1. Introduction

In accordance with the proposal of the Triple Bottom Line (TBL), it is necessary to consider social, economic and environmental aspects when it comes to policies for sustainability in an integrated way. This feature turns the evaluation of sustainability into a problem that involves several aspects. Therefore, the multi-criteria methods seem to be the most suitable for the investigation of this matter.

Another important aspect associated with the development (sustainable or not) of the companies is the provision of energy. Even with the search for alternative energy sources, the use of fossil fuels, such as oil and gas, still effectively participates in the provision of energy in the early twenty-first century. Due to the impacts caused by the use of this type of energy source, it becomes essential to develop mechanisms to assess the effects on the sustainability caused by members of the supply chain associated with the oil and gas industry. Brazil was chosen because it is an emerging economy with great potential for economic growth in the long term. Apart from this, the country has great potential to become an oil exporter in the next decade.

This work aims to build a multi-criteria model for the classification of the degree of sustainability of organizations that work in providing supplies to the oil and gas industry.

After an analysis of sustainability evaluation studies in the literature, we constructed a benchmark for quality valuation of this subject based on a set of criteria grouped in three dimensions: economic, environmental and social. A questionnaire was constructed and was applied to a group of supplier companies of the oil and gas industry. The data collected by the application of this questionnaire were submitted to the ELECTRE TRI sorting algorithm. This procedure makes it possible to obtain a classification of the degree of sustainability for the surveyed organizations. It is important to highlight that the processes of data collection and the application of ELECTRE TRI were observed and evaluated in order to identify the feasibility and the difficulties of this model implementation.

For this reason, the results of this work neither fit into the context of a prescription, nor do they intend to describe the stage of the sustainable practices in the Brazilian oil and gas industry as a whole. This work consists of seven sections. The first section is the introduction.

Section two reports on the central concepts associated with the sustainability issue.

Section three reports on the main aspects associated with the suppliers of the oil and gas industries.

Section four presents the basic concepts of ELECTRE TRI.

Section five describes the modeling of a multi-criteria problem.

Section six presents the results, and

Section seven reports the findings of the research. A list of references can be found at the end of the paper.

2. Sustainability: Concepts and Definitions

In order to remain competitive was addressed the need for paradigm shifts in companies’ policies in the oil and gas industries [

1]. Among the changes proposed in this work, we highlight the need for more transparency, better practices of corporate governance, and an increase in partnerships marked by symbiosis.

Sustainability has three broad components, often described as “people, planet and profits” [

2]. Organizations need to be aligned with the concept of The Triple Bottom Line (TBL) in order to develop the dimensions mentioned before. The main objective of the concept is to highlight that reports describing the performances on environmental and social spheres have the same importance of financial reports. Thus, as consequence, a more comprehensive view of the business activities is achieved, in a more responsible approach.

Other proposals to evaluate sustainability have been considered to be incorporated in the TBL model. To the former dimensions (environmental, social and economic) was added, for example, the spatial and cultural dimensions [

3]. However, it is plausible to consider that the spatial dimension could be included as part of the environmental dimension analysis, as well as that the cultural dimension could be included as a part of the social dimension.

TBL can be considered a conceptual view with a measurement of the inter-relationships between the dimensions of sustainable development: eco-environmental, eco-social, social-environmental and social-eco- environmental [

4].

This TBL concept synthesizes and emphasizes as an important instrument in the implementation of organization sustainability [

5,

6,

7,

8,

9,

10,

11,

12].

2.1. Economic Aspects of Sustainability

The economic dimension of sustainability evaluates the economic capacity needed for companies to be able to increase their value in the long term. The economic dimension is also linked to the relationships that companies develop with their shareholders and investors. Its importance is obvious and is related to the organization’s financial health in the short and long term [

4].

However, to the TBL’s concepts was pointed the need of joint analysis of the economic and the other aspects included in this own concept [

13]. Economic sustainability requires efficient allocation and management of resources in a social area with large investment flows.

The paradigm is the integration of the economy, environment and society, led and carried out jointly by three major groups: entrepreneurs, government and civil society organizations [

14]. A relevant issue was added: How the environmental investments are translated into financial returns for the corporate businesses and to what extent the private sector must assume responsibility for the public areas and for the social development [

15]?

Many times, the higher costs associated with social and environmental projects restrict the investments in these fields. This is the most relevant conflict regarding the discourse and the practice of sustainability inside the organizations.

2.2. Environmental Aspects of Sustainability

Environmental sustainability requires prioritization of research on the use of renewable natural resources, development and use of cleaner technologies, conservation and recycling of resources and energy, effective legislation for environmental protection, control, mitigation and compensation of the negative environmental impacts, and environmental education [

13].

Environmental aspects of development are examined through the transition from traditional economy, centered in economic growth and wealth accumulation, to green economy, which is based on responsible development and is interested in the economic growth impacts on society [

16]. In

Table 1, we can see the differences between the concepts regarding traditional and green economy.

Table 1.

Another way of economic thinking.

Table 1.

Another way of economic thinking.

| Name | Objective | Environment |

|---|

| Conventional economic | Promotion of economic growth | Narrow concern with scarce resources |

| Conventional ecological | Sustainability of the ecosystem and its species | Directly responsible for the ecosystem and its species |

| Ecological Economic | Sustainability of the ecological economic system combined | It is inserted in the economic system in a special way, not only as given data. |

2.3. Social Aspects of Sustainability

Social sustainability requires the reduction of inequality among the living standards, a better distribution of income, the meeting of tangible and intangible necessities, the search for production processes that maintain and respect the roots and characteristics of each culture and local control, and the mitigation and compensation of the negative social impacts [

13].

The social dimension of the TBL concept is associated with the acting responsibly in the company’s relationship with the society. This relationship is guided by the legal obligations, minimum conditions for their operation, and for the ethical and responsible performance. For instance, legal obligations represent the country’s labor laws prohibiting forced labor and regulating working conditions. Business ethics should go beyond the minimum required by law and ensure transparent, honest and egalitarian processes. The social dimension is also related to respectful treatment of everyone concerned with the company and the actions involving society.

Socially responsible company depends on the involvement of all its members, workers, managers, executives and suppliers [

17]. Moreover, a socially responsible company is characterized by the compliance with the rules of democracy, not seeking to obtain undue advantages or special treatment.

3. The Oil and Gas Industry

Three major groups in the oil and gas industries are segmented: Upstream—exploration and production—Midstream—transportation and refining—and Downstream—distribution of products and derivatives [

18].

The upstream can be considered the main block by different industrial characteristics. It is the stage with highest investments and in which new products are frequently being developed. This stage is more complex than the others. The upstream stage covers all, from exploration to discovery of reservoirs, passing through regular production and operation, which includes drilling and completion. The completion of wells, the costly and risky process of pilot drilling, assembly and operation of platforms (if offshore exploration) are examples of activities in this stage.

The industry is divided in two major groups: upstream and downstream [

19]. Thus, the downstream becomes the set of activities in charge of the oil transportation to the consumers, going through refining and distribution.

The refining and transportation segments (downstream) include the distribution of crude oil and gas to derivative production units. Large pumps and compressors, steam turbines, furnaces, towers, pressure vessels and systems of supervisor control, are the most relevant materials and equipment. The mechanical maintenance and the assembly of industrial plants, pipelines and storage systems are the primary services.

As shown in

Table 2, sub-classifications and the major materials and equipment used, are completed with other equipment [

20].

The equipment, materials and services for the oil and gas industry are generally offered with a high level of customization. Often, the product or service needs to be specially developed under specific condition of a given process. The large supplies of equipment for refineries include motors, pumps, compressors and other equipment that allows control of the refining process. This equipment is developed for the existing condition of the refinery process, so it is specific and specially designed. The same thought is applied to the development of special equipment for different operating conditions in the upstream stage.

In the Brazilian supplying market for the oil and gas industry, it is observed that, in order to meet the growing demand of new projects of Petrobras, foreign manufacturers have opened new branches and new offices or manufacturing plants in Brazil. In the late 1920s, most foreign companies decided to build partnerships with Brazilian suppliers settled in Brazil (ANP—National Agency of Petroleum, 1999) in search of the nationalized projects.

Table 2.

Major equipment of the oil and gas industry.

Table 2.

Major equipment of the oil and gas industry.

| Phase | Main materials and equipment | Main services |

|---|

| Upstream | Seismographs, explosives, main-frames, pipes, flexible lines, large turbine generators, pumps and compressors. | Geophysical survey and processing of soil, well log rendering and conformation assessment; well drilling and cementing; chartering of vessels to support the launch of submerged lines |

| Downstream | Large pumps and compressors, steam turbines, furnaces, towers, pressure vessels and supervisory control systems. | Mechanical maintenance and assembly of industrial plants, pipelines and storage systems. |

In the late 1920s, the National Agency of Petroleum, Natural Gas and Biofuels (ANP) was created with the aim of regulating the activities relating to oil, natural gas and biofuels, which then ceased to be a government monopoly. Among various duties of this agency, regarding oil refining, ANP allows companies to build, operate and expand refineries and plants for the processing and storage of natural gas, and to transport oil, oil-derived products and natural gas.

However, its major efforts are linked with biddings for the concession of oil well operation by interested companies, hence ending the monopoly. Among the various regulations imposed by the agency to the applicants since the first round of bidding, ANP has established a scoring system in its auctions that combines the financial bid with a commitment to purchase local goods and services—The Local Content Plan. ANP has incorporated the criterion of nationalization degree in the selection of exploration areas. Thus, the concern with the domestic industry development was reaffirmed.

Considering that the opening of the Brazilian oil industry to private investments should also provide opportunities to increase the competitiveness of the national suppliers, ANP and the several representations of the industrial sectors have debated, defined and proposed mechanisms to stimulate future utility companies to purchase domestic goods and services. Since operating under competitive conditions comparable to the international standards, there would be a natural preference for local delivery. This has been considered, because of the comparative advantages, e.g., the use of national currency and local language, the convenience of technical and post-sales services, and the supply of parts and components for machines, among others.

4. Indicators for the Evaluation of Sustainability

The result of a joint effort of the API (American Petroleum Institute) and the IPIECA. (International Petroleum Industry Environmental Conservation Association) is a guide for voluntary reporting of sustainability in the oil and gas industries. This guide sets out a proposal of indicators directly related to the oil and gas industry, both internally in its process, and externally in its relations with stakeholders. A particular criterion of this indicator system is the health and safety of employees, which is an additional dimension beyond those already defined by the concept of The Triple Bottom Line. The reason to include this item is the potential risk classification of processes and products comprehended by the oil and gas industry [

21]. In summary, IPIECA & API aim to develop and promote solutions that can be socially and economically viable for the oil and gas industry.These organizations provide a forum for discussion and their members are committed to

Contribute to the sustainable development and provide secure and renewable energy with social and environmental responsibility;

Run their operations and activities with ethics;

Develop and promote the implementation of practices and solutions with other segments of the oil and gas industry;

Engage their stakeholders considering their expectations, ideas and visions, and work jointly with governmental and non-governmental organizations.

Another widespread indicator system is the Dashboard of Sustainability. It is a tool developed by Consultative Group on Sustainability Development Indexes (CGSDI). The mission of this advisory group is promoting cooperation, coordination and strategies among individuals involved in developing and using sustainable development indicators [

22]. The Dashboard of sustainability contains four dimensions: (a) ecological (water, soil and air quality and level of toxic waste); (b) economic (level of employment, investment, productivity, income distribution, competitiveness, inflation and efficient use of materials and energy); (c) social (quality of health, level of violence, poverty, education, governance, military spending and international cooperation); and (d) institutional (development level of science and technology and monitoring of local sustainable development).

The model of the Dashboard of Sustainability is an important tool to assist decision makers, public or private ones, in rethinking their development strategies and setting goals [

22]. Its use is widely disseminated in the sustainability analysis of nations, countries and regions. By presenting the performance in several dimensions of the sustainability, and in such an easy way to understand that the Dashboard of Sustainability is officially recognized by the United Nations and the Eurostat (the Statistical Office of the European Communities). Dashboard of Sustainability as a structural indicator is applied by European Communities [

23].

The Environmental Sustainability Index (ESI) was introduced in 2002 at the World Economic Forum by researchers from Yale and Columbia. It is based on five components: (a) environmental systems; (b) reduction of the environmental pollution; (c) reduction of human vulnerability; (d) social and institutional capacity; and (e) global responsibility. This index is composed of 21 indicators associated with 76 variables [

16].

The financial market represented by the New York Stock Exchange (NYSE) and Bovespa also looks for ways to award the companies acting responsibly. Sustainability is defined as “creating long term value for shareholders by exploiting opportunities and managing risks derived from economic, social and environmental developments” [

4,

24].The Dow Jones Sustainability Index (DJSI) established in 1999 defines, classifies and ranks the companies according to sustainability criteria. The index includes the three highest ranked companies in each of the 68 industrial categories used by the family of Dow Jones indexes. The criteria are:

Transparency

Distribution of Wealth

Quality of Life

Awareness of Environmental Risk

Use of Resources

Global Warming

Valuation of Natural Resources

Advancement of Technology and Innovation

Corporate Learning

The Bovespa, in time, has created the Corporate Sustainability Index of Bovespa (ISE). The ISE has developed a portfolio comprising shares of companies that have best performed in all dimensions of corporate sustainability. It has been created to become the benchmark for socially responsible investment and also an inducer of the good practices in the Brazilian capital market.

The indicator is calculated by BOVESPA in real time throughout the trading day, considering the prices of the last trades carried out in the spot market. The stocks of the companies participating in ISE were selected in terms of liquidity. The ISE portfolio is weighted for the market value of each company’s assets.

The approach of the Ethos Institute, in a social perspective of the social responsibility of the enterprise, can be used as a tool for comparative analysis [

25]. Many other indexes were introduced regarding the Corporate Social Responsibility (CSR) in the first decade of this century. Evaluation systems like the Dashboard of Sustainability, Barometer, Global Reporting Initiative (GRI) and the Dow Jones Sustainability Index are based on the classical concept of sustainable development as defined by the Brundtland Report [

4]. However, GRI and the Dow Jones Sustainability Index reflect the business environment by means of TBL’s concept. Among all of these, the GRI underlines the importance of outlining a sustainability strategy. Hence, GRI is the most complete because it includes a guide for the organizations on how to define the sustainability goals at all levels. Besides, GRI suggests the inclusion of sustainability targets in the variable payroll of the organization along with other organizational goals.

It’s proposed the Method of Evaluation of Sustainability Indicators (MESI) [

26]. The concept used by Oliveira is based on the model of sustainability proposed by Sachs with four dimensions (economic, environmental, social and cultural) [

3,

26]. To evaluate the status or phase of the indicator (under implementation, implemented, formalized, certified, and in use for continuous improvement), was used a rating scale [

26]. After evaluation of the score, this score is aggregated into a “scoring” system to classify the organization in the face of its sustainability practices. The valuation indicators follow the original methodology and occur in three phases. In each phase, a value corresponding to the situation of the company is assigned on a scale from 0 to 3, as can be seen in

Table 3. Thus, each indicator may receive the maximum Grade 3 in each phase, if successfully assessed, amounting to a maximum score of 9 in every aspect. The phases are:

D—Development or existence of any policy or procedure. It represents the organization’s proactivity in following up the indicator development, if there is any concern whatsoever regarding its control;

I—Implementation of the procedure adopted or planned. Questions the existence of actions to control, even on informal levels;

V—Verification and control adopted in the pursuit of continuous improvement. It reflects the use of information learned as a consequence of improvement in the control process.

Table 3.

Allocation of value for stage.

Table 3.

Allocation of value for stage.

| Stage “D”—Stage existing for development of the indicator |

| 0 | No indicators; |

| 1 | An indicator informally exists in the organization, i.e., there is no documented records regarding its application; |

| 2 | The indicator existence is noted and is formally recorded, but there is no practice of it on a day-to-day basis; |

| 3 | The indicator exists and is part of the organization’s formal policy and is practiced and known by all stakeholders. There is an organization commitment to its practice; |

| Stage “I”—Implementation of the procedure adopted or planned |

| 0 | The indicator is not implemented; |

| 1 | The first indicator has been implemented to 30%; |

| 2 | The second indicator has been implemented to 70%; |

| 3 | The indicator has been implemented entirety; |

| Stage “V”—checking or control of continuous improvement |

| 0 | There is no verification and/or control of the indicator; |

| 1 | An informal verification and/or control exists |

| 2 | A formal process of verification and control exists, but it does not serve as a tool for corrective or preventive actions; |

| 3 | There is verification and it is used as a base for the organization’s continuous improvement in pursuit of organizational excellence. |

5. Principles of the ELECTRE TRI Method

This study reviews the new integrated indicator system for strategic environmental assessment (SEA) [

27].This integrated indicator system combines environmental and non-environmental issues and can be used for retrospective and predictive assessments as applied with SEA of development in Pudong New Area, Shanghai, China.

Another reviewed application was reported [

28]. They developed some environmental performance indicators (EPIs) involving environmental impacts. This study tailored EPI for the Norwegian defense sector and made it feasible to report achievements of the environmental sector.

In the North American context—Vancouver’s Vital Signs (Vancouver Foundation), Seattle’s Happiness Initiative and LEED-ND (US Green Building Council) was raised attention the need for a decisive policy change by a comparative analysis of three sustainability indicator systems [

29].These cases have shown some important outcomes toward including a new policy boundary as a political contribution to government.

In order to progress toward the sustainable development, it is important to use internationally recognized indicators and tools. As a dynamic tool for the management of environmental, social and economic information was measured the sustainability in urban areas and studied the development and the application of a system of indicators [

30].This system was applied to a case study using the Greater Thessaloniki Area, Greece, a regional place with considerable socio-economic development.

The decision-making process in a complex environment involves the consideration of multiple criteria and should be modeled of this way (MCDA) [

31,

32,

33,

34,

35]. The solution of the problem depends on a number of people, each having their own point of view, often conflicting with the others [

36]. MCDA methods are classified into the following categories: (a) multi-attribute utility theory (MAUT); (b) interactive methods; and (c) methods of outranking [

37].

In the outranking methods, a finite set of alternatives—denominated by the letter “A”—valued by a family of criteria—denominated by the letter “F”—are used to build relations between the alternatives, based on the valuations established by the decision maker. The building of this relationship is based on a non-compensatory logic that privileges more balanced choices.

The best-known family of subordination methods is the ELECTRE family (Elimination Et Choix Traidusaint la Réalité). These methods has been adopted in support of the decision-making process [

38]. The ELECTRE family consists of the following methods: ELECTRE, ELECTRE II, ELECTRE III, ELECTRE IV, ELECTRE IS and ELECTRE TRI [

38,

39,

40,

41,

42,

43,

44].

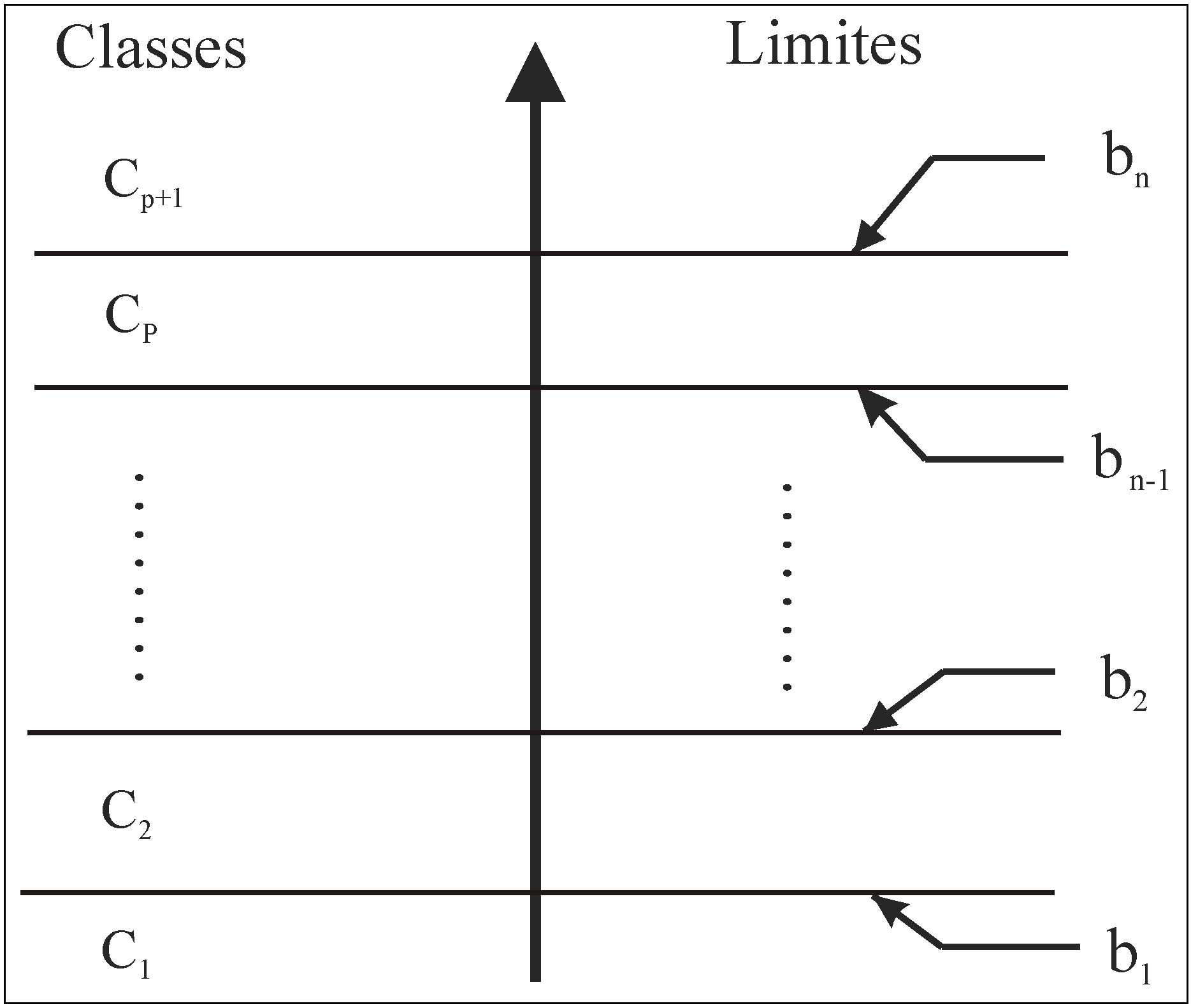

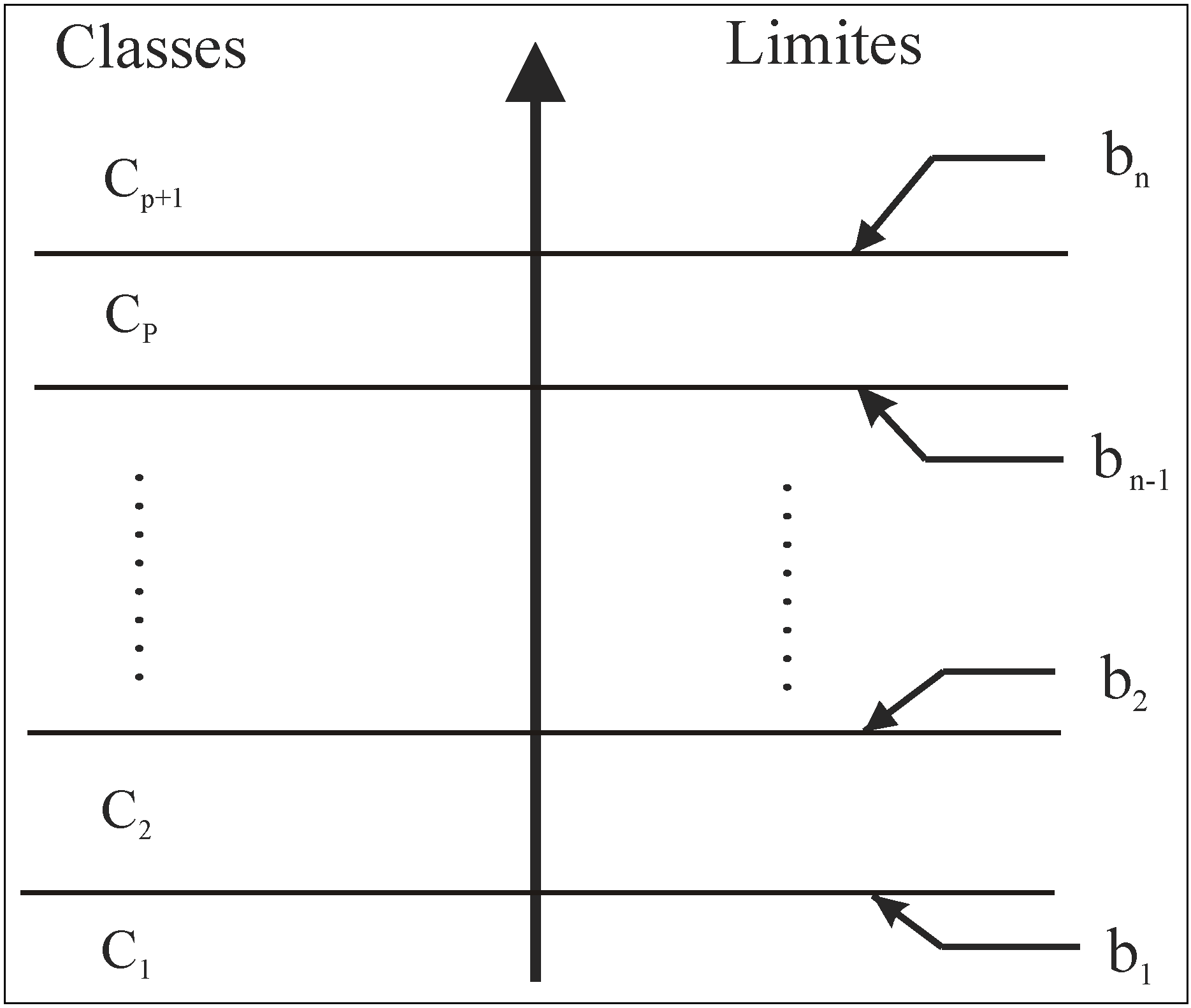

The ELECTRE TRI method is characterized by dealing with specific problems of ranking. Given a vector “A” of alternatives, this alternatives are associated with a set of ordered classes C = [C1, C2, ....., Cn].

This is done by considering the performance of “A”, a vector of one set of criteria F = [g1, g2, ..., gm].

Figure 1 illustrates a set consisting of (

p + 1) classes, delimited by the threshold

p of the classes. A generic class—denominated by Ch—is delimited by a lower threshold (bh) and an upper threshold (bh − 1).

Figure 1.

Classes of equivalence ELECTRE TRI.

Figure 1.

Classes of equivalence ELECTRE TRI.

This method integrates functions that support the decision-maker in the process of resolution and reduce the cognitive effort required in the modeling phase [

43,

44].The ELECTRE TRI ranks the alternatives by following two consecutive steps: (a) to build a subordinate vector S—denominated by the letter “S”—which characterizes how the alternatives are compared to the class boundaries, and (b) to explore the S relationship through classification procedures.

5.1. Relations of Subordination and Credibility in the ELECTRE TRI

The relations of subordination were constructed in order to allow a comparison with an alternative to a standard threshold (bh). aSbh statement means that “

a does not have a worse record than the threshold (bh)”. As for validation of aSbh assertion, it is necessary to observe two conditions:

Concordance: for a claimed aSbh—or bhSa—to be accepted, there must be sufficient criteria to support it.

Non-discordance: when the condition of concordance is not met, none of the criteria in the minority should oppose aSbh—or bhSa—assertion.

The following steps are taken in order to found this relationship:

Compute the partial concordance index cj (a, bh) and cj (bh, a)

Compute the overall concordance index c (a, bh)

Compute the partial discordance index dj (a, bh) and dj (bh, a)

Compute the fuzzy relationship of subordination as the credibility index σ (a, bh)

Determine a λ cut off level of fuzzy logic for a relationship of subordination. That is:

In these equations:

pj, qj and vj are, respectively: preference, indifference and veto threshold limits of the criterion j.

wj is the weight of the criterion j.

The credibility degree of the reported relationship σ (a, bh) expresses how likely is to “believe” that “a subordinate (bh)” is consistent with the overall concordance index cj (a, bh) and the discrepancy index dj (a, bh).

The translation of a fuzzy relationship of subordination obtained through the relation of subordination S is made under the assumption of a level λ at the cut-off. This λ level of cut off—denominated from now on just λ—is considered the smallest index value of credibility consistent with the statement of “a subordinate sbh”. That is, if σ (a, bh) ≥ λ, so aS bh.

5.2. Procedures for Classification

The role of exploration proceedings is give possibility to investigate the different possible ways to compare an alternative “a” with the standard set for the class in which “a” should be included. Two classification procedures are evaluated:

It’s suggested that the divergence of classifications is common in situations where there are conflicting criteria (for example: the cost and quality), where divergence should not be considered a flaw in the modeling [

45]. So, when there is divergence between ratings, either pessimistic or optimistic, the classifier must adopt one of the two classifications according to his profile (more demanding or less demanding).

6. Construction of the Multi-Criteria Model

Based on concepts related to supply chain management systems and indicators for assessing sustainability was developed a system for the sustainability evaluation, with specific focus on the evaluation of supply organizations for the oil and gas industries [

46]. For categorizing companies according to sustainability degree, this research explores the application of ELECTRE TRI method as an algorithm on the multi-criteria data [

46].The following steps undertaken in this modeling can be seen in the next topics.

6.1. Definition of the Set of Criteria and Assembly of these Dimensions of the Sustainability

The criteria set, from the theoretical review on sustainability, became an indicator of the sustainability evaluation, and was validated by an Expert Committee (EC) composed of five experts in at least one of the matters of Supplier Selection or Sustainability Evaluation.

The criteria were grouped by the following dimensions: environmental, economic and social-development,

i.e., the dimensions covered by the Triple Bottom Line. Following is the criteria list grouped by dimensions:

6.2. Definition of the Alternatives to be Evaluated

The alternatives are companies that have been vendors for Petrobras—a Brazilian Petroleum Company—affiliated with ABIMAQ (Brazilian Association of Machinery Industries) and that have also covered the main segments of the oil and gas industries. Another selection criterion is the existence of an easy access to information from companies. Thus, we selected the companies that had information available on websites and public reports. Many questions are related to commercial benefits for the company. Confidentiality can bring competitive advantages to the company. The score for each aspect should reflect the current condition of the company. To ensure research credibility, the companies’ data came from reliable and trustable sources.

The final group consisted of five companies producing different products for different applications in the oil and gas industry. This is a positive aspect because the model developed can be tested on companies using different processes.

The names of the companies involved in the research are kept anonymous. Hence, we used the Greek letters Alpha, Beta, Gamma, Delta and Theta to denominate them. Alpha is a manufacturer of large compressors that works essentially at the level of the refining process. Its headquarters and facilities are in Europe. Beta is a Brazilian company that manufactures mostly reactors and towers for the refining process, it has, however, some complex equipment as: Christmas Trees used for the exploration and production process of oil and gas. Gamma is a Brazilian manufacturer of boat shipyard that supports processes such as offshore well drilling and exploration and oil production. Delta is the largest company investigated. It is a giant in the American industry of large diesel machines, tractors, processors and group generators. Theta is a Brazilian manufacturer of electric motors and large generators. The latter two companies have a presence in all the market segments of the oil and gas industry.

6.3. Preliminary Analysis of the Data Collected

The companies’ performance data were collected from interviews with experts, one expert for each company, and were based on a discrete scale from 0 to 9, with intervals of 1.0 [

26,

47].

Table 4 shows the consolidation of the data collected, which represents the aggregation of the scores obtained by the company and associated with each criterion. A preliminary analysis of the data in this table indicates that:

A rise of the development level has occurred in one of the economic indicators: “indicator of the average rate of return over the capital employed”.

The second more developed indicator is another economic indicator: “management of processes, products and services”. This indicates how mature the indicators’ development in this area is. However, in the context of economic indicators, it can be observed that the development of the indicators’ “national investments in technology” and “corporate governance” is not so mature.

A mixed trend in the context of social sustainability can be observed. Concerns about the employee life quality, their safety and welfare are common among these companies. In contrast, the “impact monitoring” and “relationship with society” are little developed.

Table 4.

Consolidation of data collected.

Table 4.

Consolidation of data collected.

| Name | Criteria | | Alfa | Beta | Gama | Delta | Teta |

|---|

| Social Sustainability | Indicator of employee satisfaction; | C1 | 3 | 9 | 2 | 9 | 8 |

| Indicator of investment in education and training; | C2 | 5 | 7 | 2 | 8 | 9 |

| Indicators of health and safety at work; | C3 | 6 | 9 | 9 | 5 | 9 |

| Indicator of the remuneration performance variable; | C4 | 3 | 7 | 5 | 9 | 6 |

| Indicator of interaction with the stakeholders; | C5 | 6 | 8 | 6 | 8 | 5 |

| Indicator of suppliers evaluation; | C6 | 4 | 3 | 4 | 2 | 5 |

| Indicator of minorities inclusion; | C7 | 9 | 6 | 2 | 8 | 3 |

| Indicator of the community’s level of independence from company; | C8 | 2 | 2 | 2 | 0 | 3 |

| Indicator of the SA8000 requirements’ monitoring | C9 | 8 | 5 | 2 | 5 | 4 |

| Environmental Sustainability | Indicator of energy efficiency and renewable energy; | C10 | 3 | 1 | 0 | 0 | 9 |

| Indicator of control of the industrial process aspects and impacts; | C11 | 8 | 5 | 0 | 5 | 7 |

| Indicator of proper treatment of waste; | C12 | 5 | 4 | 6 | 6 | 9 |

| Indicator of the product life cycle evaluation; | C13 | 5 | 5 | 1 | 5 | 5 |

| Indicator of suppliers evaluation; | C14 | 4 | 4 | 6 | 2 | 5 |

| Indicator of the use of water; | C15 | 5 | 7 | 5 | 4 | 7 |

| Economic Sustainability | Indicator of average rate of return over the capital employed | C16 | 8 | 9 | 9 | 9 | 9 |

| Indicator of performance in research and development | C17 | 4 | 3 | 4 | 1 | 7 |

| Indicator of investments in domestic technology | C18 | 2 | 6 | 6 | 2 | 6 |

| Indicators of corporate governance | C19 | 2 | 2 | 7 | 1 | 7 |

| Indicator of the management of processes, products and services | C20 | 9 | 9 | 6 | 9 | 9 |

| Indicator of evaluation of suppliers and the market | C21 | 8 | 7 | 4 | 4 | 8 |

| Indicator of engagement in development programs | C22 | 7 | 6 | 2 | 0 | 2 |

6.4. Results from the Implementation of ELECTRE TRI Method

The following steps were performed while applying the ELECTRE TRI to the data shown in the previous section.

6.4.1. The Reference Classes

The scoring scale applied to the data collected has ten scores: from 0 to 9. Hence, ten classes were defined: A, B, C, D, E, F, G, H, I, and J.

Table 5 presents these classes and their threshold limits (upper and lower).

Table 5.

Classes or categories of sustainability.

Table 5.

Classes or categories of sustainability.

| | Sustainability Classes | Lower Threshold | Upper Threshold |

|---|

UPPER

![Sustainability 06 01107 i005]()

LOWER | A | 8.5 | |

| B | 7.5 | 8.5 |

| C | 6.5 | 7.5 |

| D | 5.5 | 6.5 |

| E | 4.5 | 5.5 |

| F | 3.5 | 4.5 |

| G | 2.5 | 3.5 |

| H | 1.5 | 2.5 |

| I | 0.5 | 1.5 |

| J | | 0.5 |

6.4.2. Definition of the Thresholds of Preference (pj), Indifference (qj) and Veto (vj) for each Criterion

In order to use the ELECTRE TRI, it is necessary to define the thresholds of preference (pj), indifference (qj) and veto (vj) for each criterion.

These thresholds are derived from the scale used to judge the performance of each alternative under the criteria set. Such thresholds enable to observe the hesitation or uncertainty associated with human judgment. The definition of these thresholds takes into account that: 0 ≤ qj ≤ pj ≤ I/2, whereas j is a criterion of F and I is the interval between the thresholds of two classes.

Due to the characteristics of the scale that bears unitary intervals, in the result was I = 1.0, hence: 0 ≤ qj ≤ pj ≤ 0.5 for all criteria and all classes. We also considered that the scale consisted of several integer values, which implies that the results presented by the model are not sensitive to values of qj (bh) and pj (bh ) ε (0, 0.5). Thus, we used the thresholds of preference and indifference of qj and pj equal to zero, for all criteria and all classes.

Based on a consensus decision of the Expert Committee (EC) members, the threshold of veto was not enabled in the model. The main reason for this decision by the EC was that all the alternatives had already passed through a filtering process when they were built and selected.

6.4.3. Degrees of Credibility

Table 6 illustrates the values of the credibility degree of the subordination relation. These values were calculated based on the collected data. Among other information, the results of this table show that: (a) the credibility degree is 0.09 and the companies Alfa and Delta have a sustainability of class A; (b) the credibility degree is 0.18 and Gamma and Beta have a sustainability of class A; (c) a 0.27 credibility degree is assigned to Alfa, which places it at least in the class B of sustainability; (d) the credibility degree of Delta is at least of grade E, since its value is 0.45; and (e) the credibility degree of Gamma is 0.77, placing it at least in the class F of sustainability.

Table 6.

Classes of sustainability.

Table 6.

Classes of sustainability.

| Organizations | Credibility Degrees |

|---|

| A | B | C | D | E | F | G | H | I |

|---|

| Alpha | 0.09 | 0.27 | 0.32 | 0.41 | 0.59 | 0.73 | 0.86 | 1.00 | 1.00 |

| Gamma | 0.18 | 0.23 | 0.41 | 0.55 | 0.68 | 0.77 | 0.86 | 0.95 | 1.00 |

| Delta | 0.09 | 0.09 | 0.14 | 0.36 | 0.45 | 0.59 | 0.59 | 0.86 | 0.91 |

| Beta | 0.18 | 0.32 | 0.32 | 0.36 | 0.55 | 0.64 | 0.64 | 0.77 | 0.86 |

| Teta | 0.27 | 0.36 | 0.55 | 0.64 | 0.82 | 0.86 | 0.95 | 1.00 | 1.00 |

6.4.4. Implementation of the Algorithm of ELECTRE TRI

Running the pessimist algorithm of ELECTRE TRI in the MultiCriteria Lab [

5] computer system and using the credibility degree of 0.75, we obtained the classification results of the sustainability degrees of the organizations shown in

Table 7. It is relevant to highlight that the choice of the pessimistic ELECTRE TRI algorithm was intentional in order to classify the organizations under a demanding point of view.

We can observe that, overall, the sustainability degree of these organizations can be considered to be low. The company justification is that the best performance is classified in the fifth category, among the ten existing classes.

Table 7.

Sustainability ranking of surveyed companies.

Table 7.

Sustainability ranking of surveyed companies.

| Organizations | Sustainability Classes |

|---|

| Alfa | G |

| Gama | F |

| Delta | H |

| Beta | H |

| Teta | E |

6.5. Comparison with the Usual Algorithm of the Weighted Average

Table 8 shows the ranking that would be obtained if the algorithm of the weighted average was applied to the classification of the alternatives, considering the same score as shown in

Table 4 and the same cutting off plans reported in

Table 5.

Table 8.

Classification of sustainability using the weighted average algorithm.

Table 8.

Classification of sustainability using the weighted average algorithm.

| Organizations | Sustainability Classes |

|---|

| Alpha | E |

| Gamma | D |

| Delta | F |

| Beta | E |

| Teta | D |

Comparing the results presented in

Table 8 with those shown in

Table 7, we conclude there to be contradictions between all classifications. This occurs because the ELECTRE TRI classification algorithm softens the effects presented in the compensatory aggregation methods, such as the weighted average or sum of points.

7. Conclusions

The survey achieved its goal of developing a multi-criteria classification model for evaluating the degree of organizational sustainability. The proposed questionnaire, with its methodology and the data processing, was applied to classify the suppliers of capital goods for the oil and gas industry, considering the economic criteria linked to the respect for the environment and the society to which the company belongs.

The research was essential to consolidate the method as a useful tool to measure the sustainability status of the organizations surveyed.

The data analysis recorded the condition of the organization. The innovative approach using ELECTRE TRI added the knowledge that allowed the comparison among the levels of the companies, eliminating the compensatory effects of the usual methods. Despite not having the same indicators, the companies have similar characteristics, sorted into subgroups of the sustainability dimensions that can be compared.

The survey also highlights that the studied companies have not yet reached an advanced level of maturity in the organizations’ sustainability degree. In a comprehensive vision of the sustainability based on TBL, these companies are either in the initial stage or the stage of implementation of the sustainability practices. This indicates that the use of the sustainable practices could work as a competitive advantage.

Regarding the sustainability performance, the research is descriptive, so inferences were neither sought nor achieved for the sector. The main limitation of this research is that the results found could not be generalized.

A great influence of the monitoring of environmental aspects and impacts and the waste control in the companies’ sustainability degree was observed, as can be seen in the data analysis of

Table 4. Thus, for the development of the method, further criteria associated with this item are suggested.

Another line of action derived from this work is the extensive application of the instrument to collect data in order to formulate general conclusions about the responsible development of companies in the equipment industry.

The method can also be used to raise the possibility that the reason that companies have different sustainability degrees might be their involvement with different cultures.

{kind=link}