Housing, Housing Finance and Credit Risk

1

Department of Economics and Statistics, University of Turin, Lungo Dora Siena 100 A, 10153 Turin, Italy

2

Department of Economics, University of Reading, Reading, Berkshire RG6 6AH, UK

*

Author to whom correspondence should be addressed.

Int. J. Financial Stud. 2018, 6(2), 50; https://doi.org/10.3390/ijfs6020050

Submission received: 20 December 2017

/

Revised: 16 April 2018

/

Accepted: 2 May 2018

/

Published: 9 May 2018

(This article belongs to the Special Issue Real Estate Finance)

Abstract

:This paper investigates the determinants of credit risk from a broad perspective. Particular attention is given to the role of housing affordability and household indebtedness. However, the impact of credit market developments and regulations is also closely examined. Using a large panel of countries it is found that housing affordability and household fragility significantly affect the risk of banks’ loan portfolios. In addition, an analysis of the conditional quantiles of non-performing loan ratios reveals that financial institutions in countries with greater levels of financial liberalization and less regulated markets also experience greater credit risk.

JEL Classification:

G21; G28; C231. Introduction

Financial markets are fundamental institutions in any developed economy. They play a crucial role in promoting economic growth by facilitating the channeling of saving decisions into productive investment (Gerlach and Peng 2005). A major concern for financial institutions is credit risk, because if not managed properly, it can lead to a banking collapse. In this respect, the sub-prime mortgage crisis that started in 2005 in the United States demonstrated the devastating effect that a housing market collapse can have on the real economy. Major financial innovation such as the securitization of subprime mortgages greatly increased the exposure to credit risk of financial institutions. From the late 1990s, there was a sharp increase in sub-prime mortgages fueled by low interest rates and lax lending standards. However, while the quality of banks’ loan portfolios was deteriorating due to the increase in lending to borrowers with little creditworthiness, the default rates remained artificially low due to rapid real estate appreciation. The collapse of the housing market caused a sharp increase in banks’ non-performing real estate loans, followed by a liquidity crisis in the banking system and a financial crisis that spread throughout the world bringing misery to millions of households.

If we are to learn enduring lessons from the sub-prime crisis, we need to understand the relationship between housing finance and credit risk. It is well known that in the decade prior to the recent financial crisis, there was an unprecedented expansion in the use of funded securitization and other methods of transferring credit risk, such as synthetic securitization and credit derivatives. In light of the 50% increase in delinquencies in the U.S. subprime housing market from 2005–2007 (Stiglitz 2007) and the global financial crisis that followed, it is of crucial importance to shed light on the factors that contribute to potential loan defaults in order to avoid future banking crises.

In the literature, there is a general consensus that factors such as household indebtedness and credit availability, in addition to macroeconomic factors, play an important role in determining credit risk (see for example (Pesola 2011), among others). However, most related literature focuses on one issue or the other, leaving little insight into how these risk factors interact. One lesson from the sub-prime crisis is that these factors do not act in isolation, but mutually reinforce each other (see Matheson 2013; Reinhart and Rogoff 2008; Minshkin 2011; among others).

Against this background, in this paper we take a broader view of the issue and consider the relationships between housing, housing finance and credit risk. Using panel data from a large number of countries for the period 2001 to 2010, we first consider risk factors related to the demand side of the credit market such as household indebtedness, house prices and housing affordability. We then analyze risk factors related to the credit supply side and investigate how the evolution of financial liberalization and credit market regulations affect credit risk. Particular attention is given to the degree of financial liberalization of a country and the exposure to credit risk in relation to the housing market. The period under consideration is of particular interest as it allows us to include the effects of the recent financial crisis.

With respect to credit market demand, we first examine how factors relating to borrowing, such as housing affordability, affect credit risk by considering the performance of banks’ non-performing loans (NPL). The questions we address in this article are: Is there a sizable effect of the cost of housing on credit risk? In other words, does a reduction of housing affordability lead to an increase in default rates? Also, the last few decades of economic growth have seen an enormous development in credit markets matched with a sharp increase in housing expenditure and household borrowing (see for example (Rinaldi and Sanchis-Arellano 2006)). Accordingly, in this paper we investigate whether the increase of household indebtedness in the recent years has affected the exposure to credit risk of financial institutions. Credit risk is a major concern for the stability of the financial system, therefore it is not surprising that many empirical studies have considered this issue. However, most related literature considers the relationship between real estate prices and financial distress by arguing that a decrease in lending standards by financial institutions in good times may be blamed for an increase in credit risk (see for example (Dell’Ariccia et al. 2012)). It seems to us that house prices are only one side of the coin, since owning or renting a property requires households to be able to afford it. According to Andrews (1998), an affordable house is one that costs no more than 30 per cent of the income of the household occupant, implying that buying or renting a house with acceptable standards at a cost should not overburden households’ incomes for each income class. This means that a deterioration of housing affordability due to house price increase may affect borrowers’ ability to pay their obligations, resulting in a higher probability of default. In light of this argument, housing affordability is a legitimate source of concern regarding a bank’s loan performance. Gaining a better understanding of this issue is crucial because in most cases, despite the existence of collateral and the lender’s legal protection, personal bankruptcy is costly for lenders. In this paper, we consider the issue of the relationship between the housing market and credit risk in a broader way using an indicator of housing affordability that includes the cost of renting as well as the cost of owning a property. In doing so, we are able to investigate the effect of housing affordability on credit risk from a larger perspective than most related empirical works.

Another fundamental player in credit risk is household indebtedness. The sharp increase in housing expenditure and household borrowing in many developed countries has raised concerns about a parallel rise in household financial fragility that in turn may affect credit risk. Assuming a high correlation among real estate markets, household vulnerability and credit risk is reasonable in light of the following two considerations. First, loans to real estate markets comprise somewhere between one third and more than half of bank loan portfolios in most developed countries. Second, the prevailing use of properties for collateral-based loans forms an important channel between the two markets. Indeed, the collapse of several banks, the primary activity of which was real estate financing, raises the question of whether the stability of banks is connected to changes in real estate market conditions and suggests the need for more efforts to quantify the actual impact of the real estate markets on the quality of banks’ loan portfolios. Changes in indicators such as “debt to income” ratio or “mortgage to income” ratio are clearly linked with financial problems; an increase in the level of household indebtedness is a sign of an increased proportion of financially constrained households. Therefore, household indebtedness may be used to investigate the relationship between real estate price fluctuations and credit risk.

Coming now to credit supply, there is a wide consensus in the literature that the origin of an increase in indebtedness is related to the deregulation of financial markets that occurred in many countries during the first part of the 1980s (see for example (Girouard and Blondal 2001)). On the one hand, the deregulation process boosted competition among financial institutions, prompting them to improve their efficiency. On the other hand, market imperfections may affect the risk-taking behavior of financial institutions. In an efficient world, bank lending rates should reflect the true default risk for the underlying assets and bank profitability; therefore a bank’s lending policy should be driven by its risk appetite. This, however, no longer holds when the attitude toward the risk of financial institutions changes over the cycle (see for example (Hott 2011)), or when a bank faces distorted incentives in taking lending decisions. For instance, disaster myopia, herding behavior, perverse incentives and principal-agent problems may lead to mistakes in the bank credit policy in an expansionary phase. This, combined with the loose regulatory framework under which banks operate, may excessively increase borrower’s debt levels and result in an increase in problematic loans. Thus, in this paper we aim to investigate the relationship between financial market developments, the housing market and credit risk. Accordingly, the questions we address in this work are: Is there evidence that financial liberalization has affected the performance of banks’ loan portfolios? To what extent has the increase of ratio of credit provided to private sector affected the evolution of NPL? Is it actually the case that the risk appetite of financial institutions changes over the real estate cycle? As a corollary to our investigation we consider the impact of the regulatory system on the risk of banks’ loan portfolios. Credit risk is, by definition, conditional on the regulatory framework under which banks operate. In this paper we distinguish between financial market regulations and the regulatory framework relating to the housing market. With respect to the former, a large body of literature asserts that financial institutes are more driven by risk-taking behavior in a less-regulated financial environment (see for example (Favara and Imbs 2015)). With respect to the latter, regulations on property markets may constitute a legal impediment to collateral enforcement, therefore affecting the risk of loan portfolios. Finally, since different countries have different patterns of financial developments over time as well as different regulatory frameworks, after having estimated a number of dynamic panel models, we turn our attention to country idiosyncratic effects. By conducting an analysis by quantile, we are able to discriminate the impact of the risk factors by groups of countries in relation to their risk profile.

The main findings of this paper can be summarized as follows. In general, the recent rise of debt ratios in relation to the housing market has put the banking sector in a riskier financial position. Our analysis reveals that a greater household debt burden translates into a higher probability of credit default. Similarly, the deterioration in housing affordability associated with increased deregulation poses a severe risk to the financial system. In particular, it is found that countries which score high in terms of financial liberalization and low on the level of regulations also experience greater credit risk.

The outline of the paper is as follows. Section 2 provides some theoretical background. Section 3 introduces the models under consideration and the estimation procedure used in the empirical analysis. Section 4 reports the estimation results of the main empirical analysis. Section 5 provides some further analysis on the effects of financial liberalization and regulation on credit risk, and finally, Section 6 concludes.

2. The Determinants of Credit Risk

2.1. House Prices and Credit Risk

Credit risk is closely related to the real estate market. This is due to the high dependence of real estate markets on banking products, in addition to using properties as collateral for loans. A growing number of empirical studies have found that depreciation in property prices can severely reduce the quality of banks’ assets and negatively impact on their profitability, therefore reducing their lending capacity.

In the literature, two competing hypotheses have been put forward about the effects of house prices on credit risk: the “collateral value hypothesis” (see for example (Daglish 2009)) and the “deviation hypothesis” (see for example (Gerlach and Peng 2005)). Authors that supported the collateral value hypothesis argue that rising house prices boost bank capital by increasing the value of houses owned by banks and the value of the collateral pledged by borrowers. According to this hypothesis, real estate prices should therefore be negatively related to credit risk. On the other side, the deviation hypothesis postulates a positive relationship between house prices and credit risk. The rationale underlying this hypothesis is that persistently rising real estate prices induces larger exposure and the accumulation of risky assets in banks due to excessive lending to risky borrowers at cheap rates. Relaxing lending standards in good times drives up both credit and house prices, while a tightening of standards puts downward pressure on house prices. When house prices fall and lending standards for new loans tighten, homeowners with low or negative equity will increasingly be driven to default, thus increasing the NPL. In an influential paper, Bernanke et al. (1996) suggest that endogenous developments in the financial market can greatly amplify the effects of small income shocks. Bernanke et al. (1996) call this amplification mechanism the “financial accelerator” or “credit multiplier”. In this model, the credit market channel may form part of the monetary transmission mechanism. The model focuses on the macroeconomic effects of imperfections in credit markets. Such imperfections generate premia on the external cost of raising funds, which in turn affect borrowing decisions. The model predicts that endogenous developments in credit markets, such as variations in net worth or collateral, amplify and propagate shocks to the real economy. A positive shock to economic activity causes a rise in housing demand, which leads to a rise in house prices and so an increase in homeowners’ net worth. This decreases the external finance premium, which leads to a further rise in housing demand and also spills over into consumption demand. Therefore, variations in collaterals such as house prices have an important effect on household consumption. Following a similar argument, Hott (2011) develops a model where credit and real estate cycles are produced by irrational expectations on the part of banks. The author develops a partial equilibrium model that allows analyzing the role of banks’ expectations on real estate price cycles. Iacoviello (2005) and Calza et al. (2007) use a similar general equilibrium model to describe the link between loans, real estate prices and economic performance. Marcucci and Quagliariello (2008) found that house prices are positively related to NPL in the short term, which supports the view that wealth could be used as a buffer against unexpected shocks or as collateral to facilitate access to credit (see also Borio and Lowe 2002; Pesola 2011).

2.2. Housing Affordability and Household Vulnerability

Housing affordability also plays a crucial role in credit risk. From a theoretical perspective, dealing with demand for durable goods is similar to demand for non-durable goods. Thus, demand for houses requires essentially both willingness to purchase (or rent) a house and housing affordability. However, unlike demand for non-durable goods, a deterioration of housing affordability can have important consequences on credit risk. In general, housing affordability involves the households’ ability to reasonably meet their mortgage obligations in a way that does not prevent them from accessing the basic necessities of life. This raises a question concerning the effect of changes in housing affordability on the ability of borrowers to fulfil their obligations, and consequently on the likelihood of them becoming defaulters.

Closely related to housing affordability and credit risk is the issue of household vulnerability. From the lenders’ point of view, issuing a loan depends primarily on the borrower’s ability to pay back their debts, which is highly influenced by the borrower’s financial fragility. Indeed, borrower vulnerability is used by banks when assessing loan demanders’ qualifications for a loan. Jappelli et al. (2008) investigate whether indebtedness is associated with increased financial fragility, as measured by the sensitivity of household arrears and insolvencies to macroeconomic shocks, and found that insolvencies tend to be associated with greater household’ indebtedness. Similarly, Rinaldi and Sanchis-Arellano (2006) showed a high association between indebtedness and the performance of banks’ loans.

2.3. Financial Systems

There is now general consensus in the literature that financial liberalization of the mortgage market increases credit risk (see for example (Demirguc-Kunt and Detragiache 1998; Kaminsky and Reinhart 1999)). However, the mechanism through which financial liberalization affects the housing market and credit risk is still subject of debate. The theoretical literature suggests that financial liberalization may influence bank risk through bank competition. On the one hand, the “competition-fragility” hypothesis suggests that higher bank competition following liberalization reduces banks’ charter value and increase banks’ opportunities to take risks (see for example (Keeley 1990)). Also, according to this line of thought the information asymmetries in financial markets are greater when transactions take place among agents separated by physical and cultural distances (Stiglitz 2000). On the other hand, other theoretical models postulate a positive association between competition and credit risk. According to the “competition-stability” hypothesis, more bank competition may reduce bank risk if banks charge lower interest rates to borrowers and diminish their incentives to shift into riskier projects (Boyd and De Nicolò 2005). Therefore, increases in bank competition would be a channel through which liberalization may even reduce credit risk.

Perhaps, even more to the point, there seems to be a significant gap between the lively theoretical discussion on the effect of financial liberalization and the paucity of available empirical literature investigating the structural changes in financial market, in particular in the mortgage market, and how this has affected credit risk. Noticeable exceptions are provided by Muellbauer and Murphy (1997), who found that the financial liberalization of the mortgage markets in the UK led to structural changes in the real estate market. A similar result was found by Iacoviello and Minetti (2008), who found that the sensitivity of house prices to monetary policy shocks in several Northern European countries has increased over time, possibly in relation to the process of financial deregulation.

2.4. Property Market Regulations

Housing markets often feature strong government intervention. This involvement typically takes the form of direct subsidies (e.g., housing allowances, public housing), tax incentives (e.g., mortgage interest deduction), and market regulations (e.g., tenure protection legislation), among other policy instruments. There are several reasons for this activist role of the government. First, it is claimed that housing markets are inefficient and need counterbalancing government actions to achieve pareto efficiency (Borsch-Supan 1994). A second reason, more political, is the belief that housing is a primary need and that society should support housing if individuals cannot afford it. Third, supporting housing investment is often used by government as a welfare tool to redistribute income and wealth. However, government regulations and judicial frameworks may affect the ability of financial institutions to manage credit risk effectively. For example, home ownership protection legislation or any other judicial impediments to collateral enforcement lessen a bank’s ability to implement legal proceedings against borrowers or to receive assets in payment of debt and will also affect collateral execution costs in loan loss provisioning estimations. The impact of costs associated with legal proceedings and the average length of such proceedings should affect the credit risk of financial institutions.

The effects of regulations on credit risk has been the subject of an intense political debate during the recent financial crisis that originated in the United States following the collapse of the housing market. Public opinion has also pointed at the involvement of government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac in the subprime mortgage market as bearing responsibility for the financial crisis. However, to our knowledge, there are no studies analyzing the relation between property market regulation and credit risk or cross-country heterogeneity regarding the importance of legal and institutional characteristics in channeling credit risk. In this study we aim at narrowing the gap.

2.5. Macroeconomic Factors

Finally, the academic literature on credit risk provides evidence that suggests a strong link between credit risk and macroeconomic fundamentals. In this line of research, there is a general consensus that expansionary phases of the business cycles feature lower NPL, as both consumers and firms face a sufficient stream of income to service their debts, whereas the opposite is true during contraction phases. For example, Louzis et al. (2012) found that the quality of lending for households varies inversely with GDP growth rate and house prices, and positively with the unemployment rate and the short-term nominal interest rate. Similarly, Salas and Saurina (2002) provide empirical evidence of a significant negative contemporaneous effect of GDP growth on NPL and conclude that there is a fast transmission mechanism of macroeconomic fundamental shocks and the ability of economic agents to service their loans. From a theoretical point of view, the primary macroeconomic determinants of NPL may be selected from the theoretical literature of life-cycle consumption models. Lawrance (1995) considers a type of Modigliani and Miller (1963) model and introduces explicitly the probability of default. This model implies that borrowers with low income have a higher rate of default due to an increased risk of facing unemployment and being unable to settle their debt obligation. Additionally, in equilibrium, banks charge higher interest rates to riskier clients. Rinaldi and Sanchis-Arellano (2006) extend Lawrence’s model by assuming that agents borrow in order to invest in real or financial assets. The authors’ findings support the view that the probability of default depends on current income and the unemployment rate, which in turn depends on the uncertainty regarding future income and lending rates.

3. The Empirical Investigation

In this section, the empirical models and econometric methods that were used to investigate the research questions under consideration are described. We start our investigation by considering how risk factors relate to the demand side of the credit market. We then consider the supply side and investigate how factors such as financial liberalization and credit market regulations affect credit risk.

3.1. Housing Market, Household Fragility and Credit Risk

As seen in the previous section, the role of housing affordability and household indebtedness are expected to play a significant role in determining financial institutions’ credit risk. The important works by Iacoviello (2005) and Calza et al. (2007), among others, point out that there is a close relationship between housing prices and credit risk. Accordingly, we investigate the following model

where is the natural log of “NPL to gross loans ratio” of the country i at time t. The error term includes an idiosyncratic component and an unobserved heterogeneity component . The vector refers to risk factors related to the macroeconomic fundamentals. In particular, includes: real domestic product per capita growth , unemployment rate () and real interest rate (). Finally, the vector includes a number of variables used in the model to investigate the effects of the housing market on credit risk. We discuss these variables below.

In order to investigate the effect of household indebtedness on NPL, two proxies were used. Namely, the ratio of “household debt to net disposable income” and the ratio of “household housing consumption to household housing disposable income” were considered. The former indicator has been used in many empirical works as a proxy for household debt (see for example (Jappelli et al. 2008)). The theoretical literature suggests that household borrowing can be explained within the demand–supply framework. For example, the life-cycle model and permanent income hypotheses consider the demand side by modelling consumer spending as a function of expected lifetime earnings. According to this well-known model, households aim at smoothing consumption over time to maximize utility, despite varying incomes in different periods. In practice however, consumption may be affected by current income rather than permanent income. By explicitly introducing a default option into the lifecycle consumption model, Lawrance (1995) shows that the possibility of default influences the current level of consumption and the type of borrowing constraints households are likely to face. In light of these arguments, considering household debt as a risk factor may prove to be an important determinant of credit risk. The latter indicator has been included to reflect household housing expenditure. The choice of this risk factor relies on the fact that an important channel for the impact of property prices on the economy is through consumption. Furthermore, property price fluctuations affect consumption through credit availability (see, for example, (Bernanke and Gertler 1995)). Therefore, a depreciation in consumption driven by a decline in property prices is likely to positively influence households’ default decisions.

In addition to the risk factors above, the growth rate of house prices in real terms is considered. House prices may play an important role as risk factors because real estate is used as collateral to reduce the agency costs associated with borrowing to finance housing investment and consumption. The choice of house price as a risk factor is based on three considerations: (i) house prices are closely related to the business cycle, this leads to substantial variation in households’ collateral position over the cycle and therefore cycle-related changes in the quality of a banks’ loan portfolio; (ii) the amount of secured borrowing to finance consumption is closely related to the property value that is used as collateral; and (iii) the spread of mortgage rates over the interest rate varies with the collateral position of each household, thus affecting credit risk. These arguments suggest that households’ use of housing equity as collateral may be important in explaining variations in credit risk.

Consistent with the definition of housing affordability proposed by MacLennan and Williams (1990), we used two proxies to indicate housing affordability, namely “price-to-income” ratio and “price-to-rent” ratio. The rationale for the choice of these variables relies on the fact that both these ratios can provide valuable information on the average household’s ability to afford housing as well as give insights into the performance of housing markets. In general, high values for “price-to-income” and “price-to-rent” ratios may be a signal of overvalued house prices and rents, in which case households would find it difficult to own or rent a house. However, due to the high correlation between these two variables (the calculated correlation coefficient is above 90%), and with the aim of reducing the number of regressors in the estimation, we used principal component analysis over these two indicators to construct a composite measure of housing affordability. The resulting risk factor is referred to as . Details of the principal component analysis are reported in Table A1 of Appendix A. The resulting risk factor is referred to as . Details of the principal component analysis are reported in Table A1 of Appendix A.

3.2. Financial Developments, Credit Market Regulation and Credit Risk

Having specified a model for the demand side of credit-risk-related factors, we now turn our attention to the supply side. Following the pioneering work of Barrell et al. (2010) (see also Berger et al. 2004) we considered factors related to the evolution of credit market structures in addition to the housing market. With this target in mind, the model in Equation (2) was modified as follows

where the elements of the vector are defined as in Equation (2), whereas the vector replaces the vector in Equation (2). The vector refers to a number of risk factors relating to the effect of financial liberalization and regulations on credit risk. We discuss the elements of the vector below in turn.

In the related literature, the choice of a proxy for financial developments has been quite controversial. Several authors in this regard advocate the use of monetary aggregates to reflect both the size and depth of the financial sector. However, monetary aggregates have been widely criticized for being a poor measure in the case of developing financial systems. Furthermore, monetary aggregates have been subject to criticism for reflecting the magnitude of transactional services delivered by the financial sector rather than its efficiency in channeling funds from depositors to borrowers (see for instance (Fry 1997)). As an alternative measure of financial developments, the ratio of “domestic credit provided to the private sector to GDP” has been widely advocated in empirical studies to reflect financial developments (see for example (King and Levine 1993)). The usefulness of this indicator is twofold. First, it is limited to credit allocated to the private sector that allows the efficient use of funds. Second, it is an accurate indicator of the financial institutions’ savings provided to the private sector, since it does not account for the proportion of credit assigned by the central banks. However, the use of this ratio as sole indicator of financial developments may not capture the role of mortgages in the financial system. For this reason, we increment the model with the ratio of “mortgages to GDP” to account for the effect of banks’ mortgage lending behavior. Since housing loan shares constitute the bulk loan portfolios of banks in most developed countries, this ratio can be considered to reflect banks’ lending behavior for housing-related activities. As before, principle component analysis was undertaken in order to obtain a composite indicator able to reflect financial developments, which included banks’ mortgage lending behavior. The resulting financial developments indicator is referred to as . Note that the details on the principal component analysis are provided in Appendix A.

In addition to , the vector contains a composite indicator meant to capture risk factors relating to different aspects of credit market regulation. Namely, the variable is a composite indicator of credit market regulations consisting of: (i) the number of private versus government ownership of banks; (ii) the ratio of government borrowing related to private borrowing; and (iii) the level of interest rate controls and the magnitude of negative real interest rates, if existent. Changes in regulations in a given country may change the banks’ risk taking behavior and hence affect the probability of credit risk. Therefore, the covariate broadly speaking measures the restrictions under which banks operate. We then test for the direct impacts of another component of regulations that concerns specifically the real estate market. In particular, we consider how property sale restrictions, which measure the costs of transferring ownership of a property1, denoted as , affect changes in NPL. Legal or judicial impediments to collateral enforcement influence a bank’s ability to commence legal proceedings against borrowers or to receive assets in payment of debt and also affect collateral execution costs in loan loss provisioning estimations. Therefore, regulatory and judicial frameworks relating to the housing market may influence the banks’ NPL strategy and their ability to reduce NPL.

To estimate the models in Equations (1) and (2), we adopted a dynamic panel approach suggested in Arellano and Bond (1991) and generalized by Arellano and Bover (1995) and Blundell and Bond (1998). In the estimation procedure of Equations (1) and (2), we accounted for the persistence of NPL and any measurement error by taking the first difference of the natural logarithm of NPL as the dependent variable. In the following, we use a dynamic specification allowing for the inclusion of the lagged dependent variable in the empirical model, which accommodates for the autocorrelation in the error term. In the estimation we use the available lags of the dependent variables and the lagged values of the exogenous regressors as instruments. The variables considered as endogenous were instrumented using the lagged values of the variables. Furthermore, in order to avoid potential problems of correlation between the lagged dependent variable and the error term, we used the two-step generalized method of moments (GMM) estimation with instrumental variables. In the estimation, the number of instruments is always kept below the number of groups in all our GMM specifications.

The difference GMM estimator delivers consistent estimators of the parameters in Equations (1) and (2) and it is asymptotically more efficient than the one-step estimator often used in the literature (see Arellano and Bond 1991; Blundell and Bond 1998). It also relaxes the assumption of homoscedasticity in the error term, which is often too restrictive in the empirical data. However, the two-step GMM estimation procedure relies on the estimated residuals and it may impose a downward bias on the estimated standard errors in small samples. To overcome this shortcoming, we used the finite sample correction for the two-step covariance matrix as given in Windmeijer (2005) to estimate the standard errors.

As the consistency of the GMM estimators relies upon the assumption that the instruments are exogenous, we consider two specification tests to investigate the reliability of this crucial assumption. The first specification is the Hansen (1982) test of the over-identification of restrictions, which evaluates the joint validity of the instruments. The second inference procedure is the Sargan specification test, which can be computed using a regression with instrumental variables and involves constructing a quadratic form based on the cross-product of the residuals and exogenous variables. Under the null hypothesis that the over-identifying restrictions are valid, the test statistic is asymptotically distributed as a random variable with (m − k) degrees of freedom, where m is the number of instruments and k is the number of endogenous variables. Failure to reject the null hypothesis implies that the instrumental variables are suitable instruments.

Coming to the model misspecification tests, we assess the fundamental assumption of the serially uncorrelated structure of the error term by testing the null hypothesis that the first differences of the error term are not AR(1) correlated. Failure to reject the null hypothesis of no first order autocorrelation indicates that the model is not well specified. Finally, the AR(2) test statistic is used to test the second-order autocorrelation of the residuals. Rejection of the null hypothesis of AR(2) test implies heterogeneous cross-section dependence, and thereby the inconsistency of GMM estimators.

4. Data and Empirical Results

For the empirical investigation, we used a balanced panel dataset of 23 countries over the period of 2000–2012. The sample includes countries that suffered major housing market contractions during the recent financial crisis, but also reflects a broad spectrum of financial development patterns, heterogenous levels of financial vulnerability and different housing market structures. The countries included in the sample are: Australia, Austria, Belgium, Canada, Czech Republic, Denmark, Estonia, Finland, France, Germany, Ireland, Italy, Japan, Luxembourg, The Netherlands, New Zealand, Norway, Poland, Portugal, Spain, Switzerland, the United States and the United Kingdom.

Our balanced panel data were compiled from several sources. The World Development Indicators from the UK Data Service (UKDS) and the Financial Soundness Indicators from the IMF and World Bank supply data of the NPL ratio on annual frequency, but for different time periods. Therefore, the data were retrieved primarily from the UKDS and extended from the other two sources. The probable differences in methodology between the three sources were accounted for by matching values of NPL over the overlapping periods. Real residential property prices were obtained from different national statistical offices. Data for real interest rates, ratio of household debt to disposable income, consumption to disposable income and housing affordability were accessed from the Organization for Economic Co-operation and Development (OECD). Finally, data on financial liberalization were obtained from the Fraser Institute’s Economic Freedom of the World database.

Table 1 reports the variables with the expected signs and reports the descriptive statistics. Before presenting the models below, we briefly summarize the expected signs of the different risk factors included in the empirical estimation.

4.1. Dynamic Panel Data Estimations

4.1.1. Models with Household Credit Risk Factors

Table 2 reports the estimated coefficients of Equation (1) along with statistical significance. For ease of interpretation asterisks, indicate the level of statistical significance of the estimated coefficients. Robust standard errors are reported in parenthesis.

Turning to the results, column 1 in Table 2, reports the estimated parameters of a baseline model, referred to as Model 1. This model with only macroeconomic fundamentals is used as a benchmark; then the other risk factors in Equation (1) were added sequentially and the estimation results reported in columns (3)–(5). Starting with , the coefficient of the lagged dependent variable was highly significant, thus suggesting high persistence in NPL growth ratios. Also, the implication of the negative sign for the estimated coefficient of is that the NPL growth decreases when high ratios of NPL are observed in the previous year. This result may be attributed to write-offs. From Table 2 it appears that and show high statistical significance and carry a negative sign. This finding indicates that an increase in contributes to a decrease in NPL growth ratio, implying that an economy that is enjoying a stable rate of growth also increases a borrower’s ability to service their debts. Looking now at and , the estimated coefficients carry a positive sign and are statistically significant, thus indicating a positive association between NPL and unemployment rate. The explanation of positive relationship relies on the fact that an increase in the unemployment rate negatively impacts borrowers’ income and undermines their ability to pay back their contracted debts, or at least may provide an incentive to terminate their payments. From Table 2 it appears that is significant (although at 10%) and carries the correct sign. An increase of interest rate is likely to increase impaired loans by forcing borrowers to incur higher costs on the debts. This is turn might encourage them to default if these costs become unaffordable. Overall, the results in Model 1 are consistent with the consensus in the literature, which suggests that the contractionary phases of the business cycle are often accompanied by a greater credit risk (see Louzis et al. 2012; or Salas and Saurina 2002).

Considering now Model 2, the estimated coefficients and are significantly different from zero and carry a negative sign. The estimated sign suggests that the collateral value hypothesis (see Daglish 2009) held for the data at hand. As seen in Section 2, the collateral value theory argues that rising house prices reduces the credit risk of the banks’ loan portfolios by increasing the value of the houses owned by financial institutions and the value of the collateral pledged by borrowers. Thus, it suggests a negative relationship between house price changes and bank NPL. Note that, the covariate has been dropped from this and the remaining models as it was found to be not significantly different from zero.

In Model 3, the estimated coefficient for the covariates and was statistically significant and carried positive and negative signs for the contemporaneous and lagged estimated coefficients, respectively. These findings are in line with the theoretical model in Lawrance (1995), briefly mentioned in Section 2, and confirm that liquidity constraints can explain the default decisions of consumers (see also Rinaldi and Sanchis-Arellano 2006). In particular, the results indicate that high household indebtedness burdens borrowers and undermines their ability to settle their scheduled obligations in the short term. Indeed, the greater the household indebtedness burden, the higher the default probability due to potential difficulty in fulfilling their committed debts. Consequently, banks’ loan portfolios are more likely to witness a higher volume of NPL growth. This can explain the positive sign of both and . However, over time, greater household indebtedness might warn lenders of the higher level of fragility of their borrowers and prompt more cautious lending standards to mitigate risky loans by adopting tighter lending terms on loans to households with high debts. Consequently, more constrained access to loans helps to reduce the amount of NPL. This explains the negative sign for the estimated coefficient of and . The implication of these results is that financial institutions take time to react to borrowers’ negative financial shocks.

Turning now to Model 4, from Table 2 it appears that the estimated coefficient for is statistically significant with a negative sign, whereas the lagged coefficient has negative sign. Therefore, an increase in housing affordability was found to reduce credit risk. In principle, housing becomes more affordable when either house prices (or rents) decrease or incomes increase; either case improves households’ debt servicing ability, therefore reducing the credit risk. The positive sign of the estimated coefficient for may be explained by theoretical models that suggest myopic behavior of banks or other types of irrational expectation models (see Hott 2011). According to this literature, when default rates on loans decrease, financial institutions are more optimistic about the creditworthiness of their customers. This leads to higher loan approval, which in turn leads to higher real estate prices and, according to the collateral value hypothesis, to lower default rates. However, when the rate of change of house prices gets too small to justify the high real estate price level, default rates start to increase again. Now the process is reversed and banks change their expectations, becoming more pessimistic about the risk to their loan portfolios. As a result, lending institutions impose tighter conditions on loans for households, pushing house prices down and leading to a higher volume of negative equity held by banks, which in turn causes higher NPL growth ratios. Similarly to the impact of household vulnerability, this implies that lenders take time to recognize the decline in housing affordability and adjust their lending policy by tightening lending terms to households with fragile financial health.

4.1.2. Models with Credit Supply Risk Factors

Moving to the estimation of Equation (2), Model 1 in Table 3 reports the estimated coefficients for the benchmark model as well as the proxy variables for financial developments. Note that the house price variable has been added to the baseline model. This is because sharp cyclical variations in real estate prices are expected to increase credit risk. Omitting this covariate from the model estimation procedure would induce an omitted-variable problem, leading to estimators that are biased. From Model 1, it appears that financial developments and banks’ lending behavior have an important effect on the performance of loan portfolios, as the estimated coefficients of the proxy for financial developments are highly significant. However, the estimated coefficients of this covariate have a negative sign in the contemporaneous effect and a positive sign in the lagged effect. The implication of the positive sign for is that the transmission mechanism of an increase in loans and mortgages on NPL is quite slow as it is binding only over time. Given the fact that mortgage contracts are usually issued over a long term, the negative consequences of excessive mortgage lending are supposed to appear with time delay. Note that the indicator for financial developments is a composite measure that includes the ratio of mortgages to GDP. This ensures that the proxy for financial liberalization takes into consideration the developments in the housing finance market.

All in all, the positive estimated coefficient of supports the “competition-fragility” hypothesis rather than the “competition-stability” hypothesis (see Section 2) thus suggesting that higher bank competition following liberalization increases banks’ opportunities to take risks.

Coming now to Model 2 in Table 3, the estimated coefficients for CRM are statistically significant and carry a negative sign, demonstrating that underregulated financial systems are more prone to credit risk and banking sector instability. Similarly, the estimated signs for RPS are negative and significant. This result suggests that the regulatory frameworks relating the real estate market influence the banks’ ability to reduce NPL. This may be due to the fact that legal or judicial impediments to collateral enforcement may influence a bank’s ability to commence legal proceedings against borrowers or to receive assets in payment of debt and might also affect collateral execution costs in loan loss provisioning estimations.

In Model 3, we investigate the joint effect of credit market regulations and restrictions on property sales on the growth of impaired loans by augmenting Model 2 with the interaction variable denoted as . Similarly, Model 4 investigates the joint effect of credit market regulations and financial developments on NPL by constructing another interaction variable that captures the joint effect of the two risk factors. This is denoted as . From Table 3 it appears that in both Model 3 and 4 the estimated coefficients are highly statistically significant, with a dominance of negative signs. The negative estimated signs in Model 3 indicate that imposing tighter regulations contributes to lower ratios of bad loans in the banks’ loan portfolios, and hence more sustainable banking performance and financial system. Similarly, the negative estimated signs in Model 4 indicate that market liberalization can happen without an increase in credit risk provided that the credit markets are highly regulated. More importantly, the estimation outcomes of the last two models have important policy implications, suggesting that financial development policies, credit markets and housing market regulations do not have to offset each other. In contrast, each policy may overcome the shortcomings of the other. Therefore, our findings suggest that the regulation of financial markets and real estate markets should be designed in a wider policy framework, with tight cooperation between policymakers in the real estate market and the banking industry, in order to ensure a sustainable and sound banking system.

The bottom panel of Table 2 and Table 3 report the model specification tests discussed in Section 3. The results show that all the estimated GMM models pass the misspecification tests as the null hypothesis AR(1) test is rejected (although at 10%) and the AR(2) null hypothesis in not rejected. Furthermore, the null hypotheses of the Hansen test and the Sargan test for the joint validity of the instrument set and overidentification restrictions are not rejected, confirming that the instruments are exogenous and not correlated with the error term. Overall, the misspecification tests in Table 2 and Table 3 support to the validity of the instruments used in the estimation and suggest that the models are well specified.

Summarizing the results above, our analysis indicates that credit market developments can be important in explaining credit risk. In particular, larger credit availability due to increased credit supply can lead to an increase in external financial resources and hence to an increase in current consumption and greater level of household indebtedness. A higher debt ratio in turn amplifies the impact of macroeconomic shocks on household balance sheets and affects their ability of debt servicing. Since the large increase of debt can be attributed to an increase in mortgage finance in the context of dynamic housing markets, such amplifying effects can also emerge as a result of pronounced changes in house prices via the increase in the value of collateral. In this context, a higher level of debt implies a greater risk that households will face problems in servicing their debt and as a result a higher non-performing ratio. Our estimation results suggest that market regulations also play an important role in determining credit risk.

5. Further Empirical Investigation

5.1. Country Idiosyncratic Factors and Credit Risk

Above, the relationship between financial market structure and NPL has been investigated. However, we consider a heterogeneous sample of countries with quite different histories of financial developments and financial regulatory structures. The deregulation process that started in the last few decades occurred in different countries at different paces. It is therefore of interest to consider whether different patterns of financial liberalization or heterogeneous housing market regulations have had an impact on the evolution of credit risk. Accordingly, questions of interest are: Is it actually the case that banks in countries with greater financial liberalization and fewer regulations also experienced higher credit risk? Or is it possible to establish a causal relation between credit risk and idiosyncratic regulatory systems by discriminating according to the degree of (de-)regulation? Also, does the attitude toward risk of financial institutions change over the cycle differently across countries? These empirical questions can be formulated as comparisons between the distribution functions of NPL and (de)-regulation variables corresponding to different groups in the population.

To tackle the research questions above, our first procedure relies on the concept of quantile shares, which allows us to investigate the properties of the distribution function of each variable under investigation. To be more specific, we consider the distribution function of each element of the vector . Note that to simplify the notation, the i and t subscripts for each variable were dropped from the equations. Let j (for be an element of the vector X, then for any j we can define as the distribution function of and the quantile function as

with . In order to investigate the distribution of the element we calculate the proportion of total outcome that falls into the quantile interval , for , as

The quantity in Equation (3) allows us to investigate the shares of total outcome pertaining to the population segment from relative rank to relative rank in the list of ordered outcomes.

The standard errors of the estimated quantile shares in Equation (3) can be quite cumbersome to calculate. Moreover, due to the small time series dimension of the panel dataset, the estimated standard errors and the estimated confidence intervals of the estimators of in Equation (3) may be inaccurate. To overcome this problem, the estimated standard errors of were obtained by using the non-parametric bootstrap method by resampling 1000 times from the empirical distribution of the in order to create the empirical analogue and then calculate the estimated confidence interval lower and upper bounds. Due to the panel structure of the data, the resampling has been done in both the cross-sectional and temporal dimension (see for example (Kapetanios 2008)).

Table 4 reports the estimates of the quantile shares of each element of the vector X, as well as the estimated confidence intervals. In particular, in the first column, the quantiles under consideration are reported, whereas in columns 2–5 the estimated proportion of the total outcome that falls into each quantile is reported. For ease of interpretation, the proportions are reported as percentages, and the quantiles are expressed in term of percentile shares.

From Table 4 it appears that NPL do not follow a uniform distribution. On the contrary, they are highly skewed toward the top quantile. In particular, more than 54% of NPL are concentrated in the top quantile, meaning that the top 20% of the countries had more than half of the proportion of NPL in the sample under consideration. On the other hand, countries in the bottom quantile only had approximately 3.42% of the NPL ratios. Incidentally, the distribution of FD seems to follow a similar pattern, although its distribution appears to be less left-tail skewed. To be more precise, from Table 4 it appears that countries in the top quantile have approximately 37% of the total mortgages and credits to the private sector, whereas countries in the bottom quantile only have a percentile share of 9.45%. Looking at CRM and RPS, the distribution of the shares across quantiles appears to be more uniform. This is probably due to the fact that all the countries in our sample are classified as developed countries and are likely to be bound by similar regulatory restrictions in term of credit market (e.g., Basel III Regulations) or real property sale regulations. Note that looking at the estimated confidence interval in Table 4, it appears that the bootstrap algorithm used to calculate the standard errors of the estimated quantile shares works quite well as it delivers small confidence intervals throughout the distribution of the variables under consideration.

5.2. Quantile-Based Estimation of Credit Risk

From Table 4 it appears that greater estimated shares of NPL are concentrated in countries that are in the top quantile in terms of financial developments. It is now of interest to move away from the analysis of individual distributions and establish a causal relation between the risk factors under consideration and credit risk. In this respect, in Section 4 we were particularly interested in estimating the effects of the risk factors in vector Z of Equation (2) on the conditional mean of NPL. The econometric method used to estimate Equation (2) allows us to answer the question of whether or not the risk factors considered on the right hand of the equation affect the conditional mean distribution of NPL. However, in light of the results in Table 4, the focus on the conditional mean of the NPL distribution may hide important features of the relation between the risk factors under consideration and the level of credit risk faced by financial institutions. Accordingly, in this section we are interested in answering a related question: Does a one unit increase of a given the risk factor of vector Z in Equation (2) affects countries with a low ratio of NPL differently from countries with high ratio of NPL? In other words, do countries in the bottom quantile in terms of financial liberalisation or regulatory structure also experience a different impact on credit risk with respect to countries in the top quantile?

To consider whether the marginal effects of the risk factors in vector Z are different for countries that are in the top quantiles of the NPL distribution with respect to the countries that are in the bottom quantile we focus on the estimation of , rather than considering as done in Equation (2). Thus, the p-th conditional quantile function of the response of the t-th observation on the i-th country can be represented as

The model in Equation (4) can be estimated as a non-additive fixed effect panel as suggested in Powell and Wagner (2014). The advantage of this model is that unlike the quantile method for panel data with additive fixed effects, (see Abrevaya and Dahl 2008; Geraci and Bottai 2007), the model in Equation (4) maintains the non-separable disturbance term associated with quantile estimation. In addition, the distribution of the non-separable disturbance term is allowed to have an unspecified distribution. The estimator in Equation (4) can be done by GMM by solving the optimization problem

where are the sample moments and W is a weighting matrix. As before, the two-step GMM estimation was used to estimate Equation (5) and the partial derivative:

can be interpreted as the marginal change relative to the -quantile of due to a unit increase in a given element of the vector . As increases continuously from 0 to 1, it is possible to trace the entire distribution of the conditional on .

Table 5 reports the estimated parameters for the quantiles p ∈ {0.25, 0.50, 0.80} along with the associated standard errors. Note that quantiles above the 80th quantile were difficult to estimate, probably due to the small number of observations in these quantiles, therefore estimation was restricted up to the 80th quantile. The first column of Table 5 reports the dependent variable by quantile, whereas risk factors are reported in column two. In column three, the estimated coefficients of Equation (4) for the respective quantile are reported, whereas in the fourth column the corresponding standard errors of the estimated coefficient are reported.

Looking at the results in Table 5, it appears that the estimated coefficient of is positive and significantly different from zero only for countries above the bottom quantile of NPL. Also, the magnitude of the estimated parameter is relatively low for countries in the median quantile of NPL distribution, but increases sharply for those countries in the top quantile. Therefore, the marginal effect on credit risk of a one unit increase of NPL ratio in countries in the top quantile is much greater than the marginal effect in countries that find themselves in the desirable bottom quantile. With regard to the effect of , the negative signs of the estimated parameters confirm the results in Table 3. However, from Table 5 it appears that credit market regulations are binding only in countries above the median quantile, whereas the estimated parameter is not significant for countries in the lowest quantile. Similarly, the marginal effect of on credit risk is much smaller than and is significant only for countries in the top quantile of NPL distribution.

To summarize the results above, there is great evidence that (de)-regulation has had an important impact on the credit risk faced by financial institutions in the period under investigation. The results in Table 4 and Table 5 may have important consequences for the transmission of monetary policy via the credit channel, as widespread imperfections in the credit market, such as asymmetric information or imperfect contract enforceability, affect the lending policy of banks and therefore the transmission channels of monetary policy (see for example (Bernanke and Gertler 1995)).

5.3. The Financial Accelerator Mechanism and Credit Risk

In their influential paper, Bernanke et al. (1996) suggested that the financial accelerator mechanism described in Section 2 amplifies and propagates the responses of the economy to various shocks. The key idea behind the financial accelerator is that under the assumption of a fixed leverage ratio, positive or negative shocks to income have a pro-cyclical effect on the borrowing capacity of households and firms. In particular, when house prices fall, households have a smaller deposit (i.e., lower loan to value ratio) available than they otherwise would for the purchase of their next home. Therefore, home owners are able to obtain less favorable mortgage interest rates when renegotiating their mortgage and have less scope for extracting additional equity to finance consumption. In general, fluctuations in the real estate market significantly affect the value of houses as collateral and therefore strongly influence borrowing conditions for households. Accordingly, in this section we extend our analysis to consider the role of housing as collateral for household borrowing. We are particularly interested in understanding whether the recent deregulation of the credit markets has reinforced the accelerator mechanism by amplifying the responses of the economy to macroeconomic shocks. In principle, cheaper access to home equity means that, for a given house price rise, more additional borrowing will be devoted to consumption relative to housing investment. We conjecture that house prices play an important role in amplifying the transmission mechanism of shocks since housing is used as collateral to reduce the agency costs associated with borrowing to finance housing investment and consumption. Therefore, in principle, positive shocks to household income translate into larger house price increases in countries where the prevailing leverage ratios are higher and smaller in countries where such leverage ratios are lower.

With this target in mind, we calculated a time-varying correlation coefficient between NPL and FD. If it is actually the case that house prices have an impact on consumption via credit market effects, we should see the correlation between FD and NPL changing over time. In particular, the correlation should be negative during periods of credit expansion, since the increase in house prices makes more collateral available to homeowners. This in turn may encourage households to borrow more in the form of mortgage equity withdrawal to finance the desired levels of consumption and housing investment. On the other hand, the correlation should be positive during the contraction phases of the housing market, since homeowners with low or negative equity will increasingly be driven to default. Also, if this is actually the case, and the magnitude of the propagation of the financial accelerator effect is greater for those countries with high leverage ratios, we should see countries in the top quantile of FD in Table 4 having a different correlation pattern with respect to countries in the bottom quantile.

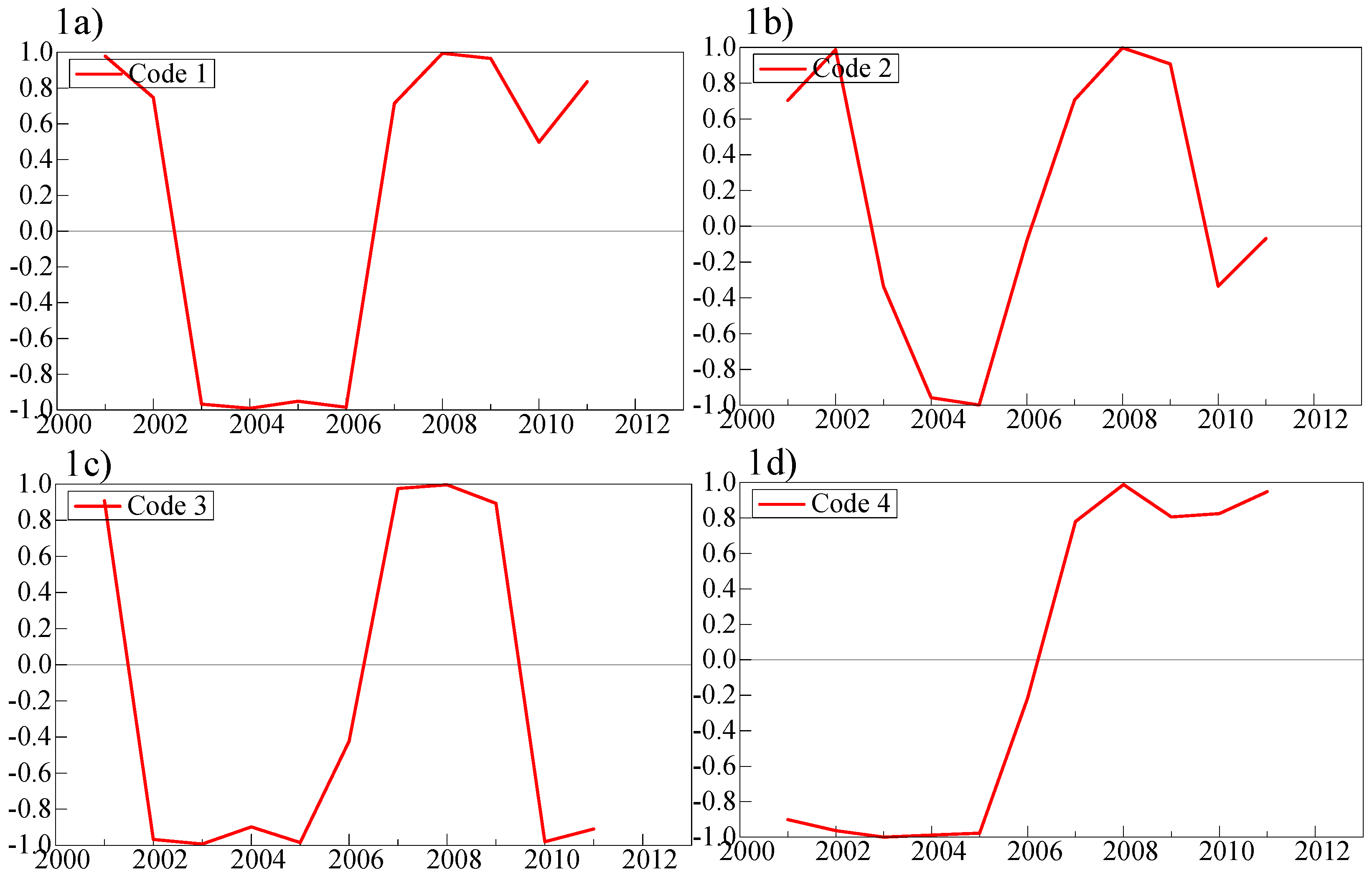

To investigate the hypothesis above we first classified each country in the sample according to the degree of financial liberalization by considering the quantile distribution of FD for each country over time. In order to classify the countries according to the degree of financial liberalization, each country i at time t was classified as belonging to the 25th, 50th, 80th or the 100th percentile of the FD distribution by assigning a code from 1 to 4 to each percentile; the 25th percentile being code 1 and the 100th percentile being code 4. In doing so, we were able to classify each country, in each year, as belonging to a given group according to the code assigned. Finally, for each country the closest integer of the arithmetic average of the assigned code over the time was taken and the countries in the sample were classified into four groups. Note that given the short timespan considered in the sample, for the majority of the countries, the code assigned did not show much variation. Table A3 in Appendix A reports the classification of the countries by code.

Figure 1 shows the time-varying coefficients between NPL and FD by code. In particular, Figure 1a–d reports the time-varying correlation coefficients between NPL and FD for countries in code 1, 2, 3 and 4, respectively. For each code, the time-varying correlation coefficients between the NPL and FD were calculated using a three-year moving window as follows

From Figure 1a–d it appears that the correlation between NPL and FD changes over time quite substantially, no matter the country code taken into consideration. There is clear evidence that the subprime mortgage crisis that originated in the U.S. toward the end 2005 had an impact in all the countries under consideration. Indeed, regardless of the code under consideration, starting from 2006, the calculated correlation coefficients have positive signs, thus confirming the predictions of the financial accelerator model in Bernanke et al. (1996). Also, it appears that the financial accelerator mechanism is greater for countries classified in code 4, which have a higher leverage ratio. Indeed, looking at Figure 1a–c it appears that for countries coded 1–3 the signs of show the features of a mean reverting stochastic process, since after 2008 the positive sign started to revert back to a negative sign. However, the same is not true for code 4 countries, where the positive signs of show greater persistence over time and actually fail to revert to the negative sign over the period under consideration.

The results in Figure 1a–d also suggest that house prices have a direct impact on consumption via credit market effects. From the negative signs of it appears that homeowners use houses as collateral to extend the amount of loans, since borrowing on a secured basis against ample housing collateral is generally cheaper than borrowing against little collateral or borrowing on an unsecured basis (via a personal loan or credit card). Thus, an increase in house prices makes more collateral available to homeowners, which in turn encourages them to borrow more in the form of mortgage equity withdrawal, to finance desired levels of consumption and housing investment. This effect of the credit market on consumption via households’ collateral position has important consequences for policy makers and their desire to minimize large variations in the property markets in order to stabilize the economy.

6. Concluding Remarks

In this paper, we investigated the determinants of non-performing loans. Particular attention was given to the housing markets and the effects of housing affordability on credit risk. Given the expansion of credit to the private sector in most developed countries, the effect of household indebtedness was also considered. Finally, the characteristic of the financial systems and regulations in which financial institutions operate were included in the analysis.

In line with the literature (see for example (Louzis et al. 2012; Salas and Saurina 2002)), it was found that macroeconomic conditions have a non-negligible impact on credit risk. The quality of lending for households varies inversely with GDP and house prices, and positively with the unemployment rate and interest rate. Evidence from analyzing a large panel of data also suggest that household affordability is positively correlated with credit risk. Similarly, an increase in household indebtedness positively effects credit risk.

From our analysis, it emerged that loose credit market regulations and restrictions to property markets play an important role in the determination the risk of loan portfolios. It was found that financial institutions in countries that are at the bottom quantile in terms of credit market liberalization and in the top quantile in terms of property market regulations, ceteris paribus, also experience lower credit risk. This result corroborates the findings of several empirical works. For example, Dell’Ariccia et al. (2012) found that innovations such as mortgage securitization contributed to a deterioration in underwriting standards in countries such as the United States in the recent financial crisis, whereas covered bonds contributed to safer mortgages in Europe.

Our findings have several implications in terms of financial regulations and housing policy. Specifically, there is evidence that household financial fragility interacts with the regulations in which financial institutions operate via the credit channel. Widespread imperfections in the credit market, such as asymmetric information or imperfect contract enforceability, result in suboptimal credit policy. In turn, the credit channel affects financial stability and the wider economy. This suggests that regulatory authorities should closely monitor the mortgage market and enforce the measure of risk management on financial institutions. Relying on banks’ voluntary efforts to manage bad loans may not be enough. Regulatory authorities may want to guide banks as to the optimal use of their capital buffers and determine target loan loss provisions. On their side, financial institutions may review the range of risk strategies available and their respective financial impact. In this respect, stress testing exercises may be used to evaluate the risk exposure of bank’s portfolio to macroeconomic conditions.

Another implication of our empirical study is that housing finance systems deeply affect household financial fragility, and therefore credit risk. In this respect, regulators may impose lower loan-to-value (LTV) ceilings to mitigate the impact of the financial accelerator mechanism by reducing the transmission from increases in income to increases in house prices. A growing literature shows that the LTV policy is a promising road to greater financial stability (see for example (Crowe et al. 2011; or Claessens et al. 2012)).

Author Contributions

Both authors contributed equally to the paper.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Principal component analysis for housing affordability, .

| Component | Eigenvalue | Difference | Proportion | Cumulative Value | Cumulative Proportion |

|---|---|---|---|---|---|

| Component 1 | 1.916 | 1.832 | 0.952 | 1.916 | 0.958 |

| Component 2 | 0.083 | - | 0.045 | 2.000 | 1.000 |

Principal component analysis on “price to income” and “price to rent”. Note that the eigenvalue accompanying the first component is significantly higher than the one on the second and can explain around 95% of the standardized variance in the variables under consideration. Thus, the first component is used as a summary indicator of housing affordability.

Table A2.

Principal component analysis for financial development, ().

| Component | Eigenvalue | Difference | Proportion | Cumulative Value | Cumulative Proportion |

|---|---|---|---|---|---|

| Component 1 | 1.724 | 1.448 | 0.862 | 1.724 | 0.862 |

| Component 2 | 0.275 | - | 0.137 | 2.000 | 1.000 |

Principal component analysis on “mortgage to GDP” and “domestic credit provided to the private sector to GDP”. The principal component analysis in Table A2 shows that the eigenvalue associated with the first component is significantly higher than one and can explain more than 86% of the standardised variance in the two variables, while the second component represents only around 13% of these variations. Therefore, the first component proxy for financial developments.

Table A3.

Classification of countries according to the degree of financial liberalization.

| Country | Code |

|---|---|

| Australia | 3 |

| Austria | 2 |

| Belgium | 1 |

| Canada | 3 |

| Czech Republic | 1 |

| Denmark | 4 |

| Estonia | 1 |

| Finland | 1 |

| France | 2 |

| Germany | 2 |

| Ireland | 3 |

| Italy | 1 |

| Japan | 3 |

| Luxembourg | 3 |

| Netherland | 4 |

| New Zealand | 3 |

| Norway | 2 |

| Poland | 1 |

| Portugal | 3 |

| Spain | 3 |

| Switzerland | 4 |

| United Kingdom | 4 |

| USA | 4 |

Note: Code 1, 2,3 and 4 correspond to the 25th, 50th, 80th and 100th percentale of FD, respectively.

References

- Abrevaya, Jason, and Christian M. Dahl. 2008. The effects of birth inputs on birthweight. Journal of Business and Economic Statistics 26: 379–97. [Google Scholar] [CrossRef]

- Andrews, Nancy O. 1998. Trends in the supply of affordable housing. Paper presented at Meeting America’s Housing Needs. [Google Scholar]

- Arellano, Manuel, and Stephen Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef]

- Arellano, Manuel, and Olympia Bover. 1995. Another look at the instrumental variable estimation of error components models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef]

- Barrell, Ray, E. Philip Davis, Dilruba Karim, and Iana Liadze. 2010. Bank regulation, property prices and early warning systems for banking crises in OECD countries. Journal of Banking and Finance 34: 2255–64. [Google Scholar] [CrossRef]

- Berger, Allen N., Asli Demirguc-Kunt, Ross Levine, and Joseph G. Haubrich. 2004. Bank and competition: An evolution in the making. Journal of Money, Credit and Banking 36: 433–51. [Google Scholar] [CrossRef]

- Bernanke, Ben S., and Mark Gertler. 1995. Inside the black box: The credit channel of monetary policy transmission. Journal of Economic Perspectives 9: 27–48. [Google Scholar] [CrossRef]

- Bernanke, Ben S., Mark Gertler, and Simon Gilchrist. 1996. The financial accelerator and the flight to quality. Review of Economics and Statistics 78: 1–15. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Borio, Claudio E., and Philip William Lowe. 2002. Asset Prices, Financial and Monetary Stability: Exploring the Nexus. Bank for International Settlements Working Paper No. 114. Basel: Bank for International Settlements. [Google Scholar]

- Borsch-Supan, Axel. 1994. Housing market regulations and housing market performance in the United States, Germany, and Japan. In Social Protection versus Economic Flexibility: Is There a Trade-Off? Edited by Rebecca M. Blank. Chicago: University of Chicago Press. [Google Scholar]

- Boyd, John, and Gianni De Nicolò. 2005. The theory of bank risk taking and competition revisited. Journal of Finance 60: 1329–43. [Google Scholar] [CrossRef]

- Calza, Alessandro, Tommaso Monacelli, and Livio Stracca. 2007. Mortgage Markets, Collateral Constraints, and Monetary Policy: Do Institutional Factors Matter? CEPR Discussion Papers No. 6231. Washington, DC: CEPR. [Google Scholar]

- Claessens, Stijn, M. Ayhan Kose, and Marco E. Terrones. 2012. How do business and financial cycles interact? Journal of International Economics 87: 178–90. [Google Scholar] [CrossRef]

- Crowe, Christopher, Giovanni Dell’Ariccia, Deniz Igan, and Paul Rabanal. 2011. How to deal with real estate Booms: Lessons from country experiences. Journal of Financial Stability 9: 300–19. [Google Scholar] [CrossRef]

- Daglish, Toby. 2009. What motivates a subprime borrower to default? Journal of Banking & Finance 33: 681–93. [Google Scholar]

- Dell’Ariccia, Giovanni, Deniz Igan, and Luc Laeven. 2012. Credit booms and lending standards: Evidence from the subprime mortgage market. Journal of Money, Credit and Banking 44: 367–84. [Google Scholar]

- Demirguc-Kunt, Asli, and Enrica Detragiache. 1998. The determinants of banking crises in developed and developing countries. IMF Staff Paper 45: 81–109. [Google Scholar] [CrossRef]

- Favara, Giovanni, and Jean Imbs. 2015. Credit supply and the price of housing. American Economic Review 105: 958–92. [Google Scholar] [CrossRef]

- Fry, Maxwell J. 1997. In Favour of financial liberalisation. The Economic Journal: The Quarterly Journal of the Royal Economic Society 107: 754–70. [Google Scholar] [CrossRef]

- Geraci, Marco, and Matteo Bottai. 2007. Quantile regression for longitudinal data using the asymmetric Laplace distribution. Biostatistics 8: 140–54. [Google Scholar] [CrossRef] [PubMed]

- Gerlach, Stefan, and Wensheng Peng. 2005. Bank lending and property prices in Hong Kong. Journal of Banking & Finance 29: 461–81. [Google Scholar]

- Girouard, Nathalie, and Sveinbjörn Blondal. 2001. House Prices and Economic Activity. OECD Working Paper No. 279. Paris: OECD. [Google Scholar]

- Gwartney, James, Robert Lawson, and Joshua Hall. 2017. Economic Freedom of the World: 2017 Annual Report. Toronto: Fraser Institute. [Google Scholar]

- Hansen, Lars Peter. 1982. Large sample properties of generalized method of moments estimators. Econometrica 50: 1029–54. [Google Scholar] [CrossRef]

- Hott, Chrisitan. 2011. Lending behaviour and real estate prices. Journal of Banking and Finance 35: 2429–42. [Google Scholar] [CrossRef]

- Iacoviello, Matteo. 2005. House prices, borrowing constraints, and monetary policy in the business cycle. American Economic Review 95: 739–64. [Google Scholar] [CrossRef]

- Iacoviello, Matteo, and Raoul Minetti. 2008. The credit channel of monetary policy: Evidence from the housing Market. Journal of Macroeconomics 30: 69–96. [Google Scholar] [CrossRef]

- Jappelli, Tullio, Marco Pagano, and Marco Di Maggio. 2008. Households’ indebtedness and financial fragility. Journal of Financial Management, Markets and Institutions 1: 26–35. [Google Scholar]