Towards More Sustainable Ironmaking—An Analysis of Energy Wood Availability in Finland and the Economics of Charcoal Production

Abstract

:1. Introduction

2. Background of Biomass Use in Blast Furnace Ironmaking

2.1. Reducing Agent Use in Ironmaking

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Application and replaced carbon source | Typical addition rate 1,2 | Charcoal substitution rate (%) 1,2 | Charcoal amount (kg/tHM) |

|---|---|---|---|

| Cokemaking(coking coal) | 480–560 kg/tHM 3 | 2–10 | 9.6–56 kg/tHM |

| BF tuyere injection(pulverized coal) | 150–200 kg/tHM | 0–100 | 0–200 kg/tHM |

| BF nut coke replacement | 45 kg/tHM | 50–100 | 22.5–45 kg/tHM |

| BF briquette 4(coking plant residues) | 10–12 kg/tHM | 0–100 | 0–12 kg/tHM |

| Sintering solid fuel 5 | 76.5–102 kg/tHM | 50–100 | 38.3–102 kg/tHM |

| Pre-reduced iron ore composite pellets 6 | Not currently practiced | 18–36 kg/tHM | |

2.2. Thermochemical Conversion of Biomass into Reducing Agent

2.3. Biomass-Based Reducing Agent Requirements in the Finnish Carbon Steel Industry

3. Biomass Availability for Ironmaking in Finland

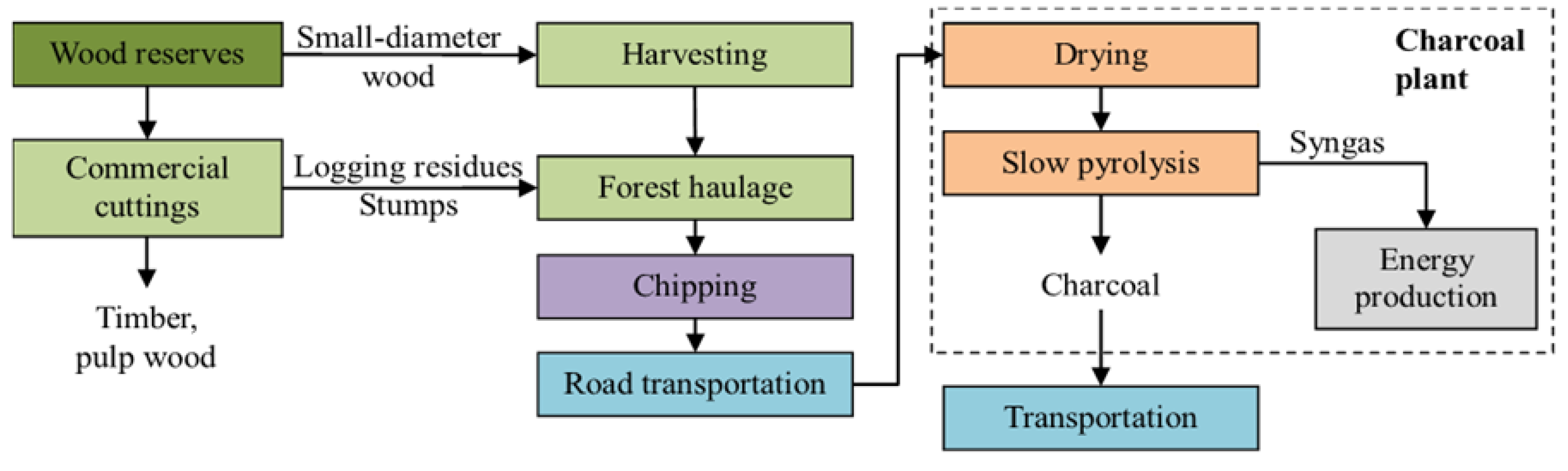

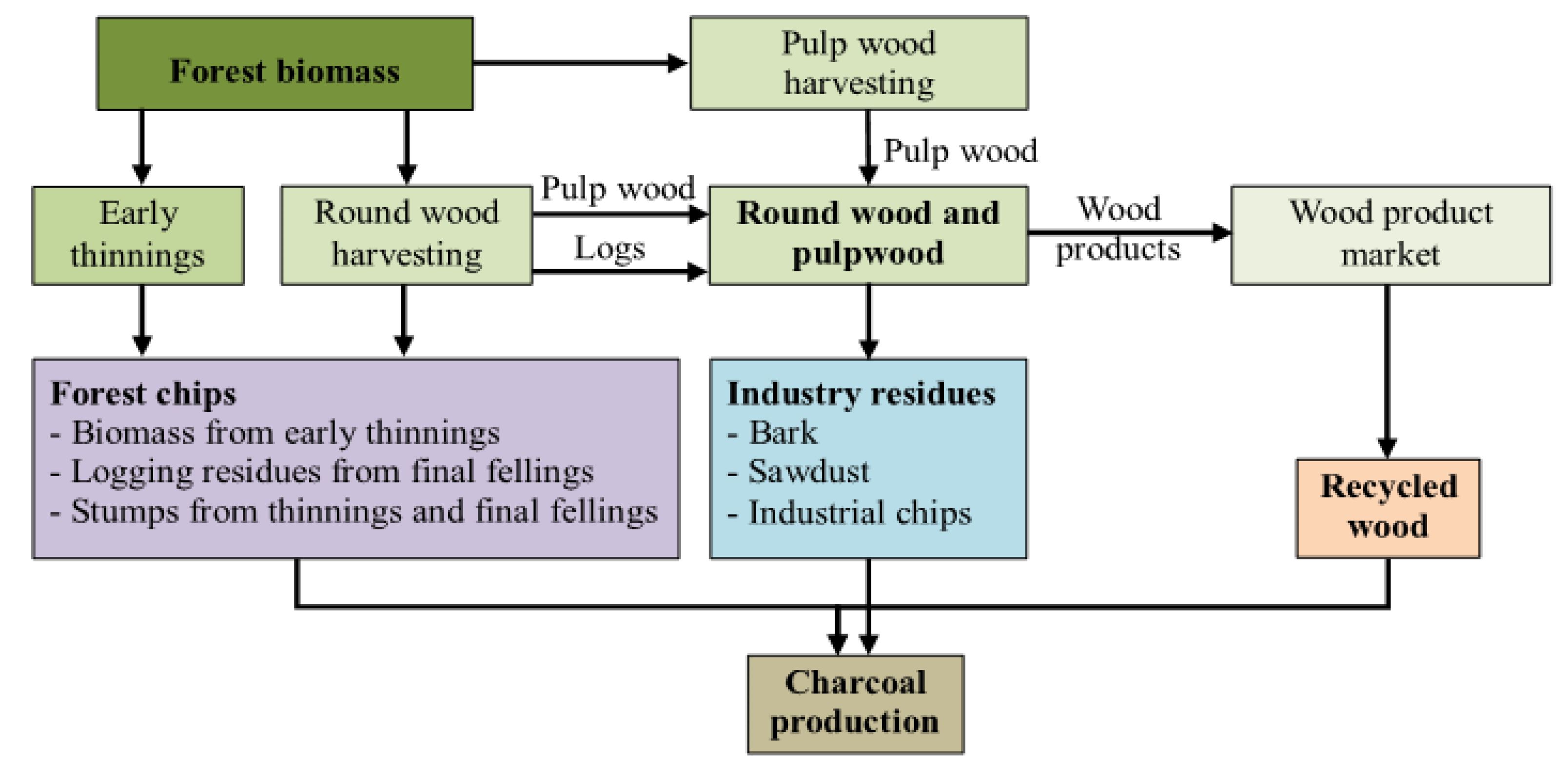

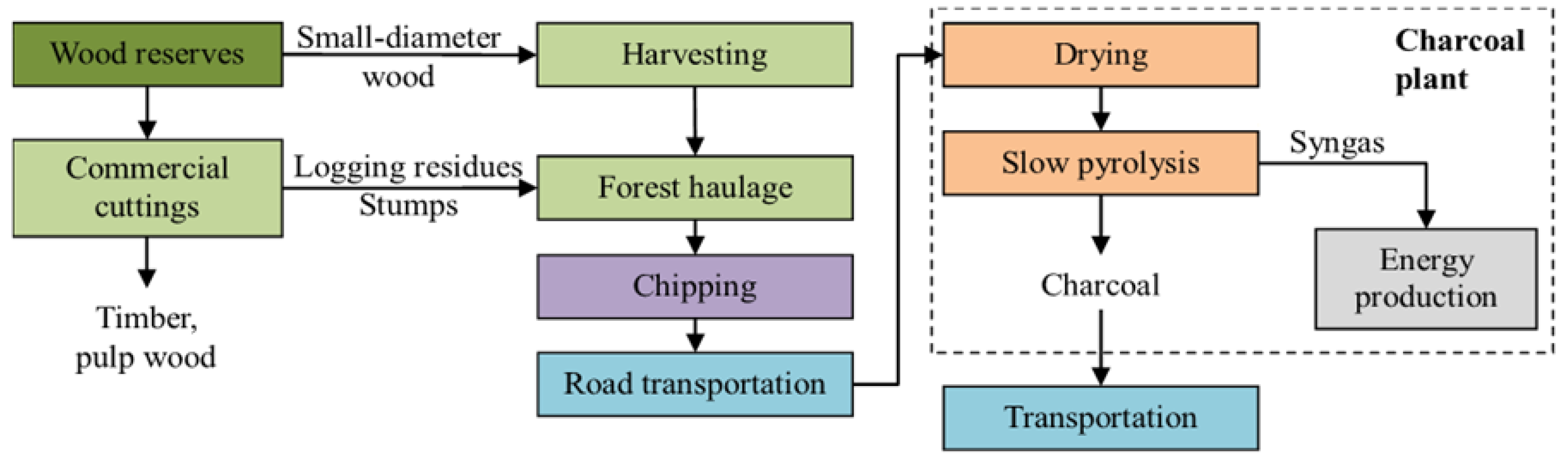

3.1. Sources of Wood-Based Biomass

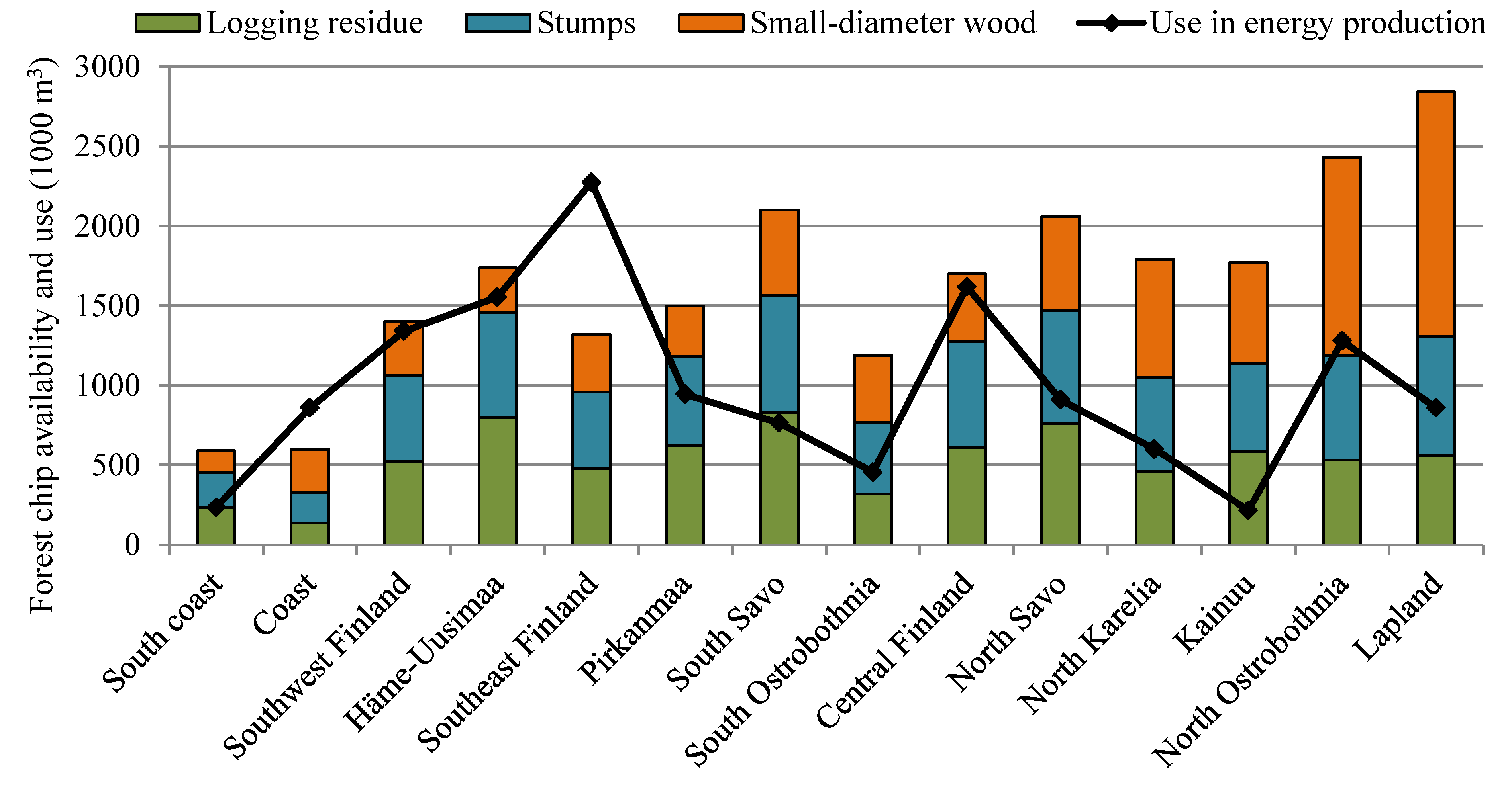

3.2. Forest Chip Potential in Finland

3.3. Competing Use of Forest Chips

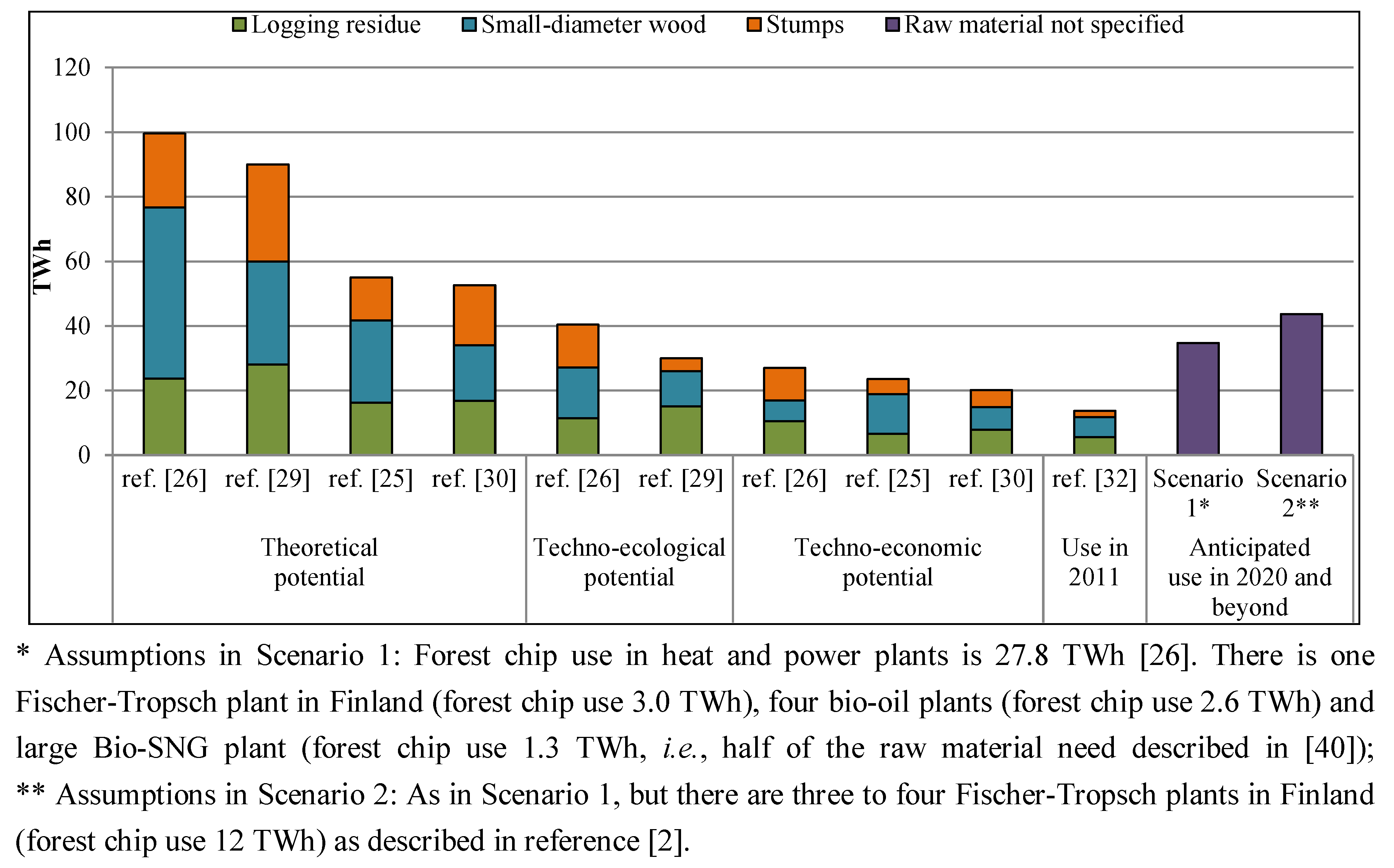

3.4. Summary of Forest Chip Production Potential

4. Economic Issues in Charcoal Production and Use in Ironmaking

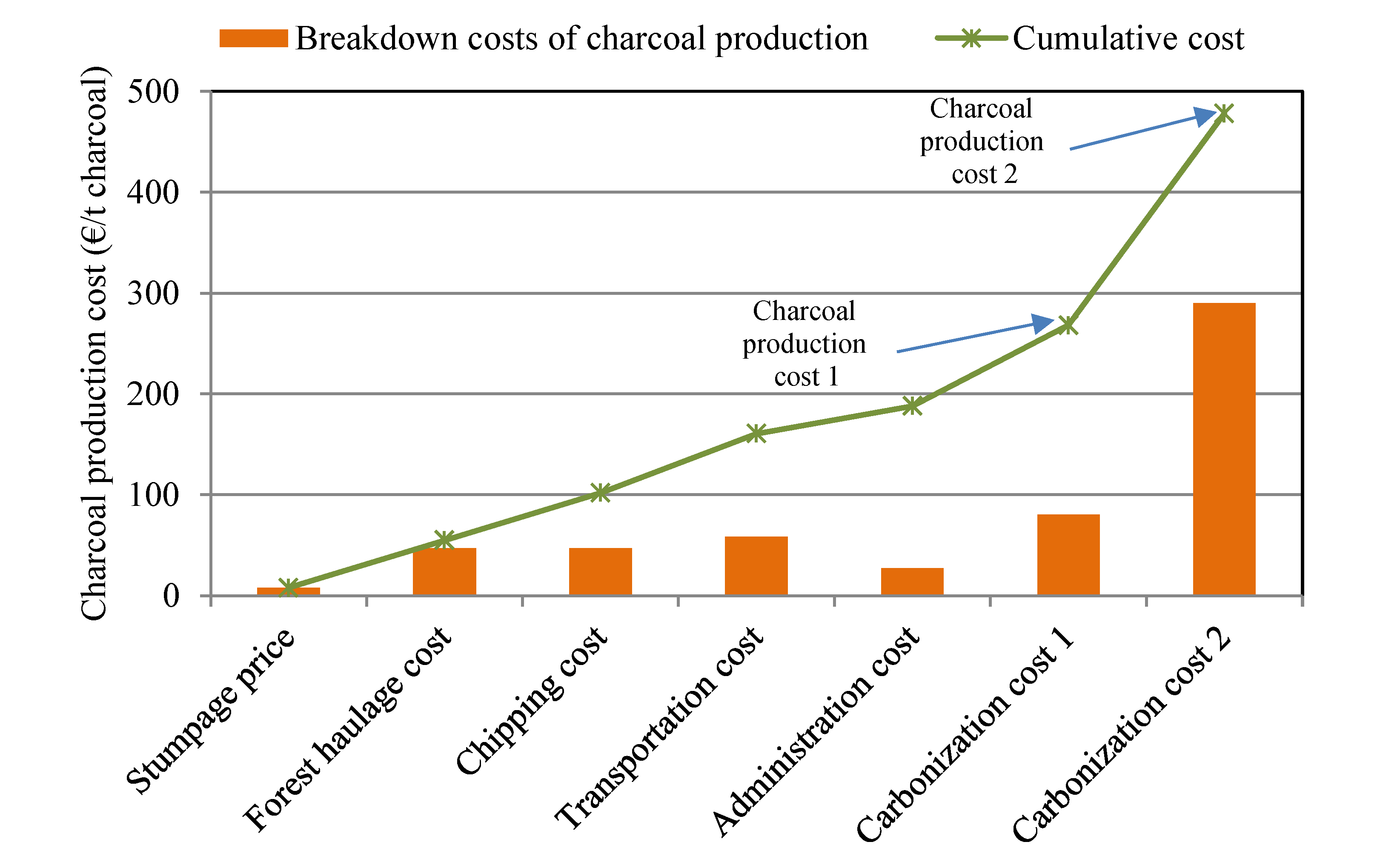

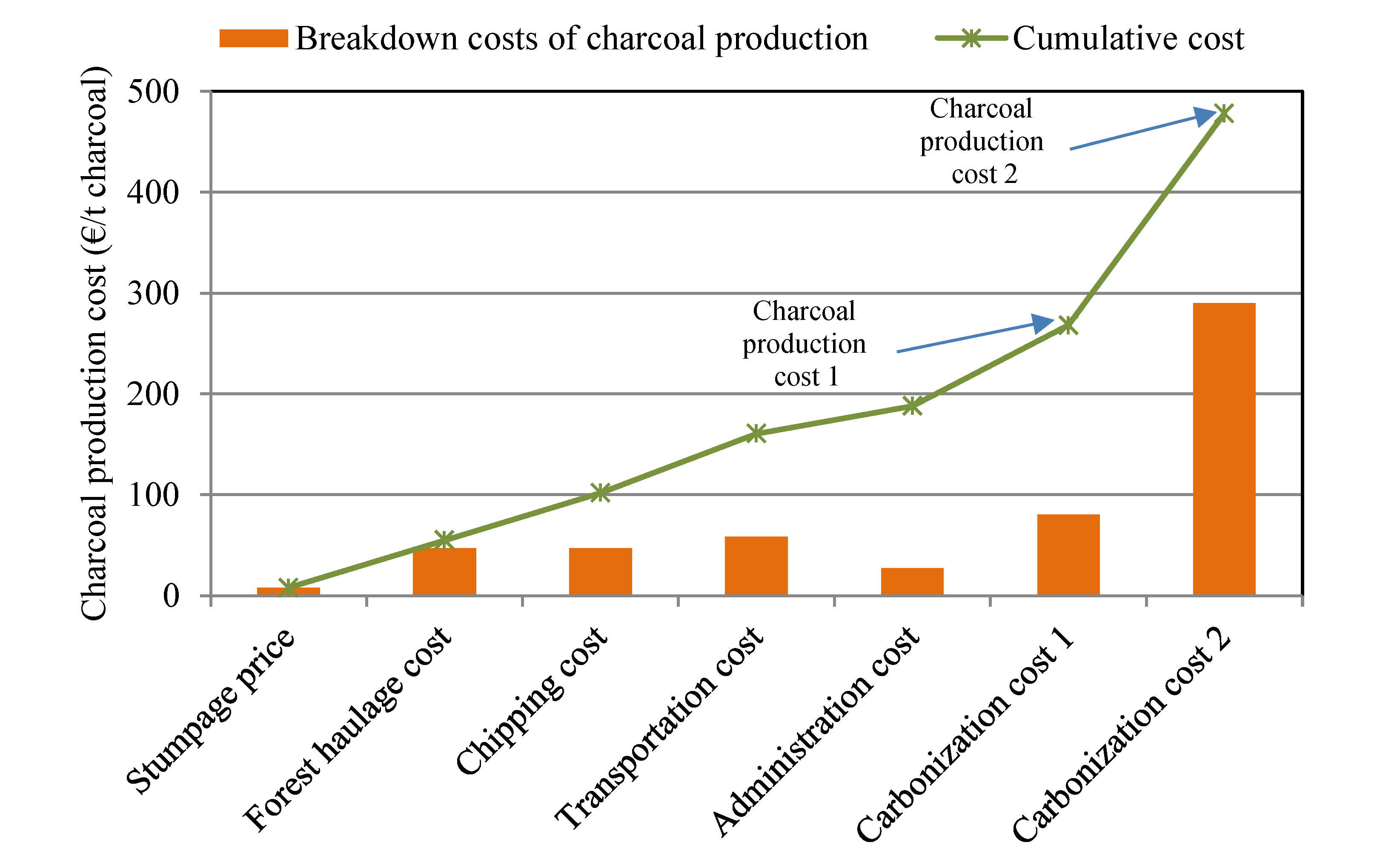

4.1. Supply Chain Costs of Charcoal Production

4.2. Total Cost of Charcoal Production

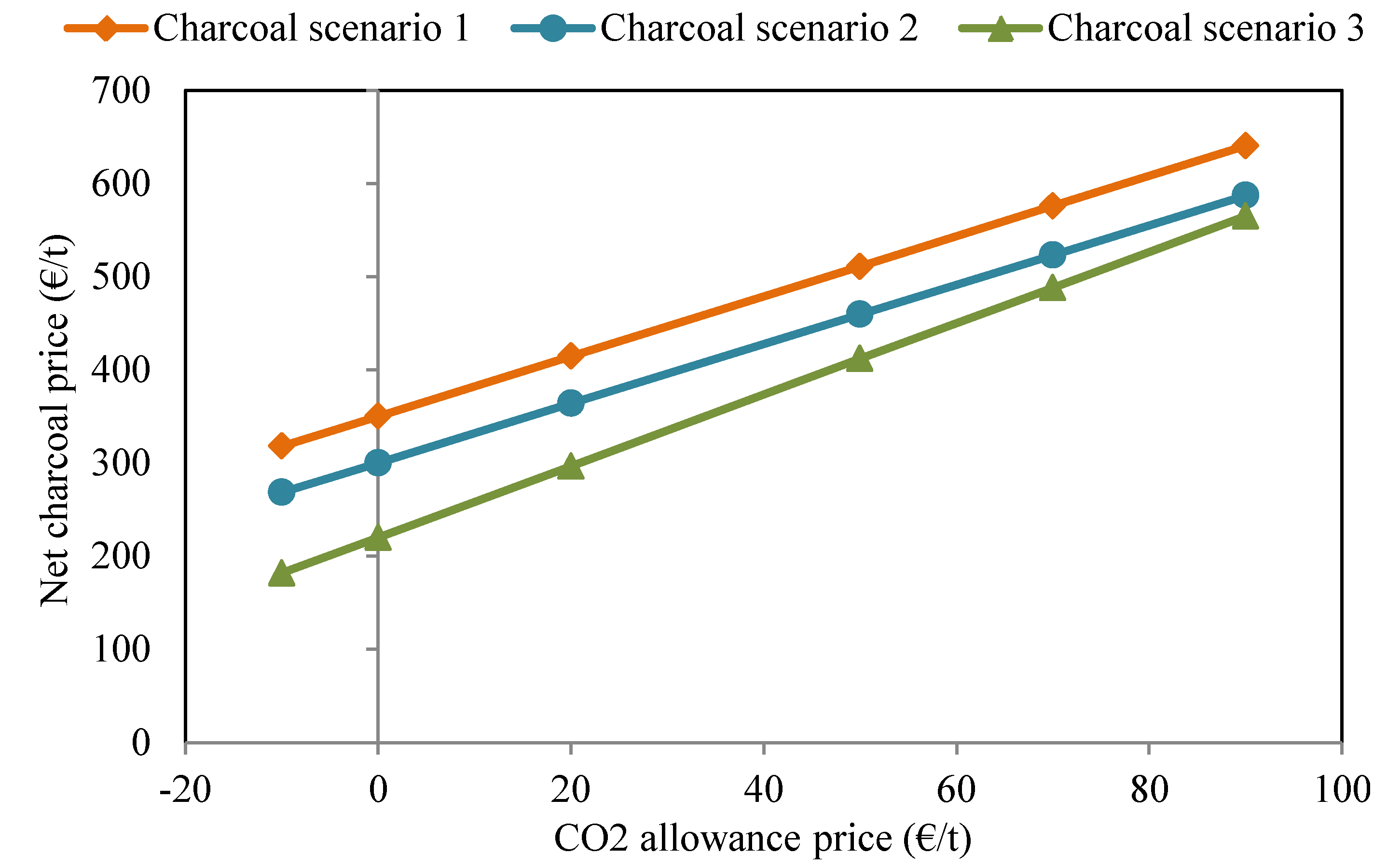

4.3. Charcoal Economics Compared to Fossil-Based Reducing Agents with CO2 Cost

| Base case 1 | Base case 2 | Charcoal scenario 1 | Charcoal scenario 2 | Charcoal scenario 3 | |

|---|---|---|---|---|---|

| Coke (kg/tHM) * | 385 | 340 | 365 | 385 | 310 |

| Bottom oil (kg/tHM) | 80 | - | 80 | 66.5 | - |

| Pulverized coal (kg/tHM) | - | 150 | - | - | - |

| Charcoal (kg/tHM) | - | - | 20 | 13.5 | 150 |

| Total reducing agent use (kg/tHM) | 465 | 490 | 465 | 465 | 460 |

| Emitted fossil CO2 (kg/tHM) | 1,496 | 1,574 | 1,432 | 1,453 | 1,000 |

5. Discussion and Conclusions

Acknowledgments

Conflict of Interest

References

- Directive 2009/28/EC of the European Parliament and of the Council of 23 April 2009 on the promotion of the use of energy from renewable sources and amending and subsequently repealing Directives 2001/77/EC and 2003/30/EC. 2003. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2009:140:0016:0062:EN:PDF (accessed on 15 October 2012).

- Laitila, J.; Leinonen, A.; Flyktman, M.; Virkkunen, M.; Asikainen, A. Metsähakkeen Hankinta-ja Toimituslogistiikan Haasteet ja Kehittämistarpeet (in Finnish); Research notes 2564 for VTT Tiedotteita; Julkaisija - Utgivare - Publisher : Helsinki, Finland, 2010. [Google Scholar]

- Griessacher, T.; Antrekowitsch, J.; Steinlechner, S. Charcoal from agricultural residues as alternative reducing agent in metal recycling. Biomass Bioenergy 2012, 39, 139–146. [Google Scholar] [CrossRef]

- Matsumura, T.; Ichida, M.; Nagasaka, T.; Kato, K. Carbonization behaviour of woody biomass and resulting metallurgical coke properties. ISIJ Int. 2008, 48, 572–577. [Google Scholar] [CrossRef]

- Machado, J.G.M.S.; Osório, E.; Vilela, C.F. Reactivity of brazilian coal, charcoal, imported coal and blends aiming to their injection into blast furnace. Mater. Res. 2010, 13, 287–292. [Google Scholar] [CrossRef]

- Babich, A.; Senk, D.; Fernandez, M. Charcoal behaviour by its injection into the modern blast furnace. ISIJ Int. 2010, 50, 81–88. [Google Scholar] [CrossRef]

- Mathieson, J.G.; Rogers, H.; Somerville, M.A.; Jahanshahi, S. Reducing net CO2 emissions using charcoal as a blast furnace tuyere injectant. ISIJ Int. 2012, 52, 1489–1496. [Google Scholar] [CrossRef]

- Suopajärvi, H.; Fabritius, T. Effects of biomass use in integrated steel plant—Gate-to-gate life cycle inventory method. ISIJ Int. 2012, 52, 779–787. [Google Scholar]

- Norgate, T.; Langberg, D. Environmental and economic aspects of charcoal use in steelmaking. ISIJ Int. 2009, 49, 587–595. [Google Scholar] [CrossRef]

- Norgate, T.; Haque, N.; Somerville, M.; Jahanshahi, S. Biomass as a source of renewable carbon for iron and steelmaking. ISIJ Int. 2012, 52, 1472–1481. [Google Scholar] [CrossRef]

- Piketty, M.G.; Wichert, M.; Fallot, A.; Aimola, L. Assessing land availability to produce biomass for energy: The case of Brazilian charcoal for steel making. Biomass Bioenergy 2009, 33, 180–190. [Google Scholar] [CrossRef]

- Luengen, H.B.; Peters, M.; Schmöle, P. Iron Making in Western Europe. In Metec InSteelCon 2011. In Proceedings of 6th European Coke and Ironmaking Congress, Düsseldorf, Germany,, 27 June–1 July 2011.

- MacPhee, J.A.; Gransden, J.F.; Giroux, L.; Price, J.T. Possible CO2 mitigation via addition of charcoal to coking blends. Fuel Process. Technol. 2009, 90, 16–20. [Google Scholar] [CrossRef]

- Hanrot, F.; Sert, D.; Delinchant, J.; Pietruck, R.; Bürgler, T.; Babich, A.; Fernández, M.; Alvarez, R.; Diez, M.A. CO2 Mitigation for Steelmaking using Charcoal and Plastics Wastes as Reducing Agents and Secondary Raw Materials. In Proceedings of the 1st Spanish National Conference on Advances in Materials Recycling and Eco-Energy, Madric, Spain, 12–13 November 2009.

- Mathieson, J.G.; Rogers, H.; Somerville, M.; Ridgeway, P.; Jahanshahi, S. Use of Biomass in the Iron and Steel Industry—An Australian Perspective. In MetecInSteelCon 2011. In Proceedings of 1st International Conference on Energy Efficiency and CO2 Reduction in the Steel Industry, Düsseldorf, Germany, 27 June–1 July 2011.

- Strezov, V. Iron ore reduction using saw dust: Experimental analysis and kinetic modeling. Renew. Energy 2006, 36, 1892–1905. [Google Scholar] [CrossRef]

- Chen, W.H.; Du, S.W.; Tsai, C.H.; Wang, Z.Y. Torrefied biomass in a drop tube furnace to evaluate their utility in blast furnaces. Bioresour. Technol. 2012, 111, 433–438. [Google Scholar] [CrossRef]

- Goyal, H.B.; Seal, D.; Saxena, R.C. Bio-fuels from thermochemical conversion of renewable resources: A review. Renew. Sustain. Energy Rev. 2008, 12, 504–517. [Google Scholar] [CrossRef]

- Antal, M.J., Jr.; Gronli, M. The art, science, and technology of charcoal producti. Ind. Eng. Chem. Res. 2003, 42, 1619–1640. [Google Scholar] [CrossRef]

- Lovel, R.R.; Vining, K.R.; Dell’amico, M. The influence of fuel reactivity on iron ore sintering. ISIJ Int. 2009, 49, 195–202. [Google Scholar] [CrossRef]

- Duku, M.H.; Gu, S.; Hagan, E.B. Biochar production potential in Ghana-A review. Renew. Sustain. Energy Rev. 2011, 15, 3539–3551. [Google Scholar] [CrossRef]

- Antal, M.J., Jr.; Croiset, E.; Dai, X.; DeAlmeida, C.; Mok, W.S.L.; Norberg, N.; Richard, J.R.; Majthoub, M.A. High-yield biomass charcoal. Energy Fuels 1996, 10, 652–658. [Google Scholar] [CrossRef]

- Kinnunen, K.; Paananen, T.; Lilja, J. Modelling and simulation of Blast Furnace Process for switch from Sinter to Pellet Operation. In Metec InSteelCon 2011, STEELSIM. In Proceedings of 4th International Conference on Modelling and Simulation of Metallurgical Processes in Steelmaking, Düsseldorf, Germany, 27 June–1 July 2011.

- Ranta, T.; Lahtinen, P.; Elo, J.; Laitila, J. The effect of CO2 emission trade on the wood fuel market in Finland. Biomass Bioenergy 2007, 31, 535–542. [Google Scholar] [CrossRef]

- Maidell, M.; Pyykkönen, P.; Toivonen, R. Metsäenergiapotentiaalit Suomen maakunnissa (in Finnish); Working Papers No. 106 for Pellervo Economic Research Institute; Helsinki, Finland, 2008. [Google Scholar]

- Kärhä, K.; Elo, J.; Lahtinen, P.; Räsänen, T.; Keskinen, S.; Saijonmaa, P.; Heiskanen, H.; Strandström , M.; Pajuoja, H. Kiinteiden puupolttoaineiden saatavuus ja käyttö Suomessa vuonna 2020. In Publications of the Ministry of the Employment and the Economy of Finland, Energy and the Climate 66/2010 (in Finnish); Helsinki, Finland, 2010. [Google Scholar]

- Ranta, T. Logging Residues from Regeneration Fellings for Biofuel Production—A GIS-based Availability and Supply Cost Analysis. Ph.D. Dissertation, Lappeenranta University of Technology, Acta Universitatis Lappeenrantaensis 128, Lappeenranta, Finland, 2002. [Google Scholar]

- Helynen, S.; Flyktman, M.; Asikainen, A.; Laitila, J. Metsätalouteen ja Metsäteollisuuteen Perustuvan Energialiiketoiminnan Mahdollisuudet (in Finnish); VTT Tiedotteita—Research Notes 2397; Julkaisija - Utgivare - Publisher: Helsinki, Finland, 2007. [Google Scholar]

- Hakkila, P. Developing technology for large-scale production of forest chips. In Wood Energy Technology Programme 1999-2003. ; Final Report, Technology Programme Report 6/2004, The Finnish Funding Agency for Technology and Innovation (Tekes): Helsinki, Finland, 2004. [Google Scholar]

- Pöyry Energy. Puupolttoaineiden kysyntä ja tarjonta Suomessa vuonna 2020—Päivitetty tilannekatsaus (in Finnish). Pöyry Energy Oy: Espoo, Finland, 2007. [Google Scholar]

- Hakkila, P. Factors driving the development of forest energy in Finland. Biomass Bioenergy 2006, 30, 281–288. [Google Scholar] [CrossRef]

- Ylitalo, E. Puun energiakäyttö 2011. Metsätilastotiedote 16/. 2012. Available online: http://www.metla.fi/metinfo/tilasto/julkaisut/mtt/2012/puupolttoaine2011.pdf (accessed on 15 October 2012).

- Solantausta, Y.; Oasmaa, A.; Sipilä, K.; Lindfors, C.; Lehto, J.; Autio, J.; Jokela, P.; Alin, J.; Heiskanen, J. Bio-oil production from biomass: Steps toward demonstration. Energy Fuels 2012, 26, 233–240. [Google Scholar] [CrossRef]

- Metso to supply a bio oil production plant to Fortum power plant in Joensuu, Finland. Available online: http://www.metso.com/news/newsdocuments.nsf/web3newsdoc/0BBB64095E823F2AC22579BA0048E651?OpenDocument&ch=ChMetsoWebEng/ (accessed on 7 January 2013).

- Green fuel Nordic Oy invests 150 MEUR in new biorefinery plants in Finland. Press Release: 13 October 2011. Available online: http://www.greenfuelnordic.fi/en/page/23?newsitem=4/ (accessed on 10 January 2013).

- Centre for Economic Development, Transport and the Environment 2012. In Environmental Impact Assessment Report, Green Fuel Nordic PLC Biorefinery project (in Finnish); 2012. Available online: http://www.ely-keskus.fi/fi/ELYkeskukset/pohjoissavonely/Ymparistonsuojelu/YVA/paattyneet/kemianteollisuus/gfnbiojalostamo/Sivut/default.aspx/ (accessed on 7 January 2013).

- European Commission memo 2012, Questions and Answers on the Outcome of the First Call for Proposals under the NER300 Programme. Brussels, 18 December 2012. Available online: http://europa.eu/rapid/press-release_MEMO-12-999_en.htm/ (accessed on 7 January 2013).

- Vapo’s Biodiesel Plant Project Moving Ahead. Press Release Forest BTL, 22 August 2012. Available online: http://www.forestbtl.com/wp-content/uploads/2011/02/Forest-BtL-press-release-22.8.2012-EN.pdf (accessed on 7 January 2013).

- UPM to Build the Worlds First Biorefinery Producing Wood-Based Biodiesel. 1 February 2012. Available online: http://www.upm.com/EN/MEDIA/All-news/Pages/UPM-to-build-the-world%E2%80%99s-first-biorefinery-producing-wood-based-biodiesel-001-Wed-01-Feb-2012-10-05.aspx/ (accessed on 7 January 2013).

- Joutsenon biojalostamo merkittävä EU-tason kehityshanke. Press Release: 28 June 2012 (in Finnish). Available online: https://newsclient.omxgroup.com/cdsPublic/viewDisclosure.action?disclosureId=512398&lang=fi/ (accessed on 9 January 2013).

- Metla (2102) Metsätilastotiedote, Puupelletit 2011, Metsäntutkimuslaitos, Metsätilastollinen tietopalvelu (in Finnish). Available online: http://www.metla.fi/metinfo/tilasto/julkaisut/mtt/2012/puupelletit11.pdf (accessed on 9 January 2013).

- Agar, D.; Wihersaari, M. Torrefaction technology for solid fuel production. Glob. Change Biol. Bioenergy 2012, 4, 475–478. [Google Scholar] [CrossRef]

- Kallio, A.M.I.; Anttila, P.; McCormick, M.; Asikainen, A. Are the Finnish targets for the energy use of forest chips realistic—Assessment with a spatial market model. J. For. Econ. 2011, 17, 110–126. [Google Scholar]

- Vamvuka, D. Bio-oil, solid and gaseous biofuels from biomass pyrolysis processes—An overview. Int. J. Energy Res. 2011, 35, 835–862. [Google Scholar] [CrossRef]

- Ihalainen, T.; Niskanen, A. Kustannustekijöiden vaikutukset bioenergian tuotannon arvoketjuissa (in Finnish). In Working Papers of the Finnish Forest Research Institute 166; Vantaa, Finland,, 2010. [Google Scholar]

- Kärhä, K. Industrial supply chains and production machinery of forest chips in Finland. Biomass Bioenergy 2011, 35, 3404–3413. [Google Scholar] [CrossRef]

- Petty, A.; Kärhä, K. Effects of subsidies on the profitability of energy wood production of wood chips from early thinnings in Finland. For. Policy Econ. 2011, 13, 575–581. [Google Scholar] [CrossRef]

- Noldin, J.H., Jr. Energy Efficiency and CO2 Reduction in the Brazil Steel Industry. In MetecInSteelCon 2011. In Proceedings of 1st International Conference on Energy Efficiency and CO2 Reduction in the Steel Industry, Düsseldorf, Germany, 27 June–1 July 2011.

- Shackley, S.; Hammond, J.; Gaunt, J.; Ibarrola, R. The feasibility and costs of biochar deployment in the UK. Carbon Manag. 2011, 2, 335–356. [Google Scholar] [CrossRef]

- Brown, T.R.; Wright, M.M.; Brown, R.C. Estimating profitability of two biochar production scenarios: Slow pyrolysis vs. fast pyrolysis. Biofuels Bioprod. Biorefin. 2011, 5, 54–68. [Google Scholar] [CrossRef]

- Larsson, M. Process Integration in the Steel Industry. Ph.D. Dissertation, Division of Energy Engineering, Department of Applied Physics and Mechanical Engineering, Luleå University of Technology, Luleå, Sweden, 2004. [Google Scholar]

- Salo, A. Masuuni-injektanttien viskositeettimittaukset (in Finnish). MSc Thesis, University of Oulu, Oulu, Finland, 2012. [Google Scholar]

- European Commission 2011/278/EU. Commission Decision of 27 April 2011 determining transitional Union-wide rules for harmonised free allocation of emission allowances pursuant to Article 10a of Directive 2003/87/EC of the European Parliament and of the Council. Off. J. Eur. Union. 2011. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:130:0001:0045:EN:PDF (accessed on 1 March 2013).

- European Commission No 601/2012. Commission regulation of 21 June 2012 on the monitoring and reporting of greenhouse gas emissions pursuant to Directive 2003/87/EC of the European Parliament and of the Council. Off. J. Eur. Union 2012. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2012:181:0030:0104:EN:PDF (accessed on 1 March 2013).

- Riesbeck, J.; Larsson, M. A System Analysis of Alternative Energy Carriers and Its Potential for Greenhouse Gas Emission Mitigation. In Proceedings of 4th International Conference on Process Development in Iron and Steelmaking (SCANMET IV), Luleå, Sweden, 10–13 June 2012.

- Wang, C.; Nilsson, L.; Larsson, M.; Bodén, A.; Sundqvist, L.; Wikström, J.O. Alternative Fuels Injection to BF and Their Impacts to the Integrated Steel Works. In Proceedings of 4th International Conference on Process Development in Iron and Steelmaking(SCANMET IV), Luleå, Sweden, 10–13 June 2012.

- Helle, H.; Helle, M.; Saxén, H.; Pettersson, F. Mathematical optimization of ironmaking with biomass as auxiliary reductant in the blast furnace. ISIJ Int. 2009, 49, 1316–1324. [Google Scholar] [CrossRef]

- BP Statistical Review of World Energy June 2012. Available online: http://www.bp.com/assets/bp_internet/globalbp/globalbp_uk_english/reports_and_publications/statistical_energy_review_2011/STAGING/local_assets/pdf/statistical_review_of_world_energy_full_report_2012.pdf (accessed on 28 January 2013).

- Steelonthenet, Metallurgical coke prices—Europe 2008–2012, Steelmaking input costs: Blast furnace raw materials. Available online: http://www.steelonthenet.com/files/blast-furnace-coke.html/ (accessed on 17 September 2012).

- Tsupari, E.; Kärki, J.; Arasto, A.; Pisilä, E. Post-combustion capture of CO2 at an integrated steel mill—Part II: Economic feasibility. Int. J. Greenhouse Gas Control. 2012, in press. Available online: http://dx.doi.org/10.1016/j.ijggc.2012.08.017/ (accessed on 15 January 2013). [Google Scholar]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Suopajärvi, H.; Fabritius, T. Towards More Sustainable Ironmaking—An Analysis of Energy Wood Availability in Finland and the Economics of Charcoal Production. Sustainability 2013, 5, 1188-1207. https://doi.org/10.3390/su5031188

Suopajärvi H, Fabritius T. Towards More Sustainable Ironmaking—An Analysis of Energy Wood Availability in Finland and the Economics of Charcoal Production. Sustainability. 2013; 5(3):1188-1207. https://doi.org/10.3390/su5031188

Chicago/Turabian StyleSuopajärvi, Hannu, and Timo Fabritius. 2013. "Towards More Sustainable Ironmaking—An Analysis of Energy Wood Availability in Finland and the Economics of Charcoal Production" Sustainability 5, no. 3: 1188-1207. https://doi.org/10.3390/su5031188

APA StyleSuopajärvi, H., & Fabritius, T. (2013). Towards More Sustainable Ironmaking—An Analysis of Energy Wood Availability in Finland and the Economics of Charcoal Production. Sustainability, 5(3), 1188-1207. https://doi.org/10.3390/su5031188