4.1. Characterisation of the Relevance of CSR Practices Worldwide

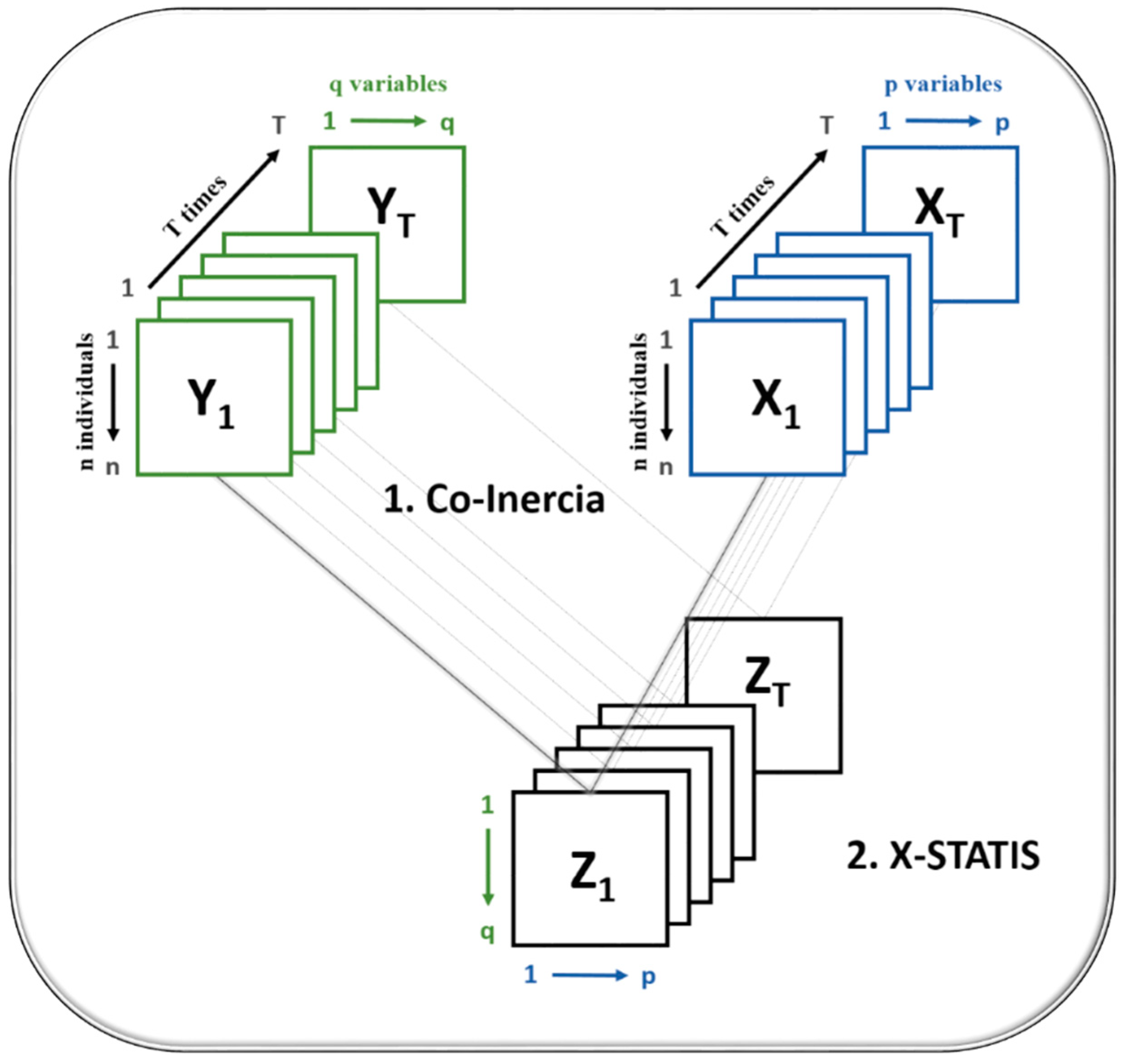

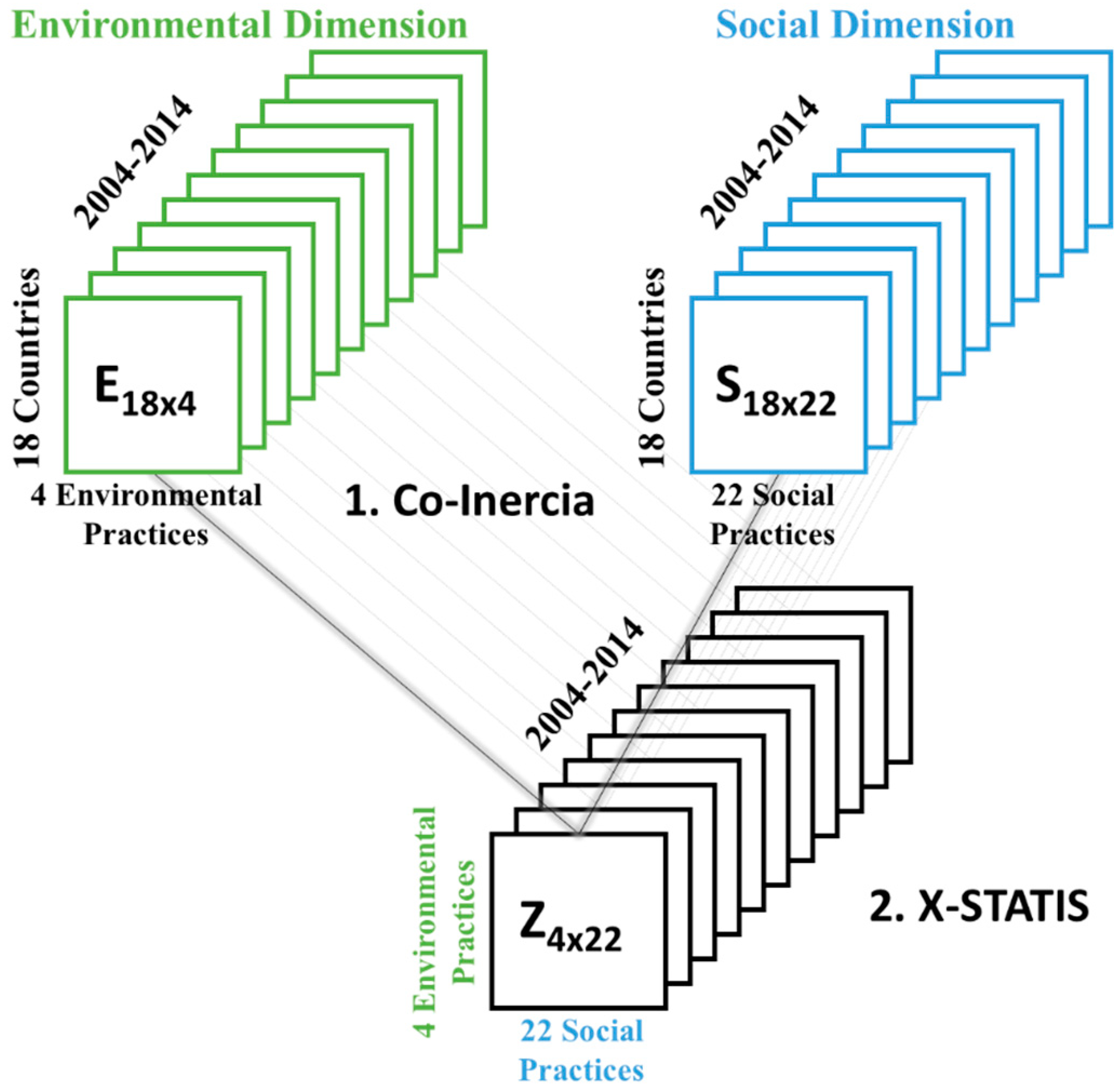

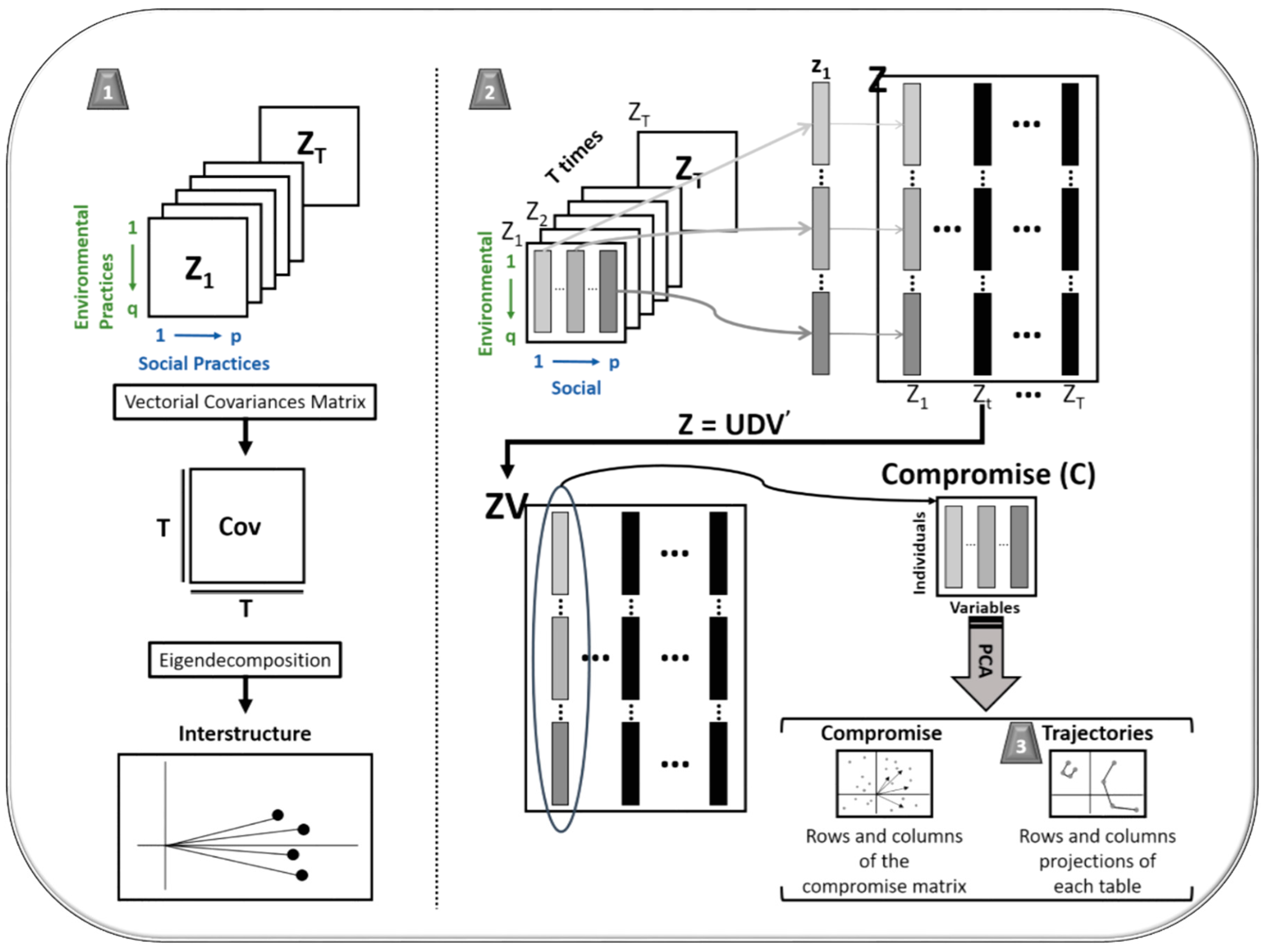

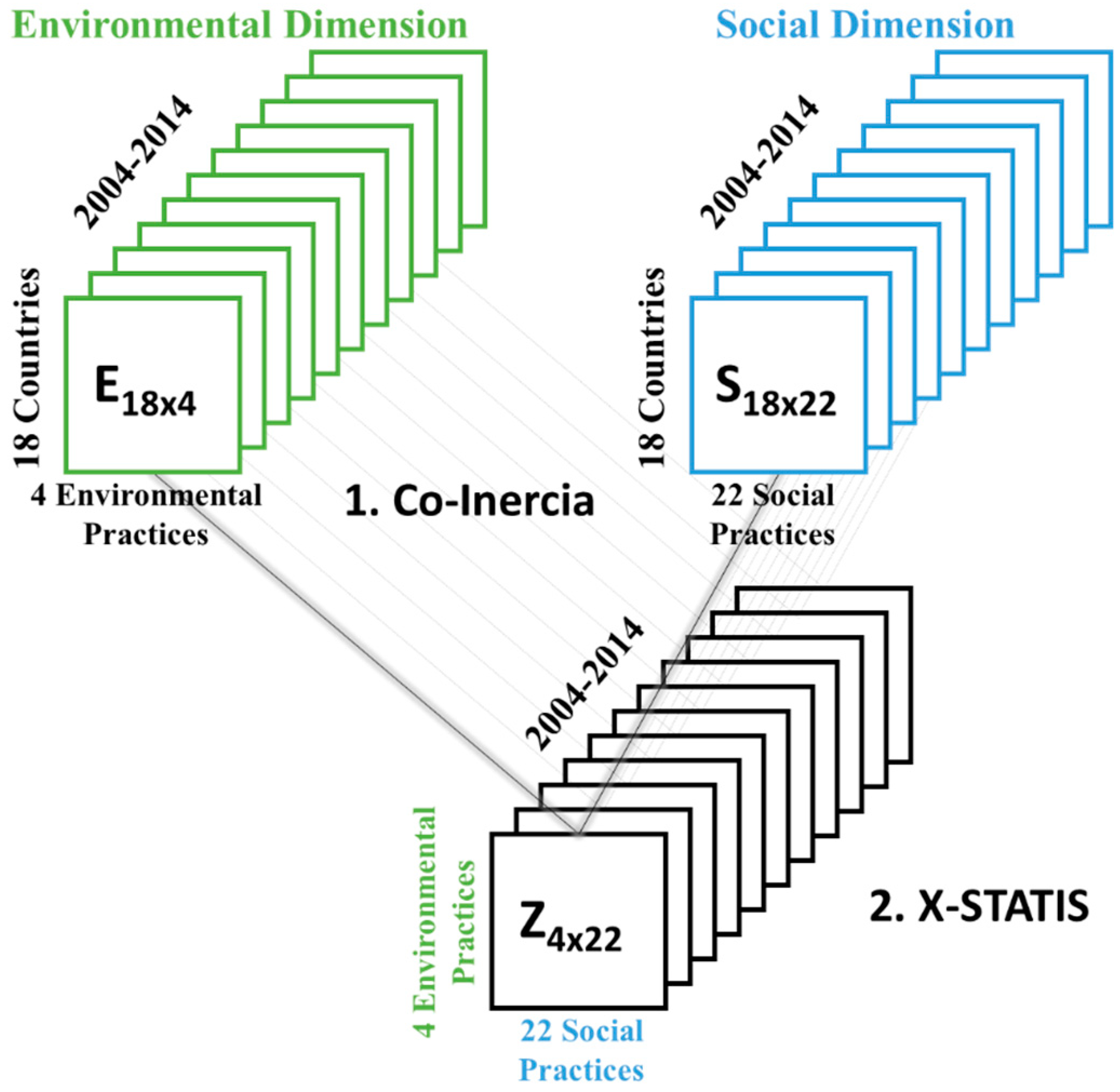

As a first step, through an X-STATICO analysis, we proceed to analyse the importance of the dimensions and sub-dimensions of the CSR considered, studying the similarities and differences that exist between each of the practices, taking into account their grouping in the established environmental and social dimensions. The data for this analysis are arranged in two cubes of 18 rows (the countries), with 11 repetitions (the years 2004–2014): a cube with four columns, corresponding to the environmental variables; and the other with 22 columns, indicating practices related to social welfare.

The first step of the X-STATICO analysis (

Figure 6) is the realisation of a co-inertia analysis between each pair of tables of both cubes. With this analysis, we seek to find the agreement established between the countries from the point of view of their environmental practices and from the point of view of their social practices, so that it provides us with a matrix for each year in which their rows will be the environmental variables and the social ones their columns, thus facilitating the vision of the most important relationships between each pair of tables. The second step consists of carrying out an X-STATIS analysis whose objective is to highlight the stable structure throughout this decade, that is, to find a ‘middle year’ to represent each of the practices and their relationships in this structure stable, and show how each of these moves away from said structure.

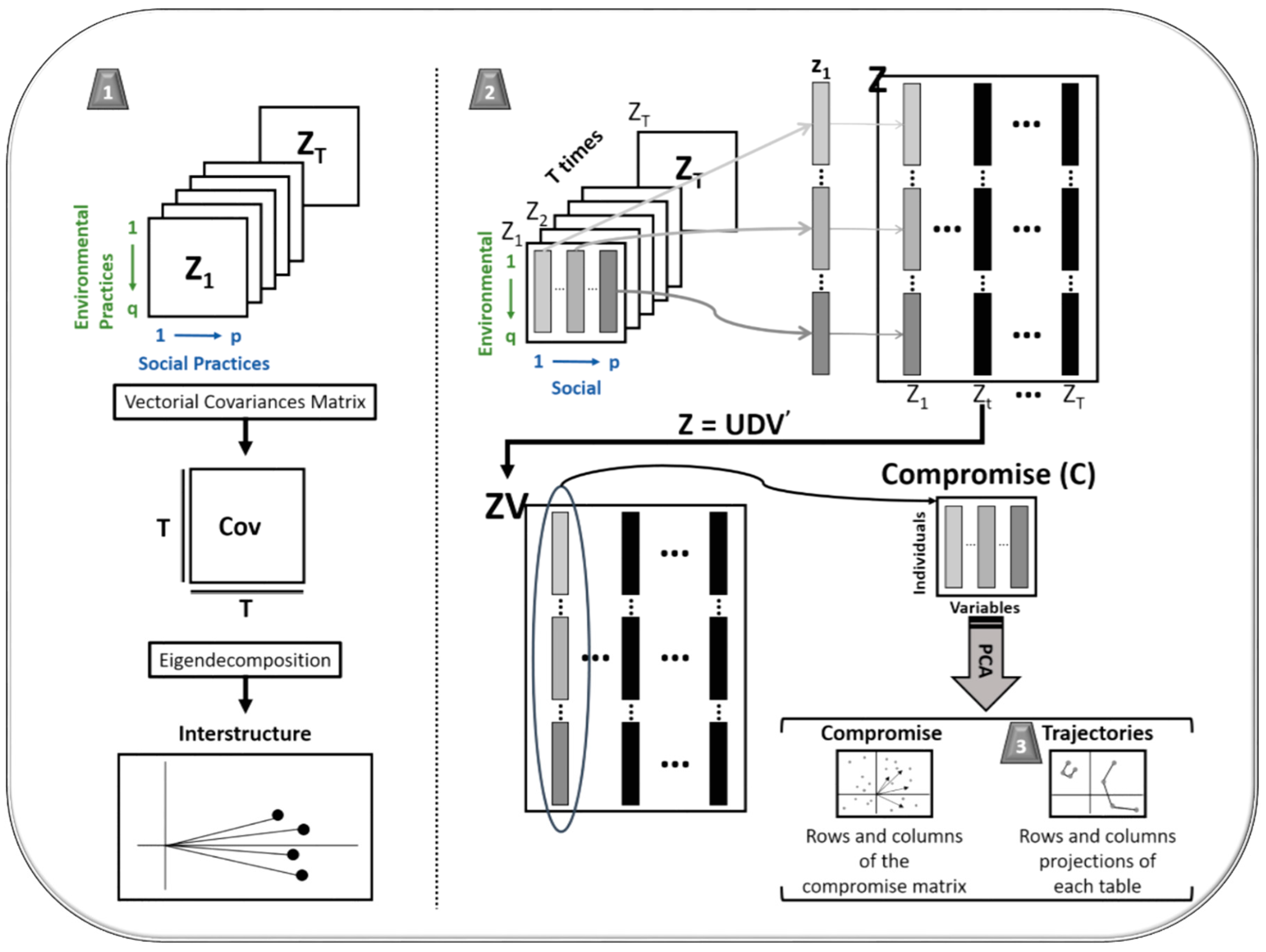

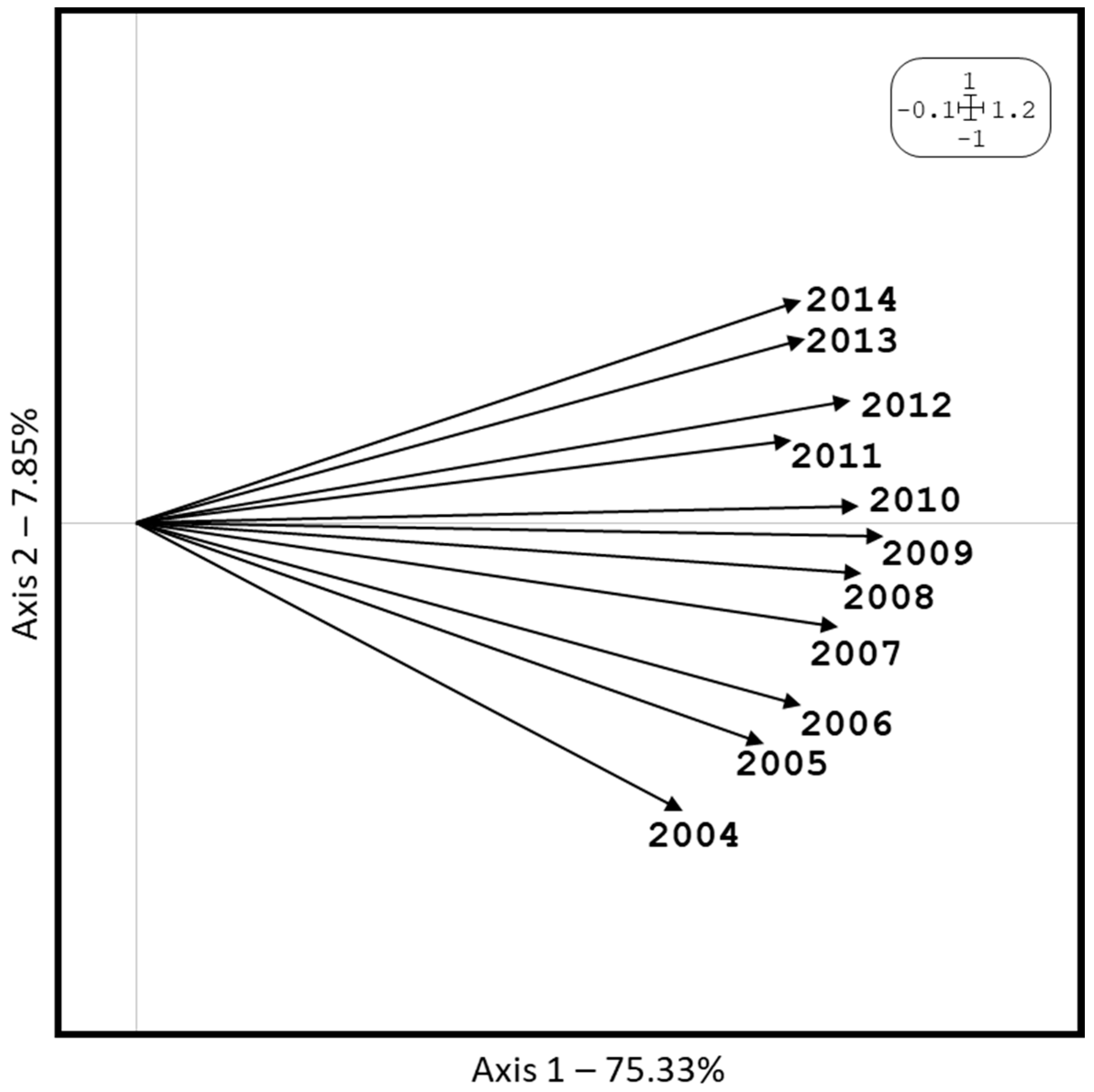

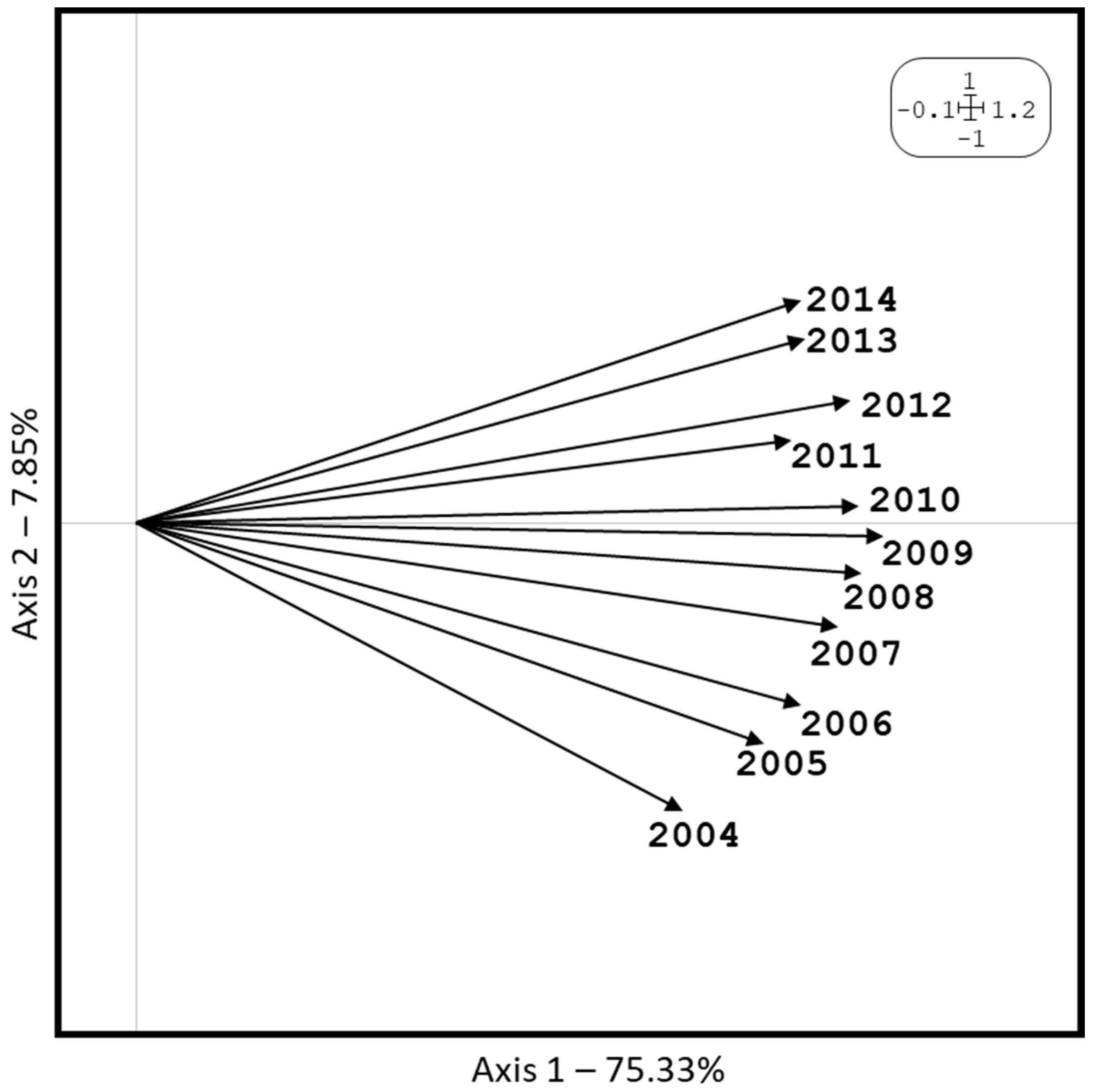

The first result that this method provides us is an interstructure study of the X-STATIS analysis after performing the co-inertia analysis, which allows us to reduce the dimensionality and represent the information in an Euclidean subspace of low dimension, in which each year (data table) is represented as a point, and joining these points to coordinates’ origin, we can visualise an estimate of said similarity in terms of the angles between vectors, associating acute angles with strong similarities (see

Figure 7). This representation includes 83.18% of the total variability, and allows the interpretation of the similarities and differences between the years of study. This representation also indicates which of these acquire greater importance in the construction of the so-called compromise matrix, that is, those years that look more like an ‘average year’, which will highlight the stable part of the evolution of the data over time.

Acute angles between vectors can be observed, that is, strong similarities between years, produced in a gradual way, since the first year of the study, 2004, is located in the lower part of the figure, and as the years increase, they increase their position until they reach 2014, which occupies the highest position. Therefore, we intuit a constant growth in the commitment of company sustainability in this decade of study. Also, the ‘average year’, which was most similar to the stable configuration, is seen for the years 2009 and 2010, which were those closest to the abscissa axis. They were also the intermediate years of the study, since as we said, the relations are produced in a gradual way.

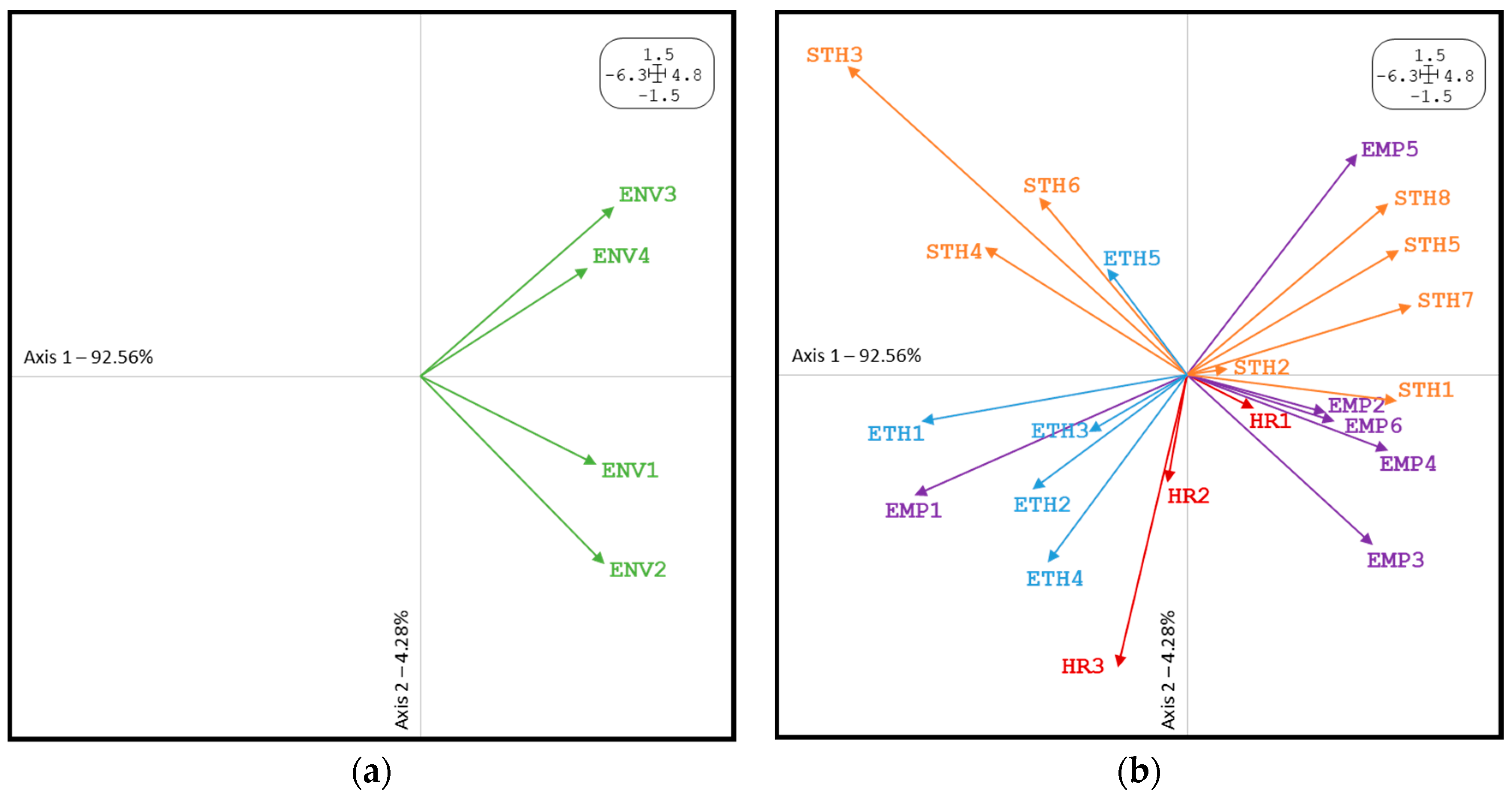

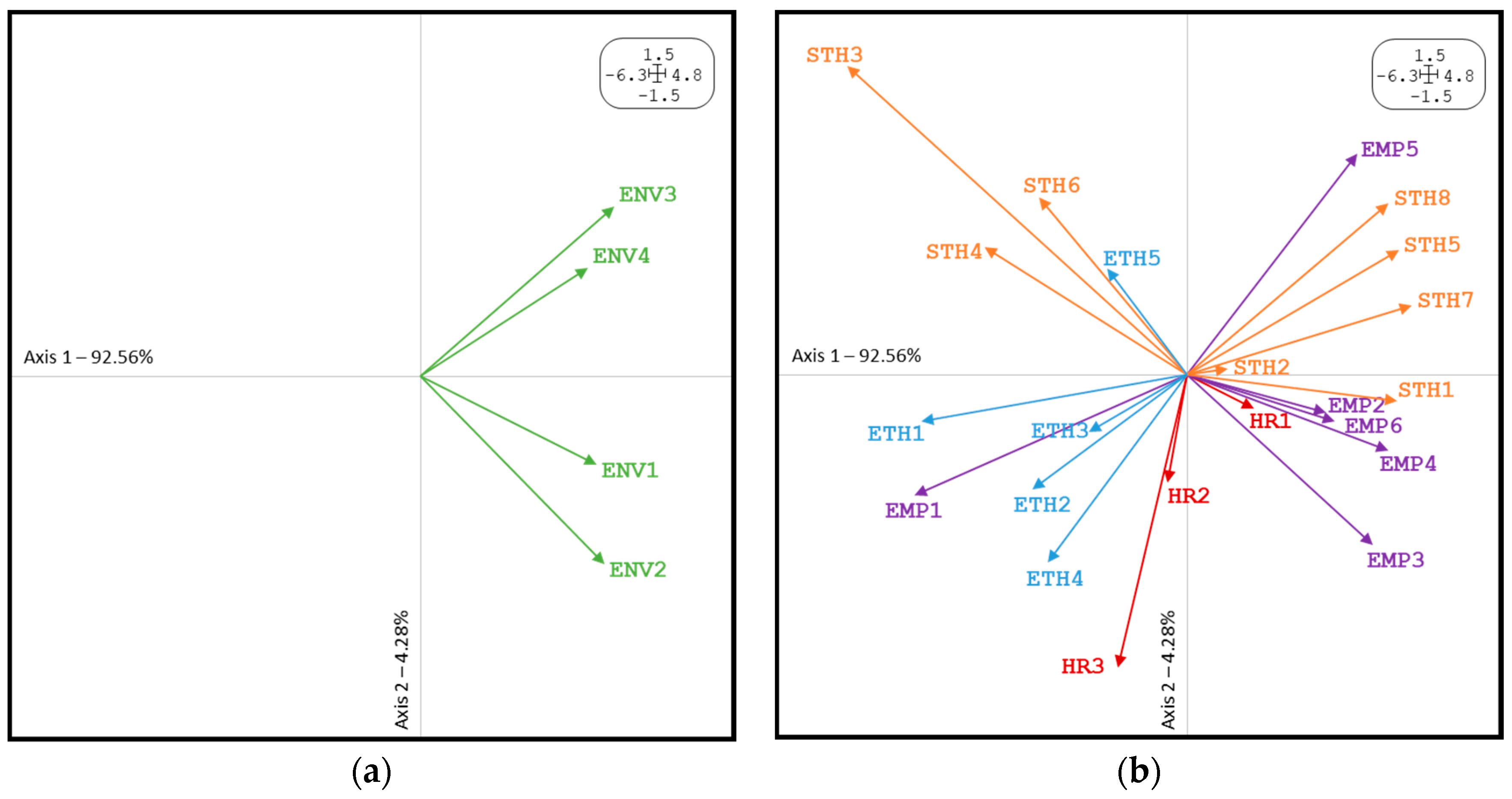

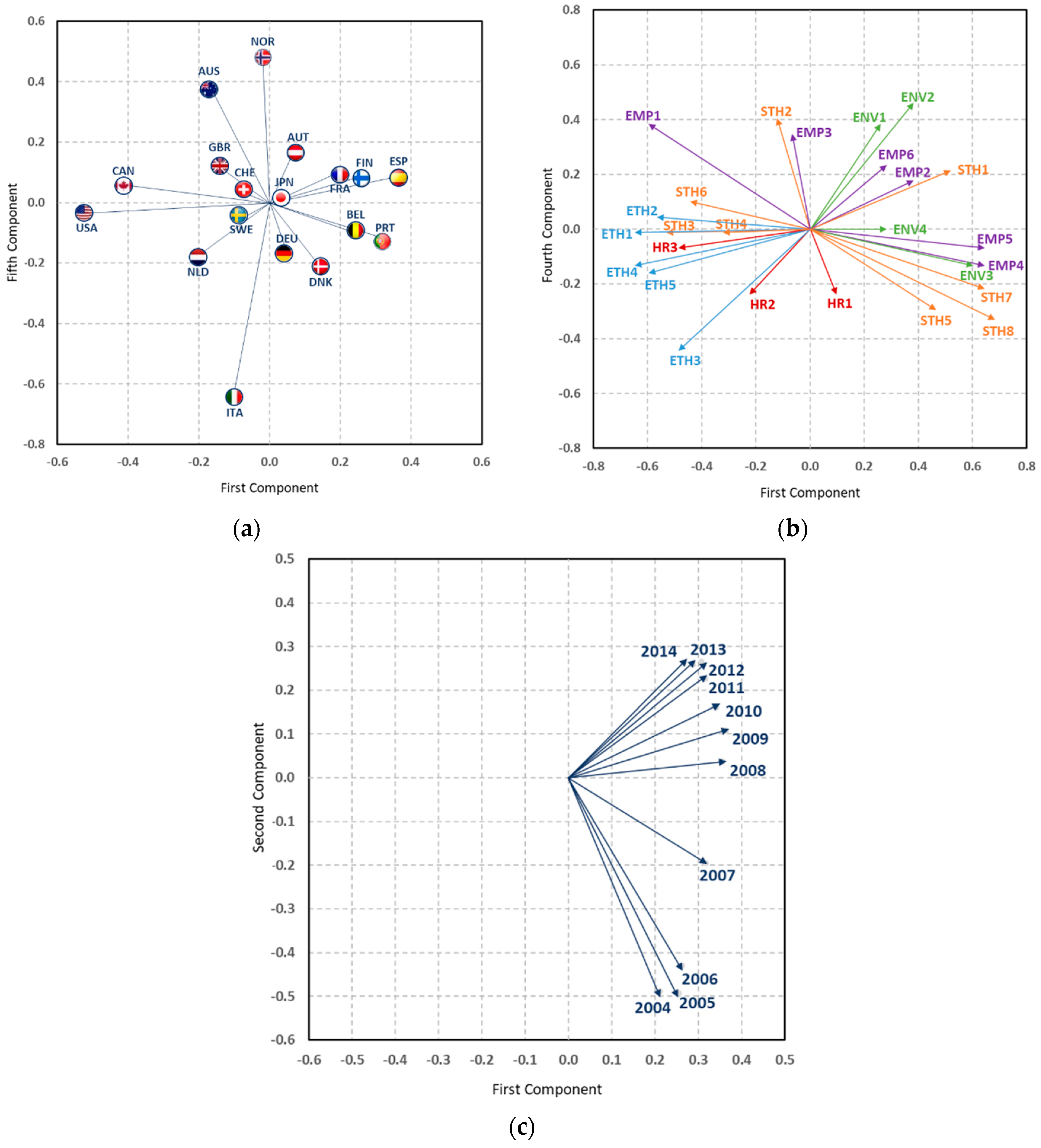

The next step is the attainment of the compromise matrix, which summarises all of the information provided by each of the configurations, since this matrix is a global summary of all of the tables. Therefore, in the subspace created by this matrix, the relationships between environmental and social variables can be interpreted according to how all of the countries behave in them. This representation (

Figure 8) collects 97% of the information, and in it, two figures can be visualised. The first, which is located on the left, corresponds to the environmental variables, which are identified as green, and the second is located on the right, and refers to the variables of social type, distinguished by colours according to their sub-dimensions. Thus, the red vectors refer to human rights, purple correspond to employees, orange are in relation to stakeholders, and blue are those referring to business ethics.

In relation to environmental practices, all of them are located in the right semi-plane (quadrants I and IV); with this information, we understand that the countries with the most sustainable companies would be positioned on the right side next to these variables, since it would be difficult to conceive that a country denominated as sustainable presented low values in environmental practices. In reference to social practices relevance, it is argued that those countries with strong demands for environmental practices give similar importance to practices aimed at the participation of both employees (EMP4) and stakeholders (STH5) in the decision making of the company; to the health and safety of these (EMP3), equal opportunities systems (EMP2), as well as training (EMP5) and job creation (EMP6); systems for the good management of stakeholders (STH7) to maintain good relations with the community (STH1), and information disclosure (STH8); all of them located in the right semi-plane (quadrants I and IV) and maintain a direct relationship with environmental variables. The rest of the variables have an inverse relationship with the environmental ones, such as equal opportunities policies (EMP1) or policies on stakeholders (STH6), and those related to human rights and ethics receive less importance.

In general terms, companies from all over the world give greater importance to their environmental levels, their relationships with their stakeholders, and the labour rights of their employees. This is because companies strive to achieve global consistency in their CSR profile, combined with the need to meet the demands of local stakeholders and trust with their employees, in order to achieve a proactive image of good prestige and social reputation and therefore, the economic advantages associated with this commitment.

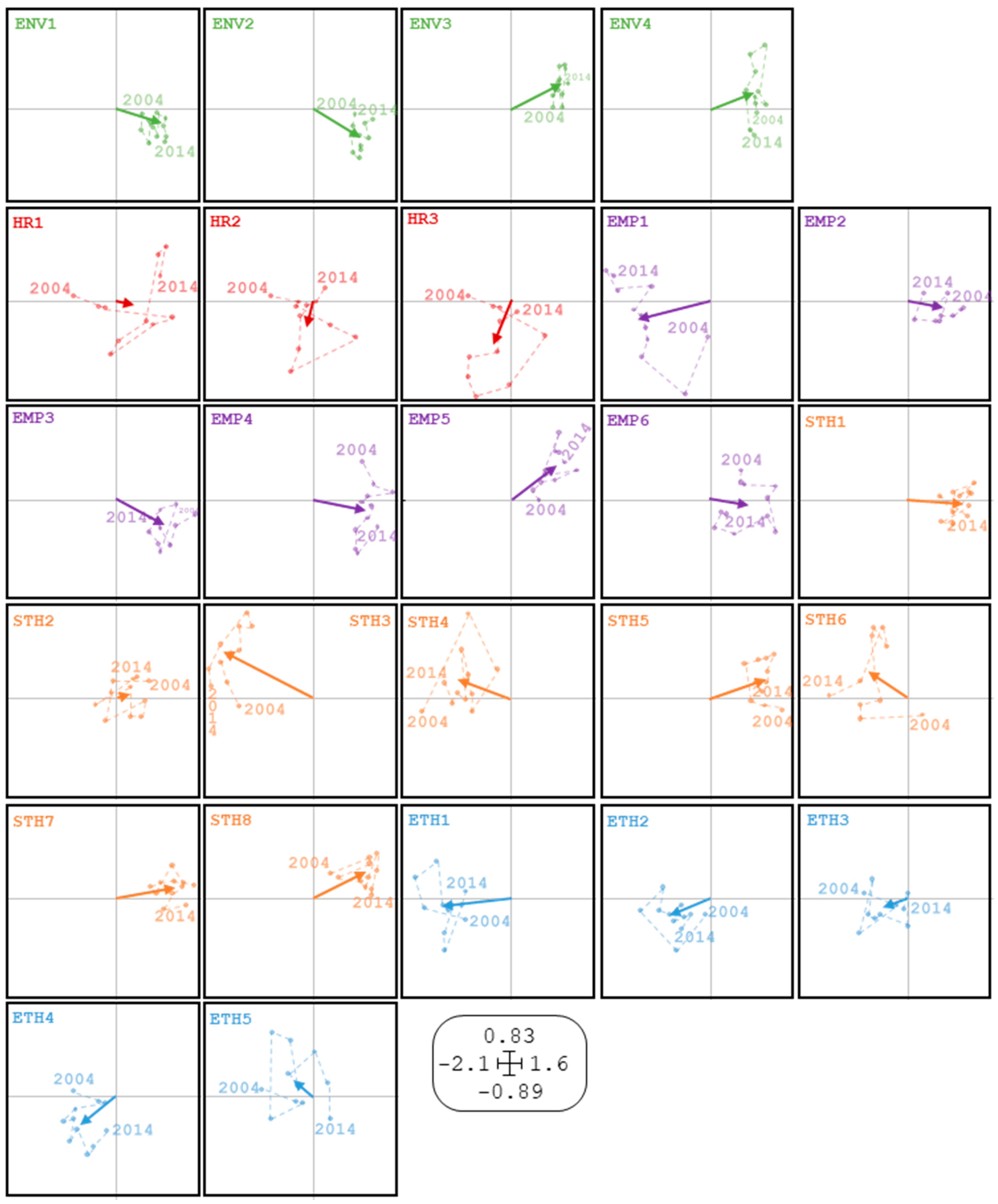

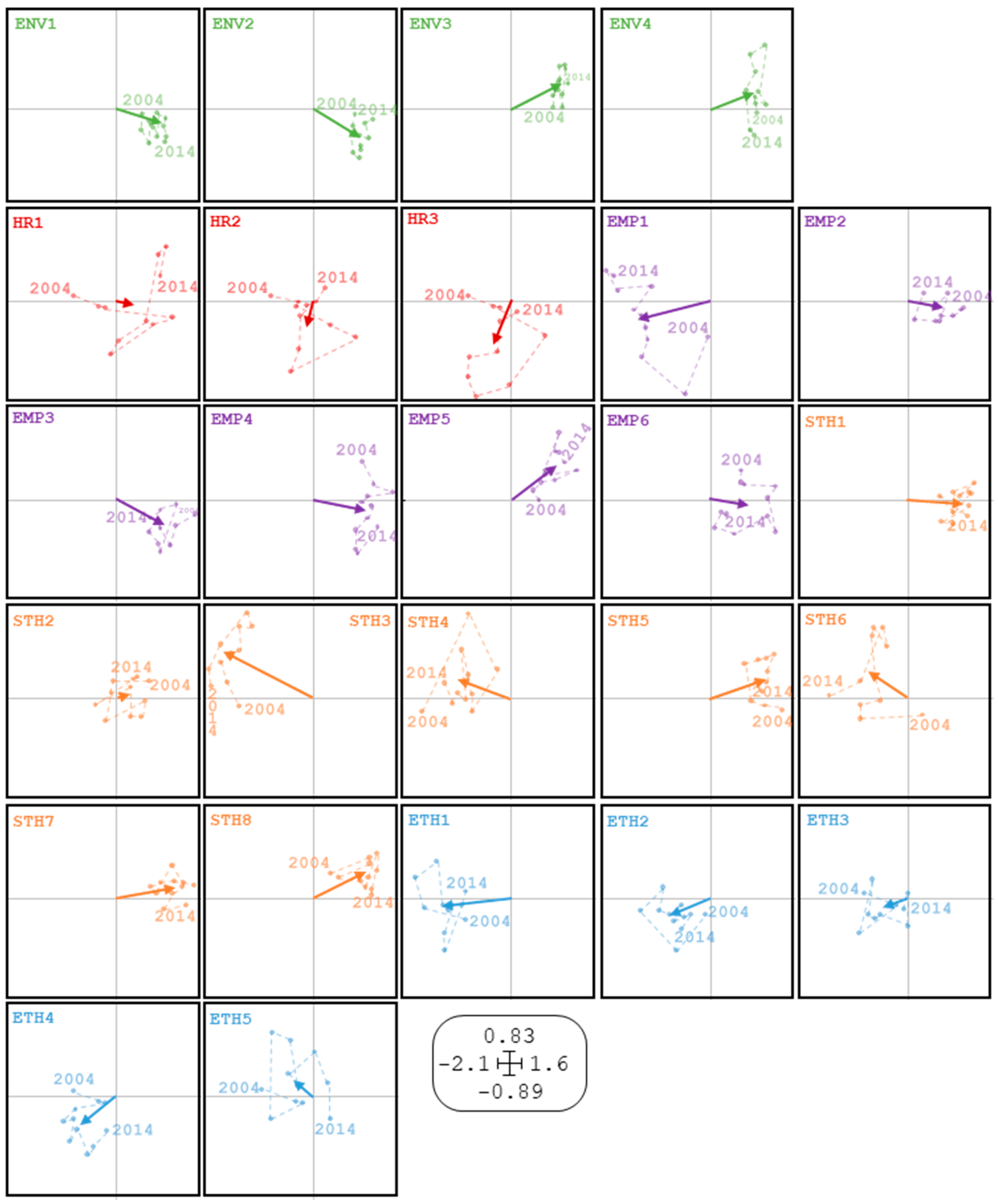

The third and last step of this analysis includes the intrastructure study, also known as trajectories, which allows us to interpret, by the projection of each one of the rows (environmental variables) and columns (social variables) of each of the starting tables (years) about the compromise subspace created, how these relationships vary over time. This representation (

Figure 9) has been separated for each of the variables in order to obtain an individualised view; the vector represents the commitment position of each variable and the union of the points the trajectory from the first year of study (2004) to the last (2014). It can be observed that social practices that have a direct relationship with the environment, that is, those positioned in the right semi-plane (quadrants I and IV), show greater stability, with homogeneous locations occupying a similar position in the plane during this decade; this may be because these practices respond to the expectations of the stakeholders that are a very important part of the company and provide great reliability on the rights of their employees, creating an image of a responsible and concerned company on their part, internally as well as externally, workers, stakeholders, consumers, etc. Apparently, these practices have forged a place next to the environmental ones, acquiring an importance close to these, so that both consumers and any other interest group of the company no longer simply demand the protection of the environment, but also the development of systems oriented to labour rights and dealing with different stakeholders that arise from the employee relationships, transparent dialogue, and participation with stakeholders.

We find the opposite situation in the rest of variables, those located in the left semi-plane (quadrants II and III), which extend over a large part of the plane, presenting great instability during these years, which explains why these practices are not the main requirement of both internal and external groups of companies. Given the possibility that they are not entrenched in some countries, in general, these variables refer to business ethics and acquire less importance than the rest. However, they will certainly have a place in certain companies, a priori; it is to be assumed in less polluting companies, given the inverse relationship with environmental practices.

4.2. Characterisation of the Relevance of CSR Practices According to the Country of Origin

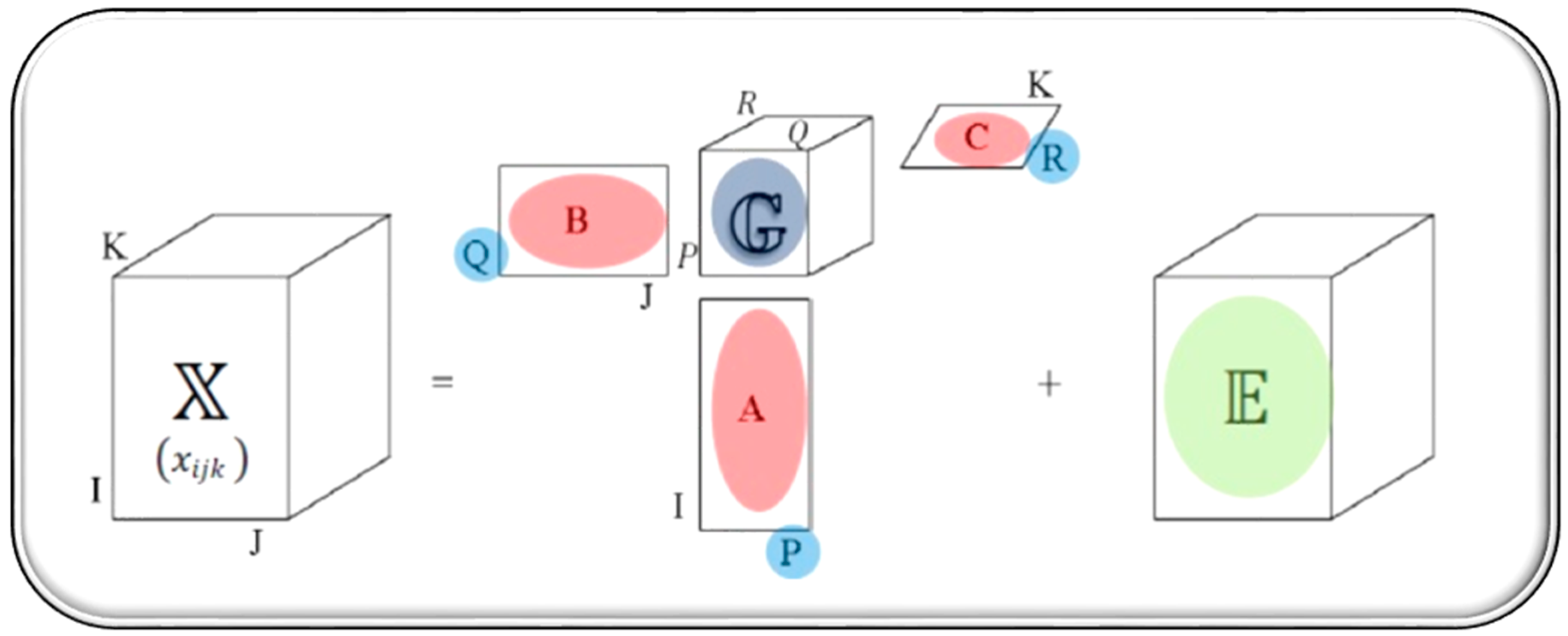

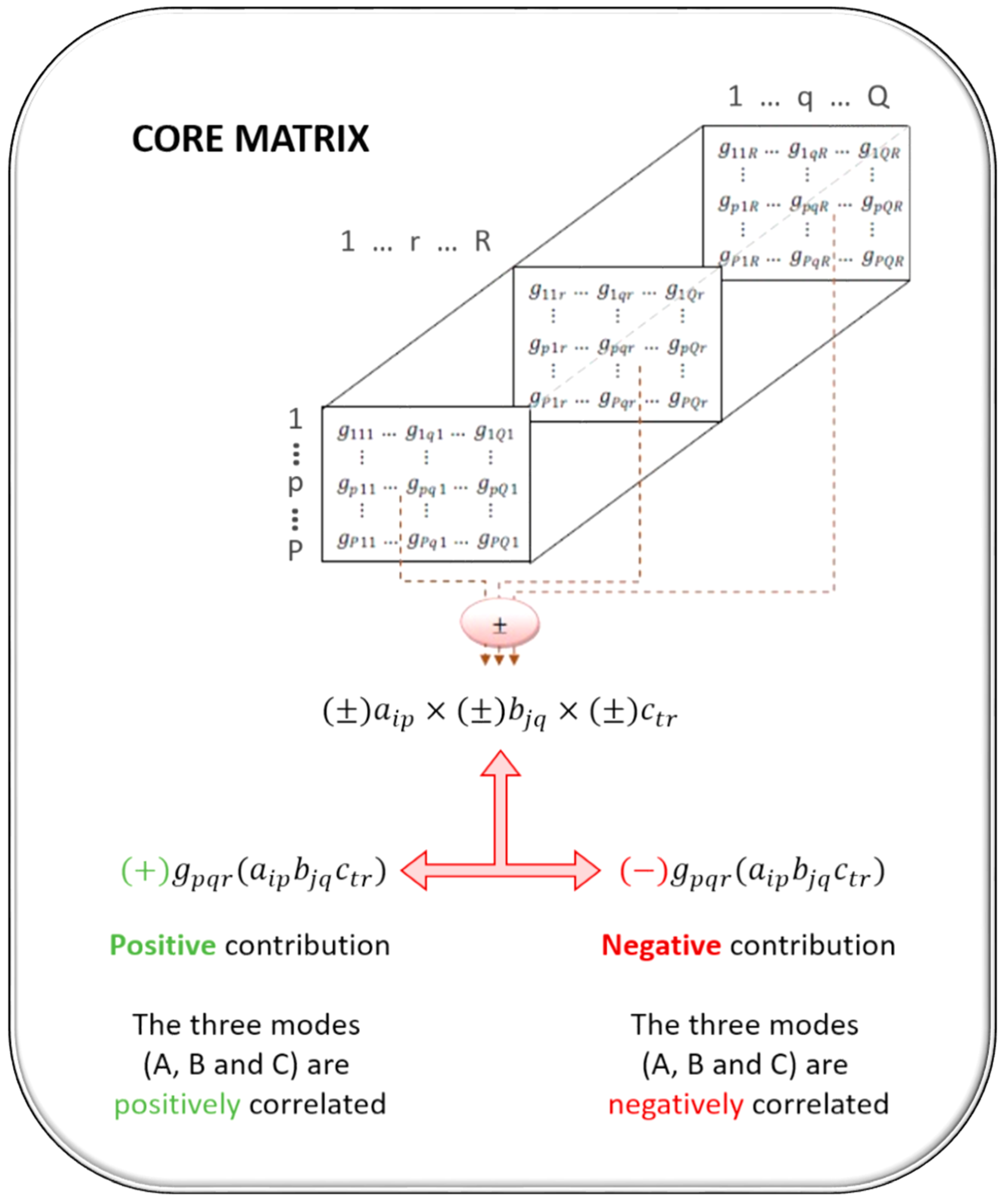

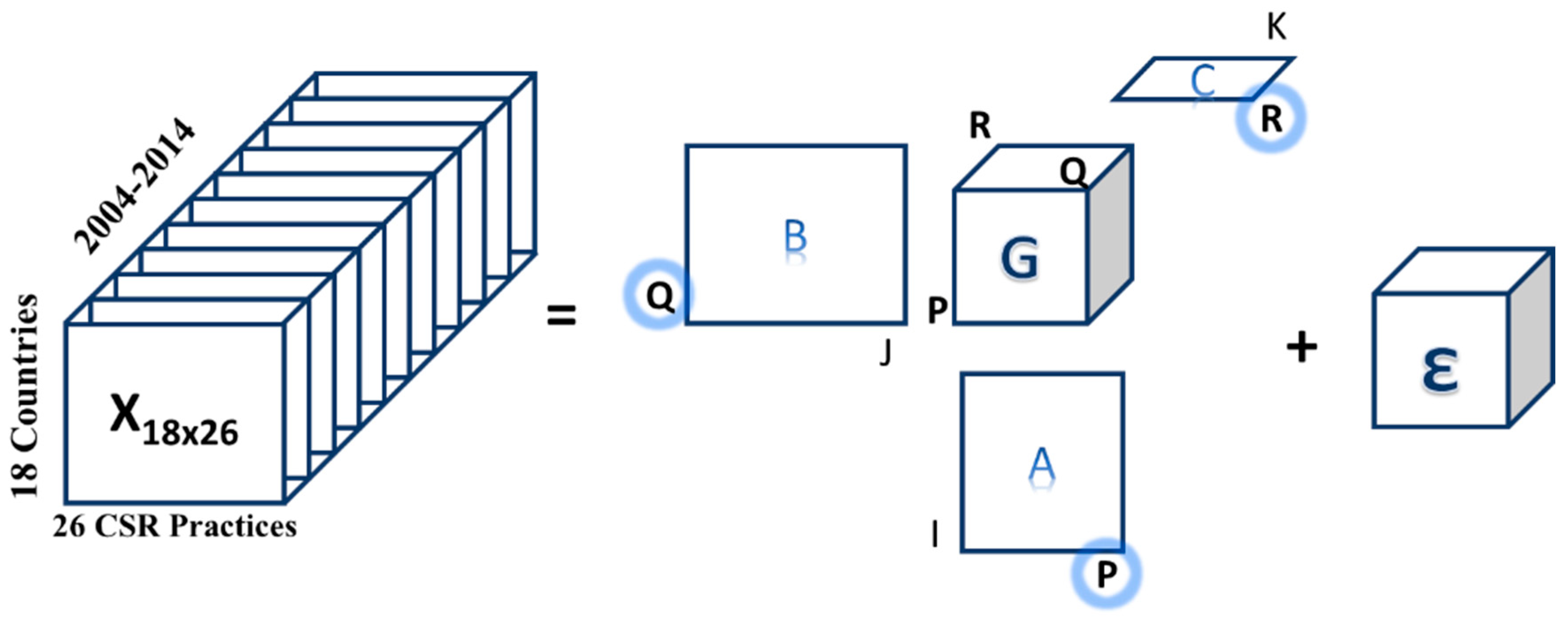

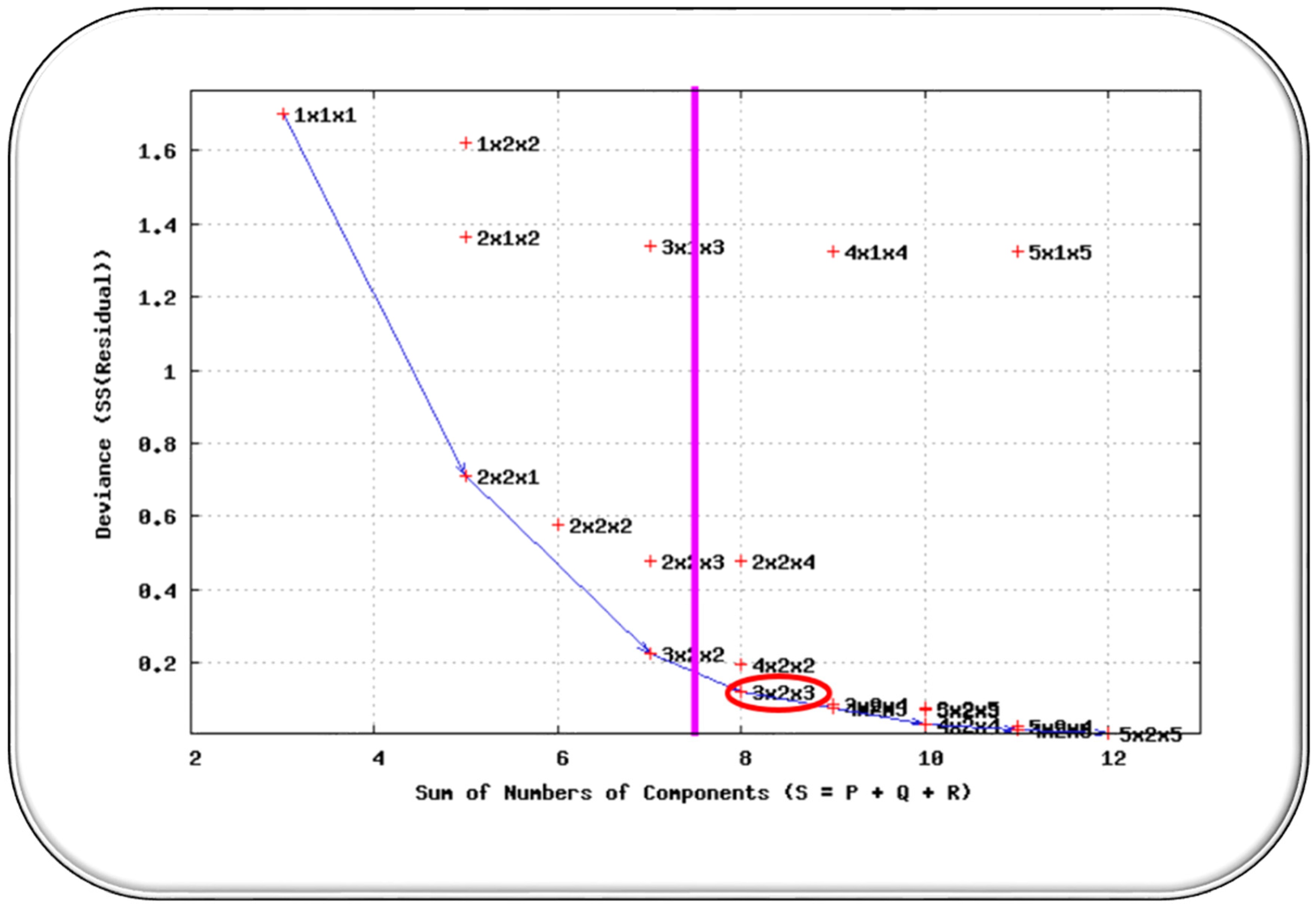

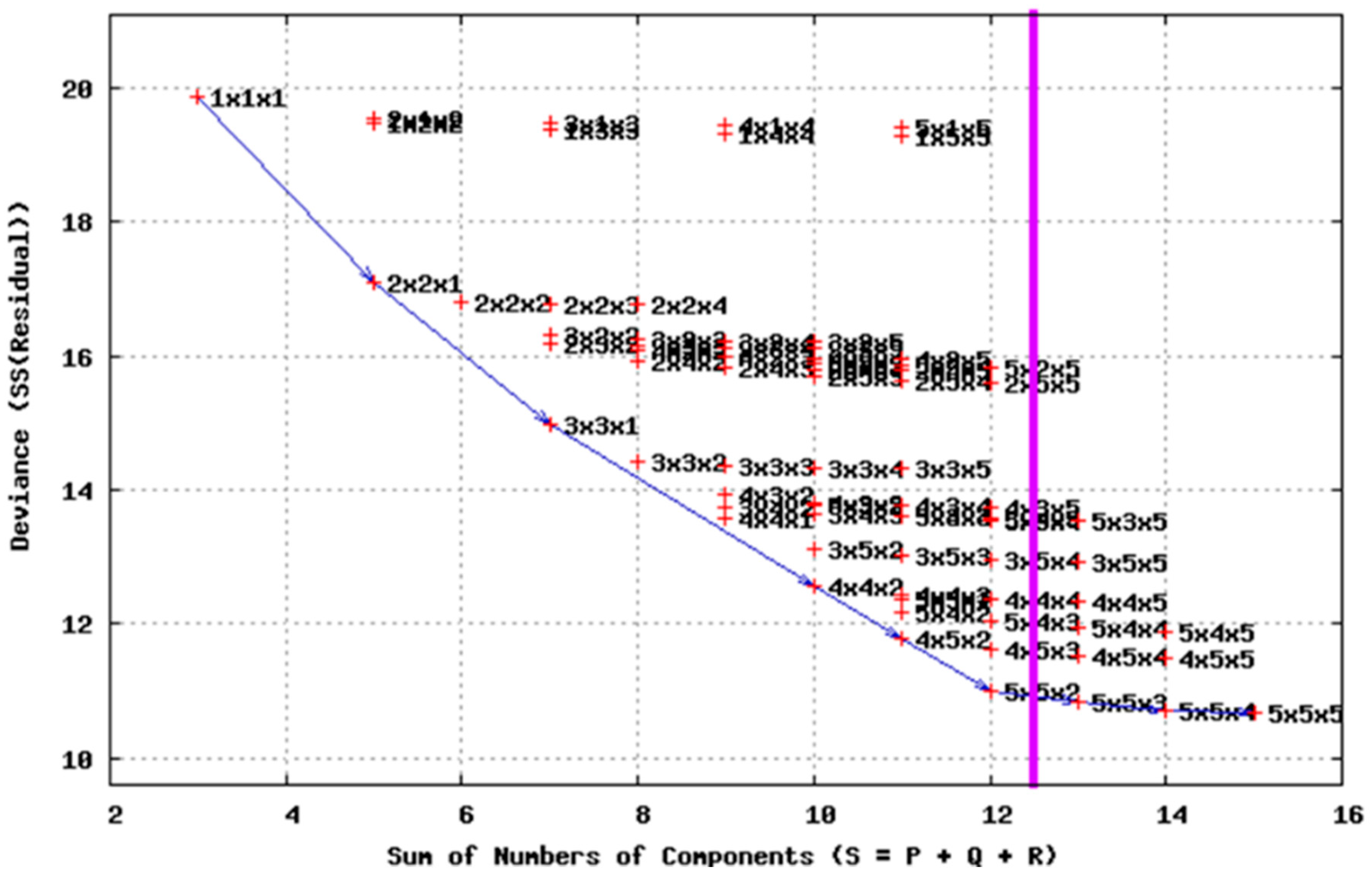

Once the analysis of the CSR has been established at the global level, in this section, we determine the development and evolution of these practices, according to the country of origin of the companies. With a Tucker3 analysis, we examine the relationships between deeper interactions, seeking to characterise each of the countries of origin of the companies in relation to the relevance of their CSR practices. The data are arranged in a cube, composed of 11 matrices (the years, 2004–2014), and each contains 18 rows (countries) and 26 columns (CSR practices). The first step is to select the number of components to be retained for each of the modes (

Figure 10), where mode A refers to the countries of dimension I = 18 and P components to retained; mode B refers to the countries of dimension J = 26 CSR practices and Q components to retained; and mode C refers to the years of study, dimension K = 11, and R components to retained. With the retained components, the core matrix (G) is created to weight all of the possible combinations of these; plus, it contains the amount of variability explained for each of these combinations.

For the selection of the components, we observe the first results that the method gives us;

Table 3 shows us the results of all of the combinations of possible models according to the selection of the components of each mode, with the significant models marked with ‘*’;

Table 4 shows us a summary of the previous table only with the significant models, that is, those models that have a better explained variance for a sum of the fixed components.

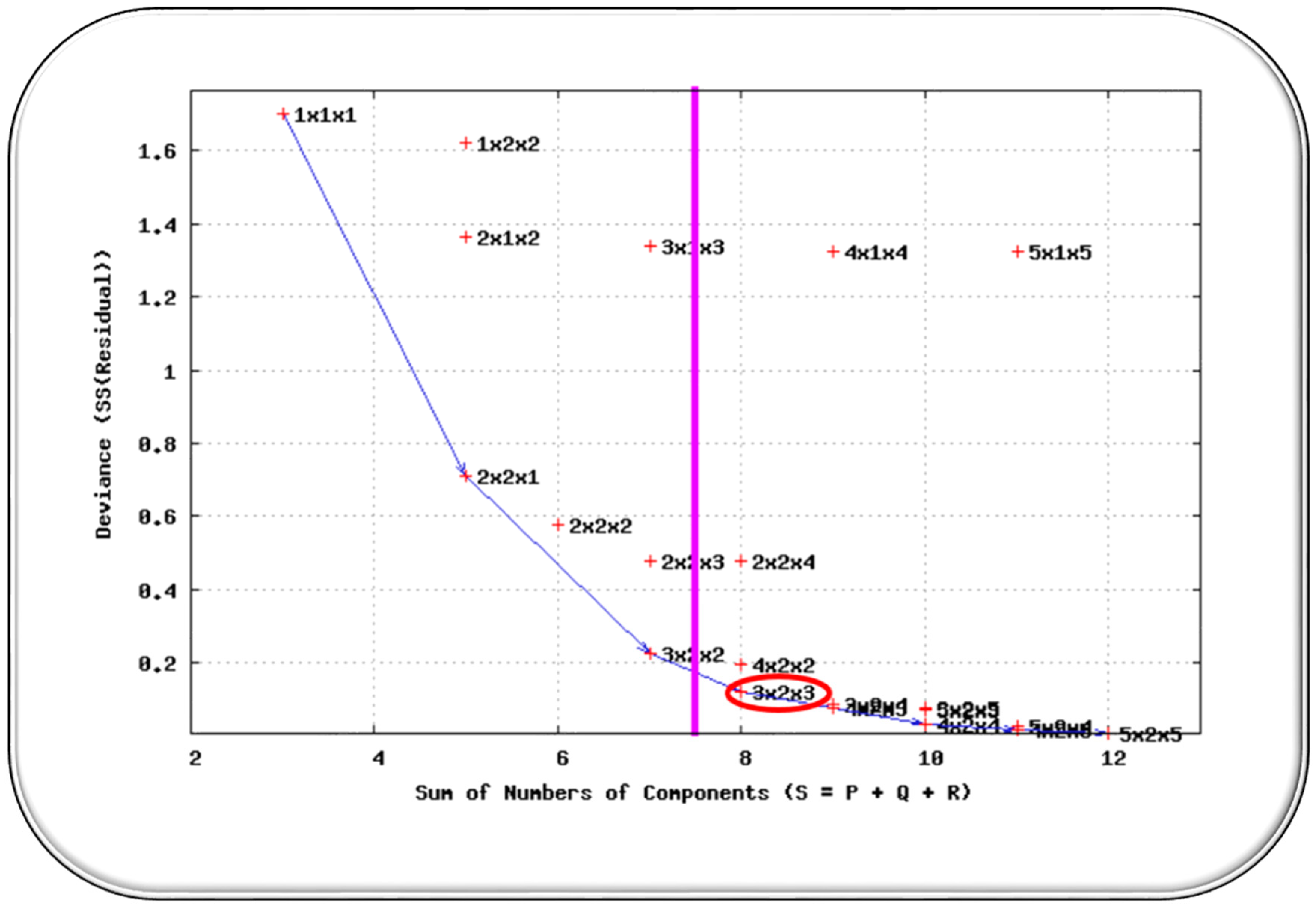

Table 4 shows the models with the best fit, a priori, the selected model results from the 5 × 5 × 2 combination, since the greatest amount of variability is sought, and the difference in the adjustment of the following models is insignificant (around 1%). Another interesting option would be to choose the previous model resulting from the combination 4 × 5 × 2, since its proportion would only decrease by 3%, and we would have a component that is less in the first mode. In addition, to facilitate the selection of the model, you can use the so-called ‘scree plot’ in which all of the possible models are represented based on the sum of the number of its components against the residual sum of squares (

Figure 11). It can be seen that the chosen model 5 × 5 × 2 has the lowest sum of residual squares for those models that have the same sum of the number of components; in addition, it is the first of the most stable, since, in the later ones, the reduction in the sum of residual square is negligible.

Once the model is selected, we perform the same analysis, but setting the number of components to be retained in each mode as 5 × 5 × 2. One of the first results obtained are those of

Table 5, which represents the amount of variance explained by each of the components retained in each of the modes.

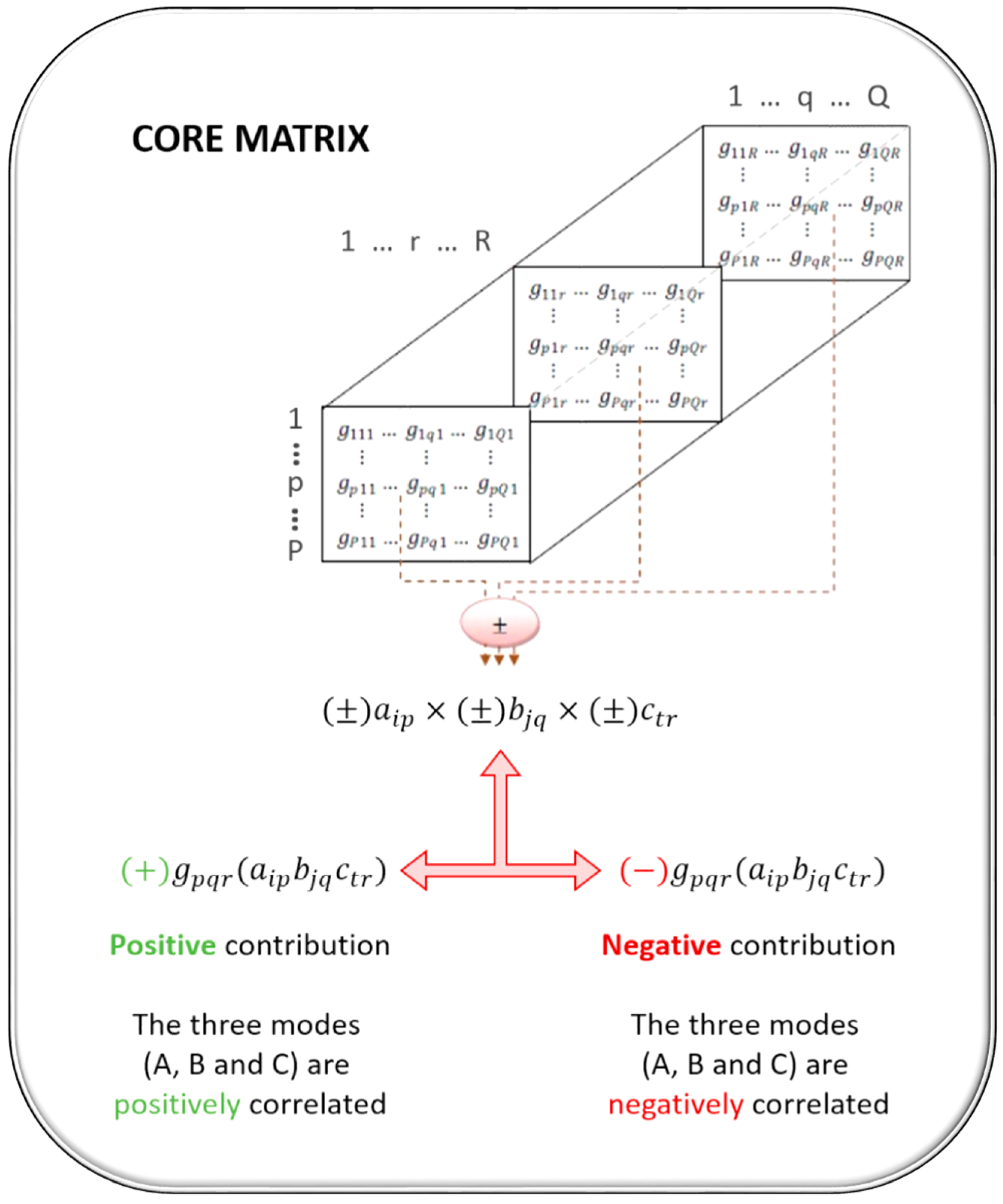

It can be seen that we obtained an amount of 57.60% of the information, which is a percentage high enough, considering that a cube of 18 × 26 × 11 has been reduced to one of 5 × 5 × 2. The next step is the analysis of the core matrix (

Table 6), where we obtain the values of the residual sum of squares and the percentages of variance explained for each of the combinations of the components retained by mode. When identifying those elements of the core matrix that we are interested in interpreting, we select those with a higher percentage of variability, which will be the ones that provide us with the greatest amount of information. In addition, in the sum of squares, the signs are shown to interpret the interactions between the components.

Those elements selected for interpretation have been highlighted, obtaining an explained variance of 41.60%. Next, we analyse each of the elements, showing the graphical results for the three modes, so each graph will represent two components in one way, one horizontally and one vertically; and, together with the results obtained from the core matrix, the interactions between countries, CSR practices, and years will be interpreted.

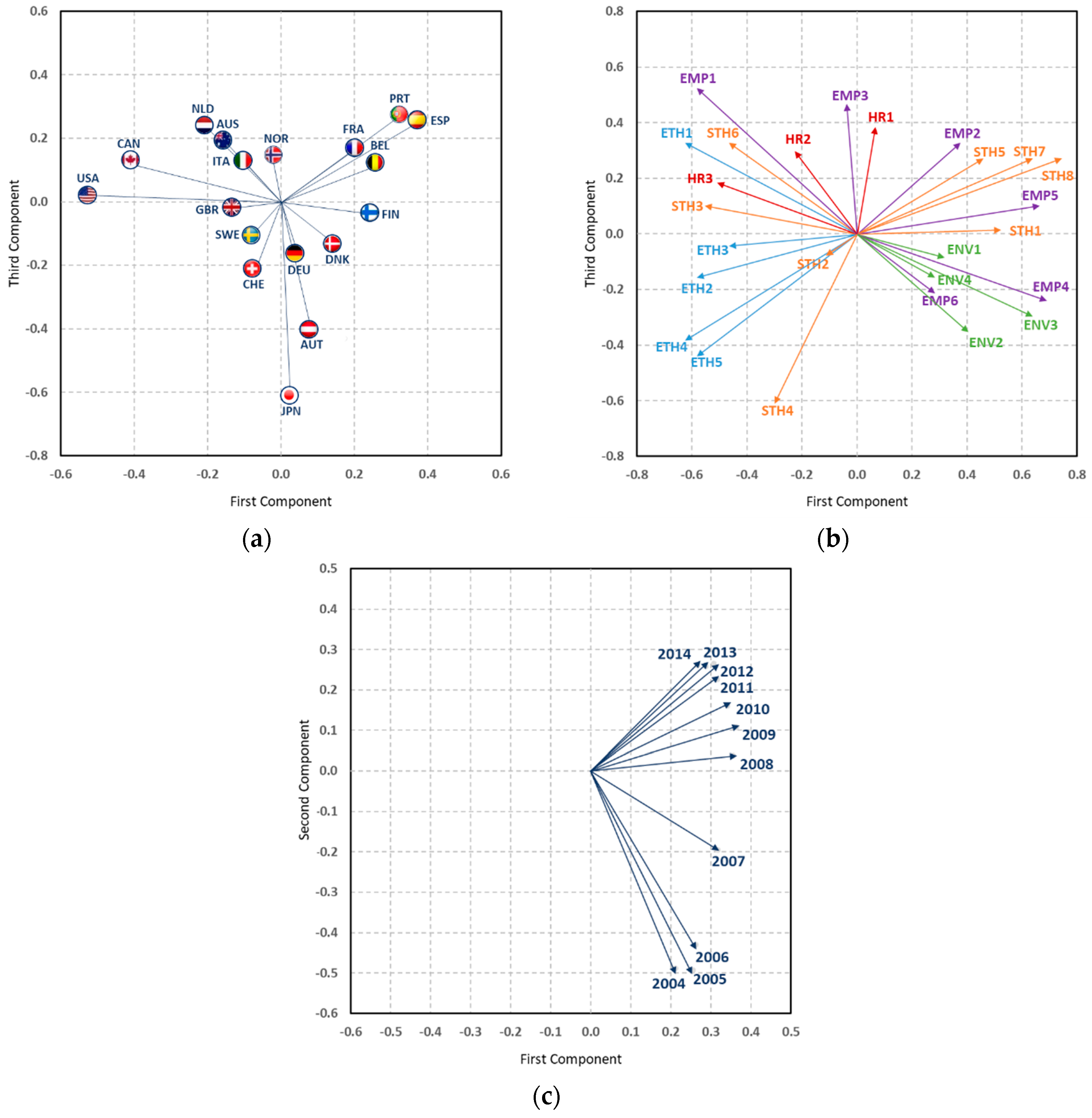

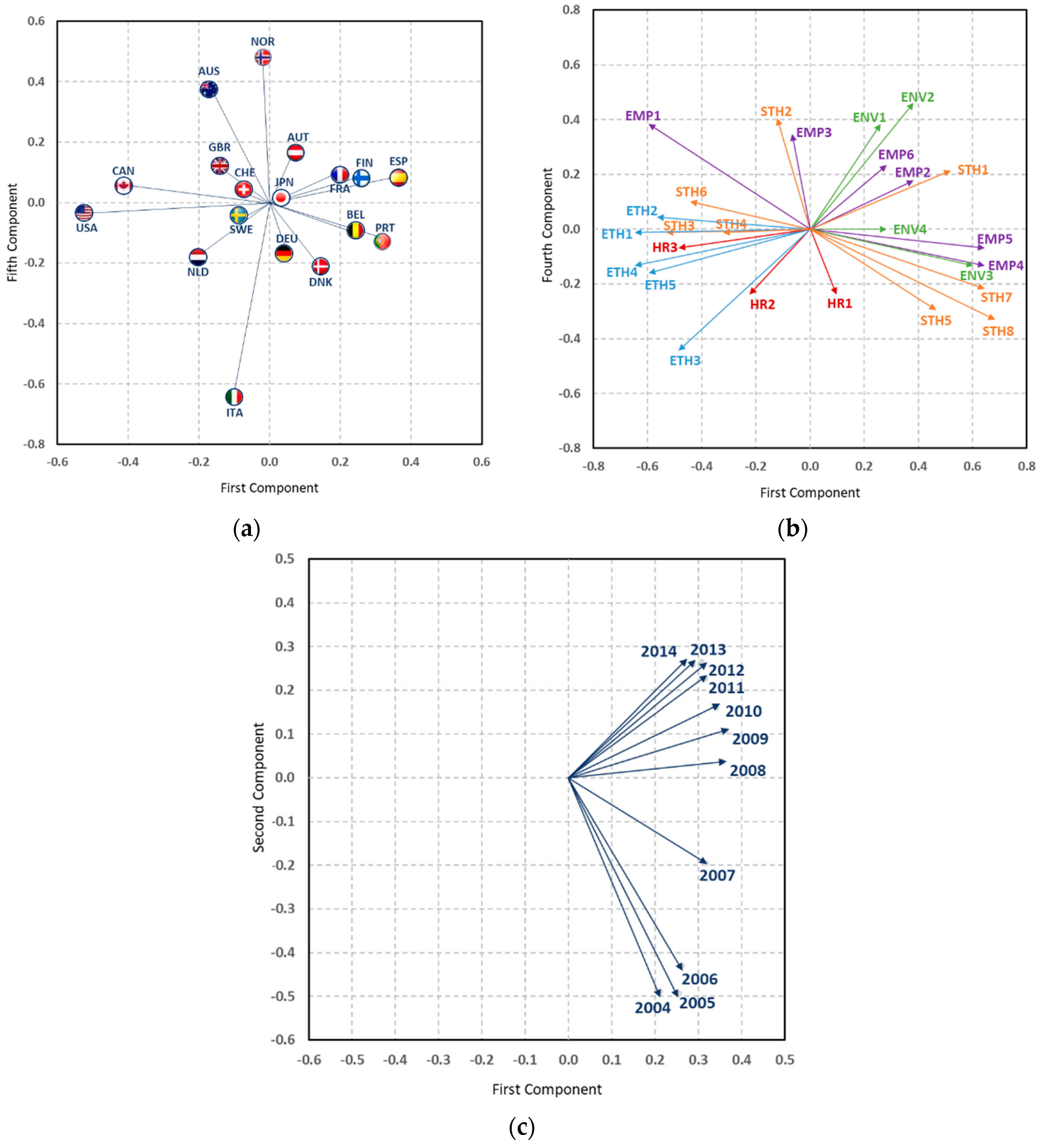

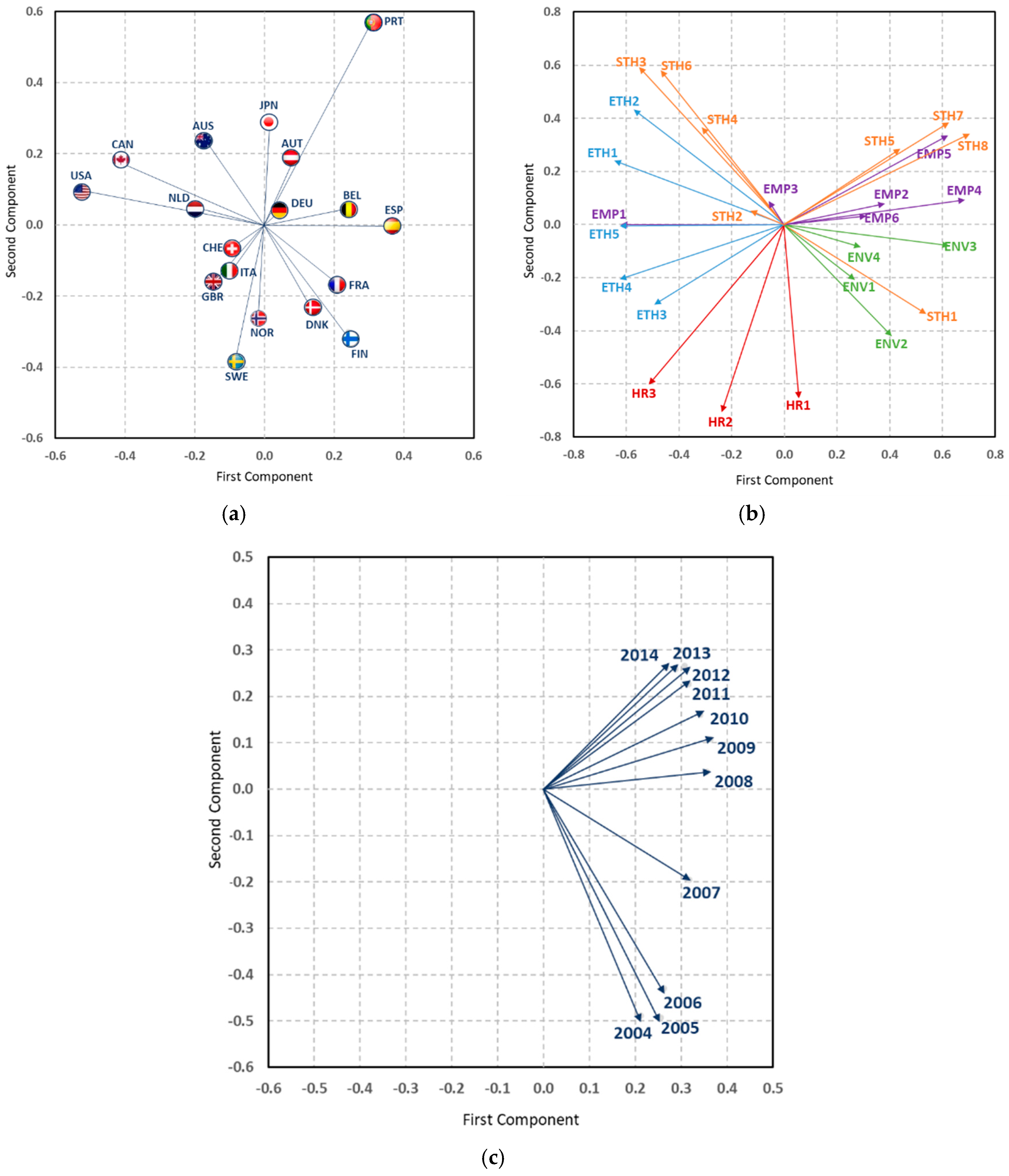

The first element of the core matrix that is interpreted is G111, in which we analyse the first component of each mode (

Figure 12); this element absorbs 23.20% of the total variability. Given that this element is positive (2.45), those countries that are located in the right semi-plane (quadrants I and IV), that is, those that obtain positive values in the first component of mode A, as shown in the first figure, present a positive interaction with the practices of CSR that are also located in the right semi-plane (quadrants I and IV) of the second figure (positive values in the first component of mode B) in all of the years of study, since all of them obtain positive coordinates by positioning themselves in the right part of the third figure.

Although depending on the country of origin of the companies, we can identify specific characteristics in the development and evolution of CSR practices, the analyses carried out allow us to speak of highly similar patterns for those companies whose headquarters are located in geographically close countries. In this sense, the commentary on the results obtained will be made for groups of countries whose companies show similar sustainable behaviour. Thus, for these groups of countries, the main characteristics observed in the development of CSR will be determined.

Thus, during the 2004–2014 decade, companies whose country of origin is located in southwestern Europe (Portugal, Spain, France, Belgium), as well as in Finland and Denmark, prioritise their practices in environmental issues, as well as systems that promote equal opportunities, participation, and training of their employees (EMP2, EMP4, EMP5), and good community relations, participation, systems, and reports on their stakeholders (STH1, STH5, STH7, and STH8).

In the same way, observing the opposite semi-planes, that is, the countries and practices with negative coordinates in the first components of their modes, it is evident for all of the years that the companies whose headquarters are centralised in North American countries, such as the United States and Canada, stand out for their high values in those practices aimed at ethical issues and human rights, as well as policies in favour of equal opportunities (EMP1) and policies towards their stakeholders (STH6), or the importance of these as board members (STH4) and relations with the community (STH3).

It should be noted that the structure found for the first components of the three modes has a very high degree of similarity when compared to the results of the X-STATICO analysis (see

Figure 8), where we observe that the variable ‘equal opportunities policy (EMP1)’ is the one that is separated from the rest of the practices in relation to dealing with employees, also losing its relationship with the environment; we find the same case with the variables towards the interest groups, ‘community involvement (STH3)’, ‘responsibility for stakeholders (STH4)’, and ‘stakeholders policy (STH6)’; likewise, we find the low degree of correlation of the ethical variables and of human rights with the environment. This shows that these methods should be used in a complementary way to obtain results that benefit from the advantages of each of them, since they provide results from different points of view with a strong degree of coherence.

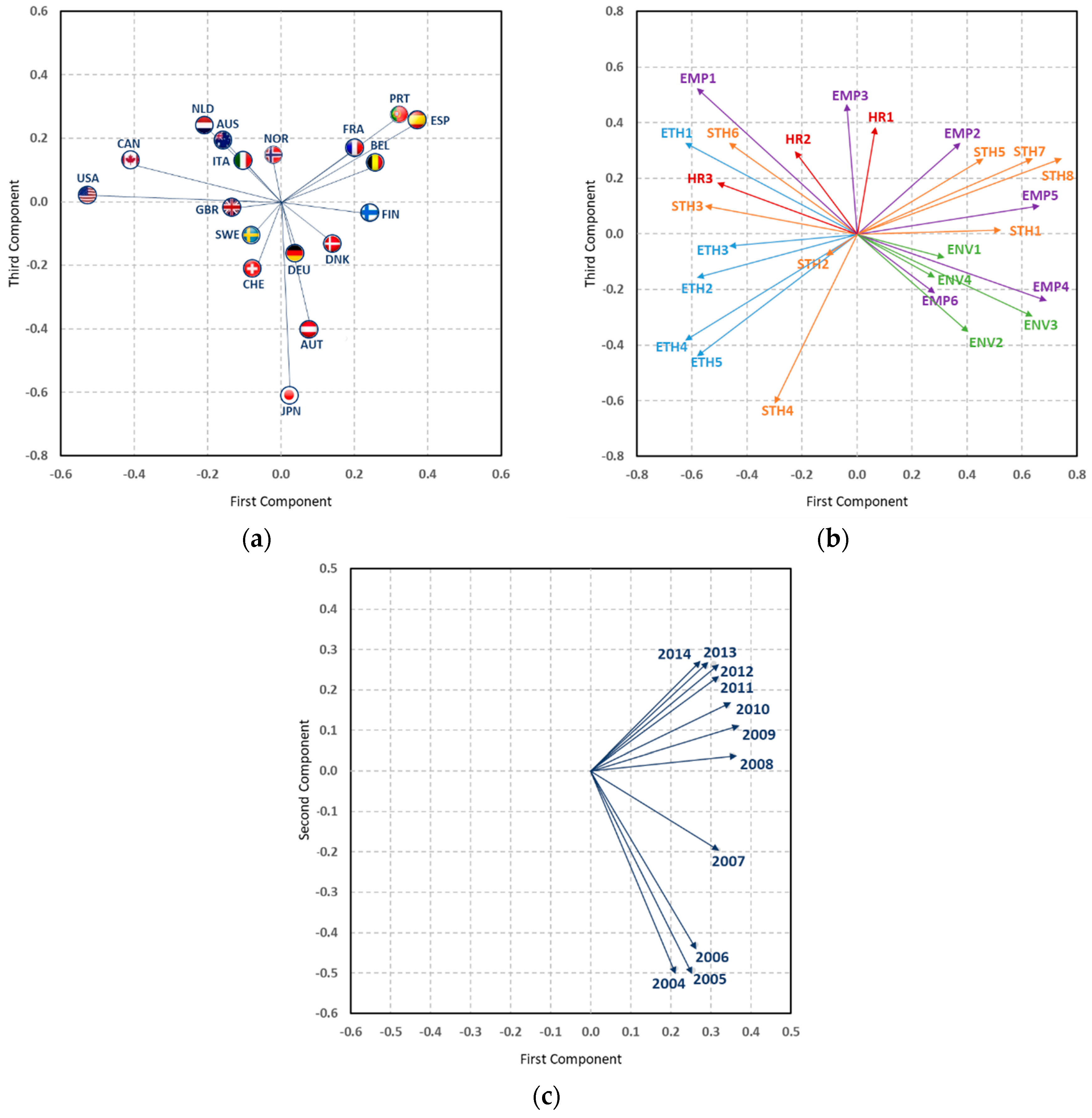

The second element of the core matrix that is interpreted is G221. This element absorbs 8.30% of information, and, since it is formed by the second component of the first and second modes and the first of the third, it is interpreted with the same figure as in the previous case (

Figure 12), with the difference that now, we observe the second components in the first two modes, that is, the vertical axes in countries and CSR practices. Thus, with this being the positive element (1.46), in all of those years, those countries and practices located in the upper semi-plane (quadrants I and II) have a positive interaction.

That is, in all of the years of study, the firms in Portugal emphasise the training of their employees (EMP5), the participation of the community, policies, systems, and reports in favour of the participation and responsibility of the stakeholders (STH3-4-5-6-7-8), and in the implementation of a code of business ethics (ETH2).

In the same way, observing the opposite semi-planes, in all of the years of study, the companies coming from in the Nordic countries—Denmark, Finland, Norway, and Sweden—stand out for presenting the highest levels in the practices related to human rights (policy, system, and report, HR1-2-3), good measures to counteract bribery (policy, system, and report, ETH3-4-5), strong practices in the environment, and a strong commitment to the community (STH1).

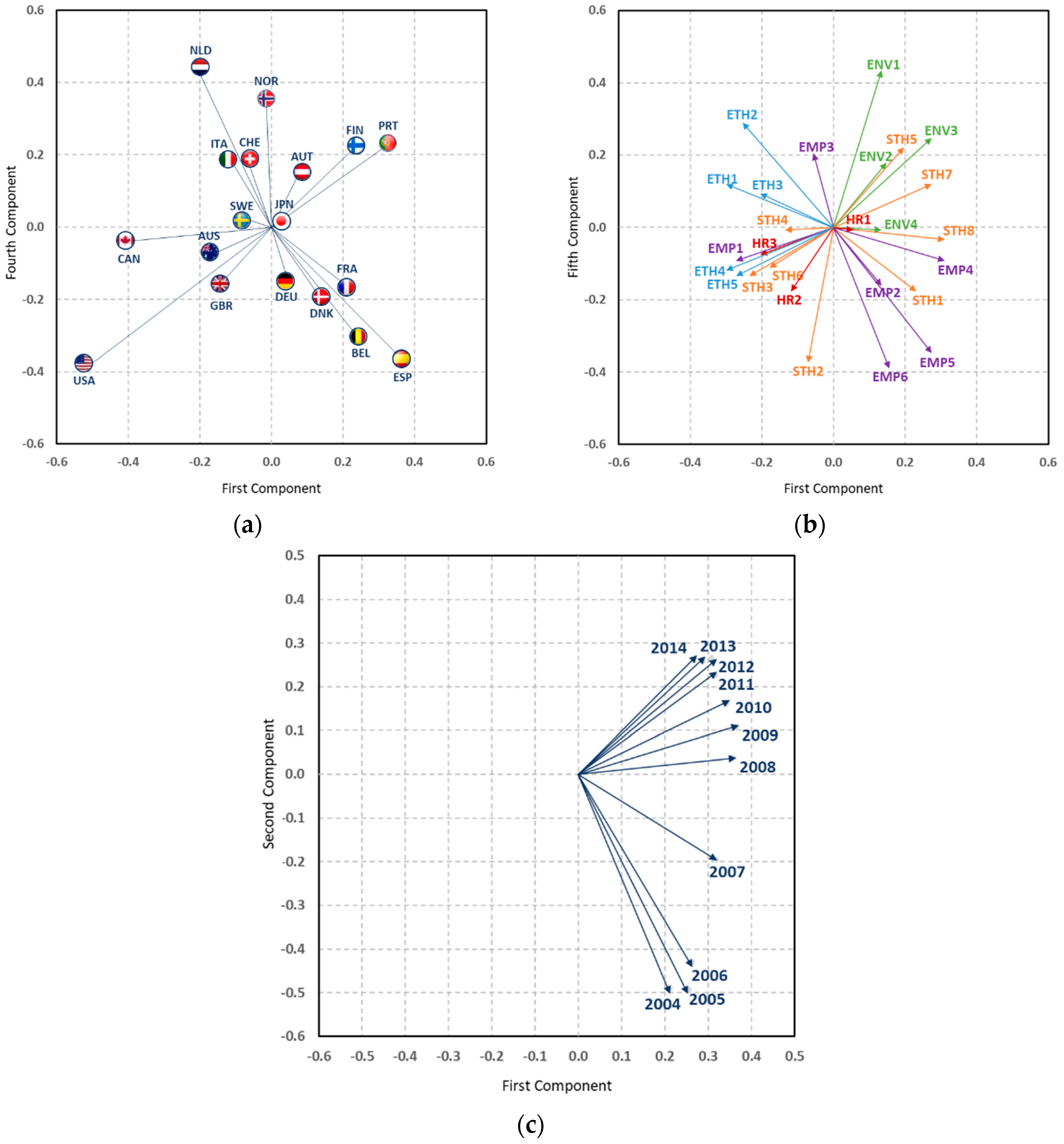

The third element of the core matrix that is interpreted is G331, which is the third component of the first and second modes, and the first component of the third mode (

Figure 13); this element absorbs 5.10% of the total variability. Given that this element is positive (1.15), those countries that obtain positive values in the third component, that is, those that are located in the upper semi-plane (quadrants I and II), present a positive interaction with CSR practices that are also located in the upper semi-plane (quadrants I and II) of the second figure, or vice versa in all of the years of study, since all of them obtain positive coordinates by positioning themselves in the right part of the third figure.

Thus, in all of the years of study, the organisations based in Japan and Austria have focussed mainly on environmental systems and reports (ENV2-3); in addition to the participation of their employees (EMP4) and the responsibility of their stakeholders (STH4) in decision-making processes, and systems and reports in the fight to counteract bribery (ETH4-5).

The fourth and fifth elements of the core matrix are interpreted are G451 and G541, which collect 3.00% and 2.00% information, respectively. The results of these elements should only be interpreted after knowing the results of the other elements of the core matrix with greater variance, understanding that these results explain less obvious differences between countries, CSR practices, and years.

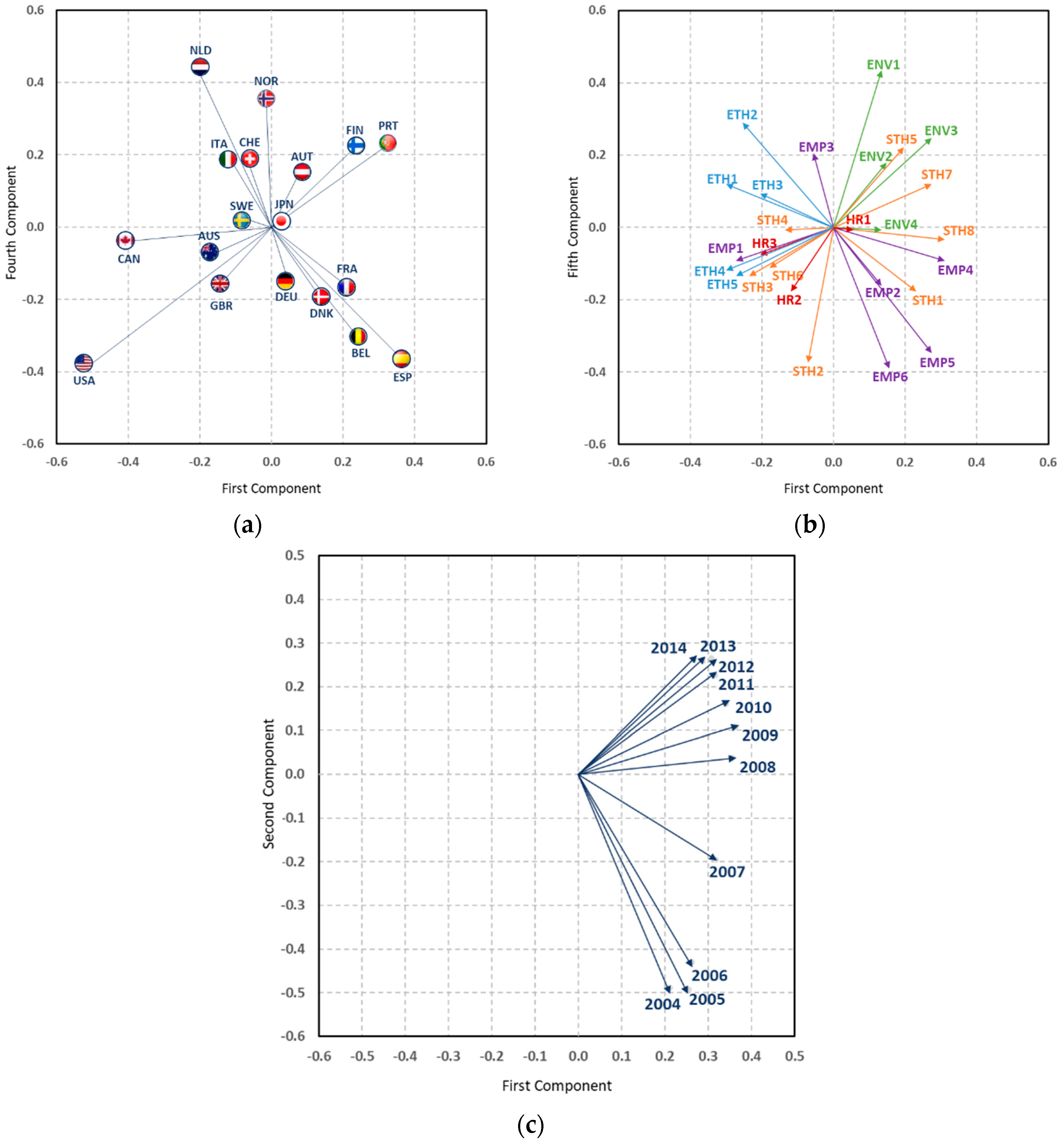

Element G451 interprets the fourth component of the first mode, the fifth of the second mode, and the first of the third mode (

Figure 14). Since this element is positive (0.89), the countries that receive positive coordinates in the fourth component, that is, those located in the upper semi-plane, present during all the years of study a positive interaction with those practices equally situated in the upper semi-plane.

In this way, in all of the years of study, the companies whose country of origin is either the Netherlands or Norway attach great importance to environmental policies and reports (ENV1-3), the health and safety of their employees (EMP3), the participation of their stakeholders (STH5), and the systems for the implementation of a code of ethics (ETH2).

Element G541 interprets the fifth component of the first mode, the fourth of the second mode, and the first of the third mode (

Figure 15). Since this element is positive (0.71), the countries that receive negative coordinates in the fifth component, that is, those located in the lower semi-plane, present during all of the years of study a positive interaction with those practices that are also located in the lower semi-plane.

That is, in all of the years of study, the corporations based in Italy emphasise their CSR practices in human rights policies and systems (HR1 and HR2), the greater participation of their stakeholders and reports on them (STH5 and STH8), as well as policies to counter bribery (ETH3).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}