Remuneration Committee, Board Independence and Top Executive Compensation

Abstract

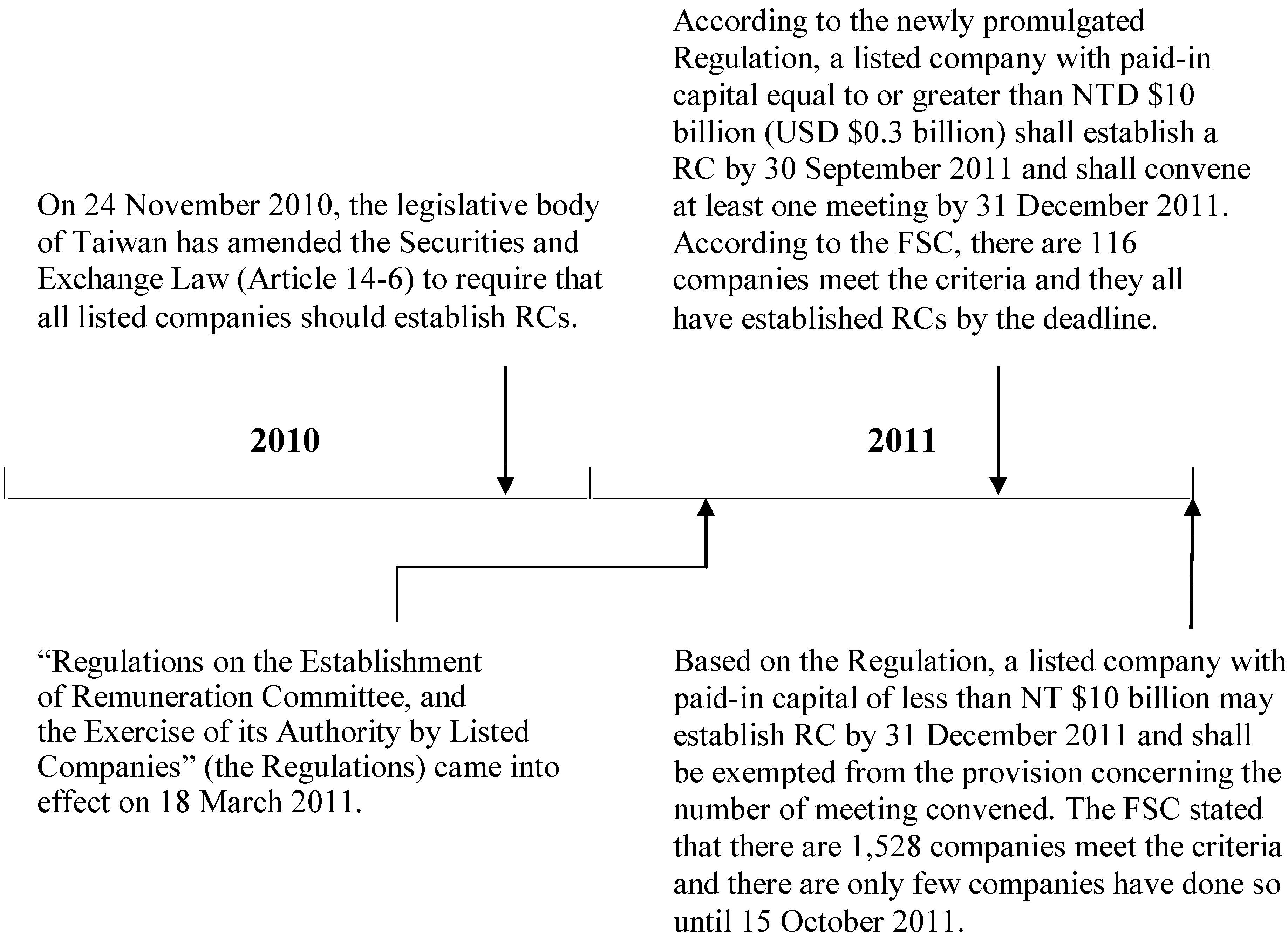

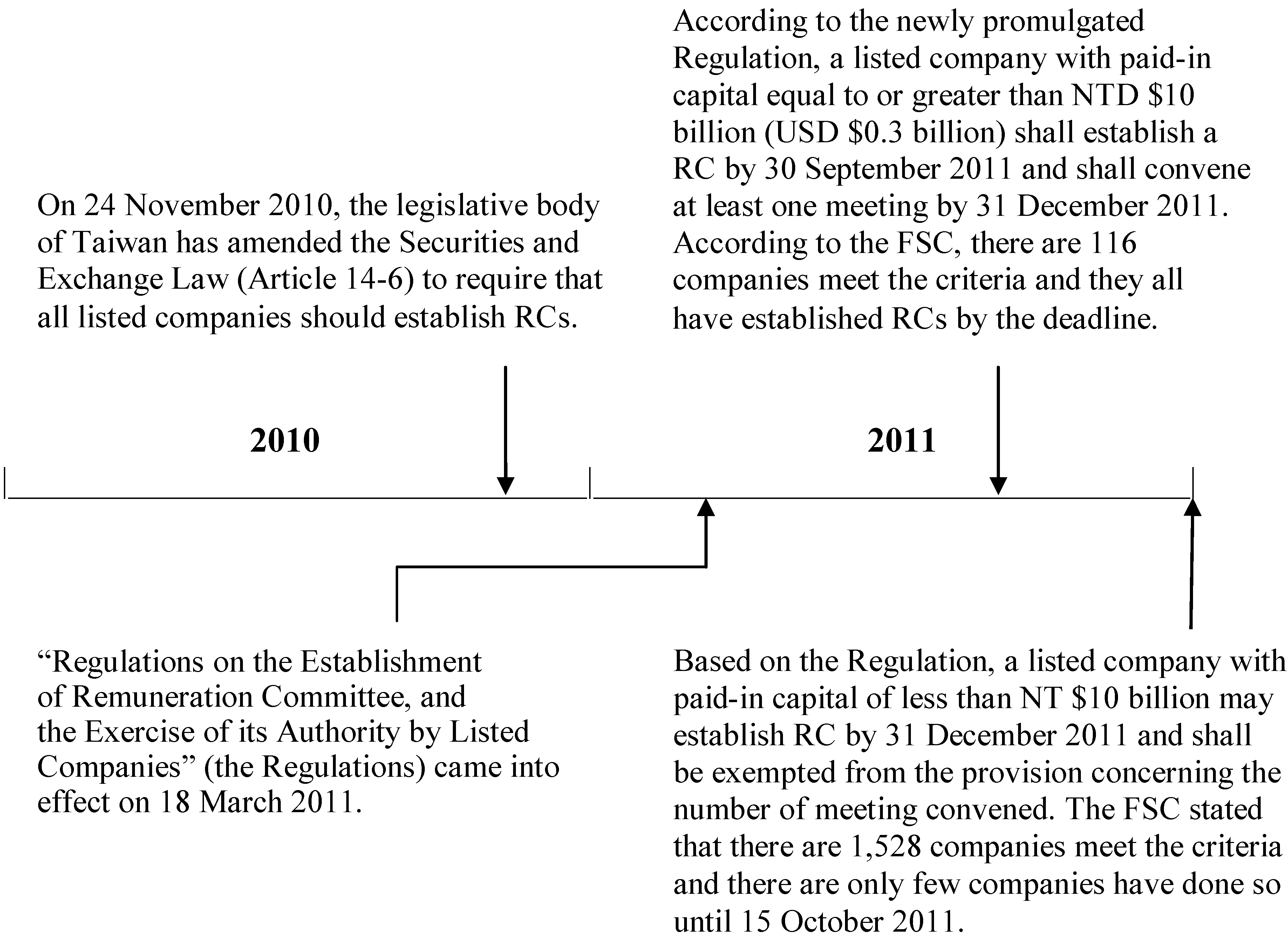

:1. Introduction

2. Prior Studies and Hypothesis Development

3. Methodology

4. Data

{kind=link}

| Num of firm-year observations | ||

|---|---|---|

| 1,734 firms listed in the Taiwan Stock Exchange (TSE), Over-the Counter (OTC), and Emerging Stock (ES) markets at the 2011 fiscal year-end from 2008 to 2011 | 6,936 | |

| Less: | Firms within the financial industry | (192) |

| CEO compensation data are missing | (811) | |

| Historical annual stock return (Ret) to calculate standard deviation of Ret or Ret for current year are missing | (1,106) | |

| Net sales to measure firm size (Firm_Size) are missing | (37) | |

| CEO ownership (CEO_Ownership) data are missing | (43) | |

| Final sample | 4,747 | |

| Variable | Unit | Mean | Std. dev. | Q1 | Median | Q3 |

|---|---|---|---|---|---|---|

| CEO_ Comp (upper) | NT$ | 6,970,603 | 8,706,381 | 2,832,000 | 5,000,000 | 10,000,000 |

| CEO_ Comp (lower) | NT$ | 3,084,053 | 4,842,515 | 0 | 2,000,000 | 5,000,000 |

| CEO_ Comp (average) | NT$ | 5,027,328 | 6,744,760 | 1,416,000 | 3,500,000 | 7,500,000 |

| Ret | % | 23.98 | 107.18 | -41.23 | -11.73 | 49.16 |

| Roa | % | 3.43 | 10.54 | 0.36 | 4.28 | 8.69 |

| Firm_Size | 14.66 | 1.56 | 13.69 | 14.56 | 15.56 | |

| Market-to-Book | 1.58 | 2.47 | 0.80 | 1.22 | 1.85 | |

| Stdev_Ret | % | 74.89 | 64.52 | 37.39 | 59.28 | 92.06 |

| Stdev_Roa | % | 5.87 | 5.31 | 2.58 | 4.42 | 7.28 |

| CEO_Chair | 0.31 | 0.46 | 0 | 0 | 1 | |

| Board_Size | 6.83 | 2.11 | 5 | 7 | 7 | |

| CEO_Ownership | % | 3.21 | 4.75 | 0.10 | 1.30 | 4.59 |

| Dir_Ownership | % | 20.53 | 13.50 | 10.86 | 16.67 | 26.36 |

| Large_Ownership | % | 19.81 | 11.38 | 11.77 | 17.91 | 25.53 |

| Non_IndDir | 0.51 | 0.50 | 0 | 1 | 1 |

5. Empirical Findings

| Dependent Variable: Ln(CEO_Comp) | ||||||

|---|---|---|---|---|---|---|

| Independent Variables | Pred. sign | (1) | (2) | (3) | (4) | (5) |

| Intercept | ? | 11.03*** | 11.22*** | 11.24*** | 11.22*** | 11.25*** |

| (60.06) | (60.11) | (59.98) | (60.29) | (59.95) | ||

| Ret | + | -0.0001 | -0.0001 | -0.0002 | -0.0001 | -0.0001 |

| (-0.87) | (-0.83) | (-1.03) | (-0.94) | (-0.97) | ||

| Roa | + | 0.02*** | 0.02*** | 0.02*** | 0.02*** | 0.02*** |

| (10.57) | (10.59) | (10.43) | (10.59) | (10.26) | ||

| Firm_Size | + | 0.25*** | 0.25*** | 0.25*** | 0.25*** | 0.25*** |

| (19.95) | (19.90) | (20.11) | (19.91) | (20.10) | ||

| Market-to-Book | + | 0.02** | 0.02** | 0.02** | 0.02** | 0.02** |

| (2.07) | (2.07) | (2.04) | (2.06) | (2.05) | ||

| Stdev_Ret † | + | -2.55 | -1.94 | -3.42 | -1.54 | -2.17 |

| (-0.13) | (-0.10) | (-0.18) | (-0.08) | (-0.11) | ||

| Stdev_Roa | + | -0.001 | -0.001 | -0.001 | -0.001 | -0.002 |

| (-0.45) | (-0.44) | (-0.54) | (-0.42) | (-0.64) | ||

| CEO_Chair | + | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 |

| (0.91) | (0.92) | (1.04) | (0.93) | (0.99) | ||

| Board_Size | + | 0.02*** | 0.02*** | 0.02*** | 0.02*** | 0.02*** |

| (3.31) | (3.29) | (2.88) | (3.28) | (2.66) | ||

| CEO_Ownership | ‒ | -0.01* | -0.01** | -0.01** | -0.01** | -0.01** |

| (-1.93) | (-1.97) | (-2.19) | (-1.97) | (-2.14) | ||

| Dir_Ownership | ‒ | -0.01*** | -0.01*** | -0.01*** | -0.01*** | -0.01*** |

| (-5.22) | (-5.20) | (-5.24) | (-5.22) | (-5.22) | ||

| Large_Ownership | ‒ | -0.004*** | -0.004*** | -0.005*** | -0.005*** | -0.004*** |

| (-3.69) | (-3.66) | (-3.79) | (-3.69) | (-3.87) | ||

| Non_IndDir | + | 0.07** | 0.08** | 0.08*** | ||

| (2.53) | (2.40) | (2.59) | ||||

| RC_Setup | ? | 0.23*** | 0.24*** | 0.23*** | ||

| (3.20) | (3.18) | (3.17) | ||||

| Non_IndDir × RC_Setup | ‒ | -0.01 | ||||

| (-0.25) | ||||||

| Ret × RC_Setup | + | 0.001 | ||||

| (0.88) | ||||||

| Non_IndDir × Ret × RC_Setup | + | 0.001 | ||||

| (0.57) | ||||||

| RC_EarlyAdopter | ? | 0.17** | ||||

| (2.53) | ||||||

| Ret × RC_EarlyAdopter | + | 0.003** | ||||

| (2.38) | ||||||

| Year dummies | Controlled | Controlled | Controlled | Controlled | Controlled | |

| Industry dummies | Controlled | Controlled | Controlled | Controlled | Controlled | |

| N | 4,747 | 4,747 | 4,747 | 4,747 | 4,747 | |

| Adjusted R-squared | 0.3406 | 0.3419 | 0.3409 | 0.3420 | 0.3408 | |

6. Conclusions

Acknowledgements

Conflicts of Interest

References

- M. Jensen, and K.J. Murphy. “Performance pay and top-management incentives.” J. Pol. Econ. 98 (1990): 225–264. [Google Scholar]

- B.J. Hall, and J.B. Liebman. “Are CEOs really paid like bureaucrats? ” Quarterly Journal of Economics 113 (1998): 651–692. [Google Scholar]

- Y.H. Yeh, T.S. Lee, and T. Woidtke. “Family control and corporate governance: Evidence from Taiwan.” Int. Rev. Financ. 2 (2001): 21–48. [Google Scholar]

- Y.H. Yeh, and T. Woidtke. “Commitment or Entrenchment? Controlling Shareholders and Board Composition.” J. Bank. Financ. 29 (2005): 1857–1885. [Google Scholar] [CrossRef]

- W.-C. Liu. “Are you ready for remuneration committee? ” Taiwan Corporate Governance Association (TCGA), 2011, (Available online: http://www.cga.org.tw). [Google Scholar]

- E. Fama, and M.C. Jensen. “Separation of ownership and control.” J. Law Econ. 26 (1983): 301–325. [Google Scholar]

- M.C. Jensen. “The modern industrial revolution, exit, and the failure of internal control mechanisms.” J. Financ. 48 (1993): 831–880. [Google Scholar] [CrossRef]

- H. Tosi, J.P. Katz, and R. Gomez-Mejia. “Disaggregating the agency contract: The effects of monitoring, incentive alignment, and term in office on agent decision making.” Acad. Manag. J. 40 (1997): 584–602. [Google Scholar] [CrossRef]

- A. Cadbury. Report of the Committee on the Financial Aspects of Corporate Governance. London, UK: Gee, 1992. [Google Scholar]

- R. Greenbury. Report on Directors Pay. London, UK: Gee, 1995. [Google Scholar]

- C.M. Daily, J.L. Johnson, A.E. Ellstrand, and D.R. Dalton. “Compensation committee composition as a determinant of CEO compensation.” Acad. Manag. J. 41 (1998): 209–220. [Google Scholar] [CrossRef]

- J.S. Linck, J.M. Netter, and T. Yang. “The determinants of board structure.” J. Financ. Econ. 87 (2008): 308–328. [Google Scholar] [CrossRef]

- S. Rosenstein, and J.G. Wyatt. “Outside directors, board independence and shareholder wealth.” J. Financ. Econ. 26 (1990): 175–191. [Google Scholar] [CrossRef]

- M.J. Conyon, and S.I. Peck. “Board control, remuneration committees, and top management compensation.” Acad. Manag. J. 41 (1998): 146–157. [Google Scholar] [CrossRef]

- H.A. Newman, and H.A. Mozes. “Does the composition of the compensation committee influence CEO compensation practices? ” Financ. Manag. 28 (1999): 41–53. [Google Scholar] [CrossRef]

- C.S. Mishra, and J.F. Nielsen. “Board independence and compensation policies in large bank holding companies.” Financial Management 28 (2000): 51–70. [Google Scholar] [CrossRef]

- N. Vafeas, J.F. Waegelein, and M. Papamichael. “The response of commercial banks to compensation reform.” Rev. Quant. Finan. Acc. 20 (2003): 335–354. [Google Scholar]

- A.L. Boone, L.C. Field, J.M. Karpoff, and C.G. Raheja. “The determinants of corporate board size and composition: An empirical analysis.” J. Financ. Econ. 85 (2007): 66–101. [Google Scholar] [CrossRef]

- S. Finkelstein, and D. Hambrick. Strategic Leadership: Top Executive and their Effects on Organizations. Eagan, MN, USA: West Publishing Company, 1996. [Google Scholar]

- L. Cohen, A. Frazzini, and C. Malloy. “Hiring cheerleaders: Board appointments of “independent” directors.” Working paper. Cambridge, MA, USA: Harvard Business School, 2010. [Google Scholar]

- R.C. Anderson, and J.M. Bizjak. “An empirical examination of the role of the CEO and the compensation committee in structuring executive pay.” J. Bank. Financ. 27 (2003): 1323–1348. [Google Scholar] [CrossRef]

- T. Perry, and M. Zenner. “Pay for performance? Government regulation and the structure of compensation contracts.” J. Financ. Econ. 62 (2001): 453–488. [Google Scholar] [CrossRef]

- C. O’Reilly, B. Main, and G. Crystal. “CEO compensation as tournament and social comparison.” Admin. Sci. Q. 33 (1988): 257–274. [Google Scholar]

- M. Ezzamel, and R. Watson. “Executive Remuneration and Corporate Performance.” In Corporate Governance: Responsibilities, Risks and Remuneration. Edited by K. Keasey and M. Wright. Chichester, UK: Wiley, 1997, pp. 61–92. [Google Scholar]

- B.G.M. Main, and J. Johnson. “Remuneration committees and corporate governance.” Accounting and Business Research. 23 (1993): 351–362. [Google Scholar] [CrossRef]

- S. Young. “The increasing use of non-executive directors: Its impact on UK board structure and governance arrangements.” J. Bus. Financ. Acc. 27 (2000): 1311–1348. [Google Scholar]

- C. Laux, and V. Laux. “Board committees, CEO compensation, and earnings management.” Acc. Rev. 84 (2009): 869–891. [Google Scholar] [CrossRef]

- J. Sun, S.F. Cahan, and D. Emanuel. “Compensation committee governance quality, chief executive officer stock option grants, and future firm performance.” J. Bank. Financ. 33 (2009): 1507–1519. [Google Scholar] [CrossRef]

- M. Mace. Directors: Myth and Reality. Boston, MA, USA: Harvard Business School Press, 1986. [Google Scholar]

- P. Jiraporn, M. Singh, and C.I. Lee. “Ineffective corporate governance: Director busyness and board committee memberships.” J. Bank. Financ. 33 (2009): 819–828. [Google Scholar] [CrossRef]

- S. Gilson. “Bankruptcy, boards, banks, and blockholders.” J. Financ. Econ. 27 (1990): 355–387. [Google Scholar] [CrossRef]

- S. N. Kaplan, and D. Reishus. “Outside directorships and corporate performance.” J. Financ. Econ. 27 (1990): 389–410. [Google Scholar] [CrossRef]

- H.E. Ryan Jr., and R. Wiggins III. “Who is in whose pocket? Director compensation, board independence, and barriers to effective monitoring.” J. Financ. Econ. 73 (2004): 497–524. [Google Scholar] [CrossRef]

- J.E. Core, R.W. Holthausen, and D.F. Larcker. “Corporate governance, chief executive officer compensation and firm performance.” J. Financ. Econ. 51 (1999): 371–406. [Google Scholar] [CrossRef]

- D. Yermack. “Companies’ modest claims about the value of CEO stock options awards.” Rev. Quant. Financ. Acc. 10 (1998): 207–226. [Google Scholar] [CrossRef]

- T.A. Baker. “Option reporting and the political costs of CEO pay.” J. Acc. Auditing Financ. 14 (1999): 125–145. [Google Scholar]

- F. Elloumi, and J. Gueyie. “CEO compensation, IOS and the role of corporate governance.” Corp. Gov. 1 (2001): 23–33. [Google Scholar] [CrossRef]

- C.W. Smith, and R.L. Watts. “The investment opportunity set and corporate financing dividend and compensation policies.” J. Financ. Econ. 32 (1992): 263–292. [Google Scholar] [CrossRef]

- R. Lambert, D. Larcker, and K. Weigelt. “The structure of organizational incentives.” Adm. Sci. Q. 38 (1993): 438–461. [Google Scholar] [CrossRef]

- Amacom. Executive Compensation Service: Top Management Report. New York, USA: American Management Association, 1975. [Google Scholar]

- W.K. Newey, and K.D. West. “A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix.” Econometrica 55 (1987): 703–708. [Google Scholar] [CrossRef]

- 1According to the Securities and Exchange Law (Article 14-6), a company whose stock is listed on the Taiwan stock exchange (TSE) or traded in the over-the-counter (OTC) market shall establish a remuneration committee. Regulations governing the professional qualifications for its members, the exercise of their powers of office, and related matters shall be prescribed by the Financial Supervisory Committee (FSC). Top executive remuneration includes cash salary, stock options, stock bonuses, retirement benefits and severance pay, various subsidies and allowances, and other material incentives.

- 2For example, [5].

- 3Relatedly, the Greenbury Committee [10] urged the adoption of RCs consisting of solely nonexecutive directors. Similarly, the U.S. Securities and Exchange Committee (SEC) in 1992 adopted provisions encouraging nonexecutive directors to be more responsible for establishing executive pay by increasing disclosure requirements when corporate insiders serve on RCs. In addition, the 1993 congressional tax code stipulates that RCs must be composed solely of two or more nonexecutive directors, or performance-based executive pay in excess of USD $1 million is not tax deductible. The listing requirements of the New York Stock Exchange (NYSE) and NASDAQ mandate majority-independent boards. The NYSE also requires entirely independent compensation committees. The NASDAQ rules are similar, while more flexible, than the NYSE (e.g., [11,12]).

- 4However, this position does not necessarily imply an association between affiliated or interdependent RC members and CEO compensation [11, 15]. One possible reason for this is that affiliated or interdependent directors serving on a powerful committee are mindful of their duty to shareholders, regardless of their level of dependence [11].

- 5In contrast to the alternative form, the null hypothesis states that voluntary appointment of independent directors has no impact on the levels of CEO pay. Though prior studies have provided conflicting evidence regarding how the independence of boards affects the CEO pay levels, to the extent that the board independence can reasonably reduce the agency cost we expect to observe a higher level of CEO pay for non-adopters of independent directors. To formulate hypotheses in an alternative form can be widely seen in prior accounting or finance research papers. In this study we also follow this convention.

- 6Moreover, [26] suggested that the increasing use of non-executive directors has a positive impact on U.K. board structure and governance arrangements.

- 7To test our hypotheses, we need to control for the effects of CEO pay determinants which can affect the CEO pay level but are irrelevant to our research questions. Therefore, in our model specification, we include economic determinants of top executive pay, including firm growth potential, operating risk, firm size and firm performance [34,35,36].

- 8One major reason for the use of log-transformed CEO compensation in our regression analysis is that the “guide charts” are constructed by regressing the logarithm of pay on the logarithm of firm size (e.g., [40]). This practice is widely used by human resource consultants to determine the pay levels [34].

- 9We do not use a lag structure in our model specification because our interest is mainly on the contemporaneous pay-performance association and the levels of CEO pay are determined largely on the firm performance rather than on the pay level for the previous period. In addition, the year-dummies and industry-dummies are chosen based on the sample period (i.e., 2008–2011) and 27 industry sectors, based on the TSE industry classification codes.

- 10If sample firms do not meet the listing requirements of TSE for some reasons (e.g., financial distress), they are required to stop trading temporarily or delisted by the authority. This is the main reason why the stock price, financial and CEO pay data are missing.

- 11Untabulated statistics show that the average CEO annual compensation increases over the 2008-2010 period. The means of the midpoint of CEO annual pay are NT$ 4.64 (NT$ 4.71 and NT$ 5.41) million for 2008 (2009 and 2010). However, the mean drops a little in 2011, which is NT$ 5.28 million.

- 12For the regression analysis of the first hypothesis, we conduct two sets of diagnostic tests. First, we run Breusch-Pagan test for heteroskedasticity. The chi-square is 8.54, which rejects the null of constant variance at the 1% significance level. Second, we run the test for autocorrelation in the panel data; the F-statistics is 75.42, which reject the null of no first-order autocorrelation at the 1% significance level. To address these issues, we calculate the t-statistics (in parentheses) based on [41] heteroskedasticity and autocorrelation-consistent standard errors. Since the diagnostic checks for regression analyses from the second to the fifth hypotheses all reject the null of homogeneity of variance and no autocorrelation, in Table 3 we report t-statistics based on [41] heteroskedasticity and autocorrelation-consistent standard errors for all test results.

- 13We notice that the adjusted R-squares reported in Table 3 seem comparable. Even though some of the above coefficient estimates are significant, Non_IndDir, RC_Setup, Non_IndDir × RC_Setup, Ret × RC_Setup, Non_IndDir × Ret × RC_Setup, RC_EarlyAdopter and Ret×RC_EarlyAdopter have negligible explanatory power for ln(CEO_Comp), causing adjusted R-squares to remain barely unchanged.

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Kuo, C.-S.; Yu, S.-T. Remuneration Committee, Board Independence and Top Executive Compensation. J. Risk Financial Manag. 2014, 7, 28-44. https://doi.org/10.3390/jrfm7020028

Kuo C-S, Yu S-T. Remuneration Committee, Board Independence and Top Executive Compensation. Journal of Risk and Financial Management. 2014; 7(2):28-44. https://doi.org/10.3390/jrfm7020028

Chicago/Turabian StyleKuo, Chii-Shyan, and Shih-Ti Yu. 2014. "Remuneration Committee, Board Independence and Top Executive Compensation" Journal of Risk and Financial Management 7, no. 2: 28-44. https://doi.org/10.3390/jrfm7020028