Factors Affecting the Capital Cost of Prefabrication—A Case Study of China

Abstract

:1. Introduction

2. Literature Review

2.1. Barriers to Cost-Saving for Prefabrication

2.2. Drivers for Cost-Saving for Prefabrication

3. Research Methodology

3.1. Mean Analysis

3.2. Calculation of Prefabrication Capital Cost

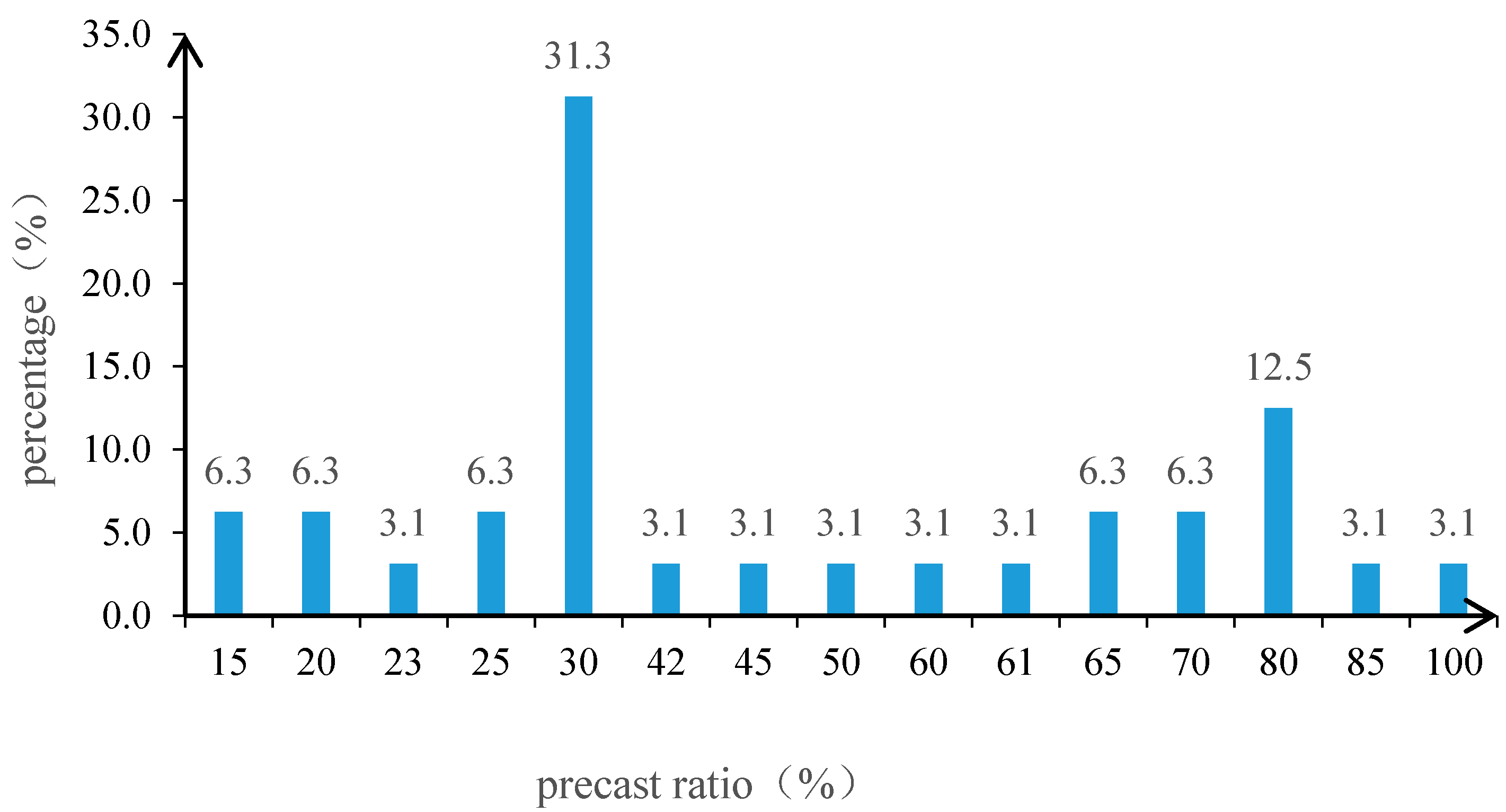

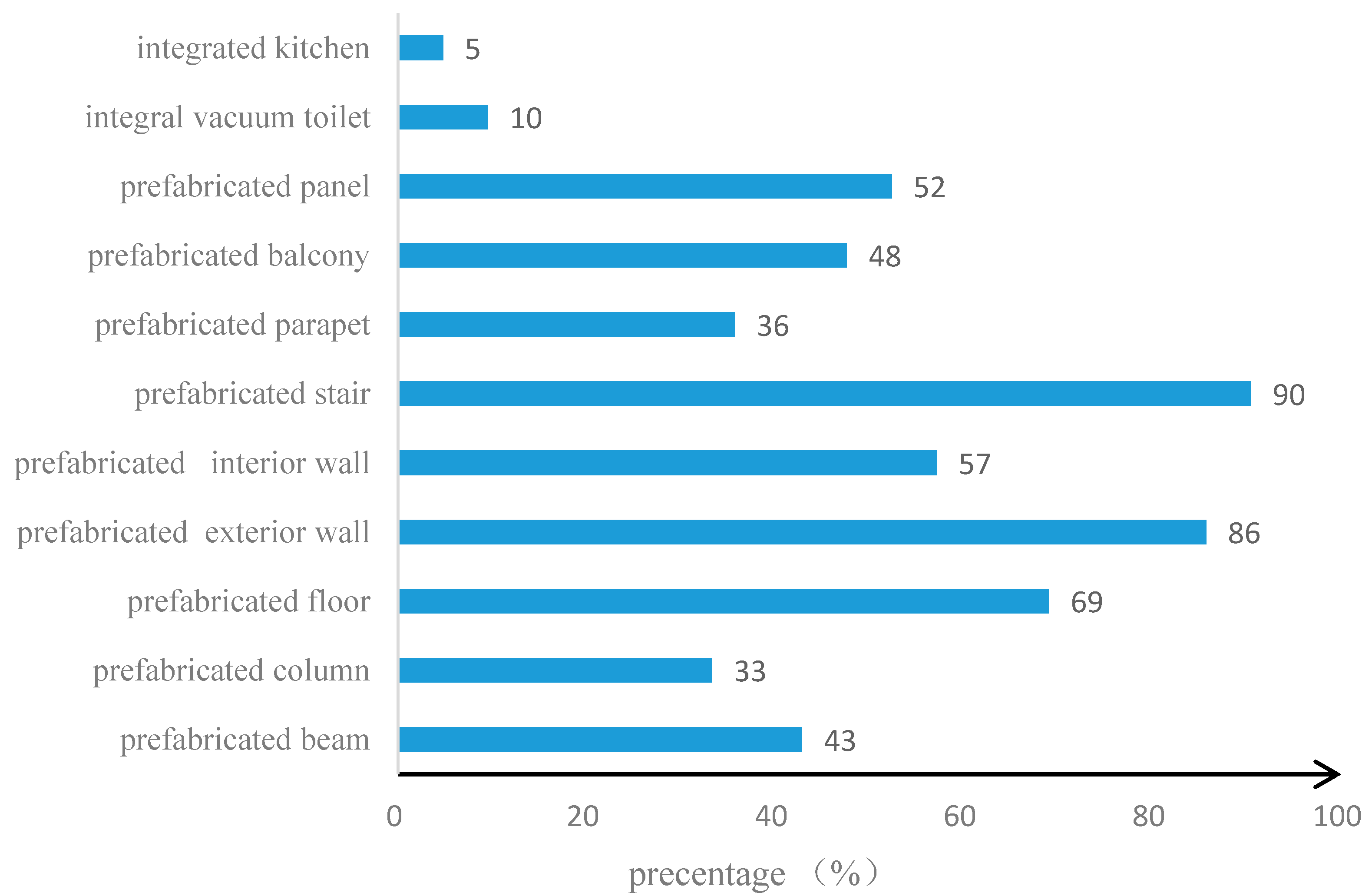

3.3. Data Collection

3.3.1. Factors Affecting the Capital Cost of Prefabrication

3.3.2. Questionnaire Design

3.4. Descriptive Statistics

4. Research Findings

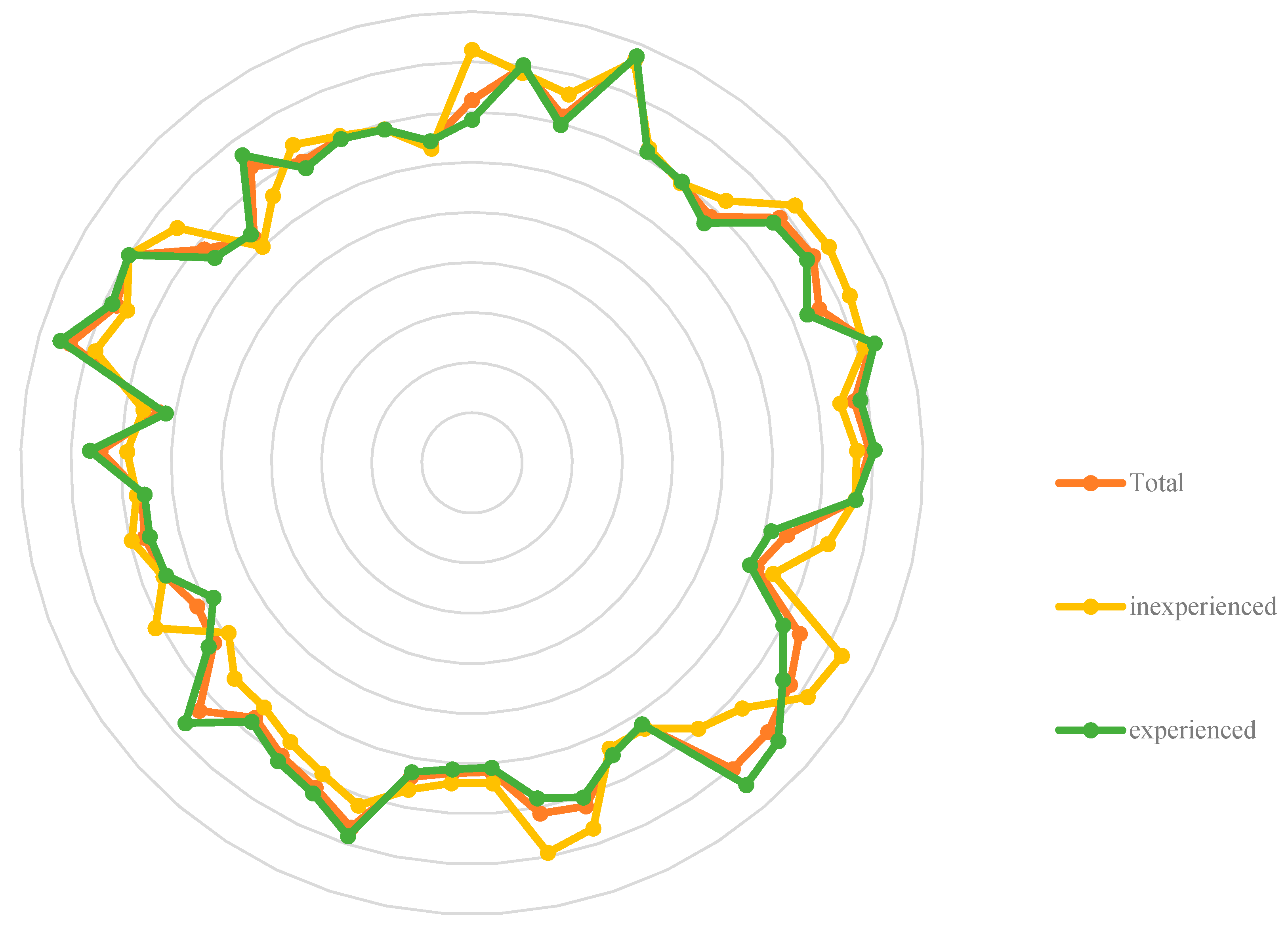

4.1. t-Test

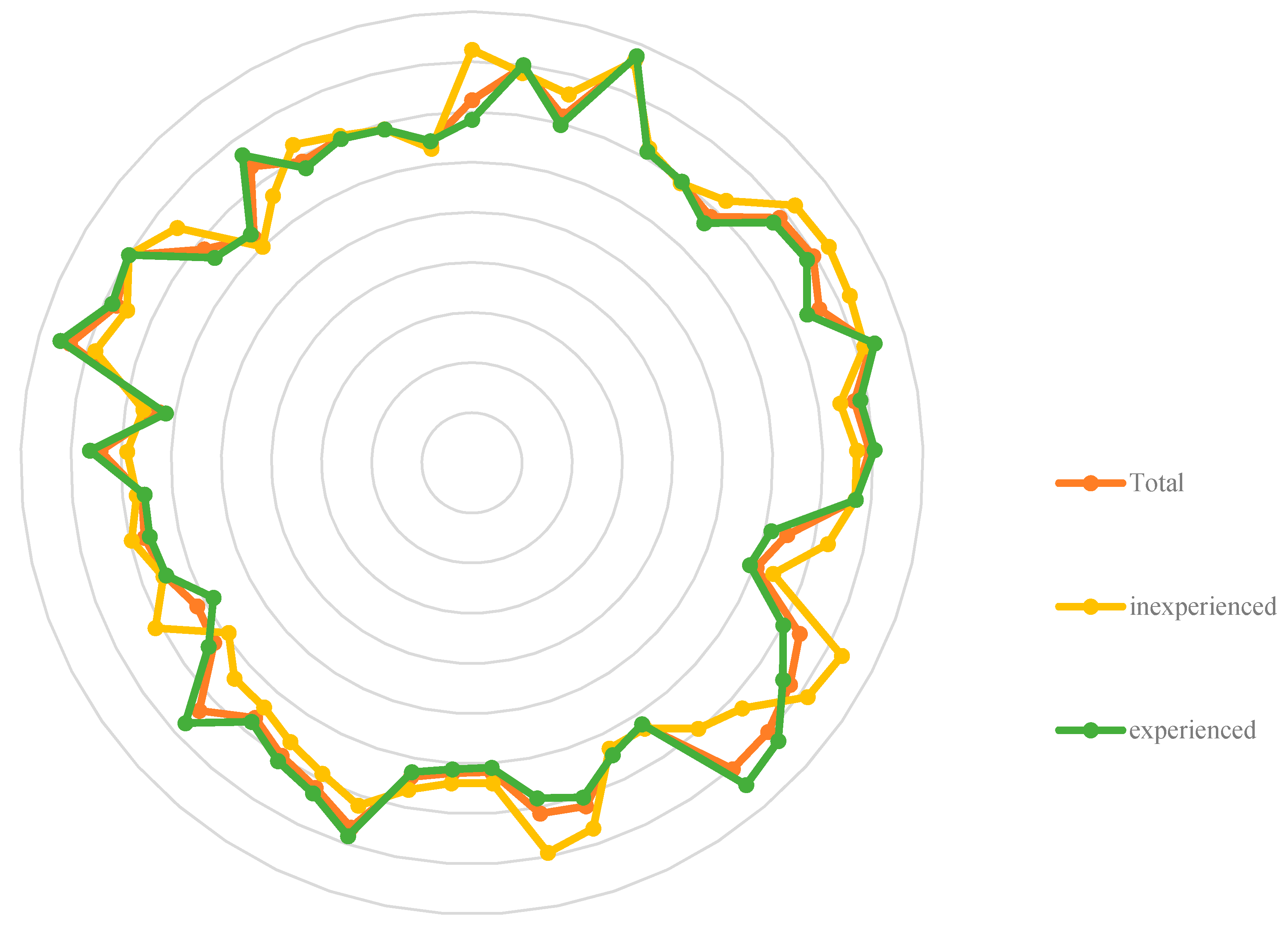

4.2. One-Way ANOVA

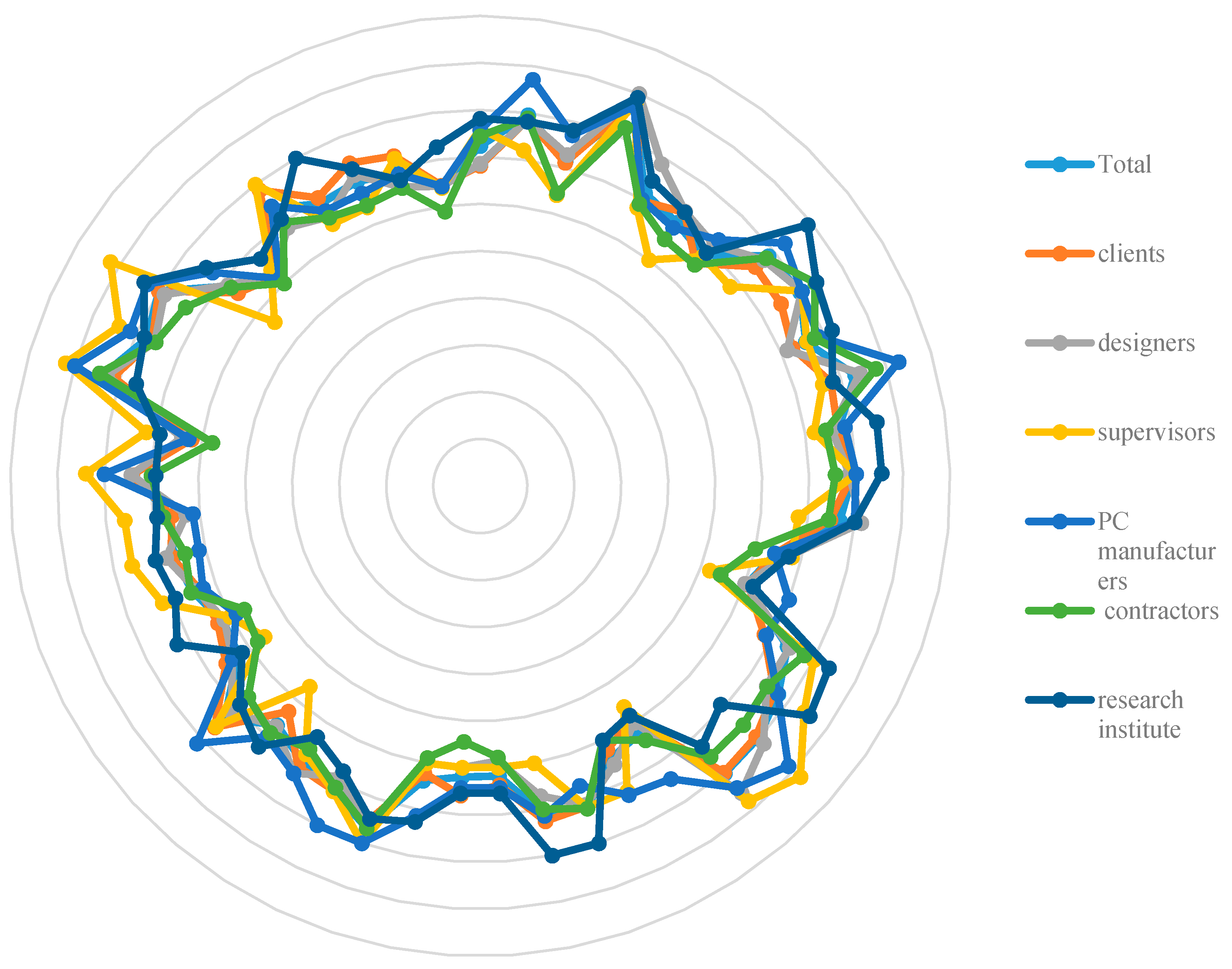

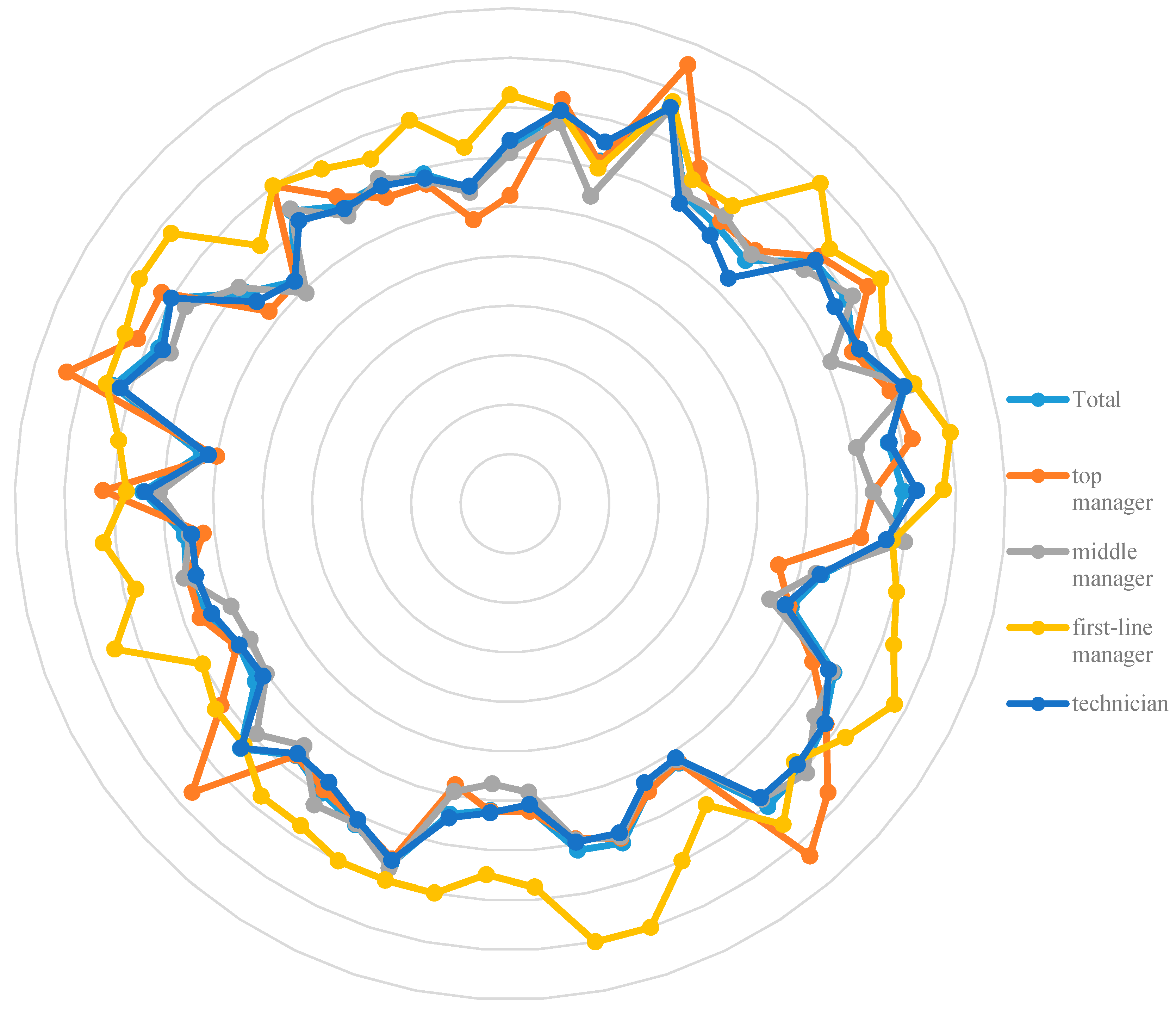

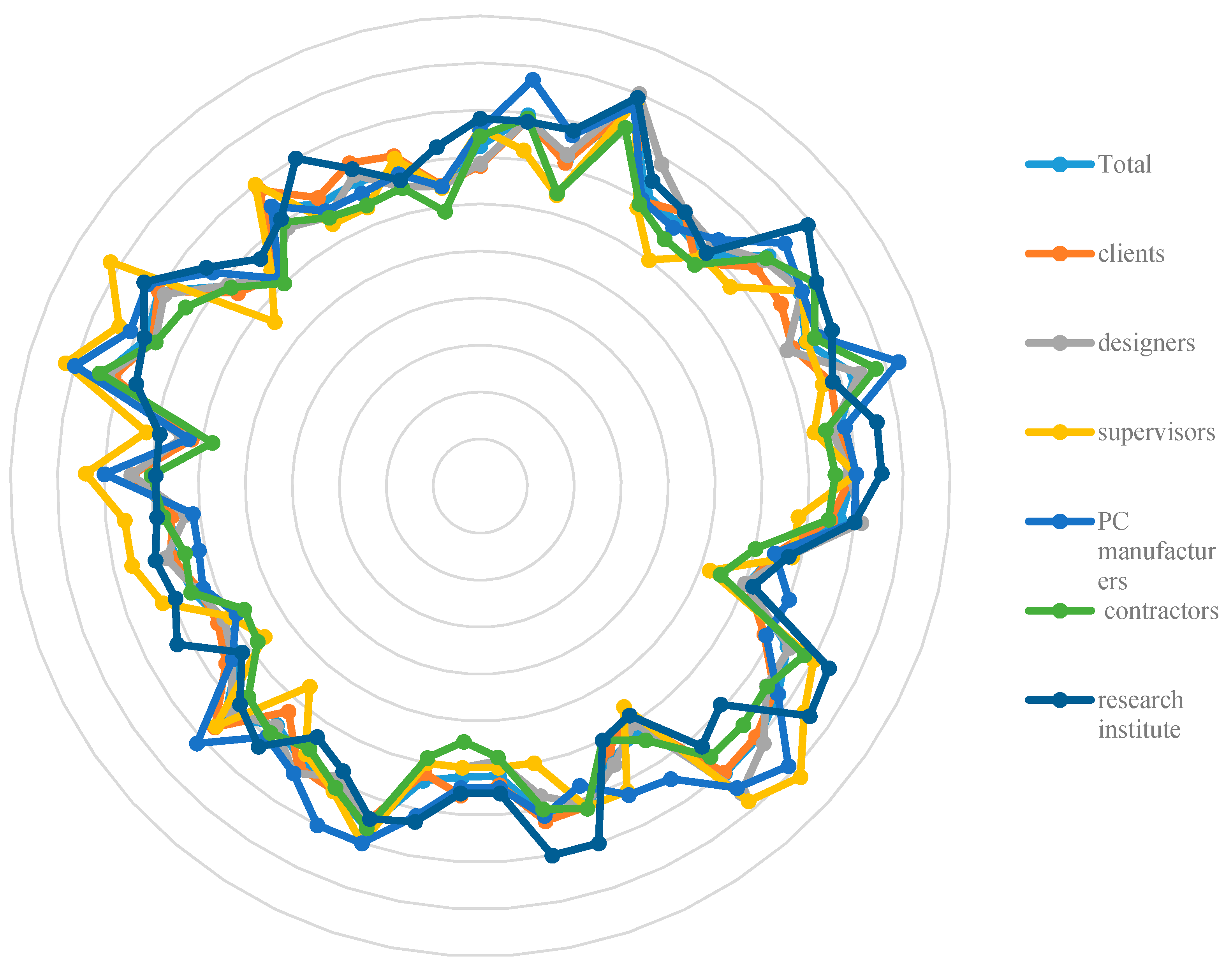

4.2.1. One-Way ANOVA for the Stakeholders

4.2.2. One-Way ANOVA Test for the Function

5. Discussion

6. Conclusions

Supplementary Materials

Supplementary File 1Acknowledgments

Author Contributions

Conflicts of Interest

References

- Arashpour, M.; Wakefield, R.; Lee, E.W.M.; Chan, R.; Hosseini, M.R. Analysis of interacting uncertainties in on-site and off-site activities: Implications for hybrid construction. Int. J. Proj. Manag. 2016, 34, 1393–1402. [Google Scholar] [CrossRef]

- Matthews, J.; Love, P.E.D.; Heinemann, S.; Chandler, R.; Rumsey, C.; Olatunj, O. Real time progress management: Re-engineering processes for cloud-based BIM in construction. Autom. Constr. 2015, 58, 38–47. [Google Scholar] [CrossRef]

- Low, S.P. Quantifying the relationships between buildability, structural quality and productivity in construction. Struct. Surv. 2001, 19, 106–112. [Google Scholar]

- Hwang, B.; Zhao, X.; Tan, L.L.G. Green building projects: Schedule performance, influential factors and solutions. Eng. Constr. Arch. Manag. 2015, 22, 327–346. [Google Scholar] [CrossRef]

- Jaillon, L.; Poon, C.S. Life cycle design and prefabrication in buildings: A review and case studies in Hong Kong. Autom. Const. 2014, 39, 195–202. [Google Scholar] [CrossRef]

- Kim, M.; Woo, C.; Rho, J.; Chung, Y. Environmental Capabilities of Suppliers for Green Supply Chain Management in Construction Projects: A Case Study in Korea. Sustainability 2016, 8, 82. [Google Scholar] [CrossRef]

- Mao, C.; Xie, F.; Hou, L.; Wu, P.; Wang, J.; Wang, X. Cost analysis for sustainable off-site construction based on a multiple-case study in China. Habitat Int. 2016, 57, 215–222. [Google Scholar] [CrossRef]

- Gan, Y.; Shen, L.; Chen, J.; Tam, V.; Tan, Y.; Illankoon, I. Critical Factors Affecting the Quality of Industrialized Building System Projects in China. Sustainability 2017, 9, 216. [Google Scholar] [CrossRef]

- Faghirinejadfard, A.; Mahdiyar, A.; Marsono, A.K.; Mohandes, S.R.; Omrany, H.; Tabatabaee, S.; Tap, M.M. Economic Comparison of Industrialized Building System and Conventional Construction System Using Building Information Modeling. J. Tecnol. 2016, 78, 195–207. [Google Scholar] [CrossRef]

- Tao, W.; Yulong, L.; Limao, Z.; Guijun, L. Case Study of Integrated Prefab Accommodations System for Migrant On-Site Construction Workers in China. J. Prof. Issue Eng. Educ. Pract. 2016, 142, 1–11. [Google Scholar]

- Chen, Y.; Okudan, G.E.; Riley, D.R. Decision support for construction method selection in concrete buildings: Prefabrication adoption and optimization. Autom. Constr. 2010, 19, 665–675. [Google Scholar] [CrossRef]

- Zabihi, H.; Habib, F.; Mirsaeedie, L. Definitions, concepts and new directions in Industrialized Building Systems (IBS). KSCE J. Civ. Eng. 2013, 17, 1199–1205. [Google Scholar] [CrossRef]

- Lopez, D.; Froese, T.M. Analysis of Costs and Benefits of Panelized and Modular Prefabricated Homes. Proc. Eng. 2016, 145, 1291–1297. [Google Scholar] [CrossRef]

- Seaden, G.; Manseau, A. Public policy and construction innovation. Build. Res. Inf. 2001, 29, 182–196. [Google Scholar] [CrossRef]

- Chiang, Y.; Hon-Wan Chan, E.; Ka-Leung Lok, L. Prefabrication and barriers to entry—A case study of public housing and institutional buildings in Hong Kong. Habitat Int. 2006, 30, 482–499. [Google Scholar] [CrossRef]

- Tam, V.W.Y.; Tam, C.M.; Zeng, S.X.; Ng, W.C.Y. Towards adoption of prefabrication in construction. Build. Environ. 2007, 42, 3642–3654. [Google Scholar] [CrossRef]

- Liu, X.C.; Pu, S.H.; Zhang, A.L.; Xu, A.X.; Ni, Z.; Sun, Y.; Ma, L. Static and seismic experiment for bolted-welded joint in modularized prefabricated steel structure. J. Constr. Steel Res. 2015, 115, 417–433. [Google Scholar] [CrossRef]

- Isaac, S.; Bock, T.; Stoliar, Y. A methodology for the optimal modularization of building design. Autom. Constr. 2016, 65, 116–124. [Google Scholar] [CrossRef]

- Luo, L.; Mao, C.; Shen, L.; Li, Z. Risk factors affecting practitioners’ attitudes toward the implementation of an industrialized building system:A case study from China. Eng. Constr. Arch. Manag. 2015, 22, 622–643. [Google Scholar]

- Chen, Y.; Okudan, G.E.; Riley, D.R. Sustainable performance criteria for construction method selection in concrete buildings. Autom. Constr. 2010, 19, 235–244. [Google Scholar] [CrossRef]

- Gibb, A.; Isack, F. Re-engineering through pre-assembly: Client expectations and drivers. Build. Res. Inf. 2003, 31, 146–160. [Google Scholar] [CrossRef] [Green Version]

- Pan, W.; Gibb, A.G.F.; Dainty, A.R.J. Perspectives of UK housebuilders on the use of offsite modern methods of construction. Constr. Manag. Econ. 2007, 25, 183–194. [Google Scholar] [CrossRef] [Green Version]

- Tan, Y.; Shen, L.; Yao, H. Sustainable construction practice and contractors’ competitiveness: A preliminary study. Habitat Int. 2011, 35, 225–230. [Google Scholar] [CrossRef]

- Amin Hosseini, S.M.; de la Fuente, A.; Pons, O. Multi-criteria decision-making method for assessing the sustainability of post-disaster temporary housing units technologies: A case study in Bam, 2003. Sustain. Cities Soc. 2016, 20, 38–51. [Google Scholar] [CrossRef]

- Shahzad, W.; Mbachu, J.; Domingo, N. Marginal productivity gained through prefabrication: Case studies of building projects in auckland. Buildings 2015, 5, 196–208. [Google Scholar] [CrossRef]

- Onat, N.C.; Kucukvar, M.; Halog, A.; Cloutier, S. Systems thinking for life cycle sustainability assessment: A review of recent developments, applications, and future perspectives. Sustainability 2017, 9, 706. [Google Scholar] [CrossRef]

- Voellinger, T.; Bassi, A.; Heitel, M. Facilitating the incorporation of VIP into precast concrete sandwich panels. Energ. Build. 2014, 85, 666–671. [Google Scholar] [CrossRef]

- Yun, S.; Jung, W. Benchmarking sustainability practices use throughout industrial construction project delivery. Sustainability 2017, 9, 1007. [Google Scholar] [CrossRef]

- Steinhardt, D.A.; Manley, K. Adoption of prefabricated housing–the role of country context. Sustain. Cities Soc. 2016, 22, 126–135. [Google Scholar] [CrossRef]

- Blismas, N.; Pasquire, C.; Gibb, A. Benefit evaluation for off-site production in construction. Constr. Manag. Econ. 2006, 24, 121–130. [Google Scholar] [CrossRef] [Green Version]

- Zhao, X.; Hwang, B.; Gao, Y. A fuzzy synthetic evaluation approach for risk assessment: A case of Singapore’s green projects. J. Clean. Prod. 2016, 115, 203–213. [Google Scholar] [CrossRef]

- Hwang, B.; Shan, M.; Phua, H.; Chi, S. An exploratory analysis of risks in green residential building construction projects: The case of Singapore. Sustainability 2017, 9, 1116. [Google Scholar] [CrossRef]

- Arashpour, M.; Wakefield, R.; Blismas, N.; Minas, J. Optimization of process integration and multi-skilled resource utilization in off-site construction. Autom. Constr. 2015, 50, 72–80. [Google Scholar] [CrossRef]

- Rahman, M.M. Barriers of Implementing Modern Methods of Construction. J. Manag. Eng. 2014, 30, 69–77. [Google Scholar] [CrossRef]

- Arashpour, M.; Wakefield, R.; Blismas, N.; Maqsood, T. Autonomous production tracking for augmenting output in off-site construction. Autom. Constr. 2015, 53, 13–21. [Google Scholar] [CrossRef]

- Polat, G. Factors Affecting the Use of Precast Concrete Systems in the United States. J Constr. Eng. 2008, 134, 169–178. [Google Scholar] [CrossRef]

- Hwang, B.G.; Zhao, X.; Van Do, T.H. Influence of trade-level coordination problems on project productivity. Proj. Manag. J. 2014, 45, 5–14. [Google Scholar] [CrossRef]

- Asri, M.; Nawi, M.; Saad, R.; Wan, N.O.; Anuar, H.S. Exploring lean construction component for Malaysian industrialized building system logistics management—A literature review. Adv. Sci. Lett. 2016, 22, 1593–1596. [Google Scholar] [CrossRef]

- Pan, W.; Sidwell, R. Demystifying the cost barriers to offsite construction in the UK. Constr. Manag. Econ. 2011, 29, 1081–1099. [Google Scholar] [CrossRef]

- Khalili, A.; Chua, D.K. Integrated Prefabrication Configuration and Component Grouping for Resource Optimization of Precast Production. J. Constr. Eng. Manag. 2014, 140, 1–12. [Google Scholar] [CrossRef]

- Jaillon, L.; Poon, C.S. Sustainable construction aspects of using prefabrication in dense urban environment: A Hong Kong case study. Constr. Manag. Econ. 2008, 26, 953–966. [Google Scholar] [CrossRef]

- Polat, G. Precast concrete systems in developing vs. industrialized countries. J. Civ. Eng. Manag. 2010, 16, 85–94. [Google Scholar] [CrossRef]

- David, G.; Edward, B.; Nahid, H. Influence of Risk and Change Events on Cost, Schedule, and Predictability Performances. J. Prof. Issues Eng. Educ. Prac. 2016, 142, 1–9. [Google Scholar]

- Poirier, E.A.; Staub-French, S.; Forgues, D. Measuring the impact of BIM on labor productivity in a small specialty contracting enterprise through action-research. Autom. Constr. 2015, 58, 74–84. [Google Scholar] [CrossRef]

- Kim, Y.; Han, S.; Yi, J.; Chang, S. Supply chain cost model for prefabricated building material based on time-driven activity-based costing. Can. J. Civil. Eng. 2016, 43, 287–293. [Google Scholar] [CrossRef]

- Jaillon, L.; Poon, C.S. The evolution of prefabricated residential building systems in Hong Kong: A review of the public and the private sector. Autom. Constr. 2009, 18, 239–248. [Google Scholar] [CrossRef]

- Hill, R.C.; Bowen, P.A. Sustainable construction: principles and a framework for attainment. Constr. Manag. Econ. 1997, 15, 223–239. [Google Scholar] [CrossRef]

- Winch, G. Models of manufacturing and the construction process: The genesis of re-engineering construction. Build. Res. Inf. 2003, 31, 107–118. [Google Scholar] [CrossRef]

- Alazzaz, F.; Whyte, A. Linking employee empowerment with productivity in off-site construction. Eng. Constr. Arch. Manag. 2015, 22, 21–37. [Google Scholar] [CrossRef]

- Matic, D.; Calzada, J.R.; Eric, M.; Babin, M. Economically feasible energy refurbishment of prefabricated building in Belgrade, Serbia. Energy Build. 2015, 98, 74–81. [Google Scholar] [CrossRef] [Green Version]

- Gann, D. Putting academic ideas into practice: Technological progress and the absorptive capacity of construction organizations. Constr. Manag. Econ. 2010, 19, 321–330. [Google Scholar] [CrossRef]

- Shan, Y.; Imran, H.; Lewis, P.; Zhai, D. Investigating the latent factors of quality of work-life affecting construction craft worker job satisfaction. J. Constr. Eng. Manag. 2017, 143, 1–10. [Google Scholar] [CrossRef]

- Qian, Q.; Chan, E.; Khalid, A. Challenges in Delivering Green Building Projects: Unearthing the Transaction Costs (TCs). Sustainability 2015, 7, 3615–3636. [Google Scholar] [CrossRef]

- Zhong, R.Y.; Peng, Y.; Xue, F.; Fang, J.; Zou, W.; Luo, H.; Thomas Ng, S.; Lu, W.; Shen, G.Q.P.; Huang, G.Q. Prefabricated construction enabled by the internet-of-things. Autom. Constr. 2017, 76, 59–70. [Google Scholar] [CrossRef]

- Xue, H. Factors Affecting the Capital Cost of Prefabrication. Available online: https://sojump.com/jq/12604390.aspx (accessed on 23 August 2017).

- Hwang, B.G.; Zhao, X.; Ong, S.Y. Value management in Singaporean building projects: Implementation status, critical success factors, and risk factors. J. Manag. 2015, 31, 4014091–4014094. [Google Scholar] [CrossRef]

- Kwofie, T.E.; Alhassan, A.; Botchway, E.; Afranie, I. Factors contributing towards the effectiveness of construction project teams. Int. J. Constr. Manag. 2015, 15, 170–178. [Google Scholar] [CrossRef]

- Zainul Abidin, N. Investigating the awareness and application of sustainable construction concept by Malaysian developers. Habitat Int. 2010, 34, 421–426. [Google Scholar] [CrossRef]

- Hwang, B.G.; Zhao, X.; See, Y.L.; Zhong, Y. Addressing risks in green retrofit projects: The case of Singapore. Proj. Manag. J. 2015, 46, 76–89. [Google Scholar] [CrossRef]

- Correia, I.; Saldanha-da-Gama, F. The impact of fixed and variable costs in a multi-skill project scheduling problem: An empirical study. Comput. Eng. 2014, 72, 230–238. [Google Scholar] [CrossRef]

- Arifa, F.; Lodib, S.H.; Azhar, N. Factors influencing accuracy of construction project cost estimates in Pakistan: Perception and reality. Int. J. Constr. Manag. 2015, 15, 59–70. [Google Scholar] [CrossRef]

- Pan, W.; Gibb, A.G.F.; Dainty, A.R.J. Leading UK housebuilders’ utilization of offsite construction methods. Build. Res. Inf. 2008, 36, 56–67. [Google Scholar] [CrossRef] [Green Version]

- Xin, H.; Bo, X.; Kunhui, Y.; Martin, S. Underlying knowledge of construction management consultants in China. J. Prof. Issue Eng. Educ. Pract. 2015, 142, 1–9. [Google Scholar]

- Chan, A.P.C.; Darko, A.; Ameyaw, E.E. Strategies for promoting green building technologies adoption in the construction Industry-An international study. Sustainability 2017, 9, 969. [Google Scholar] [CrossRef]

- Jarkas, A.M. Factors influencing labour productivity in Bahrain’s construction industry. Int. J. Constr. Manag. 2015, 15, 94–108. [Google Scholar] [CrossRef]

- Gao, S.; Low, S.P. Toyota way style human resource management in large Chinese construction firms: A qualitative study. Int. J. Constr. Manag. 2015, 15, 17–32. [Google Scholar] [CrossRef]

- Chan, A.P.C.; Hu, Y.; Ma, L.; Shan, M.; Le, Y. Improving the Outcomes of Public Drainage Projects through NEC3-Based Relational Contracting: Hong Kong Case Study. J. Prof. Issue Eng. Educ. Pract. 2015, 142, 1–3. [Google Scholar] [CrossRef]

- Xue, X.; Zhang, X.; Wang, L.; Skitmore, M.; Wang, Q. Analyzing Collaborative Relationships among Industrialized Construction Technology Innovation Organizations: A Combined SNA and SEM Approach. Available online: http://www.sciencedirect.com/science/article/pii/S0959652617300094 (accessed on 23 August 2017).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Stage | Factors | Source |

|---|---|---|

| design | repetitiveness, qualified civil engineers, specialized architects, poor design, design alteration, unable to freeze the design early on, standardization design, repetition ratio of PC, experience, specification of design | Arashpour [35], Polat [36], Gibb [21], Blismas [30], Pan [39], Pan [22], Isaac [18], Chiang [15], Jaillon [5], Gibb [21], Matic [54] |

| production | higher capital cost, economies of scale, mold types, turnover rate, proficiency of the workers, employee empowerment, procurement method, mass production | Asri [38], Khalili [40], Isaac [18], Poirier [44], Alazzaz [49], Mao [7], Matic [54] |

| transportation | transportation cost of PC, collaborative efforts, distance | Jaillon and Poon [41], Kim [45] |

| on-site installation | plant and production management, erection practices, labor productivity, skilled worker’s wages, scale of construction projects, construction time, complexity between joints, mismatching between on and off-site joints, experience, project management | Polat [36], Asri [38], Arashpour [33], Pan [39], Isaac [18], Gibb [21] |

| the whole process | material cost, labor cost, machinery cost and factory, mold cost, training, communication, cooperation, management mode, knowledge management, technological innovation, professional institutions | Mao [7], Arashpour [33], Jaillon [41], Polat [42], David [43], Hill [47], Gann [51] |

| Stage | Code | Factors |

|---|---|---|

| Design stage | FD1 | Coordination between designer and builder |

| FD2 | Coordination between designer and PC manufacturer | |

| FD3 | Coordination between designer and contractor | |

| FD4 | Specification and standards for prefabricated building design | |

| FD5 | Standard component catalogue of prefabricated building | |

| FD6 | Design pattern of prefabricated building | |

| FD7 | Diversity of prefabricated building structure | |

| FD8 | Related experience of designer | |

| FD9 | Collaborative capacity among professional designers | |

| FD10 | Design level of teamwork | |

| FD11 | Rationality of PC split | |

| FD12 | Node coordination between PC and on-site component | |

| FD13 | Coordination of connection nodes of PC components | |

| FD14 | Reuse ratio of standard components | |

| FD15 | Type of building structure | |

| FD16 | Third party of drawing audit organization | |

| Production and Transportation stage | FPT1 | Specification and Standards for PC production |

| FPT2 | Design plan for PC production line | |

| FPT3 | Order quantity of PC | |

| FPT4 | Capacity of production line in PC | |

| FPT5 | Depreciation of fixed assets | |

| FPT6 | Maintenance of mechanical installation | |

| FPT7 | Production technology of PC | |

| FPT8 | Technical standards system of prefabricated building | |

| FPT9 | Attrition rate of reinforcement | |

| FPT10 | Additional reinforcement due to connection points | |

| FPT11 | Curing condition to PC | |

| FPT12 | Reuse rate of PC mold | |

| FPT13 | Types and specifications in PC mold | |

| FPT14 | Scrap quantity of mold | |

| FPT15 | Number of professionals | |

| FPT16 | Efficiency of production worker | |

| FPT17 | Turnover rate of production worker | |

| FPT18 | Training cost of production workers | |

| FPT19 | Storage cost of PC in precast plant | |

| FPT20 | Selection of transport machinery used for PC | |

| FPT21 | Transportation and shipment forms of PC | |

| FPT22 | Transport distance | |

| FPT23 | Attrition rate of PC component in transportation | |

| On-site Installation stage | FC1 | Related experience of manager |

| FC2 | Coordination of all types of work on site | |

| FC3 | Operant level on installation personnel | |

| FC4 | Technical specifications and standards for PC installation | |

| FC5 | Storage condition of PC on-site | |

| FC6 | Mechanical efficiency of tower crane | |

| FC7 | Hoisting procedure of PC | |

| FC8 | Redundancy of installation process | |

| FC9 | The scale of prefabricated construction project | |

| FC10 | Rental fee of installation equipment |

| Code | N | Mean | SD | Rank |

|---|---|---|---|---|

| FD4 | 178 | 4.36 | 0.827 | 1 |

| FC1 | 178 | 4.18 | 0.871 | 2 |

| FD11 | 178 | 4.16 | 0.849 | 3 |

| FPT4 | 178 | 4.01 | 0.857 | 4 |

| FC3 | 178 | 4.00 | 0.767 | 5 |

| FPT3 | 178 | 3.99 | 0.883 | 6 |

| FD2 | 178 | 3.98 | 0.766 | 7 |

| FD9 | 178 | 3.98 | 0.809 | 8 |

| FD13 | 178 | 3.97 | 0.830 | 9 |

| FD8 | 178 | 3.92 | 0.770 | 10 |

| FC2 | 178 | 3.88 | 0.702 | 11 |

| FD12 | 178 | 3.87 | 0.840 | 12 |

| FPT2 | 178 | 3.87 | 0.755 | 13 |

| FD14 | 178 | 3.84 | 0.913 | 14 |

| FPT12 | 178 | 3.83 | 0.880 | 15 |

| FD10 | 178 | 3.79 | 0.883 | 16 |

| FPT22 | 178 | 3.71 | 0.853 | 17 |

| FPT1 | 178 | 3.69 | 0.981 | 18 |

| FC6 | 178 | 3.69 | 0.934 | 19 |

| FPT16 | 178 | 3.67 | 0.899 | 20 |

| FD1 | 178 | 3.62 | 1.120 | 21 |

| FPT7 | 178 | 3.61 | 0.790 | 22 |

| FPT13 | 178 | 3.60 | 0.860 | 23 |

| FD5 | 178 | 3.57 | 0.888 | 24 |

| FD3 | 178 | 3.57 | 0.996 | 25 |

| FPT8 | 178 | 3.56 | 0.938 | 26 |

| FD6 | 178 | 3.49 | 0.891 | 27 |

| FC8 | 178 | 3.49 | 0.811 | 28 |

| FPT14 | 178 | 3.48 | 0.903 | 29 |

| FC7 | 178 | 3.45 | 0.902 | 30 |

| FC9 | 178 | 3.44 | 0.901 | 31 |

| FD7 | 178 | 3.42 | 0.937 | 32 |

| FC4 | 178 | 3.42 | 1.006 | 33 |

| FPT20 | 178 | 3.35 | 0.928 | 34 |

| FPT15 | 178 | 3.34 | 0.962 | 35 |

| FPT21 | 178 | 3.30 | 0.882 | 36 |

| FPT19 | 178 | 3.26 | 0.844 | 37 |

| FD15 | 178 | 3.22 | 0.911 | 38 |

| FPT6 | 178 | 3.21 | 0.895 | 39 |

| FC10 | 178 | 3.21 | 0.920 | 40 |

| FPT11 | 178 | 3.19 | 0.937 | 41 |

| FPT23 | 178 | 3.16 | 0.961 | 42 |

| FPT17 | 178 | 3.13 | 0.904 | 43 |

| FPT5 | 178 | 3.12 | 0.972 | 44 |

| FC5 | 178 | 3.12 | 0.807 | 45 |

| FPT10 | 178 | 3.10 | 0.927 | 46 |

| FPT9 | 178 | 3.09 | 0.970 | 47 |

| FPT18 | 178 | 3.09 | 0.982 | 48 |

| FD16 | 178 | 3.02 | 1.104 | 49 |

| Code | Levene’s Test for Equality of Variances | Mean Value | t-Test for Equality of Means | Significant Difference (N/Y) | ||||

|---|---|---|---|---|---|---|---|---|

| F | Sig. | Total | Series 1 (N) | Series 2 (Y) | t | Sig. | ||

| FD1 | 12.286 | 0.001 | 3.618 | 4.120 | 3.422 | 4.372 | 0.000 | Y |

| FD2 | 5.959 | 0.016 | 3.978 | 3.920 | 4.000 | −0.584 | 0.561 | N |

| FD3 | 0.221 | 0.639 | 3.573 | 3.800 | 3.484 | 1.915 | 0.057 | N |

| FD4 | 0.299 | 0.585 | 4.360 | 4.320 | 4.375 | −0.398 | 0.691 | N |

| FD5 | 0.537 | 0.465 | 3.573 | 3.600 | 3.563 | 0.253 | 0.801 | N |

| FD6 | 1.202 | 0.275 | 3.494 | 3.480 | 3.500 | −0.134 | 0.893 | N |

| FD7 | 0.044 | 0.834 | 3.416 | 3.640 | 3.328 | 2.014 | 0.046 | Y |

| FD8 | 0.108 | 0.743 | 3.921 | 4.120 | 3.844 | 2.174 | 0.031 | Y |

| FD9 | 1.229 | 0.269 | 3.978 | 4.160 | 3.906 | 1.894 | 0.060 | N |

| FD10 | 10.341 | 0.002 | 3.787 | 4.120 | 3.656 | 3.581 | 0.001 | Y |

| FD11 | 0.308 | 0.579 | 4.157 | 4.080 | 4.188 | −0.758 | 0.449 | N |

| FD12 | 5.178 | 0.024 | 3.865 | 3.720 | 3.922 | −1.278 | 0.205 | N |

| FD13 | 24.145 | 0.000 | 3.966 | 3.840 | 4.016 | −1.005 | 0.319 | N |

| FD14 | 4.508 | 0.035 | 3.843 | 3.840 | 3.844 | −0.022 | 0.982 | N |

| FD15 | 4.306 | 0.039 | 3.225 | 3.640 | 3.063 | 3.776 | 0.000 | Y |

| FD16 | 6.100 | 0.014 | 3.022 | 3.200 | 2.953 | 1.201 | 0.234 | N |

| FPT1 | 1.398 | 0.239 | 3.685 | 4.160 | 3.500 | 4.221 | 0.000 | Y |

| FPT2 | 0.551 | 0.459 | 3.865 | 4.080 | 3.781 | 2.406 | 0.017 | Y |

| FPT3 | 9.215 | 0.003 | 3.989 | 3.640 | 4.125 | −3.018 | 0.004 | Y |

| FPT4 | 10.856 | 0.001 | 4.011 | 3.480 | 4.219 | −4.957 | 0.000 | Y |

| FPT5 | 12.510 | 0.001 | 3.124 | 3.160 | 3.109 | 0.277 | 0.783 | N |

| FPT6 | 0.370 | 0.544 | 3.213 | 3.160 | 3.234 | −0.497 | 0.620 | N |

| FPT7 | 0.167 | 0.684 | 3.607 | 3.840 | 3.516 | 2.498 | 0.013 | Y |

| FPT8 | 3.838 | 0.052 | 3.562 | 3.960 | 3.406 | 3.661 | 0.000 | Y |

| FPT9 | 11.054 | 0.001 | 3.090 | 3.200 | 3.047 | 0.851 | 0.398 | N |

| FPT10 | 15.310 | 0.000 | 3.101 | 3.200 | 3.063 | 0.758 | 0.451 | N |

| FPT11 | 7.259 | 0.008 | 3.191 | 3.320 | 3.141 | 1.062 | 0.291 | N |

| FPT12 | 17.442 | 0.000 | 3.831 | 3.600 | 3.922 | −1.988 | 0.051 | N |

| FPT13 | 1.047 | 0.308 | 3.596 | 3.440 | 3.656 | −1.513 | 0.132 | N |

| FPT14 | 2.010 | 0.158 | 3.483 | 3.320 | 3.547 | −1.511 | 0.132 | N |

| FPT15 | 11.349 | 0.001 | 3.337 | 3.200 | 3.391 | −1.020 | 0.312 | N |

| FPT16 | 5.788 | 0.017 | 3.674 | 3.200 | 3.859 | −4.214 | 0.000 | Y |

| FPT17 | 0.020 | 0.888 | 3.135 | 2.960 | 3.203 | −1.619 | 0.107 | N |

| FPT18 | 9.393 | 0.003 | 3.090 | 3.560 | 2.906 | 3.834 | 0.000 | Y |

| FPT19 | 0.917 | 0.339 | 3.258 | 3.280 | 3.250 | 0.213 | 0.832 | N |

| FPT20 | 0.047 | 0.828 | 3.348 | 3.480 | 3.297 | 1.185 | 0.238 | N |

| FPT21 | 3.038 | 0.083 | 3.303 | 3.360 | 3.281 | 0.534 | 0.594 | N |

| FPT22 | 3.319 | 0.070 | 3.708 | 3.440 | 3.813 | −2.663 | 0.008 | Y |

| FPT23 | 8.282 | 0.005 | 3.157 | 3.320 | 3.094 | 1.415 | 0.159 | N |

| FC1 | 0.036 | 0.849 | 4.180 | 3.920 | 4.281 | −2.525 | 0.012 | Y |

| FC2 | 8.138 | 0.005 | 3.876 | 3.760 | 3.922 | −1.249 | 0.216 | N |

| FC3 | 0.012 | 0.911 | 4.000 | 4.000 | 4.000 | 0.000 | 1.000 | N |

| FC4 | 7.616 | 0.006 | 3.416 | 3.760 | 3.281 | 2.578 | 0.012 | Y |

| FC5 | 0.674 | 0.413 | 3.124 | 3.000 | 3.172 | −1.279 | 0.202 | N |

| FC6 | 10.619 | 0.001 | 3.685 | 3.320 | 3.828 | −2.967 | 0.004 | Y |

| FC7 | 2.197 | 0.140 | 3.449 | 3.640 | 3.375 | 1.772 | 0.078 | N |

| FC8 | 0.038 | 0.845 | 3.494 | 3.520 | 3.484 | 0.263 | 0.793 | N |

| FC9 | 0.184 | 0.668 | 3.438 | 3.440 | 3.438 | 0.017 | 0.987 | N |

| FC10 | 7.405 | 0.007 | 3.213 | 3.160 | 3.234 | −0.443 | 0.659 | N |

| Code | Test of Homogeneity of Variances | Mean Value | One-Way-Test for Equality of Means | Significant Difference (N/Y) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Levene Statistic | Sig. | Total | Series 1 | Series 2 | Series 3 | Series 4 | Series 5 | Series 6 | F | Sig. | ||

| FD1 | 0.718 | 0.610 | 3.618 | 3.407 | 3.429 | 3.800 | 3.786 | 3.722 | 3.909 | 1.083 | 0.372 | N |

| FD2 | 0.636 | 0.673 | 3.978 | 3.926 | 3.929 | 3.600 | 4.357 | 3.944 | 3.909 | 2.039 | 0.076 | N |

| FD3 | 1.826 | 0.110 | 3.573 | 3.556 | 3.643 | 3.200 | 3.857 | 3.222 | 3.909 | 2.237 | 0.053 | N |

| FD4 | 0.732 | 0.601 | 4.360 | 4.407 | 4.500 | 4.400 | 4.357 | 4.111 | 4.455 | 0.908 | 0.477 | N |

| FD5 | 7.454 | 0.000 | 3.573 | 3.481 | 3.929 | 3.400 | 3.500 | 3.444 | 3.727 | 1.427 | 0.217 | N |

| FD6 | 1.258 | 0.284 | 3.494 | 3.630 | 3.643 | 3.000 | 3.429 | 3.278 | 3.636 | 1.616 | 0.158 | N |

| FD7 | 2.756 | 0.020 | 3.416 | 3.296 | 3.571 | 3.400 | 3.643 | 3.278 | 3.455 | 0.820 | 0.537 | N |

| FD8 | 0.578 | 0.717 | 3.921 | 3.741 | 3.857 | 3.400 | 4.143 | 3.889 | 4.455 | 4.553 | 0.001 | Y |

| FD9 | 1.440 | 0.212 | 3.978 | 3.741 | 4.000 | 4.000 | 4.000 | 4.167 | 4.182 | 1.638 | 0.153 | N |

| FD10 | 2.629 | 0.026 | 3.787 | 3.630 | 3.571 | 3.800 | 3.929 | 3.889 | 4.091 | 1.458 | 0.206 | N |

| FD11 | 1.586 | 0.166 | 4.157 | 3.889 | 4.214 | 3.800 | 4.643 | 4.389 | 3.909 | 4.633 | 0.001 | Y |

| FD12 | 2.051 | 0.074 | 3.865 | 3.852 | 3.786 | 3.600 | 3.929 | 3.722 | 4.273 | 1.554 | 0.176 | N |

| FD13 | 9.571 | 0.000 | 3.966 | 3.963 | 3.929 | 4.000 | 4.000 | 3.778 | 4.273 | 0.996 | 0.422 | N |

| FD14 | 6.249 | 0.000 | 3.843 | 3.741 | 4.071 | 3.400 | 4.000 | 3.722 | 4.000 | 1.393 | 0.229 | N |

| FD15 | 0.633 | 0.675 | 3.225 | 3.222 | 3.357 | 3.400 | 3.214 | 3.000 | 3.364 | 0.727 | 0.604 | N |

| FD16 | 0.580 | 0.715 | 3.022 | 3.037 | 3.000 | 2.600 | 3.500 | 2.722 | 3.091 | 1.943 | 0.090 | N |

| FPT1 | 1.625 | 0.156 | 3.685 | 3.407 | 3.714 | 4.000 | 3.429 | 3.889 | 4.182 | 3.067 | 0.011 | Y |

| FPT2 | 3.396 | 0.006 | 3.865 | 3.815 | 3.714 | 4.200 | 3.857 | 3.722 | 4.273 | 2.289 | 0.048 | Y |

| FPT3 | 2.751 | 0.020 | 3.989 | 3.963 | 4.071 | 4.600 | 4.429 | 3.778 | 3.455 | 4.919 | 0.000 | Y |

| FPT4 | 3.409 | 0.006 | 4.011 | 4.000 | 4.286 | 4.400 | 4.214 | 3.778 | 3.636 | 2.816 | 0.018 | Y |

| FPT5 | 5.120 | 0.000 | 3.124 | 2.963 | 3.000 | 2.800 | 3.714 | 3.222 | 2.909 | 3.142 | 0.010 | Y |

| FPT6 | 0.786 | 0.561 | 3.213 | 3.111 | 3.286 | 3.600 | 3.643 | 3.000 | 3.000 | 2.611 | 0.026 | Y |

| FPT7 | 2.878 | 0.016 | 3.607 | 3.593 | 3.571 | 3.600 | 3.357 | 3.611 | 4.000 | 1.697 | 0.138 | N |

| FPT8 | 2.188 | 0.058 | 3.562 | 3.630 | 3.357 | 3.000 | 3.571 | 3.500 | 4.000 | 2.094 | 0.068 | N |

| FPT9 | 4.220 | 0.001 | 3.090 | 3.185 | 2.929 | 3.000 | 3.214 | 2.889 | 3.273 | 0.830 | 0.530 | N |

| FPT10 | 3.879 | 0.002 | 3.101 | 3.296 | 3.000 | 3.000 | 3.214 | 2.722 | 3.273 | 2.066 | 0.072 | N |

| FPT11 | 3.450 | 0.005 | 3.191 | 3.111 | 3.000 | 3.000 | 3.571 | 2.944 | 3.636 | 2.964 | 0.014 | Y |

| FPT12 | 3.890 | 0.002 | 3.831 | 3.741 | 3.857 | 4.000 | 4.000 | 3.833 | 3.727 | 0.453 | 0.810 | N |

| FPT13 | 2.213 | 0.055 | 3.596 | 3.593 | 3.429 | 3.600 | 4.000 | 3.556 | 3.364 | 1.828 | 0.110 | N |

| FPT14 | 1.275 | 0.277 | 3.483 | 3.556 | 3.643 | 3.400 | 3.643 | 3.333 | 3.182 | 1.128 | 0.347 | N |

| FPT15 | 1.628 | 0.155 | 3.337 | 3.148 | 3.357 | 2.800 | 3.500 | 3.444 | 3.636 | 1.756 | 0.125 | N |

| FPT16 | 5.227 | 0.000 | 3.674 | 3.815 | 3.571 | 3.800 | 4.071 | 3.333 | 3.455 | 2.916 | 0.015 | Y |

| FPT17 | 0.877 | 0.498 | 3.135 | 3.296 | 3.214 | 2.800 | 3.214 | 2.889 | 3.091 | 1.257 | 0.285 | N |

| FPT18 | 1.871 | 0.102 | 3.090 | 3.148 | 3.071 | 3.000 | 2.929 | 2.833 | 3.636 | 2.129 | 0.064 | N |

| FPT19 | 2.815 | 0.018 | 3.258 | 3.185 | 3.214 | 3.600 | 3.143 | 3.278 | 3.455 | 0.765 | 0.576 | N |

| FPT20 | 4.319 | 0.001 | 3.348 | 3.370 | 3.429 | 3.800 | 3.071 | 3.222 | 3.545 | 1.366 | 0.239 | N |

| FPT21 | 3.001 | 0.013 | 3.303 | 3.296 | 3.143 | 3.800 | 3.071 | 3.389 | 3.455 | 1.422 | 0.219 | N |

| FPT22 | 4.196 | 0.001 | 3.708 | 3.704 | 3.714 | 4.200 | 4.000 | 3.500 | 3.455 | 2.212 | 0.055 | N |

| FPT23 | 2.132 | 0.064 | 3.157 | 3.111 | 3.214 | 3.600 | 3.143 | 2.889 | 3.455 | 1.471 | 0.202 | N |

| FC1 | 1.242 | 0.291 | 4.180 | 4.074 | 4.143 | 4.600 | 4.500 | 4.222 | 3.818 | 2.244 | 0.052 | N |

| FC2 | 2.397 | 0.039 | 3.876 | 3.815 | 3.786 | 4.200 | 4.071 | 3.778 | 3.909 | 1.191 | 0.316 | N |

| FC3 | 2.519 | 0.031 | 4.000 | 4.000 | 3.929 | 4.600 | 4.143 | 3.667 | 4.182 | 3.275 | 0.008 | Y |

| FC4 | 0.972 | 0.436 | 3.416 | 3.296 | 3.429 | 2.800 | 3.643 | 3.389 | 3.727 | 1.643 | 0.151 | N |

| FC5 | 2.341 | 0.044 | 3.124 | 3.111 | 3.143 | 3.200 | 3.071 | 3.000 | 3.364 | 0.598 | 0.701 | N |

| FC6 | 1.831 | 0.109 | 3.685 | 3.926 | 3.429 | 4.000 | 3.714 | 3.500 | 3.545 | 1.794 | 0.116 | N |

| FC7 | 0.433 | 0.825 | 3.449 | 3.519 | 3.286 | 3.200 | 3.357 | 3.278 | 4.000 | 2.456 | 0.035 | Y |

| FC8 | 0.282 | 0.922 | 3.494 | 3.704 | 3.571 | 3.200 | 3.357 | 3.222 | 3.636 | 2.211 | 0.055 | N |

| FC9 | 1.816 | 0.112 | 3.438 | 3.630 | 3.286 | 3.600 | 3.429 | 3.278 | 3.364 | 0.970 | 0.438 | N |

| FC10 | 0.942 | 0.456 | 3.213 | 3.222 | 3.214 | 3.200 | 3.214 | 2.944 | 3.636 | 1.571 | 0.171 | N |

| Code | Test of Homogeneity of Variances | Mean Value | One-Way-Test for Equality of Means | Significant Difference (N/Y) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Levene Statistic | Sig. | Total | Group 1 | Group 2 | Group 3 | Group 4 | F | Sig. | ||

| FD1 | 4.507 | 0.005 | 3.618 | 3.111 | 3.542 | 4.125 | 3.667 | 2.520 | 0.060 | N |

| FD2 | 1.984 | 0.118 | 3.978 | 4.111 | 3.875 | 4.000 | 4.000 | 0.497 | 0.685 | N |

| FD3 | 0.873 | 0.456 | 3.573 | 3.556 | 3.208 | 3.500 | 3.771 | 3.589 | 0.015 | Y |

| FD4 | 3.480 | 0.017 | 4.360 | 4.778 | 4.292 | 4.375 | 4.313 | 1.772 | 0.154 | N |

| FD5 | 0.805 | 0.492 | 3.573 | 3.889 | 3.583 | 3.750 | 3.479 | 1.338 | 0.264 | N |

| FD6 | 1.523 | 0.210 | 3.494 | 3.556 | 3.625 | 3.750 | 3.375 | 1.395 | 0.246 | N |

| FD7 | 0.620 | 0.603 | 3.416 | 3.556 | 3.500 | 4.500 | 3.167 | 11.378 | 0.000 | Y |

| FD8 | 1.520 | 0.211 | 3.921 | 4.000 | 3.792 | 4.125 | 3.938 | 0.902 | 0.441 | N |

| FD9 | 3.255 | 0.023 | 3.978 | 4.222 | 4.042 | 4.375 | 3.833 | 3.055 | 0.030 | Y |

| FD10 | 0.919 | 0.433 | 3.787 | 3.778 | 3.542 | 4.125 | 3.854 | 2.251 | 0.084 | N |

| FD11 | 0.365 | 0.778 | 4.157 | 4.000 | 4.208 | 4.250 | 4.146 | 0.329 | 0.804 | N |

| FD12 | 0.675 | 0.568 | 3.865 | 4.111 | 3.542 | 4.500 | 3.875 | 6.498 | 0.000 | Y |

| FD13 | 4.448 | 0.005 | 3.966 | 3.667 | 3.667 | 4.375 | 4.104 | 5.428 | 0.001 | Y |

| FD14 | 5.022 | 0.002 | 3.843 | 3.556 | 4.000 | 3.875 | 3.813 | 1.112 | 0.346 | N |

| FD15 | 0.593 | 0.620 | 3.225 | 2.778 | 3.167 | 4.000 | 3.208 | 5.817 | 0.001 | Y |

| FD16 | 0.451 | 0.717 | 3.022 | 3.000 | 2.792 | 4.125 | 2.958 | 6.717 | 0.000 | Y |

| FPT1 | 2.366 | 0.073 | 3.685 | 3.444 | 3.667 | 4.375 | 3.625 | 3.242 | 0.023 | Y |

| FPT2 | 2.119 | 0.100 | 3.865 | 3.889 | 3.750 | 4.125 | 3.875 | 1.017 | 0.387 | N |

| FPT3 | 0.102 | 0.959 | 3.989 | 4.333 | 4.042 | 3.875 | 3.917 | 1.279 | 0.283 | N |

| FPT4 | 1.244 | 0.295 | 4.011 | 4.667 | 3.917 | 4.250 | 3.896 | 5.019 | 0.002 | Y |

| FPT5 | 0.133 | 0.940 | 3.124 | 3.111 | 3.083 | 3.625 | 3.063 | 1.589 | 0.194 | N |

| FPT6 | 2.473 | 0.063 | 3.213 | 3.222 | 3.125 | 4.000 | 3.125 | 4.887 | 0.003 | Y |

| FPT7 | 4.514 | 0.004 | 3.607 | 3.556 | 3.542 | 4.500 | 3.500 | 8.493 | 0.000 | Y |

| FPT8 | 3.141 | 0.027 | 3.562 | 3.444 | 3.458 | 4.500 | 3.479 | 6.407 | 0.000 | Y |

| FPT9 | 4.516 | 0.004 | 3.090 | 3.111 | 2.917 | 3.875 | 3.042 | 4.315 | 0.006 | Y |

| FPT10 | 6.352 | 0.000 | 3.101 | 3.111 | 2.833 | 3.750 | 3.125 | 4.182 | 0.007 | Y |

| FPT11 | 1.466 | 0.226 | 3.191 | 2.889 | 2.958 | 4.000 | 3.229 | 6.125 | 0.001 | Y |

| FPT12 | 1.766 | 0.155 | 3.831 | 3.778 | 3.875 | 4.000 | 3.792 | 0.319 | 0.812 | N |

| FPT13 | 1.572 | 0.198 | 3.596 | 3.556 | 3.583 | 4.000 | 3.542 | 1.329 | 0.267 | N |

| FPT14 | 0.372 | 0.773 | 3.483 | 3.444 | 3.625 | 3.875 | 3.354 | 2.100 | 0.102 | N |

| FPT15 | 2.506 | 0.061 | 3.337 | 3.333 | 3.208 | 3.875 | 3.313 | 2.009 | 0.114 | N |

| FPT16 | 8.471 | 0.000 | 3.674 | 4.333 | 3.458 | 3.625 | 3.667 | 4.405 | 0.005 | Y |

| FPT17 | 1.364 | 0.256 | 3.135 | 3.556 | 3.000 | 3.625 | 3.042 | 3.725 | 0.012 | Y |

| FPT18 | 0.162 | 0.922 | 3.090 | 3.111 | 2.958 | 3.500 | 3.083 | 1.227 | 0.301 | N |

| FPT19 | 2.736 | 0.045 | 3.258 | 3.333 | 3.000 | 4.250 | 3.208 | 10.467 | 0.000 | Y |

| FPT20 | 0.845 | 0.471 | 3.348 | 3.333 | 3.375 | 3.875 | 3.250 | 2.132 | 0.098 | N |

| FPT21 | 0.977 | 0.405 | 3.303 | 3.111 | 3.250 | 4.125 | 3.229 | 5.607 | 0.001 | Y |

| FPT22 | 2.836 | 0.040 | 3.708 | 4.111 | 3.542 | 3.875 | 3.688 | 2.216 | 0.088 | N |

| FPT23 | 3.596 | 0.015 | 3.157 | 3.000 | 3.083 | 4.000 | 3.083 | 4.838 | 0.003 | Y |

| FC1 | 0.912 | 0.436 | 4.180 | 4.667 | 4.125 | 4.250 | 4.104 | 2.262 | 0.083 | N |

| FC2 | 0.989 | 0.399 | 3.876 | 4.111 | 3.750 | 4.250 | 3.833 | 2.910 | 0.036 | Y |

| FC3 | 1.243 | 0.296 | 4.000 | 4.111 | 3.833 | 4.375 | 4.000 | 2.203 | 0.089 | N |

| FC4 | 3.586 | 0.015 | 3.416 | 3.111 | 3.500 | 4.375 | 3.271 | 6.776 | 0.000 | Y |

| FC5 | 1.531 | 0.208 | 3.124 | 3.111 | 2.958 | 3.625 | 3.125 | 2.815 | 0.041 | Y |

| FC6 | 3.452 | 0.018 | 3.685 | 4.000 | 3.708 | 4.000 | 3.563 | 1.877 | 0.135 | N |

| FC7 | 0.329 | 0.805 | 3.449 | 3.556 | 3.333 | 3.875 | 3.417 | 1.593 | 0.193 | N |

| FC8 | 0.562 | 0.641 | 3.494 | 3.333 | 3.542 | 3.750 | 3.458 | 0.882 | 0.452 | N |

| FC9 | 5.486 | 0.001 | 3.438 | 3.333 | 3.375 | 4.000 | 3.396 | 2.355 | 0.074 | N |

| FC10 | 1.607 | 0.189 | 3.213 | 2.889 | 3.167 | 3.625 | 3.229 | 1.892 | 0.133 | N |

| Function | Context | Content |

|---|---|---|

| top manager | industry chain | technology, management, cooperation of team exterior and team inner, consciousness and human subjective initiative |

| middle manager | enterprise | technology, management, cooperation of team exterior and team inner, consciousness |

| first-line manager | project | technology, management on-site, cooperation within a team |

| technician | practical problem | technology, cooperation of teamwork, and practical problems |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xue, H.; Zhang, S.; Su, Y.; Wu, Z. Factors Affecting the Capital Cost of Prefabrication—A Case Study of China. Sustainability 2017, 9, 1512. https://doi.org/10.3390/su9091512

Xue H, Zhang S, Su Y, Wu Z. Factors Affecting the Capital Cost of Prefabrication—A Case Study of China. Sustainability. 2017; 9(9):1512. https://doi.org/10.3390/su9091512

Chicago/Turabian StyleXue, Hong, Shoujian Zhang, Yikun Su, and Zezhou Wu. 2017. "Factors Affecting the Capital Cost of Prefabrication—A Case Study of China" Sustainability 9, no. 9: 1512. https://doi.org/10.3390/su9091512