Environmental Fiscal Reform and the Double Dividend: Evidence from a Dynamic General Equilibrium Model

Abstract

:1. Introduction

2. The Energy-Environment-Economy Dynamic CGE Model

- Households: Their main role is to supply labor, purchase goods and services and receive incomes from the labor they supply, from the capital and land they own, from the government and from the rest of the world. Households also pay taxes to government and save part of their total income.

- Government: Its main economic role is to collect and redistribute other agents’ incomes though taxes, subsidies and transfers. In our model, we categorize these taxes as tax on capital; tax on labor; property tax; tax on dividends; value-added tax (VAT) on products; special taxes on alcohol, tobacco, hydrocarbons, electricity and retail hydrocarbons; sales tax; other taxes on production; social security contributions; and import taxes (or tariffs). We also factor in other non-tax revenues from households and companies, along with production subsidies. The government also buys goods and services, invests and pays interests for government bonds. Government deficits are covered by domestic and foreign borrowing.

- Enterprises: Their role is mainly to produce commodities using intermediate and primary inputs purchased in the market; their revenue includes government output subsidies and other payments. They spend their earnings on dividends to households and taxes to government; they also save a share of their income by retaining part of the earnings. Regarding production, the model identifies 101 industries that produce 101 commodities, with high levels of detail in the electricity generation and waste treatment technology sectors.

- Rest of world: Its main role it to purchase exports, sell imports and provide foreign investment. It also receives and pays incomes from other agents. Imports and domestic output follow Armington’s assumption [43], to be combined through constant elasticity of substitution (CES) functions, producing a composite commodity supply.

3. Data

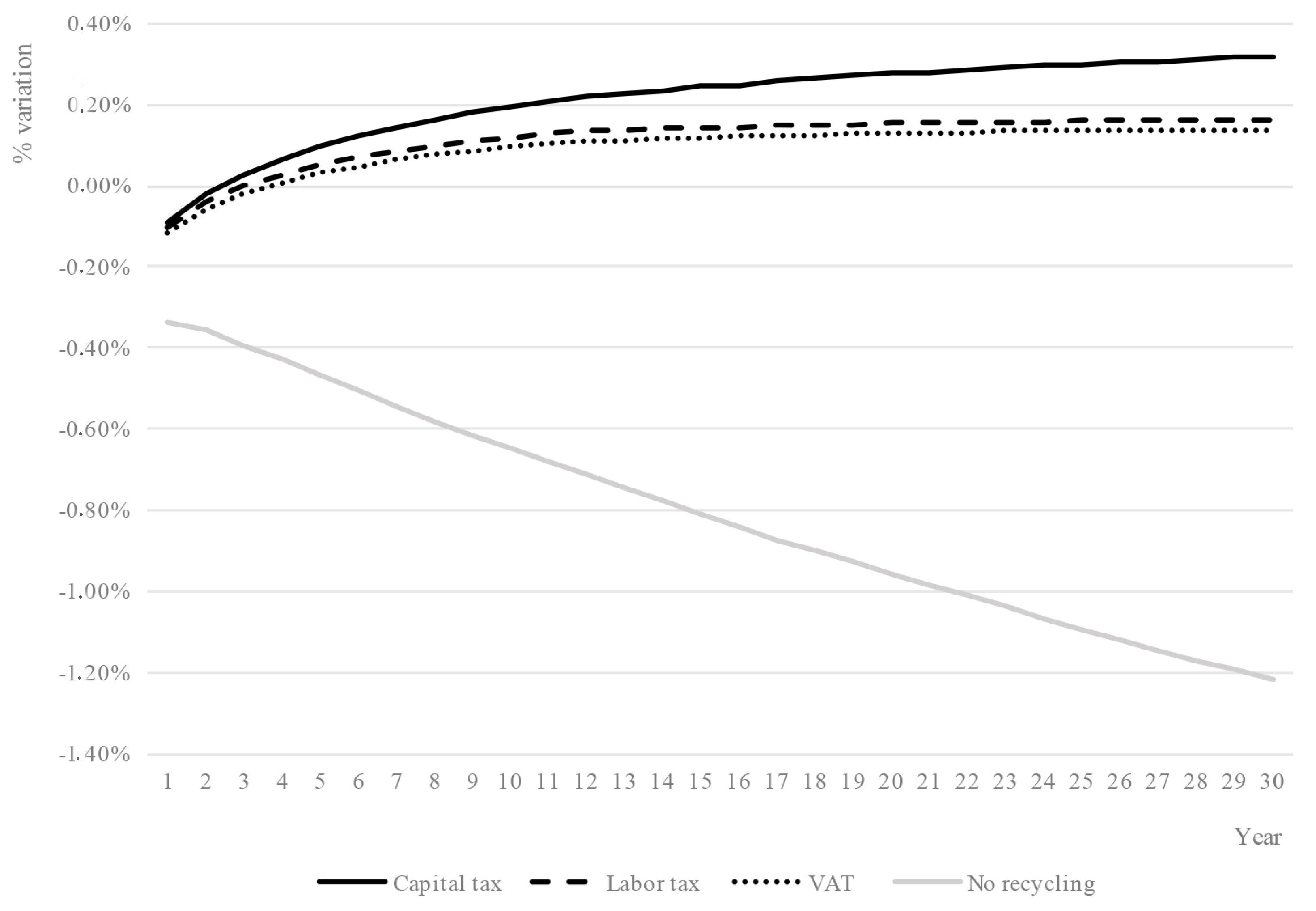

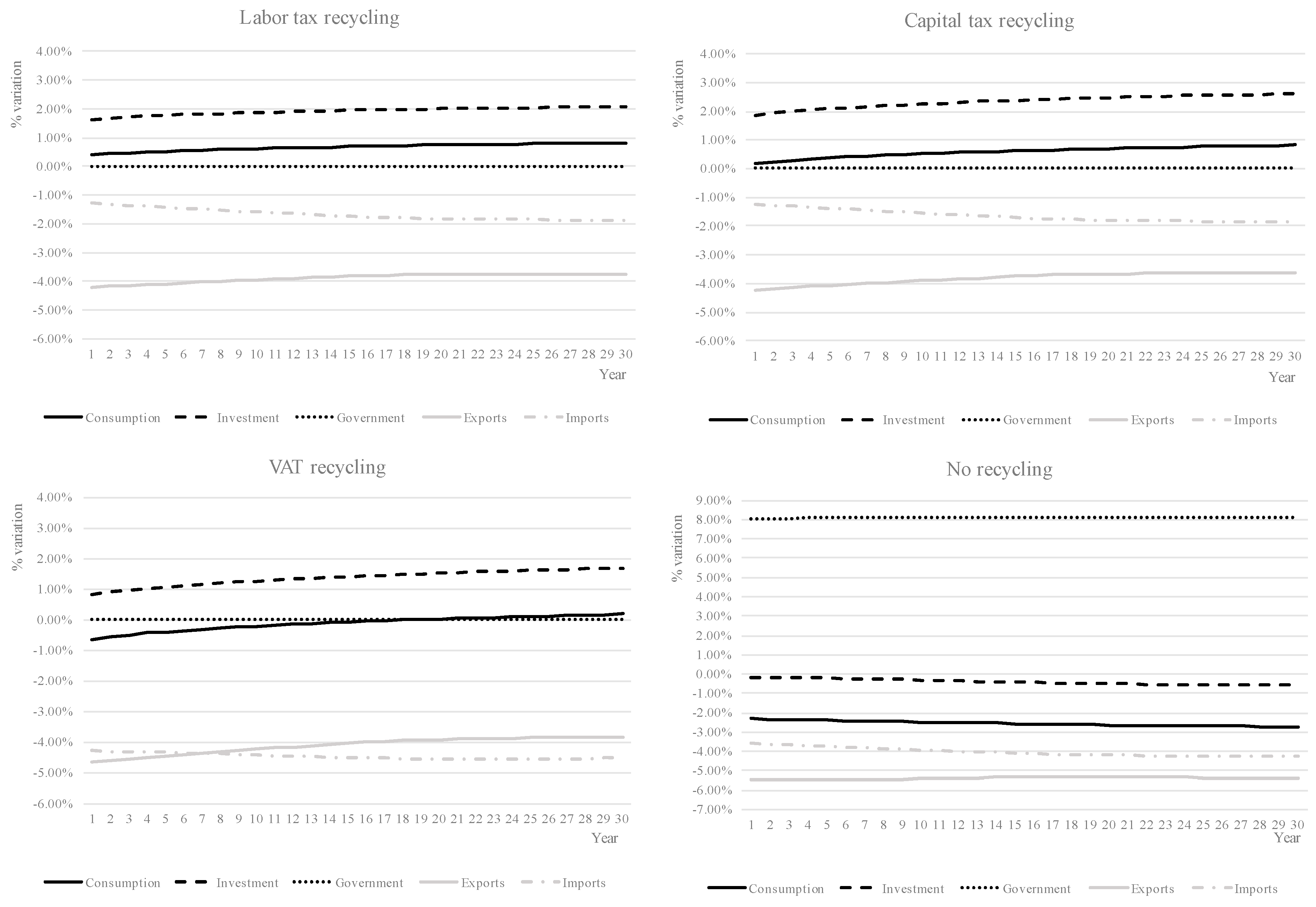

4. Scenarios and Results

- Energy industry reforms are expected to increase the price of energy, thus reducing overall demand and consequently the emission of several pollutants. Particularly, they are expected to have a specific impact on GHG emissions. In our model, there are 16 industries in this category: coal and lignite peat; extraction of crude petroleum and services related to crude oil extraction; extraction of natural gas and services related to natural gas extraction, excluding surveying and mining of uranium and thorium ores; coke, refinement of petroleum and nuclear fuel; electricity by coal; electricity by gas; electricity by nuclear; electricity by hydro; electricity by wind; electricity by petroleum and other oil derivatives, electricity by biomass and waste, electricity by solar photovoltaic; electricity by solar thermal; electricity (other); transmission services of electricity; distribution and trade services of electricity; and production and distribution of natural gas.

- Water supply industry fiscal reform is expected to increase the price of water and thereby reduce its consumption. This reduction is not reflected in air pollutants modeled in this research but is consistent with an EFR that aims to reduce environmental loads. Given the constraints of the model, we tax the overall sector; in practice, however, the reform should be implemented as a progressive tax. The specific industry affected is: “Collected and purified water, distribution services of water”.

- Fiscal reform of transport industries is expected to have an effect similar to that of taxation of water, increasing the price of levied transport and reducing its consumption. We have simulated affectation on three transport industries, with different types of effects, some related to the production of transport units and some to their use: (i) “Sale of motor vehicles” would reduce purchases of motor vehicles and thus the externalities associated with their production; (ii) “Retail trade services of motor fuel” would reduce the use of motor vehicles and therefore the externalities associated with their use; (iii) “Air transport services” would reduce the use of air transportation.

- Waste-treatment industry reform aims to increase the costs and market prices of waste treatment and thereby to reduce waste generation. Consequently, pollutants associated with waste treatment would drop. There are 19 industries in this category: food waste for treatment—incineration; paper waste for treatment—incineration; plastic waste for treatment—incineration; inert/metal waste for treatment—incineration; textiles waste for treatment—incineration; wood waste for treatment—incineration; oil/hazardous waste for treatment—incineration; food waste for treatment—biogasification and land application; paper waste for treatment—biogasification and land application; sewage sludge for treatment—biogasification and land application; food waste for treatment—composting and land application; food waste for treatment—wastewater treatment; other waste for treatment—wastewater treatment; food waste for treatment—landfill; paper for treatment—landfill; plastic waste for treatment—landfill; inert/metal/hazardous waste for treatment—landfill; textiles waste for treatment—landfill; and wood waste for treatment—landfill.

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A. Detailed Description of the Model

Appendix A.1. Firms

Appendix A.2. Households

Appendix A.3. Government

Appendix A.4. Capital, Investment and Financial System

Appendix A.5. Foreign Sector

Appendix A.6. Markets

Appendix A.7. Energy and Pollutant Emissions

References

- European Environment Agency. Using the Market for Cost-Effective Environmental Policy: Market-Based Instruments in Europe; Report No. 1/2006; EEA: Copenhagen, Denmark, 2006. [Google Scholar]

- Eurostat. Taxation Trends in the European Union Data for the EU Member States Iceland and Norway; Publication Office of the European Union: Luxembourg, 2013. [Google Scholar]

- COM. Council Recommendation on Spain’s 2014 National Reform Programme and Delivering a Council Opinion on Spain’s Stability Programme; European Commission: Brussels, Belgium, 2014. [Google Scholar]

- European Environment Agency. Environmental Fiscal Reform: Illustrative Potential in Spain; Staff Position Note SPN12/01; EEA: Copenhagen, Denmark, 2012. [Google Scholar]

- Baumol, W. On taxation and the control of externalities. Am. Econ. Rev. 1972, 62, 307–321. [Google Scholar]

- Baumol, W.; Oates, W. The use of standards and prices for the protection of the environment. Swed. J. Econ. 1971, 73, 42–54. [Google Scholar] [CrossRef]

- Pigou, A.C. The Economics of Welfare; Macmillan and Company: London, UK, 1920. [Google Scholar]

- Grubb, M.; Edmonds, J.; Ten Brink, P.; Morrison, M. The cost of limiting fossil-fuel CO2 emissions: A survey and analysis. Annu. Rev. Energy Environ. 1993, 18, 397–478. [Google Scholar] [CrossRef]

- Nordhaus, W. Optimal greenhouse gas reductions and tax policy in the “DICE” model. Am. Econ. Rev. 1993, 83, 313–317. [Google Scholar]

- Pearce, D. The role of carbon taxes in adjusting to global warming. Econ. J. 1991, 101, 938–948. [Google Scholar] [CrossRef]

- Repetto, R.; Dower, R.; Jenkins, R.; Geoghegan, J. Green Fees: How a Tax Shift Can Work for the Environment and the Economy; World Resource Institute: New York, NY, USA, 1992. [Google Scholar]

- Babiker, M.H.; Metcalf, G.E.; Reilly, J. Tax distortions and global climate policy. J. Environ. Econ. Manag. 2003, 46, 269–287. [Google Scholar] [CrossRef]

- Bovenberg, A.L.; Goulder, L.H. Environmental taxation and regulation. In Handbook of Public Economics; Auerbach, A., Feldstein, M., Eds.; Elsevier: Amsterdam, The Netherlands, 2002; pp. 1471–1545. [Google Scholar]

- Carbone, J.; Morgenstern, R.D.; Williams, R.C., III; Burtraw, D. Deficit Reduction and Carbon Taxes: Budgetary, Economic and Distributional Impacts; Resources for the Future: Washington, DC, USA, 2013. [Google Scholar]

- Devarajan, S.; Go, D.S.; Robinson, S.; Thierfelder, K. Tax policy to reduce carbon emissions in a distorted economy: Illustrations from a South Africa CGE model. B E J. Econ. Anal. Policy 2011, 11, 1–24. [Google Scholar] [CrossRef]

- Dixon, P.B.; Jorgenson, D.W. Handbook of Computable General Equilibrium Modeling; Newnes: Boston, MA, USA, 2012. [Google Scholar]

- Bye, B. Environmental tax reform and producer foresight: An intertemporal computable general equilibrium analysis. J. Policy Model. 2000, 22, 719–752. [Google Scholar] [CrossRef]

- Ciaschini, M.; Pretaroli, R.; Severini, F.; Socci, C. Regional double dividend from environmental tax reform: An application for the Italian economy. Res. Econ. 2012, 66, 273–283. [Google Scholar] [CrossRef] [Green Version]

- Fernández, E.; Pérez, R.; Ruiz, J. Optimal green tax reforms yielding double dividend. Energy Policy 2011, 39, 4253–4263. [Google Scholar] [CrossRef]

- Holmlund, B.; Kolm, A.S. Environmental tax reform in a small open economy with structural unemployment. Int. Tax Public Financ. 2000, 7, 315–333. [Google Scholar] [CrossRef]

- Jorgenson, D.W.; Goettle, R.J.; Ho, M.S.; Wilcoxen, P.J. Double Dividend: Environmental Taxes and Fiscal Reform in the United States; MIT Press: Cambridge, MA, USA, 2013. [Google Scholar]

- Patuelli, R.; Nijkamp, P.; Pels, E. Environmental tax reform and the double dividend: A meta-analytical performance assessment. Ecol. Econ. 2005, 55, 564–583. [Google Scholar] [CrossRef]

- Wendner, R. An applied dynamic general equilibrium model of environmental tax reforms and pension policy. J. Policy Model. 2001, 23, 25–50. [Google Scholar] [CrossRef]

- Freire-González, J. Environmental taxation and the double dividend hypothesis in CGE modeling literature: A critical review. J. Policy Model. 2018. [Google Scholar] [CrossRef]

- Bosquet, B. Environmental Tax Reform: Does it Work? A Survey of the Empirical Evidence. Ecol. Econ. 2000, 34, 19–32. [Google Scholar] [CrossRef]

- Ekins, P.; Speck, S. Competitiveness and Exemptions from Environmental Taxes in Europe. Environ. Resour. Econ. 1999, 13, 369–396. [Google Scholar] [CrossRef]

- Gago, A.; Labandeira, X.; Picos, F.; Rodríguez, M. Environmental Taxes in Spain: A Missed Opportunity; International Studies Program Working Paper 06–09; Georgia State University, Andrew Young School of Policy Studies: Atlanta, GA, USA, 2006. [Google Scholar]

- Gago, A.; Labandeira, X. Un Nuevo Modelo de Reforma Fiscal Verde, Rede; Working Paper; Universidad de Vigo: Pontevedra, Spain, 2012. [Google Scholar]

- López-Guzmán, T. Environmental Taxes in Spain; Research Paper; Department of Social Sciences, Roskilde University: Roskilde, Denmark, 2004; pp. 1–21. [Google Scholar]

- Markandya, A.; Gonzalez-Eguino, M.; Escapa, M. Environmental Fiscal Reform and Unemployment in Spain; Working Paper Series 2012-4; BC3: Bilbao, Spain, 2012. [Google Scholar]

- Barker, T.; Köhler, J. Equity and ecotax reform in the EU: Achieving a 10 percent reduction in CO2 emissions using excise duties. Fisc. Stud. 1998, 19, 375–402. [Google Scholar] [CrossRef]

- Bosello, F.; Carraro, C. Recycling energy taxes: Impacts on a disaggregated labour market. Energy Econ. 2001, 23, 569–594. [Google Scholar] [CrossRef]

- Carraro, C.; Galeotti, M.; Gallo, M. Environmental taxation and unemployment: Some evidence on the “double dividend hypothesis” in Europe. J. Public Econ. 1996, 62, 141–181. [Google Scholar] [CrossRef]

- Conrad, K.; Schmidt, T. Economic effects of an uncoordinated versus a coordinated carbon dioxide policy in the European Union: An applied general equilibrium analysis. Econ. Syst. Res. 1998, 10, 161–182. [Google Scholar] [CrossRef]

- De Miguel, C.; Manzano, B. Gradual Green Tax Reforms. Energy Econ. 2011, 33, S50–S58. [Google Scholar] [CrossRef]

- Labandeira, X.; Labeaga, J.M.; Rodríguez, M. Green tax reforms in Spain. Eur. Environ. 2004, 14, 290–299. [Google Scholar] [CrossRef]

- Manresa, A.; Sancho, F. Implementing a double dividend: Recycling ecotaxes towards lower labour taxes. Energy Policy 2005, 33, 1577–1585. [Google Scholar] [CrossRef]

- Cao, J.; Ho, S.; Jorgenson, D.W. The local and global benefits of green tax policies in China. Rev. Environ. Econ. Policy 2009, 3, 189–208. [Google Scholar] [CrossRef]

- Cao, J.; Ho, S.; Jorgenson, D.W. The economics of environmental policies in China. In Clearer Skies over China; Nielsen, C.P., Ho, M.S., Eds.; MIT Press: Cambridge, MA, USA, 2013; pp. 329–372. [Google Scholar]

- Ho, M.S.; Jorgenson, D. Policies to control air pollution damages. In Clearing the Air: The Health and Economic Damages of Air Pollution in China; Ho, M.S., Nielsen, C.P., Eds.; MIT Press: Cambridge, MA, USA, 2007; pp. 331–372. [Google Scholar]

- Jorgenson, D.W.; Wilcoxen, P.J. Reducing U.S. carbon emissions: An econometric general equilibrium assessment. Resour. Energy Econ. 1993, 14, 243–268. [Google Scholar]

- Freire-González, J.; Ho, M.S. Carbon taxes and the double dividend hypothesis in a dynamic CGE framework. 2018. under review. [Google Scholar]

- Armington, P.S. A theory of demand for products distinguished by place of production. Staff Pap. 1969, 16, 159–178. [Google Scholar] [CrossRef]

- IEA. World CO2 Emissions from Fuel Combustion; OECD/IEA: Paris, France, 2016. [Google Scholar]

- Tukker, A.; de Koning, A.; Wood, R.; Hawkins, T.; Lutter, S.; Acosta, J.; Rueda Cantuche, J.M.; Bouwmeester, M.; Oosterhaven, J.; Drosdowski, T.; et al. EXIOPOL: Development and illustrative analyses of a detailed global MR EE SUT/IOT. Econ. Syst. Res. 2013, 25, 50–70. [Google Scholar] [CrossRef]

- Wood, R.; Stadler, K.; Bulavskaya, T.; Lutter, S.; Giljum, S.; de Koning, A.; Kuenen, J.; Schütz, H.; Acosta-Fernández, J.; Usubiaga, A.; et al. Global sustainability accounting: Developing Exiobase for multi-regional footprint analysis. Sustainability 2015, 7, 138–163. [Google Scholar] [CrossRef] [Green Version]

- Jäger, K. EU KLEMS Growth and Productivity Accounts 2016 Release, Statistical Module. Available online: http://www.euklems.net/TCB/2016/Metholology_EU%20KLEMS_2016.pdf (accessed on 12 February 2018).

- Bohm, P. Environmental taxation and the double dividend: Fact or fallacy? In Ecotaxation; O’Riordan, T., Ed.; Earthscan: London, UK, 1997; pp. 106–124. [Google Scholar]

- Kemfert, C.; Welsch, H. Energy-capital-labor substitution and the economic effects of CO2 abatement: Evidence for Germany. J. Policy Model. 2000, 22, 641–660. [Google Scholar] [CrossRef]

- McKitrick, R. Double dividend environmental taxation and Canadian carbon emissions control. Can. Public Policy/Anal. Polit. 1997, 23, 417–434. [Google Scholar] [CrossRef]

- Sajeewani, D.; Siriwardana, M.; Mcneill, J. Household distributional and revenue recycling effects of the carbon price in Australia. Clim. Chang. Econ. 2015, 6, 1550012-1–1550012-23. [Google Scholar] [CrossRef]

- Garbaccio, R.F.; Ho, M.S.; Jorgenson, D.W. Controlling carbon emissions in China. Environ. Dev. Econ. 1999, 4, 493–518. [Google Scholar] [CrossRef]

- Lvovsky, K.; Hughes, G. An Approach to Projecting Ambient Concentrations of SO2 and PM-10. Unpublished. 1997. [Google Scholar]

{kind=link}

{kind=link}

| Commodity | Industry | Labor | Capital | Land | Households | Enterprise | Government | Taxes Less Subs. on Products | Other Taxes on Products | Social Security | Tariff | VAT for Import | Capital a/c | Rest of World | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Commodity | 1,126,644 | 604,429 | 193,474 | 326,422 | 283,331 | 2,534,300 | ||||||||||

| Industry | 2,151,706 | 2,151,706 | ||||||||||||||

| Labor | 510,296 | 510,296 | ||||||||||||||

| Capital | 414,982 | 414,982 | ||||||||||||||

| Land | 18,822 | 18,822 | ||||||||||||||

| Households | 373,879 | 18,822 | 299,539 | 155,808 | –20,312 | 827,736 | ||||||||||

| Enterprise | 404,703 | 404,703 | ||||||||||||||

| Government | 10,279 | 84,363 | 89,388 | 80,238 | 724 | 136,417 | 145 | 28,330 | –14,238 | 415,646 | ||||||

| Taxes less subs. on products | 80,238 | 80,238 | ||||||||||||||

| Other taxes on products | 724 | 724 | ||||||||||||||

| Social Security | 136,417 | 136,417 | ||||||||||||||

| Tariff | 145 | 145 | ||||||||||||||

| VAT for import | 28,330 | 28,330 | ||||||||||||||

| Capital a/c | 138,944 | 15,776 | 49,467 | 107,996 | 312,184 | |||||||||||

| Rest of World | 354,119 | 16,897 | 371,016 | |||||||||||||

| Total | 2,534,300 | 2,151,706 | 510,296 | 414,982 | 18,822 | 827,736 | 404,703 | 415,646 | 80,238 | 724 | 136,417 | 145 | 28,330 | 312,184 | 371,016 |

| Pollutant Emissions | % Variation | Pollutant Emissions | % Variation |

|---|---|---|---|

| CO2 | −13.99% | HCB | −12.35% |

| CH4 | −44.14% | NMVOC | −3.50% |

| N2O | −4.91% | TSP | −6.17% |

| HFC | −3.42% | PCBs | −10.44% |

| PM10 | −11.89% | As | −6.61% |

| PM2.5 | −6.25% | Cd | −6.28% |

| SO2 | −24.47% | Cr | −5.07% |

| NOx | −16.30% | Cu | −6.25% |

| NH3 | −1.76% | Hg | −6.57% |

| CO | −7.59% | Ni | −8.39% |

| Benzo(a)pyrene | −1.72% | Pb | −3.62% |

| Benzo(b)fluoranthene | −0.86% | Se | −22.39% |

| Benzo(k)fluoranthene | −3.97% | Zn | −7.30% |

| Indeno(1,2,3-cd)pyrene | −5.16% | SF6 | −8.61% |

| PAH | −1.60% | PFC | −5.50% |

| PCDD_F | −5.18% |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Freire-González, J.; Ho, M.S. Environmental Fiscal Reform and the Double Dividend: Evidence from a Dynamic General Equilibrium Model. Sustainability 2018, 10, 501. https://doi.org/10.3390/su10020501

Freire-González J, Ho MS. Environmental Fiscal Reform and the Double Dividend: Evidence from a Dynamic General Equilibrium Model. Sustainability. 2018; 10(2):501. https://doi.org/10.3390/su10020501

Chicago/Turabian StyleFreire-González, Jaume, and Mun S. Ho. 2018. "Environmental Fiscal Reform and the Double Dividend: Evidence from a Dynamic General Equilibrium Model" Sustainability 10, no. 2: 501. https://doi.org/10.3390/su10020501