Evaluating the Quality of Enterprise Environmental Accounting Information Disclosure

School of Business Administration, China University of Petroleum-Beijing, Beijing 102249, China

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(7), 2136; https://doi.org/10.3390/su10072136

Submission received: 18 May 2018

/

Revised: 17 June 2018

/

Accepted: 19 June 2018

/

Published: 22 June 2018

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:To grasp the overall disclosure of the quality of enterprise environmental accounting information and find the weakness of disclosure for precise improvements, an approach for the evaluation for the quality of enterprise environmental accounting information disclosure was proposed. First, the evaluation index system of enterprise environmental accounting information disclosure quality was constructed from three aspects: relevance, reliability, and compliance. Relevance measured whether the relevant information was disclosed comprehensively; reliability checked whether the disclosed information was in accordance with the reality; and compliance assessed whether the disclosed information complied with the laws and regulations. Considering that the ratings derived from multiple appraisers with respect to the evaluation index were in linguistic forms, the aggregation method based on triangular fuzzy numbers was constructed. The consistency of ratings was used to calculate the weight of appraisers for the deduction of personal bias and a case study verified the feasibility and practicality of the proposed approach. The approach not only was applied to the assessment of the company, but also provided some suggestions based on the evaluation results.

1. Introduction

Sustainability is an important issue for both business and society [1] and environment protection is critical for sustainability [2]. Continuous investments in energy consumption and natural resource consumption as well as manufacturing sectors and infrastructure have had seriously harmful impacts on the environment. Disclosure of enterprise environmental accounting information can promote the regulation of corporate environmental behaviors [3]. The disclosure forces managers to make sustainable decisions that take environmental and social considerations into account [4] and promotes enterprises to formulate effective environmental protection and business strategies to reduce the obstacles caused by environmental problems.

By disclosing accounting information related to environmental protection, the environmental protection department can master the overall situation of the environment and make an objective evaluation on the environmental contribution of the enterprise. Disclosure affects managers’ reputation and social profile [5] and will help the public and investors make the right investment decision.

Environmental accounting information includes financial, environmental performance, and policy aspects [6], which are scattered in many parts of annual reports and social responsibility reports. The quality of disclosures can be characterized from aspects of comprehensiveness, reliability, and compliance [7,8,9,10]. High-quality disclosure of environmental accounting information is important, but there are fewer regulations on the disclosure of enterprise environmental accounting information [11]. It is not identical to compiling financial reports and the quality of the environmental accounting information disclosure is also different.

Next, the question of how to comprehensively evaluate the overall quality of environmental accounting information disclosure arises. With the evaluation results, the public, investors, and officials can grasp the overall quality of the disclosure of environmental accounting information. In addition, the strengths and weaknesses of the disclosure of the environmental accounting information can be found, which can then be improved precisely.

Many efforts have been made into the research of how to influence the disclosure of environmental accounting information. For example, the impact of France’s ‘Grenelle 2′ law of 2010, which applies to environmental accounting disclosures (EADs), has been analyzed [12]. CEO characteristics such as education and tenure also have an influence on the will to disclose environmental information [13]. Stakeholder theory is used to identify the determinant factors that affect the disclosure level of corporate environmental information [14]. The extent to which voluntary disclosure theory can explain the corporate disclosure of general and financial environmental information was studied in [15]. Disclosure of information on corporate environmental responsibility information has been modeled as a sequential game and a partial disclosure equilibrium was derived [16]. The influence of the disclosure of environmental accounting information has also been studied. It has been found that environmental information disclosure positively influenced economic performance as better discourse leads to better economic performance [17,18].

However, there is a lack of research on the quality evaluation of the disclosure of environmental accounting information. Without evaluation, the weaknesses of the disclosure cannot be found, and improvements cannot be made accurately. At the same time, the quality of the disclosure cannot be mastered directly.

To resolve this question, in this paper, an approach to the quality evaluation of enterprise environmental accounting information disclosure was proposed. First, the evaluation index system was established from the aspects of relevance, reliability, and compliance. Financial indexes and environmental performance indexes were included in the evaluation index system. Moreover, the generation environment of environmental accounting information and the authentication and supervision of the disclosed information by external parties were considered. Then, more than one appraisers were invited to rate the company with respect to the evaluation indexes. Since the ratings were given by multiple appraisers with linguistic terms, triangular fuzzy numbers were used to model the linguistic rating, and the corresponding method was proposed to aggregate these ratings. To reduce the personal bias, the consistency of ratings was used to weight the appraisers. Finally, a case study was constructed to verify the feasibility and practicality of the proposed approach.

The rest of the paper is organized as follows. The following section proposes the evaluation index system along with the corresponding illustrations. The method to aggregate and deal with the linguistic rating is given in Section 3. The case study is provided in Section 4. Our conclusions and future research directions are discussed in Section 5.

2. Evaluation Index System of Quality of Enterprise Environmental Accounting Information Disclosure

The purpose of evaluating the quality of the disclosure of enterprise environmental accounting information is to measure whether the disclosed environmental accounting information is reliable, comprehensive, and conforms to the laws and regulations.

According to the results in the existing research [7,8,9,10,19,20,21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38], the index system was constructed, which is shown in Table 1. In the evaluation index system, both the disclosure of environmental performance information [7] and the financial information [8] of the enterprise were considered. At the same time, the environment of information generation [9] and compliance with relevant laws and regulations [10] were also considered. The whole index system included three aspects: relevance, reliability, and compliance. The relevance index was used to measure whether the disclosed information of environment was related to the financial situation, business performance, and development prospects of enterprises [20]. The reliability index was to check whether the information was disclosed by the enterprise according to the actual events [20]. The compliance index refers to whether the accounting activities and disclosure scope of enterprises complied with the laws and regulations [21].

(1) Financial standing

This index mainly refers to the extent of the disclosure of sources and destination of funds used for the environment. It includes the total investment in environmental protection [22], the liabilities due to environmental problems [24], and the disclosure of facilities and technologies for environmental protection [23] owned by the enterprises. The disclosure of the information helps master the overall situation of the enterprise regarding environmental protection and reflects how much importance the enterprise attaches to environment protection.

(2) Operating results

This index is about the disclosure of information on the results and costs in the field of the environment over a certain period. It includes the income related to environmental protection [27], government subsidies [22], expenditures of environmental protection departments [25], litigation expenses and fines related to environment [26] as well as other related expenses such as afforestation fees [22]. Disclosure of the information reflects the enterprise’s environmental protection efforts.

(3) Information on environmental policy

This index reflects the disclosure of information on the environmental policies of enterprises. It includes the disclosure of environmental system certifications and the precautionary information such as clean production [28] together with the establishment and operation of environmental management systems [29]. The managers’ attitude to environmental protection can be obtained with the disclosed information.

(4) Pollution control

This index refers to the impact on the environment and the corresponding measures taken by the enterprises in the process of production and operation. It mainly includes the information disclosure of the pollutants standardized discharge [30], pollutants recycling such as exhaust gases [30], resource consumption and reduction measures [29]. Disclosure of the information shows the achievements of the enterprises in pollution control and urges enterprises to better control pollutant discharge.

(5) Company structure

This index indicates whether the internal structure of the enterprise is sound. It includes the health degree of the governance structure of the enterprise [31], the corporate audit committee, its performance [32] and so on, which directly affects the reliability of the information disclosed by the enterprise. If the corporate governance structure is perfect with the audit committee performing well, the information disclosed is reliable.

(6) Regulatory situation

What the index reveals are the external organizations’ supervision and inspection of information disclosed by the enterprises. It includes the supervision of enterprises from financial enforcement together with industrial, commercial, and tax enforcement as well as the Securities Regulatory Commission and Stock Exchanges [33]. The supervision of enterprises by these institutions increases the cost of providing low-quality accounting information to enterprises [33], which helps urge enterprises to disclose high-quality information. If the enterprise is not punished for these reasons, the reliability of the environmental accounting information disclosed by the enterprise will be much higher.

(7) External authentication

This index includes enterprise annual reports, environmental information audit opinions [34], and audits of the enterprise internal control system and its implementation [35]. We evaluated the reliability of the environmental accounting information disclosed by enterprises based on the audit opinions issued by accounting firms.

(8) Timeliness

What this index reveals is the timeliness of the information disclosure, i.e., whether the disclosures of financial reports and related reports [36] and major announcements [37] are timely. If the enterprise can disclose the environmental reports and information in time, it clarifies the specific situation of the environmental accounting information in time.

(9) Integrity

This index mainly evaluates whether the content and scope of enterprise disclosure, the accounting processes, and contents of financial information conform to the provisions of laws and regulations [38]. It emphasizes that the disclosure of financial information should comply with the accounting laws [21]. If the enterprise can completely account and disclose information according to the accounting laws, it will increase the degree of trust.

3. Evaluation Method Based on Triangular Fuzzy Numbers

From the evaluation index system, we can see that this is a judgment based on the disclosed information. It is difficult to give numeric values, and linguistic terms such as good, very good, and medium are more apt for the expression of opinions. Triangular fuzzy numbers are most commonly used to model linguistic terms where membership function is used to characterize the linguistic terms [39].

More than one appraiser was invited in the evaluation to reduce the subjectivity of the evaluation. To reduce the personal bias, the consistency of the evaluation information was used to measure the weight of the appraisers. There are two kinds of weight of appraisers. The first one is based on the evaluation of the importance of evaluation indexes. The other one is based on the evaluation of the company with respect to the evaluation index. It is based on the idea that appraisers who are familiar with the evaluation index may not be familiar with the disclosed information of the company [40].

The calculation processes are shown in Figure 1:

First, the weight of the appraiser for evaluating the importance of the index is calculated. Consistency of individual opinions with group opinions of appraisers is generally considered in the process of calculating the weight of appraisers. The closer the individual opinion of the appraiser to the opinion of the appraiser group, the more important weight should be given to the appraiser [41], as detailed in Steps 1 to 5.

Step 1: The linguistic evaluation information of index importance is converted into a triangular fuzzy set. For the appraisers’ linguistic evaluation terminology set for the importance of the index at the level, the linguistic term set is converted into a triangular fuzzy set , indicating the importance of the index, , , .

After transforming the evaluation results into triangular fuzzy numbers by Step 1, we calculated the first kind of weight of the appraiser based on the evaluation of the importance of the evaluation index. The specific process is from Step 2 to Step 5.

Step 2: Calculate the distance between the evaluation results (, ) of the two appraisers on the importance of the evaluation index [41]:

Step 3: Similarity between the appraiser and the appraiser in decision making under the same index is calculated [41].

Step 4: For the same index , calculate the average consistency of the appraiser for all appraisers to evaluate the importance of the evaluation index [41].

Step 5: Use the following formula to normalize and calculate the appraiser’s weight [41].

Similarly, Steps 1 to 5 can be used to calculate the second kind of weight of appraisers for evaluating the disclosure performance of the enterprise according to the evaluation index. The calculation process in this part is similar to the calculation in the first part. Consistency of the appraisers’ individual opinions with group opinions is also generally considered in the process of calculating the weight of appraisers. The closer the individual opinion of the appraiser to the opinion of the appraiser group, the more important weight should be given to the appraiser [41]. can be used to express the individual weight of the appraiser that considers the consistency of the appraisers’ individual opinions with group opinions. is used to express the evaluation value of the performance of a certain index of the enterprise.

After deriving the importance of the index and the evaluation value of the disclosure performance of the enterprise and integrating them with the corresponding weight of appraisers, the final evaluation results can be obtained. The specific calculation process is from Step 6 to Step 7.

Step 6: Determine the weighted importance of the index. For the same index , using the appraiser’s weight and the evaluation result to evaluate the importance of the index, the weighted average is calculated to obtain the weighted importance evaluation result of the index of the level.

According to the operation rule of triangular fuzzy numbers, we can obtain:

Step 7: Determine the expert-weighted evaluation value. For the same index , using the appraiser’s weight and the evaluation result to evaluate the performance of the enterprise of the index, the weighted average is calculated to obtain the evaluation value’s weighted evaluation result of the index of the level.

According to the operation rule of triangular fuzzy numbers, we can obtain:

4. An Example of Quality Evaluation of Environmental Accounting Information Disclosure in Company A

Company A is a large-scale corporation with various business collections of explorations and mining of bauxite, coal, and other resources, alumina and aluminum alloy production, production sales, technology research and development, thermal power generation as well as new energy generation. It is state-owned under the direct supervision and management of the State-owned Assets Supervision and Administration Commission of the State Council. During the process of production, many pollutants such as waste water and waste gas are produced. Company A has been publishing social responsibility reports since 2006, which involves the disclosure of environmental accounting information. The company has a strong sense of responsibility and representativeness.

Company A employs more than 200,000 people. In 2016, the revenue was 144.066 billion yuan, revenue in 2015 was 123.475 billion yuan, and revenue in 2014 was 142.060 billion yuan. In 2016, the total assets of Company A were 19,077 million yuan. In 2015, the total assets were 19,025 million yuan. In 2014, the total assets were 194,822 million yuan. According to the annual reports of 2016, the working capital of Company A was negative. Its long-term and short-term solvency was rather poor, and the asset-liability ratio reached 70.76%. The net operating interest rate was only 0.87; the net income rate of equity was 2.26%; and the net income rate of total assets was 0.66%. In addition, the operating profit deducting the non-recurrent profit and loss was negative. The total assets turnover ratio was 75.40%. The turnover ratio of accounts receivable was 21.3, and the inventory turnover rate was 7.53. To conclude, we can see that the operating ability of company A is relatively good.

We studied the quality of environmental accounting information disclosure in Company A by using the above evaluation index system and method. The questionnaires included three parts. The first part collected the personal information of the appraisers including four questions focusing on department and position. The second part included 23 questions to evaluate the index’s importance of the enterprise environmental accounting information disclosure. The third part, which included 23 questions, was the enterprise environmental accounting information quality evaluation table. The purpose of the two parts was to collect the appraisers’ views on the importance of the index and evaluate Company A’s performance. A total of 22 valid questionnaires were collected whose participants were in financial, auditing, and environment-related fields. We analyzed the results, put forward the problems existing in Company A, and provide suggestions for improvements.

In this part, the environmental accounting information disclosure quality of Company A was evaluated. The calculated comprehensive evaluation results of the index of Company A were transformed into real numbers as its comprehensive evaluation value, and thus we analyzed the results of the quality evaluation of environmental accounting information disclosure in Company A. The higher the comprehensive evaluation value, the higher the quality of environmental accounting information disclosure.

First, the weight of the appraiser based on the importance of indexes was calculated, then the weight of the indexes was derived. Second, the weight of the appraiser based on the evaluation value of Company A was calculated, then the evaluation value of the evaluation indexes of Company A as obtained. Finally, Company A’s comprehensive evaluation value of the quality index of the environmental accounting information disclosure was obtained.

4.1. Evaluation Results of the Index Importance

The evaluation results of the index importance of the evaluation index system of the quality of the enterprise environmental accounting information disclosure are shown in Table 2. This part mainly analyzed the index importance of the enterprise accounting information disclosure quality, which was calculated from the importance evaluation index table of the enterprise environmental accounting information disclosure quality. To facilitate the comparative analysis of indexes, this part calculates the expected values representing the index importance, which were expressed in the form of triangular fuzzy numbers. The higher the number, the more important the index.

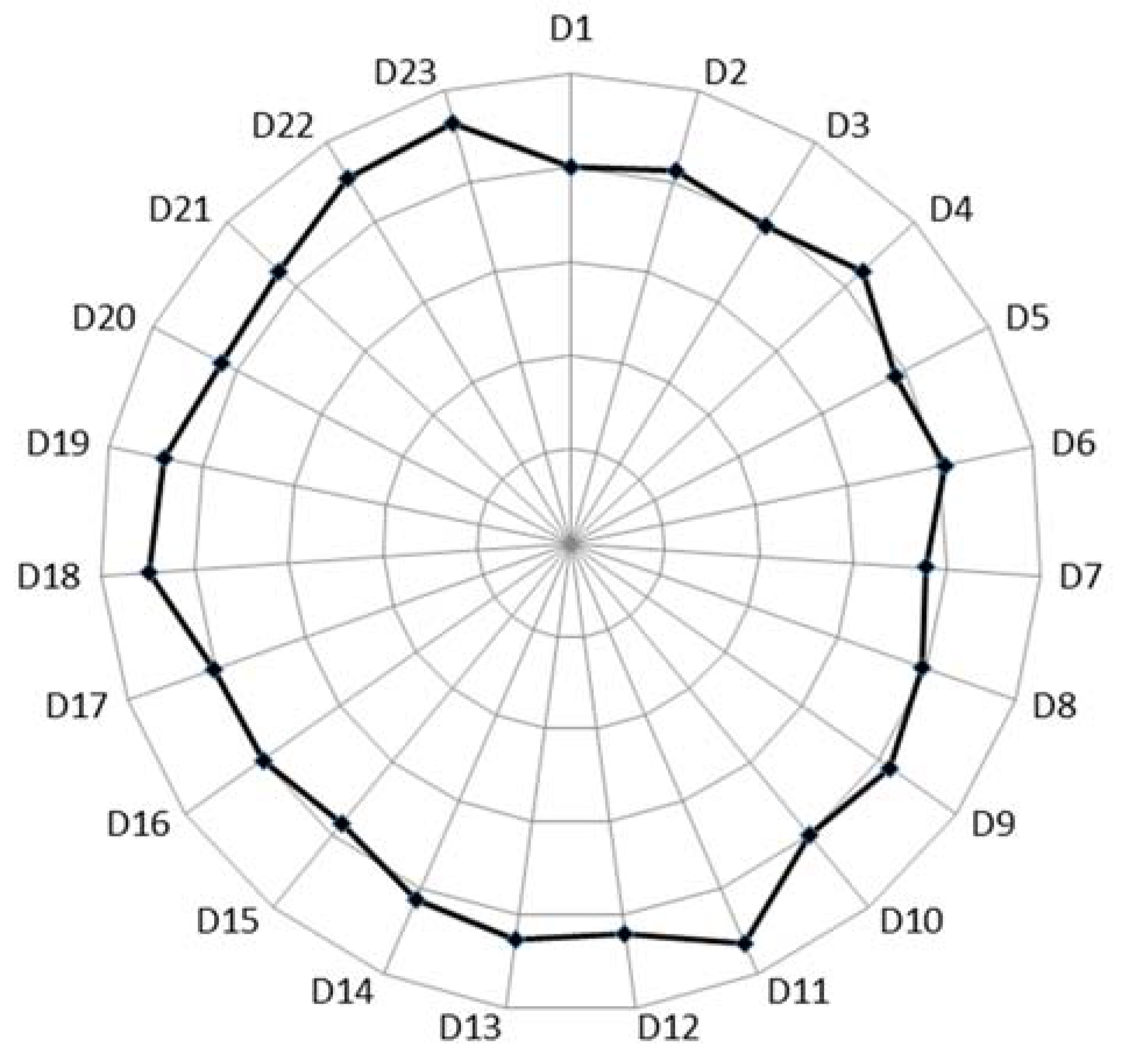

As shown in Table 2, the most important index was 0.8281, and the lowest was 0.6551 among the 23 indexes. There were three indexes above 0.8 and five indexes below 0.7. The remaining indexes were in the range of 0.7 to 0.8.

To compare the importance of each index, the radar image shown in Figure 2 was drawn.

The most important index was the integrity of the accounting processes and contents of financial information according to laws and regulations (D23). The second most important index was the disclosure of the pollutants standardized discharge (D11). The following was the integrity of the contents and scope of the disclosure according to laws and regulations (D22). The next was the enterprise annual reports and environmental information audit opinions (D18). The last was the enterprise internal control system and its implementation (D19). What the appraisers considered significant were (D23), (D22), (D18), and (D19) as they are related to the environment in which the enterprise generates information, and the quality of the environment directly affects the integrity and accuracy of the information generated by the enterprise. If the environment in which the enterprise generates information is poor, the environmental accounting information disclosed by the enterprise will be invalid. Detailed disclosure of the pollutant standardized discharge (D11) clarifies the direct environmental impact caused by the production and operation of the enterprise. This is conducive to the supervision of enterprises by the public.

In contrast, the least significant index was the disclosure of income related to environmental protection (D7). Other indexes that were not that significant included the corporate audit committee and its performance (D15), disclosure of litigation expenses and fines related to the environment (D5), disclosure of other environment-related expenditures (D8), along with disclosure of liabilities due to environmental problems (D3). Among the five indexes, four belonged to relativity, which led to the low importance of relativity. Disclosure of income related to the environmental protection (D7) was the least important, which showed that appraisers did not fully realize that if enterprises performed environmental protection work well, it would bring considerable income and perspective to the enterprises. Accordingly, the personnel concerned should transform ideas to raise environmental protection consciousness. The reason the corporate audit committee and its performance (D15) was considered unimportant was that it was difficult for external parties to fully understand the specific fulfillment of the responsibilities of accounting departments such as the corporate audit committee.

4.2. Results of the Quality Evaluation of the Environmental Accounting Information Disclosure in Company A

This part, based on the situation of Company A, analyzed the evaluation value of the environmental accounting information disclosure quality of Company A calculated according to the evaluation index table of enterprise environmental accounting information disclosure quality. Taking the same steps as the previous section, we transformed the calculated comprehensive evaluation results of the indexes of Company A into real numbers as its comprehensive evaluation value, and thus analyzed the results of the quality evaluation of the environmental accounting information disclosure of Company A. The higher the comprehensive evaluation value, the higher the quality of the environmental accounting information disclosure.

The comprehensive evaluation value of the evaluation index system of environmental accounting information disclosure quality in Company A is shown in Table 3.

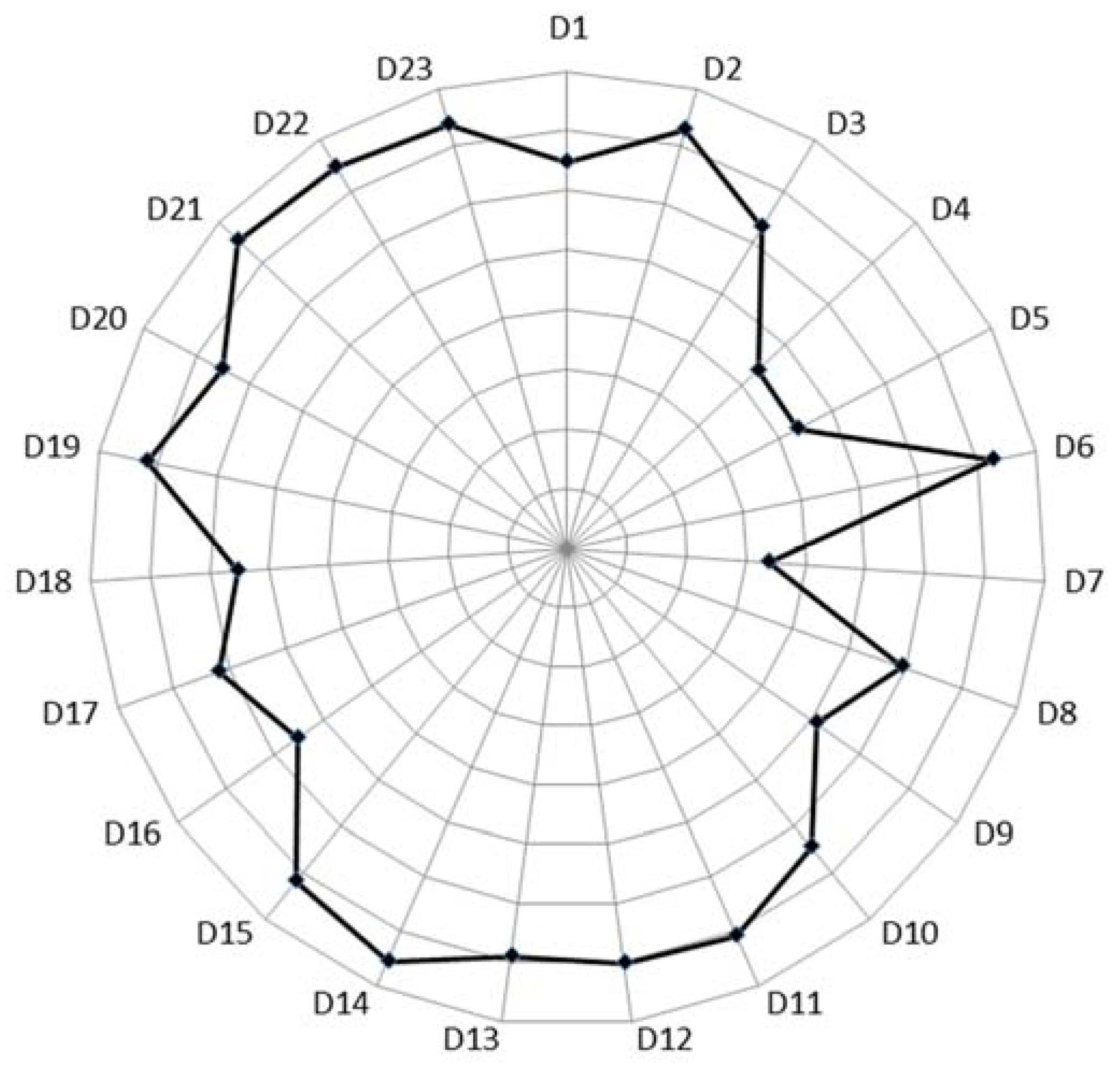

According to Table 3, the highest evaluation value of all the indexes was 0.7548 and the lowest was 0.3368. There were 10 indexes with an evaluation value above 0.7 and seven indexes with an evaluation value below 0.6. The remaining indexes were between 0.6 and 0.7.

To compare the comprehensive evaluation values of each index, the radar image shown in Figure 3 was drawn.

As clearly indicated by Figure 3, out of the 23 indexes, the one with the highest comprehensive evaluation value was the health degree of the governance structure of the enterprise (D14). This was followed by the timeliness of the disclosure of major announcements (D21). The third highest index was the integrity of the contents and scope of the disclosure according to laws and regulations (D22). The next was the integrity of the accounting processes and contents of financial information according to laws and regulations (D23). The last one was the disclosure of government subsidies related to the environment (D6). The reason the health degree of the governance structure of the enterprise (D14) was high is that according to the annual report of Company A, the corporate governance structure was sound, and the company was in good operation. Integrity of the contents and scope of the disclosure according to the laws and regulations (D22) and the integrity of the accounting processes and contents of financial information according to laws and regulations (D23) was high due mainly to the fact revealed by the CCER database that Company A had not violated any laws and regulations in the past five years and that their disclosure of major announcements was also timely. Disclosure of government subsidies related to the environment (D6) had a high value given the detailed disclosure in its annual report notes including the items, start quantity, and end quantity during each year of government subsidies and related accounting treatments. However, there is still room for improvement. Company A disclosed all the government subsidies it received, i.e., government subsidies related to the environmental protection were not disclosed separately. This information was disclosed in conjunction with other types of government subsidies, which requires unnecessary time and cost to extract certain information.

Indexes with relatively low comprehensive evaluation values were the disclosure of the expenditure of environmental protection departments in enterprises (D4), the disclosure of litigation expenses and fines related to the environment (D5), and the disclosure of income related to environmental protection (D7). The information was not even disclosed in its annual reports, which directly led to poor evaluation results. From the calculated index importance above, the importance of the disclosure of income related to the environmental protection (D7) was low, reflecting the weak awareness of its personnel in environmental protection. Company A should enhance its personnel’s awareness of the environmental protection through future training.

4.3. Suggestions

(1) Raise the environmental protection awareness

Company A should enhance the environmental awareness of its workforce, especially its top management so that the workforce realizes that the disclosure of the environmental accounting information is of great importance for both the external stakeholders and the enterprise itself. Specifically, Company A can organize relative training to raise staff awareness of environmental responsibilities.

(2) Establish and improve environmental management systems

Company A should establish and continuously improve its environmental protection system and emergency system. We suggest that Company A should attach more importance to the establishment of environmental management systems, set up the employment of full-time personnel related to environmental protection, and strive to pass the ISO certification. In addition, the environmental management system should be effectively implemented in the process of business operation, and the responsibility should be carried out by everyone in each department. By specifically implementing measures, the company can bring individual performance into departmental and individual performance evaluation and formulate a corresponding rewards and punishment system. Meanwhile, Company A should pay attention to the changes in environmental policies to adjust its systems in a timely manner.

(3) Disclose environmental accounting information separately

Under the current legal systems, there are no specific provisions for the disclosure of enterprise environmental accounting information. According to the current laws and regulations, Company A could set up a single section in the annual report to disclose its environmental accounting information. In this way, Company A could show its attitude towards environment protection to the outside world without significantly increasing the cost of the enterprise and help to reduce the costs of inquiring after information and establish a positive image of the enterprise. From the government and the public perspective, this practice contributes to the supervision of Company A by themselves.

(4) Establish an auditing system of the environmental accounting information

The purpose of disclosing enterprise environmental accounting information is to meet the needs of different stakeholders. Only when the information disclosed by enterprises is true and reliable, can the information be used well. Therefore, it is recommended that Company A should establish an auditing system for environmental accounting information including all publicly published reports such as social responsibility reports, which contain a great deal of environmental accounting information. This measure will improve the reliability of the information and increase trust in the enterprise. As early as 2006, China issued the New China Audit Standards for Certified Public Accountants No. 1631-Audit of Financial statements that considered environmental issues. Although the audit report issued does not guarantee that all the information disclosed by the enterprise is true and accurate, the audit report is issued by a third party and therefore maintains a certain degree of independence. Therefore, the audited report is obviously more reliable and trustworthy than the unaudited report.

(5) Disclose financial information related to the environment timely

From the above analysis, we can see that the disclosure of financial information related to the environment was inadequate, which is an important factor when stakeholders would like to know about the environmental information. Company A is therefore encouraged to uncover more monetized and quantitative financial information. As for the accounting personnel of the enterprise, Company A should require them to change their ideas, update their knowledge, and have the basic ability to disclose the environmental accounting information of the enterprise by offering them more opportunities to obtain relative training.

(6) Disclose financial information related to the environment comprehensively

According to the analysis above, most information disclosed by Company A was positive to the enterprise. However, the negative information was not clearly mentioned in its financial statements. Company A should make an all-round disclosure of the environmental accounting information of the enterprise. Although the disclosure of negative information may have a negative influence on the enterprise in the short term, in the long run, all-round disclosure of environmental accounting information will help the public supervise the enterprise better and enhance the environmental awareness of the enterprise personnel, which is conducive to the improvement of environmental protection conditions and the establishment of a positive image of the enterprise.

4.4. Discussion

This research was to evaluate the disclosure of the enterprise environmental accounting information comprehensively. By using linguistic terms, appraisers could express their opinions more easily. At the same time, taking the consistency of opinions as the weight of the appraisers into consideration can reduce the influence of the deviation of abnormal evaluation opinions and more accurate and authentic results can be obtained.

According to the evaluation results of the case study, with this method the disclosure of the enterprise environmental accounting information can be reflected directly and comprehensively. Instead of spending much time reading many annual financial and social responsibility reports, stakeholders can employ the evaluation results to obtain a concrete understanding of the quality of environmental accounting information disclosure.

The index weights obtained in the case have universality as they cannot only be applied to the company in the case study, but also provide important references for other enterprises to set their index weights. From the evaluation results of the enterprise, we figured out that there was a consistency in part of the indexes. For example, the disclosure of income related to the environmental protection (D7) was not disclosed in the annual report of Company A and looking back on the process of calculating the importance of indexes, the importance of (D7) was also relatively low.

For the personnel of the enterprise, the index weights also play a guiding role. The score of the disclosure of government subsidies related to the environment (D6) was 0.7292. This score was relatively high, but there is still room for improvement. This is primarily because government subsidies related to environmental protection were not disclosed separately and were disclosed in conjunction with other types of government subsidies, which required a certain amount of time to extract the environmental information. Therefore, Company A could set up a separate section to disclose the environmental accounting information. This practice will be convenient for people inquiring after this information.

This method plays an important role in guiding both the external stakeholders and internal personnel of the company and can provide concrete guidance and references for further optimization.

5. Conclusions

In this paper, an evaluation index system of enterprise environmental accounting information disclosure quality was constructed from the aspects of relevance, reliability, and compliance. Considering the linguistic evaluation information, a method based on triangular fuzzy numbers was used to aggregate the evaluation information. Moreover, the consistency of the evaluation information was used as the expert weight to reduce the personal bias. The case study showed that the proposed approach was feasible, and the evaluation results were helpful for both the stakeholders and enterprise staff.

Although a case study was conducted, further verification of other enterprises is needed. Moreover, the index system was mainly aimed at enterprises with heavy environmental pollution and may not fit a specific industry well. In future research, the evaluation index can be refined and enriched to adapt to the characteristics of different industries. The approach can be verified by involving more enterprises. Moreover, other methods can also be used to deal with the linguistic evaluation information.

Author Contributions

M.L. and A.T. constructed the evaluation index and evaluation approach. A.T. and S.L. wrote the paper. M.L., A.T. and X.Q. revised the paper.

Funding

The research was supported by the National Natural Science Foundation of China (Grant Nos. 71571191, 91646122), the Humanity and Social Science Youth Foundation of Ministry of Education in China (Project No. 15YJCZH081), and the Science Foundation of China University of Petroleum, Beijing (No. 2462015YQ0722).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Hatefi, S.M.; Tamošaitienė, J. Construction projects assessment based on the sustainable development criteria by an integrated fuzzy AHP and improved GRA model. Sustainability 2018, 10, 991. [Google Scholar] [CrossRef]

- Koroneos, C.J.; Rokos, D. Sustainable and integrated development—A critical analysis. Sustainability 2012, 4, 141–153. [Google Scholar] [CrossRef]

- Solomon, A.; Lewis, L. Incentives and disincentives for corporate environmental disclosure. BSE 2002, 11, 154–169. [Google Scholar] [CrossRef]

- Deegan, C. Environmental disclosures and share prices—A discussion about efforts to study this relationship. In Accounting Forum, School of Accounting and Law; RMIT Business, RMIT University, Australia, 2004; Elsevier: Amsterdam, The Netherlands, 2004; pp. 87–97. [Google Scholar]

- Deegan, C.; Cooper, B.J.; Shelly, M. An investigation of TBL report assurance statements: UK and European evidence. Manag. Audit. J. 2006, 21, 329–371. [Google Scholar] [CrossRef]

- Jasch, C. Environmental performance evaluation and indicators. J. Clean. Prod. 2000, 8, 79–88. [Google Scholar] [CrossRef]

- Jones, M.J. Accounting for the environment: Towards a theoretical perspective for environmental accounting and reporting. In Accounting Forum, School of Economics, Finance and Management, University of Bristol 8 Woodland Road Bristol BS8 1TN, United Kingdom, 2010; Elsevier: Amsterdam, The Netherlands, 2010; pp. 123–138. [Google Scholar]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Org. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Bajra, U.; Čadež, S. Audit committees and financial reporting quality: The 8th EU Company Law Directive perspective. Econ. Syst. 2018, 42, 151–163. [Google Scholar] [CrossRef]

- Eiler, L.A.; Miranda-Lopez, J.; Tama-Sweet, I. The Impact of Accounting Disclosures and the Regulatory Environment on the Information Content of Earnings Announcements. Int. J. Account. 2015, 50, 142–169. [Google Scholar] [CrossRef]

- Chan, J.C.; Welford, R. Assessing corporate environmental risk in China: An evaluation of reporting activities of Hong Kong listed enterprises. Corp. Soc. Responsib. Environ. Manag. 2005, 12, 88–104. [Google Scholar] [CrossRef]

- Senn, J. ‘Comply or Explain’ If You Do Not Disclose Environmental Accounting Information: Does New French Regulation Work? In Sustainability Accounting: Education, Regulation, Reporting and Stakeholders; Ataur, B., Stuart, C., Eds.; Emerald Group Publishing Limited, Emerald Publishing Limited Howard House: Wagon Lane, UK, 2018; Volume 7, pp. 113–133. [Google Scholar]

- Lewis, B.W.; Walls, J.L.; Dowell, G.W.S. Difference in degrees: CEO characteristics and firm environmental disclosure. Strateg. Manag. J. 2014, 35, 712–722. [Google Scholar] [CrossRef]

- Liu, X.; Anbumozhi, V. Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 2009, 17, 593–600. [Google Scholar] [CrossRef]

- Bewley, K.; Li, Y. Disclosure of environmental information by Canadian manufacturing companies: A voluntary disclosure perspective. In Advances in Environmental Accounting & Management; Emerald Group Publishing Limited, Emerald Publishing Limited Howard House: Wagon Lane, UK, 2000; pp. 201–226. [Google Scholar]

- Li, Y.; Richardson, G.D.; Thornton, D.B. Corporate disclosure of environmental liability information: Theory and evidence. Contemp. Account. Res. 1997, 14, 435–474. [Google Scholar] [CrossRef]

- Zhongfu, Y.; Jianhui, J.; Pinglin, H. The study on the correlation between environmental information disclosure and economic performance-With empirical data from the manufacturing industries at shanghai stock exchange in China. Energy Procedia 2011, 5, 1218–1224. [Google Scholar] [CrossRef]

- Iatridis, G.E. Environmental disclosure quality: Evidence on environmental performance, corporate governance and value relevance. Emerg. Mark. Rev. 2013, 14, 55–75. [Google Scholar] [CrossRef]

- Liu, Y. Accounting Information Quality Evaluation System and Standard. Journal of Yunyang Teachers College. 2012, 32, 106–108. [Google Scholar]

- He, C. Construction of Environmental Accounting Information Evaluation Index System. Bus. Econ. 2014, 8, 117–118. [Google Scholar]

- Yuan, Y.M. Analysis on Compliance of Accounting Information Disclosure of Listed Companies in China. Times Financ. 2014, 26, 155–157. [Google Scholar]

- Luo, Y.Q.; Wu, X.L.; Deng, Y. Impact of Environmental Accounting Information Disclosure on Corporate Market Performance—Based on Listed Company Data of Pharmaceutical Industry. Friends Account. 2016, 15, 50–53. [Google Scholar]

- Lu, Q.S.; Gan, S.D. Research on Enterprise Environmental Accounting Information Disclosure Based on Stakeholder Expectations. Guangxi Soc. Sci. 2015, 11, 76–83. [Google Scholar]

- Luo, L.J. Thoughts on the Construction of the Content Framework of Enterprise Environmental Accounting Information Disclosure. J. Hunan Adm. Inst. 2007, 1, 50–52. [Google Scholar]

- Meng, F.L. On Environmental Accounting Information Disclosure and Related Theoretical Problems. Account. Res. 1999, 4, 10. [Google Scholar]

- Wu, J.F.; Ye, C.G.; Liu, M. Environmental Performance, Political Relevance and Environmental Information Disclosure. J. Shanxi Financ. Econ. Univ. 2015, 7, 99–110. [Google Scholar]

- Liu, J.L.; Xin, Q.; Zha, L.R. Environmental Accounting Elements Confirmation and Measurement Exploration. China Manag. Inf. 2010, 11, 16–18. [Google Scholar]

- Ma, L. Establish a Modern Enterprise Environment Management System. Sichuan Environ. 1996, 2, 70–71. [Google Scholar]

- Liu, C.Z.; Pan, A.L. Quality Evaluation and Suggestion of Environmental Information Disclosure of Circular Economy Listed Companies. Financ. Account. Mon. 2014, 2, 37–39. [Google Scholar]

- Chen, W. On the Content of Enterprise Environmental Accounting Information Disclosure. Mod. Bus. Trade Ind. 2010, 23, 271–272. [Google Scholar]

- Ran, G.; Fang, Q.; Luo, S.; Chan, K.C. Supervisory board characteristics and accounting information quality: Evidence from China. Int. Rev. Econ. Financ. 2015, 37, 18–32. [Google Scholar] [CrossRef]

- Sun, Y.; Yi, Y.; Lin, B. Board independence, internal information environment and voluntary disclosure of auditors’ reports on internal controls. China J. Account. Res. 2012, 5, 145–161. [Google Scholar] [CrossRef]

- Su, Y.J.; Hou, X.Y. Construction of Listed Companies Accounting Information Quality Evaluation Index System Based on Total Budget Management. Commer. Account. 2015, 7, 17–20. [Google Scholar]

- Cui, M.H.; Li, H.L. Quality Evaluation of Accounting Information in Small and Medium-sized Enterprises. Green Financ. Account. 2013, 5, 27–31. [Google Scholar]

- Li, L.X. Discussion on Internal Control of State-owned Enterprise Group Companies. Policy Res. 2012, 2, 59–60. [Google Scholar]

- Yuan, J.G.; Yu, A.Q.; Yang, H. The Construction of Accounting Information Quality Evaluation Index System. Commer. Account. 2005, 24, 50–51. [Google Scholar]

- Wang, X.J.; Wan, Y.H. Construction of Big Data Enterprise Accounting Information Quality Evaluation Index System-Based on Fuzzy Comprehensive Evaluation Method. Financ. Account. Mon. 2015, 14, 74–77. [Google Scholar]

- Qin, Y.W.; Yi, J. Study on the Evaluation of Accounting Information Quality of Listed Companies in China and Its Countermeasures. Mod. Econ. Inf. 2015, 1, 164–165. [Google Scholar]

- Wan, S.P.; Dong, J.Y. Possibility linear programming with trapezoidal fuzzy numbers. Appl. Math. Model. 2014, 38, 1660–1672. [Google Scholar] [CrossRef]

- Li, M.; Wei, W.; Wang, J.; Qi, X. Approach to Evaluating Accounting Informatization Based on Entropy in Intuitionistic Fuzzy Environment. Entropy 2018, 20, 476. [Google Scholar] [CrossRef]

- Lin, Z.M.; Mao, Z.Y. A Triangular Fuzzy Number Multiple Index Group Decision Making Method. Stat. Decis. 2012, S3, 169–170. [Google Scholar]

Figure 1.

Evaluation process.

Figure 2.

The index importance based on the expected value.

Figure 3.

Comprehensive evaluation value of index.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Evaluation index system of the quality of enterprise environmental accounting information disclosure.

Table 1.

Evaluation index system of the quality of enterprise environmental accounting information disclosure.

| Primary Index | Secondary Index | Tertiary Index |

|---|---|---|

| Relevance (B1) | Financial standing (C1) | Disclosure of total investment in environmental protection [22] (D1) |

| Disclosure of facilities and technologies for environmental protection [23] (D2) | ||

| Disclosure of liabilities due to environmental problems [24] (D3) | ||

| Operating results (C2) | Disclosure of expenditure of environmental protection departments in enterprises [25] (D4) | |

| Disclosure of litigation expenses and fines related to environment [26] (D5) | ||

| Disclosure of government subsidies related to the environment [22] (D6) | ||

| Disclosure of income related to environmental protection [27] (D7) | ||

| Disclosure of other environment-related expenditures [22] (D8) | ||

| Information on environmental policy (C3) | Disclosure of environmental system certification and clean production [28] (D9) | |

| Disclosure of the establishment and operation of environmental management system [29] (D10) | ||

| Pollution control (C4) | Disclosure of pollutants standardized discharge [30] (D11) | |

| Disclosure of pollutants recycling such as exhaust gases [30] (D12) | ||

| Disclosure of resource consumption and reduction measures [29] (D13) | ||

| Reliability (B2) | Company structure (C5) | Health degree of the governance structure of the enterprise [31] (D14) |

| Corporate audit committee and its performance [32] (D15) | ||

| Regulatory situation (C6) | Inspection and punishment of Department of Finance and Administration for Industry, Commerce and Taxation [33] (D16) | |

| Supervision on information disclosure of listed companies by Securities Regulatory Commission and Stock Exchange [33] (D17) | ||

| External authentication (C7) | Enterprise annual reports and environmental information audit opinions [34] (D18) | |

| Enterprise internal control system and its implementation [35] (D19) | ||

| Compliance (B3) | Timeliness (C8) | Timeliness of disclosure of financial reports and related reports [36] (D20) |

| Timeliness of disclosure of major announcements [37] (D21) | ||

| Integrity (C9) | Integrity of contents and scopes of the disclosure according to laws and regulations [38] (D22) | |

| Integrity of accounting processes and contents of financial information according to laws and regulations [38] (D23) |

Table 2.

Evaluation results of index importance.

| Index | Evaluation Results of the Importance | Index Importance Based on the Expected Value |

|---|---|---|

| Disclosure of total investment in the environmental protection (D1) | (0.60, 0.70, 0.80) | 0.7009 |

| Disclosure of facilities and technologies for the environmental protection(D2) | (0.62, 0.72, 0.82) | 0.7214 |

| Disclosure of liabilities due to environmental problems (D3) | (0.59, 0.69, 0.79) | 0.6917 |

| Disclosure of expenditure of environmental protection departments in enterprises (D4) | (0.65, 0.75, 0.85) | 0.7453 |

| Disclosure of litigation expenses and fines related to the environment (D5) | (0.57, 0.67, 0.77) | 0.6737 |

| Disclosure of government subsidies related to the environment (D6) | (0.61, 0.71, 0.81) | 0.7090 |

| Disclosure of income related to the environmental protection (D7) | (0.56, 0.66, 0.76) | 0.6551 |

| Disclosure of other environment-related expenditures (D8) | (0.59, 0.69, 0.79) | 0.6903 |

| Disclosure of the environmental system certification and clean production (D9) | (0.63, 0.73, 0.83) | 0.7289 |

| Disclosure of the establishment and operation of the environmental management system (D10) | (0.60, 0.70, 0.80) | 0.7000 |

| Disclosure of the pollutants standardized discharge (D11) | (0.73, 0.83, 0.93) | 0.8279 |

| Disclosure of pollutants recycling such as exhaust gases (D12) | (0.64, 0.74, 0.84) | 0.7410 |

| Disclosure of the resource consumption and reduction measures (D13) | (0.65, 0.75, 0.85) | 0.7522 |

| Health degree of the governance structure of the enterprise (D14) | (0.63, 0.73, 0.83) | 0.7271 |

| Corporate audit committee and its performance (D15) | (0.57, 0.67, 0.77) | 0.6720 |

| Inspection and punishment of Department of Finance and Administration for Industry, Commerce and Taxation (D16) | (0.60, 0.70, 0.80) | 0.7000 |

| Supervision of information disclosure of listed companies by Securities Regulatory Commission and Stock Exchange (D17) | (0.60, 0.70, 0.80) | 0.7027 |

| Enterprise annual reports and environmental information audit opinions (D18) | (0.70, 0.80, 0.90) | 0.7972 |

| Enterprise internal control system and its implementation (D19) | (0.68, 0.78, 0.88) | 0.7831 |

| Timeliness of disclosure of financial reports and related reports (D20) | (0.64, 0.74, 0.84) | 0.7367 |

| Timeliness of disclosure of major announcements (D21) | (0.65, 0.75, 0.85) | 0.7464 |

| Integrity of contents and scopes of the disclosure according to laws and regulations (D22) | (0.71, 0.81, 0.91) | 0.8105 |

| Integrity of accounting processes and contents of financial information according to laws and regulations (D23) | (0.73, 0.83, 0.93) | 0.8281 |

Table 3.

Comprehensive evaluation results.

| Index | Comprehensive Evaluation Results | Comprehensive Evaluation Values |

|---|---|---|

| Disclosure of total investment in the environmental protection (D1) | (0.55, 0.65, 0.75) | 0.6477 |

| Disclosure of facilities and technologies for the environmental protection (D2) | (0.63, 0.73, 0.83) | 0.7279 |

| Disclosure of liabilities due to environmental problems (D3) | (0.53, 0.63, 0.73) | 0.6289 |

| Disclosure of expenditure of environmental protection departments in enterprises (D4) | (0.34, 0.44, 0.54) | 0.4360 |

| Disclosure of litigation expenses and fines related to the environment (D5) | (0.34, 0.44, 0.54) | 0.4357 |

| Disclosure of government subsidies related to the environment (D6) | (0.63, 0.73, 0.83) | 0.7292 |

| Disclosure of income related to the environmental protection (D7) | (0.24, 0.34, 0.44) | 0.3368 |

| Disclosure of other environment-related expenditures (D8) | (0.50, 0.60, 0.69) | 0.5950 |

| Disclosure of the environmental system certification and clean production (D9) | (0.41, 0.51, 0.61) | 0.5107 |

| Disclosure of the establishment and operation of the environmental management system (D10) | (0.55, 0.65, 0.75) | 0.6461 |

| Disclosure of the pollutants standardized discharge (D11) | (0.61, 0.71, 0.81) | 0.7093 |

| Disclosure of pollutants recycling such as exhaust gases (D12) | (0.60, 0.70, 0.80) | 0.7024 |

| Disclosure of resource consumptions and reduction measures (D13) | (0.59, 0.69, 0.79) | 0.6907 |

| Health degree of the governance structure of the enterprise (D14) | (0.65, 0.75, 0.85) | 0.7548 |

| Corporate audit committee and its performance (D15) | (0.62, 0.72, 0.82) | 0.7197 |

| Inspection and punishment of Department of Finance and Administration for Industry, Commerce and Taxation (D16) | (0.45, 0.55, 0.65) | 0.5537 |

| Supervision on information disclosure of listed companies by Securities Regulatory Commission and Stock Exchange (D17) | (0.52, 0.62, 0.72) | 0.6181 |

| Enterprise annual reports and environmental information audit opinions (D18) | (0.45, 0.55, 0.65) | 0.5537 |

| Enterprise internal control system and its implementation (D19) | (0.62, 072, 0.82) | 0.7183 |

| Timeliness of disclosure of financial reports and related reports (D20) | (0.55, 0.65, 0.75) | 0.6504 |

| Timeliness of disclosure of major announcements (D21) | (0.65, 0.75, 0.85) | 0.7548 |

| Integrity of contents and scopes of the disclosure according to laws and regulations (D22) | (0.65, 0.75, 0.85) | 0.7458 |

| Integrity of accounting processes and contents of financial information according to laws and regulations (D23) | (0.64, 0.74, 0.84) | 0.7366 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Li, M.; Tian, A.; Li, S.; Qi, X. Evaluating the Quality of Enterprise Environmental Accounting Information Disclosure. Sustainability 2018, 10, 2136. https://doi.org/10.3390/su10072136

AMA Style

Li M, Tian A, Li S, Qi X. Evaluating the Quality of Enterprise Environmental Accounting Information Disclosure. Sustainability. 2018; 10(7):2136. https://doi.org/10.3390/su10072136

Chicago/Turabian StyleLi, Ming, Anning Tian, Shuyi Li, and Xiaoyu Qi. 2018. "Evaluating the Quality of Enterprise Environmental Accounting Information Disclosure" Sustainability 10, no. 7: 2136. https://doi.org/10.3390/su10072136

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.