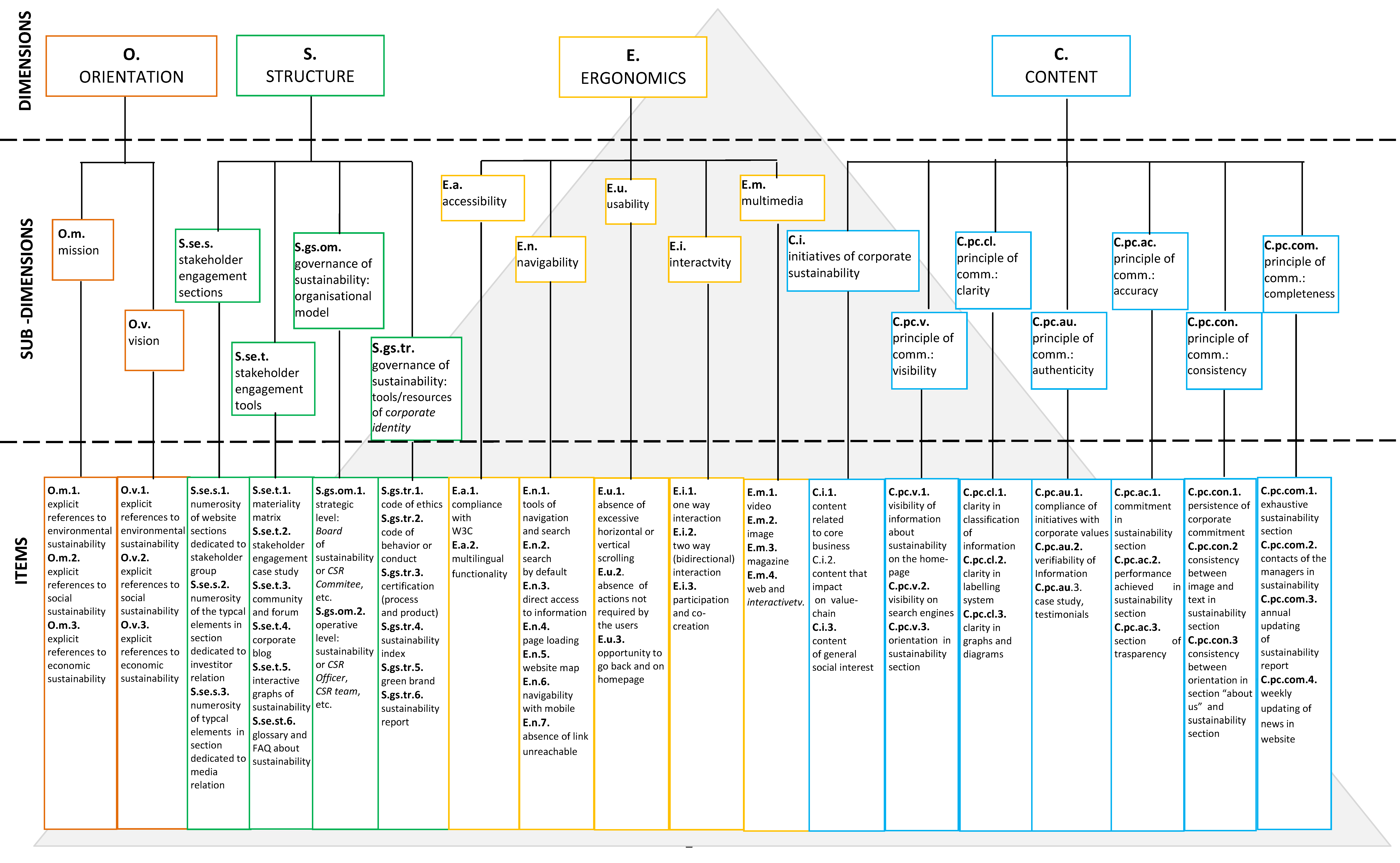

4. The Operational Model: Architecture and Metrics

- (1)

- 4 dimensions

- (2)

- 18 sub-dimensions

- (3)

- 64 items

4.1. Strategic Orientation to Sustainability Expressed on the Corporate Website

4.2. The Structure and the Website Tools

4.3. The Ergonomics of the Website

- (1)

- “Accessibility” refers to the inclusive practice of making websites accessible to all typology of users, including those with disabilities, and concerns the compliance of World Wide Web Consortium (W3C) guidelines.

- (2)

- “Navigability” regards the ease and the quickness with which users find desired information within the website, including the presence of research tools, the organization of content into classification hierarchies, and their fruition by mobile devices.

- (3)

- “Usability” encompasses the effectiveness, efficiency, and satisfaction due to website design and measures the quality of the user experience in achieving specific goals while visiting a website;

- (4)

- “Interactivity” concerns the presence in the website of two-way communication processes and tools addressed to engage users in the process of navigation.

- (5)

- “Multimedia” refers to the simultaneous and integrated use of different media within the website.

4.4. Content on the Website

- (1)

- “Visibility” is the organization’s ability to make visible, traceable, and usable its communication activities for sustainability.

- (2)

- “Clarity” is the organization’s ability to communicate in a clear and understandable manner, avoiding doubts and misunderstandings.

- (3)

- “Authenticity” refers to not only truthful but also verifiable and verified communication, through the support of credible sources.

- (4)

- “Accuracy” is the ability of corporate communication to relate to specific, concrete, and demonstrable aspects, avoiding generic and vague statements.

- (5)

- “Consistency” is the company’s ability to convey content of sustainability in line with its commitments undertaken in the corporate orientation.

- (6)

- “Completeness” refers to the presence on the website of the key elements of sustainability communication to satisfy all of the information needs of stakeholders.

4.5. The Greenwashing Penalties

4.6. Value of the OSEC Scores

- (1)

- s > 80. This score range includes firms that show an excellent compliance to sustainability communication requisites.

- (2)

- 70 < s < 79. This type of result indicates firms that fulfill communication requirements in a satisfactory way.

- (3)

- 60 < s < 69. This range presents firms with an acceptable compliance to communication requisites. Improvement actions are however possible on different dimensions.

- (4)

- 50 < s < 59. Firms in this range show some weaknesses in digital sustainability communication. Several changes are required to avoid reputational risks.

- (5)

- s < 49. In the last range, firms present a poor compliance of communication requirements. A complete revision of digital communication strategies and practices is needed.

5. Pilot Study

6. Implications and Future Research

Author Contributions

Conflicts of Interest

References

- Herrick, C.N.; Pratt, J.L. Communication and the narrative basis of sustainability: Observations from the municipal water sector. Sustainability 2013, 5, 4428–4443. [Google Scholar] [CrossRef]

- Edwards, A.R. The Sustainability Revolution: Potrait of a Paradigm Shift; New Society Publichers: Gabriola Island, BC, Canada, 2005. [Google Scholar]

- Crane, A.; Matten, D. Business Ethics; Oxford University Press: New York, NY, USA, 2007. [Google Scholar]

- Fuchs, C. The implications of new information and communication technologies for sustainability. Environ. Dev. Sustain. 2008, 10, 291–309. [Google Scholar] [CrossRef]

- Du, S.; Bhattacharya, C.B.; Sen, S. Maximizing business returns to Corporate Social Responsibility (CSR): The role of CSR communication. Int. J. Manag. Rev. 2010, 12, 8–19. [Google Scholar] [CrossRef]

- Fieseler, C.; Fleck, M.; Meckel, M. Corporate Social Responsibility in the Blogosphere. J. Bus. Ethics 2010, 91, 599–614. [Google Scholar] [CrossRef]

- Siano, A. (Ed.) Management della Comunicazione per la Sostenibilità; FrancoAngeli: Milano, Italy, 2014.

- Basil, E.; Erlandson, J. Corporate social responsibility website representation: A longitudinal study of internal and external self-presentations. J. Mark. Commun. 2008, 14, 125–137. [Google Scholar] [CrossRef]

- Capriotti, P. Communicating Corporate Social Responsibility through the Internet and Social Media. In The Handbook of Communication and Corporate Social Responsibility; Ihlen, Ø., Bartlett, J.L., May, S., Eds.; Wiley-Blackwell: Oxford, UK, 2011. [Google Scholar]

- Dade, A.; Hassenzahl, D.M. Communicating sustainability: A content analysis of website communications in the United States. Int. J. Sustain. High. Educ. 2013, 14, 254–263. [Google Scholar] [CrossRef]

- Franz-Balsen, A.; Heinrichs, H. Managing sustainability communication on campus: Experiences from Lüneburg. Int. J. Sustain. High. Educ. 2007, 8, 431–445. [Google Scholar]

- Krätzig, S.; Warren-Kretzschmar, B. Using interactive web tools in environmental planning to improve communication about sustainable development. Sustainability 2014, 6, 236–250. [Google Scholar] [CrossRef] [Green Version]

- Newig, J.; Schulz, D.; Fischer, D.; Hetze, K.; Laws, N.; Lüdecke, G.; Rieckmann, M. Communication regarding sustainability: Conceptual perspectives and exploration of societal subsystems. Sustainability 2013, 5, 2976–2990. [Google Scholar] [CrossRef]

- Wanderley, L.S.O.; Lucian, R.; Farache, F.; de Sousa Filho, J.M. CSR information disclosure on the web: A context-based approach analysing the influence of country of origin and industry sector. J. Bus. Ethics 2008, 82, 369–378. [Google Scholar] [CrossRef]

- Parker, C.M.; Zutshi, A.; Fraunholz, B. Online corporate social responsibility communication by Australian SMEs: A framework for website analysis. In Proceedings of the 23rd Bled eConference eTrust: Implications for the Individual, Enterprises and Society, Bled, Slovenia, 20–23 June 2010; pp. 509–523.

- Lundquist. 6th CSR Online Awards 2014—White Paper. Available online: http://www.lundquist.it/6th-csr-online-awards-white-paper?cat_slug=whats-on/white-papers (accessed on 4 June 2016).

- Siano, A.; Piciocchi, P.; Vollero, A.; Della Volpe, M.; Palazzo, M.; Conte, F.; De Luca, D.; Amabile, S. Developing a Framework for Measuring Effectiveness of Sustainability Communications through Corporate Websites. In Procedia Manufacturing—6th International Conference on Applied Human Factors and Ergonomics (AHFE) and the Affiliated Conferences; Ahram, T., Karwowski, W., Schmorrow, D., Eds.; Elsevier: Amsterdam, The Netherlands, 2015; Volume 3, pp. 3615–3620. [Google Scholar]

- S&P Dow Jones Indices; RobecoSAM. Dow Jones Sustainability World Index 2015. Available online: http://www.sustainability-indices.com/ (accessed on 14 April 2016).

- Elkington, J. Towards the sustainable corporation: Win-win-win business strategies for sustainable development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Baumgartner, R.J. Organizational culture and leadership: Preconditions for the development of a sustainable corporation. Sustain. Dev. 2009, 17, 102–113. [Google Scholar] [CrossRef]

- Iasevoli, G.; Massi, M. The relationship between sustainable business management and competitiveness: Research trends and challenge. Int. J. Technol. Manag. 2012, 58, 32–48. [Google Scholar] [CrossRef]

- Savitz, A.; Weber, K. The Triple Bottom Line, How Today’s Best-Run Companies Are Achieving Economic, Social and Environmental Success, and How You Can Too; Jossey Bass: San Francisco, CA, USA, 2006. [Google Scholar]

- Quaddus, M.A.; Siddique, M.A.B. Handbook of Corporate Sustainability: Frameworks, Strategy and Tools; Edward Elgar Publishing: London, UK, 2011. [Google Scholar]

- Siano, A. La comunicazione per la sostenibilità nel management delle imprese. Sinergie Ital. J. Manag. 2012, 89, 3–23. [Google Scholar]

- Schultz, F.; Wehmeier, S. Institutionalization of corporate social responsibility within corporate communications. Combining institutional, sensemaking and communication perspectives. Corp. Commun. Int. J. 2010, 15, 9–29. [Google Scholar] [CrossRef]

- Schoeneborn, D.; Trittin, H. Transcending transmission: Towards a constitutive perspective on CSR communication. Corp. Commun. Int. J. 2013, 18, 193–211. [Google Scholar]

- Gill, D.L.; Dickinson, S.J.; Scharl, A. Communicating sustainability: A web content analysis of North American, Asian and European firms. J. Commun. Manag. 2008, 12, 243–262. [Google Scholar] [CrossRef]

- Moreno, A.; Capriotti, P. Communicating CSR, citizenship and sustainability on the web. J. Commun. Manag. 2009, 13, 157–175. [Google Scholar] [CrossRef]

- Illia, L.; Romenti, S.; Rodríguez Cánovas, B.; Murtarelli, G.; Carroll, C.E. Exploring Corporations’ Dialogue About CSR in the Digital Era. J. Bus. Ethics 2015. [Google Scholar] [CrossRef]

- Rowbottom, N.; Lymer, A. Exploring the use of online corporate sustainability information. Account. Forum 2009, 33, 176–186. [Google Scholar] [CrossRef]

- Gomez, L.; Chalmeta, R. Corporate responsibility in US corporate websites: A pilot study. Public Relat. Rev. 2011, 37, 93–95. [Google Scholar] [CrossRef]

- Sanil, H.S.; Ramakrishnan, S. Communicating the corporate social responsibility on the company website: A study conducted on worldwide responsible accredited production certified apparel manufacturers in India. Int. J. Econ. Financ. Issues 2015, 5, 52–56. [Google Scholar]

- Hunter, T.; Bansal, P. How Standard Is Standardized MNC Global Environmental Communication? J. Bus. Ethics 2007, 71, 135–147. [Google Scholar] [CrossRef]

- Fombrun, C.J.; van Riel, C.B.M. Fame & Fortune. How Successful Companies Build Winning Reputations; Financial Times: Upper Suddle River, NJ, USA, 2004. [Google Scholar]

- Cornelissen, J. Corporate Communication. A Guide to Theory and Practice, 3rd ed.; Sage: London, UK, 2011. [Google Scholar]

- Fombrun, C.J. Corporate reputations as economic assets. In The Blackwell Handbook of Strategic Management; Hitt, M.A., Freeman, R.E., Harrison, J.S., Eds.; Blackwell Publishers: Oxford, UK, 2001. [Google Scholar]

- Gaultier-Gaillard, S.; Louisot, J.P. Risks to reputation: A global approach. Geneva Pap. Risk Insur. Issues Pract. 2006, 31, 425–445. [Google Scholar] [CrossRef]

- Gaudenzi, B.; Confente, I.; Christopher, M. Managing reputational risk: Insights from a European survey. Corp. Reput. Rev. 2015, 8, 248–260. [Google Scholar] [CrossRef]

- Delmas, M.A.; Burbano, V.C. The drivers of greenwashing. Calif. Manag. Rev. 2011, 54, 64–87. [Google Scholar]

- Lyon, T.P.; Montgomery, W. The means and end of greenwash. Organ. Environ. 2015, 28, 223–249. [Google Scholar] [CrossRef]

- Vollero, A. Il rischio greenwashing nella comunicazione per la sostenibilità: Implicazioni manageriali. Sinergie Ital. J. Manag. 2013, 92, 3–23. [Google Scholar]

- Kucuk, S.U.; Krishnamurthy, S. An analysis of consumer power on the Internet. Technovation 2007, 27, 47–56. [Google Scholar] [CrossRef]

- Martin, G.; Farndale, E.; Paauwe, J.; Stiles, P.G. Corporate governance and strategic human resource management: Four archetypes and proposals for a new approach to corporate sustainability. Eur. Manag. J. 2016, 34, 22–35. [Google Scholar] [CrossRef]

- Farné, S. Qualità Sostenibile. Strategie e Strumenti per Creare Valore, Competere Responsabilmente e Ottenere Successo Duraturo; FrancoAngeli: Milano, Italy, 2013. [Google Scholar]

- Fiocca, R.; Sebastiani, R. Marketing, competitività e sviluppo sostenibile. Le evidenze della ricerca SIMktg. Mercati e Competitività 2009, 2, 11–40. [Google Scholar]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The impact of corporate sustainability on organizational processes and performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef]

- Birth, G.; Illia, L.; Lurati, F.; Zamparini, A. Communicating CSR: The practice in the top 300 companies in Switzerland. Corp. Commun. Int. J. 2008, 3, 182–196. [Google Scholar] [CrossRef]

- Manetti, G. Il Triple Bottom Line Reporting: Dal Coinvolgimento Degli Stakeholder Alle Verifiche Esterne; FrancoAngeli: Milano, Italy, 2006. [Google Scholar]

- Marimon, F.; Alonso-Almeida, M.M.; Rodriguez, M.P.; Cortez Alejandro, K.A. The worldwide diffusion of the global reporting initiative: What is the point? J. Clean. Prod. 2012, 33, 132–144. [Google Scholar] [CrossRef]

- Fisher, R.; Oyelere, P.; Laswad, F. Corporate reporting on the Internet: Audit issues and content analysis of practices. Manag. Audit. J. 2004, 19, 412–439. [Google Scholar] [CrossRef]

- Coupland, C. Corporate social and environmental responsibility in web-based reports: Currency in the banking sector? Crit. Perspect. Account. 2006, 17, 865–881. [Google Scholar] [CrossRef]

- Tarquinio, L.; Rossi, A. Customizzazione dei report di sostenibilità e stakeholder engagement. II contributo del World Wide Web. Impresa Progett. Electron. J. Manag. 2014, 1, 1–28. [Google Scholar]

- Fukukawa, K.; Moon, J. A Japanese model of corporate social responsibility. J. Corp. Citizsh. 2004, 16, 45–59. [Google Scholar] [CrossRef]

- Bondy, K.; Matten, D.; Moon, J. The adoption of voluntary codes of conduct in MNCs: A three-country comparative study. Bus. Soc. Rev. 2004, 109, 449–477. [Google Scholar] [CrossRef]

- Castelo Branco, M.; Delgado, C.; Sá, M.; Sousa, C. Comparing CSR communication on corporate web sites in Sweden and Spain. Balt. J. Manag. 2014, 9, 231–250. [Google Scholar] [CrossRef]

- Serra, R. L’etica della certificazione. Etica Econ. 2000, 2, 149–166. [Google Scholar]

- Gallastegui, I.G. The use of eco-labels: A review of the literature. Eur. Environ. 2002, 12, 316–331. [Google Scholar] [CrossRef]

- Amaladoss, M.X.; Manohar, H.L.; Jacob, F. Document communicating corporate governance through websites: A case study from India. Int. J. Bus. Gov. Ethics 2011, 6, 311–339. [Google Scholar] [CrossRef]

- Márquez, A.; Fombrun, C.J. Measuring corporate social responsibility. Corp. Reput. Rev. 2005, 7, 304–308. [Google Scholar] [CrossRef]

- Greenwood, M. Stakeholder engagement: Beyond the myth of corporate responsibility. J. Bus. Ethics 2007, 74, 315–327. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating shared value. How to reinvent capitalism and unleash a wave of innovation and growth. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Ledingham, J.A.; Bruning, S.D. Public Relations as Relationship Management: A Relational Approach to Public Relations; Lawrence Erlbaum Associates, Inc.: Mahwah, NJ, USA, 2000. [Google Scholar]

- Wunsch-Vincent, S.; Vicker, G. Participative Web and User-Created Content; Organisation for Economic Co-operation and Development (OECD): Paris, France, 2007. [Google Scholar]

- Sridhar, S.; Srinivasan, R. Social influence effects in online product ratings. J. Mark. 2012, 76, 70–88. [Google Scholar] [CrossRef]

- Singer, J.B. User-Generated visibility: Secondary gatekeeping in a shared media space. New Media Soc. 2014, 16, 55–73. [Google Scholar] [CrossRef]

- Pires, G.D.; Stanton, J.; Rita, P. The internet, consumer empowerment and marketing strategies. Eur. J. Mark. 2006, 40, 936–949. [Google Scholar]

- Rezabakhsh, B.; Bornemann, D.; Hansen, U.; Schrader, U. Consumer power: A comparison of the old economy and the Internet economy. J. Consum. Policy 2006, 29, 3–36. [Google Scholar] [CrossRef]

- Miles, M.P.; Munilla, L.S.; Darroch, J. The role of strategic conversations with stakeholders in the formation of corporate social responsibility strategy. J. Bus. Ethics 2006, 69, 195–205. [Google Scholar] [CrossRef]

- Eccles, R.G.; Krzus, M.P.; Rogers, J.; Serafeim, G. The need for sector-specific materiality and sustainability reporting standards. J. Appl. Corp. Financ. 2012, 24, 65–71. [Google Scholar] [CrossRef]

- Michelini, L. Strategie Collaborative per Lo Sviluppo Della Corporate Social Responsibility: Caratteristiche e Strumenti di Gestione Delle Alleanze Tra Imprese e Organizzazioni Non Profit; FrancoAngeli: Milano, Italy, 2007. [Google Scholar]

- Menon, S.; Kahn, B.E. Corporate sponsorships of philanthropic activities: When do they impact perception of sponsor brand? J. Consum. Psychol. 2003, 13, 316–327. [Google Scholar] [CrossRef]

- Elving, W.J.L. Scepticism and corporate social responsibility communications: The influence of fit and reputation. J. Mark. Commun. 2013, 19, 277–292. [Google Scholar] [CrossRef]

- Williams, S.M.; Pei, C.H.W. Corporate Social Disclosures by Listed Companies on their Web Sites: An International Comparison. Int. J. Account. 1999, 34, 389–419. [Google Scholar] [CrossRef]

- Campbell, D.; Cornelia Beck, A. Answering allegations: The use of the corporate website for restorative ethical and social disclosure. Bus. Ethics Eur. Rev. 2004, 13, 100–116. [Google Scholar] [CrossRef]

- Tagesson, T.; Blank, V.; Broberg, P.; Collin, S.O. What explains the extent and content of social and environmental disclosures on corporate websites: A study of social and environmental reporting in Swedish listed corporations. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 352–364. [Google Scholar] [CrossRef]

- Siano, A.; Conte, F.; Amabile, S.; Vollero, A.; Piciocchi, P. Valutare e migliorare la comunicazione digitale per la sostenibilità: Un modello operativo per i siti web. In Proceedings of the XXVIII Sinergie Annual Conference: Management in a Digital World. Decisions, Production, Communication, Udine, Italy, 9–10 June 2016.

- Porter, M.E.; Kramer, M.R. Strategy & society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Van Den Bosch, A.L.M.; De Jong, M.D.T.; Elving, W.J.L. How corporate visual identity supports reputation. Corp. Commun. Int. J. 2005, 10, 108–116. [Google Scholar] [CrossRef]

- Testa, F.; Iraldo, F.; Tessitore, S.; Frey, M. Strategies and approaches green advertising: An empirical analysis of the Italian context. Int. J. Environ. Sustain. Dev. 2011, 10, 375–395. [Google Scholar] [CrossRef]

- Ladwein, R. Il web design e l’ergonomia dei siti di commercio elettronico. Micro Macro Mark. 2001, 10, 51–64. [Google Scholar]

- Mich, L.; Franch, M.; Gaio, L. Evaluating and designing web site quality. Multi Media IEEE 2003, 10, 34–43. [Google Scholar] [CrossRef]

- Chevalier, A.; Kicka, M. Web designers and web users: Influence of the ergonomic quality of the web site on the information search. Int. J. Hum. Comput. Stud. 2006, 64, 1031–1048. [Google Scholar] [CrossRef]

- Reputation Institute. Global CSR RepTrak 2015. Available online: https://www.reputationinstitute.com/CMSPages/GetAzureFile.aspx?path=~%5Cmedia%5Cmedia%5Cdocuments%5C2015-global-csr-reptrak-results.pdf&hash=f375854351576541ae88db1e043e7417e9f057f83955bb3768454dd8e0417353&ext=.pdf (accessed on 23 June 2016).

- Brusa, G. La Percezione del Valore; Maggioli: Milano, Italy, 2008. [Google Scholar]

- Adams, C.A.; Frost, G.R. Accessibility and functionality of the corporate web site: Implications for sustainability reporting. Bus. Strategy Environ. 2006, 15, 275–287. [Google Scholar] [CrossRef]

- Terra Choice. The Sins of Greenwashing: Home and Family Edition; TerraChoice Group, Inc.: Ottawa, ON, Canada, 2010. [Google Scholar]

- Kuo, L.; Yeh, C.-C.; Yu, H.-C. Disclosure of corporate social responsibility and environmental management: Evidence from China. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 273–287. [Google Scholar] [CrossRef]

- GRI. Sustainability Topics for Sectors: What Do Stakeholders Want to Know? 2013. Available online: https://www.globalreporting.org/resourcelibrary/sustainability-topics.pdf (accessed on 27 July 2016).

- López, M.V.; Garcia, A.; Rodriguez, L. Sustainable development and corporate performance: A study based on the Dow Jones sustainability index. J. Bus. Ethics 2007, 75, 285–300. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones Sustainability Index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Beloe, S.; Scherer, J.; Knoepfel, I. Values for Money: Reviewing the Quality of SRI Research; SustainAbility: London, UK, 2004. [Google Scholar]

- Sadowski, M.; Whitaker, K.; Ayars, A. Rate the Raters: Phase Three e Uncovering Best Practices; SustainAbility: London, UK, 2011. [Google Scholar]

- Fowler, S.J.; Hope, C. A critical review of sustainable business indices and their impact. J. Bus. Ethics 2007, 76, 243–252. [Google Scholar] [CrossRef]

- Marradi, A. L'Analisi Monovariata; FrancoAngeli: Milano, Italy, 1998. [Google Scholar]

- Reilly, A.H.; Hynan, K.A. Corporate communication, sustainability, and social media: It’s not easy (really) being green. Bus. Horiz. 2014, 57, 747–758. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Description of Sins | Signals |

|---|---|

| 1. Sin of No Proof Statements about sustainability, without adequate support of credible sources. | Cross-checking the items related to orientation and the items that detect the principle of authenticity. |

| 2. Sin of Irrelevance Statements that divert attention on topics with a low impact in terms of sustainability. | Cross-checking the items related to orientation and the items of content related to the core business or value chain impact. |

| 3. Sin of Vagueness Statements about sustainability based on vague or inaccurate information. | Cross-checking the items related to orientation and the items that detect the principle of accuracy. |

| 4. Unidirectional Approach to Stakeholder Statement about sustainability, without the support of stakeholder engagement tools. | Cross-checking the items related to orientation in the sustainability section and the absence of items related to stakeholder engagement tools. |

| 5. Sin of Worshiping False Labels The presence of sustainability labels (e.g., green brand) not based on a recognized labeling system or certifications. | Cross-checking the item related to the presence of a green brand and the items related to the verifiability of the information (authenticity) and the labeling system (clarity). |

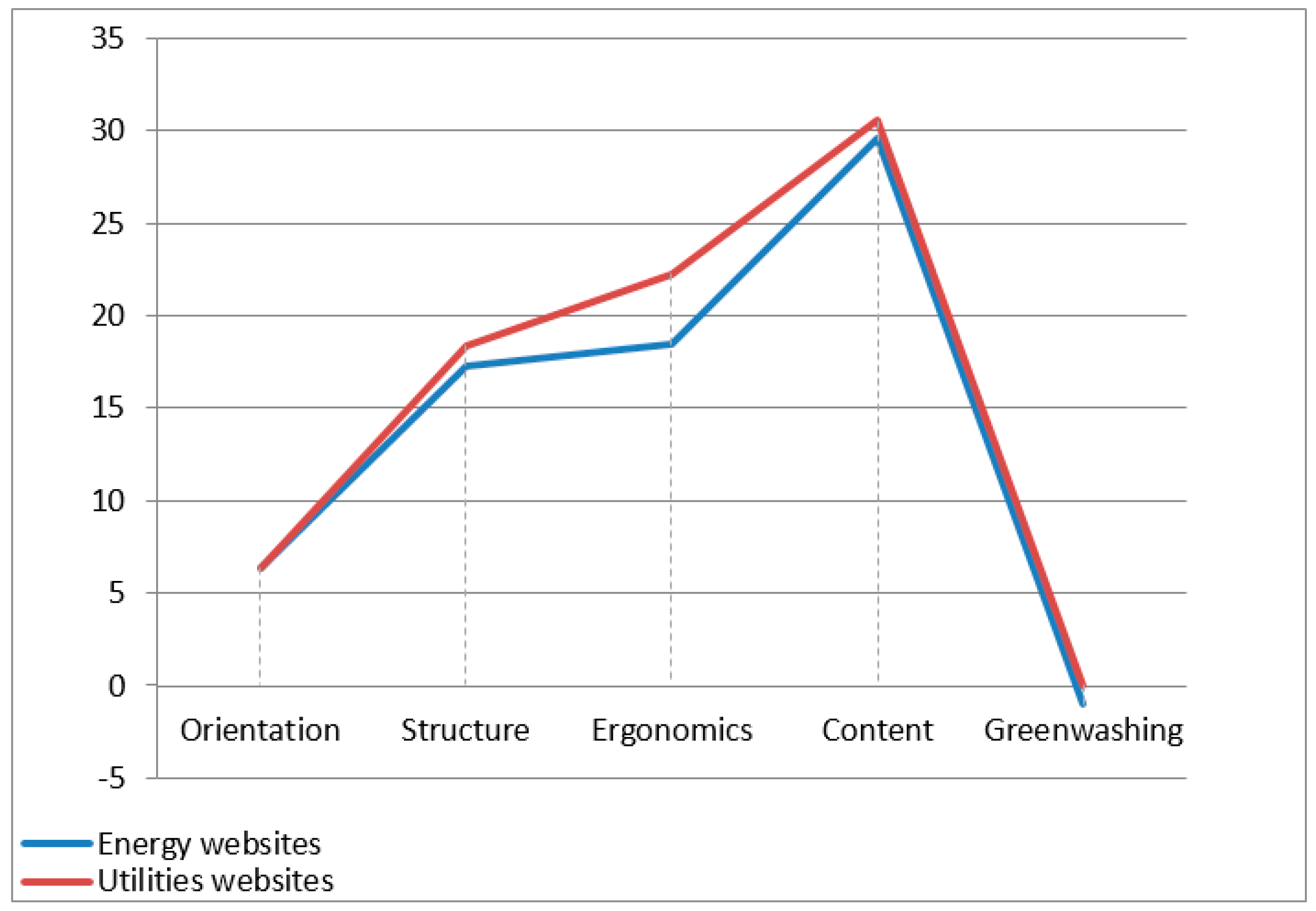

| Energy and Utilities Companies | Dimensions | Green-Washing | Total Score | |||

|---|---|---|---|---|---|---|

| Orientation (0–9.37) | Structure (0–26.56) | Ergonomics (0–29.69) | Content (0–34.37) | |||

| Iberdrola | 9.37 | 23.91 | 26.51 | 30.08 | 89.87 | |

| Eni | 9.37 | 19.93 | 23.26 | 34.37 | 86.93 | |

| United Utilities Group PLC | 9.37 | 20.15 | 23.89 | 32.70 | 86.11 | |

| Repsol SA | 9.37 | 21.69 | 20.93 | 32.70 | 84.69 | |

| Terna | 4.69 | 22.14 | 21.56 | 34.37 | 82.76 | |

| Snam SPA | 4.69 | 22.36 | 22.90 | 32.70 | 82.65 | |

| Acciona SA | 9.37 | 18.16 | 23.89 | 30.79 | 82.21 | |

| Red Eletrica Corp | 6.25 | 15.05 | 26.51 | 33.66 | 81.47 | |

| Cia Energetica De Minas | 9.37 | 17.49 | 23.68 | 30.32 | 80.86 | |

| Enagas SA | 6.25 | 19.92 | 21.92 | 32.70 | 80.79 | |

| Galp Energia SGPS | 6.25 | 16.38 | 25.37 | 31.99 | 79.99 | |

| Total SA | 9.37 | 20.14 | 20.08 | 29.84 | 79.43 | |

| Technip SA | 7.81 | 17.93 | 22.41 | 29.12 | 77.27 | |

| CGG SA | 6.25 | 20.36 | 18.45 | 31.99 | 77.05 | |

| Engie | 4.69 | 17.71 | 22.76 | 30.55 | 75.71 | |

| Ptt PLC | 9.37 | 18.15 | 14.91 | 32.95 | 75.38 | |

| EDP Energias De Portugal SA | 6.25 | 19.70 | 19.22 | 30.08 | 75.25 | |

| Trans Canada Corp | 4.69 | 17.71 | 22.05 | 30.79 | 75.24 | |

| Santos LTD | 7.81 | 20.36 | 15.34 | 30.32 | 73.83 | |

| Woodside Petroleum LTD | 6.25 | 18.59 | 20.57 | 28.41 | 73.82 | |

| Gas Natural SDG | 7.81 | 13.72 | 22.19 | 30.09 | 73.81 | |

| Endesa SA | 3.12 | 14.17 | 24.53 | 31.75 | 73.57 | |

| Exxaro Resources | 4.69 | 21.69 | 23.54 | 23.63 | 73.55 | |

| Enel | 3.12 | 16.38 | 20.08 | 30.32 | 69.90 | |

| Baker Hughes Inc. | 9.37 | 15.05 | 17.75 | 27.69 | 69.86 | |

| Ptt Exploration and Production | 6.25 | 19.70 | 13.57 | 30.08 | 69.60 | |

| Bg Group PLC | 4.69 | 15.72 | 19.79 | 28.64 | 68.84 | |

| Cenovus Energy | 4.69 | 16.38 | 15.97 | 30.08 | 67.12 | |

| Sembra Energy Corp | 4.69 | 15.93 | 15.13 | 31.03 | 66.78 | |

| Ecopetrol | 6.25 | 15.94 | 14.14 | 30.31 | 66.64 | |

| Enbridge | 7.81 | 17.93 | 12.58 | 28.17 | 66.49 | |

| Neste | 3.12 | 15.05 | 16.40 | 30.32 | 64.89 | |

| Halliburton Co. | 4.69 | 13.95 | 19.93 | 26.02 | 64.59 | |

| Suez Environment | 6.25 | 19.04 | 18.73 | 18.62 | 62.64 | |

| Spectra Energy Corp | 0 | 14.39 | 15.13 | 30.79 | 60.31 | |

| SBM Offshore NV | 9.37 | 13.72 | 16.61 | 29.37 | –10.94 | 58.13 |

| S-Oil Corp | 1.56 | 10.19 | 18.73 | 23.15 | –10.94 | 42.69 |

| Energy and Utilities Companies | Dimensions | Green-Washing | Total Score | ||||

|---|---|---|---|---|---|---|---|

| Orientation (0–9.37) | Structure (0–26.56) | Ergonomics (0–29.69) | Content (0–34.37) | ||||

| Positional values | Maximum (Iberdrola) | 9.37 | 23.91 | 26.51 | 30.08 | 89.87 | |

| Minimum (S-Oil Corp) | 1.56 | 10.19 | 18.73 | 23.15 | –10.94 | 42.69 | |

| Median | 6.25 | 17.93 | 20.08 | 30.32 | 73.83 | ||

| Synthetic values | Mean | 6.33 | 17.75 | 20.00 | 30.01 | 73.53 | |

| Std dev | 2.47 | 2.98 | 3.84 | 3.12 | 9.34 | ||

| CV | 0.39 | 0.17 | 0.19 | 0.10 | 0.13 | ||

| Energy | Dimensions | G. | SC. | Utilities | Dimensions | G. | SC. | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| O. | S. | E. | C. | O. | S. | E. | C. | |||||||

| Positional values | Max. Eni | 9.37 | 19.93 | 23.26 | 34.37 | 86.93 | Max. Iberdrola | 9.37 | 23.91 | 26.51 | 30.08 | 89.87 | ||

| Min. S-Oil | 1.56 | 10.19 | 18.73 | 23.15 | –10.94 | 42.69 | Min. Suez En. | 6.25 | 19.04 | 18.73 | 18.62 | 62.64 | ||

| Median | 6.25 | 17.82 | 18.45 | 30.08 | 71.70 | Median | 6.25 | 18.15 | 22.76 | 30.79 | 80.79 | |||

| Synthetic values | Mean | 6.32 | 17.31 | 18.40 | 29.58 | 70.74 | Mean | 6.35 | 18.39 | 22.23 | 30.65 | 77.62 | ||

| Std dev | 2.66 | 2.93 | 3.61 | 2.74 | 9.63 | Std dev | 2.24 | 3.05 | 3.01 | 3.61 | 7.42 | |||

| CV | 0.42 | 0.17 | 0.20 | 0.09 | 0.14 | CV | 0.35 | 0.16 | 0.13 | 0.12 | 0.09 | |||

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Siano, A.; Conte, F.; Amabile, S.; Vollero, A.; Piciocchi, P. Communicating Sustainability: An Operational Model for Evaluating Corporate Websites. Sustainability 2016, 8, 950. https://doi.org/10.3390/su8090950

Siano A, Conte F, Amabile S, Vollero A, Piciocchi P. Communicating Sustainability: An Operational Model for Evaluating Corporate Websites. Sustainability. 2016; 8(9):950. https://doi.org/10.3390/su8090950

Chicago/Turabian StyleSiano, Alfonso, Francesca Conte, Sara Amabile, Agostino Vollero, and Paolo Piciocchi. 2016. "Communicating Sustainability: An Operational Model for Evaluating Corporate Websites" Sustainability 8, no. 9: 950. https://doi.org/10.3390/su8090950

APA StyleSiano, A., Conte, F., Amabile, S., Vollero, A., & Piciocchi, P. (2016). Communicating Sustainability: An Operational Model for Evaluating Corporate Websites. Sustainability, 8(9), 950. https://doi.org/10.3390/su8090950