Corporate Social Responsibility, the Atmospheric Environment, and Technological Innovation Investment

Abstract

1. Introduction

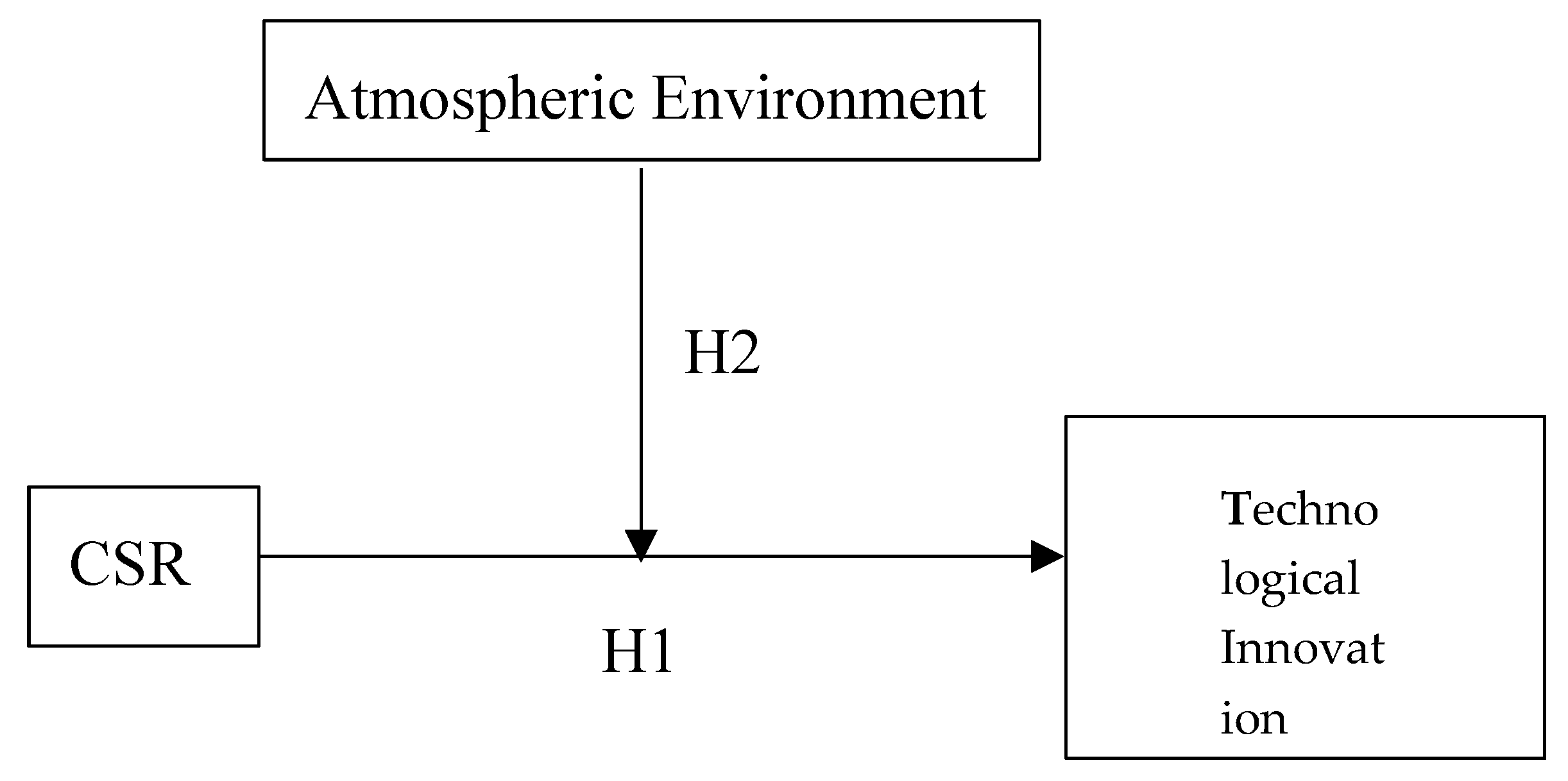

2. Theoretical Background and Hypotheses

2.1. The Relationship Between CSR and Technological Innovation Investment

2.2. The Regulatory Role of the Atmospheric Environment on the Relationship Between CSR and Technological Innovation Investment

3. Data, Variables, and Methodology

3.1. Data

3.2. Variables

3.2.1. Technological Innovation Investment

3.2.2. CSR

3.2.3. Atmospheric Environment

3.2.4. Control Variables

3.3. Methodology

4. Results and Discussion

4.1. Variable Descriptive Analysis

4.2. Correlation Analysis

4.3. Empirical Statistical Results

4.3.1. The Relationship Between CSR and Technological Innovation Investment

4.3.2. Influence of the Atmospheric Environment on CSR and Technological Innovation Investment

4.4. Robustness Examination

4.5. Discussion of Statistical Results

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Wang, Y.; Li, Y.X.; Ma, Z.; Song, J.B. Media attention, environmental regulation and corporate environmental protection investment. Nankai Manag. Rev. 2017, 20, 83–94. [Google Scholar]

- Jia, X.P.; Liu, Y. External Environment, Internal Resources and Corporate Social Responsibility. Nankai Manag. Rev. 2014, 17, 13–18. [Google Scholar]

- Flammer, C. Does product market competition foster corporate social responsibility? Strateg. Manag. J. 2015, 36, 1469–1485. [Google Scholar] [CrossRef]

- Zhai, L.Z.; Wang, L.; Liu, Y. Research on the Influence of External Environmental Factors on the Social Responsibility of Small Enterprises. Soft Sci. 2016, 30, 69–73. [Google Scholar] [CrossRef]

- Testa, F.; Gusmerottia, N.M.; Corsini, F.; Passetti, E.; Iraldo, F. Factors Affecting Environmental Management by Small and Micro Firms: The Importance of Entrepreneurs’ Attitudes and Environmental Investment. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 373–385. [Google Scholar] [CrossRef]

- Espinoza, M.J.P.; Carrion, C.E.; Mocha, B.P. Corporate social responsibility and environmentalapproach: A sustainable vision to the future. Rev. Univ. Y Soc. 2016, 8, 169–178. [Google Scholar]

- Li, H.Z.; Zeng, E.Y.; You, J. Mitigating pesticide pollution in China requires law enforcement, farmer training, and technological innovation. Environ. Toxicol. Chem. 2014, 33, 963–971. [Google Scholar] [CrossRef] [PubMed]

- Flammer, C. Does Corporate Social Responsibility Lead to Superior Financial Performance? A Regression Discontinuity Approach. Manag. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef]

- Petrenko, O. Corporate social responsibility or CEO narcissism? CSR motivations and organizational performance. Strateg. Manag. J. 2016, 37, 262–279. [Google Scholar] [CrossRef]

- Korschun, D. Corporate Social Responsibility, Customer Orientation, and the Job Performance of Frontline Employees. J. Mark. 2014, 78, 20–37. [Google Scholar] [CrossRef]

- Tang, Y. How CEO hubris affects corporate social (ir)responsibility. Strateg. Manag. J. 2015, 36, 1338–1357. [Google Scholar] [CrossRef]

- González-Ramos, M.; Donate, M.J.; Guadamillas, F. An empirical study on the link between corporate social responsibility and innovation in environmentally sensitive industries. Eur. J. Int. Manag. 2018, 12, 402–422. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Sofian, S.; Saeidi, P. How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. J. Bus. Res. 2015, 68, 341–350. [Google Scholar] [CrossRef]

- Jaklic, M.; Cerne, M.; Skerlavaj, M. Management innovation enters the game: Re-considering the link between technological innovation and financial performance. Innovation 2015, 17, 429–449. [Google Scholar] [CrossRef]

- Coccia, M. Sources of technological innovation: Radical and incremental innovation problem-driven to support competitive advantage of firms. Technol. Anal. Strateg. Manag. 2017, 29, 1048–1061. [Google Scholar] [CrossRef]

- Fuentes-Blasco, M.; Moliner-Velazquez, B.; Servera-Frances, D.; Gil-Saura, I. Role of marketing and technological innovation on store equity, satisfaction and word-of-mouth in retailing. J. Prod. Brand Manag. 2017, 26, 650–666. [Google Scholar] [CrossRef]

- Oginni, O.S.; Omojowo, A.D. Sustainable Development and Corporate Social Responsibility in Sub-Saharan Africa: Evidence from Industries in Cameroon. Economies 2016, 4, 10. [Google Scholar] [CrossRef]

- Clarkson, M.E. A Stakeholder Framework for Analyzing and Evaluating Corporate Social Performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Jia, X.P.; Liu, Y.; Liao, Y.H. Stakeholder pressure, corporate social responsibility and corporate value. Chin. J. Manag. 2016, 13, 267. [Google Scholar] [CrossRef]

- Laforet, S. Organizational innovation outcomes in SMEs: Effects of age, size, and sector. J. World Bus. 2013, 48, 490–502. [Google Scholar] [CrossRef]

- Cavallo, E.; Ferrari, E.; Bollani, L.; Coccia, M. Strategic management implications for the adoption of technological innovations in agricultural tractor: The role of scale factors and environmental attitude. Technol. Anal. Strateg. Manag. 2014, 26, 765–779. [Google Scholar] [CrossRef]

- Santana, N.B.; Rebelatto, D.A.D.; Perico, A.; Moralles, H.F.; Leal, W. Technological innovation for sustainable development: An analysis of different types of impacts for countries in the BRICS and G7 groups. Int. J. Sustain. Dev. World Ecol. 2015, 22, 425–436. [Google Scholar] [CrossRef]

- Michael, E.P.; Claas, V.D.L. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar]

- Gallego-Álvarez, I.; Prado-Lorenzo, J.M.; García-Sánchez, I.-M. Corporate social responsibility and innovation: A resource-based theory. Manag. Decis. 2011, 49, 1709–1727. [Google Scholar] [CrossRef]

- Rachel, B.; Christian, L.B.; Caroline, M.; Nicolas, P. Are firms with different CSR profiles equally innovative? An empirical analysis with survey data. Eur. Manag. J. 2013, 31, 642–654. [Google Scholar] [CrossRef]

- Maria, G.R.; Mario, D.; Maria, F.G.R. Technological Posture and Corporate Social Responsibility: Effects on Innovation Performance. Environ. Eng. Manag. J. 2014, 13, 2497–2505. [Google Scholar]

- Brammer, S.; Millington, A. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar] [CrossRef]

- Clark, J.M. The Changing Basis of Economic Responsibility. J. Polit. Econ. 1916, 24, 209–229. [Google Scholar] [CrossRef]

- Jiang, W.Y.; Wong, J.K.W. Key activity areas of corporate social responsibility (CSR) in the construction industry: A study of China. J. Clean. Prod. 2016, 113, 850–860. [Google Scholar] [CrossRef]

- Yuan, B.L.; Ren, S.G.; Hu, X.; Yang, X.Y. The Difference Effect of Environmental Regulation on Two Stages of Technology Innovation in China’s Manufacturing Industry. Front. Eng. Manag. 2016, 3, 24–29. [Google Scholar] [CrossRef]

- Costantini, V.; Mazzanti, M. On the green and innovative side of trade competitiveness? The impact of environmental policies and innovation on EU exports. Res. Policy 2012, 41, 132–153. [Google Scholar] [CrossRef]

- Kneller, R.; Manderson, E. Environmental regulations and innovation activity in UK manufacturing industries. Resour. Energy Econ. 2012, 34, 211–235. [Google Scholar] [CrossRef]

- Sen, S. Corporate governance, environmental regulations, and technological change. Eur. Econ. Rev. 2015, 80, 36–61. [Google Scholar] [CrossRef]

- Yuan, B.L. Does the “unlocking” of the system and technology drive the green development of China’s manufacturing industry? China Popul. Resour. Environ. 2018, 28, 117–127. [Google Scholar] [CrossRef]

- Zhang, C.Y.; Lv, Y. Green Production Regulation and Enterprise R&D Innovation—Influence and Mechanism Research. Econ. Manag. 2018, 40, 71–91. [Google Scholar] [CrossRef]

- Borger, F.G.; Kruglianskas, I. Corporate social responsibility and environmental and technological innovation performance: Case studies of Brazilian companies. Int. J. Technol. Policy Manag. 2006, 6, 399–412. [Google Scholar] [CrossRef]

- Frank, M.; Robert, S.; Ram, N. An examination of corporate reporting, environmental management practices and firm performance. J. Oper. Manag. 2007, 25, 998–1014. [Google Scholar] [CrossRef]

- Aguilera-Caracuel, J.; Guerrero-Villegas, J. How Corporate Social Responsibility Helps MNEs to Improve their Reputation. The Moderating Effects of Geographical Diversification and Operating in Developing Regions. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 355–372. [Google Scholar] [CrossRef]

- Stefano, F.; Eugenio, D.; Daniela, C.; Silvia, S. Does environmental performance affect companies’ environmental disclosure? Meas. Bus. Excell. 2015, 19, 42–57. [Google Scholar] [CrossRef]

- Ju, S.; Chung, M.S. Evaluation of corporate social responsibility activities for fashion company’s sustainable management: On the moderating effects of consumers’ perceived fit and motivation. Res. J. Costume Cult. 2015, 23, 644–660. [Google Scholar] [CrossRef]

- Jaffe, A.B.; Robert, N.S. Dynamic Incentives of Environmental Regulations: The Effects of Alternative Policy Instruments on Technology Diffusion. J. Environ. Econ. Manag. 1995, 29, S43–S63. [Google Scholar] [CrossRef]

- Zhang, P.; Zhang, P.P.; Cai, G.Q. Comparative Study on the Impact of Different Types of Environmental Regulation on Enterprises’ Technological Innovation. China Popul. Resour. Environ. 2016, 26, 8–13. [Google Scholar] [CrossRef] [PubMed]

- Cao, Y.H.; You, J.X. The contribution of environmental regulation to technological innovation and quality competitiveness an empirical study based on Chinese manufacturing enterprises. Chin. Manag. Stud. 2017, 11, 51–71. [Google Scholar] [CrossRef]

- Duan, W.; Jiang, T.W.; Zhang, J.Y.; Wang, G.L. Research on the Evaluation of Technological Innovation Development of Regional Enterprises—Analysis of the Evaluation Index System of Technological Innovation of Zhejiang Province, 11 Districts and Cities and Enterprises. China Soft Sci. 2014, 5, 85–96. [Google Scholar]

- Wang, Q.G.; Xu, X.Y. The Value Creation Mechanism and Empirical Test of Corporate Social Responsibility—Based on Stakeholder Theory and Life Cycle Theory. China Soft Sci. 2016, 2, 179–192. [Google Scholar]

- Lin, X.Q.; Wang, D. Temporal and spatial evolution characteristics and socio-economic driving forces of urban air quality in China. J. Geogr. Sci. 2016, 26, 1533–1549. [Google Scholar] [CrossRef]

- Halme, M.; Korpela, M. Responsible Innovation toward Sustainable Development in Small and Medium-Sized Enterprises: A Resource Perspective. Bus. Strategy Environ. 2014, 23, 547–566. [Google Scholar] [CrossRef]

- Huang, W.; Chen, W. Foreign capital entry, supply chain pressure and Chinese CSR. Manag. World 2015, 2, 91–100. [Google Scholar]

- Yu, L.C.; Zhang, W.G.; Bi, Q. Research on the Innovation Effect of Environmental Tax. J. Yunnan Univ. Financ. Econ. 2018, 34, 78–90. [Google Scholar] [CrossRef]

- Jimenez-Parra, B.; Alonso-Martinez, D.; Godos-Diez, J.L. The influence of corporate social responsibility on air pollution: Analysis of environmental regulation and eco-innovation effects. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1363–1375. [Google Scholar] [CrossRef]

- Li, D.; Cao, C.; Zhang, L.; Chen, X.; Ren, S.; Zhao, Y. Effects of corporate environmental responsibility on financial performance: The moderating role of government regulation and organizational slack. J. Clean. Prod. 2017, 166, 1323–1334. [Google Scholar] [CrossRef]

- Shin, J.Y.; Jung, M.; Khoe, K.I.; Chae, M.S. Effects of Government Involvement in Corporate Social Responsibility: An Analysis of the Indian Companies Act, 2013. Emerg. Mark. Financ. Trade 2015, 51, 377–390. [Google Scholar] [CrossRef]

- Liang, H.; Renneboog, L. On the foundations of corporate social responsibility. J. Financ. 2017, 72, 853–910. [Google Scholar] [CrossRef]

- Park, B.I.; Ghauri, P.N. Determinants influencing CSR practices in small and medium sized MNE subsidiaries: A stakeholder perspective. J. World Bus. 2015, 50, 192–204. [Google Scholar] [CrossRef]

- Vashchenko, M. An external perspective on CSR: What matters and what does not? Bus. Ethics Eur. Rev. 2017, 26, 396–412. [Google Scholar] [CrossRef]

- Qi, G.Y.; Zeng, S.X.; Tam, C.M.; Yin, H.T.; Zou, H.L. Stakeholders’ Influences on Corporate Green Innovation Strategy: A Case Study of Manufacturing Firms in China. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 1–14. [Google Scholar] [CrossRef]

{kind=link}

| Variable | N | Max | Min | Mean | Median | sd |

|---|---|---|---|---|---|---|

| Inno | 2316 | 12762.1 | 0.0047 | 178.799 | 52.489 | 460345.247 |

| CSR | 2316 | 87.25 | −18.18 | 27.23 | 22.52 | 309.009 |

| Envi | 2316 | 363.0 | 196.0 | 279.186 | 283.0 | 2493.237 |

| DAR | 2316 | 1.003 | 0.017 | 0.386 | 0.368 | 0.038 |

| ROE | 2316 | 0.741 | −2.474 | 0.082 | 0.07675 | 0.012 |

| STATE | 2316 | 1 | 0 | 0.28 | 0.00 | 0.201 |

| Industry | N | Mean | Max | Min | Median |

|---|---|---|---|---|---|

| Mining industry | 32 | 103.39 | 644 | 0.471 | 45.933 |

| Electricity, heat, gas, water production and supply industry | 21 | 16.558 | 96.505 | 0.21 | 10.28 |

| Real estate industry | 9 | 16.306 | 50.516 | 2.181 | 12.747 |

| Construction industry | 52 | 1047.55 | 10592.471 | 2.983 | 83.74 |

| Transport, warehousing and postal industries | 24 | 18.589 | 73.159 | 0.684 | 8.354 |

| Education | 1 | 22.1114 | 22.1114 | 22.1114 | 22.1114 |

| Agriculture, forestry, animal husbandry and fishery industries | 20 | 31.2 | 223.792 | 1.262 | 16.263 |

| Wholesale and retailing industry | 33 | 53.645 | 386.098 | 0.598 | 32.757 |

| Water resources, environment and public facilities industries | 15 | 39.557 | 75.432 | 16.01 | 42.59 |

| Public health and social work | 2 | 72.28 | 102.7 | 41.86 | 72.28 |

| Cultural, sports and recreational industries | 17 | 88.08 | 613.611 | 1.484 | 35.585 |

| Information transfer, and software and information technology service industry | 138 | 121.89 | 1351.275 | 0.018 | 69.214 |

| Manufacturing industry | 1235 | 128.882 | 12762.1 | 0.405 | 49.355 |

| Comprehension | 8 | 35.011 | 117.891 | 5.481 | 20.538 |

| Leasing and commercial service industry | 15 | 32.38 | 229 | 2.852 | 12.637 |

| total | 2316 | 178.799 | 12762.1 | 0.0047 | 52.489 |

| Industry | N | Mean | Max | Min | Median |

|---|---|---|---|---|---|

| Mining industry | 32 | 103.39 | 644 | 0.471 | 45.933 |

| Electricity, heat, gas, water production and supply industry | 21 | 16.558 | 96.505 | 0.21 | 10.28 |

| Real estate industry | 9 | 16.306 | 50.516 | 2.181 | 12.747 |

| Construction industry | 52 | 1047.55 | 10592.471 | 2.983 | 83.74 |

| Transport, warehousing and postal industries | 24 | 18.589 | 73.159 | 0.684 | 8.354 |

| Education | 1 | 22.1114 | 22.1114 | 22.1114 | 22.1114 |

| Agriculture, forestry, animal husbandry and fishery industries | 20 | 31.2 | 223.792 | 1.262 | 16.263 |

| Wholesale and retailing industry | 33 | 53.645 | 386.098 | 0.598 | 32.757 |

| Water resources, environment and public facilities industries | 15 | 39.557 | 75.432 | 16.01 | 42.59 |

| Public health and social work | 2 | 72.28 | 102.7 | 41.86 | 72.28 |

| Cultural, sports and recreational industries | 17 | 88.08 | 613.611 | 1.484 | 35.585 |

| Information transfer, and software and information technology service industry | 138 | 121.89 | 1351.275 | 0.018 | 69.214 |

| Manufacturing industry | 1235 | 128.882 | 12762.1 | 0.405 | 49.355 |

| Comprehension | 8 | 35.011 | 117.891 | 5.481 | 20.538 |

| Leasing and commercial service industry | 15 | 32.38 | 229 | 2.852 | 12.637 |

| total | 2316 | 178.799 | 12762.1 | 0.0047 | 52.489 |

| Inno | CSR | Envi | DAR | ROE | STATE | |

|---|---|---|---|---|---|---|

| Inno | 0.183 *** | −0.053 ** | 0.267 *** | 0.138 *** | 0.13 *** | |

| CSR | 0.102 *** | 0.013 | −0.078 *** | 0.496 *** | 0.064 *** | |

| Envi | −0.079 *** | −0.004 | −0.034 | 0.042 *** | −0.115 *** | |

| DAR | 0.215 *** | 0.028 | −0.04 | −0.097 *** | 0.328 *** | |

| ROE | 0.038 | 0.242 *** | 0.022 | −0.122 *** | −0.157 *** | |

| STATE | 0.145 *** | 0.151 *** | −0.115 *** | 0.341 *** | −0.135 *** |

| Independent Variable | Technological Innovation Investment | |

|---|---|---|

| CSR | 2.793 *** | (3.422) |

| DAR | 668.792 *** | (8.993) |

| ROE | 330.766 *** | (2.563) |

| STATE | 114.750 *** | (3.461) |

| Constant term | −214.438 *** | (−5.712) |

| N | 2316 | |

| R2 | 0.062 | |

| F | 38.185 | |

| Independent Variable | Good Atmospheric Environment | Poor Atmospheric Environment | ||

|---|---|---|---|---|

| CSR | 2.811 *** | (3.183) | 2.427 * | (1.788) |

| DAR | 485.985 *** | (5.948) | 814.528 *** | (6.705) |

| ROE | 87.194 | (0.677) | 646.512 *** | (2.754) |

| STATE | −4.875 | (0.898) | 186.787 *** | (3.517) |

| Constant term | −126.447 *** | (−3.037) | −282.699 *** | (−4.67) |

| N | 1130 | 1186 | ||

| R2 | 0.042 | 0.08 | ||

| F | 12.288 | 25.575 | ||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, G.; Zhang, L.; Zhang, L. Corporate Social Responsibility, the Atmospheric Environment, and Technological Innovation Investment. Sustainability 2019, 11, 481. https://doi.org/10.3390/su11020481

Zhou G, Zhang L, Zhang L. Corporate Social Responsibility, the Atmospheric Environment, and Technological Innovation Investment. Sustainability. 2019; 11(2):481. https://doi.org/10.3390/su11020481

Chicago/Turabian StyleZhou, Guichuan, Lan Zhang, and Liming Zhang. 2019. "Corporate Social Responsibility, the Atmospheric Environment, and Technological Innovation Investment" Sustainability 11, no. 2: 481. https://doi.org/10.3390/su11020481

APA StyleZhou, G., Zhang, L., & Zhang, L. (2019). Corporate Social Responsibility, the Atmospheric Environment, and Technological Innovation Investment. Sustainability, 11(2), 481. https://doi.org/10.3390/su11020481