Sustainable Innovation, Management Accounting and Control Systems, and International Performance

Abstract

:1. Introduction

2. Literature Review

2.1. Sustainable Innovation and Organizational Performance

2.2. MACS as Guide for Enhancing the Success of Innovations

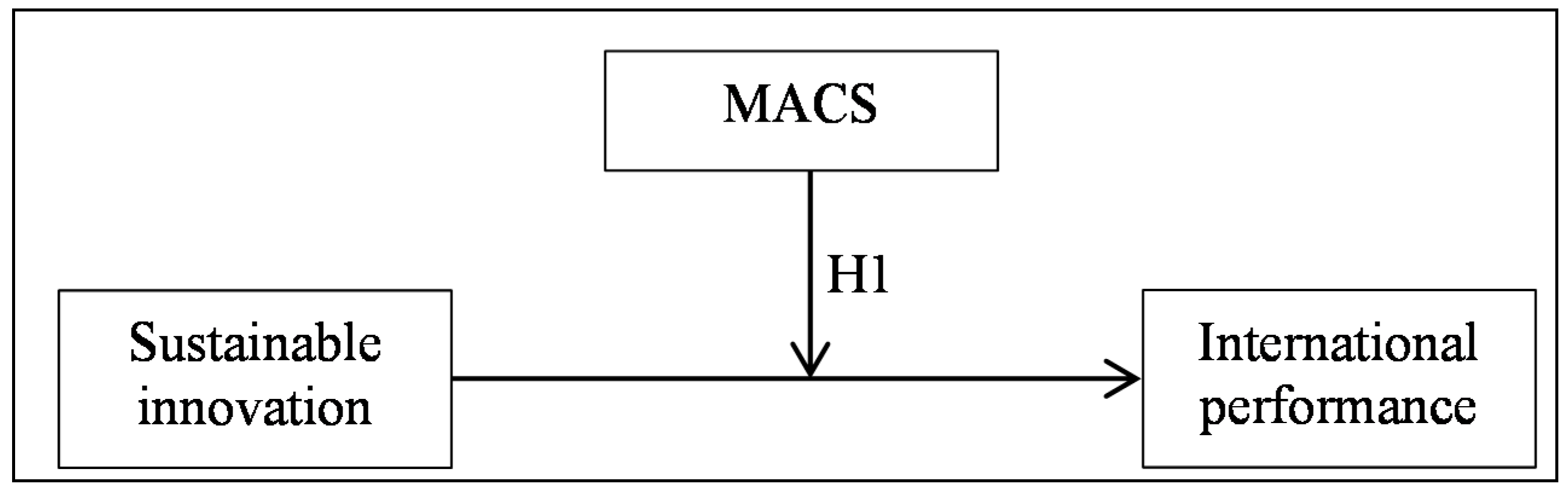

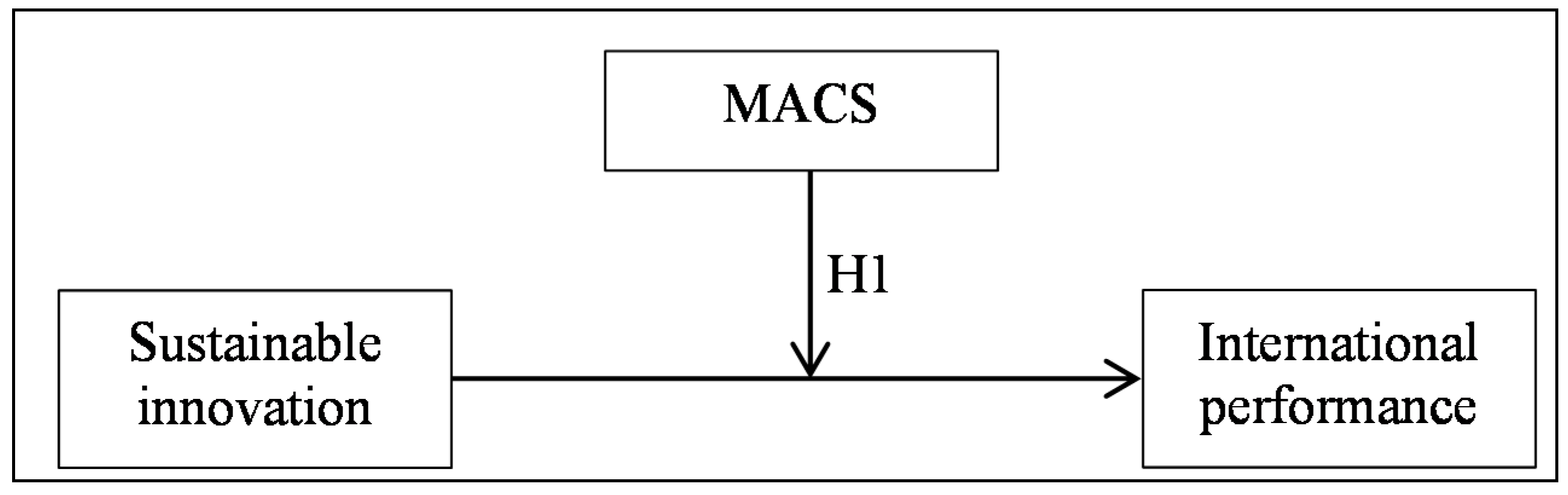

3. Hypothesis Development

4. Methodology and Measurement

4.1. Study Design

{kind=link}

| Number | % | |

|---|---|---|

| Size (Number of Employees) | ||

| <10 | 35 | 28.45 |

| 10–49 | 42 | 34.15 |

| 50–199 | 32 | 26.02 |

| 200–499 | 11 | 8.94 |

| >500 | 3 | 2.44 |

| Age (years) | ||

| <10 | 37 | 30.08 |

| 10–25 | 42 | 34.15 |

| 26–50 | 24 | 19.51 |

| >50 | 20 | 16.26 |

4.2. Variables Measurement

| Construct | Mean | Standard Deviation |

|---|---|---|

| Sustainable innovation | 2.47 | 0.87 |

| Traditional MACS | 3.57 | 1.10 |

| Contemporary MACS | 2.45 | 1.04 |

| Internationalization | 2.64 | 1.28 |

5. Empirical Results

5.1. Measurement Model: Assessing Psychometric Properties

| Standardized Loadings | Composite Reliability | Average Variance Extracted | Cronbach Alpha | |

|---|---|---|---|---|

| Sustainable innovation | 0.685 | 0.510 | 0.690 | |

| SI1. Eco-efficient and biodegradable materials | 0.674 | |||

| SI2. Reclamation of subproducts and waste | 0.859 | |||

| SI3. Local biological resources | 0.565 | |||

| SI4. New equipment | 0.598 | |||

| Traditional MACS | 0.857 | 0.752 | 0.707 | |

| TMACS1. Cost accounting | 0.766 | |||

| TMACS2. Budget system | 0.957 | |||

| Contemporary MACS | 0.840 | 0.724 | 0.618 | |

| CMACS1. Balanced Scorecard | 0.854 | |||

| CMACS2. Benchmarking | 0.847 |

| Sustainable Innovation | Traditional MACS | Contemporary MACS | Internationalization | |

|---|---|---|---|---|

| Sustainable innovation | 0.628 | - | - | - |

| Traditional MACS | 0.395 *** | 0.867 | - | - |

| Contemporary MACS | 0.382 *** | 0.469 *** | 0.851 | - |

| Internationalization | 0.285 *** | 0.346 *** | 0.329 *** | N/A |

5.2. Structural Model

| Paths | Traditional MACS | ||

|---|---|---|---|

| Stage I | Stage II | Stage III | |

| Sustainable innovation → Internationalization | 0.285 * | 0.190 * | 0.164 |

| Traditional MACS → Internationalization | 0.278 *** | 0.273 *** | |

| Sustainable innovation x Traditional MACS → Internationalization | 0.127 | ||

| R2 adjusted | 0.101 | 0.168 | 0.189 |

| Paths | Contemporary MACS | ||

|---|---|---|---|

| Stage I | Stage II | Stage III | |

| Sustainable innovation → Internationalization | 0.285 * | 0.203 * | 0.188 * |

| Contemporary MACS → Internationalization | 0.252 *** | 0.205 ** | |

| Sustainable innovation x Contemporary MACS → Internationalization | 0.193 ** | ||

| R2 adjusted | 0.101 | 0.170 | 0.199 |

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Kobayashi, H.; Kato, M.; Maezawa, Y.; Sano, K. An R&D management framework for eco-technology. Sustainability 2011, 3, 1282–1301. [Google Scholar] [CrossRef]

- Sánchez-Medina, P.S.; Corbett, J.; Toledo-López, A. Environmental innovation and sustainability in small handicraft businesses in Mexico. Sustainability 2011, 3, 984–1002. [Google Scholar] [CrossRef]

- OECD. Eco-Innovation in Industry: Enabling Green Growth; OECD Publishing: Paris, France, 2010. [Google Scholar]

- OECD. Better Policies to Support Eco-Innovation; OECD Publishing: Paris, France, 2011. [Google Scholar]

- Fritz, M.; Schiefer, G. Food chain management for sustainable food system development: A European research agenda. Agribusiness 2008, 24, 440–452. [Google Scholar] [CrossRef]

- Wagner, M. Links Between sustainability-related innovation and sustainability management. Available online: http://sfb649.wiwi.huberlin.de/papers/pdf/SFB649DP2008-046.pdf (accessed on 12 December 2014).

- Boons, F.; Montalvo, C.; Quist, J.; Wagner, M. Sustainable innovation, business models and economic performance: An overview. J. Clean. Prod. 2013, 45, 1–8. [Google Scholar] [CrossRef]

- Ada, E.; Kazancoglu, Y.; Sagnak, M. Improving competitiveness of small- and medium-sized enterprises (smes) in agriproduct export business through ANP: The Turkey case. Agribusiness 2013, 29, 524–537. [Google Scholar]

- Moon, J.; Gond, J.-P.; Grubnic, S.; Herzig, C. Management Control for Sustainability Strategy; CIMA Research Executive Summary Series 7; Chartered Institute of Management Accountants: London, UK, 2011. [Google Scholar]

- Ansuategi, A.; Escapa, M.; Galarraga, I.; González-Eguino, M. Impacto económico de la eco-innovación en Euskadi. Una aproximación cuantitativa. Ekonomiaz 2014, 86, 246–273. [Google Scholar]

- Chenhall, R. Accounting for the horizontal organization: A review essay. Acc. Org. Soc. 2008, 33, 517–550. [Google Scholar] [CrossRef]

- Bisbe, J.; Malagueño, R. The choice of interactive control systems under different innovation management modes. Eur. Acc. Rev. 2009, 18, 371–405. [Google Scholar] [CrossRef] [Green Version]

- Chenhall, R.; Langfield-Smith, K. Adoption and benefits of Management Accounting practices: An Australian study. Manag. Acc. Res. 1998, 9, 1–19. [Google Scholar] [CrossRef]

- Maletič, M.; Maletič, D.; Dahlgaard, J.J.; Dahlgaard-Park, S.M.; Gomišček, B. Sustainability exploration and sustainability exploitation: From a literature review towards a conceptual framework. J. Clean. Prod. 2014, 79, 182–194. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Hull, C.E.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strat. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Dunk, A.S. Product innovation, budgetary control, and the financial performance of firms. Br. Acc. Rev. 2011, 43, 102–111. [Google Scholar] [CrossRef]

- Bisbe, J.; Otley, D.T. The effects of the interactive use of management control systems on product innovation. Acc. Org. Soc. 2004, 29, 709–737. [Google Scholar] [CrossRef]

- Lopez-Valeiras, E.; Gonzalez-Sanchez, B.; Gomez-Conde, J. The effects of the interactive use of management control systems on process and organizational innovation. Rev. Manag. Sci. 2015. [Google Scholar] [CrossRef]

- Schaltegger, S.; Beckmann, M.; Hansen, E.G. Transdisciplinarity in corporate sustainability: Mapping the field. Bus. Strateg. Environ. 2013, 22, 219–229. [Google Scholar] [CrossRef]

- Porter, M.; van der Linde, C. Toward a new conception of the environment- competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Konar, S.; Cohen, M. Does the market value environmental performance? Rev. Econ. Stat. 2001, 83, 281–289. [Google Scholar] [CrossRef]

- Battaglia, M.; Testa, F.; Bianchi, L.; Iraldo, F.; Frey, M. Corporate social responsibility and competitiveness within SMEs of the fashion industry: Evidence from Italy and France. Sustainability 2014, 2, 872–893. [Google Scholar]

- Wagner, M. The role of corporate sustainability performance for economic performance: A firm-level analysis of moderation effects. Ecol. Econ. 2010, 69, 1553–1560. [Google Scholar] [CrossRef]

- Christmann, P. Effects of ‘‘best practices’’ of environmental management on cost advantage: The role of complementary assets. Acad. Manag. J. 2000, 43, 663–680. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Strategy; Free Press: New York, NY, USA, 1980. [Google Scholar]

- Patel, P.C.; Fernhaber, S.; Mcdougall-Covin, P.-P.; van der have, R.P. Beating competitors to international markets: The value of geographically balanced networks for innovation. Strat. Manag. J. 2014, 35, 691–711. [Google Scholar] [CrossRef]

- OECD. Top Barriers and Drivers to SME Internationalization; OECD Publishing: Paris, France, 2009. [Google Scholar]

- Frondel, M.; Horbach, J.; Rennings, K. End-of-pipe or cleaner production? An empirical comparison of environmental innovation decisions across OECD countries. Bus. Strat. Environ. 2007, 16, 571–584. [Google Scholar] [CrossRef]

- Hollensen, S. Essentials of Global Marketing; Pearson Education: Harlow, UK, 2008. [Google Scholar]

- Anthony, R. Planning and Control Systems: A Framework for Analysis; Harvard Business School Press: Boston, MA, USA, 1965. [Google Scholar]

- Goold, M.; Quinn, J.J. The paradox of strategic controls. Strat. Manag. J. 1990, 11, 43–57. [Google Scholar] [CrossRef]

- Simons, R. Levers of Control: How Managers Use Innovative Control Systems to Drive Strategic Renewal; Harvard Business School Press: Boston, MA, USA, 1995. [Google Scholar]

- Henri, J. Management control systems and strategy: A resource-based perspective. Acc. Org. Soc. 2006, 31, 529–558. [Google Scholar] [CrossRef]

- Langevin, P.; Mendoza, C. How can management control system fairness reduce managers’ unethical behaviours? Eur. Manag. J. 2013, 31, 209–222. [Google Scholar] [CrossRef]

- Mahama, H. Management control systems, cooperation and performance in strategic supply relationships: A survey in the mines. Manag. Acc. Res. 2006, 17, 315–339. [Google Scholar] [CrossRef]

- Cadez, S.; Guilding, C. An exploratory investigation of an integrated contingency model of strategic management accounting. Acc Org. Soc. 2008, 33, 836–863. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard. Translating Strategy into Action; McGraw-Hill: Boston, MA, USA, 1996. [Google Scholar]

- Wong-On-Wing, B.; Guo, L.; Li, W.; Yang, D. Reducing conflict in balanced scorecard evaluations. Acc. Org. Soc. 2007, 32, 363–377. [Google Scholar] [CrossRef]

- Ansari, S.L. Towards an open systems approach to budgeting. Acc. Org. Soc. 1979, 4, 149–161. [Google Scholar] [CrossRef]

- Calantone, R.J.; Vickery, S.K.; Droger, C. Business performance and strategic new product development activities: An empirical investigation. J. Prod. Innovat. Manag. 1995, 12, 214–223. [Google Scholar] [CrossRef]

- Schrerer, F.M. Industrial Market Structure and Economic Performance; Houghton Miflin: Boston, MA, USA, 1990. [Google Scholar]

- Kafouros, M.I.; Buckley, P.J.; Sharp, J.A.; Wang, C. The role of internationalization in explaining innovation performance. Technovation 2008, 28, 63–74. [Google Scholar] [CrossRef]

- Rosenbusch, N.; Brinckmann, J.; Bausch, A. Is innovation always beneficial? A meta-analysis of the relationship between innovation and performance in SMEs. J. Bus. Ventur. 2011, 26, 441–457. [Google Scholar] [CrossRef] [Green Version]

- Story, V.; O’Malley, L.; Hart, S. Roles, role performance, and radical innovation competences. Ind. Market. Manag. 2011, 40, 952–966. [Google Scholar] [CrossRef]

- Rajesh, S.; Anju, S. Can quality-oriented firms develop innovative new products? J. Prod. Innovat. Manag. 2009, 26, 206–221. [Google Scholar] [CrossRef]

- Kotabe, M.; Srinivasan, S.S.; Aulakh, P.S. Multinationality and firm performance: The moderating role of R&D and marketing capabilities. J. Int. Bus. Stud. 2002, 33, 79–97. [Google Scholar] [CrossRef]

- Clark, G.; Kosoris, J.; Hong, L.N.; Crul, M. Design for Sustainability: Current Trends in Sustainable Product Design and Development. Sustainability 2009, 1, 409–424. [Google Scholar] [CrossRef]

- Pondeville, S.; Swaen, V.; de Rongé, Y. Environmental management control systems: The role of contextual and strategic factors. Manag. Acc. Res. 2013, 24, 317–332. [Google Scholar] [CrossRef]

- Van Hoof, G.; Weisbrod, A.; Kruse, B. Assessment of Progressive Product Innovation on Key Environmental Indicators: Pampers® Baby Wipes from 2007–2013. Sustainability 2014, 6, 5129–5142. [Google Scholar] [CrossRef]

- Narver, J.C.; Slater, S.; MacLachian, D.L. Responsive and proactive market orientation and new-product success. J. Prod. Innovat. Manag. 2004, 21, 334–347. [Google Scholar] [CrossRef]

- Cooper, D.J.; Ezzamel, M. Globalization discourses and performance measurement systems in a multinational firm. Acc. Org. Soc. 2013, 38, 288–313. [Google Scholar] [CrossRef]

- Shamma, H.; Hassan, S. Customer-driven benchmarking: A strategic approach toward a sustainable marketing performance. Benchmarking 2013, 20, 377–395. [Google Scholar] [CrossRef]

- Gerpott, T.J.; Jakopin, N.M. The degree of internationalization and the financial performance of European mobile network operators. Telecommun. Policy 2005, 29, 635–661. [Google Scholar] [CrossRef]

- Lu, J.W.; Beamish, P.W. The internationalization and performance of SMEs. Strat. Manag. J. 2001, 22, 565–586. [Google Scholar] [CrossRef]

- Chin, W.W. The Partial Least Squares Approach for Structural Equation Modeling. In Modern Methods for Business Research; Marcoulides, G.A., Ed.; Lawrence Erlbaum Associates: London, UK, 1998; pp. 295–236. [Google Scholar]

- Hulland, J. Use of partial least squares (PLS) in strategic management research: A review of four recent studies. Strat. Manag. J. 1999, 20, 195–204. [Google Scholar] [CrossRef]

- Chin, W.W.; Marcolin, B.L.; Newsted, P.R. A partial least squares latent variable modeling approach for measuring interaction effects: Results from a Monte Carlo simulation study and voice mail emotion/adoption study. Inf. Syst. Res. 2003, 14, 189–217. [Google Scholar] [CrossRef]

- Davila, A.; Foster, G.; Oyon, D. Accounting and control, entrepreneurship and innovation: Venturing into new research opportunities. Eur. Acc. Rev. 2009, 18, 281–311. [Google Scholar] [CrossRef]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lopez-Valeiras, E.; Gomez-Conde, J.; Naranjo-Gil, D. Sustainable Innovation, Management Accounting and Control Systems, and International Performance. Sustainability 2015, 7, 3479-3492. https://doi.org/10.3390/su7033479

Lopez-Valeiras E, Gomez-Conde J, Naranjo-Gil D. Sustainable Innovation, Management Accounting and Control Systems, and International Performance. Sustainability. 2015; 7(3):3479-3492. https://doi.org/10.3390/su7033479

Chicago/Turabian StyleLopez-Valeiras, Ernesto, Jacobo Gomez-Conde, and David Naranjo-Gil. 2015. "Sustainable Innovation, Management Accounting and Control Systems, and International Performance" Sustainability 7, no. 3: 3479-3492. https://doi.org/10.3390/su7033479

APA StyleLopez-Valeiras, E., Gomez-Conde, J., & Naranjo-Gil, D. (2015). Sustainable Innovation, Management Accounting and Control Systems, and International Performance. Sustainability, 7(3), 3479-3492. https://doi.org/10.3390/su7033479