3.2. Trading Rules

The ten-day returns for our

MACD and

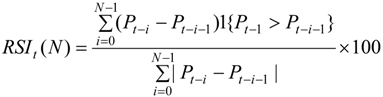

RSI trading rules are summarized in

Table 2A to

Table 3F. In these tables, “N(Buy)” and “N(Sell)” in the second and third columns respectively denote the number of buy-and-sell signals produced during the sample period. “Buy” and “Sell” in the next two columns in each table refer to the average ten-day returns generated by the corresponding buy-and-sell signals. Note that a negative return from the sell signal implies a positive profit. The

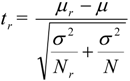

t-statistics reported in these two columns test the null hypothesis of equality between the return generated by the trading rule (

μr) and the buy-and-hold return (

μ),

i.e.,

![Jrfm 07 00001 i003]()

:

μr =

μ, where

r denotes buy or sell. Following Brock

et al. (1992), the

t-statistic for buy or sell returns is computed as:

where

μ is the mean ten-day return of the sample,

μr is the mean ten-day return of buy or sell signal, and

Nr is the number of buy or sell signals. σ

2 and

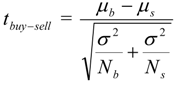

N are the estimated variances and the number of observations of the sample, respectively. “Buy > 0” and “Sell > 0” in the sixth and seventh columns refer to the fractions of times that the associated buy-and-sell signals are higher than zero. “Buy–Sell” in the last column contains the returns from buy signals less those from their sell signal counterparts. The null hypothesis of zero profit (

![Jrfm 07 00001 i005]()

=0) against the alternative of positive profit (

![Jrfm 07 00001 i006]()

> 0) is tested using the following test statistic:

where

μb and

μs denote the mean ten-day returns of buy-and-sell signals, respectively, whereas

Nb and

Ns refer to the number of the corresponding buy-and-sell signals.

Rule 1

Table 2A summarizes the average ten-day return from the MACD(12,26,0) rule. The

MACD(12,26,0) rule performs well in the Milan Comit General and the S&P/TSX Composite indices. The null hypothesis of the equality between returns from market indicators and the buy-and-hold strategy is rejected at conventional significance levels. This suggests that the trading strategy outperforms the buy-and-hold strategy. The most profitable buy (sell) signal appears in the Milan Comit General index with an average ten-day return of 1.379%. Note that the buy–sell returns are significantly positive. For the S&P/TSX Composite Index, both the null hypotheses are rejected at the 5% significance level.

Table 2A.

Average ten-day returns from MACD(12,26,0).

Table 2A.

Average ten-day returns from MACD(12,26,0).

| Sample Period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 75 | 79 | 0.01093 | −0.00286 | 0.667 | 0.506 | 0.01379 * |

| | | | (1.236) | (−1.220) | | | (1.746) |

| S&P/TSX Composite Index | 72 | 82 | 0.01159 ** | −0.00177 | 0.694 | 0.549 | 0.01335 ** |

| | | | (2.321) | (−1.295) | | | (2.593) |

| DAX 30 | 78 | 84 | 0.00404 | −0.00008 | 0.564 | 0.488 | 0.00411 |

| | | | (0.350) | (−0.602) | | | (0.674) |

| Dow Jones Industrials | 93 | 104 | 0.00464 | 0.00534 | 0.624 | 0.615 | −0.00070 |

| | | | (0.386) | (0.628) | | | (−0.152) |

| Nikkei 225 Stock Average | 78 | 88 | 0.00457 | 0.00485 | 0.551 | 0.602 | −0.00029 |

| | | | (0.866) | (0.992) | | | (−0.050) |

Rule 2

Table 2B shows the results of the MACD(12,26,9) rule. For Germany, the performance of this rule is far from satisfactory. The rule is unable to yield a higher profit than the buy-and-hold strategy. The buy–sell return is significantly negative at the 5% level, suggesting that investors who follow the trading signals of MACD(12,26,9) will suffer a negative return of 0.944% from a pair of buy-and-sell signals. The loss is sizeable compared to the positive buy-and-hold return of 0.249%.

Table 2B.

Average ten-day returns from MACD(12,26,9).

Table 2B.

Average ten-day returns from MACD(12,26,9).

| Sample Period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 157 | 164 | 0.00367 | 0.00307 | 0.529 | 0.561 | 0.00060 |

| | | | (−0.058) | (−0.215) | | | (0.110) |

| S&P/TSX Composite Index | 161 | 162 | 0.00254 | 0.00243 | 0.522 | 0.519 | 0.00011 |

| | | | (−0.111) | (−0.155) | | | (0.031) |

| DAX 30 | 168 | 182 | −0.00201 | 0.00743 * | 0.524 | 0.593 | −0.00944 ** |

| | | | (−1.484) | (1.693) | | | (−2.272) |

| Dow Jones Industrials | 178 | 167 | −0.00006 | 0.00436 | 0.545 | 0.527 | −0.00442 |

| | | | (−1.390) | (0.405) | | | (−1.274) |

| Nikkei 225 Stock Average | 175 | 154 | 0.00078 | −0.00088 | 0.566 | 0.513 | 0.00166 |

| | | | (−0.064) | (−0.616) | | | (0.410) |

Among the five series examined, the trading rules perform the worst in the DAX 30. For the remaining series, the

MACD(12,26,9) has no predictability. As the combination of eight-day, seventeen-day

EMAs and signal line crossover can produce more reliable buy signals [

21], we also examine the

MACD(8,17,9) rule in this paper. From

Table 2C, the return from buy signals is negative for Italy. For Germany, the

MACD(8,17,9) rule produces sell signals which yield negative returns. The buy–sell returns are also significantly negative at the 5% level for both countries.

Table 2C.

Average ten-day returns from MACD(8,17,9).

Table 2C.

Average ten-day returns from MACD(8,17,9).

| Sample Period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 194 | 185 | −0.00272 * | 0.00738 | 0.448 | 0.589 | −0.01010 ** |

| | | | (−1.857) | (0.953) | | | (−2.007) |

| S&P/TSX Composite Index | 186 | 197 | 0.00424 | 0.00158 | 0.575 | 0.518 | 0.00266 |

| | | | (0.599) | (−0.539) | | | (0.816) |

| DAX 30 | 201 | 190 | −0.00143 | 0.00755 * | 0.512 | 0.621 | −0.00898 ** |

| | | | (−1.412) | (1.770) | | | (−2.286) |

| Dow Jones Industrials | 205 | 194 | 0.00242 | 0.00294 | 0.566 | 0.593 | −0.00051 |

| | | | (−0.402) | (−0.172) | | | (−0.160) |

| Nikkei 225 Stock Average | 195 | 193 | −0.00069 | 0.00022 | 0.513 | 0.523 | −0.00090 |

| | | | (−0.620) | (−0.278) | | | (−0.244) |

Rule 3

From

Table 3A, the RSI(7,50) rule generates negative returns in the Milan Comit General. The results in

Table 3B indicate that the 14-day RSI rule has some predictability too. In general, the buy–sell values are positive, implying that the rule is profitable. In most cases, the RSI(14,50) rule is able to generate profits. The predictability of the trading rule for the 21-day RSI is reported in

Table 3C. The rule beats the buy-and-hold strategy in the Milan Comit General and the S&P/TSX Composite.

Table 3A.

Average ten-day returns from RSI(7, 50).

Table 3A.

Average ten-day returns from RSI(7, 50).

| Sample Period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 188 | 199 | −0.00215 * | 0.00668 | 0.463 | 0.558 | −0.00884 * |

| | | | (−1.671) | (0.791) | | | (−1.774) |

| S&P/TSX Composite Index | 171 | 216 | 0.00232 | 0.00175 | 0.526 | 0.528 | 0.00057 |

| | | | (−0.203) | (−0.488) | | | (0.176) |

| DAX 30 | 168 | 224 | 0.00123 | 0.00663 | 0.560 | 0.589 | −0.00541 |

| | | | (−0.416) | (1.571) | | | (−1.364) |

| Dow Jones Industrials | 176 | 231 | 0.00312 | 0.00028 | 0.580 | 0.528 | 0.00284 |

| | | | (−0.089) | (−1.422) | | | (0.882) |

| Nikkei 225 Stock Average | 182 | 205 | −0.00066 | 0.00135 | 0.549 | 0.556 | −0.00201 |

| | | | (−0.591) | (0.151) | | | (−0.541) |

Table 3B.

Average ten-day returns from RSI(14, 50).

Table 3B.

Average ten-day returns from RSI(14, 50).

| Sample Period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 136 | 129 | 0.00433 | −0.00488** | 0.515 | 0.442 | 0.00921 |

| | | | (0.102) | (−2.017) | | | (1.530) |

| S&P/TSX Composite Index | 128 | 150 | 0.00372 | 0.00069 | 0.539 | 0.5 | 0.00303 |

| | | | (0.318) | (−0.809) | | | (0.791) |

| DAX 30 | 142 | 165 | 0.00427 | 0.00082 | 0.542 | 0.527 | 0.00345 |

| | | | (0.540) | (−0.546) | | | (0.776) |

| Dow Jones Industrials | 145 | 174 | 0.00492 | 0.00318 | 0.607 | 0.5 | 0.00174 |

| | | | (0.585) | (−0.064) | | | (0.481) |

| Nikkei 225 Stock Average | 144 | 163 | 0.00430 | −0.00031 | 0.597 | 0.503 | 0.00461 |

| | | | (1.084) | (−0.439) | | | (1.103) |

Table 3C.

Average ten-day returns from RSI(21, 50).

Table 3C.

Average ten-day returns from RSI(21, 50).

| Sample Period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 111 | 104 | 0.01200 * | −0.01069 ** | 0.613 | 0.404 | 0.02268 ** |

| | | | (1.728) | (−3.014) | | | (3.394) |

| S&P/TSX Composite Index | 119 | 111 | 0.00614 | −0.00271 * | 0.546 | 0.450 | 0.00885 * |

| | | | (1.127) | (−1.813) | | | (2.105) |

| DAX 30 | 118 | 126 | 0.00455 | 0.00178 | 0.576 | 0.524 | 0.00278 |

| | | | (0.572) | (−0.204) | | | (0.558) |

| Dow Jones Industrials | 119 | 146 | 0.00287 | 0.00153 | 0.597 | 0.541 | 0.00134 |

| | | | (−0.160) | (−0.674) | | | (0.337) |

| Nikkei 225 Stock Average | 122 | 121 | 0.00016 | −0.00055 | 0.525 | 0.479 | 0.00071 |

| | | | (−0.239) | (−0.449) | | | (0.151) |

Table 3D.

Average ten-day returns from RSI(7, 30/70).

Table 3D.

Average ten-day returns from RSI(7, 30/70).

| Sample Period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 189 | 211 | −0.00504 ** | 0.00659 | 0.444 | 0.545 | −0.01163 ** |

| | | | (−2.475) | (0.786) | | | (−2.371) |

| S&P/TSX Composite Index | 177 | 232 | 0.00179 | 0.00561 | 0.497 | 0.569 | −0.00382 |

| | | | (−0.425) | (1.311) | | | (−1.201) |

| DAX 30 | 187 | 243 | 0.00226 | 0.00268 | 0.540 | 0.527 | −0.00042 |

| | | | (−0.081) | (0.076) | | | (−0.112) |

| Dow Jones Industrials | 192 | 239 | 0.00574 | 0.00217 | 0.557 | 0.552 | 0.00357 |

| | | | (1.018) | (−0.552) | | | (1.143) |

| Nikkei 225 Stock Average | 187 | 229 | −0.00339 | 0.00210 | 0.513 | 0.559 | −0.00549 |

| | | | (−1.604) | (0.464) | | | (−1.523) |

Table 3E.

Average ten-day returns from RSI(14, 30/70).

Table 3E.

Average ten-day returns from RSI(14, 30/70).

| Sample period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 132 | 158 | −0.00242 | 0.00783 | 0.492 | 0.614 | −0.01025 * |

| | | | (−1.468) | (0.997) | | | (−1.774) |

| S&P/TSX Composite Index | 127 | 169 | 0.00569 | 0.00175 | 0.614 | 0.533 | 0.00393 |

| | | | (1.003) | (−0.429) | | | (1.050) |

| DAX 30 | 114 | 167 | 0.00135 | 0.01049 ** | 0.491 | 0.653 | −0.00914 * |

| | | | (−0.312) | (2.628) | | | (−1.937) |

| Dow Jones Industrials | 111 | 164 | 0.01017 ** | 0.00367 | 0.658 | 0.585 | 0.00650 |

| | | | (2.217) | (0.128) | | | (1.643) |

| Nikkei 225 Stock Average | 125 | 164 | −0.00114 | −0.00031 | 0.496 | 0.518 | −0.00083 |

| | | | (−0.636) | (−0.440) | | | (−0.191) |

Table 3F.

Average ten-day returns from RSI(21, 30/70).

Table 3F.

Average ten-day returns from RSI(21, 30/70).

| Sample period (76-02) | N(Buy) | N(Sell) | Buy | Sell | Buy > 0 | Sell > 0 | Buy–Sell |

|---|

| Milan Comit General | 93 | 127 | −0.00842 ** | 0.00424 | 0.398 | 0.559 | −0.01266* |

| | | | (−2.410) | (0.077) | | | (−1.894) |

| S&P/TSX Composite Index | 74 | 127 | 0.00074 | −0.00076 | 0.541 | 0.520 | 0.00150 |

| | | | (−0.558) | (−1.254) | | | (0.322) |

| DAX 30 | 66 | 113 | −0.00415 | 0.00409 | 0.470 | 0.584 | −0.00824 |

| | | | (−1.383) | (0.435) | | | (−1.370) |

| Dow Jones Industrials | 60 | 110 | 0.00085 | 0.00386 | 0.5 | 0.609 | −0.00301 |

| | | | (−0.598) | (0.166) | | | (−0.583) |

| Nikkei 225 Stock Average | 70 | 118 | −0.00366 | 0.00351 | 0.514 | 0.559 | −0.00717 |

| | | | (−1.052) | (0.752) | | | (−1.301) |

Rule 4

From

Table 3D, most series have negative returns under the

RSI(7, 30/70) rule. The return in Milan Comit General is significantly negative. The loss is 1.163% from a pair of buy-and-sell transactions. For other countries, none of the returns is significantly higher than the buy-and-hold strategy. The

RSI(14, 30/70) rule yields negative returns for three series. For the Milan Comit General, a pair of buy-and-sell transactions generate a negative return of 1.03%, while it is −0.91% for the DAX30. Note that the sell signal produces a significant loss of 1.049% for the DAX30. However, the rule slightly outperforms the buy-and-hold strategy in the Dow Jones Industrials. For all other rules, no significant return is found. The

RSI(21, 30/70) rule generates a negative return for the Milan Comit General.

3.3. Transaction Cost

The above results are obtained in the absence of transaction costs. In this section, we relax this assumption. According to the survey of Hudson

et al. [

22] on stockbrokers and stock broking divisions of major clearing banks, the minimum commission fee is at least 0.1%. When the bid-offer spreads of 0.5% and government stamp duty of 0.5% are included, the round-trip transaction cost is at least 1%.

5 They show that technical trading rules of Brock

et al. [

20] do not generate excess returns in the UK market after taking a round-trip transaction cost of 1% into consideration. Mills [

23] also shows that the moving average and trading range breakout rules cannot produce returns higher than the buy-and-hold strategy when a 1% transaction cost is taken into account. Therefore, in this paper, a 1% transaction cost is included to compute the net profits from each of the trading rule.

6 We will focus on the Italian and Canadian markets, which contain the largest number of profitable trading rules. It is found that in the presence of a 1% transaction cost, the

MACD(12,26,0) applied to these two countries are still profitable. For the Milan Comit General Index and S&P/TSX Composite Index, the net profits of the

MACD(12,26,0) rule are 1.021%

7 and 0.776% respectively. Moreover, the average annual return of the

RSI(21,50) rule net of a 1% round-trip transaction cost for the Milan Comit General Index is 5.069%.

: μr = μ, where r denotes buy or sell. Following Brock et al. (1992), the t-statistic for buy or sell returns is computed as:

: μr = μ, where r denotes buy or sell. Following Brock et al. (1992), the t-statistic for buy or sell returns is computed as:

=0) against the alternative of positive profit (

=0) against the alternative of positive profit (  > 0) is tested using the following test statistic:

> 0) is tested using the following test statistic: