Investigation of Barriers and Factors Affecting the Reverse Logistics of Waste Management Practice: A Case Study in Thailand

Abstract

:1. Introduction

2. Review of the Literature

3. Research Concept and Methodology

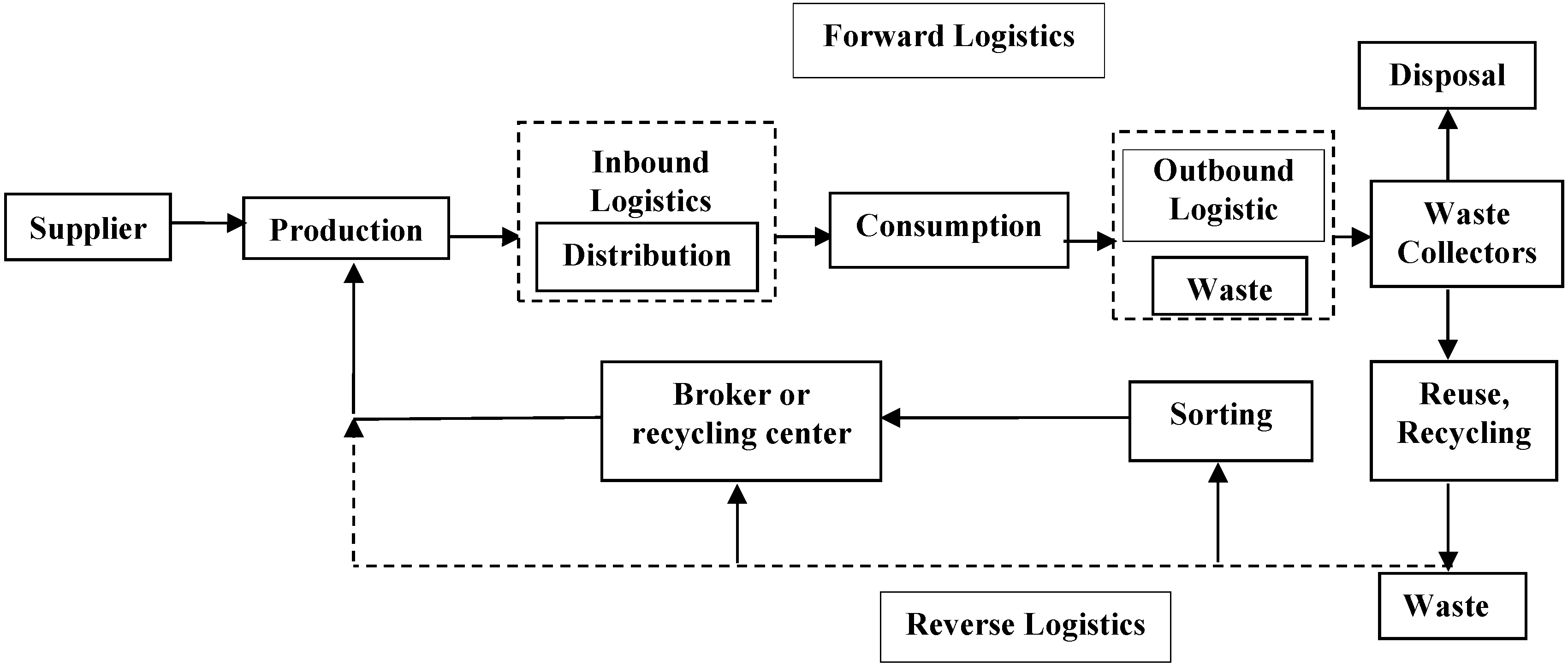

3.1. Research Concept

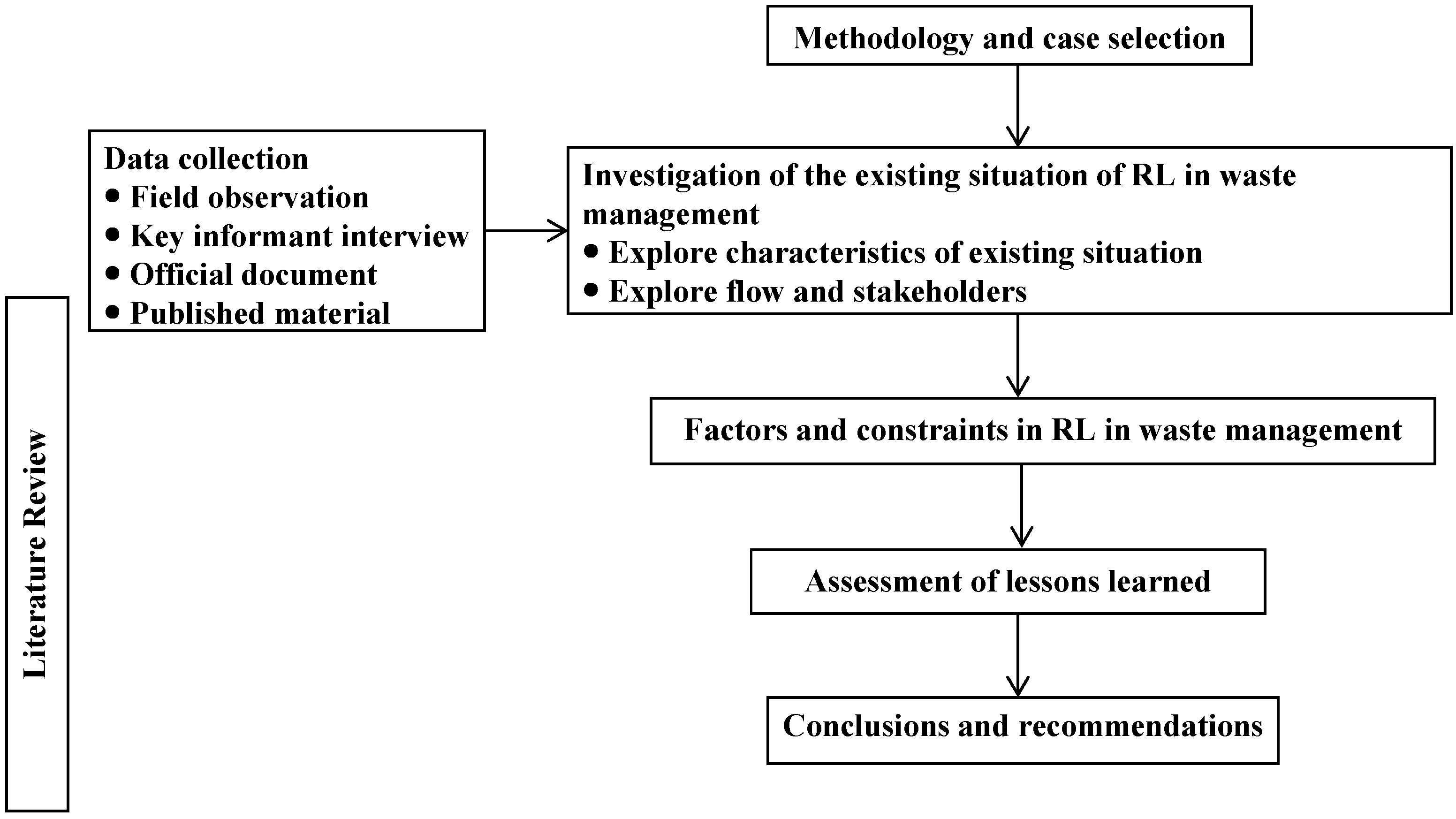

3.2. Research Methodology

3.3. Data Collection and Analysis

4. Results of the Study

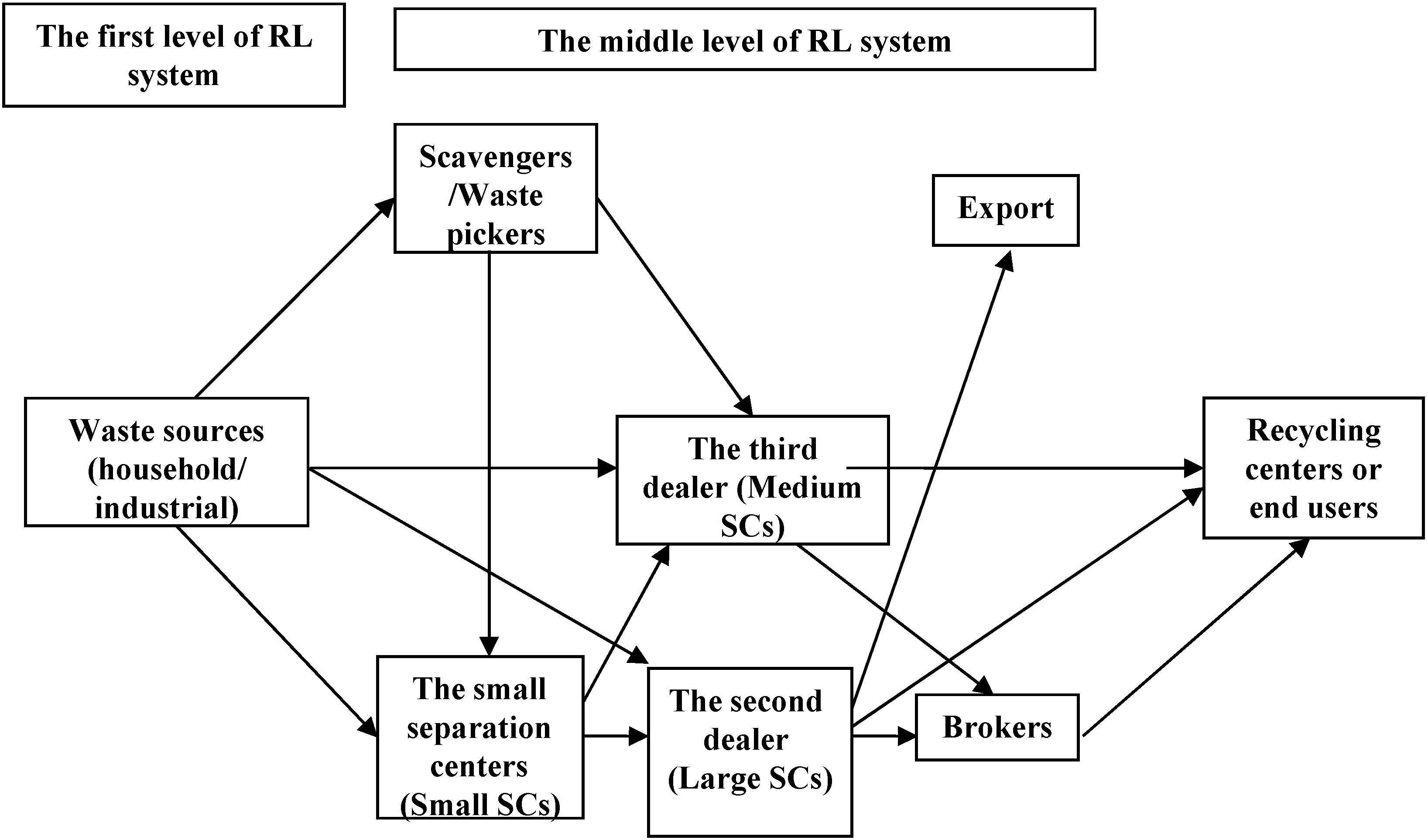

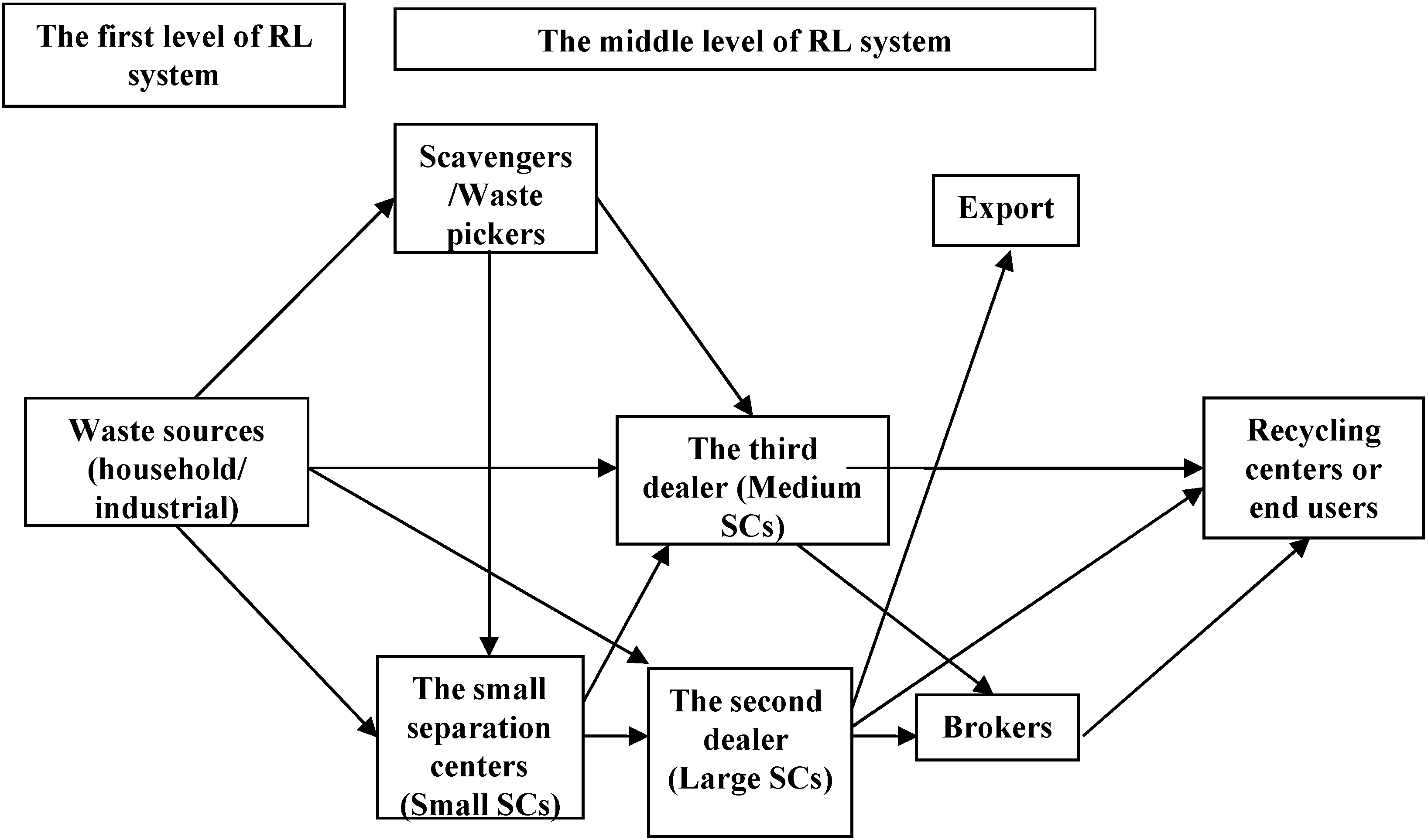

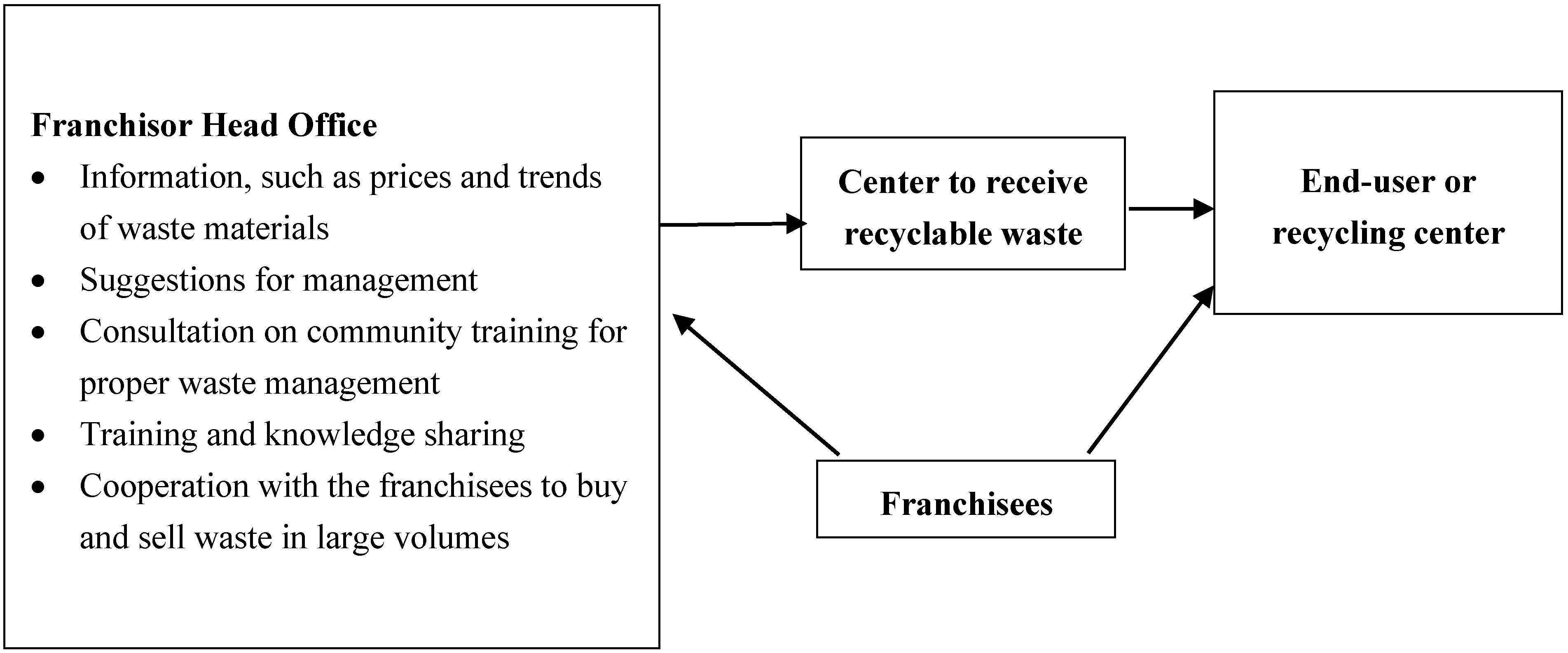

4.1. Investigated Existing Situation of RL Practice

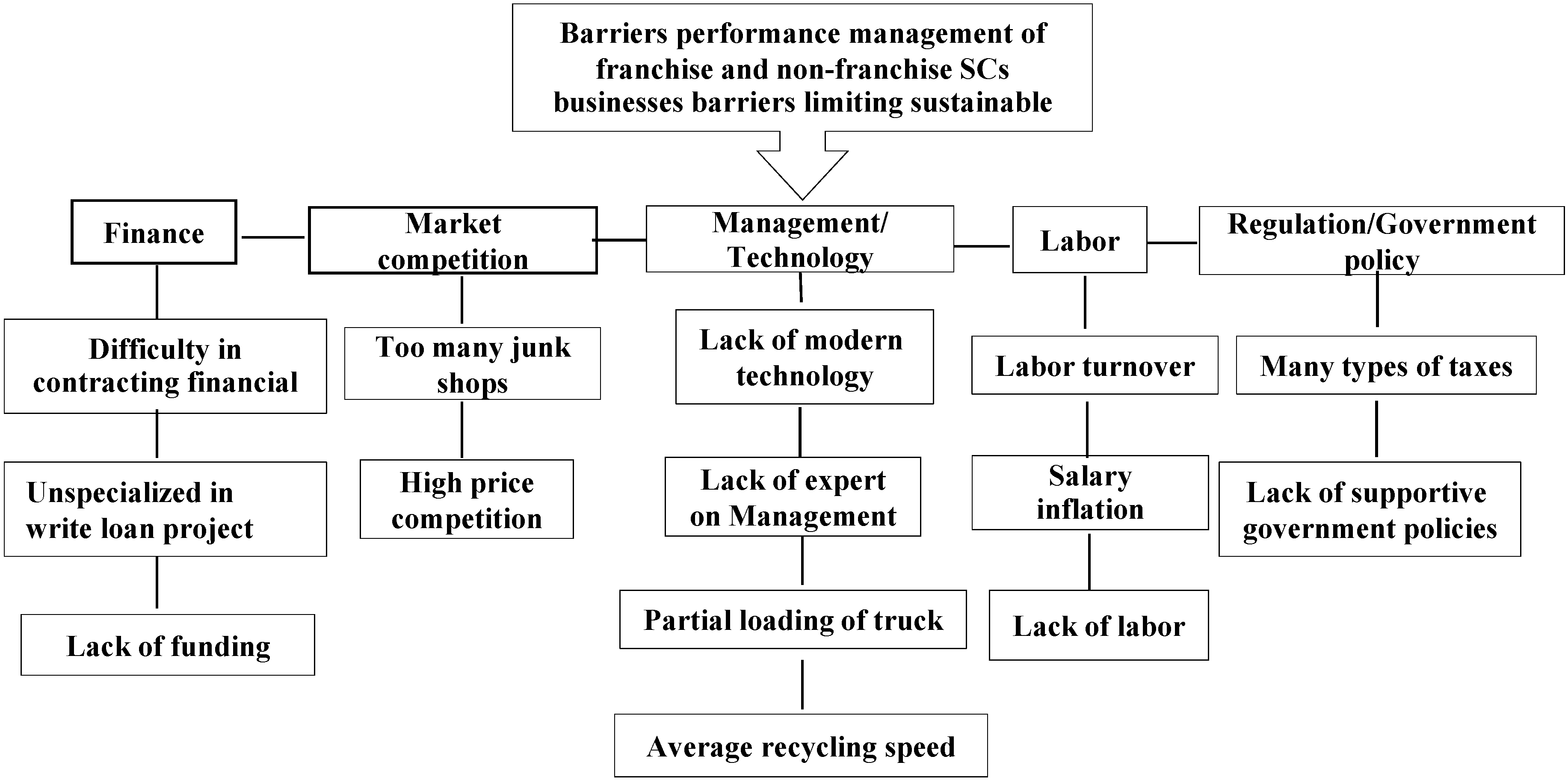

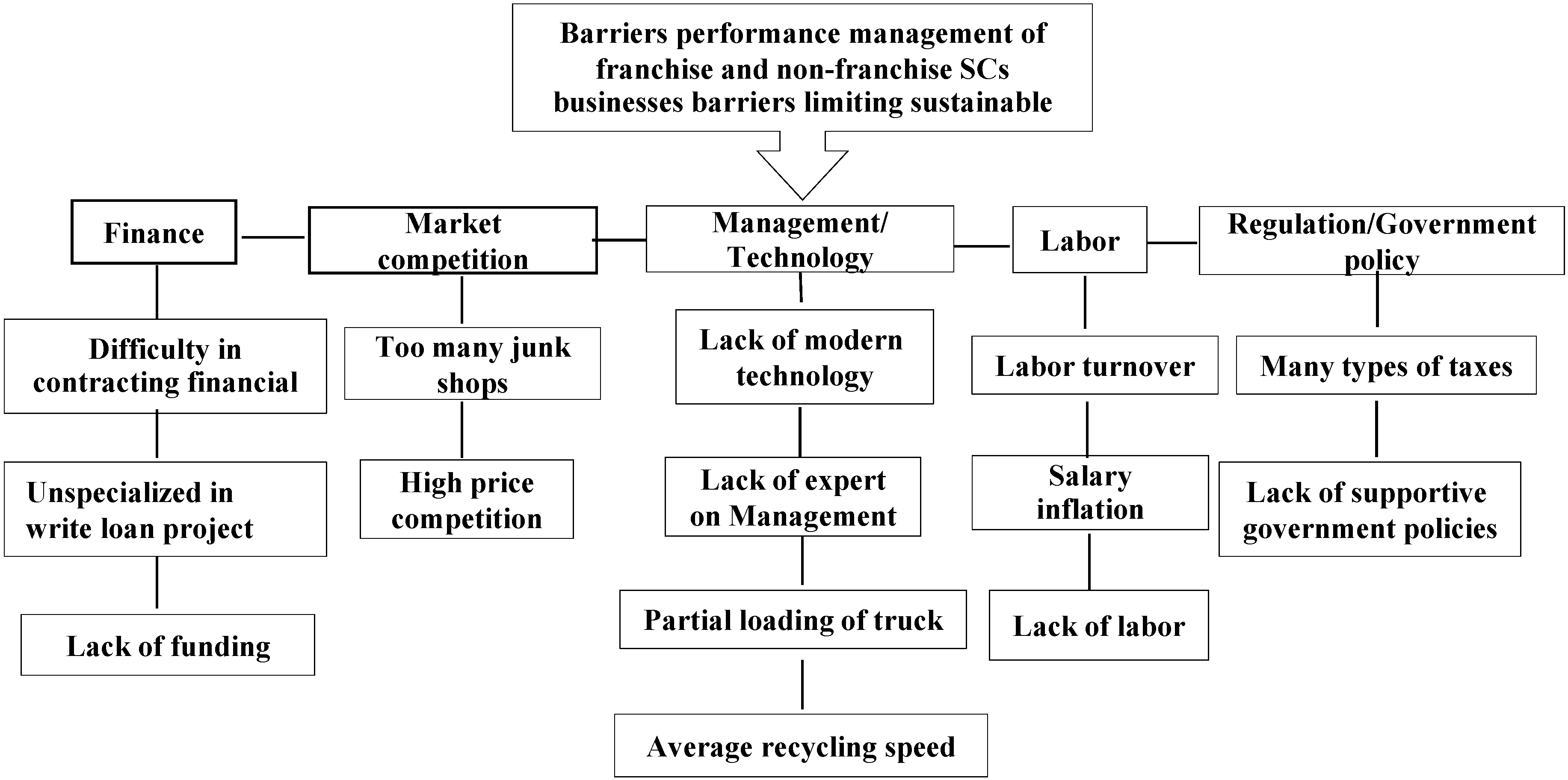

4.2. Investigated Factors Influencing and Barriers to RL Practice

4.2.1. The Potential Factor Influencing and Constraint of RL of Waste Practice

4.2.2. Factor Influencing RL of Waste Management Practices in Thailand

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Detail | Proportion (%) |

|---|---|

| Recyclable waste in SCs | Metals (29%), paper (26.6%), plastic (23.2%), glass (20.9%) and other materials (0.3%) |

| Sources of waste | Households (23.6%), industries (22%), offices (16.7%), scavengers using pickup trucks (15.7%), junk shops (10.2%), scavengers using carts (7.5%) and other sources (4.3%). |

| Channels for selling recyclable of SCs | Recycling centers (56.6%), brokers (42.7%) and other channels (0.7%) |

| Machine in waste separation | Cutting metal (22.2%), compacting paper (20%), compacting metal (15.9%), compacting plastic (10.1%) and other purposes (31.8%) |

| Weighted average index | |||

|---|---|---|---|

| Aspects | Criterion | Non-Franchise | Franchise |

| (n = 74) | (n = 24) | ||

| Environmental | Capability in waste management practice * | 0.6721 | 0.7833 |

| • Level of cleanliness of recyclable wastes | 0.8243 | 0.8000 | |

| • Highly skilled workers * | 0.6378 | 0.7333 | |

| • Technological level * | 0.5541 | 0.8167 | |

| Environmental concern * | 0.7932 | 0.8917 | |

| • Perception level of entrepreneurs on environmental impacts | 0.7486 | 0.9250 | |

| • Mitigation of noise, smells, and other disturbances to neighborhood * | 0.8378 | 0.8583 | |

| Economic | Economies of scale * | 0.7151 | 0.7850 |

| • Increase in the amount of sales and purchases this year when compared to last year * | 0.7595 | 0.7667 | |

| • Adaptation to change in business * | 0.7486 | 0.8083 | |

| • Access to transportation network * | 0.7351 | 0.8417 | |

| • Having business plan * | 0.6973 | 0.8083 | |

| • Increase in turnover rate * | 0.6351 | 0.7000 | |

| Customer satisfaction * | 0.7770 | 0.8583 | |

| • Trust in product and service quality * | 0.8054 | 0.9083 | |

| • Waste is sufficiently separated at a generation source | 0.7892 | 0.7333 | |

| Social | Relationship within RL network | 0.7662 | 0.9083 |

| • Level of social involvement * | 0.7351 | 0.9333 | |

| • Well-known in retail customer | 0.7973 | 0.8833 | |

| Weighted average index | ||

|---|---|---|

| Constraints | Non-Franchise SCs | Franchise SCs |

| Finance/Accounting | 0.81 | 0.50 |

| Market competition | 0.78 | 0.69 |

| Management/Technology | 0.51 | 0.46 |

| Labor | 0.76 | 0.69 |

| Regulation/Government policy | 0.39 | 0.32 |

5. Discussions

6. Conclusions

Acknowledgments

Author Contributions

Appendix

| Non-franchise | Franchise | Total | |

|---|---|---|---|

| Amount of waste buy and sale per day | |||

| Less than 10 ton/day | 46 (46.9%) | 2 (2.0%) | 48 (49.0%) |

| 10–30 ton/day | 25 (25.5%) | 15 (15.3%) | 40 (40.8%) |

| More than 30 ton/day | 3 (3.1%) | 7 (7.1%) | 10 (10.2%) |

| Investment | |||

| Less than 5 million baht | 50 (51.0%) | 7 (7.1%) | 57 (58.2%) |

| 5–30 million Baht | 20 (20.4%) | 13 (13.3%) | 33 (33.7%) |

| More than 30 million Baht | 4 (4.1%) | 4 (4.1%) | 8 (8.2%) |

| Employee | |||

| 1–10 worker | 37 (37.8%) | 3 (3.1%) | 40 (40.8%) |

| 11–50 | 36 (36.7%) | 20 (20.4%) | 56 (57.1%) |

| More than 50 | 1 (1%) | 1 (1%) | 2 (2.0%) |

| Cooperation | |||

| SMEs | 0 (0%) | 7 (7.1%) | 7 (7.1%) |

| Department of Industrial Promotion | 3 (3.1%) | 3 (3.1%) | 6 (6.1%) |

| The Federation of Thai Industries | 0 (0%) | 3 (3.1%) | 3 (3.1%) |

| Pollution Control Department | 46 (46.9%) | 2 (2.0%) | 48 (49%) |

| None | 25 (25.5%) | 9 (9.2%) | 34 (34.7%) |

| Sex | |||

| Male | 42 (42.9%) | 12 (12.2%) | 54 (55.1%) |

| Female | 32 (32.7%) | 12 (12.2%) | 44 (44.9%) |

| Age | |||

| Less than 30 | 7 (7.1%) | 0 (0%) | 7 (7.1%) |

| 31–40 | 22 (22.4%) | 8 (8.2%) | 30 (30.6%) |

| 41–50 | 28 (28.6%) | 14 (14.3%) | 42 (42.9) |

| 51–60 | 16 (16.3%) | 1 (1.0%) | 17 (17.3%) |

| More than 60 | 1 (1.0%) | 1 (1.0%) | 2 (2.0%) |

| Education | |||

| Primary | 18 (18.4%) | 1 (1.0%) | 19 (19.4%) |

| Junior secondary | 1 (1.0%) | 0 (0%) | 1 (1%) |

| Senior secondary | 3 (3.1%) | 0 (0%) | 3 (3.1%) |

| Commerce | 26 (26.5%) | 2 (2.0%) | 28 (28.6%) |

| Bachelor | 22 (22.4%) | 13 (13.3%) | 35 (35.7%) |

| Master or higher | 4 (4.1%) | 8 (8.2%) | 12 (12.2%) |

Conflicts of Interest

References

- Rogers, D.; Tibben-Lembke, R. An examination of reverse logistics practices. J. Bus. Logist. 2001, 22, 129–148. [Google Scholar]

- Stock, J.R.; Speh, T.W.; Shear, H.W. Many happy (product) returns. Harv. Bus. Rev. 2002, 80, 16–17. [Google Scholar]

- Pohlen, T.L.; Farris, M.T. Reverse logistics in plastics recycling. Inter. J. Phys. Distrib. Logist. Manag. 1992, 22, 35–47. [Google Scholar]

- Pollution Control Department. State of Thailand Pollution Report 2011; Pollution Control Department: Bangkok, Thailand, 2011.

- Achapan, I. Recycling as Habitual Behavior: The Impact of Habit on Household Waste Recycling Behavior in Thailand. Asian Soc. Sci. 2012. [Google Scholar] [CrossRef]

- The Thai Pulp and Paper Industries Association. 2013 Directory; Thai Pulp and Paper Industries Association: Bangkok, Thailand, 2013. [Google Scholar]

- Wilson, D.C.; Velis, C.; Cheeseman, C. Role of informal sector recycling in waste management in developing countries. Habitat. Int. 2006, 30, 797–808. [Google Scholar]

- Stock, J.R. Reverse Logistics; Council of Logistics Management: Oak Brook, IL, USA, 1992. [Google Scholar]

- Fleischmann, M.; Krikke, H.R.; Dekker, R.; Flapper, S.D.P. A characterization of logistics networks for product recovery. Omega 2000, 28, 653–666. [Google Scholar]

- Thierry, M.C.; Salomon, M.; van Nunen, J.; van Wassenhove, L.N. Strategic issues in product recovery management. Calif. Manag. Rev. 1995, 37, 114–135. [Google Scholar]

- De Brito, M.P.; Dekker, R. Reverse Logistics—A framework. Econom. Inst. Rep. EI 2002, 38, 1–19. [Google Scholar]

- Meade, L.; Sarkis, J.; Presley, A. The theory and practice of reverse logistics. Inter. J. Logist. Sys. Manag. 2007, 3, 56–84. [Google Scholar]

- Louwers, D.; Kip, B.J.; Peters, E.; Souren, F.; Flapper, S.D.P. A facility location allocation model for reusing carpet materials. Comp. Ind. Eng. 1999, 36, 855–869. [Google Scholar]

- Heng, N.; Laptaned, U.; Mehrdadi, N. Recycling and reuse of household plastics. Int. J. Environ. Resour. 2008, 2, 27–36. [Google Scholar]

- Wongthatsanekorn, W. A goal programming approach for plastic recycling in Thailand. World Acad. Sci. Eng. Tech. 2009, 49, 513–518. [Google Scholar]

- Chowdhury, M.; Paul, H.; Das, A. The impact of top management commitment on total quality management practice: An exploratory study in the Thai government industry. Glob. J. Flex. Syst. Manag. 2007, 8, 17–29. [Google Scholar]

- Pollution Control Department. State of Thailand Pollution Report 2012; Pollution Control Department: Bangkok, Thailand, 2012.

- Yamane, T. Statistics, An Introductory Analysis, 2nd ed.; Harper and Row: New York, NY, USA, 1967. [Google Scholar]

- Miah, M.A.Q.; Miẏa, M.A.K.; Simpson, H.R. Applied Statistics: A Course Handbook for Human Settlements Planning; Asian Institute of Technology: Bangkok, Thailand, 1993. [Google Scholar]

- Samonporn, S.; Vilas, N. Assessment of factors influencing the performance of solid waste recycling programs. Resour. Conservat. Recycl. 2008, 53, 45–56. [Google Scholar]

- Rousta, K.; Ekström, K.M. Assessing Incorrect Household Waste Sorting in a Medium-Sized Swedish City. Sustainability 2014, 5, 4349–4361. [Google Scholar]

- Jahre, M. Household waste collection as a reverse channel. Int. J. Phys. Distrib. Logist. Manag. 1995, 25, 39–55. [Google Scholar]

- Rogers, D.; Tibben-Lembke, R. Going Backwards: Reverse Logistics Trends and Practices; Reverse Logistics Executive Council Press: Pittsburgh, PA, USA, 1999. [Google Scholar]

- Klang, A.; Vikman, P.A.; Brattebo, H. Sustainable management of demolition waste: An integrated model for the evaluation of environmental, economic and social aspects. Res. Conservat. Recycl. 2003, 38, 317–334. [Google Scholar]

- De Brito, M.P.; Carboneb, V.; Blanquart, C.M. Towards a sustainable fashion retail supply chain in Europe: Organizations and performance. Int. J. Prod. Econ. 2008, 114, 534–553. [Google Scholar]

- Pati, R.K.; Vrat, P.; Kumar, P. A goal programming model for paper recycling system. Omega 2008, 36, 405–417. [Google Scholar]

- Daugherty, P.; Richey, R.; Hudgens, B.; Autry, C. Reverse logistics in the automobile aftermarket industry. Int. J. Logis. Manag. 2003, 14, 49–62. [Google Scholar]

- Ravi, V.; Ravi, S.; Tiwari, M.K. Productivity improvement of a computer hardware supply chain. Int. J. Prod. Perform. Manag. 2005, 3, 239–255. [Google Scholar]

- Ramirez, A.M. Product return and logistics knowledge: Influence on performance of the firm. Transport. Res. E Logist. Transport. Rev. 2012, 48, 1137–1151. [Google Scholar]

- Shih, K.H.; Chang, C.J.; Binshan, L. Assessing knowledge creation and intellectual capital in the banking industry. J. Intel. Cap. 2010, 11, 74–89. [Google Scholar]

- Wadhwa, S.; Madaan, J. Conceptual framework for knowledge management in reverse enterprise systems. J. Knowl. Manag. Pract. 2007, 8, 1–22. [Google Scholar]

- Kumar, S.; Putnam, V. Cradle to cradle: Reverse logistics strategies and opportunities across three industry sectors. Int. J. Prod. Econ. 2005, 115, 305–315. [Google Scholar]

- Abdulrahman, M.D.; Gunasekaran, A.; Subramanian, N. Critical barriers in implementing reverse logistics in the Chinese manufacturing sectors. Int. J. Prod. Econ. 2014, 147, 460–471. [Google Scholar]

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pumpinyo, S.; Nitivattananon, V. Investigation of Barriers and Factors Affecting the Reverse Logistics of Waste Management Practice: A Case Study in Thailand. Sustainability 2014, 6, 7048-7062. https://doi.org/10.3390/su6107048

Pumpinyo S, Nitivattananon V. Investigation of Barriers and Factors Affecting the Reverse Logistics of Waste Management Practice: A Case Study in Thailand. Sustainability. 2014; 6(10):7048-7062. https://doi.org/10.3390/su6107048

Chicago/Turabian StylePumpinyo, Sumalee, and Vilas Nitivattananon. 2014. "Investigation of Barriers and Factors Affecting the Reverse Logistics of Waste Management Practice: A Case Study in Thailand" Sustainability 6, no. 10: 7048-7062. https://doi.org/10.3390/su6107048