2.1. Change Trends in Domestic and Overseas Construction Orders of Korean Construction Firms

The Korean construction market was seriously depressed when Korea was hit by the IMF crisis in 1998. However, the market was reactivated by the Korean government’s active market policy and demand-supply imbalance in the 2000s. Although the global financial crisis in 2008 hit the Korean construction market again and drove the economy into a severe recession, the market has gradually recovered with the influence of policy.

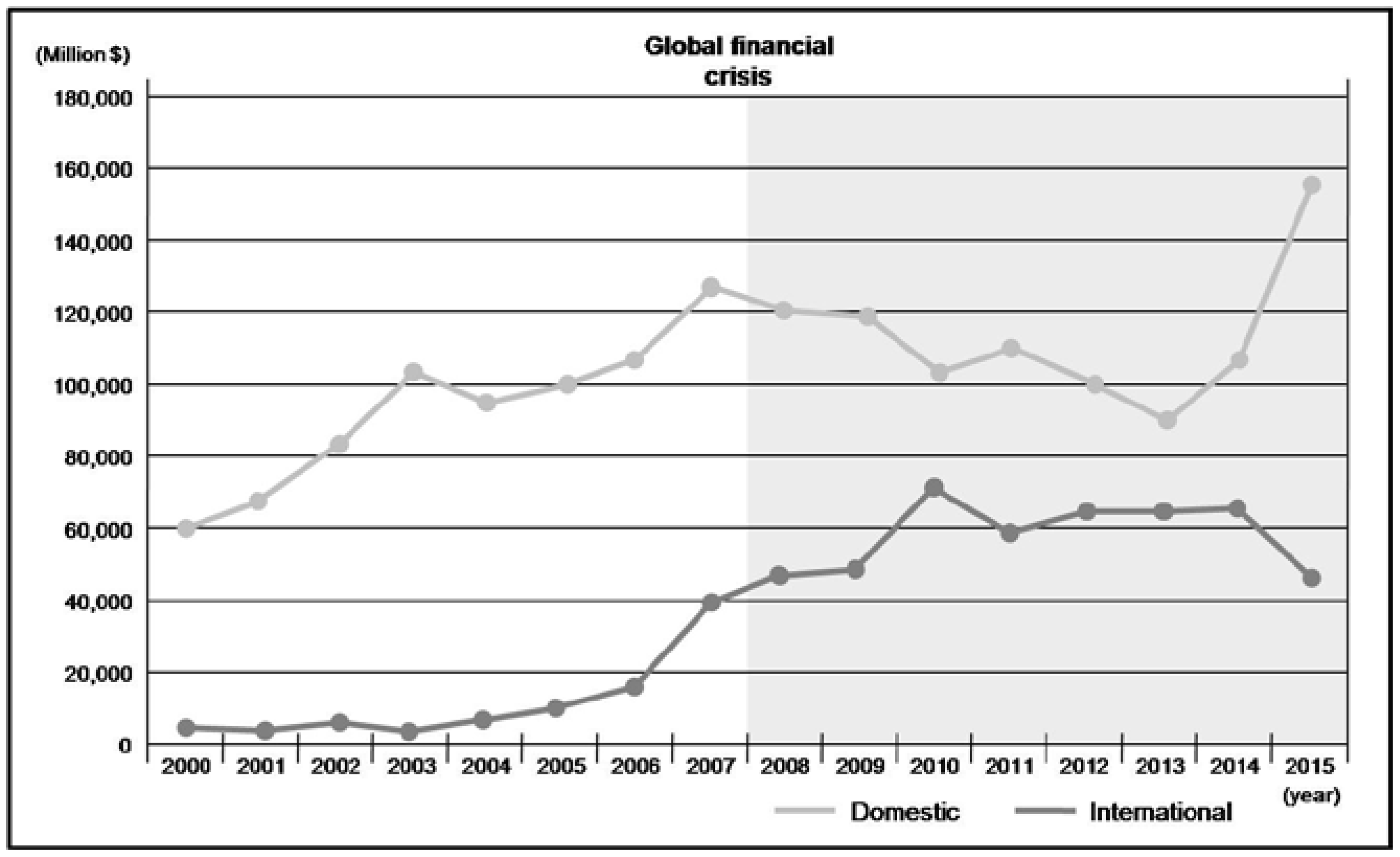

Figure 1 shows the domestic construction orders of Korean construction firms, which increased from approximately 60,152 million USD in 2000 to 102,447 million USD in 2003. Although this amount decreased again in 2004, domestic construction orders gradually increased and reached 127,912 million USD in 2007. Thus, domestic construction orders of Korean construction firms increased before the global financial crisis in 2008. If we examine overseas construction orders of Korean construction firms for the same period, the orders fluctuated widely from 5433 million USD in 2000 to 3677 million USD in 2003. However, orders continuously increased after they reached 7498 million USD in 2004 and recorded 39,788 million USD in 2007 before the global financial crisis. Therefore, Korean construction firms expanded actively in the domestic and overseas markets beginning in 2004 and before the global financial crisis.

However, after the global financial crisis, specific factors have been observed concerning the changes between domestic and overseas construction orders of Korean construction firms. After the domestic construction orders reached 120,085 million USD in 2008, orders gradually decreased to 91,307 million USD in 2013. In contrast, during the same period, overseas construction orders increased from 47,640 million USD in 2008 to 65,212 million USD in 2013, which was relatively satisfactory. Construction orders for Korean firms showed an increasing tendency despite the effects of the global financial crisis worldwide, which caused overall shrinkage in the overseas construction market.

This study aims to empirically analyze the influence of Korean construction firms’ regional diversification characteristics on management performance, particularly with respect to the financial sustainability of firms.

2.2. Literature Review

Korean construction firms enter the overseas construction market to diversify and maintain stable management. A diversification strategy is designed to achieve sustainable firm performance in the various markets and industries. Considerable research has been conducted on the relationship between business diversification and firms’ management performance. However, studies have shown conflicting results on the effect of diversification on firms’ performance.

Previous studies have noted a positive influence from diversification on firm performance because of resource management efficiency, enhancement of self-financing capability, and firms’ financial risk reduction effect. Rumelt (1974) showed that, in the research conducted on Fortune 500 companies between 1949 and 1974, related diversification was a superior strategy in terms of profitability than unrelated diversification [

12]. Palepu (1985) discovered a similar result in research on US food companies. Additionally, several studies confirmed the effectiveness of business diversification strategy according to resource management efficiency [

13]. Studies targeted the different countries, that is, Lecraw (1984) for Canada [

14], Itami (1982) for Japan [

15], and Buhner (1987) for Germany [

16]. The results of these studies implied that related diversification has a positive effect on firm performance because the firm’s technology and resources are applied to the related market. Khanna et al. (2000), in an empirical analysis targeting emerging markets, noticed that the influence of business diversification on firm performance showed stronger positive aspects than negative aspects [

17].

In contrast, the existing studies that address the contradictory aspects have noted that business diversification has a negative impact on firm management performance due to overinvestment, a cross-subsidization effect, and the occurrence of asymmetric information cost. Lang et al. (1994) insisted, from their analysis of companies with assets of over 100 million USD from 1978 to 1990 on the relationship between the rate of diversification and firm performance, that the performance of diversified firms is inferior to the performance of specialized firms. The authors noticed that enhancing self-financing capability through business diversification causes over investment and a negative impact on a firm’s performance [

18]. Berger et al. (1995) analyzed the influence of firm diversification on the performance of companies for which total sales exceeded 20 million USD for six years, 1986 to 1991. The result showed that diversified companies suffered a value loss of, on average, 13%–15%. The authors insisted that cross-subsidization among business sectors was the cause, and the sectors with satisfactory investment performance supported the sectors with poor performance [

19]. Comment et al. (1995) investigated 2000 companies listed on the NYSE and ASE for three years, 1987 to 1989, to identify the relationship between corporate focus and stock returns. The results revealed that the company group with intensified corporate focus had a higher rate of earnings while a weak corporate focus showed the lowest earnings rates [

20]. Lins et al. (1999) examined whether the companies’ value loss occurred as a result of diversification in countries other than the US. The result showed that the decline in corporate value due to diversification was significant in Japan and the UK [

21].

Diversification has also been adopted by construction firms. The studies related to diversification for the construction sector can be classified into diversification strategy and performance measurement studies. The research on diversification strategy in the construction sector mainly investigates the growth fundamentals in construction companies for one of the various strategies. Cheah (2002) investigated the diversification strategy of 21 construction firms that conduct business in overseas construction markets according to the market segmentation matrix. The market segmentation matrix suggested in this study categorized the diversification patterns of construction forms into (1) project type diversification (for example, residence construction, commercial construction, and industrial facility); (2) regional diversification (for example, domestic and overseas); and (3) service diversification (for example, validity verification, planning, design, and construction) [

22]. Yee et al. (2006) [

23] analyzed the globalization, diversification, and financial strategy of construction firms on 61 E&C companies in Korea, Japan, Europe, and the US. The results found that globalized firms show characteristics of a high current ratio and low leverage while diversified firms show a low current ratio and high leverage. Yee et al. (2006) [

7] studied the relationships among companies’ scale, profitability, and diversification strategy for the same companies examined by Yee et al. (2006) [

23]. The authors concluded that small-scale companies show a tendency to concentrate, and when the scale and resources of a company grow to a certain degree, the company expands to new market sectors.

The diversification performance measurement studies for the construction industry focused on the verification of diversification performance by measuring the rate of diversification and quantitatively analyzing the relationship with management performance. Choi et al. (2005) [

24] investigated diversification and profitability of 59 contractors and 49 non-contractors—including, for example, material suppliers, construction engineers, and environmental firms—in the US based on 12 years of data. In this study, they divided the firms into two groups, specialized firms and diversified firms, and analyzed the difference between the two groups but found no significant difference between the firms in terms of either a high or low level of diversification. Kim et al. (2012) [

25] examined the diversification performance of 400 construction companies and 500 construction design firms in the US between 1994 and 2009. This study executed four correlation analyses; diversification and corporate scale, diversification and corporate growth, diversification and stability, and corporate growth and scale. The results showed that large-scale companies were more diversified than small-scale companies; however, diversification was not related to the corporate growth rate. Additionally, corporate performances of diversified construction companies and design firms were more stable than the standard deviation of the companies that were the objects of study. This study concluded that construction companies might grow with specialization followed by diversification for stability and survival. Panagiotidis et al. (2016) examined the Greek market in their study of the potential interdependencies between the housing price index and various macroeconomic determinants utilizing a VECM framework. This study found that housing market fluctuations had a considerable influence on the whole construction market, concluding that when the housing market is depressed, the financial sustainability of the construction company is vulnerable [

26].

In this study, we verify the performance of multinational business diversification—which has characteristically appeared in Korea—in terms of the corporate sustainability based on the business diversification studies. A number of studies on the overseas expansion of construction companies have been reported in the literature. For example, Han et al. (2004) looked at how financial portfolio risk management can be implemented for both individual and corporate international projects in order to integrate their risk hierarchies, recommending the use of a multicriterion decision-making method to maximize total value [

27]. Gunhan et al. (2005) developed a decision-making model for construction firms intending to expand their business internationally [

28], while Jung et al. (2012) [

29] suggested several sustainable construction strategies for international construction companies that function well under changing market conditions. In particular, they found that regional diversification is a useful strategy for overcoming prolonged recessionary periods, and localization is also helpful, particularly during the subsequent post-recession boom. Jung et al. (2012) [

30] suggested the use of a country portfolio model to manage such market uncertainties, proposing a quantitative diversification strategy to optimize country portfolio solutions based on four critical country-level objectives.

The mentioned papers typically recognize multinational business diversification from construction firms’ overseas expansion as an important strategy. However, the majority of study has been on the search for risk management measures, because the uncertainty of overseas expansion was comparably larger than the uncertainty associated with a domestic construction business. Therefore, these studies should differentiate between the influence of a construction firm business portfolio and the influence of overseas construction business as well as domestic business on the management performance of construction firms. In this study, we confirm the impact of multinational business diversification on the financial sustainability of construction firms, focusing particularly on the stability and continuity of Korean construction companies.

{kind=link}

{kind=link}

{kind=link}