Suggestion for a Framework for a Sustainable Infrastructure Asset Management Manual in Korea

Abstract

:1. Introduction

1.1. Background and Purpose of Study

1.2. Subjects and Methods of Study

2. Asset Management Status of Domestic Infrastructure

2.1. Environmental Change and Current Status of Infrastructure Asset Management

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Item | 5 Years or Less | 6~10 Years | 11~15 Years | 16~20 Years | 21~25 Years | 26~30 Years | 31 Years or More | Total |

|---|---|---|---|---|---|---|---|---|

| Bridges | 2291 | 2042 | 2016 | 1219 | 543 | 343 | 516 | 8970 |

| 25.5% | 22.8% | 22.5% | 13.6% | 6.1% | 3.8% | 5.8% | 100.0% | |

| Tunnels | 803 | 553 | 502 | 289 | 74 | 124 | 108 | 2453 |

| 32.7% | 22.5% | 20.5% | 11.8% | 3.0% | 5.1% | 4.4% | 100.0% | |

| Harbors | 71 | 49 | 53 | 62 | 31 | 17 | 49 | 332 |

| 21.4% | 14.8% | 16.0% | 18.7% | 9.3% | 5.1% | 14.8% | 100.0% | |

| Dams | 18 | 38 | 52 | 29 | 32 | 53 | 300 | 522 |

| 3.4% | 7.3% | 10.0% | 5.6% | 6.1% | 10.2% | 57.5% | 100.0% | |

| Buildings | 9609 | 11,463 | 12,021 | 8143 | 1124 | 468 | 432 | 43,260 |

| 22.2% | 26.5% | 27.8% | 18.8% | 2.6% | 1.1% | 1.0% | 100.0% | |

| Rivers | 945 | 89 | 98 | 129 | 125 | 86 | 264 | 1736 |

| 54.4% | 5.1% | 5.6% | 7.4% | 7.2% | 5.0% | 15.2% | 100.0% | |

| Waterworks and sewage | 238 | 284 | 297 | 177 | 130 | 125 | 137 | 1388 |

| 17.1% | 20.5% | 21.4% | 12.8% | 9.4% | 9.0% | 9.9% | 100.0% | |

| Retaining walls | 424 | 212 | 142 | 99 | 35 | 15 | 108 | 1035 |

| 41.0% | 20.5% | 13.7% | 9.6% | 3.4% | 1.4% | 10.4% | 100.0% | |

| Cut slopes | 82 | 179 | 105 | 29 | 2 | 2 | 0 | 399 |

| 20.6% | 44.9% | 26.3% | 7.3% | 0.5% | 0.5% | 0.0% | 100.0% | |

| Total | 14,481 | 14,909 | 15,286 | 10,176 | 2096 | 1233 | 1914 | 60,095 |

| 24.1% | 24.8% | 25.4% | 16.9% | 3.5% | 2.1% | 3.2% | 100.0% |

2.2. Domestic Infrastructure Maintenance and Asset Management System

| Chapter | Composition | Major Details |

|---|---|---|

| Chapter 1 | Grounds for establishment of corporation | Type of corporation |

| Chapter 2 | Asset overview and system | Classification of assets |

| Inventory assets | ||

| Fixed assets | ||

| Off-balance fixed assets | ||

| Off-balance inventory assets | ||

| Chapter 3 | Asset management work | Fixed asset constant |

| Inventory level of spare materials | ||

| Supply plan establishment system | ||

| Acquisition of fixed assets | ||

| Management and depreciation of fixed assets | ||

| Depreciation of fixed assets | ||

| Disuse and disposition of fixed assets | ||

| Chapter 4 | Real estate management | Concept and type of real estate management |

| Real estate management work | ||

| Acquisition of real estate | ||

| Real estate study | ||

| Chapter 5 | Taxes related to assets | Review of value added tax upon purchase and sale of delivery vehicles |

| Value added tax upon selling of company house | ||

| Acquisition of generation plant building and facility upon completion of dam construction | ||

| Matters on acquisition/registration taxes according to national investment in kind | ||

| Payment of ship and pontoon acquisition tax | ||

| Problem of local tax on approval of booster station building | ||

| Chapter 6 | Accounting related to assets | Accounting on acquisition, disuse and disposition of fixed assets |

| Accounting on landscape trees | ||

| Accounting method on insurance gain | ||

| Land resale accounting know-how | ||

| Accounting on additional tax after payment of ship acquisition and registration taxes | ||

| Accounting on advertisement display boards | ||

| Arrangement of tangible and intangible assets according to implementation of financial accounting standards | ||

| Questions related to accounting on fixed assets | ||

| Chapter 7 | Asset-related system | Financial Accounting Standards Provision 3 Intangible Assets |

| Financial Accounting Standards Provision 5 Tangible Assets | ||

| Chapter 8 | Methods of using asset management and material management systems | Method of using asset management systems |

| Method of using spare material management systems |

3. Current Status and System of Infrastructure Asset Management Manuals in Developed Foreign Nations

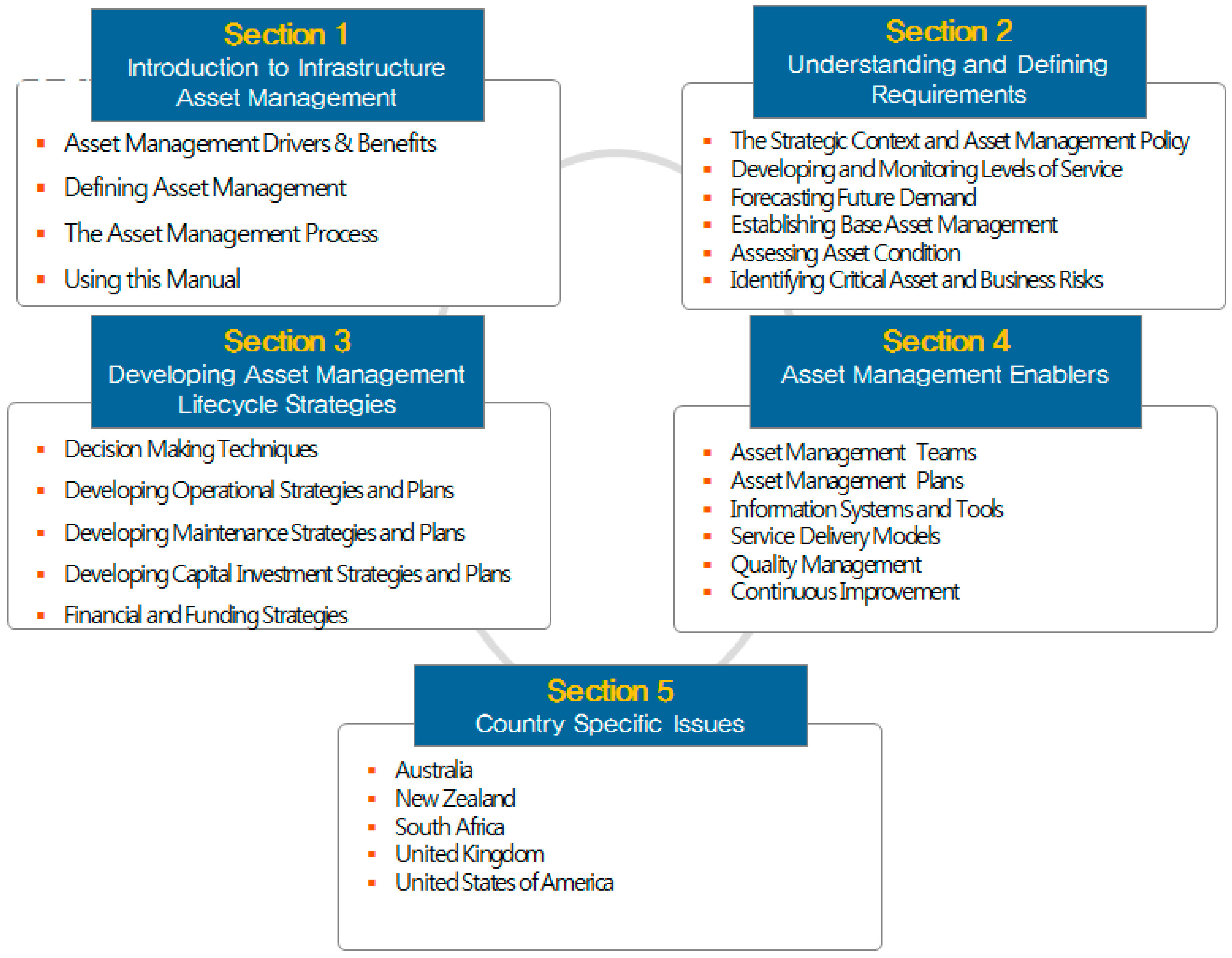

3.1. Australia

3.2. The United Kingdom

3.3. The United States

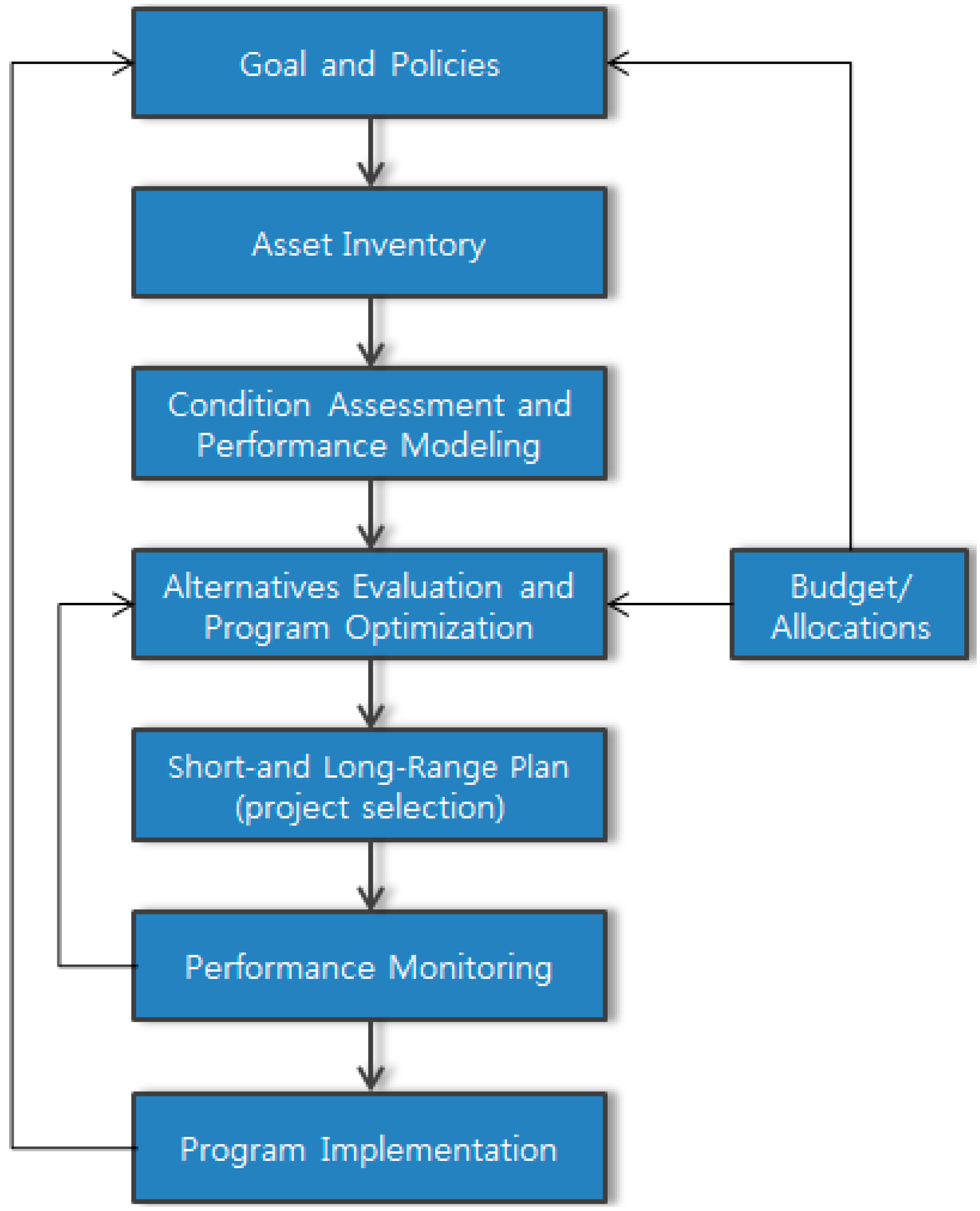

| Item | Major Details |

|---|---|

| Goal and Policies | Setting forth Level of Service requirements for infrastructures |

| Setting forth management objectives with consideration of safety, sustainability and economic feasibility | |

| Asset Inventory | Selection of assets subject to management |

| Input regarding infrastructure location, type, size, traffic volume, construction expense and maintenance history | |

| Condition Assessment and Performance Modeling | Analysis on the history of inspection, diagnosis, maintenance and reinforcement |

| Evaluation of conditions and residual lifetime of existing infrastructures | |

| Evaluation of asset value of existing infrastructures | |

| Alternatives Evaluation and Program Optimization | Computation of budget necessary for accomplishing the target Level of Service |

| Composition of applicable scenarios for budget level | |

| Determination of optimal scenarios through asset evaluation and value evaluation for each scenario | |

| Short- and Long-Range Planning (Project Selection) | Establishment of maintenance program implementation planning based on scenario |

| Determination of program priority and selection of infrastructure subject to maintenance | |

| Establishment of short-term and long-term program implementation plans | |

| Program Implementation and Performance Monitoring | Implementation of a program for achievement of management objectives |

| Continued feedback management through monitoring of implementation results |

3.4. Analysis of Characteristics

| Classification | IIMM (Australia) | PAS-55 (UK) | AMP (US) | Note |

|---|---|---|---|---|

| Composition of manual | 5 Sections | 7 Chapters | 8 Chapters | |

| Government initiation | × | △ | ○ | |

| Generality | ○ | ○ | △ | The US focuses on the transit sector |

| Consideration of specific areas | × | × | △ | |

| Consideration of specific users | × | × | △ | |

| Consideration of maturity of each stage | ○ | × | × | IIMM considers maturity of stage |

| Cyclic structure | ○ | ○ | ○ | Structure in which asset management strategy/policy affects decision-making and offers feedback |

| Connection with ISO | × | ○ | × |

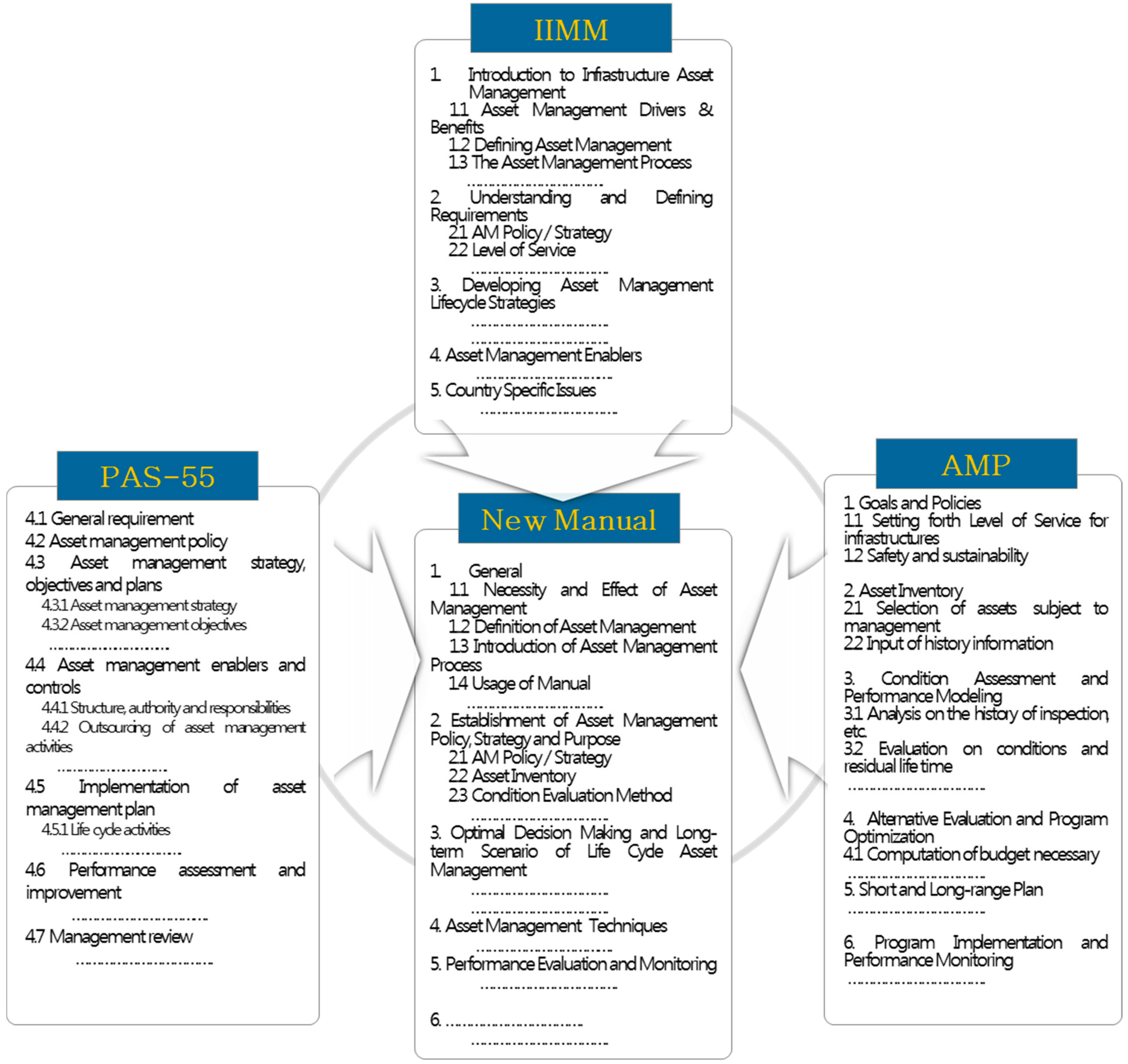

4. Suggestion of a Framework for an Infrastructure Asset Management Manual in Korea

4.1. General Infrastructure Asset Management Manual Connected to Global Asset Management Manuals

4.2. Manual with Consideration of Asset Management Experience of Ordering Authority

| Type | Experience Level | Criteria | Recommended Application Period |

|---|---|---|---|

| Simple type (A) | Beginner | Focuses on the basics of infrastructure asset management | 1–4 years |

| Maximal utilization of existing maintenance data for conversion from infrastructure maintenance to asset management | |||

| Standard type (B) | Intermediate | Focuses on the essential basics of foreign asset management manuals | 5–10 years |

| Detailed type (C) | Advanced | In-depth steps for more advanced asset management | 10 years or longer |

| IIMM (Australia) | PAS-55 (UK) | AMP (United States) | New Draft (Sustainable Infrastructure Asset Manual, SIAM) | Simple Type (A) | Standard Type (B) | Detailed Type (C) | Note |

|---|---|---|---|---|---|---|---|

|

|

| 1. General | Introduction and use of asset management | |||

| 1.1 Necessity and Effect of AM | ○ | ○ | ○ | ||||

| 1.2 Definition of AM | ○ | ○ | ○ | ||||

| 1.3 Introduction of the AM Process | ○ | ○ | ○ | ||||

| 1.4 Usage of Manual | ○ | ○ | ○ | ||||

| 2. Establishment of Asset Management Policy, Strategy and Purpose | How to establish AM policy, strategy and purpose | ||||||

| 2.1 AM Policy/Strategy | ○ | ○ | ○ | ||||

| 2.2 Asset Inventory | ○ | ○ | ○ | ||||

| 2.3 Condition Evaluation Method | ○ | ○ | ○ | ||||

| 2.4 Prediction of Future Demand | × | ○ | ○ | ||||

| 2.5 Level of Service | ○ | ○ | ○ | ||||

| 2.6. Continuous Plan | × | × | ○ | ||||

| 3. Optimal Decision-making and Long-term Scenario of Lifecycle Asset Management | Optimal analysis/establishment and long-term scenario | ||||||

| 3.1 Decision-making Techniques (BCA, MCA) | ○ | ○ | ○ | ||||

| 3.2 Operational Strategies and Plans | × | × | ○ | ||||

| 3.3 Maintenance Strategies and Plans | × | × | ○ | ||||

| 3.4 Capital Investment Strategies and Plans | × | × | ○ | ||||

| 3.5 Selection of Target Infrastructures and Determination of Priorities | ○ | ○ | ○ | ||||

| 3.6 Computation of a Budget for Achieving the Target Level of Service | ○ | ○ | ○ | ||||

| 3.7. Financing and Funding Strategies | ○ | ○ | ○ | ||||

| 3.8 Applicable Scenarios for the Budget Level | × | ○ | ○ | ||||

| 3.9 Determination of the Optimal Scenario through Asset and Value Evaluation for Each Scenario | × | ○ | ○ | ||||

| 3.10 Establishment of a Maintenance Program Implementation Plan based on the Scenario | × | × | ○ | ||||

| 4. Asset Management Techniques | Separate elements that allow for AM | ||||||

| 4.1 AM Organization (Structure/Authority and Responsibility, Training, Communication/Participation) | △ | ○ | ○ | Possible only with function | |||

| 4.2 Information Systems and Tools | △ | ○ | ○ | Possible with Excel | |||

| 4.3 Risk Management (Law, Demand management, etc.) | ○ | ○ | ○ | ||||

| 4.4 Service Procurement Method | × | ○ | ○ | ||||

| 4.5 Quality Management | × | × | ○ | ||||

| 5. Performance Evaluation and Monitoring | Performance evaluation and monitoring | ||||||

| 5.1 Performance and Condition Monitoring | ○ | ○ | ○ | ||||

| 5.2 Investigation of Asset-related Failures, Incidents, etc. | × | × | ○ | ||||

| 5.3 Audit and Records | × | ○ | ○ | ||||

| 5.4 Continuous Feedback with Monitoring | ○ | ○ | ○ | ||||

| 6. Foreign Examples | ○ | ○ | ○ | AM examples of different nations | |||

| 6.1 Australia | |||||||

| 6.2 New Zealand | |||||||

| 6.3 United Kingdom | |||||||

| 6.4 United States of America | |||||||

| 6.5 Korea | |||||||

| 7. Asset Management Forms and Templates | ○ | ○ | ○ | Forms needed for AM | |||

| 7.1 Establishment of AM Policy, Strategy and Purpose | |||||||

| 7.2 Establishment of Lifecycle AM Strategy and Long-term Scenarios | |||||||

| 7.3 AM Techniques | |||||||

| 7.4 Performance Assessment and Monitoring | |||||||

| 7.5 Other | |||||||

| 8. References | ○ | ○ | ○ | References needed for AM | |||

| 8.1 IIMM | |||||||

| 8.2 PAS-55 | |||||||

| 8.3 FHWA Manual | |||||||

| 8.4 Others |

4.3. Systematic Manual with Consideration of User Convenience

4.4. Cyclic Process in Which Infrastructure Policy Is Connected to the Decision-Making Step

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- National Settlement Report for 2011 Fiscal Year. Available online: http://korea.na.go.kr/ (accessed on 22 November 2015).

- Internal Data from the Ministry of Strategy and Finance, 2013. Available online: http://english.mosf.go.kr/ (accessed on 22 November 2015).

- Current Status of Direction of Capital in Japan; Japanese Ministry of Land, Infrastructure, Transport and Tourism: Tokyo, Japan, 2013.

- Martin, D.; Paul, N.S. Five Countries pioneering Accrual Budgeting and Accounting in Central Government. Available online: http://www.intosaijournal.org/technicalarticles/technicaljan04b.html (accessed on 3 November 2015).

- A Study on the Implementation of Government Capital Asset Accounting and Depreciation; Ministry of Strategy and Finance: Sejong, Korea, 2010. (In Korean)

- Hong, S.H.; Kim, T.J.; Jeong, D.U. 3rd Basic Plan for Safety and Maintenance of Infrastructure; Korea Infrastructure Safety and Technology Corporation: Seoul, South Korea, 2012. [Google Scholar]

- Data on Facility Management System; Korea Infrastructure Safety and Technology Corporation: Seoul, South Korea, 2014. (In Korean)

- Statistics Yearbook of Maintenance; Korea Facilities Maintenance Association: Seoul, Korea, 2014. (In Korean)

- General Construction Statistics DB; Construction Association of Korea: Seoul, Korea, 2014. (In Korean)

- Internal Data from Ministry of Land Infrastructure and Transport, 2013. Available online: http://www.molit.go.kr/ (accessed on 22 November 2015).

- Internal Data from the Korea Expressway Corporation, 2011. Available online: http://www.ex.co.kr/ (accessed on 22 November 2015).

- Asset Management Manual; Korea Water Resources Corporation: Daejeon, Korea, 2006. (In Korean)

- Transportation Asset Management in Australia, Canada, England, and New Zealand; Federal Highway Administration: Washington, DC, USA, 2005.

- Chae, M.J.; Jin, G.H. A Study on Introduction of Asset Management System in Infrastructures such as Roads and Railroads; Korea Institute of Construction and Technology: Goyang, Seoul, 2008. [Google Scholar]

- International Infrastructure Management Manual (IIMM); National Asset Management Support: Wellington, New Zealand, 2011.

- The Institute of Asset Management. IAM Strategy for Members 2014–2019. Available online: https://theiam.org/Strategy (accessed on 5 October 2015).

- PAS-55 Asset Management; British Standards Institution: London, UK, 2012.

- Shrestha, K.; Shrestha, P. A GIS-enabled Cost Estimation Tool for Road Upgrade and Maintenance to Assist Road Asset Management Systems. Constr. Manag. 2014, 2014, 1239–1248. [Google Scholar]

- GASB43 (Basic Financial Statement and Management Discussion and Analysis for State and Local Government); Governmental Accounting Stands Board: Washington, DC, USA, 1999.

- 2009 Report Card for America’s Infrastructure; ASCE: New York, NY, USA, 2009.

- Asset Management Primer; Federal Highway Administration: Washington, DC, USA, 1999.

- 2010 Status of the Nation’s Highways, Bridges, and Transit: Conditions & Performance; U.S. Department of Transportation: Washington, DC, USA, 2010.

- Khaled, E.A.; Richard, D.; Tieling, Z. The strategic role of engineering asset management. Int. J. Prod. Econ. 2013, 146, 227–239. [Google Scholar] [CrossRef]

- Ruikar, K.; Anumba, C.J.; Carillo, P.M. VERDICT—An e-readiness assessment application for construction companies. Autom. Constr. 2006, 15, 98–110. [Google Scholar] [CrossRef]

- Lin, L.K.; Chang, C.C.; Lin, Y.C. Structure development and performance evaluation of construction knowledge management system. J. Civil Eng. Manag. 2011, 17, 184–196. [Google Scholar] [CrossRef]

- Bamber, C.J.; Sharp, J.M.; Castka, P. Third party assessment: The role of the maintenance function in an integrated management system. J. Qual. Maint. Eng. 2006, 10, 26–36. [Google Scholar]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lee, S.-H.; Park, S.; Kim, J.M. Suggestion for a Framework for a Sustainable Infrastructure Asset Management Manual in Korea. Sustainability 2015, 7, 15003-15028. https://doi.org/10.3390/su71115003

Lee S-H, Park S, Kim JM. Suggestion for a Framework for a Sustainable Infrastructure Asset Management Manual in Korea. Sustainability. 2015; 7(11):15003-15028. https://doi.org/10.3390/su71115003

Chicago/Turabian StyleLee, Sang-Ho, Sanghoon Park, and Jong Myung Kim. 2015. "Suggestion for a Framework for a Sustainable Infrastructure Asset Management Manual in Korea" Sustainability 7, no. 11: 15003-15028. https://doi.org/10.3390/su71115003

APA StyleLee, S.-H., Park, S., & Kim, J. M. (2015). Suggestion for a Framework for a Sustainable Infrastructure Asset Management Manual in Korea. Sustainability, 7(11), 15003-15028. https://doi.org/10.3390/su71115003