Abstract

This paper contributes to the literature concerning the natural resource curse by exploring the role of banking development in reducing the resource curse in a natural resource-based country, Yemen. Using time series data over the period 1980–2012, we find that natural resource dependence is negatively related to productivity, and this relationship depends on the level of banking development. Increasing this level reduces the negative consequences of the natural resource curse. Therefore, policymakers should proactively encourage credit to enable the banking sector to play a more efficient intermediary role in mobilizing domestic savings and channeling them to productive investments. This will help to accumulate permanent productive wealth to enhance any diversification effort and compensate for the decline in natural resource production.

JEL Classification:

O13; O16; C22

1. Introduction

For some decades, it has been observed that the possession of natural resources does not necessarily confer economic success. Many countries in Africa and the Middle East are rich in oil and other natural resources, and yet their people continue to experience low per capita income and low quality of life. This puzzling phenomenon is called the “natural resource curse” (). The term refers to the paradox that countries that heavily depend on natural resources, such as oil, natural gas, and minerals, tend to have less economic growth and worse development outcomes compared to countries with fewer natural resources. Angola, Congo, Nigeria, Venezuela and some Middle Eastern countries are good instances of natural resource-based economies that also suffer low or negative GDP growth and widespread poverty. In contrast, East Asian economies, such as Japan, Korea, Taiwan, Singapore and Hong Kong, have achieved a high-level standard of living despite having no exportable natural resources. Several economic and political explanations have been introduced for this phenomenon; see for a comprehensive survey.

While most of the research on the resource curse has focused on economic growth, an increasing number of papers have studied the effect of resource dependence on productivity (; ; ). Since productivity is a major determinant of economic growth, lower productivity would also mean lower economic growth.1 Indeed, a careful look at productivity growth is important. As pointed out by , most of the differences in cross-country GDP growth rates are not the result of factor accumulation, but of differences in total factor productivity (TFP) growth (). , and found that in the natural resource-based countries, there is a productivity difference between the resource sector and the non-resource sector due to the Dutch disease mechanism. The Dutch disease channel works as follows: A discovery of natural resources in a country causes overinvestment in the natural resource sector and ignores the sectors that are conducive to long-run growth. This leads to a decrease in TFP, an important factor of the Solow growth model that is vital for continuous growth. The decrease in productivity is reflected in the diminishing growth rate of GDP.

This paper builds its theoretical argument on the strand of literature that studies the likelihood of the resource curse on different macroeconomic factors by focusing on productivity factors. Our work contributes to the literature concerning the natural resource curse in two ways. First, we explore the role of banking development in reducing the resource curse.2 We argue that a well-structured and effective banking sector can weaken the negative link between natural resource dependence and productivity. A key merit of a strong banking sector is its capacity to provide low-cost information about investment opportunities (). This information improves the efficient allocation of resources and allows investors to monitor their investments better.

Second, this study is the first attempt to identify the relationship between natural resource dependence and productivity under a time series framework. The available studies in this field have only been undertaken in a panel of countries (). The results of panel data studies encouraged us to investigate this relationship on a country-specific basis using a time series approach, which is more useful for estimating the relationship ().

Our analysis focuses on a resource-based economy, Yemen. This country is among those that are blessed with natural resources; namely, crude oil and natural gas. It is among the 11 oil producing and exporting countries in the Arab region, and is the 32nd biggest oil exporter and 16th biggest seller of liquefied natural gas (). It also falls into the group of Arab oil economies that are endowed with limited amounts of oil reserves. The economy of Yemen is highly dependent on this declining resource, which generates more than 70% of government revenue, 80–90% of its exports and accounts for roughly 25% of its GDP. As a result, the Yemeni fiscal position and economic output are highly vulnerable to a shift in international commodity prices and domestic oil outputs.

Economic growth in Yemen was driven by capital accumulation and an expanded labor force (to a lesser extent) but without productivity gain (). During 1990–2010, the average annual growth was five percent, but growth per capita was only 1.7 percent due to high rate of population growth. The contribution of capital to GDP per capita was 2.6 percentage points on average, while labor and other human capital contributed an average of only 0.3 percentage points. On average, the contribution of TFP to economic growth per capita was negative, at −1.2 percentage points. This fact suggests that the absence of sustained high growth in Yemen can be attributed to the weak contribution of productivity in economic growth.

The remaining parts of the paper are organized as follows: Stylized facts about the Yemeni economy are presented in Section 2. The literature review is in Section 3. In Section 4, we focus on data and methodology. The empirical results and discussion are presented in Section 5. Finally, Section 6 provides the conclusion, with implications.

2. Yemeni Economy: Stylized Facts

Yemen is an Arab country in Western Asia occupying the South Western to Southern end of the Arabian Peninsula. The Republic of Yemen was established in May 1990, after the unification of the Yemen Arab Republic (YAR) and the Marxist People’s Democratic Republic of Yemen (PDRY). For the last two decades, the country’s economic performance has been good but unimpressive. On average, the economy grew at five percent annually between 1990 and 2010 (). However, due to rapid population growth, GDP per capita rose only 1.3 percent a year, which is not sufficient to reduce poverty. As mentioned earlier, the country’s growth was mainly driven by capital accumulation with very little improvement in productivity.

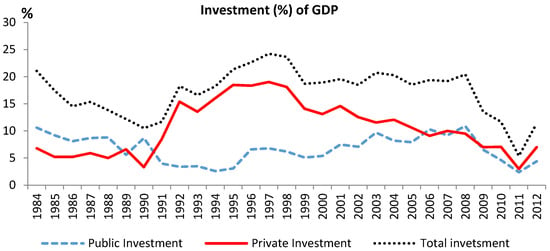

Investment, which is a main source of productivity, was relatively low, averaging around 18% to GDP over the period 1990–2000. Investment has been mainly concentrated in the private oil related rent-seeking activities. According to the , private investment is still ambiguous in spite of many structural reform efforts. Moreover, during 2001–2010, private investment declined to around 10.6% of GDP (see Figure 1). According to the , the small contribution of private investment in the economy can be attributed to the dominance of the oil sector (which is dominated by public investment) in the economy. Hence, there will be relatively little room for the development of private investment (). As a result of the low private investment rate, the gross investment remains relatively low. In addition, the low contribution of public investment is another reason for the low investment rate in Yemen.

Figure 1.

Investment in Yemen. Source: WDI and IMF reports.

Clearly, the deep-rooted obstacles to investment and high real interest rates stifle private investment projects. Nevertheless, this can also be attributed to the ineffective financial sector that lacks the ability to mobilize domestic savings and channel them into productive investments. The argued that the weak performance of the financial sector in Yemen is attributed to the weak legal and judicial environment where the creditors’ rights are not enforced. Intermediation between depositors and private sector credits is less than 10% of GDP. The vast majority of Yemen’s population does not use formal financial services. With reference to bank deposits, only 800,000 people have an account with a formal financial institution. The number of deposits accounts per 1000 people is only about 35 in Yemen, the lowest country globally.

In this paper, we argue that building a sound financial sector in Yemen that channels capital to its most productive uses is beneficial to avoid the potentially negative effect of natural resource dependence on the economy. A sound and efficient financial sector is especially important for sustaining growth in the country because the efficiency of investment (productivity) will overshadow the quantity of investment (capital accumulation) as the driver of growth in the country.

3. Literature Review

Since the late 1980s, a considerable amount of literature that challenges the view of natural resources as a blessing for developing countries has emerged. The literature on this phenomenon has increased significantly (; ; ; ; ; ; ; ). What is more, both economic and social scientists have contributed to showing new aspects of the resource curse. Recently, new reasons and new approaches to this hypothesis have been added. While it is important to study the relationship between resources and overall growth, we still need to identify the channels through which the resource curse works. That is, natural resource dependence can affect growth through its impact on the growth determinants, i.e., physical capital, human capital, social capital and productivity. In this paper, we focus on productivity.3

argued that during a natural resource boom, increased rents in the primary sector cause a reallocation of factors of production from manufacturing towards the booming primary sector. Since the manufacturing sector is often characterized by increasing returns to scale and positive externalities, a decrease in the scale of manufacturing decreases the productivity and profitability of investment. The issue of externalities can find its roots in the work of (, p. 476), who stated that manufactures “provide the growing points for increased technical knowledge, urban education, the dynamism, and resilience that goes with urban civilization.” Therefore, trade specialized in natural resources would provide low spillovers compared to the trade specialized in manufacturing. Later, externalities (increasing returns) and natural resources were dealt with by Dutch disease theorists. They built models that considered learning to be a transmission mechanism that was mostly associated with the tradable sector. built a two-period model with a tradable and a non-tradable sector. The tradable sector is subject to learning by doing from production. Therefore, the level of production in the first period may affect the outcome of the second period. He showed that with a foreign currency premium that implies a real valuation of the country’s currency, the production of the tradable sector in the first period will be smaller, generating a negative effect in the second period, which damages the welfare of people.

In the same context, , through the endogenous growth model, proved that heavy natural resource dependence leads to distortions in the allocation of installed capital. This is due to a poorly developed financial system and trade restrictions or government subsidies that attract capital to unproductive uses in protected industries or in state-owned enterprises where capital may be less productive than in the private sector.

Recently, found that natural resource rents have a negative and significant effect on productivity. However, the authors argued that the more market-oriented resource-rich economies may experience significantly higher productivity growth than less market-oriented ones. Additionally, they found that the relationship between natural resource dependence and productivity improves as economic freedom increases.

However, one important question arises here: How could financial (banking) development enhance productivity and thereby mitigate the natural resource effects on productivity? An efficient banking sector contributes to the increase in capital productivity through the two mechanisms of risk reduction and monitoring services. There are several types of risk associated with financial intermediation, such as liquidity risk, default risk, investment risk, and payment risk.

Uncertainty is a problem for economic agents in their daily economic life. It usually arises from the irregularity in business cycles and the possibility of economic shocks and sudden changes in circumstances and conditions. Therefore, the main concern of savers is the speed with which they can liquidate their assets to face the unexpected shocks (the liquidity risk). A well-structured financial sector can reduce the liquidity risk by having good liability and asset management on the one hand, and by diversifying its investments, on the other. Asset management means holding cash and liquidity assets at a level above that required to meet the expected volatility of cash flows. Liability management occurs by determining the desired quantities of assets and then adjusting interest rates to attract the desired levels of deposits to fund the transactions (). The more financial intermediaries facilitate and ensure the liquidity of savings at any time in the face of uncertain income shocks, the greater the individual’s willingness to save (). According to , well-structured banks enable individuals to face the liquidity risk and invest most of their funds in more productive and illiquid projects, which would result in higher productivity of investments and higher growth rates. By eliminating self-financed capital investment, banks enable entrepreneurs to face the liquidity shocks without liquidizing their productive assets to compensate ().

4. Data, Model and Methodology

4.1. Data and Variables

The study employs data for Yemen over the period 1980–2012. Following for the German case, we use Northern Yemen data for the period prior to 1990 and the united Yemen data after 1990, combined with a dummy variable to account for the unification.4,5

4.1.1. Productivity

Productivity is usually measured by total factor productivity (TFP). TFP is the portion of output that is not explained by the inputs used in a firm’s production, and, therefore, measures how efficiently and intensely the inputs are utilized in a production process (). An increase in TFP implies that a firm contributes a higher amount of value-added to the economy holding factor inputs constant ().

TFP is derived from a standard neoclassical Cobb-Douglas production function (; ):

where Y is the real GDP, K is the real physical capital stock, and L is the total labor force. Therefore, TFP is measured as A = TFP = y/kα, where y is the output-worker ratio (Y/L) and k is the capital-worker ratio (K/L). The set the capital’s income share (α) for Yemen at 0.3. K is constructed using the perpetual inventory method, Kt = It + (1 − ϑ)Kt-1, where, I is the real investment, ϑ is the depreciation rate, which is assumed to be 5% following the . The initial capital stock is estimated using the Solow model steady-state value of I0/(ϑ + g), where I0 is the initial real investment, and g is the growth rate in real investment over the period 1980–2012.

4.1.2. Natural Resource Dependence

To gauge the reliance of the economy on natural resources, the ratio of oil resource export to GDP has been widely used in the relevant literature since . However, in Yemen, in addition to the export of the government’s share of natural resources, natural resource revenue includes other grants and taxes.6 Therefore, we use oil revenue (which includes the components mentioned above) relative to GDP as a proxy for oil dependence.

4.1.3. Banking Development

It is observed that certain studies used a single indicator for financial/banking development, whereas others have used two or more indicators to reflect the entire dimension of financial development. In this paper, due to limited development in the capital markets and the dominant role of the banking system in Yemen, we use two proxies to measure the level of financial intermediation.

The first proxy is M2 as a share of GDP, which was put forward by and , and used by , and many other studies. This measure equals cash outside banks plus the demand and interest-bearing liabilities of banks and non-financial intermediaries divided by GDP.

The second proxy is domestic credit to private sector as a share of GDP (PRV). Domestic credit to private sector refers to financial resources provided to the private sector, such as through loans, purchases of non-equity securities, and trade credits and other accounts receivable, that establish a claim for repayment. This proxy is considered to be one of the best indicators to measure financial development, and has been widely used in the literature (; ; ). This proxy provides information regarding the credit allocated to the private sector by commercial banks, compared to the size of the economy as a whole. Therefore, this indicator accurately measures the role of financial intermediation in channeling funds to the private sector. The higher ratio implies more financial services and therefore greater financial development.

As one of the main determinants of TFP, public expenditure on education (EDU) is added as a proxy for human capital (; ). A dummy variable to capture the unification period (1990–2012) is also added to our models. It will take 1 if the observation is in the period of 1990–2012 and 0 if the observation is in the period of 1980–1989.7

4.2. Model

We construct two models to capture the relationship between natural resource dependence and productivity (TFP), and also the role of banking development in respect of this relationship by using an interaction term between banking development indicators and natural resource dependence. We regress TFP on natural resource dependence, banking development and an interaction term between banking development and natural resource dependence.

The following two models have been inspired by :

Model 1

Model 2

where TFP is the total factor productivity, NR is natural resource dependence, M2 and PRV are banking development indicators. All variables are transformed into natural logarithms. The interaction term between natural resource dependence and banking development captures the role of banking development on the relationship between natural resource dependence and total factor productivity, which can be derived from Equations (1) and (2).

The coefficients σ3 and ω3 represent the role of banking development in the relationship between natural resource dependence and productivity. If σ3, ω3 > 0 and σ1, ω1 < 0, a small increase in banking development would result in a weaker relationship between natural resources and TFP. However, if σ3, ω3 < 0 and σ1, ω1 < 0, a small increase in banking development would result in a greater relationship between natural resources and TFP.

4.3. Methodology

The Augmented Dicky Fuller (ADF) stationary test and Phillip-Perron (PP) test are employed to examine the time-series properties of each variable. This paper uses the auto-regressive distributed lag (ARDL) bound testing approach of cointegration by to find the long-run equilibrium among the variables. The ARDL model is preferable because it is reliable and applicable irrespective of whether the underlying regressors are I (0) or I (1).

In addition, this approach performs well for a small sample size. The short-run and long-run effects of the independent variables on the dependent variable can be assessed at the same time. Finally, all variables are assumed to be endogenous and thus the endogeneity problems associated with the Engle-Granger method can be avoided.

The ARDL models in the unrestricted error correction form are written as Equations (5) and (6), respectively:

The coefficients of the first portion of the model measure the long-term relation, whereas the coefficients of the second portion that attach with Σ represent the short-term dynamics. The F-statistic is used to test the existence of a long-run relationship among the variables. We test the null hypothesis, H0: β1= β2 = β3 = β4 = β5 = 0 in (5),8 that there is no cointegration among the variables. The F-statistic is then compared with the critical value given in , which is more suitable for small samples. If the computed F-statistic is greater than the upper-bound critical value, then we reject the null hypothesis of no cointegration and conclude that a steady state equilibrium exists among the variables. If the computed F-statistic is less than the lower-bound critical value, then the null hypothesis of no cointegration cannot be rejected. However, if the computed F-statistic lies between the lower- and upper-bound critical values, then the result is inconclusive.

5. Empirical Findings and Discussion

As the ARDL approach is applicable to variables with I (0), I (1) or mutually integrated, we check the order of integration of each variable to ensure that no variables are I (2) or beyond. Table 1 summarizes the outcomes of ADF and PP unit root tests on the level and first differences of the variables. The result suggests that all variables are I (1), which supports the use of the ARDL approach to cointegration.

Table 1.

Unit root test results.

After investigating the time series properties of all the variables, the ARDL approach is used to examine the potential long-term equilibrium. This test is sensitive to the number of lags used. Given the limited number of observations in this study, lags with a maximum of two years have been imposed on the first difference of each variable, and the Schwarz-Bayesian Criterion (SBC) is used to select the optimal lag length for each variable. SBC suggests ARDL (1,1,1,0,0) and (1,1,0,2,0) for our two models, respectively. The result of the ARDL bound test of cointegration is tabulated in Table 2.

Table 2.

Result from auto-regressive distributed lag (ARDL) Cointegration Test.

Table 2 shows that the F-statistic is greater than its upper bound critical values at the five-percent level for the case of the M2 model, thereby indicating the existence of cointegration in this model. Moreover, the coefficient of lagged error correction term (ECTt-1) is significant and negative, which confirms the existence of cointegration. On the other hand, the F-statistic for the case of the credit to private sector model lies between the upper and lower bound critical values. Hence, it is inconclusive. Therefore, we seek an alternative way by testing the coefficient of lagged error correction term (ECTt-1), which is considered by as a more efficient way of establishing cointegration. argued that a significant and negative coefficient for ECTt-1 indicates the adjustment of the variables towards equilibrium, and, hence, cointegration. Accordingly, the cointegration is supported by the significant and negative coefficient obtained for ECTt-1.

With cointegration among the variables, we can derive the long-run coefficient as the estimated coefficient of the one lagged level independent variable divided by the estimated coefficient of the one lagged level dependent variable and multiply it with a negative sign. Conversely, the short-term coefficient is calculated as the sum of the lagged coefficient of the first differenced variable.

Table 3 Panel A reports a negative relationship between natural resource dependence and productivity growth in Yemen for both models. This result supports the idea of . Resource dependence reduces the productivity of capital and raises the ensuing rate of depreciation. Hence, a given investment rate is likely to generate a lower rate of growth of output. According to , in resource-dependent economies, during a natural resource boom, increased revenue in the primary sector causes a reallocation of factors of production from manufacturing towards the booming primary sector. As the manufacturing sector is often characterized by increasing returns to scale and positive externalities, a decrease in the scale of manufacturing decreases the productivity and profitability of investment (; ). In fact, the weak performance of the manufacturing sector during the oil era in Yemen has been empirically proven by , and can be considered as an important sign of the negative consequences of natural resource dependence on productivity.9

Table 3.

Long-run estimates based on selected ARDL model.

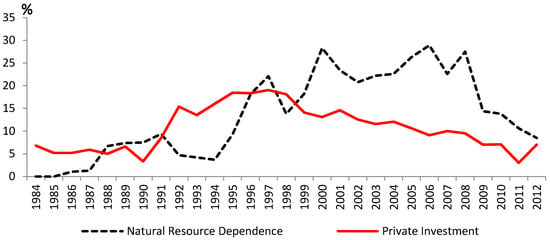

In order to further illustrate the dominant role of the oil sector on the productivity of the Yemeni economy, one can investigate the ratio of private investment to GDP over the study period, and analyze the situation of private investment and public investment. This investigation can provide another explanation of the negative relationship between natural resource dependence and productivity in Yemen. Figure 2 shows that the ratio of private investment to GDP was decreasing since the level of natural resource dependence reached its peak in 1996, whilst Figure 1 shows the increasing trend of public investment during the same period. This indicates that the greater the level of natural resource dependence, the lower the contribution of private investment to total investment and the higher public investment share. As private investment is more efficient than public investment, high dependence on natural resources replaces a more efficient investment by less efficient investments. Hence, productivity suffers and thereby the economic growth (; ).10

Figure 2.

Natural resource dependence and private investment. Source: WDI, IMF Reports.

We could not find a significant long-run relationship between banking development and productivity, which confirms argument. argued that finance does not have an impact on productivity growth in the less developed economies. The impact does not occur until a country has reached a certain income level. Productivity is a long-term investment. Uncertainty and macroeconomic instability prevent the financial sector becoming involved in long-term high-efficiency investments.

The positive sign of the interaction term between banking development and natural resource dependence sheds new light on the role that can be played by banking development in mitigating the resource curse. This result is in line with the emerging consensus in the resource curse literature: the development of financial/banking sector ultimately determines whether the natural resource curse is more or less pronounced (; ). The financial sector can reduce the risk associated with a natural resource dependent environment by having good liability and asset management and diversifying the investments. Furthermore, well-structured banks will enable individuals to invest most of their funds in more productive and illiquid projects, which would result in higher productivity.

In sum, our results reveal that the negative relationship between natural resource dependence and TFP growth is consistent with the resource curse hypothesis, implying that the curse exists. However, the finding suggests that if the level of banking development (represented by credit to the private sector) improves over time, it would slightly mitigate the curse.

The short-run estimation results in error-correction representation are provided in Table 3 Panel B. The coefficient of the estimated error correction model is negative and significant, which confirms the existence of long-run equilibrium among our variables in the two models. In addition, the coefficient suggests that a deviation from the long-run equilibrium following a short-run shock is corrected by about 63% and 43% per year in both models, respectively. Similar to the long-run analysis for the private credit model, a positive relationship exists between the interaction term and TFP. This finding implies the important role of banking development in Yemen in the short run.

On the other hand, we note that the results of the M2 model are not significant. This could be due to a large portion of M2 consisting of currency that is held outside the banks in Yemen. Therefore, an increase in the M2 to GDP ratio may reflect the extensive use of currency rather than an increase in the bank deposits (). Hence, its role in mitigating the resource curse is not significant11.

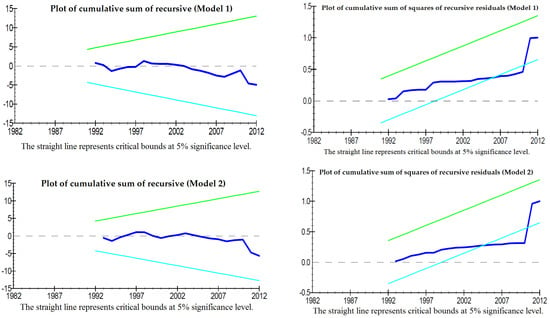

Panel C in the same table notes that all models pass all diagnostic tests for serial correlation, autoregressive conditional heteroskedasticity and model specification. The CUSUM and CUSUMSQ in Figure 3 remain within the critical boundaries for the five-percent significance level. These statistics confirm that the long-term coefficients and all short-term coefficients in the error correction model are stable.

Figure 3.

Plots of cumulative sum of recursive and cumulative sum of squares of recursive.

6. Conclusions

The vast empirical literature following highlighted the negative relationship between natural resource dependence and economic growth and numerous plausible growth determinants, i.e., capital accumulation and productivity. This paper empirically examines whether the well-developed banking sector can mitigate the negative influences of natural resource dependence on productivity in Yemen. Our empirical findings suggest that natural resource dependence is negatively and significantly related to productivity. The interaction term between natural resource dependence and banking development is positive, which implies that more banking development may reduce the negative consequences of natural resource dependence on productivity. This can occur through two important mechanisms: risk reduction and monitoring services. The results show that the negative relationship between natural resources and productivity improves as banking development increases. However, given the small sample size and the differences in resource-based countries, these results must be viewed with caution, and further analyses over a longer sample period or among different countries would allow a more accurate conclusion.

Therefore, strengthening the role of the banking sector in financial intermediaries in Yemen through boosting the confidence in the banking system and reforms is key to higher productivity in a resource-based country like Yemen. The government should play a more proactive role in encouraging credit to enable the financial sector to play a more efficient intermediary role in mobilizing domestic savings and channeling them to private productive investment across economic sectors. To do so, the government will have to provide various incentives to the financial sector to provide long-term loans for greater involvement in efficient investment activities. The efficiency of these investments is expected to support the economic diversification efforts to reduce the level of natural resource dependence.

Author Contributions

The paper is a joint contribution of two authors.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix

and (TYDL), based on an augmented VAR modeling, introduced a modified Wald test statistic (MWALD). This procedure has been found to be superior to ordinary Granger-causality test since it does not require pre-testing for the cointegrating properties of the system and thus avoids the potential bias associated with unit roots and cointegration tests as it can be applied regardless of whether a series is I (0), I (1) or I (2), non-cointegrated or cointegrated of an arbitrary order.

TYDL test suggests the following augmented VAR framework with p = (k + dmax) lag length. Here dmax is the maximal order of integration for the series in the system. Following , dmax = 1 is used as it performs better than other orders of dmax. The optimal lag length k is selected on the basis of the Schwarz Bayesian Criterion (SBC). Then the standard Wald tests are applied to the first k VAR coefficient matrix (but not all lagged coefficients) in order to draw the inference about the direction of Granger causality.

Table A1 reports the result of causation. There is only one unidirectional causality that runs from natural resource dependence to TFP in Model 2. In fact, the result of causality is not conclusive evidence because it is significant at 10% level, but it gives a general hint about the direction of the causality and the potential effect of natural resource on productivity. Therefore, this result must be taken with caution.

Table A1.

Results of TYDL causality test (χ2).

Table A1.

Results of TYDL causality test (χ2).

| Model 1 | Model 2 | |

|---|---|---|

| BD → TFP | 3.5807 | 3.5648 |

| TFP → BD | 3.8897 | 3.1852 |

| NR → TFP | 1.4501 | 4.6169 * |

| TFP → NR | 2.6663 | 2.3135 |

Note: BD is banking development, * denotes the significance at 10% level.

References

- Abu-Bader, Suleiman, and Aamer S. Abu-Qarn. 2008. Financial Development and Economic Growth: The Egyptian Experience. Journal of Policy Modelling 30: 887–98. [Google Scholar] [CrossRef]

- Angelini, E., and M. Marcellino. 2011. Econometric Analysis with Backdated Data Unified Germany and the Euro Area. Economic Modelling 28: 1405–414. [Google Scholar] [CrossRef]

- Anwar, Sajid, and Sizhong Sun. 2011. Financial Development, Foreign Investment and Economic Growth in Malaysia. Journal of Asian Economics 22: 335–42. [Google Scholar] [CrossRef]

- Arezki, Rabah, and Frederick Van der Ploeg. 2011. Do Natural Resources Depress Income Per Capita? Review of Development Economics 15: 504–21. [Google Scholar] [CrossRef]

- Auty, Richard. 1993. Sustaining Development in Mineral Economies: The Resource Curse Thesis. London: Routledge. [Google Scholar]

- Badeeb, Ramez Abubakr, and Hooi Hooi Lean. 2017. Natural Resources, Financial Development and Sectoral Value Added in a Resource Based Economy. In Robustness in Econometrics. Edited by Vladik Kreinovich, Songsak Sriboonchitta and Van-Nam Huynh. Berlin: Springer, pp. 401–17. [Google Scholar]

- Badeeb, Ramez Abubakr, Hooi Hooi Lean, and Russell Smyth. 2016. Oil Curse and Finance–Growth Nexus in Malaysia: The Role of Investment. Energy Economics 57: 154–65. [Google Scholar] [CrossRef]

- Badeeb, Ramez Abubakr, Hooi Hooi Lean, and Jeremy Clark. 2017. The Evolution of the Natural Resource Curse Thesis: A Critical Literature Survey. Resources Policy 51: 123–34. [Google Scholar] [CrossRef]

- Banerjee, Pradeep. 2011. Microeconomic Policy Environment–An Analytical Guide for Managers. New York: Tata McGraw-Hill. [Google Scholar]

- Bencivenga, Valerie R., and Bruce D. Smith. 1991. Financial Intermediation and Endogenous Growth. The Review of Economic Studies 58: 195–209. [Google Scholar] [CrossRef]

- Benhabib, Jess, and Mark M. Spiegel. 1994. The Role of Human Capital in Economic Development Evidence from Aggregate Cross-Country Data. Journal of Monetary Economics 34: 143–73. [Google Scholar] [CrossRef]

- Buckle, Mike, and John L. Thompson. 1998. The UK Financial System: Theory and Practice. Manchester: Manchester University Press. [Google Scholar]

- Caprio, Gerard, and Stijn Claessens. 1997. The Importance of the Financial System for Development: Implications for Egypt. Distinguished Lecture Series 6: 1–49. [Google Scholar]

- Corden, Warner Max. 1984. Booming Sector and Dutch Disease Economics: Survey and Consolidation. Oxford Economic Papers 36: 359–80. [Google Scholar] [CrossRef]

- Corden, Warner Max, and J. Peter Neary. 1982. Booming Sector and De-Industrialisation in a Small Open Economy. The Economic Journal 92: 825–48. [Google Scholar] [CrossRef]

- Dasgupta, Dipak, Jennifer Keller, and T. G. Srinivasan. 2005. Reform and Elusive Growth in the Middle East-What Happened in the 1990s? Trade Policy and Economic Integration in the Middle East and North Africa: Economic Boundaries in Flux 1: 13. [Google Scholar]

- Dolado, J.J., and H. Lütkepohl. 1996. Making Wald Tests Work for Cointegrated VAR. Econometric Reviews 15: 369–86. [Google Scholar] [CrossRef]

- Easterly, William, and Ross Levine. 2000. It’s Not Factor Accumulation: Stylized Facts and Growth Models. World Bank Economic Review 15: 177–219. [Google Scholar] [CrossRef]

- Farhadi, Minoo, Md Rabiul Islam, and Solmaz Moslehi. 2015. Economic Freedom and Productivity Growth in Resource-rich Economies. World Development 72: 109–26. [Google Scholar] [CrossRef]

- Gylfason, Thorvaldur. 2001. Natural resources, education, and economic development. European Economic Review 45: 847–59. [Google Scholar] [CrossRef]

- Gylfason, Thorvaldur, and Gylfi Zoega. 2006. Natural Resources and Economic Growth: The Role of Investment. World Economy 29: 1091–115. [Google Scholar] [CrossRef]

- International Monetary Fund. 2001. Republic of Yemen: Selected Issues. IMF Country Report No. 0161. Washington: International Monetary Fund. [Google Scholar]

- Karl, T. L. 2005. Understanding the Resource Curse in S. Tsalik and A. Schiffrin (eds) Covering Oil: A Reporter’s Guide to Energy and Development. New York: Open Society Institute, pp. 21–30. [Google Scholar]

- Khan, Mohsin S., and Manmohan Kumar. 1993. Public and Private Investment and the Convergence of Per Capita Incomes in Developing Countries. IMF Working Paper 93/51. Washington: International Monetary Fund. [Google Scholar]

- Khan, Mohsin S., and Carmen M. Reinhart. 1990. Private Investment and Economic Growth in Developing Countries. World development 18: 19–27. [Google Scholar] [CrossRef]

- King, Robert G., and Ross Levine. 1993. Finance and Growth: Schumpeter Might be Right. Quarterly Journal of Economics 108: 717–38. [Google Scholar] [CrossRef]

- Kremers, Jeroen J. M., Neil R. Ericsson, and Juan J. Dolado. 1992. The Power of Cointegration Tests. Oxford Bulletin of Economics and Statistics 54: 325–48. [Google Scholar] [CrossRef]

- Levine, Oliver, and Missaka Warusawitharana. 2014. Finance and Productivity Growth: Firm-Level Evidence. Finance and Economics Discussion Series; Washington: Divisions of Research & Statistics and Monetary Affairs, Federal Reserve Board. [Google Scholar]

- McKinnon, R. I. 1973. Money and Capital in Economic Development. Washington: Brookings Institution. [Google Scholar]

- Mehlum, Halvor, Karl Moene, and Ragnar Torvik. 2006. Institutions and the Resource Curse. The Economic Journal 116: 1–20. [Google Scholar] [CrossRef]

- Narayan, Paresh Kumar. 2005. The Saving and Investment Nexus for China: Evidence from Cointegration Tests. Applied Economics 17: 1979–990. [Google Scholar] [CrossRef]

- Neumayer, Eric. 2004. Does the “Resource Curse” Hold for Growth in Genuine Income as Well? World Development 32: 1627–640. [Google Scholar] [CrossRef]

- Nili, Masoud, and Mahdi Rastad. 2007. Addressing the Growth Failure of the Oil Economies: The Role of Financial Development. The Quarterly Review of Economics and Finance 46: 726–40. [Google Scholar] [CrossRef]

- Pagano, Marco. 1993. Financial Markets and Growth: An Overview. European Economic Review 37: 613–22. [Google Scholar] [CrossRef]

- Papyrakis, Elissaios, and Reyer Gerlagh. 2004. The Resource Curse Hypothesis and Its Transmission Channels. Journal of Comparative Economics 32: 181–93. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds Testing Approaches to the Analysis of Level Relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Rioja, Felix, and Neven Valev. 2004. Finance and the Sources of Growth at Various Stages of Economic Development. Economic Inquiry 42: 127–40. [Google Scholar] [CrossRef]

- Saborowski, Christian. 2009. Capital Inflows and the Real Exchange Rate: Can Financial Development Cure the Dutch Disease? IMF Working Papers 09/20. Washington: International Monetary Fund. [Google Scholar]

- Sachs, Jeffrey D., and Andrew M. Warner. 1995. Natural Resources Abundance and Economic Growth. NBER Working Paper No. 5398. Cambridge: National bureau for Economic Research. [Google Scholar]

- Sachs, Jeffrey D., and Andrew M. Warner. 2001. The Curse of Natural Resources. European Economic Review 45: 827–38. [Google Scholar] [CrossRef]

- Schoar, Antoinette. 2002. Effects of Corporate Diversification on Productivity. The Journal of Finance 57: 2379–403. [Google Scholar] [CrossRef]

- Serven, L., and A. Solimano. 1990. Private Investment and Macroeconomic Adjustment: Theory, Country Experience, and Policy Implication. In Macroeconomic Adjustment and Growth Division. Washington: World Bank. [Google Scholar]

- Shahbaz, Muhammad, and Hooi Hooi Lean. 2012. Does Financial Development Increase Energy Consumption? The Role of Industrialization and Urbanization in Tunisia. Energy Policy 40: 473–79. [Google Scholar] [CrossRef]

- Shaw, E. S. 1973. Financial Deepening and Economic Development. New York: Oxford University Press. [Google Scholar]

- Singer, H. W. 1950. The Distribution of Gains between Investing and Borrowing Countries. The American Economic Review 40: 473–85. [Google Scholar]

- Singh, Tarlok. 2008. Financial Development and Economic Growth nexus: A Time-Series Evidence from India. Applied Economics 40: 1615–627. [Google Scholar] [CrossRef]

- Stevens, Paul, and Evelyn Dietsche. 2008. Resource Curse: An Analysis of Causes, Experiences and Possible Ways Forward. Energy Policy 36: 56–65. [Google Scholar] [CrossRef]

- Toda, H. Y., and T. Yamamoto. 1995. Statistical Inference in Vector Autoregressions with Possibly Integrated Processes. Journal of Econometrics 66: 225–50. [Google Scholar] [CrossRef]

- Van der Ploeg, Frederick, and Steven Poelhekke. 2009. Volatility and the Natural Resource Curse. Oxford Economic Papers 61: 727–60. [Google Scholar] [CrossRef]

- Van Wijnbergen, Sweder. 1984. The Dutch Disease’: A Disease after all? The Economic Journal 94: 41–55. [Google Scholar] [CrossRef]

- Vetlov, I., and T. Warmedinger. 2006. The German Block of the ESCB Multi-Country Model. Working Paper Series No. 654; Frankfurt am Main: European Central Bank. [Google Scholar]

- World Bank. 2002. Economic Growth in the Republic of Yemen: Sources, Constraints, and Potentials. A World Bank Country Study, Report No: 24976. Washington: World Bank. [Google Scholar]

- World Bank. 2013. Project Appraisal Document on A Proposed Grant to the Republic of Yemen. Finance and Private Sector Development Department Middle East and North Africa Region. Report No: 78624-YE. Washington: World Bank. [Google Scholar]

- World Bank. 2015. Republic of Yemen: Unlocking the Potential for Economic Growth. Washington: World Bank. [Google Scholar]

| 1 | Although we lack a universally accepted theory of the natural resources curse, most explanations of the curse have a crowding-out logic. When natural resources crowd-out activity x, and activity x drives growth, natural resources harm growth (). |

| 2 | The reason for focusing on banking development rather than all financial development is that most natural resource-based economies have limited development on the stock market, and banks are the main source of finance. The financial sector in Yemen is also dominated by the banking sector, with no existence of a stock market. |

| 3 | See for a comprehensive literature survey on natural resource curse hypothesis. |

| 4 | argued that this simple treatment of the unification problem has been used widely in empirical macroeconomic analyses in Europe. It is based on the economic reasoning that East Germany’s economy represented a very small portion of the unified Germany economy in real GDP terms in 1991. |

| 5 | Evidence of the validity of this treatment comes from the fact that the economy of former Southern Yemen accounted for only 17.3 percent of real GDP of united Yemen. Additionally, the economy of united Yemen is largely based on the market system, which was followed by the Northern part before unification. |

| 6 | Natural resource revenues in Yemen include the concession commissions that the government receives from natural resource production companies, tax charges on foreign oil companies that operate in Yemen, and grants that the government receives from oil companies after signing contracts (Yemeni Ministry of Finance). |

| 7 | Yemeni unification took place in 1990, when the area of the People’s Democratic Republic of Yemen (also known as South Yemen) was united with the Yemen Arab Republic (also known as North Yemen), forming the Republic of Yemen (known simply as Yemen). |

| 8 | The same approach is applied to Equation (6). |

| 9 | During the oil decades, the contribution of the manufacturing sector to the GDP declined from 16.5% to 7%. |

| 10 | A number of studies have been conducted on developing countries and concluded that public investment has a smaller impact on growth than private investment (; ). Others maintain that this effect may even be negative (). |

| 11 | and causality test has been employed to verify the causal relationship among the variables that are studied in this paper (see Appendix). We thank an anonymous reviewer for this suggestion. |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).