Corporate Social Responsibility Drivers and Barriers According to Managers’ Perception; Evidence from Spanish Firms

Abstract

:1. Introduction

2. Theoretical Background, Materials and Methods

2.1. Theoretical Background and Theories about Drivers/Barriers

2.1.1. Two Perspectives of CSR Drivers/Barriers

2.1.2. Drivers of and Barriers to CSR Strategies: Content Analysis

- (1)

- Integrating ethics: The managerial idea that CSR implies a new management idea [41], which integrates ethical standards [42] into the firm’s management and organizational culture [33,43] and corporate governance procedures [44] is the most commonly cited in 31.9% of the papers. The ethical values and preferences of top management [45,46], culture beliefs [47] and CEO characteristics [39], would thus be aspects with an impact on the degree of CSR development in an organization.

- (2)

- Sustainable development: CSR may be seen as sharing normative goals with the concept of sustainable development [48]. The second most cited concept, with a frequency of 18.7%, is that managers believe that, in general, CSR integrates aspects related to social–environmental–economic performance or sustainability [49,50,51]. This would include strategic approaches to CSR and commitment to earning profits or the need for a better bottom-line [52], the generation of reliable sustainable CSR [53], the adoption of a more long-term perspective or a realistic view of CSR [54], among other aspects.

- (3)

- Organizational commitment to transparency (stakeholder confidence): The managerial idea that CSR implies a new organizational commitment to transparency and stakeholder confidence is found with a frequency of 13.2% in the reviewed literature. Specific aspects such as risk management [55], conflict-resolution [56], responsibilities towards stakeholder activism [57] and transparency [58,59] could be contemplated here.

- (4)

- (5)

- Public relations exercise: The fact that managers believe that CSR is an image strategy rather than a true strategic conviction of the firm is found in 8.8% of the papers, with specific references to aspects such as an exercise in public relations and media campaigns [52].

- (6)

- (1)

- Stakeholder pressure: Some kind of pressure from the relationship with stakeholders [4,34] and from stakeholder dialogue [89], from one or several stakeholders including NGOs [90], appears to be the most commonly mentioned aspect in favor of CSR in the organization, cited in 25.8% of the papers. The objective drivers cited include social demands [48] and stakeholders’ expectations and pressures [45].

- (2)

- Institutional framework: There is increasing top-down pressure impacting CSR [52]. Institutional issues like public and private regulations, rules regarding corporate behavior and associative behavior among corporations themselves [25,91] are the second most commonly cited objective CSR drivers, cited in 15.9% of our sample. Highlighted aspects include the country-level institutional factors [92], the role that governments can play [93], institutional pressure [10,94] and developing an institutional framework [8].

- (3)

- Reputation management: CSR has a positive effect on corporate reputation [36], and lowering the cost of capital [95], on loyalty [29] with the integration of the organization into its host community [27] on improving firms’ reputations in relation to their stakeholders [96,97] and their performance in the eyes of governments [98]. This is also one of the most commonly mentioned aspects as a CSR driver, cited in 13.6% of the papers.

- (4)

- The impact of leading corporations [17] based on aspects such as visibility, the publication of sustainability reports [90], foreign partners [86], international diversification [99], etc., is cited in 6.8%, and aspects in favor of CSR related to sectorial trends and private sector-led initiatives [100] are cited in 6.1%.

- (5)

- Availability of resources (financial, time-related and human resources): Economic factors such as lack of economic resources [100], a difficult economic situation [86], a situation in which it is difficult to show any significant positive correlation between CSR and the “bottom line” [51], etc., are most commonly cited as barriers, with 9.1% frequency. They are followed by lack of structure and human resources [31] with 7.6%, and lack of time-related resources [37], with 6.1%.

- (6)

- (7)

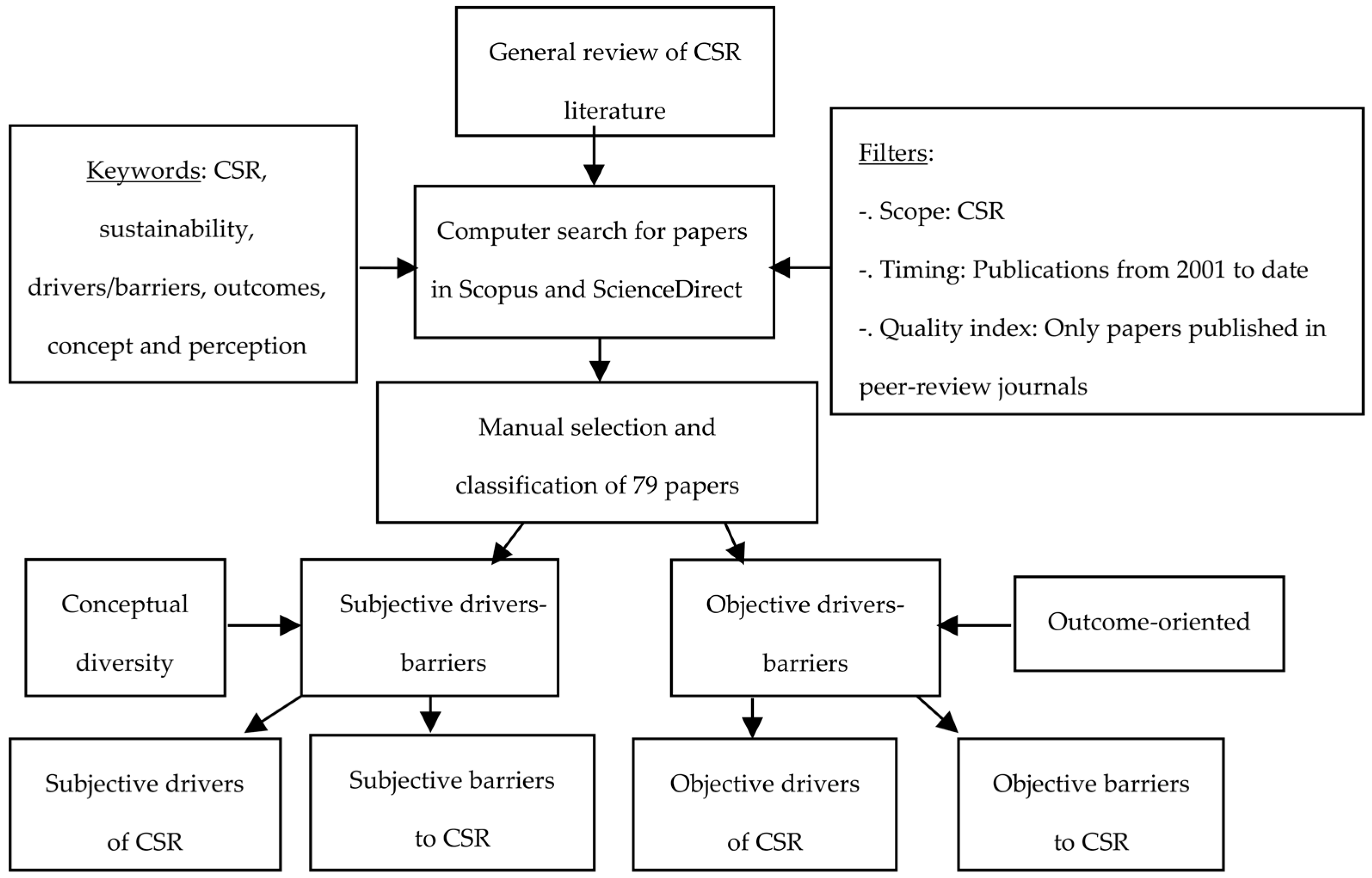

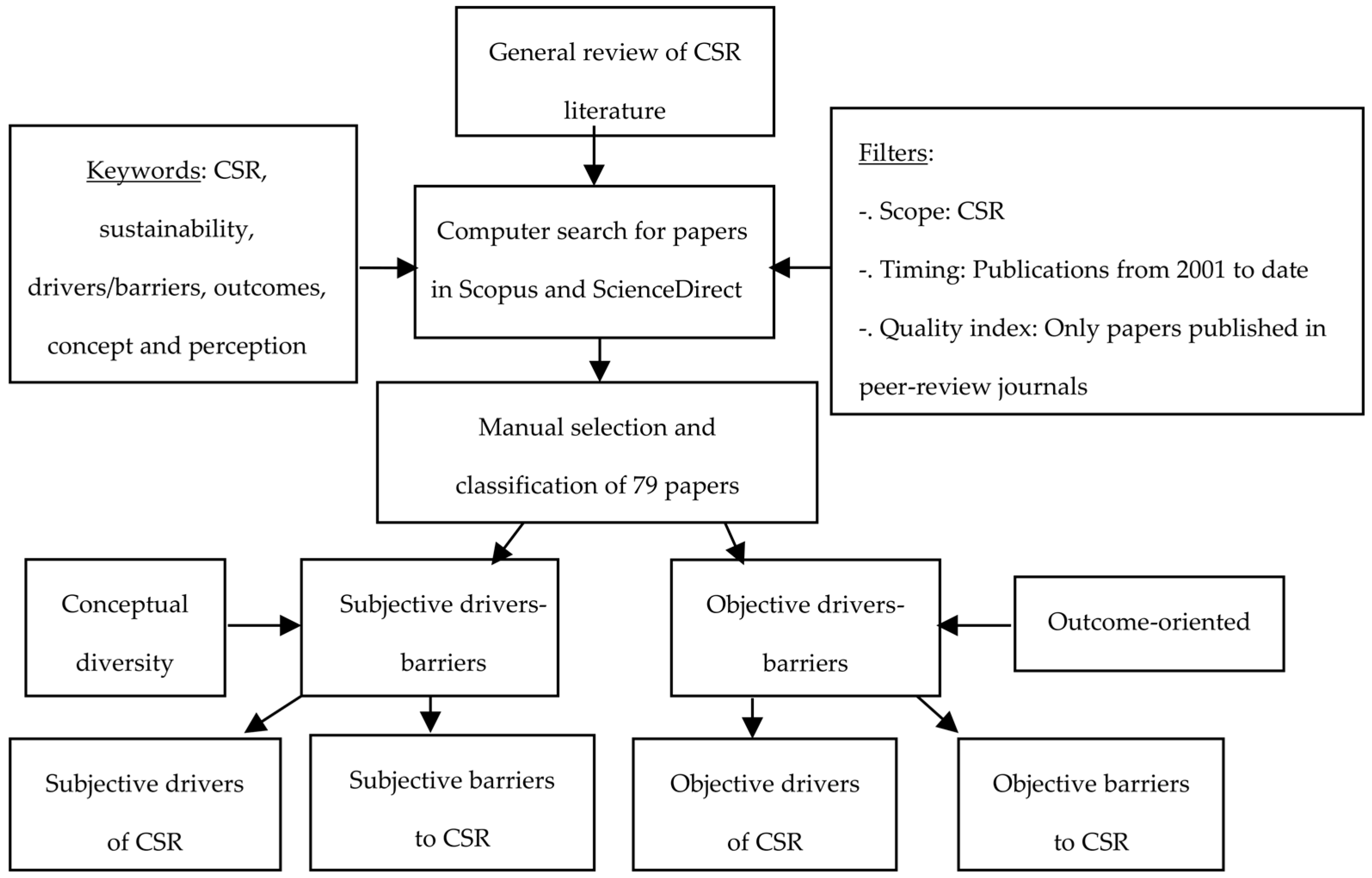

2.2. Data and Methods

2.2.1. Methodology

2.2.2. Sources of Information and Sample of Firms

2.2.3. Description of the Variables

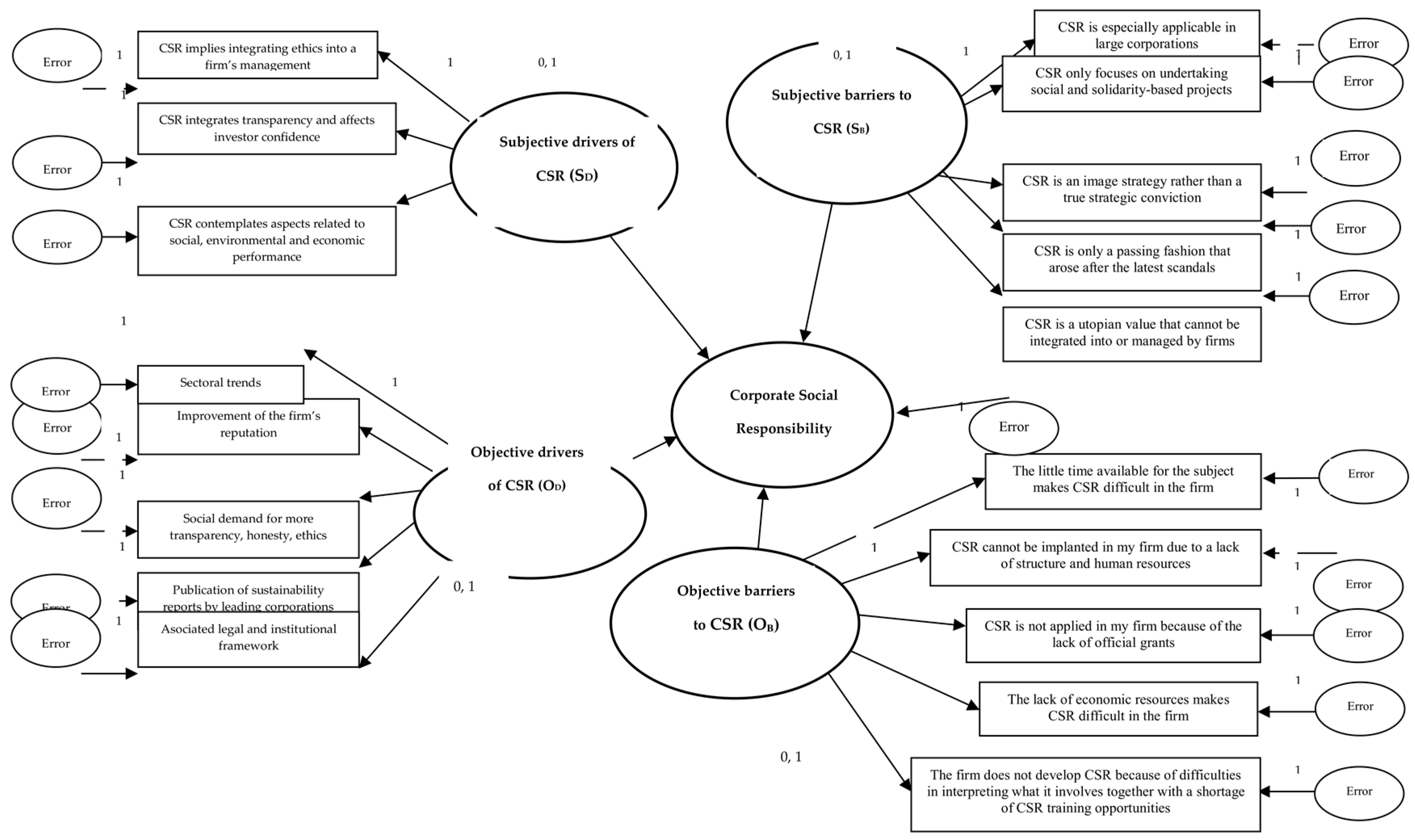

- (1)

- Measuring CSR: The evaluation of each firm’s CSR was carried out following the methodology described in Agudo et al. [133] and based on the model proposed by Carroll [40]. The former authors use a set of 53 items, on a 0 to 10 continuous scale, that cover aspects of the different types of responsibility considered by Carroll [40] and later researchers [66,134,135] related to the different stakeholder groups to which measurements of the organization’s responsibility apply. Agudo et al. [133] propose a second-order factor model where the 53 items are grouped in 13 first-order factors and, finally, in a single second order factor denoted here as “Corporate Social Responsibility (FCSR)”. The construct finally obtained as the second-order factor thus summarizes the information contained in the variables related to the organization’s activities and commitments related to CSR. The FCSR determines the organization’s CSR, the variable now estimated for the rest of the study.

- (2)

- Measuring factors determining CSR initiatives: Following the previous literature, we chose a set of variables that enabled objective measurement of the extent to which managers are aware of the favorable or unfavorable conditions for the development of CSR in their organization, and their conception of CSR. We thus consider eight subjective variables related to management’s conception of CSR and 10 objective conditions for the development of CSR in the organization. Measurement of the 18 variables was based on a seven-point Likert scale, according to the degree of agreement with the issue represented by the variable in the firm, where 1 represents “agree completely” and 7 “disagree completely”. All computations were made using SPSS 15.0.

2.2.4. Structural Model

3. Empirical Results

3.1. Estimation of the Model

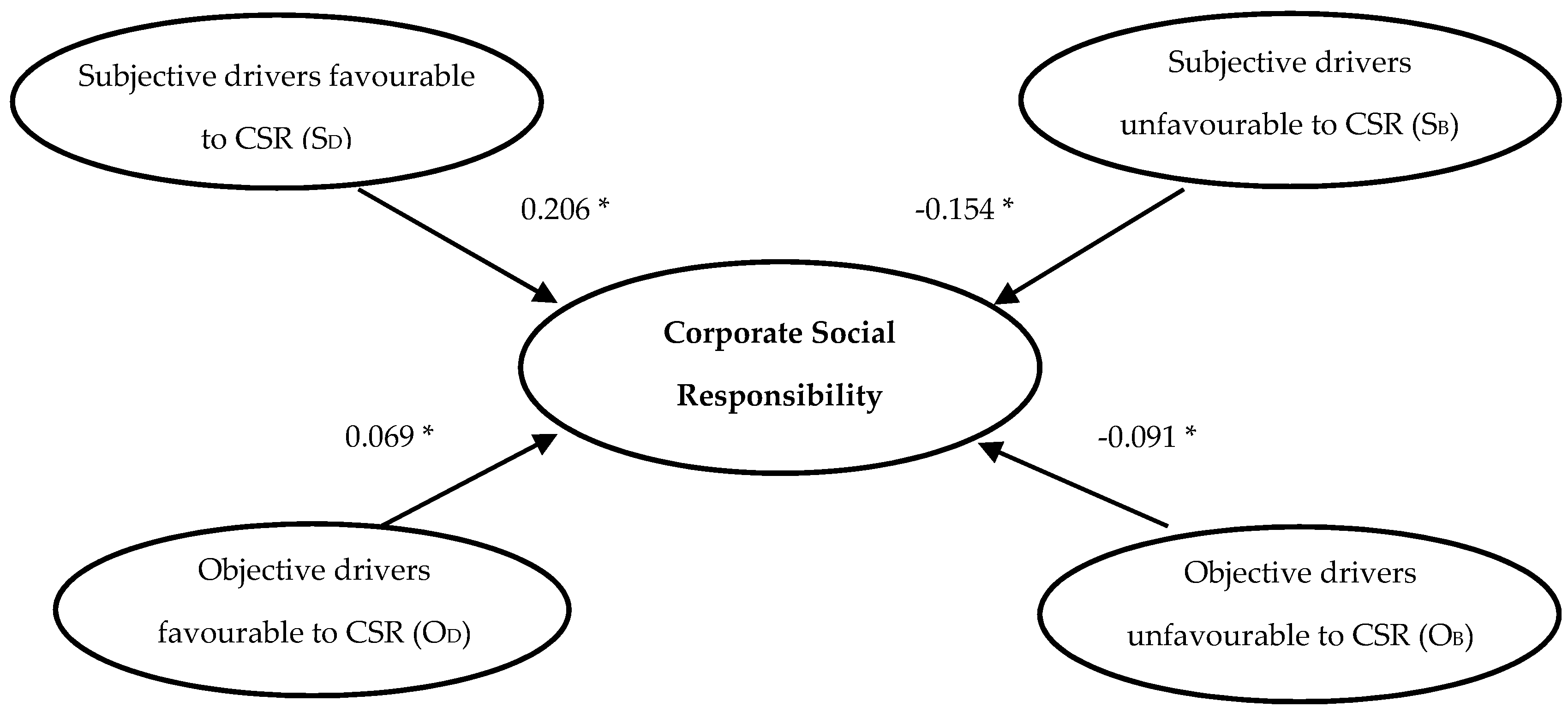

3.2. Joint Analysis of Subjective and Objective Drivers of CSR

4. Discussion

5. Conclusions

5.1. General Conclusions

5.2. Managerial Implications

5.3. Limitations and Directions for Future Research

Acknowledgments

Author Contributions

Conflicts of Interest

References and Notes

- Lo, S.-F.; Sheu, H.-J. Is corporate sustainability a value-increasing strategy for business? Corp. Gov. Int. Rev. 2007, 15, 345–358. [Google Scholar] [CrossRef]

- Eweje, G. Emerging Trends in CSR and Sustainability. Bus. Strategy Environ. 2015, 24, 601–603. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Jo, H. Legal vs. Normative CSR: Differential impact on analyst dispersion, stock return volatility, cost of capital, and firm value. J. Bus. Ethics 2015, 128, 1–20. [Google Scholar] [CrossRef]

- Fabrizi, M.; Mallin, C.; Michelon, G. The role of CEO’s personal incentives in driving corporate social responsibility. J. Bus. Ethics 2014, 124, 311–326. [Google Scholar] [CrossRef] [Green Version]

- Hahn, R. ISO 26000 and the standardization of strategic management processes for sustainability and corporate social responsibility. Bus. Strategy Environ. 2013, 22, 442–455. [Google Scholar] [CrossRef]

- Govindasamy, V.; Suresh, K. Exploring approaches to drivers and barriers of corporate social responsibility implementation in academic literature. EDP Sci. 2017, 33, 1–8. [Google Scholar] [CrossRef]

- Zientara, P. Socioemotional wealth and corporate social responsibility: A critical analysis. J. Bus. Ethics 2017, 144, 185–199. [Google Scholar] [CrossRef]

- Matten, D.; Moon, J. Implicit and explicit CSR: A conceptual framework for a comparative understanding of corporate social responsibility. Acad. Manag. Rev. 2008, 33, 404–424. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.A. Corporate social responsibility in the multinational enterprise: Strategic and institutional approaches. J. Int. Bus. Stud. 2006, 37, 838–849. [Google Scholar] [CrossRef] [Green Version]

- Lattemann, C.; Fetscherin, M.; Alon, I.; Li, S.M.; Schneider, A.M. CSR Communication intensity in Chinese and Indian multinational companies. Corp. Gov. Int. Rev. 2009, 17, 426–442. [Google Scholar] [CrossRef]

- Tarabella, A.; Burchi, B. Systematic review of the business case for CSR. Int. J. Econ. Pract. Theor. 2013, 3, 10–29. [Google Scholar]

- Reverte, C. Determinants of corporate social responsibility disclosure ratings by Spanish listed firms. J. Bus. Ethics 2009, 88, 351–366. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39. [Google Scholar] [CrossRef]

- Arevalo, J.A.; Aravind, D. Corporate social responsibility practices in India: Approach, drivers, and barriers. Corp. Gov. Int. J. Bus. Soc. 2011, 11, 399–414. [Google Scholar] [CrossRef]

- Jones, M. The institutional determinants of social responsibility. J. Bus. Ethics. 1999, 20, 163–179. [Google Scholar] [CrossRef]

- Garriga, E.; Melé, D. Corporate social responsibility theories: Mapping the territory. J. Bus. Ethics 2004, 53, 51–71. [Google Scholar] [CrossRef]

- Bondy, K.; Moon, J.; Matten, D. An institution of corporate social responsibility in multi-national corporations: Form and implications. J. Bus. Ethics. 2012, 111, 281–299. [Google Scholar] [CrossRef] [Green Version]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Cramer, J. Experiences with structuring corporate social responsibility in Dutch industry. J. Clean. Prod. 2005, 13, 583–592. [Google Scholar] [CrossRef]

- Zhao, Z.Y.; Zhao, X.J.; Davidson, K.; Zuo, J. A corporate social responsibility indicator system for construction enterprises. J. Clean. Prod. 2012, 29–30, 277–289. [Google Scholar] [CrossRef]

- Jones, M. Missing the forest for the trees: A critique of the social responsibility concept and discourse. Bus. Soc. 1996, 35, 7–41. [Google Scholar] [CrossRef]

- Walsh, J.; Weber, K.; Margolis, J. Social issues and management: Our lost cause found. J. Manag. 2003, 29, 859–881. [Google Scholar]

- Miras-Rodríguez, M.M.; Carrasco-Gallego, A.; Escobar-Pérez, B. Has the CSR engagement of electrical companies had an effect on their performance? A closer look at the environment. Bus. Strategy Environ. 2015, 24, 819–835. [Google Scholar] [CrossRef]

- Maignan, I.; Ralston, D.A. Corporate social responsibility in Europe and the U.S.: Insights from businesses’ self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Campbell, J.L. Institutional analysis and the paradox of corporate social responsibility. Am. Behav. Sci. 2006, 49, 925–938. [Google Scholar] [CrossRef]

- Selvi, Y.; Wagner, E.; Türel, A. Corporate social responsibility in the time of financial crisis: Evidence from Turkey. Ann. Univ. Apulensis Ser. Oecon. 2010, 12, 281–290. [Google Scholar]

- Hemingway, C.A.; Maclagan, P.W. Managers’ personal values as drivers of corporate social responsibility. J. Bus. Ethics. 2004, 50, 33–44. [Google Scholar] [CrossRef]

- Margolis, J.; Elfenbein, H.A.; Walsh, J.P. Does It Pay to Be Good...And Does It Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial Performance; SSRN Working Paper Series; Rochester Publishing Inc: Rochester, NY, USA, 2009. [Google Scholar]

- Pérez, A.; del Bosque, I.R. An integrative framework to understand how CSR affects customer loyalty through identification, emotions and satisfaction. J. Bus. Ethics 2015, 129, 571–584. [Google Scholar] [CrossRef]

- Friedman, M. The social responsibility of business is to increase its profits. The New York Times, 13 September 1970; p. 17. [Google Scholar]

- López-Gamero, M.D.; Claver-Cortés, E.; Molina-Azorín, J.F. Complementary resources and capabilities for an ethical and environmental management: A qual/quan study. J. Bus. Ethics 2008, 82, 701–732. [Google Scholar] [CrossRef]

- O’Connor, M.; Spangenberg, J.H. A methodology for CSR reporting: Assuring a representative diversity of indicators across stakeholders, scales, sites and performance issues. J. Clean. Prod. 2008, 16, 1399–1415. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. Extrinsic and intrinsic drivers of corporate social performance: Evidence from foreign and domestic firms in Mexico. J. Manag. Stud. 2010, 47, 1–26. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef] [Green Version]

- McWilliams, A.; Siegel, D.S. Creating and capturing value: Strategic corporate social responsibility, resource-based theory, and sustainable competitive advantage. J. Manag. 2011, 37, 1480–1495. [Google Scholar] [CrossRef]

- Block, J.H.; Wagner, M. The effect of family ownership on different dimensions of corporate social responsibility: Evidence from large US firms. Bus. Strategy Environ. 2014, 23, 475–492. [Google Scholar] [CrossRef]

- Van der Heijden, A.; Driessen, P.; Cramer, J. Making sense of corporate social responsibility: Exploring organizational processes and strategies. J. Clean. Prod. 2010, 18, 1787–1796. [Google Scholar] [CrossRef]

- Moon, J. Government as a Driver of Corporate Social Responsibility—The UK in Comparative Perspective; ICCSR Research Paper Series; University of Nottingham: Nottingham, UK, 2004; Volume 20, pp. 1–27. [Google Scholar]

- Hemingway, C.A. The Role of Personal Values in Corporate Social Entrepreneurship; Research Paper Series; Nottingham University, International Centre for Corporate Social Responsibility: Nottingham, UK, 2005. [Google Scholar]

- Carroll, A.B. A three dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar]

- Quazi, A.M.; O’Brien, D. An empirical test of a cross-national model of corporate social responsibility. J. Bus. Ethics. 2000, 25, 33–51. [Google Scholar] [CrossRef]

- Erwin, P.M. Corporate codes of conduct: The effects of code content and quality on ethical performance. J. Bus. Ethics 2011, 99, 535–548. [Google Scholar] [CrossRef]

- Wu, L.; Kwan, H.K.; Yim, F.H.; Chiu, R.K.; He, X. CEO ethical leadership and corporate social responsibility: A moderated mediation model. J. Bus. Ethics 2015, 130, 819–831. [Google Scholar] [CrossRef]

- Frankental, P. Corporate social responsibility—A PR invention. Corp. Commun. Int. J. 2001, 6, 18–23. [Google Scholar] [CrossRef]

- Ciliberti, F.; Pontrandolfo, P.; Scozzi, B. Investigating corporate social responsibility in supply chains: A SME perspective. J. Clean. Prod. 2008, 16, 1579–1588. [Google Scholar] [CrossRef]

- Sajjad, A.; Eweje, G.; Tappin, D. Sustainable supply chain management: Motivators and barriers. Bus. Strategy Environ. 2015, 24, 643–655. [Google Scholar] [CrossRef]

- Deniz Deniz, M.; Cabrera Suarez, K. Corporate social responsibility and family business in Spain. J. Bus. Ethics 2005, 56, 27–41. [Google Scholar] [CrossRef]

- Dobers, P.; Springett, D. Corporate social responsibility: Discourse, narratives and communication. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 63–69. [Google Scholar] [CrossRef]

- Cacioppe, R.; Forster, N.; Fox, M. A Survey of managers’ perceptions of corporate ethics and social responsibility and actions that may affect companies’ success. J. Bus. Ethics 2008, 82, 681–700. [Google Scholar] [CrossRef]

- Strand, R.; Freeman, R.E.; Hockerts, K. Corporate social responsibility and sustainability in Scandinavia: An overview. J. Bus. Ethics 2015, 127, 1–15. [Google Scholar] [CrossRef]

- Chan, A.K.K.; Cheung, S.Y.L. Special issue on corporate social responsibility and sustainability: An Introduction. J. Bus. Ethics 2015, 130, 753–754. [Google Scholar] [CrossRef]

- Clement-Jones, T. Corporate social responsibility-bottom-line issue or public relations exercise? In Investing in Corporate Social Responsibility: A Guide to Best Practice, Business Planning& The UK`s Leading Companies; Hancock, J., Ed.; Kogan Page Limited: Business Books: London, UK; Sterling, VA, USA, 2005. [Google Scholar]

- Godkin, L. Mid-management, employee engagement, and the generation of reliable sustainable corporate social responsibility. J. Bus. Ethics 2015, 130, 15–28. [Google Scholar] [CrossRef]

- Bénabou, R.; Tirole, J. Individual and corporate social responsibility. Economica 2010, 77, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Ducassy, I. Does corporate social responsibility pay off in times of crisis? An alternate perspective on the relationship between financial and corporate social performance. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 157–167. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Jo, H. Corporate governance and CSR nexus. J. Bus. Ethics 2011, 100, 45–67. [Google Scholar] [CrossRef]

- Sjostrom, E. Shareholders as norm entrepreneurs for corporate social responsibility. J. Bus. Ethics 2010, 94, 177–191. [Google Scholar] [CrossRef]

- Carter, C.R.; Rogers, D.S. A framework of sustainable supply chain management: Moving toward new theory. Int. J. Phys. Distrib. Logist. Manag. 2008, 38, 360–387. [Google Scholar] [CrossRef]

- Tschopp, D.; Nastanski, M. The harmonization and convergence of corporate social responsibility reporting standards. J. Bus. Ethics 2014, 125, 147–162. [Google Scholar] [CrossRef]

- Sigurthorsson, D. The Icelandic banking crisis: A reason to rethink CSR. J. Bus. Ethics 2012, 111, 147–156. [Google Scholar] [CrossRef]

- Qian, C.; Gao, X.; Tsang, A. Corporate philanthropy, ownership type, and financial transparency. J. Bus. Ethics 2015, 130, 851–867. [Google Scholar] [CrossRef]

- Giannarakis, G.; Litinas, N. Corporate social responsibility performance in the Greek telecommunication sector. Strateg. Chang. 2011, 20, 73–84. [Google Scholar] [CrossRef]

- Rotter, J.P.; Airike, P.; Mark-Herbert, C. Exploring political corporate social responsibility in global supply chains. J. Bus. Ethics 2014, 125, 581–599. [Google Scholar] [CrossRef]

- Baron, D. Managerial contracting and corporate social responsibility. J. Public Econ. 2008, 92, 268–288. [Google Scholar] [CrossRef]

- Cramer, J.; Van Der Heijde, A.; Jonker, J. Corporate social responsibility: Making sense through thinking and acting. Bus. Ethics Eur. Rev. 2006, 15, 380–389. [Google Scholar] [CrossRef]

- Graafland, J.; Mazereeuw-Van der Duijn Schouten, C. The heavenly calculus and socially responsible business conduct: An explorative study among executives. Econ. Neth. 2007, 155, 161–181. [Google Scholar] [CrossRef]

- Hartmann, M. Corporate social responsibility in the food sector. Eur. Rev. Agric. Econ. 2011, 38, 297–324. [Google Scholar] [CrossRef]

- Ibrahim, N.A.; Howard, D.P.; Angelidis, J.P. Board members in the service industry: An empirical examination of the relationship between corporate social responsibility orientation and directorial type. J. Bus. Ethics 2003, 47, 393–401. [Google Scholar] [CrossRef]

- Idowu, S.; Papasolomou, I. Are the corporate social responsibility matters based on good intentions or false pretences? An empirical study of the motivations behind the issuing of CSR reports by UK companies. Corp. Gov. Int. J. Bus. Soc. 2007, 7, 136. [Google Scholar] [CrossRef]

- Lozano, R. A holistic perspective on corporate sustainability drivers. Corp. Soc. Responsib. Environ. Manag. 2013, 22, 32–44. [Google Scholar] [CrossRef]

- Manner, M.H. The Impact of CEO characteristics on corporate social performance. J. Bus. Ethics 2010, 93, 53–72. [Google Scholar] [CrossRef]

- Pater, A.; Van Lierop, K. Sense and sensitivity: The roles of organisation and stakeholders in managing corporate social responsibility. Bus. Ethics Eur. Rev. 2006, 15, 339–351. [Google Scholar] [CrossRef]

- Perrini, F.; Minoja, M. Strategizing corporate social responsibility: Evidence from an Italian medium-sized, family-owned company. Bus. Ethics Eur. Rev. 2008, 17, 47–63. [Google Scholar] [CrossRef]

- Peterson, R.T.; Jun, M. Small business manager attitudes relating to the significance of social responsibility issues: A longitudinal study. J. Appl. Manag. Entrep. 2006, 11, 32–50. [Google Scholar]

- Salam, M.A. Corporate social responsibility in purchasing and supply chain. J. Bus. Ethics 2009, 85, 355–370. [Google Scholar] [CrossRef]

- Tengblad, S.; Ohlsson, C. The framing of corporate social responsibility and the globalization of national business systems: A longitudinal case study. J. Bus. Ethics 2010, 93, 653–669. [Google Scholar] [CrossRef]

- Waldman, D.A.; Sully de Luque, M.; Washburn, N.; House, R.J. Cultural and leadership predictors of corporate social responsibility values of top management: A globe study of 15 countries. J. Int. Bus. Stud. 2006, 37, 823–837. [Google Scholar] [CrossRef] [Green Version]

- Bansal, P.; Hunter, T. Strategic explanations for the early adoption of ISO 14001. J. Bus. Ethics 2003, 46, 289–299. [Google Scholar] [CrossRef]

- Cheah, E.; Jamali, D.; Johnson, J.; Sung, M.C. Drivers of corporate social responsibility attitudes: The demography of socially responsible investors. Br. J. Manag. 2011, 22, 305–323. [Google Scholar] [CrossRef]

- Cramer, J.; Jonker, J.; Van Der Heijden, A. Making sense of corporate social responsibility. J. Bus. Ethics 2004, 55, 215–222. [Google Scholar] [CrossRef]

- Hopkins, M. The Planetary Bargain–CSR Matters; Earthscan: London, UK, 2003. [Google Scholar]

- Jamali, D.; Safieddine, A.M.; Rabbath, M. Corporate governance and corporate social responsibility synergies and interrelationships. Corp. Gov. Int. Rev. 2009, 16, 443–459. [Google Scholar] [CrossRef]

- Pedersen, E.R. Modelling CSR: How managers understand the responsibilities of business towards society. J. Bus. Ethics 2010, 91, 155–166. [Google Scholar] [CrossRef]

- Siltaoja, M.E. Revising the corporate social performance model—Towards knowledge creation for sustainable development. Bus. Strategy Environ. 2014, 23, 289–302. [Google Scholar] [CrossRef]

- Greenfield, W.M. In the name of corporate social responsibility. Bus. Horiz. 2004, 47, 19–28. [Google Scholar] [CrossRef]

- Lewicka-Strzalecka, A. Opportunities and limitations of CSR in the postcommunist countries: Polish case. Corp. Gov. Int. Rev. 2006, 6, 440–448. [Google Scholar] [CrossRef]

- Argandoña, A. The stakeholder theory and the common good. J. Bus. Ethics 1998, 17, 1093–1102. [Google Scholar] [CrossRef]

- Hung, H. Directors’ roles in corporate social responsibility: A stakeholder perspective. J. Bus. Ethics 2011, 103, 385–402. [Google Scholar] [CrossRef]

- Golob, U.; Podnar, K. Critical points of CSR-related stakeholder dialogue in practice. Bus. Ethics Eur. Rev. 2014, 23, 248–257. [Google Scholar] [CrossRef]

- Kronenberg, J.; Bergier, T. Sustainable development in a transition economy: Business case studies from Poland. J. Clean. Prod. 2012, 26, 18–27. [Google Scholar] [CrossRef]

- Chih, H.L.; Chih, H.H.; Chen, T.Y. On the determinants of corporate social responsibility: International evidence on the financial industry. J. Bus. Ethics 2010, 93, 115–135. [Google Scholar] [CrossRef]

- Kolk, A.; Perego, P. Determinants of the adoption of sustainability assurance statements: An international investigation. Bus. Strategy Environ. 2010, 19, 182–198. [Google Scholar] [CrossRef]

- Gond, J.P.; Kang, N.; Moon, J. The government of self-regulation: On the comparative dynamics of corporate social responsibility. Econ. Soc. 2011, 40, 640–671. [Google Scholar] [CrossRef]

- Jamali, D.; Neville, B. Convergence versus divergence of CSR in developing countries: An embedded multi-layered institutional lens. J. Bus. Ethics 2011, 102, 599–621. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; Banerjee, S.; García-Sánchez, I.M. Corporate Social Responsibility as a Strategic Shield Against Costs of Earnings Management Practices. J. Bus. Ethics 2016, 133, 305–324. [Google Scholar] [CrossRef]

- Eberle, D.; Berens, G.; Li, T. The impact of interactive corporate social responsibility communication on corporate reputation. J. Bus. Ethics 2013, 118, 731–746. [Google Scholar] [CrossRef] [Green Version]

- Hur, W.; Kim, H.; Woo, J. How CSR leads to corporate brand equity: Mediating mechanisms of corporate brand credibility and reputation. J. Bus. Ethics 2014, 125, 75–86. [Google Scholar] [CrossRef]

- Moon, J.; Crane, A.; Matten, D. Can corporations be citizens? Corporate citizenship as a metaphor for business participation in society. Bus. Ethics Q. 2005, 15, 427–451. [Google Scholar] [CrossRef]

- Cheung, Y.; Kong, D.; Tan, W.; Wang, W. Being good when being international in an emerging economy: The case of China. J. Bus. Ethics 2015, 130, 805–817. [Google Scholar] [CrossRef]

- Lund-Thomsen, P.; Lindgreen, A.; Vanhamme, J. Industrial clusters and corporate social responsibility in developing countries: What we know, what we do not know, and what we need to know. J. Bus. Ethics 2016, 133, 9–24. [Google Scholar] [CrossRef]

- Dahlsrud, A. How corporate social responsibility is defined: An analysis of 37 definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Graafland, J.; Zhang, L. Corporate social responsibility in China: Implementation and challenges. Bus. Ethics Eur. Rev. 2014, 23, 34–49. [Google Scholar] [CrossRef]

- Den Hond, F.; Bakker, F. Ideologically motivated activism: How activist groups influence corporate social change activities. Acad. Manag. Rev. 2007, 32, 901–924. [Google Scholar] [CrossRef]

- Dobele, A.R.; Westberg, K.; Steel, M.; Flowers, K. An examination of corporate social responsibility implementation and stakeholder engagement: A case study in the Australian mining industry. Bus. Strategy Environ. 2014, 23, 145–159. [Google Scholar] [CrossRef]

- Doh, J.P.; Howton, S.D.; Howton, S.W.; Siegel, D.S. Does the market respond to an endorsement of social responsibility? The role of institutions, information, and legitimacy. J. Manag. 2010, 36, 1461–1485. [Google Scholar] [CrossRef]

- Henderson, D. The role of business in the world of today. J. Corp. Citizsh. 2005, 17, 30–32. [Google Scholar]

- Huang, C.L.; Kung, F.H. Drivers of environmental disclosure and stakeholder expectation: Evidence from Taiwan. J. Bus. Ethics 2010, 96, 435–451. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M. Analyst coverage, corporate social responsibility, and firm risk. Bus. Ethics Eur. Rev. 2014, 23, 272–292. [Google Scholar] [CrossRef]

- Marquis, C.; Glynn, M.A.; Davis, G. Community isomorphism and corporate social action. Acad. Manag. Rev. 2007, 32, 925–945. [Google Scholar] [CrossRef]

- Morsing, M.; Schultz, M. Corporate social responsibility communication: Stakeholder information, response and involvement strategies. Bus. Ethics Eur. Rev. 2006, 15, 323–338. [Google Scholar] [CrossRef]

- Perrini, F.; Russo, A.; Tencati, A.; Vurro, C. Going beyond a Long-Lasting Debate: What Is behind the Relationship between Corporate Social and Financial Performance; Working Paper; Bocconi University: Milano, Italy, 2009. [Google Scholar]

- Post, J.E.; Preston, L.E.; Sachs, S. Managing the extended enterprise: The new stakeholder view. Calif. Manag. Rev. 2002, 45, 5–27. [Google Scholar] [CrossRef]

- Preuss, L. Ethical sourcing codes of large UK-based corporations: Prevalence, content, limitations. J. Bus. Ethics 2009, 88, 735–747. [Google Scholar] [CrossRef]

- Weber, M. The business case for corporate social responsibility: A company-level measurement approach for CSR. Eur. Manag. J. 2008, 26, 247–261. [Google Scholar] [CrossRef]

- Pedersen, E.R.G.; Neergaard, P.; Pedersen, J.T.; Gwozdz, W. Conformance and deviance: Company responses to institutional pressures for corporate social responsibility reporting. Bus. Strategy Environ. 2013, 22, 357–373. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–411. [Google Scholar] [CrossRef]

- Welford, R.; Frost, S. Corporate social responsibility in Asian supply chains. Corp. Soc. Responsib. Environ. Manag. 2006, 13, 166–176. [Google Scholar] [CrossRef]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Marimon, F.; Alonso-Almeida, M.; Rodríguez, M.; Cortez Alejandro, K.A. The worldwide diffusion of the global reporting initiative: What is the point. J. Clean. Prod. 2012, 33, 132–144. [Google Scholar] [CrossRef]

- Schadewitz, H.; Niskala, M. Communication via responsibility reporting and its effect on firm value in Finland. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 96–106. [Google Scholar] [CrossRef]

- Jackson, G.; Apostolakou, A. Corporate social responsibility in western Europe: An institutional mirror or substitute? J. Bus. Ethics 2010, 94, 371–394. [Google Scholar] [CrossRef]

- Jenkins, H. Small business champions for corporate social responsibility. J. Bus. Ethics 2006, 67, 241–256. [Google Scholar] [CrossRef]

- Malik, M. Value-enhancing capabilities of CSR: A brief review of contemporary literature. J. Bus. Ethics. 2015, 127, 419–438. [Google Scholar] [CrossRef]

- Morrow, J.; Mowatt, S. The implementation of authentic sustainable strategies: I-SITE middle managers, employees and the delivery of 100% pure New Zealand. Bus. Strategy Environ. 2015, 24, 656–666. [Google Scholar] [CrossRef]

- Welford, R. Corporate social responsibility in Europe, North America and Asia. 2004 Survey results. J. Corp. Citizsh. 2005, 17, 33–52. [Google Scholar]

- Bollen, K.A. Structural Equations with Latent Variables; Wiley Series in Probability and Mathematical Statistics; John Wiley & Sons: New York, NY, USA, 1989. [Google Scholar]

- Lee, S.-Y. Structural Equation Modelling a Bayesian Approach; Wiley Series in Probability and Statistics; John Wiley & Sons: New York, NY, USA, 2007. [Google Scholar]

- Aragón is a medium-sized 47,669 km2 region in northeastern Spain. Per capita gross domestic product year 2013: Aragon 24,693 €, Spain 22,519 €, EU 25,700 €. Components of Gross Domestic Product year 2013 of Aragon (Services 59%, Industry 15%, Taxes on products 9%, Energy 6%, Construction 6% and Agriculture 5%) and of Spain (Services 67%, Industry 12%, Taxes on products 9%, Energy 4%, Construction 5% and Agriculture 3%).

- European Commission. Commission Recommendation 2003/361/EC May 2003 concerning the definition of micro, small and medium-sized enterprises. Off. J. Eur. Union 2003, L 124, 36–41. [Google Scholar]

- The European Commission establishes the following classification of SMEs: Micro enterprises with less than 10 employees and a turnover/balance sheet of less than €2 million; small enterprises with less than 50 employees and a turnover/balance sheet of less than ECU €10 million; medium enterprises with less than 250 employees and a turnover of less than €50 million or annual balance sheet of less than €43 million. Other organizations are classified as large firms.

- Alcaide, J.; Alcaide, P. Renta Nacional de España y Su Distribución Provincial; Año 1995 y Avances 1996 a 1999; Fundación BBVA: Bilbao, Spain, 1999. [Google Scholar]

- Centelles, F. El Estado Autonómico: Teoría y Práctica; Editorial Azacanes: Toledo, Spain, 1993. [Google Scholar]

- Agudo-Valiente, J.M.; Garcés-Ayerbe, C.; Salvador-Figueras, M. Social responsibility practices and evaluation of corporate social performance. J. Clean. Prod. 2012, 35, 25–38. [Google Scholar] [CrossRef]

- Murray, K.B.; Vogel, C. Using a hierarchy-of-effects approach to gauge the effectiveness of corporate social responsibility to generate goodwill toward the firm financial versus nonfinancial impacts. J. Bus. Res. 1997, 38, 141–159. [Google Scholar] [CrossRef]

- Wartick, S.L.; Cochran, P. The evolution of the corporate social performance model. Acad. Manag. Rev. 1985, 10, 758–769. [Google Scholar]

- In the Bayesian approach, inferences about the parameters of the model θ are made from their posterior distribution θ|Y where Y is the matrix of data. This distribution is calculated by means of the Bayes theorem and it is given by where [Y|θ], [θ] and [Y] = are, respectively, the likelihood function of θ, the prior distribution of θ and the marginal distribution of Y. In our case, Y contains the answers to the items of our poll an θ contains the means of the variables (µ), the factor loadings (λ), the factor scores of the individuals (F), the regression coefficients of the structural model (γ) and the error variances (σ2). Y|θ is multivariate normal the means and covariance matrices of which depend on θ. Prior distributions of the factor scores F are N(0,1); prior distributions of µ, λ, γ are normal distributions with mean 0 and large variances (106) and prior distribution of error variances σ2 are inverted Gamma (0.01, 0.01). These distributions are standard in the Bayesian literature and correspond to a diffuse distribution which let the data speak for themselves.

- A quantile is a location measure which generalizes the notion of quartiles, deciles or percentiles. For 0 ≤ α ≤ 100, the α-quantile of a continuous random variable X is defined as the value qα such that P(X ≤ qα) = . In particular if α = 25, 50, 75 we have the three quartiles of the probability distribution of X.

- The number of iterations of the algorithm was 20,000 with a burning period of 10,000. The sample size was equal to 10,000.

- Spiegelhalter, D.J.; Best, N.G.; Carlin, B.P.; Van Der Linde, A. Bayesian measures of model complexity and fit. J. R. Stat. Soc. 2002, 64, 583–639. [Google Scholar] [CrossRef]

- Fifka, M.S. Corporate responsibility reporting and its determinants in comparative perspective—A review of the empirical literature and a meta-analysis. Bus. Strategy Environ. 2013, 22, 1–35. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Frequency (%) | |

|---|---|

| Integrating ethics a | 31.9% |

| Sustainable development b | 18.7% |

| Organizational commitment to transparency c | 13.2% |

| Philanthropy d | 11.0% |

| Public relations exercise e | 8.8% |

| Fashion following f | 8.8% |

| A skeptical view only for large corporations g | 4.4% |

| A utopic value h | 3.3% |

| Total | 100% |

| Frequency (%) | |

|---|---|

| Stakeholder pressure a | 25.8% |

| Institutional framework b | 15.9% |

| Reputation management c | 13.6% |

| Availability of financial resources d | 9.1% |

| Availability of temporary resources e | 7.6% |

| Leading corporations f | 6.8% |

| Sectorial trends g | 6.1% |

| Availability of human resources h | 6.1% |

| Difficulties involved in interpreting CSR i | 5.3% |

| Low institutional interest j | 3.8% |

| Total | 100% |

| Number | % | |

|---|---|---|

| Sample distribution by sector | ||

| Industry | 185 | 44.5% |

| Construction | 48 | 11.5% |

| Hostelry and Commerce | 83 | 20.0% |

| Other Services | 100 | 24.0% |

| TOTAL | 416 | 100.0% |

| Sample distribution by size of organization following EU criteria | ||

| Micro-sized enterprises | 122 | 29.3% |

| Small-sized enterprises | 177 | 42.5% |

| Medium-sized enterprises | 72 | 17.3% |

| Large-sized enterprise | 45 | 10.8% |

| TOTAL | 416 | 100.0% |

| Factor Score | Survey Variable Contemplated in the Study | Mean | Typical Deviation | % Missing | Alpha Cronbach |

|---|---|---|---|---|---|

| Subjective drivers of CSR (SD) | YSD1 CSR implies integrating ethics into a firm’s management. | 5.82 | 1.73 | 5.3% | 0.581 |

| YSD2 CSR integrates transparency and affects investor confidence. | 5.37 | 1.75 | 5.3% | ||

| YSD3 CSR contemplates aspects related to social, environmental and economic performance. | 5.68 | 1.68 | 5.1% | ||

| Subjective barriers to CSR (SB) | YSB1 CSR is especially applicable in large corporations. | 3.25 | 2.04 | 5.1% | 0.738 |

| YSB2 CSR only focuses on undertaking social and solidarity-based projects. | 2.75 | 1.69 | 5.3% | ||

| YSB3 CSR is an image strategy rather than a true strategic conviction. | 3.46 | 1.90 | 4.8% | ||

| YSB4 CSR is only a passing fashion that arose after the latest scandals. | 2.56 | 1.71 | 5.5% | ||

| YSB5 CSR is a utopian value that cannot be integrated into or managed by firms. | 3.24 | 1.78 | 5.3% | ||

| Objective drivers of CSR (OD) | YOD1 Sectorial trends. | 3.58 | 2.10 | 6.5% | 0.773 |

| YOD2 Improvement of the firm’s reputation. | 5.11 | 1.95 | 5´8% | ||

| YOD3 Social demand for more transparency, honesty, ethics. | 5.10 | 1.93 | 4.3% | ||

| YOD4 Publication of sustainability reports by leading corporations. | 4.27 | 2.13 | 7.2% | ||

| YOD5 Associated legal and institutional framework. | 4.21 | 2.14 | 7.4% | ||

| Objective Barriers to CSR (OB) | YOB1 The little time available for the subject makes CSR difficult in the firm. | 5.29 | 1.95 | 2.9% | 0.812 |

| YOB2 CSR cannot be implanted in my firm due to a lack of structure and human resources. | 4.77 | 2.14 | 3.6% | ||

| YOB3 CSR is not applied in my firm because of the lack of official grants. | 4.86 | 2.14 | 3.6% | ||

| YOB4 The firm does not develop CSR because of difficulties in interpreting what it involves together with a shortage of CSR training opportunities. | 4.87 | 2.11 | 3.6% | ||

| YOB5 The lack of economic resources makes CSR difficult in the firm. | 4.90 | 2.09 | 3.6% |

| Criterion | Independent | Model Proposed | Complete |

|---|---|---|---|

| BIC | 2.43 × 1012 | 2.38 × 1012 | 2.44 × 1012 |

| DIC | 4.52 × 1012 | 2.40 × 1012 | 4.03 × 1012 |

| LPRED | −1.73 × 1012 | −1.18 × 1012 | −1.56 × 1012 |

| R2 | 0.4499 | ||

| COV95 | 95.04% | ||

| COV99 | 98.97% |

| a. Posterior Factors Loading Estimations of the CFA Measurement Model | ||||

| Factor | Factor Loading | Median | Limits to 95% of the Distribution | |

| Lower | Upper | |||

| Subjective drivers of CSR (SD) | SD1 | 1 | ||

| SD2 | 0.724 | 0.550 | 0.900 | |

| SD3 | 0.694 | 0.525 | 0.863 | |

| Subjective barriers to CSR (SB) | SB1 | 1 | ||

| SB2 | 0.991 | 0.813 | 1.171 | |

| SB3 | 1.046 | 0.847 | 1.247 | |

| SB4 | 0.837 | 0.664 | 1.011 | |

| SB5 | 0.861 | 0.675 | 1.044 | |

| Objective driver of CSR (OD) | OD1 | 1 | ||

| OD2 | 1.163 | 1.006 | 1.325 | |

| OD3 | 0.876 | 0.692 | 1.059 | |

| OD4 | 1.392 | 1.210 | 1.586 | |

| OD5 | 1.218 | 1.024 | 1.418 | |

| Objective barriers to CSR (OB) | OB1 | 1 | ||

| OB2 | 1.251 | 1.069 | 1.440 | |

| OB3 | 1.408 | 1.224 | 1.598 | |

| OB4 | 1.193 | 1.013 | 1.377 | |

| OB5 | 1.063 | 0.880 | 1.252 | |

| b. Posterior Estimation of the Parameters of the Structural Model | ||||

| Median | Limits to 95% of the Distribution | |||

| Lower | Upper | |||

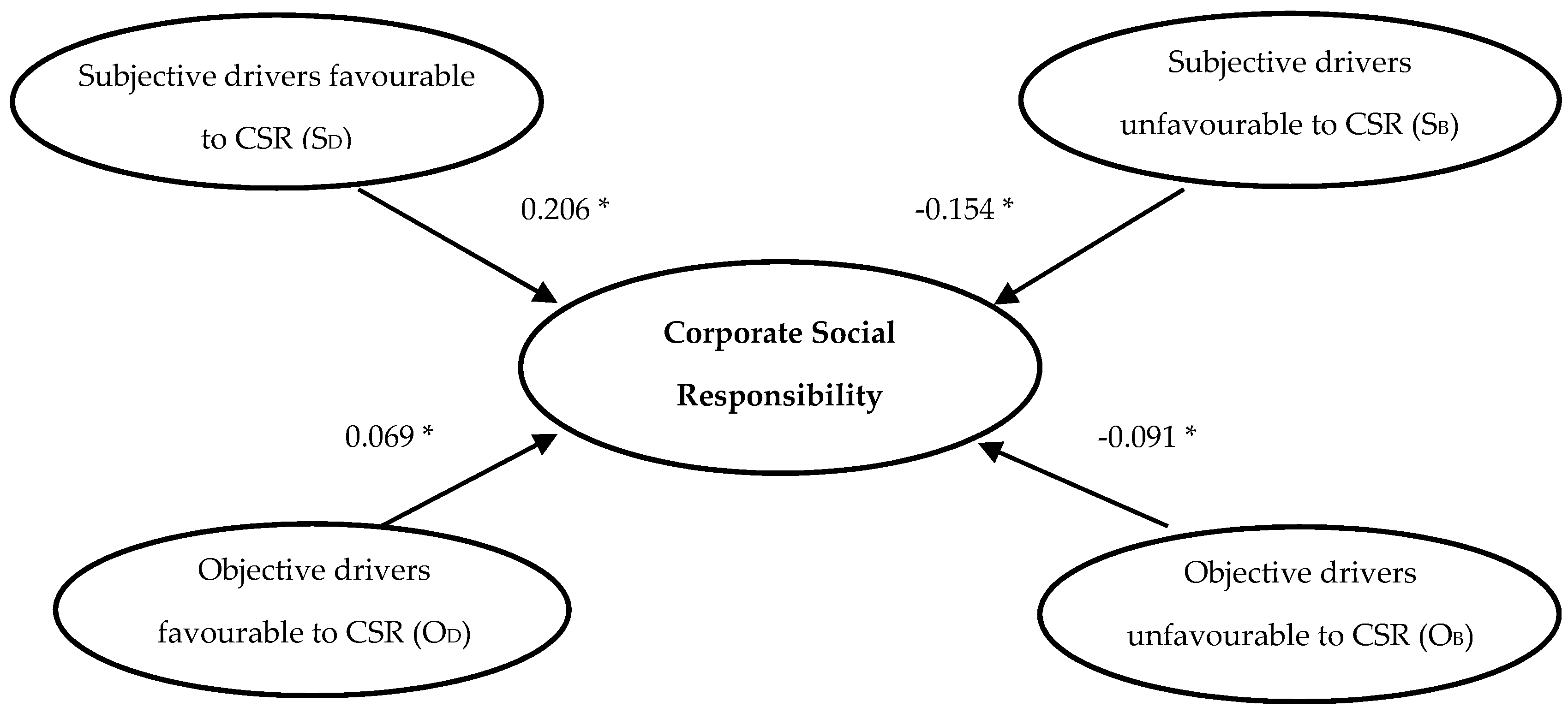

| γSD | 0.203 | 0.126 | 0.302 | |

| γSB | −0.153 | −0.233 | −0.079 | |

| γOD | 0.069 | 0.012 | 0.125 | |

| γOB | −0.091 | −0.148 | −0.037 | |

| Approach to CSR | Total | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Modern | Socioeconomic | Classical | Philanthropic | ||||||||

| Nº | % | Nº | % | Nº | % | Nº | % | Nº | % | ||

| Size | Micro-sized enterprises | 27 | 22.1% | 16 | 13.1% | 66 | 54.1% | 13 | 10.7% | 122 | 100% |

| Small-sized enterprise | 62 | 35.0% | 27 | 15.3% | 61 | 34.5% | 27 | 15.3% | 177 | 100% | |

| Medium-sized enterprise | 44 | 61.1% | 10 | 13.9% | 10 | 13.9% | 8 | 11.1% | 72 | 100% | |

| Large-sized enterprise | 24 | 53.3% | 10 | 22.2% | 7 | 15.6% | 4 | 8.9% | 45 | 100% | |

| Total | 157 | 37.7% | 63 | 15.1% | 144 | 34.6% | 52 | 12.5% | 416 | 100% | |

| Sector | Industry | 74 | 40.0% | 26 | 14.1% | 68 | 36.8% | 17 | 9.2% | 185 | 100% |

| Construction | 15 | 31.3% | 6 | 12.5% | 20 | 41.7% | 7 | 14.6% | 48 | 100% | |

| Hostelry and commerce | 24 | 28.9% | 11 | 13.3% | 36 | 43.4% | 12 | 14.5% | 83 | 100% | |

| Other Services | 44 | 44.0% | 20 | 20.0% | 20 | 20.0% | 16 | 16.0% | 100 | 100% | |

| Total | 157 | 37.7% | 63 | 15.1% | 144 | 34.6% | 52 | 12.5% | 416 | 100% | |

| By Size; p-value χ2 = 0 | |||||||||||

| By Sector; p-value χ2 = 0,040 | |||||||||||

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Agudo-Valiente, J.M.; Garcés-Ayerbe, C.; Salvador-Figueras, M. Corporate Social Responsibility Drivers and Barriers According to Managers’ Perception; Evidence from Spanish Firms. Sustainability 2017, 9, 1821. https://doi.org/10.3390/su9101821

Agudo-Valiente JM, Garcés-Ayerbe C, Salvador-Figueras M. Corporate Social Responsibility Drivers and Barriers According to Managers’ Perception; Evidence from Spanish Firms. Sustainability. 2017; 9(10):1821. https://doi.org/10.3390/su9101821

Chicago/Turabian StyleAgudo-Valiente, José María, Concepción Garcés-Ayerbe, and Manuel Salvador-Figueras. 2017. "Corporate Social Responsibility Drivers and Barriers According to Managers’ Perception; Evidence from Spanish Firms" Sustainability 9, no. 10: 1821. https://doi.org/10.3390/su9101821