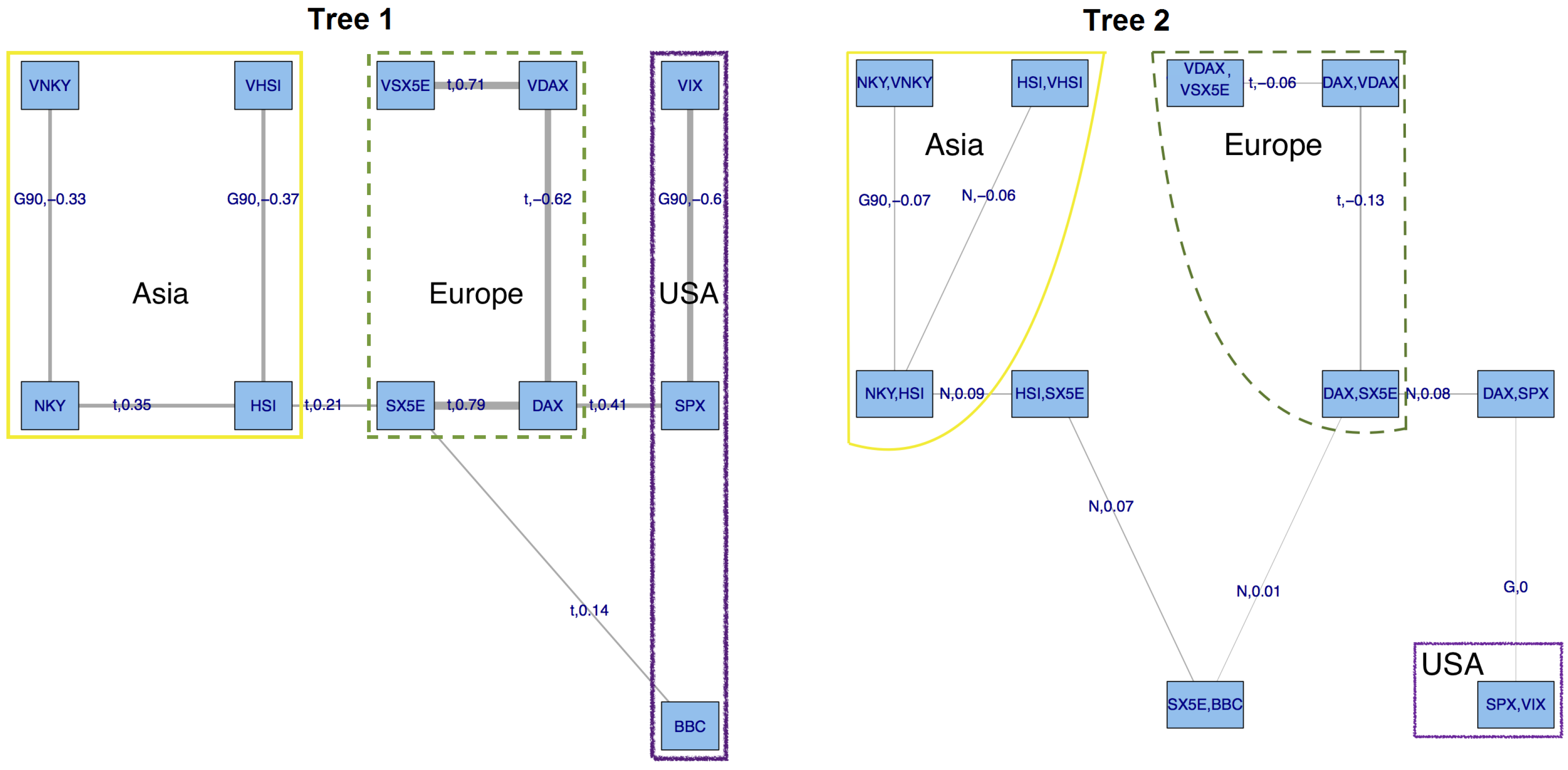

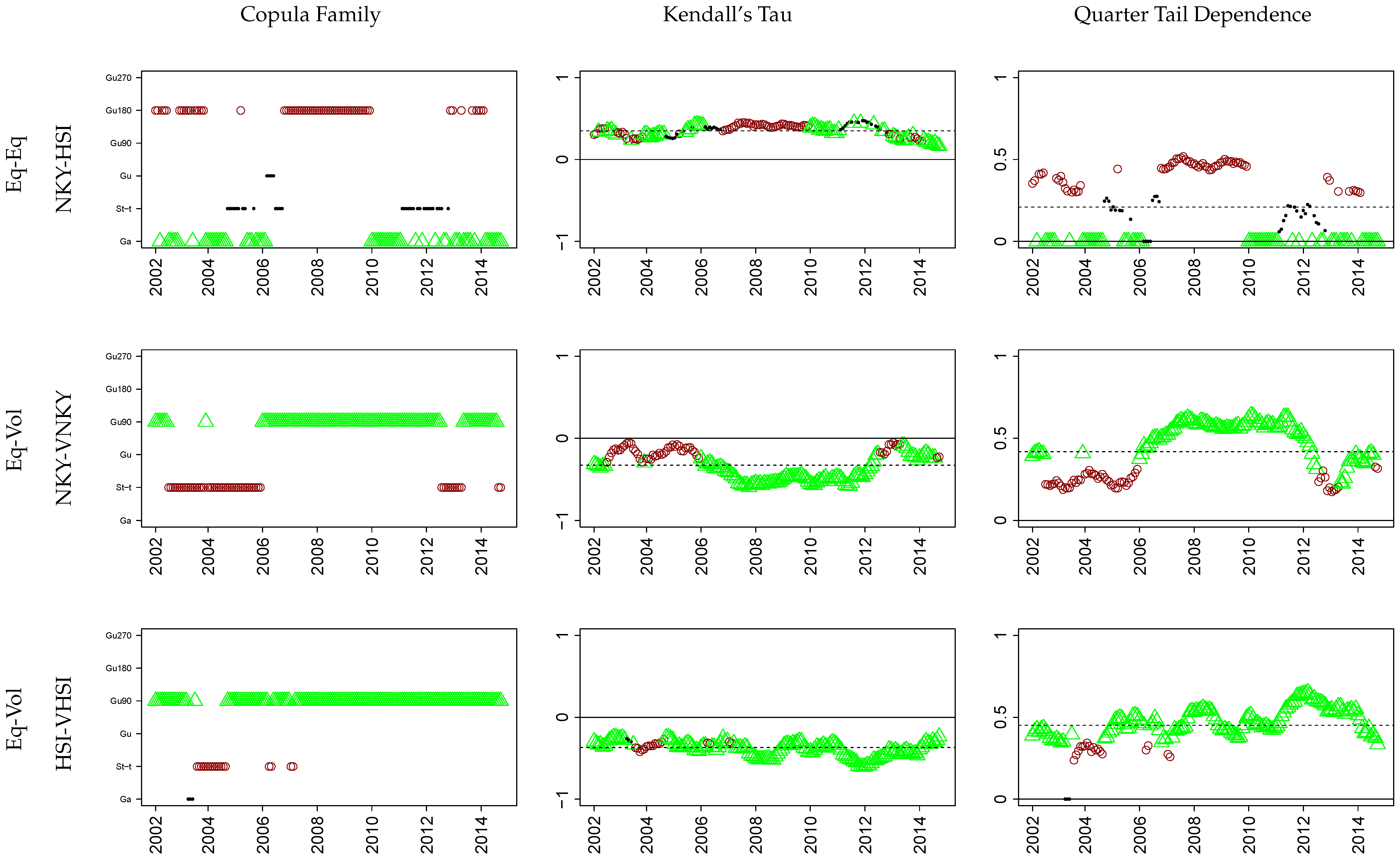

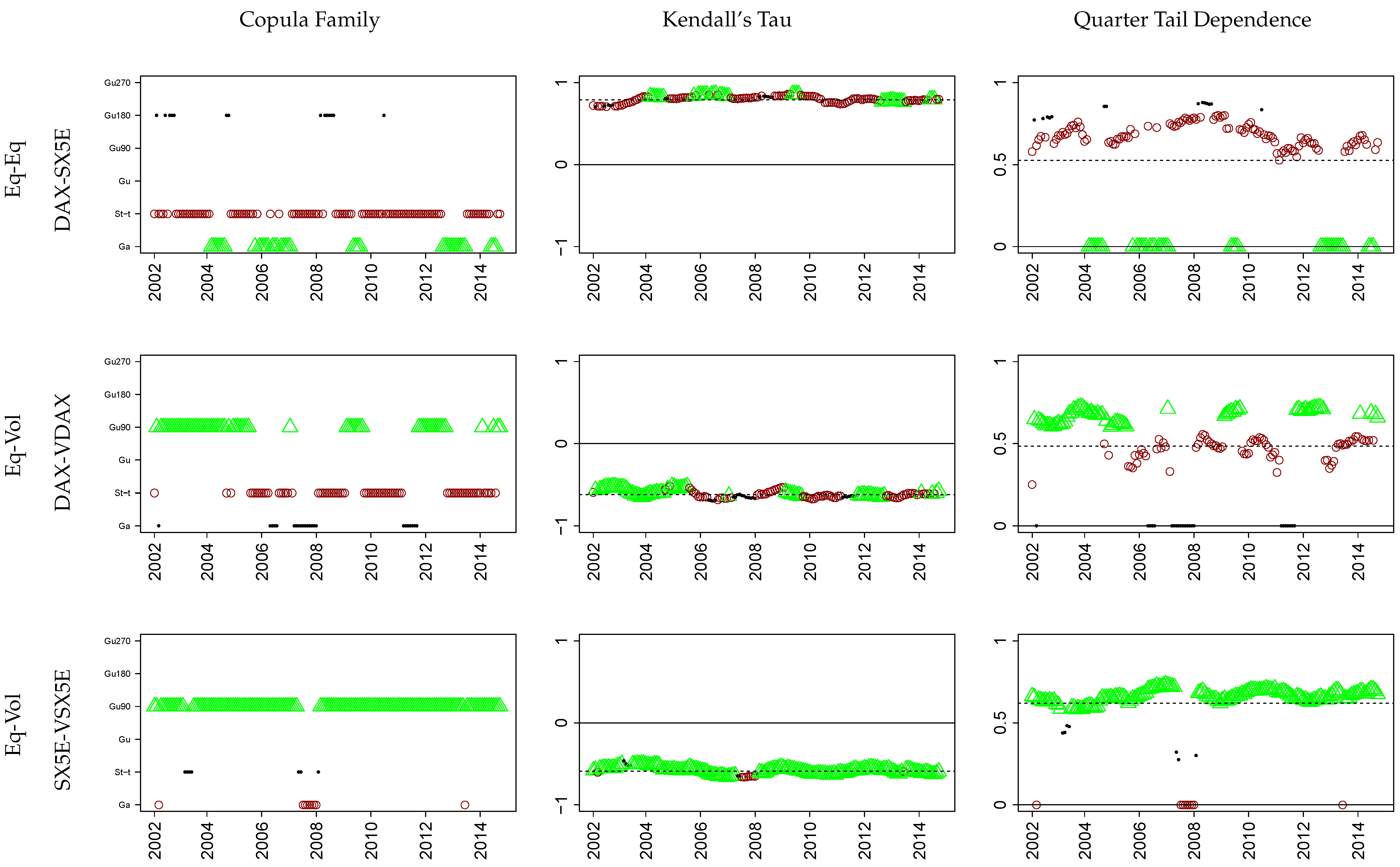

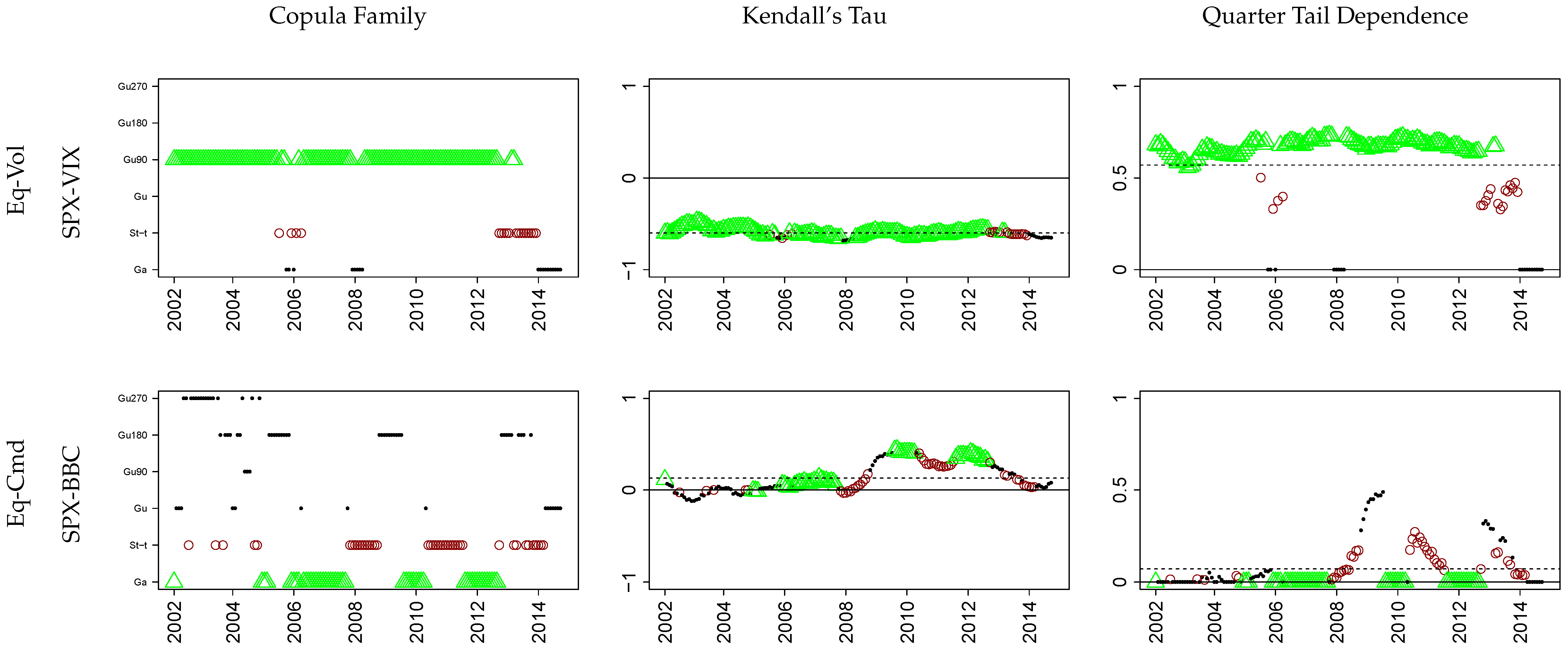

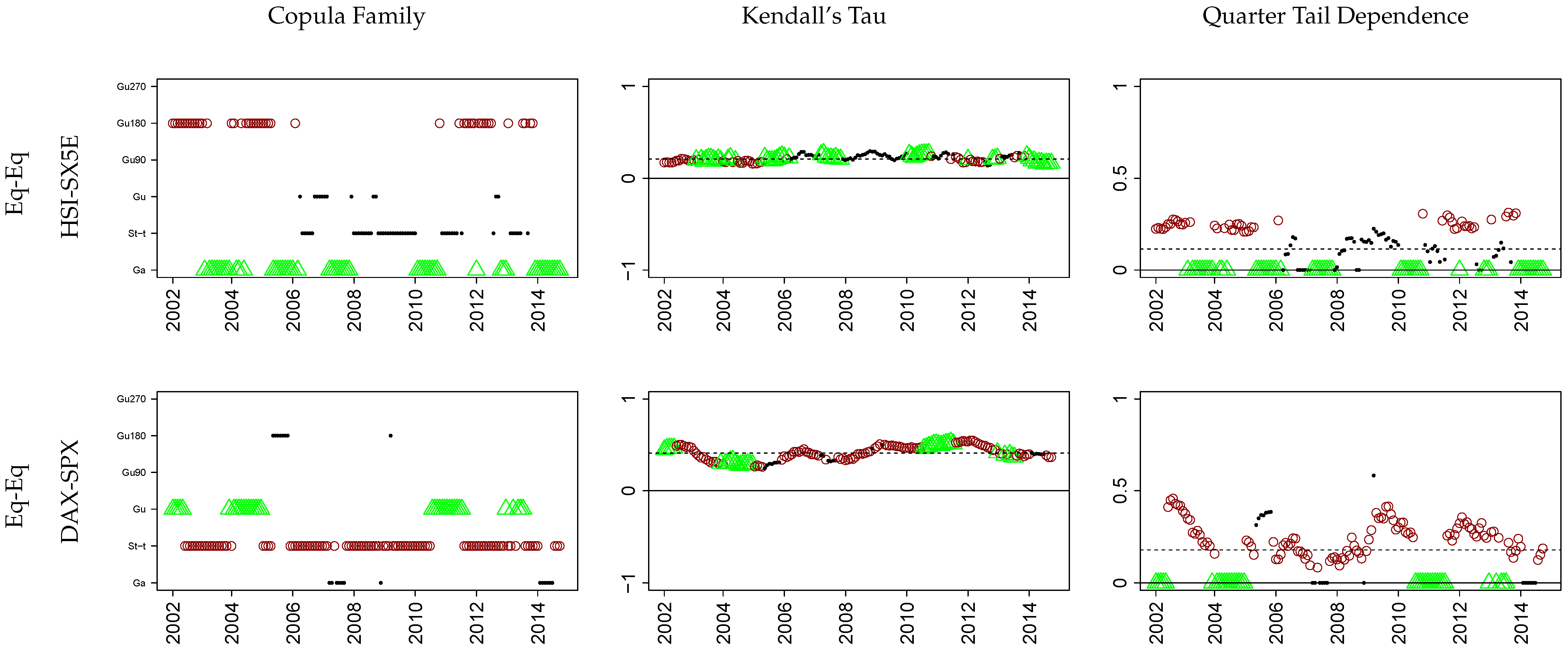

Appendix A. Model Summaries

The following section contains all estimated model specifications. To compactly summarize each setup, we follow the

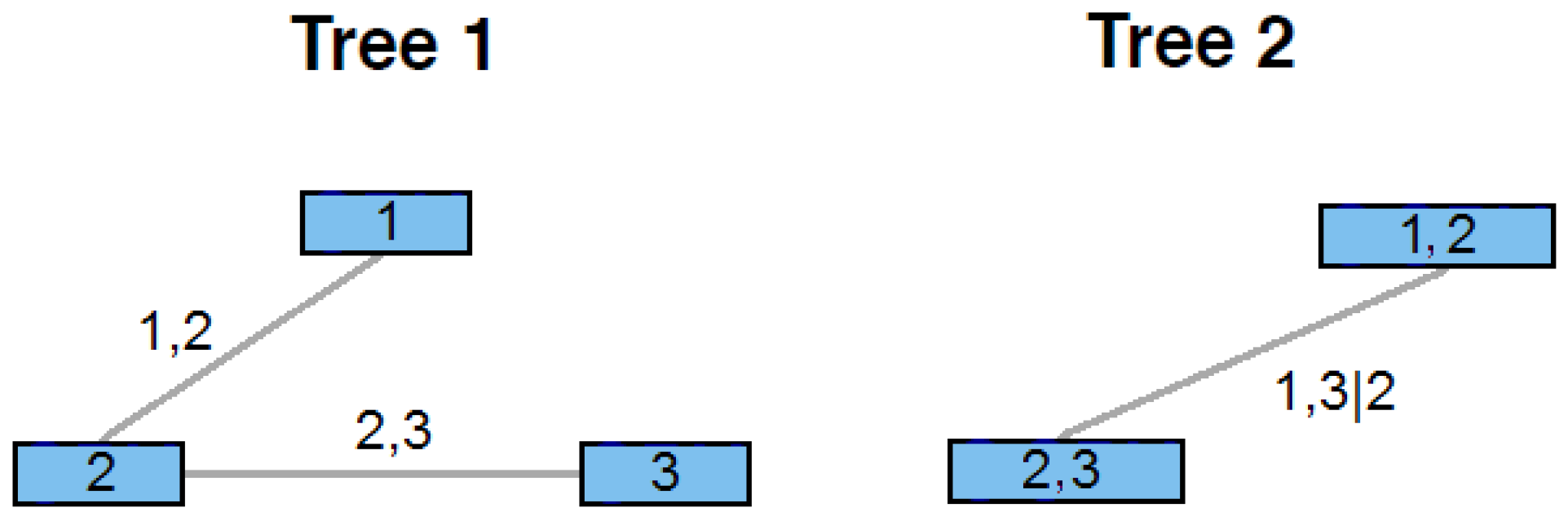

R-vine notation of [

68]: The

R-vine-matrix

stores the specific nodes and edges for each tree (cf. Equation (

4) and Figure 2 of [

68]) while the copula-family-matrix

contains the respective bivariate copula types using the abbreviations of [

40] (i.e., ‘1 = Ga’, ‘2 = St-

t’, ‘4=Gu’, ‘14 = Gu180’, ‘24 = Gu90’ and ‘34 = Gu270’). Finally, the copula parameters are presented via

(and additionally

for the degrees of freedom in the Student-

t case) while the switching probabilities are denoted by

P.

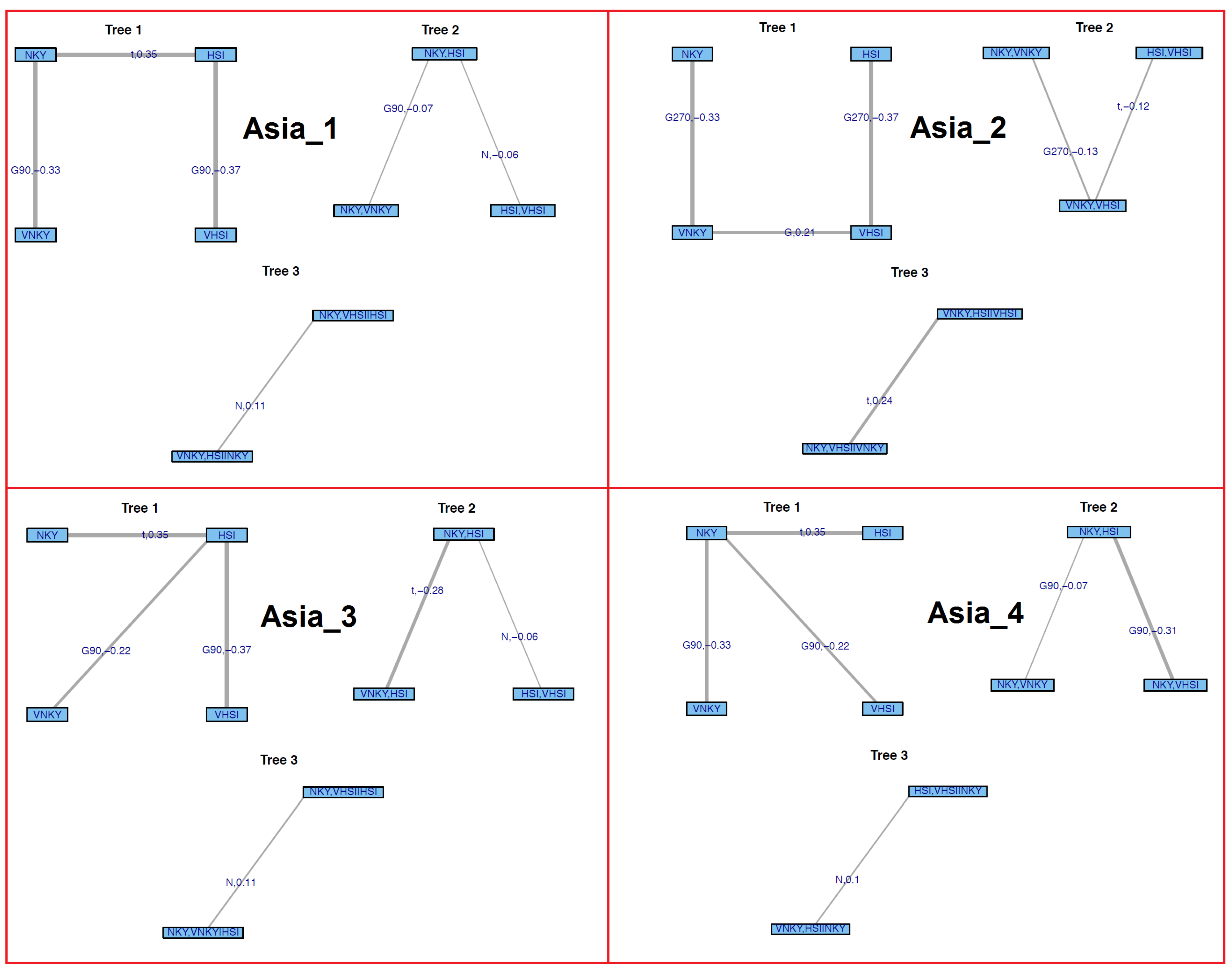

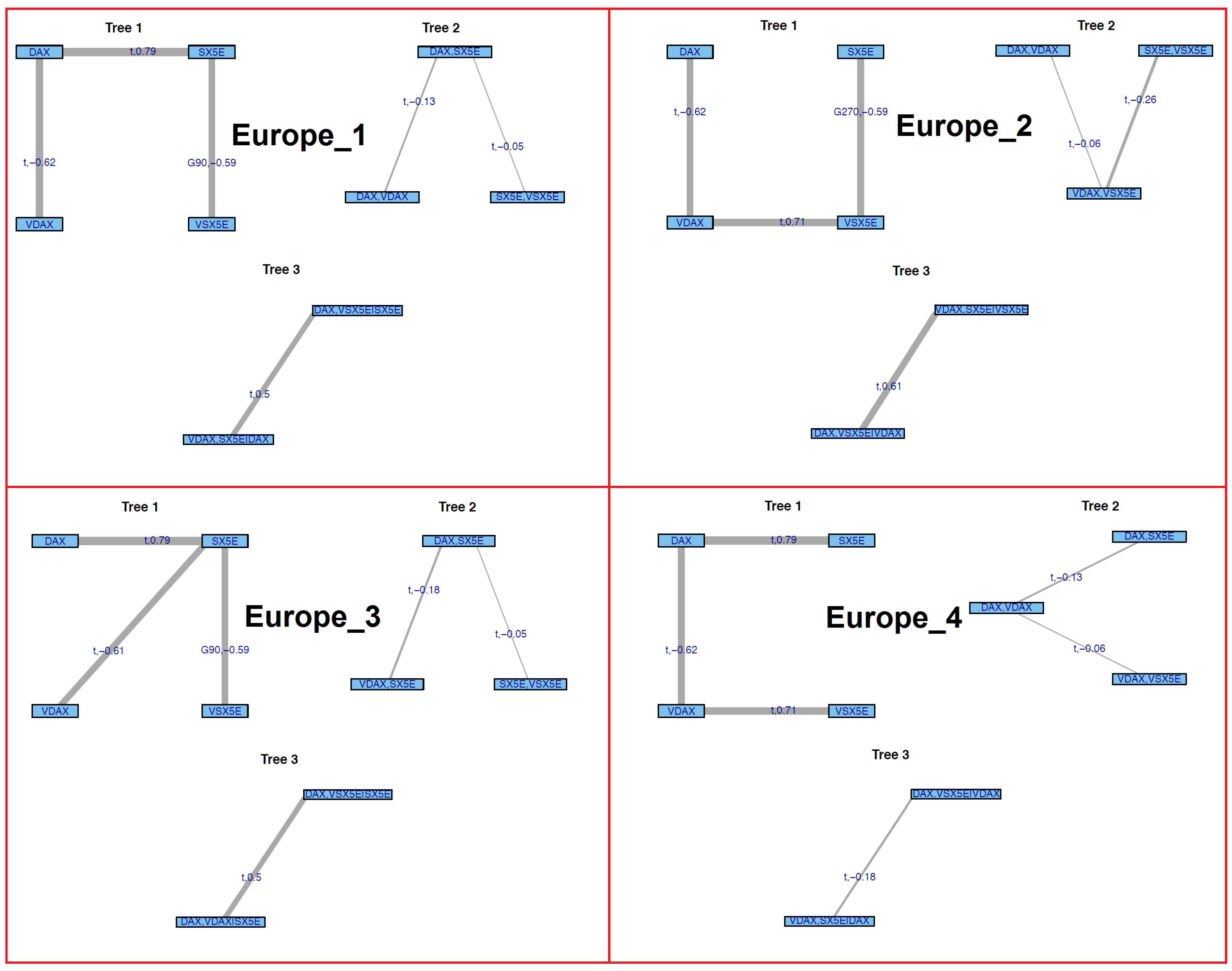

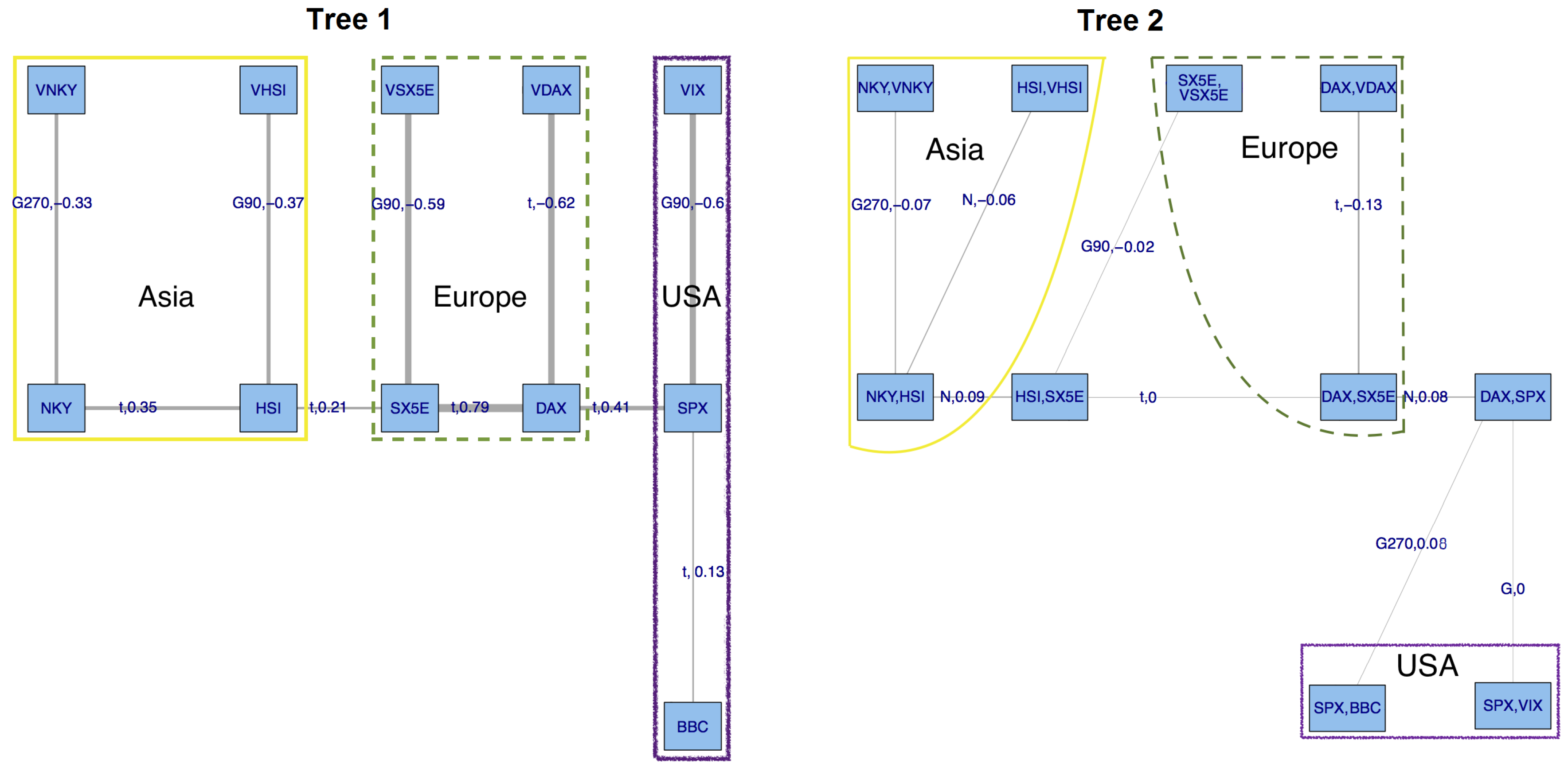

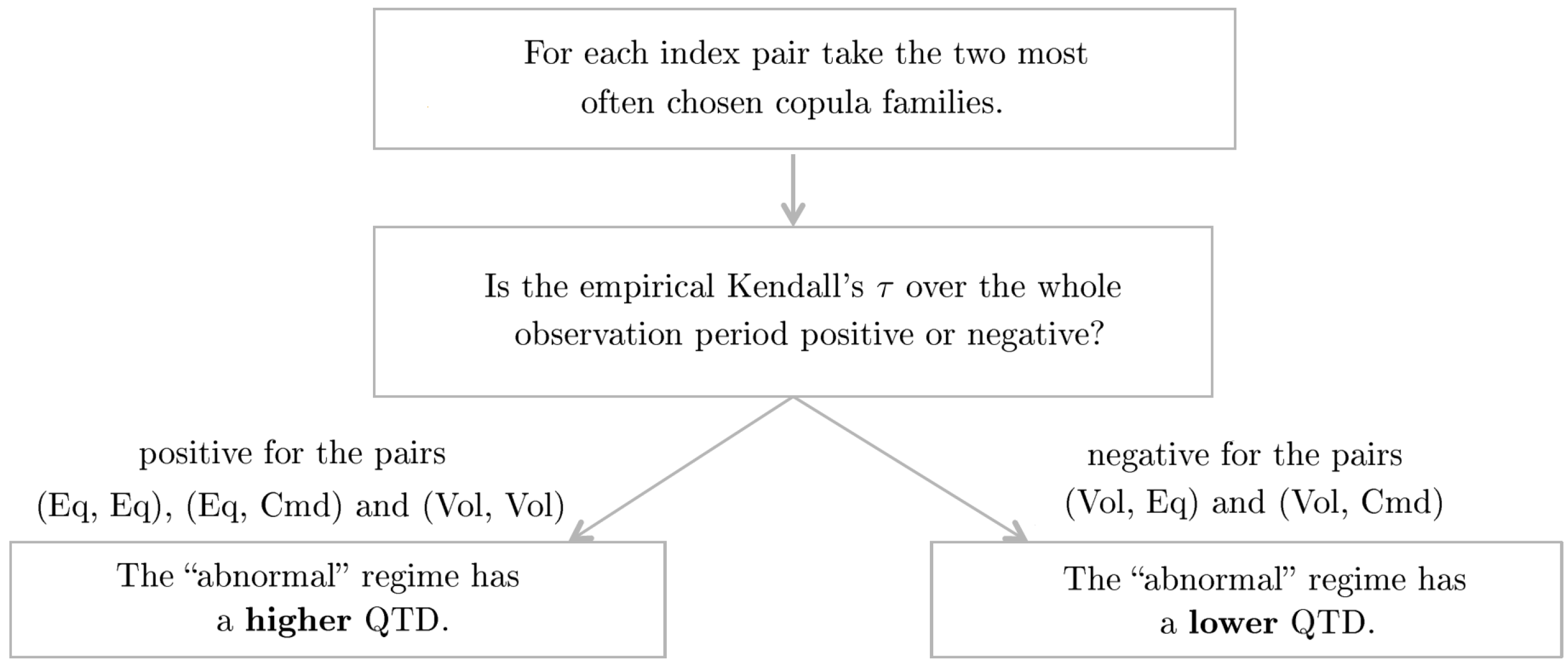

We want to stress that (1-dependent) is the only setup where a selection algorithm determined the

R-Vine structure

and the bivariate copula families

. For the non-switching regional models (Asia

–Asia

, Europe

–Europe

and USA

–USA

) as well as (2-dependent) the structure was manually chosen and only the copulas

were algorithmically selected based on maximum likelihood and AIC (cf.

RVineCopSelect out of the

VineCopula package by [

40]). For the Markov-switching setups (Asia

, Europa

, USA

and (3-dependent-MS))

and

for both regimes were manually determined. Parameters were always estimated and never fixed.

All “independence” model log-likelihoods were obtained via the sum of the regional setups.

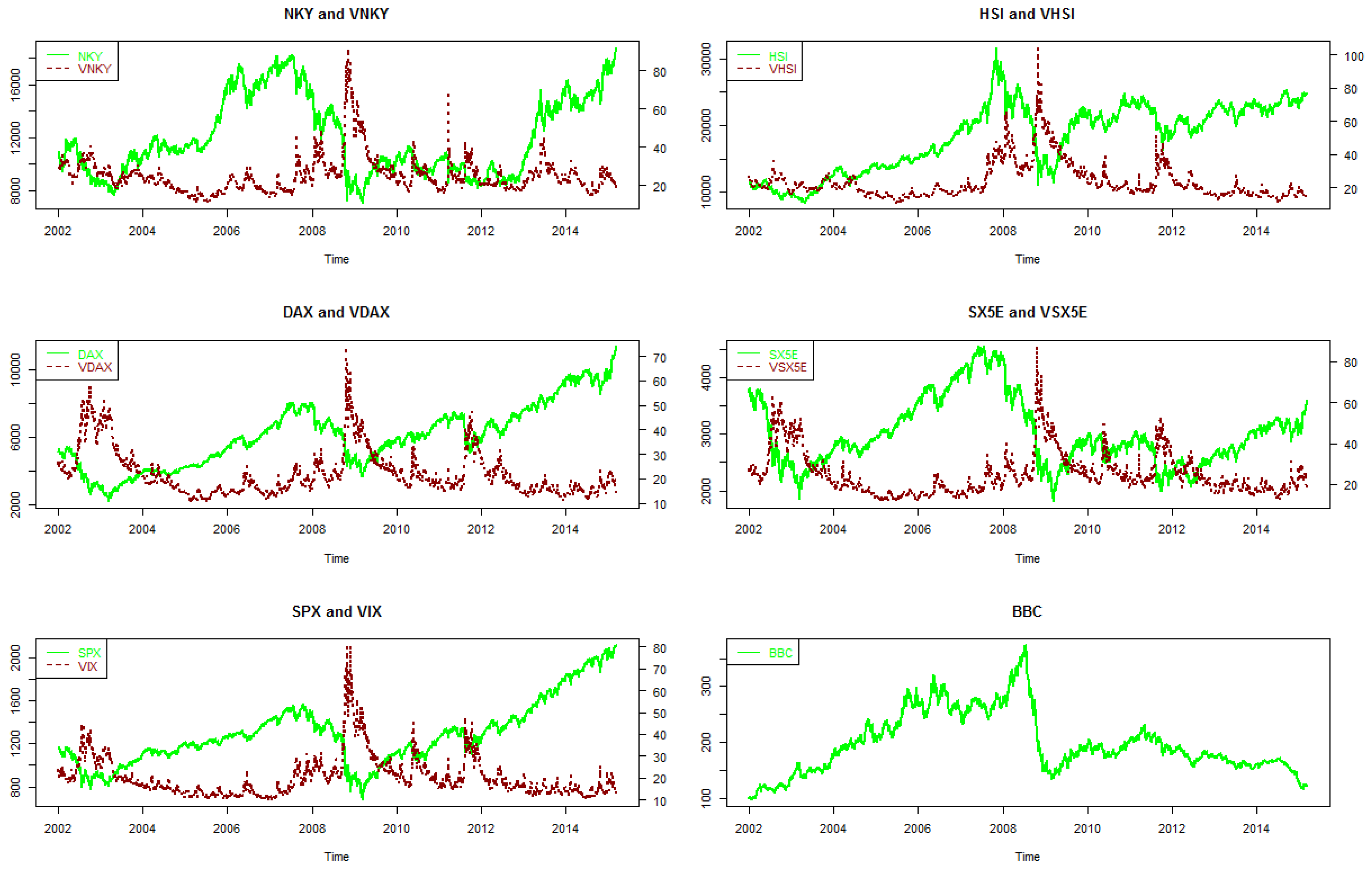

(1-dependent): 1-NKY 2-VNKY 3-HSI 4-VHSI 5-DAX 6-VDAX 7-SX5E 8-VSX5E 9-SPX 10-VIX 11-BBC

(2-dependent): 1-NKY 2-VNKY 3-HSI 4-VHSI 5-DAX 6-VDAX 7-SX5E 8-VSX5E 9-SPX 10-VIX 11-BBC

Asia: 1-NKY 2-VNKY 3-HSI 4-VHSI

Asia: 1-NKY 2-VNKY 3-HSI 4-VHSI

Asia: 1-NKY 2-VNKY 3-HSI 4-VHSI

Asia: 1-NKY 2-VNKY 3-HSI 4-VHSI

Europe: 1-DAX 2-VDAX 3-SX5E 4-VSX5E

Europe: 1-DAX 2-VDAX 3-SX5E 4-VSX5E

Europe: 1-DAX 2-VDAX 3-SX5E 4-VSX5E

Europe: 1-DAX 2-VDAX 3-SX5E 4-VSX5E

USA: 1-SPX 2-VIX 3-BBC

USA: 1-SPX 2-VIX 3-BBC

Asia: 1-NKY 2-VNKY 3-HSI 4-VHSI

“normal” regime

“abnormal” regime

Europe: 1-DAX 2-VDAX 3-SX5E 4-VSX5E

“normal” regime

“abnormal” regime

USA: 1-SPX 2-VIX 3-BBC

“normal” regime

“abnormal” regime

(3-dependent-MS): 1-NKY 2-VNKY 3-HSI 4-VHSI 5-DAX 6-VDAX 7-SX5E 8-VSX5E 9-SPX 10-VIX 11-BBC

“normal” regime

“abnormal” regime

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}