How to Generate Economic and Sustainability Reports from Big Data? Qualifications of Process Industry

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Background

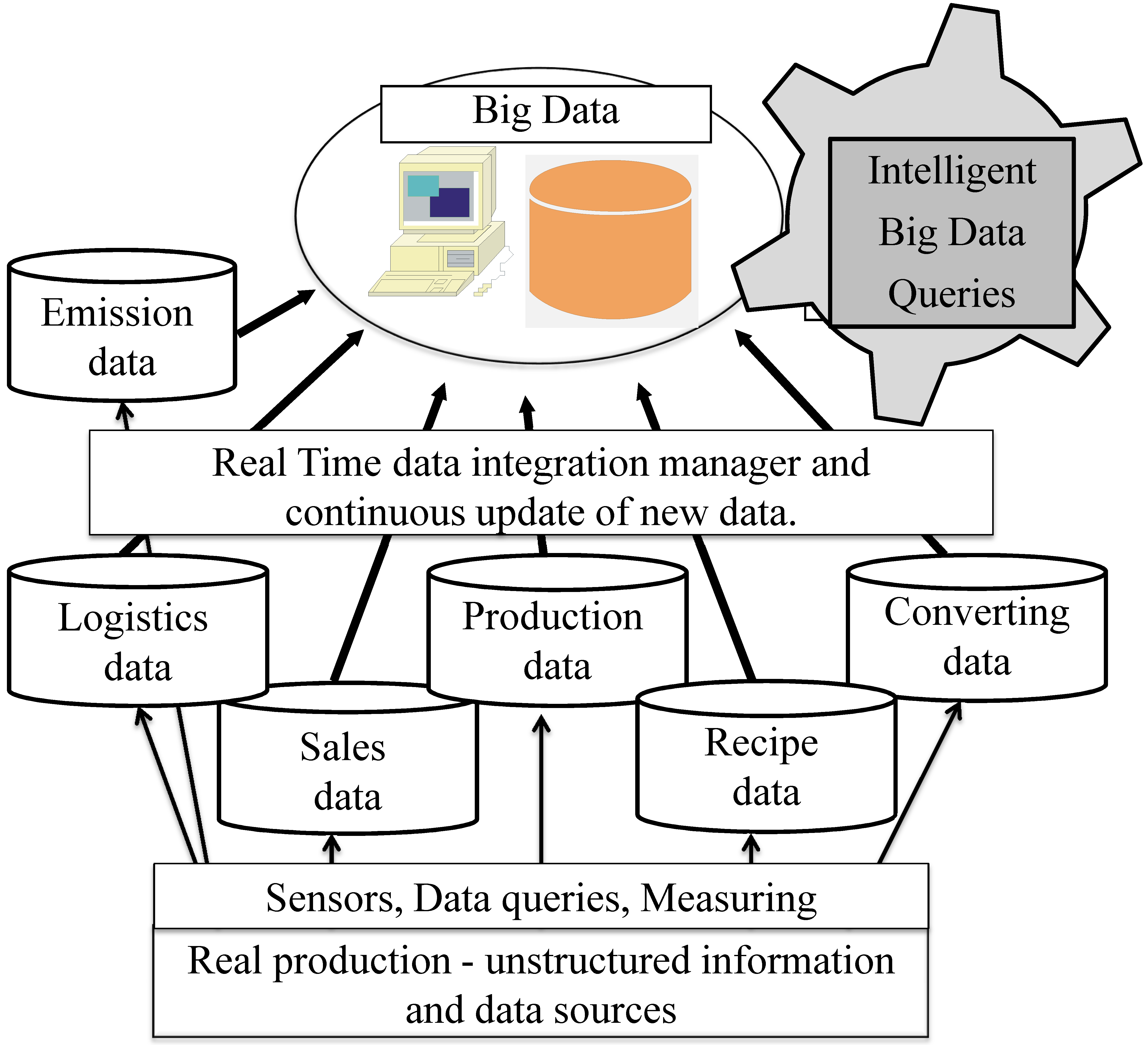

2.1. Big Data

2.2. Refining and Filtering of Big Data

3. Research Topics

3.1. Cost Management

- Unit-level activities—performed each time a unit is produced

- Batch-level activities—performed each time the production of a batch of goods is initiated

- Product-level activities—performed as needed to support the production or marketing of each type of product

- Facility-level activities—which simply sustain a facility’s general manufacturing processes

3.2. Emission and Sustainability Measuring and Calculations

4. Practical Examples from the Process Industry

4.1. Special Qualifications of Process Industry Costing Models

- (1)

- The cost allocations should consider the behavior of processes and materials, and how various products are running through a paper machine line.

- (2)

- So-called fixed costs should be allocated by production throughput, or production tonnes.

- (3)

- The batch costs, which are often considered as other costs, should be allocated per paper tonne, because they normally cannot be measured in any way. In a mill, there are factors, which cannot be measured by grades.

- (4)

- Paper machine costs (or any other machine costs concerning the main process, where a machine is the bottleneck) are the most important ones to consider, because the main production unit is always a bottleneck, and also the most expensive unit on a site. Other ones include raw material problems, logistics challenges, and warehousing and transporting costs from paper mills to customers.

- (5)

- Waste and recycling should be taken into account to make cost calculations more process-inherited. There can be big differences between paper grades in a paper mill in regard to waste and recycling.

- (6)

- There are big requirements for calculating anticipated cost functions in paper production based on corresponding resource consumption. This necessitates that all of the costs and income is estimated or anticipated as accurately as possible beforehand, and that this is done along with continuously updated customer orders, product prices, raw materials, and production data.

- (7)

- The cost model cannot be based on linearity, because the cost and material behavior can be distorted. Cost functions in the paper industry must be nonlinear. Variety should always be considered explicit when making cost calculations for a paper machine, and calculations are normally based on paper machine lines. The machine lines must be integrated with the cost management system so that users are able to receive the results on the mill level. Resolving this topic can offer a fundamental remedy for the Big Data-inherited industrial solution.

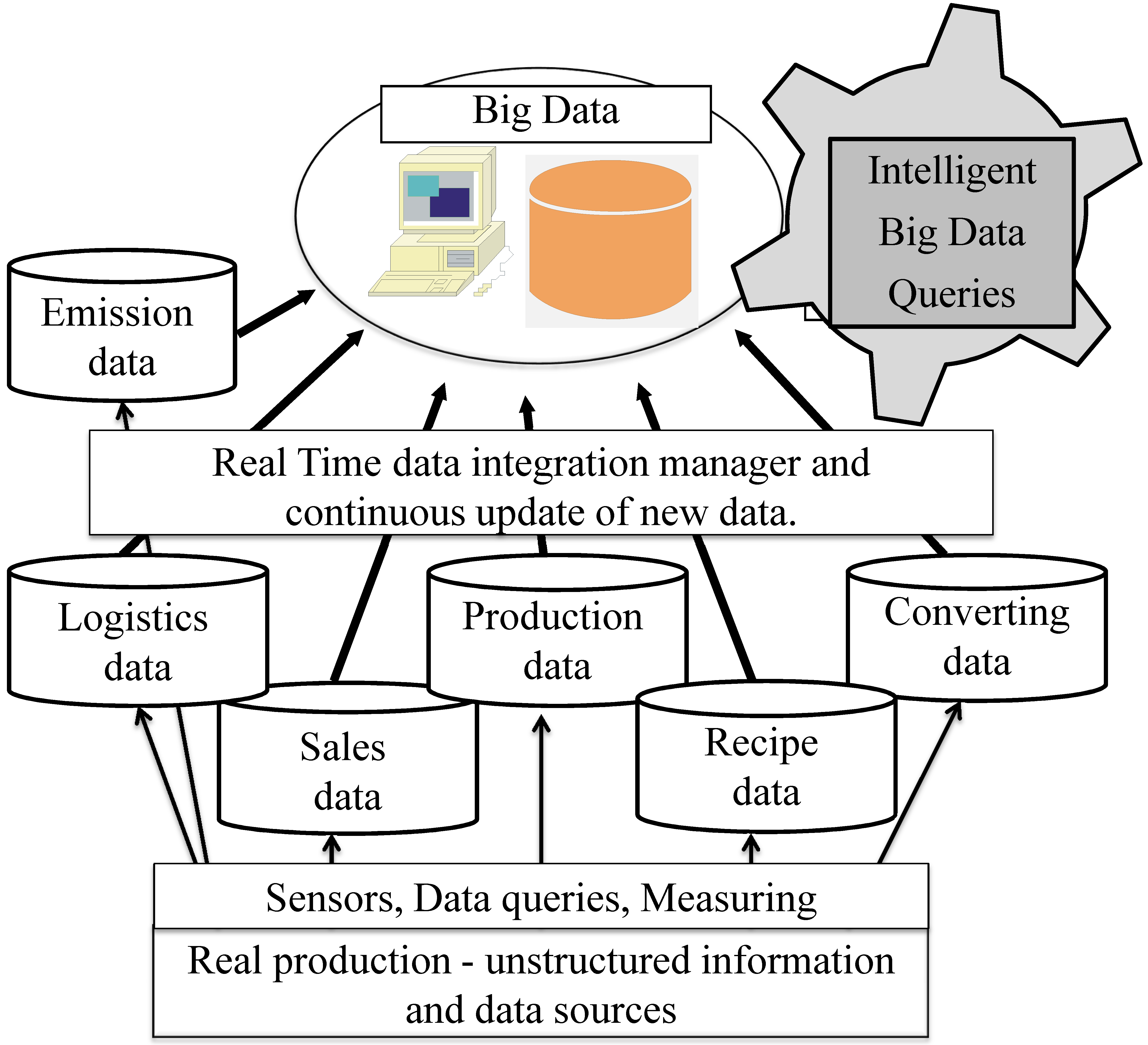

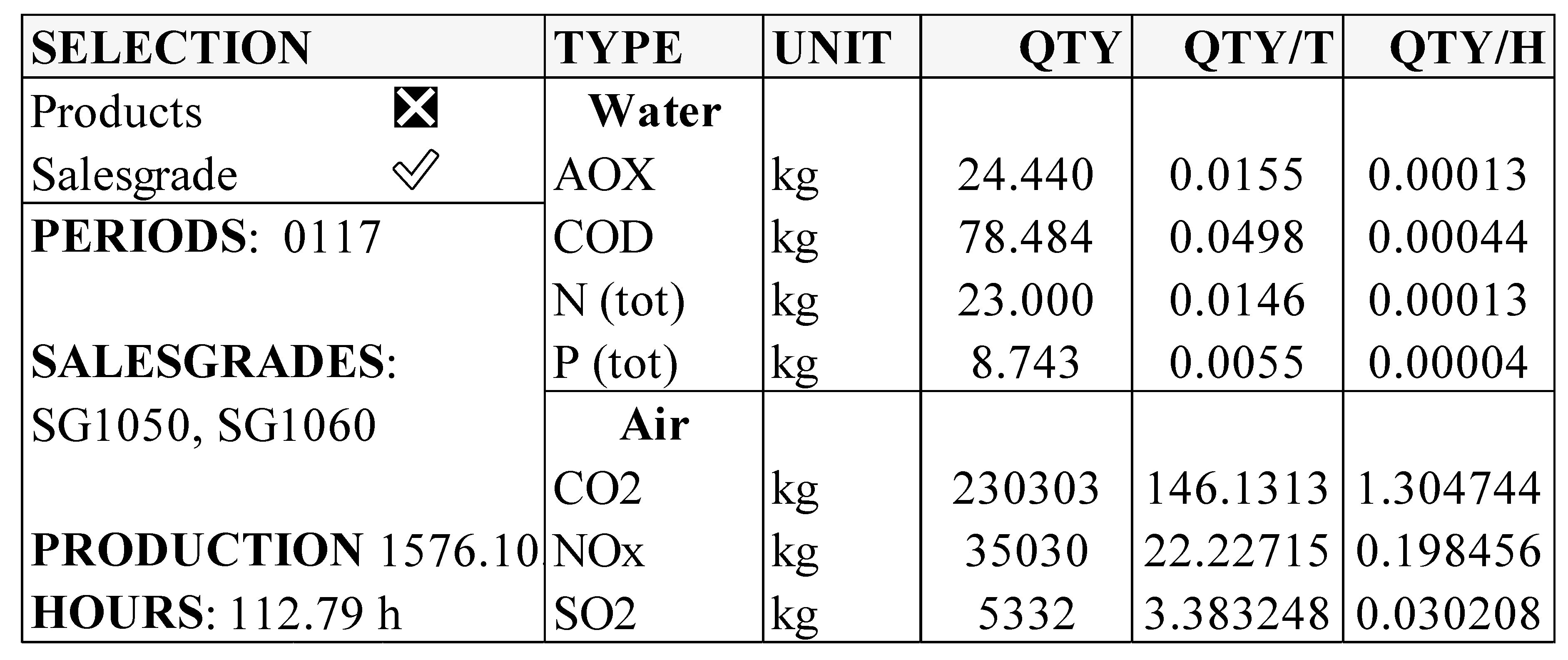

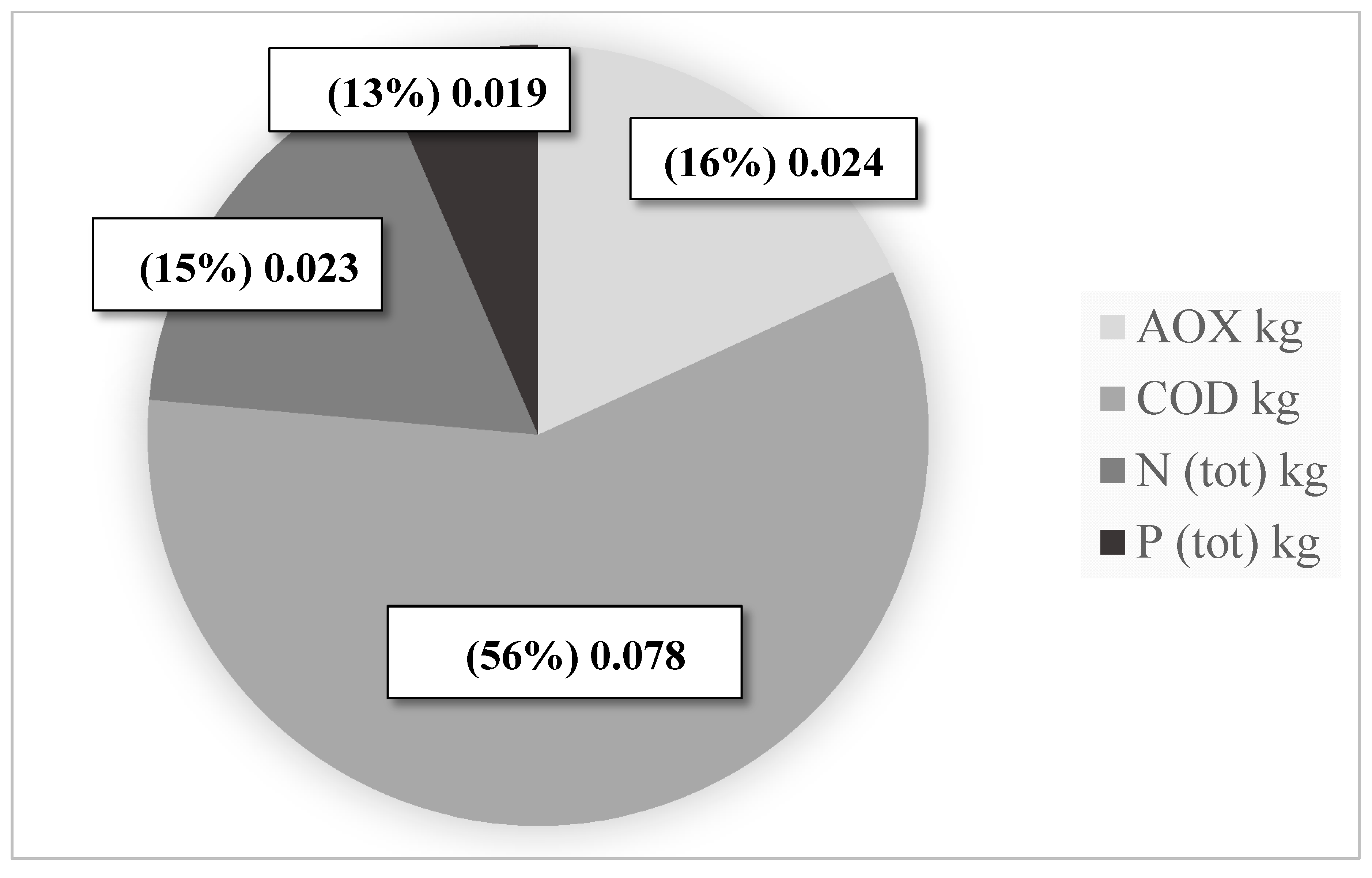

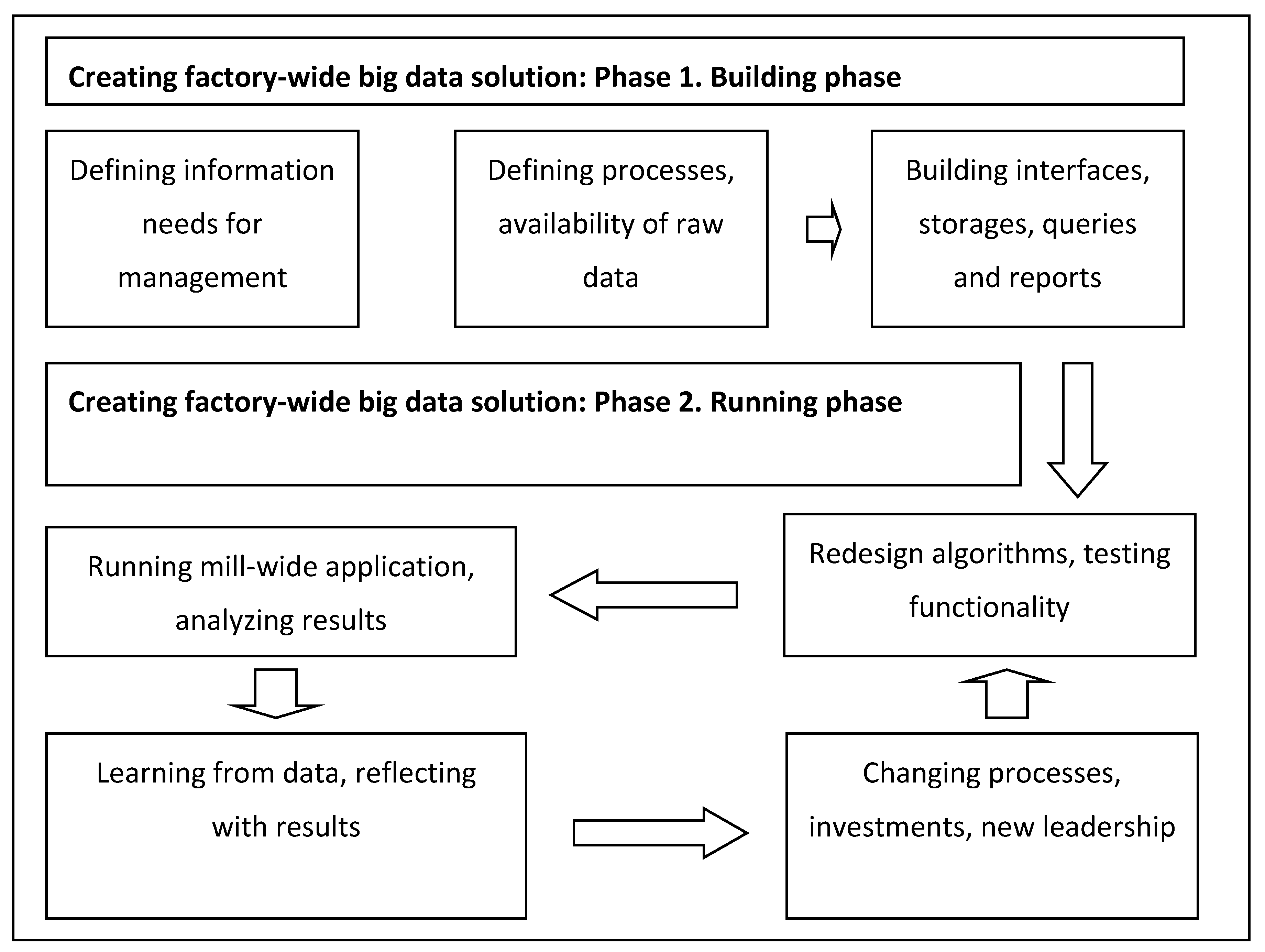

4.2. Creating Big Data by Measuring and Collecting Values from a Real Process

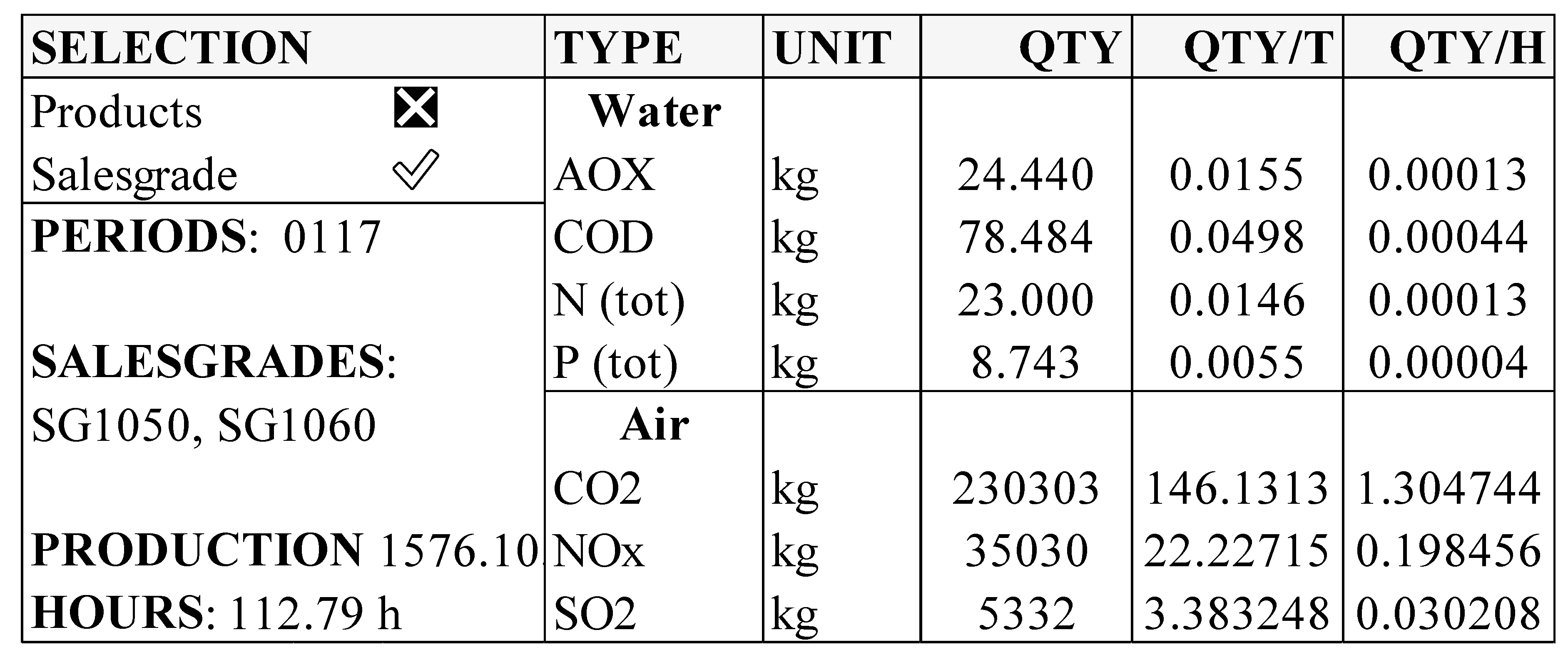

4.3. Data Description; Sources for Profit, Cost and Environment Reporting

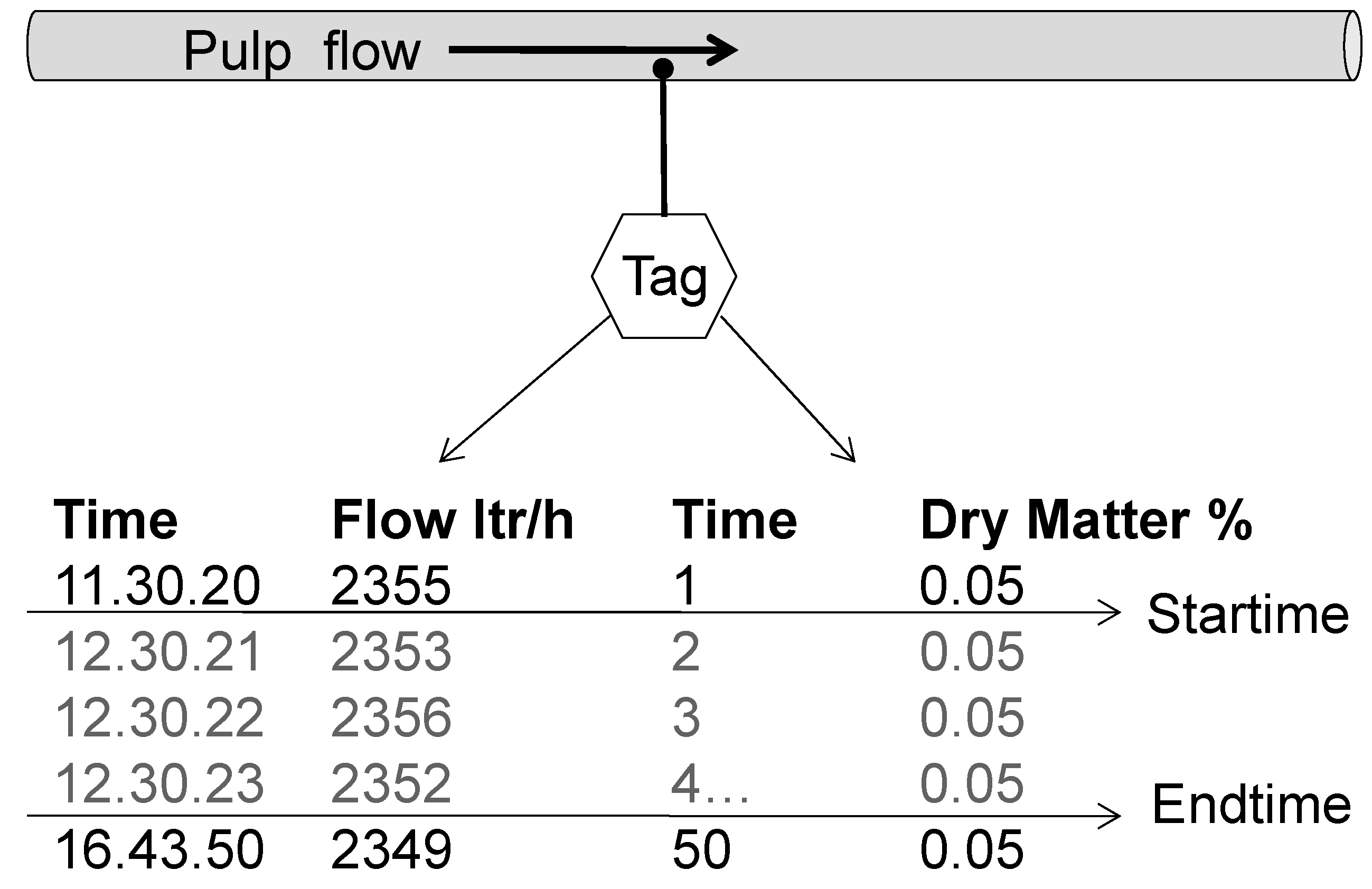

4.4. Transforming Flow Measurements to Mill Big Data

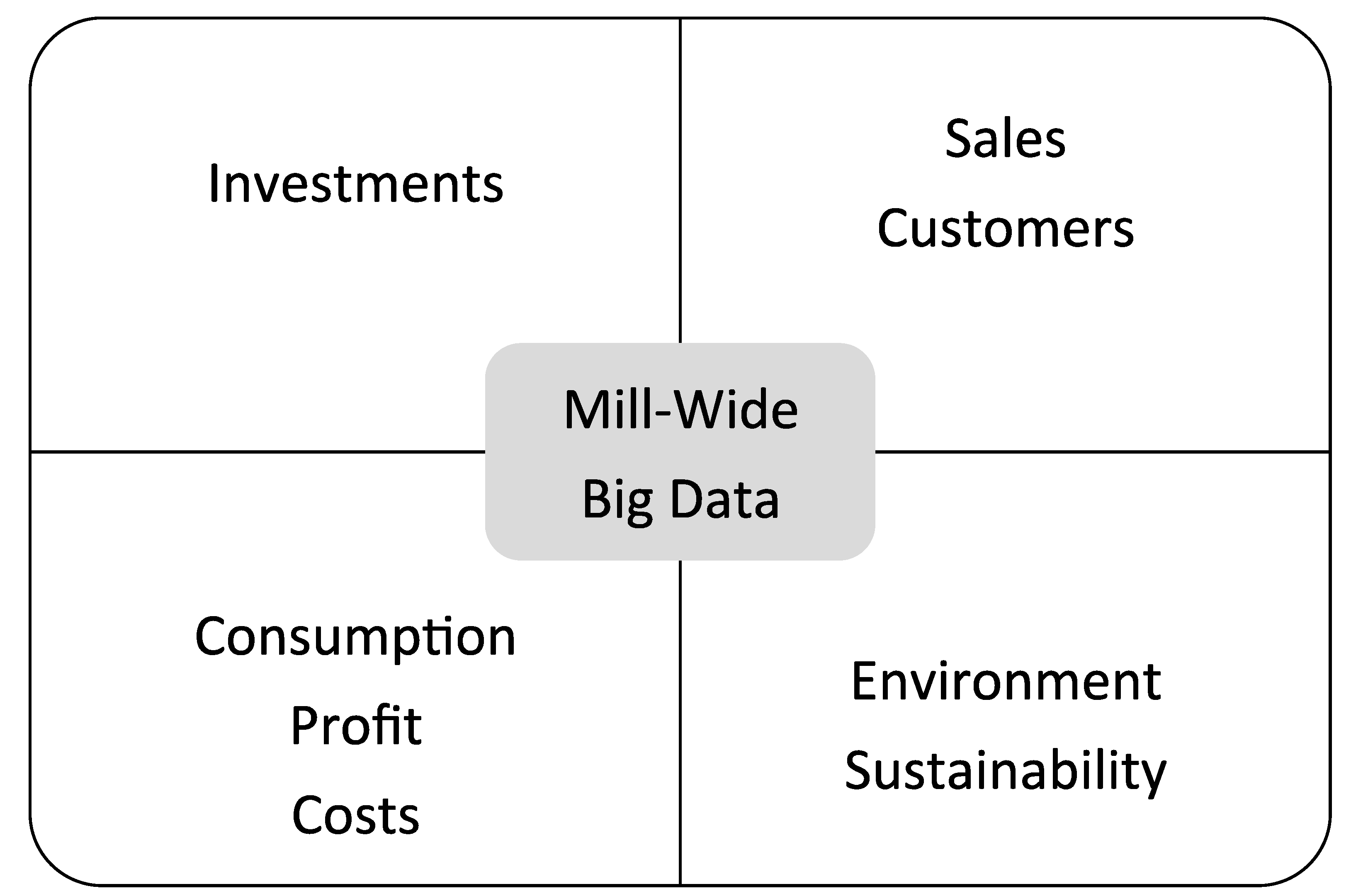

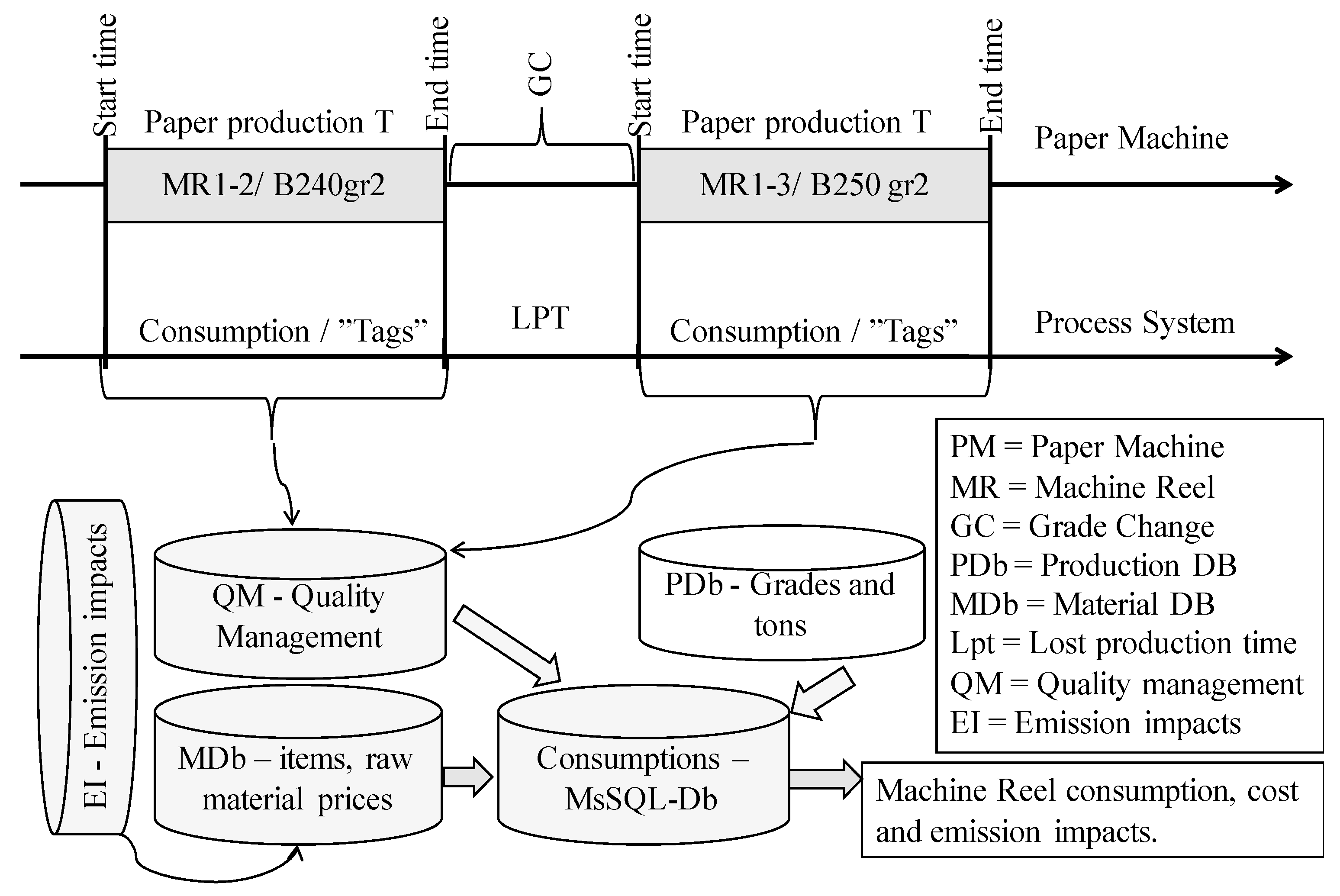

5. Integrated Production and Economic and Emission Reporting

- Emissions: global warming potential, ozone depletion potential, acidification potential, and eutrophication potential.

- Production data: Material consumption and paper production in detail.

- Economic data: From sales down to the gross margin, as an example. In a real production environment, the system composes all necessary economic reports

6. Summary

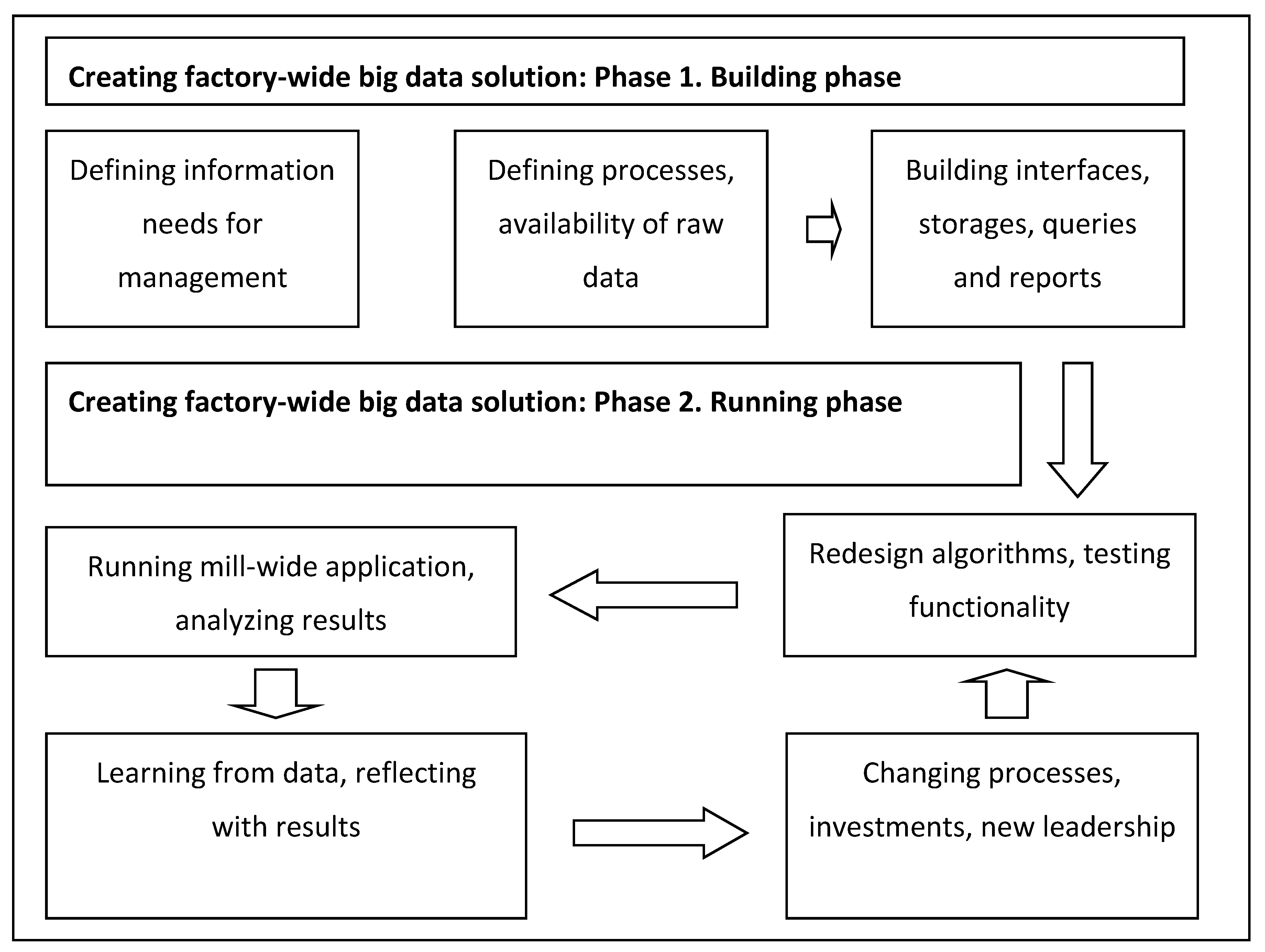

7. Discussion and Conclusions

8. Future Research Views

Author Contributions

Conflicts of Interest

References

- Beer, S. Diagnosing the System; Wiley: Chichester, UK, 1988. [Google Scholar]

- Fogelholm, J. Cost Function Modelling in the Paper Industries; Helsinki University of Technology: Otamedia, Espoo, 2000. [Google Scholar]

- Xu, S.; Lu, B.; Baldea, M.; Edgar, T.F.; Wojsznis, W.; Blevins, T.; Nixon, M. Data cleaning in the process industries. Rev. Chem. Eng. 2015, 31, 453–490. [Google Scholar] [CrossRef]

- Fogelholm, J.; Hämäläinen, E. Economic Reporting in Different Configurations in Paper Mills. IPPTA J. 2003, 15, 37–41. [Google Scholar]

- Weill, P.; Woerner, S.L. Driving in an increasingly digital ecosystem. MIT Sloan Manag. Rev. 2015, 56, 27–34. [Google Scholar]

- Loebbeckeand, C.; Picot, A. Reflections on societal and business model transformation arising from digitization and Big Data analytics: A research agenda. J. Strateg. Inf. Syst. 2015, 24, 149–157. [Google Scholar] [CrossRef]

- Wang, L.; Alexander, C.A. Big Data driven supply chain management and business administration. Am. J. Econ. Bus. Adm. 2015, 7, 60–67. [Google Scholar] [CrossRef]

- Glock, C.H.; Taebok, K. Coordinating a supply chain with a heterogeneous vehicle fleet under greenhouse gas emissions. Int. J. Logist. Manag. 2015, 26, 494–516. [Google Scholar] [CrossRef]

- Gartner. Gartner’s IT Glossary. 2015. Available online: http://www.gartner.com/it-glossary/big-data (accessed on 15 January 2017).

- Anderson, S.W. Managing costs and cost structure throughout the value chain: Research on strategic cost management. In Handbook of Management Accounting Research; Chapman, C.S., Hopwood, A.G., Shields, M.D., Eds.; Elsevier: Oxford, UK, 2007; p. 481. [Google Scholar]

- Zhong, R.Y.; Newman, S.T.; Huang, G.Q.; Lan, S. Big Data for supply chain management in the service and manufacturing sectors: Challenges, opportunities, and future perspectives. Comput. Ind. Eng. 2016, 101, 572–591. [Google Scholar] [CrossRef]

- Wang, G.; Gunasekaran, A.; Ngai, E.W.T.; Papadopoulos, T. Big Data analytics in logistics and supply chain management: Certain investigations for research and applications. Int. J. Prod. Econ. 2016, 176, 98–110. [Google Scholar] [CrossRef]

- Chen, C.P.; Zhang, C.-Y. Data-intensive applications, challenges, techniques and technologies: a survey on Big Data. Inf. Sci. 2014, 275, 314–347. [Google Scholar] [CrossRef]

- Gil, D.; Song, I.-Y. Modelling and management of Big Data: Challenges and opportunities. Futur. Gener. Comput. Syst. 2016, 63, 96–99. [Google Scholar] [CrossRef]

- Chen, R.-H.; Lin, Y.; Tseng, M.-L. Multi-attributes analysis of sustainable development indicators in the construction minerals industry in China. Recour. Policy 2014, 46, 123–133. [Google Scholar] [CrossRef]

- Severson, K.; Chaiwatanodom, P.; Braatz, R.D. Perspectives on process monitoring of industrial systems. Annu. Rev. Control 2016, 42, 190–200. [Google Scholar] [CrossRef]

- Chiang, L.; Lu, B.; Castillo, I. Big Data analytics in chemical engineering. Annu. Rev. Chem. Biomol. Eng. 2017, 8, 63–85. [Google Scholar] [CrossRef] [PubMed]

- Reis, M.S.; Braatz, R.D.; Chiang, L.H. Big Data challenges and future research directions. Chem. Eng. Prog. 2016, 12, 46–50. [Google Scholar]

- Chan, H.K.; He, H.; Wang, Y.C. Green marketing and its impact on supply chain management in industrial markets. Ind. Mark. Manag. 2012, 41, 557–562. [Google Scholar] [CrossRef]

- Qin, S.J. Process data analytics in the era of Big Data. Aiche J. 2014, 60, 3092–3100. [Google Scholar] [CrossRef]

- Koetsier, J. Top 10 Marketing Automation Companies: The VB Index Report. 2014. Available online: http://venturebeat.com/2014/02/26/top-10-marketing-automation-companies-the-vb-index-report/ (accessed on 15 January 2017).

- Larson, E. What Sort of Car-rt-Sort Am I? Junk Mail and the Search for Self Harper’s Magazine. 1989. Available online: http://harpers.org/archive/1989/07/what-sort-of-car-rt-sort-am-i-junk-mail-and-the-search-for-self/ (accessed on 15 January 2017).

- European Commission (EU). Digital Single Market Big Data. 2016. Available online: https://ec.europa.eu/digital-single-market/en/big-data/ (accessed on 15 January 2017).

- Deming, W.E. Out of Crisis; Center for Advanced Engineering Study, The MIT Press: Cambridge, MA, USA, 1986. [Google Scholar]

- Gartner. Gartner Identifies the Top 10 Strategic Technology Trends for 2013. 2012. Available online: http://www.gartner.com/newsroom/id/2209615/ (accessed on 15 January 2017).

- Mantha, B. Five guiding principles for realizing the promise of Big Data. Bus. Intell. J. 2014, 11, 8–11. [Google Scholar]

- Ala-Harja, H.; Helo, P. Green supply chain decisions—Case-based performance analysis from the food industry. Transp. Res. Part E Logist. Transp. Rev. 2015, 74, 11–21. [Google Scholar] [CrossRef]

- Zhu, Q.H.; Sarkis, J. The moderating effect of institutional pressure on emergent green supply chain practices. Int. J. Prod. Res. 2007, 45, 4333–4355. [Google Scholar] [CrossRef]

- Vachon, S.; Klassen, R.D. Extending green practices across supply chain: Impact of upstream and downstream integration. J. Oper. Prod. Manag. 2006, 26, 795–821. [Google Scholar] [CrossRef]

- Van der Vorst, J.G.A.J.; Beulens, A.J.M.; De Wit, W.; Van Beek, P. Supply chain management in food chains: Improving performance by reducing uncertainty. Int. Trans. Oper. Res. 1998, 5, 487–499. [Google Scholar] [CrossRef]

- Wald, A.; Schneider, C.; Schulze, M.; Marfleet, F. A study on the status quo, current trends, and success factors in cost management. Cost Manag. 2013, 27, 28–38. [Google Scholar]

- Wald, A.; Marfleet, F.; Schneider, C.; Gorner, A.; Gleich, R. The Hidden Potential Overhead Cost Reduction: A Study in European Countries. Cost Manag. 2013, 27, 28–38. [Google Scholar]

- Williamson, P. Cost Innovation: Preparing for a “Value-for-Money” revolution. Long Range Plan. 2010, 43, 343–353. [Google Scholar] [CrossRef]

- Rogozhin, A.; Gallaher, M.; Helfand, G.; McManus, M. Using indirect cost multipliers to estimate the total cost of adding new technology in the automobile industry. Int. J. Prod. Econ. 2010, 124, 360–368. [Google Scholar] [CrossRef]

- Reiner, G.; Trcka, M. Customized supply chain design: Problems and alternatives for a production company in the food industry. A simulation based analysis. Int. J. Prod. Econ. 2004, 89, 217–229. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Anderson, S.R. Time-Driven Activity-Based Costing: A Simpler and More Powerful Path to Higher Profits; Harvard Business School Press: Boston, MA, USA, 2007. [Google Scholar]

- Cokins, G. Activity Based Costing: Optional or Required? AACE International Transactions: New Orleans, LA, USA, 2002. [Google Scholar]

- Hämäläinen, E. Economic Geographical Analysis of the Finnish Paper Industry; Annales Universitatis Turkuensis: Turku, Finland, 2011. [Google Scholar]

- Krupnicki, M.; Tyson, T. Using ABC to determine the cost of servicing customers. Manag. Account. 1997, 79, 40–46. [Google Scholar]

- Cooper, R.; Kaplan, R.S. Cost & Effect: Using Integrated Cost Systems to Drive Profitability and Performance; Harvard Business School Press: Boston, MA, USA, 1997. [Google Scholar]

- Zeller, T.L.; Kublank, D.R.; Makris, P.G. How art.com Uses ABC to Succeed. Strateg. Financ. 2001, 82, 1–6. [Google Scholar]

- Cooper, R. Cost classification in unit-based and activity-based manufacturing cost systems. J. Cost Manag. 1990, 4, 4–14. [Google Scholar]

- Askarany, D.; Smith, M.; Yazdifar, H. Technological innovations, activity based costing and satisfaction. J. Account. Bus. Manag. 2007, 14, 53–63. [Google Scholar]

- Chopra, S.; Sodhi, M.S. Managing risk to avoid supply-chain breakdown. MIT Sloan Manag. Rev. 2004, 46, 53–61. [Google Scholar]

- Wu, K.-J.; Liao, C.-J.; Tseng, M.-L.; Lim, M.K.; Hu, J.; Tan, K. Toward sustainability: Using Big Data to explore the decisive attributes of supply chain risks and uncertainties. J. Clean. Prod. 2016, 142 Pt 2, 663–676. [Google Scholar] [CrossRef]

- Belaud, J.-P.; Negny, S.; Dupros, F.; Michéa, D.; Vautrin, B. Collaborative simulation and scientific Big Data analysis: Illustrations for sustainability in natural hazards management and chemical process engineering. Comput. Ind. 2014, 65, 521–535. [Google Scholar] [CrossRef]

- Esteves, A.M.; Franks, D.; Vanclay, F. Social impact assessment: The state of the art, Impact Assessment. Proj. Apprais. 2012, 30, 34–42. [Google Scholar] [CrossRef]

- Marnika, E.; Christodoulou, E.; Xenidis, A. Sustainable development indicators for mining sites in protected areas: Tool development, ranking, and scoring of potential environmental impacts and assesment of management scenarios. J. Clean. Prod. 2015, 191, 59–70. [Google Scholar] [CrossRef]

- Rahdari, A.H.; Anvary Rostamy, A.A. Designing a general set of sustainability indicators at the corporate level. J. Clean. Prod. 2015, 108, 757–771. [Google Scholar] [CrossRef]

- Sroufe, R. Effects of environmental management systems on environmental management practices and operations. Prod. Oper. Manag. 2003, 12, 416–431. [Google Scholar] [CrossRef]

- Darnall, N.; Jolley, G.; Handfield, R. Environmental management systems and green supply chain management: Complements for sustainability? Bus. Strateg. Environ. 2008, 17, 30–45. [Google Scholar] [CrossRef]

- Feng, T.; Cai, D.; Wang, D.; Zhang, X. Environmental management systems and financial performance; The joint effect of switching cost and competitive intensity. J. Clean. Prod. 2016, 113, 781–791. [Google Scholar] [CrossRef]

- Hämäläinen, E. Estimated impacts of the sulphur directive on the Nordic industry. Eur. Transp. Res. Rev. 2015, 7, 13. [Google Scholar] [CrossRef]

- Hämäläinen, E. Can slow steaming lower cost impacts of sulphur directive—Shippers’ perspective. World Rev. Int. Transp. Res. 2014, 5, 59–79. [Google Scholar] [CrossRef]

- Hatch, M.J.; Cunliffe, A.L. Organisation Theory: Modern, Symbolic and Postmodern Perspectives; Oxford University Press: Oxford, UK, 2006. [Google Scholar]

- Henri, J.-F.; Boiral, O.; Roy, M.-J. Strategic costs management and performance. The case of environmental costs. Br. Account. Rev. 2016, 48, 269–282. [Google Scholar] [CrossRef]

- Allenby, B.R. Industrial Ecology: Policy Framework and Implementation; Prentice-Hall: Upper Saddle River, NJ, USA, 1999. [Google Scholar]

- Graedel, T.; Allenby, B.R. Industrial Ecology; Prentice-Hall: Enlewood Cliffs, CA, USA, 1995. [Google Scholar]

- Parker, L.D. Environmental Costing: An Exploratory Examination Melbourne; VIC A.S. O C.P. Accountants: Melbourne, Australia, 1999. [Google Scholar]

- Pizzini, M.J. The relation between costs system design, manager’s evaluation, of the relevance and usefulness of cost data, and financial performance: an empirical study of US hospitals. Account. Organ. Soc. 2006, 31, 179–210. [Google Scholar] [CrossRef]

- Scariatelli, A. How to Breathe Easier in China’s Most Polluted Cities. 2014. Available online: http://www.echinacities.com/expat-corner/How-to-Breathe-Easier-in-Chinas-Most-Polluted-Cities/ (accessed on 15 January 2017).

- De Villiers, C.; Rouse, P.; Kerr, J. A new conceptual model of influences driving sustainability based on case evidence of the integration of corporate sustainability management control and reporting. J. Clean. Prod. 2016, 136 Pt A, 78–85. [Google Scholar] [CrossRef]

- Stacchezzini, R.; Melloni, G.; Lai, A. Sustainability management and reporting: The role of integrated reporting for communicating corporate sustainability management. J. Clean. Prod. 2016, 136 Pt A, 102–110. [Google Scholar] [CrossRef]

- Talvivaara. Talvivaara Gypsum Pond Leakage Has Been Stemmed. 2013. Available online: http://www.talvivaara.com/media-en/Talvivaara_announcements/stock_exchange_releases/stock_exchange_release/t=talvivaara-gypsum-pond-leakage/id=32889934/ (accessed on 15 January 2017).

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hämäläinen, E.; Inkinen, T. How to Generate Economic and Sustainability Reports from Big Data? Qualifications of Process Industry. Processes 2017, 5, 64. https://doi.org/10.3390/pr5040064

Hämäläinen E, Inkinen T. How to Generate Economic and Sustainability Reports from Big Data? Qualifications of Process Industry. Processes. 2017; 5(4):64. https://doi.org/10.3390/pr5040064

Chicago/Turabian StyleHämäläinen, Esa, and Tommi Inkinen. 2017. "How to Generate Economic and Sustainability Reports from Big Data? Qualifications of Process Industry" Processes 5, no. 4: 64. https://doi.org/10.3390/pr5040064

APA StyleHämäläinen, E., & Inkinen, T. (2017). How to Generate Economic and Sustainability Reports from Big Data? Qualifications of Process Industry. Processes, 5(4), 64. https://doi.org/10.3390/pr5040064