A Study on the Impact of Financial Literacy and Digital Capabilities on Entrepreneurial Intention: Mediating Effect of Entrepreneurship

Abstract

:1. Introduction

2. Theoretical Background

2.1. Financial Literacy

2.2. Digital Capabilities

2.3. Entrepreneurship

2.4. Entrepreneurial Intention

2.5. Influence Relationship between Variables

3. Research Design

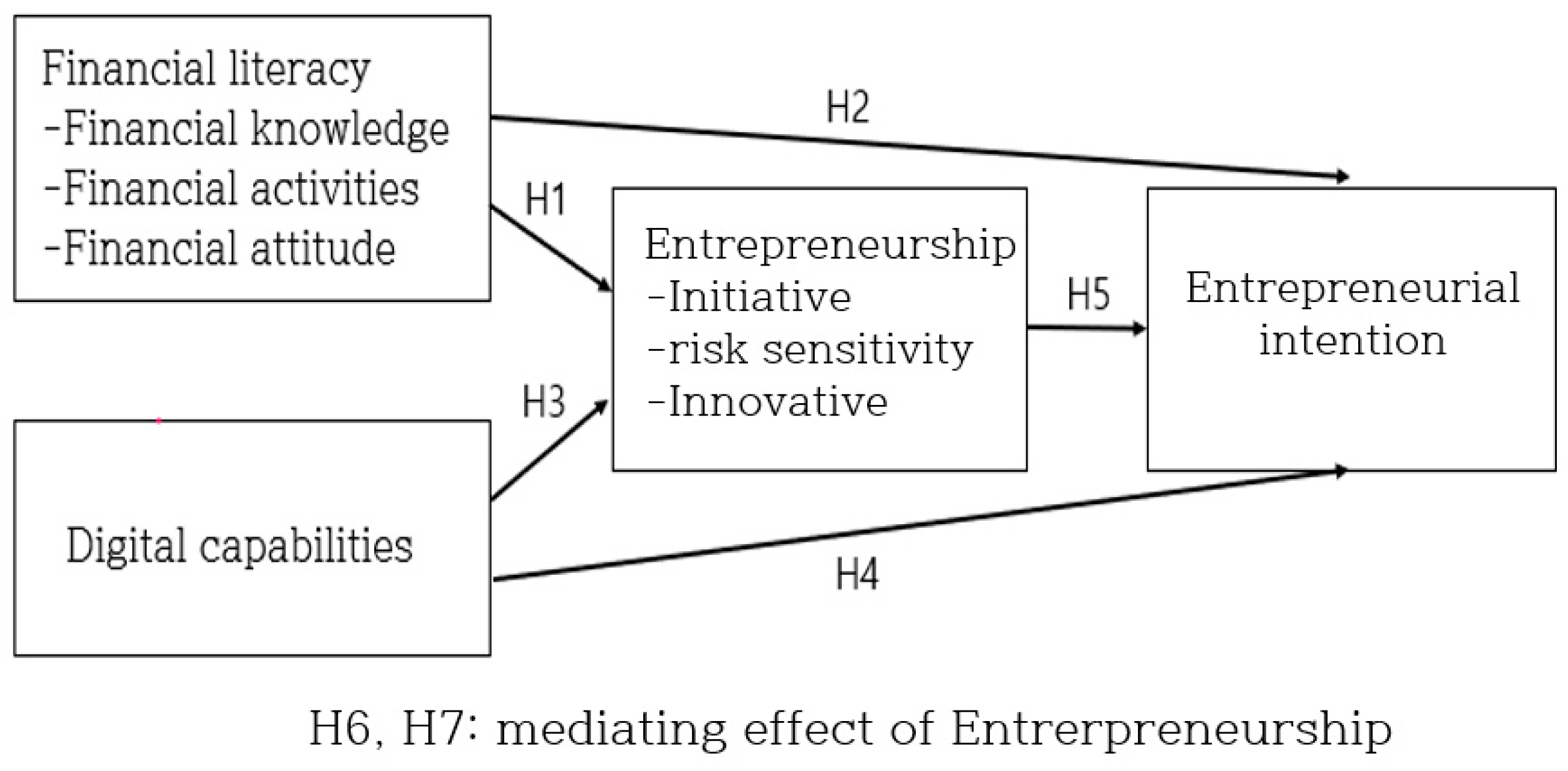

3.1. Establishment of Research Model and Hypothesis

3.2. Construction of Measurement Tools and Data Collection

4. Analysis of Research Results

4.1. Demographic Characteristics

4.2. Reliability, Factor Analysis, Technical Statistics, and Correlation Analysis

4.3. Test Results of Hypothesis

4.3.1. Regression Results

4.3.2. Mediated Regression Results

4.4. Hypothesis Verification Results and Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Yoon, S.M. WEF Geneva. 2022. Available online: https://www.weforum.org (accessed on 11 January 2020).

- Future of Jobs Report. 2023. WEF. Available online: https://www.weforum.org (accessed on 30 April 2023).

- Langdal, T.H.; Johansen, V.; Sølvberg, A.M. Learn to teach and learn from teaching: Teacher’s experiences with programs focusing on financial literacy and entrepreneurship education. Int. J. Innov. Educ. 2022, 7, 145–161. [Google Scholar] [CrossRef]

- Bank of Korea. Results of the 2022 National Financial Literacy Survey. 2023. Available online: https://www.bok.or.kr/portal/cmmn/file/fileDown.do?menuNo=200690&atchFileId=FILE_000000000037734&fileSn=1 (accessed on 29 March 2023).

- OECD INFE. OECD/INFE High-Level Principles on National Strategies for Financial Education; OECD: Paris, France, 2012. [Google Scholar]

- Aprea, C.; Wuttke, E. Financial literacy of adolescents and young adults: Setting the course for a competence-oriented assessment instrument. In International Handbook of Financial Literacy; Springer: Singapore, 2016; pp. 397–414. [Google Scholar]

- European Commission Joint Research Centre. Dig Comp 2.1 The Digital Competence Framework for Citizens with Eight Proficieny, Levels and Examples of Use; European Commission Joint Research Centre: Brussels, Belgium, 2017. [Google Scholar]

- Ilomäki, L.; Kantosalo, A.; Lakkala, M. What Is Digital Competence? In Linked Portal; European Schoolnet: Brussels, Belgium, 2011; Available online: http://linked.eun.org/web/guest/in-depth3 (accessed on 30 April 2023).

- Lee, C.H.; Jeon, J.O. Exploring Digital Competence for the Era of the 4th Industrial Revolution. J. Learn. Centered Curric. Instr. 2020, 20, 311–338. [Google Scholar] [CrossRef]

- Timmons, J.A.; Spinelli, S.; Tan, Y. New Venture Creation: Entrepreneurship for the 21st Century; Irwin: Burr Ridge, IL, USA, 1994; Volume 4. [Google Scholar]

- Kuratko, D.F.; Hodgetts, R.M. Entrepreneurship: Theory, Process, Practice, 6th ed.; Thomson/South-Western: Mason, OH, USA, 2004. [Google Scholar] [CrossRef]

- Lumpkin, G.T.; Dess, G.G. Clarifying the entrepreneurial orientation construct and linking it to performance. Acad. Manag. Rev. 1996, 21, 135–172. [Google Scholar] [CrossRef]

- Miller, D. Revisited: A Reflection on EO Research and Some Suggestions for the Future. Entrep. Theory Pract. 1983, 35, 873–894. [Google Scholar] [CrossRef]

- Shane, S.; Venkataraman, S. The promise of entrepreneurship as a field of research. Acad. Manag. Rev. 2000, 25, 217–226. [Google Scholar] [CrossRef]

- OECD. 2017. Available online: www.oecd.org (accessed on 30 April 2023).

- Gnyawali, D.R.; Fogel, D.S. Environments for entrepreneurship development: Key dimensions and research implications. Entrep. Theory Pract. 1994, 18, 43–62. [Google Scholar] [CrossRef]

- Lieș, G.L.; Mureșan, I.C.; Arion, I.D.; Arion, F.H. The Influence of Economic and Entrepreneurial Education on Perception and Attitudes towards Entrepreneurship. Adm. Sci. 2023, 13, 212. [Google Scholar] [CrossRef]

- Yoon, N.S. The Effect of Potential Entrepreneurial Motivations on Entrepreneurship and Commitment to Starts-up: Mediating Role of Entrepreneurship. J. Ind. Econ. Bus. 2012, 25, 1537–1557. [Google Scholar]

- Jeong, Y.S.; Cho, D.H. A Study on the Comparison of the Importance of Determinants in the Intention of Start-up of University Students. J. Korean Entrep. Socieity 2020, 15, 145–165. [Google Scholar]

- Valdez-Juárez, L.E.; Ramos-Escobar, E.A.; Ruiz-Zamora, J.A.; Borboa-Álvarez, E.P. Personal and Psychological Traits of University-Going Women That Affect Opportunities and Entrepreneurial Intentions. Behav. Sci. 2024, 14, 66. [Google Scholar] [CrossRef] [PubMed]

- Kim, W.J. The Effects of Entrepreneurship and Strategic Orientation on the Firm Performance: Moderated Mediation Effect of Digital Literacy and Learning Orientation. Ph.D. Thesis, The Graduate School of Chung-Ang University, Seoul, Republic of Korea, 2016. [Google Scholar]

- Hwang, S.Y. Study on the Effect of Digital Education and Digital Competency on the Entrepreneurial Intention in the Fourth Industrial Revolution Age: Based on the Perception of Elementary School Students. Master’s Thesis, The Graduate School of Industrial & Entrepreneurial Management Chung-Ang University, Seoul, Republic of Korea, 2019. [Google Scholar]

- Kim, K.S.; Park, W.J.; Bae, B.Y. A Study of Influence of B anker’s Big5 Personality Traits on Entrepreneurial Intention: Mediated Effect of Digital Media Utilization Capability. Asia-Pac. J. Bus. Ventur. Entrep. 2020, 15, 209–220. [Google Scholar] [CrossRef]

- Retzmann, T.; Seeber, G. Financial education in general education schools: A competence model. In International Handbook of Financial Literacy; Springer: Singapore, 2016; pp. 9–23. [Google Scholar]

- Kim, A.R.; Yang, H.K. The Effects of Financial Literacy and Financial Distress on the Financial Management Behavior of Young Working Adults. Financ. Plan. Rev. 2016, 9, 79–105. [Google Scholar] [CrossRef]

- Choi, A.R.; Koo, J.Y. A Study on the Interrelationship between Financial Literacy and Financial Management Behaviors of University Students. J. Korean Data Anal. Soc. 2016, 18, 2637–2650. [Google Scholar] [CrossRef]

- Ahn, H.S.; Yang, D.W. The Influence of Entrepreneurs’ Personal Characteristics on Entrepreneurial Intention with the Moderating Effect of Perception of Startup Support System. J. Korean Entrep. Soc. 2019, 14, 378–410. [Google Scholar] [CrossRef]

- Jeon, H.Y. Current status and implications of domestic and overseas startups. Koreanstud. Inf. Serv. Syst. 2016, 16, 1–17. [Google Scholar]

- von Briel, F.; Davidsson, P.; Recker, J. Digital Technologies as External Enablers of New Venture Creation in the IT Hardware Sector. Entrep. Theory Pract. 2018, 42, 47–69. [Google Scholar] [CrossRef]

- Bachmann, N.; Rose, R.; Maul, V.; Hölzle, K. What makes for future entrepreneurs? The role of digital competencies for entrepreneurial intention. J. Bus. Res. 2024, 174, 1–18. [Google Scholar] [CrossRef]

{kind=link}

| Comprehension Components | Defining Terms | Measurement Item |

|---|---|---|

| Financial Knowledge | Fundamental knowledge to help compare financial instruments or services and make appropriate informed financial decisions | Inflation and purchasing power, understanding of interest concepts, simple calculation, compounding concepts, risk-to-return relationships, meaning of inflation, decentralized investment concepts |

| Financial Behavior | Actions performed by consumers in relation to finance, such as financial planning and budget management, and selection of financial products based on information | Household budget management efforts, active savings activities, careful purchases, timely payment of bills, usual financial inspections, long-term financial objectives, information-based financial product selection, and household balance deficit resolution |

| Financial Attitude | Preference for consumption and savings, present and future, the value of money’s existence, etc. | Preference for consumption over savings, preference for present over future, money exists to be spent |

| Sortation | Analytical Factors | Number of Measurement Questions | How to Respond |

|---|---|---|---|

| Independent variable | Financial literacy | 10 | A five-point Likert scale |

| Digital capabilities | 4 | ||

| Parameters | Entrepreneurship | 12 | |

| Dependent variable | Entrepreneurial intention | 5 | |

| Demographic questions | 3 | ||

| Sum | 34 | ||

| Factor | Operational Definition of Measurement Variables | Researcher |

|---|---|---|

| Entrepreneurship | Initiative: Plan and prepare for what needs to be done actively. The more difficult things you face, the more you try to solve them. To be considered passionate. | Yoon Nam-soo [18], Ahn Hee-Soo and Yang Dong-Woo [27] |

| Risk sensitivity: Tend to push ahead with what I have to do even if it comes with risks. Perform aggressive and bold actions to achieve results. Tend to be bold when it comes to new items. | ||

| Innovative: Likes to challenge new tasks and tasks. Active acceptance of original and innovative ideas. Trying to find creative ideas. | ||

| Digital capabilities | Collect the information you need through the internet. Find and utilize the information appropriate for problem solving. Effective management and utilization of the information gathered. Process financial transactions, travel reservations, taxes, etc., through the internet. Items can be purchased online. | Lee Chul-hyun and Jeon Jong-ho [9] |

| Financial literacy | Financial Knowledge: Inflation and purchasing power, the relationship between risk and return, and the concept of diversification investment. | OECD, INFE [5], The Bank of Korea [4] |

| Financial activities: Timely payment of claims, check the financial situation, and strive to set and implement long-term financial goals. Manage personal budgets and make effective decisions. | ||

| Financial attitude: Preferred present over future, preferred consumption over savings, money exists to spend. | ||

| Entrepreneurial Intention | If you start a business, you are confident that you will succeed. Want to run my own company. Running my company is the best way to improve my financial ability. | Yoon Nam-soo [18], Valdez-Juárez et al. [20] |

| Sortation | Frequency (Number) | Percentage (%) | |

|---|---|---|---|

| Gender | Man | 83 | 64.3 |

| Woman | 46 | 35.7 | |

| Start-up experience | I do | 50 | 38.8 |

| I don’t | 79 | 61.2 | |

| Major field | Social sciences | 43 | 33.3 |

| Natural science | 7 | 5.4 | |

| Engineering field | 70 | 31.0 | |

| So on | 39 | 30.2 | |

| Number of frequencies | 162 | ||

| Financial Knowledge | Financial Behavior | Financial Attitude | Digital Capabilities | Innovation | Risk Sensitivity | Initiative | Entrepreneurial Intention | |

|---|---|---|---|---|---|---|---|---|

| Financial knowledge | 1 | |||||||

| Financial behavior | 0.612 ** | 1 | ||||||

| Financial attitude | 0.449 ** | 0.378 ** | 1 | |||||

| Digital capabilities | 0.634 ** | 0.936 ** | 0.460 ** | 1 | ||||

| Innovation | 0.466 ** | 0.321 ** | 0.513 ** | 0.388 ** | 1 | |||

| Risk sensitivity | 0.390 ** | 0.260 ** | 0.442 ** | 0.320 ** | 0.763 ** | 1 | ||

| Initiative | 0.313 ** | 0.273 ** | 0.424 ** | 0.324 ** | 0.682 ** | 0.731 ** | 1 | |

| Entrepreneurial intention | 0.973 ** | 0.638 ** | 0.537 ** | 0.665 ** | 0.500 ** | 0.405 ** | 0.360 ** | 1 |

| Sortation | Non-Standardized Coefficient | Standardized Coefficient | t | sig. | Perfect Multicollinearity Statistics | |||

|---|---|---|---|---|---|---|---|---|

| Dependent Variable | Independent Variables | B | Standard Error | β | Tolerance Limit | VIF | ||

| Initiative | Financial knowledge | 0.113 | 0.095 | 0.112 | 10.195 | 0.234 | 0.571 | 1.752 |

| Financial behavior | 0.083 | 0.102 | 0.074 | 0.811 | 0.419 | 0.813 | 1.632 | |

| Financial attitude | 0.281 | 0.065 | 0.346 | 40.302 | <0.001 | 0.781 | 1.280 | |

| R = 0.449 R2 = 0.202 R2adj = 0.187 F = 13.333 sig.0.001 | ||||||||

| Risk sensitivity | Financial knowledge | 0.242 | 0.088 | 0.252 | 20.750 | 0.007 | 0.571 | 1.752 |

| Financial behavior | −0.023 | 0.095 | −0.021 | −0.242 | 0.809 | 0.613 | 1.632 | |

| Financial attitude | 0.260 | 0.061 | 0.337 | 40.296 | <0.001 | 0.781 | 1.280 | |

| R = 0.492 R2 = 0.242 R2adj = 0.227 F = 16.7800 sig.0.001 | ||||||||

| Innovation | Financial knowledge | 0.271 | 0.078 | 0.298 | 30.460 | <0.001 | 0.571 | 1.752 |

| Financial behavior | −0.005 | 0.084 | −0.005 | −0.063 | 0.950 | 0.613 | 1.632 | |

| Financial attitude | 0.280 | 0.054 | 0.382 | 50.195 | <0.001 | 0.781 | 1.280 | |

| R = 0.577 R2 = 0.333 R2adj = 0.320 F = 26.293 sig.0.001 | ||||||||

| Entrepreneurial intention | Financial knowledge | 0.890 | 0.021 | 0.889 | 420.162 | <0.001 | 0.571 | 1.752 |

| Financial behavior | 0.056 | 0.023 | 0.050 | 20.463 | 0.015 | 0.613 | 1.632 | |

| Financial attitude | 0.096 | 0.015 | 0.119 | 60.602 | <0.001 | 0.781 | 1.280 | |

| R = 0.980 R2 = 0.960 R2adj = 0.959 F = 1262.581 sig.0.001 | ||||||||

| Entrepreneurial intention | Initiative | 0.018 | 0.104 | 0.018 | 0.171 | 0.864 | 0.428 | 2.334 |

| Risk sensitivity | 0.049 | 0.124 | 0.046 | 0.390 | 0.697 | 0.335 | 2.987 | |

| Innovation | 0.498 | 0.122 | 0.452 | 40.079 | <0.001 | 0.385 | 2.598 | |

| R = 0.502 R2 = 0.252 R2adj = 0.237 F = 17.704 sig.0.001 | ||||||||

| Initiative | Digital capabilities | 0.395 | 0.091 | 0.324 | 40.339 | <0.001 | 1.000 | 1.000 |

| R = 0.324 R2 = 0.105 R2adj = 0.100 F = 18.823 sig.0.001 | ||||||||

| Risk sensitivity | Digital capabilities | 0.369 | 0.087 | 0.320 | 4.266 | <0.001 | 1.000 | 1.000 |

| R = 0.320 R2 = 0.102 R2adj = 0.097 F = 18.199 sig.0.001 | ||||||||

| Innovation | Digital capabilities | 0.425 | 0.080 | 0.388 | 5.317 | <0.001 | 1.000 | 1.000 |

| R = 0.388 R2 = 0.150 R2adj = 0.145 F = 28.275 sig.0.001 | ||||||||

| Entrepreneurial intention | Digital capabilities | 0.803 | 0.071 | 0.665 | 11.248 | <0.001 | 1.000 | 1.000 |

| R = 0.665 R2 = 0.442 R2adj = 0.438 F = 126.524 sig.0.001 | ||||||||

| Independent/Parameter/ Dependent Variables | Mediation Effect Verification Stage | Standardized Beta Values | t Value | p-Value | R2 | Sobel-Test | |

|---|---|---|---|---|---|---|---|

| Z | p | ||||||

| Financial knowledge Initiative Entrepreneurial intention | stage 1 | 0.313 | 4.165 | <0.001 | 0.098 | 2.567 | 0.000 *** |

| stage 2 | 0.973 | 52.874 | <0.001 | 0.946 | |||

| stage (Independent) | 0.953 | 50.735 | <0.001 | 0.949 | |||

| stage 3 (Parameter) | 0.062 | 3.323 | 0.001 | ||||

| Financial knowledge Risk sensitivity Entrepreneurial intention | stage 1 | 0.390 | 5.362 | <0.001 | 0.152 | 1.423 | 0.155 |

| stage 2 | 0.973 | 52.874 | <0.001 | 0.946 | |||

| stage (Independent) | 0.961 | 48.285 | <0.001 | 0.947 | |||

| stage 3 (Parameter) | 0.030 | 1.494 | 0.137 | ||||

| Financial knowledge Innovation Entrepreneurial intention | stage 1 | 0.466 | 6.659 | <0.001 | 0.217 | 2.733 | 0.000 *** |

| stage 2 | 0.973 | 52.874 | <0.001 | 0.946 | |||

| stage (Independent) | 0.945 | 46.532 | <0.001 | 0.949 | |||

| stage 3 (Parameter) | 0.060 | 2.965 | 0.003 | ||||

| Financial behavior Initiative Entrepreneurial intention | stage 1 | 0.273 | 3.591 | <0.001 | 0.075 | 2.418 | 0.000 *** |

| stage 2 | 0.638 | 10.491 | <0.001 | 0.408 | |||

| stage (Independent) | 0.583 | 9.500 | <0.001 | 0.445 | |||

| stage 3 (Parameter) | 0.201 | 3.275 | 0.001 | ||||

| Financial behavior Risk sensitivity Entrepreneurial intention | stage 1 | 0.260 | 3.407 | <0.001 | 0.068 | 2.651 | 0.000 *** |

| stage 2 | 0.638 | 10.491 | <0.001 | 0.408 | |||

| stage (Independent) | 0.572 | 9.551 | <0.001 | 0.469 | |||

| stage 3 (Parameter) | 0.256 | 4.277 | <0.001 | ||||

| Financial behavior Innovation Entrepreneurial intention | stage 1 | 0.321 | 4.288 | <0.001 | 0.103 | 3.398 | 0.000 *** |

| stage 2 | 0.638 | 10.491 | <0.001 | 0.408 | |||

| stage (Independent) | 0.533 | 9.040 | <0.001 | 0.505 | |||

| stage 3 (Parameter) | 0.329 | 5.585 | <0.001 | ||||

| Financial attitude Initiative Entrepreneurial intention | stage 1 | 0.424 | 5.926 | <0.001 | 0.180 | 2.093 | 0.000 *** |

| stage 2 | 0.537 | 8.048 | <0.001 | 0.288 | |||

| stage (Independent) | 0.468 | 6.433 | <0.001 | 0.310 | |||

| stage 3 (Parameter) | 0.162 | 2.225 | 0.027 | ||||

| Financial attitude Risk sensitivity Entrepreneurial intention | stage 1 | 0.442 | 6.230 | <0.001 | 0.195 | 2.603 | 0.000 *** |

| stage 2 | 0.537 | 8.048 | <0.001 | 0.288 | |||

| stage (Independent) | 0.445 | 6.115 | <0.001 | 0.323 | |||

| stage 3 (Parameter) | 0.208 | 2.863 | 0.005 | ||||

| Financial attitude Innovation Entrepreneurial intention | stage 1 | 0.513 | 7.569 | <0.001 | 0.264 | 3.598 | 0.000 *** |

| stage 2 | 0.537 | 8.048 | <0.001 | 0.288 | |||

| stage (Independent) | 0.380 | 5.129 | <0.001 | 0.357 | |||

| stage 3 (Parameter) | 0.305 | 4.113 | <0.001 | ||||

| Digital capabilities Initiative Entrepreneurial intention | stage 1 | 0.324 | 4.339 | <0.001 | 0.105 | 2.255 | 0.000 *** |

| stage 2 | 0.665 | 11.248 | <0.001 | 0.442 | |||

| stage (Independent) | 0.612 | 9.980 | <0.001 | 0.465 | |||

| stage 3 (Parameter) | 0.162 | 2.641 | 0.009 | ||||

| Digital capabilities Risk sensitivity Entrepreneurial intention | stage 1 | 0.320 | 4.266 | <0.001 | 0.102 | 2.725 | 0.000 *** |

| stage 2 | 0.665 | 11.248 | <0.001 | 0.442 | |||

| stage (Independent) | 0.596 | 9.903 | <0.001 | 0.483 | |||

| stage 3 (Parameter) | 0.214 | 3.560 | <0.001 | ||||

| Digital capabilities Innovation Entrepreneurial intention | stage 1 | 0.388 | 5.317 | <0.001 | 0.150 | 3.544 | 0.000 *** |

| stage 2 | 0.665 | 11.248 | <0.001 | 0.442 | |||

| stage (Independent) | 0.554 | 9.206 | <0.001 | 0.511 | |||

| stage 3 (Parameter) | 0.286 | 4.745 | <0.001 | ||||

| Hypothesis | Accept Status | |

|---|---|---|

| Hypothesis 1: Financial Literacy—Entrepreneurship | Partially Accept | |

| 1-1 | Financial knowledge—Initiative | Reject |

| 1-2 | Financial knowledge—Risk sensitivity | Accept |

| 1-3 | Financial knowledge—Innovation | Accept |

| 1-4 | Financial behavior—Initiative | Reject |

| 1-5 | Financial behavior—Risk sensitivity | Reject |

| 1-6 | Financial behavior—Innovation | Reject |

| 1-7 | Financial attitude—Initiative | Accept |

| 1-8 | Financial attitude—Risk sensitivity | Accept |

| 1-9 | Financial attitude—Innovation | Accept |

| Hypothesis 2: Financial Literacy—Entrepreneurial Intention | Accept | |

| 2-1 | Financial knowledge—Entrepreneurial intention | Accept |

| 2-2 | Financial behavior—Entrepreneurial intention | Accept |

| 2-3 | Financial attitude—Entrepreneurial intention | Accept |

| Hypothesis 3: Digital capabilities—Entrepreneurship | Accept | |

| 3-1 | Digital capabilities—Initiative | Accept |

| 3-2 | Digital capabilities—Risk sensitivity | Accept |

| 3-3 | Digital capabilities—Innovation | Accept |

| Hypothesis 4: Digital capabilities—Entrepreneurial intention | Accept | |

| Hypothesis 5: Entrepreneurship—Entrepreneurial intention | Partially Accept | |

| 5-1 | Initiative—Entrepreneurial intention | Reject |

| 5-2 | Risk sensitivity—Entrepreneurial intention | Reject |

| 5-3 | Innovation—Entrepreneurial intention | Accept |

| Hypothesis 6: Financial Literacy—Entrepreneurship—Entrepreneurial intention (Mediating effect) | Partially Accept | |

| 6-1 | Financial knowledge—Initiative—Entrepreneurial intention | Accept |

| 6-2 | Financial knowledge—Risk sensitivity—Entrepreneurial intention | Reject |

| 6-3 | Financial knowledge—Innovation—Entrepreneurial intention | Accept |

| 6-4 | Financial behavior—Initiative—Entrepreneurial intention | Accept |

| 6-5 | Financial behavior—Risk sensitivity—Entrepreneurial intention | Accept |

| 6-6 | Financial behavior—Innovation—Entrepreneurial intention | Accept |

| 6-7 | Financial attitude—Initiative—Entrepreneurial intention | Accept |

| 6-8 | Financial attitude—Risk sensitivity—Entrepreneurial intention | Accept |

| 6-9 | Financial attitude—Innovation—Entrepreneurial intention | Accept |

| Hypothesis 7: Digital capabilities—Entrepreneurship—Entrepreneurial intention (Mediating effect) | Accept | |

| 7-1 | Digital capabilities—Initiative—Entrepreneurial intention | Accept |

| 7-2 | Digital capabilities—Risk sensitivity—Entrepreneurial intention | Accept |

| 7-3 | Digital capabilities—Innovation—Entrepreneurial intention | Accept |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kang, G.-L.; Park, C.-W.; Jang, S.-H. A Study on the Impact of Financial Literacy and Digital Capabilities on Entrepreneurial Intention: Mediating Effect of Entrepreneurship. Behav. Sci. 2024, 14, 121. https://doi.org/10.3390/bs14020121

Kang G-L, Park C-W, Jang S-H. A Study on the Impact of Financial Literacy and Digital Capabilities on Entrepreneurial Intention: Mediating Effect of Entrepreneurship. Behavioral Sciences. 2024; 14(2):121. https://doi.org/10.3390/bs14020121

Chicago/Turabian StyleKang, Gyung-Lan, Cheol-Woo Park, and Seung-Hwan Jang. 2024. "A Study on the Impact of Financial Literacy and Digital Capabilities on Entrepreneurial Intention: Mediating Effect of Entrepreneurship" Behavioral Sciences 14, no. 2: 121. https://doi.org/10.3390/bs14020121