1. Introduction

The corporate approach to environmental protection has been evolving from a regulation-driven reactive mode to a more proactive approach involving an internally motivated organizational change in corporate culture and management practices towards environmental self-regulation. A growing number of firms are taking a strategic view towards environmental management and adopting environmental management practices (EMPs) that establish formal procedures and organizational routines that can help to achieve environmental goals. Many firms are also taking a holistic view of pollution control and treating it as synonymous with minimizing waste streams associated with the design, manufacture, use and disposal of products and materials and preventing pollution at source rather than at the “end of the pipe,” that is, they are adopting what we refer to as Pollution Prevention (P2) practices. Adoption of EMPs and P2 practices is voluntary since there are no regulations mandating their adoption. Firms have considerable flexibility in the EMPs and/or P2 activities they adopt and the degree to which each is implemented within the organization.

Both the adoption of EMPs and P2 activities are forms of environmental management that can be expected to be synergistic with each other. However, P2 activities require changes in production methods and pollution control technologies, whereas EMPs require changes in procedures and policies. As a result, they are likely to differ in their costs of implementation, visibility and appeal to stakeholders and potential for mitigating regulatory threats. The purpose of this paper is to examine the type of perceived pressures that influence the extent to which firms adopt EMPs and P2 practices and to analyze differences (if any) in the types of pressures likely to motivate these two approaches to environmental management. Many firms face external demands for adopting EMPs from trade associations, customers and agencies, while others may adopt EMPs to improve internal efficiency, provided they have the capacity to bear the costs of adoption. Depending on their motivations for adopting EMPs, the decision to adopt them may or may not be linked to a decision to reduce pollution at source rather than at the end of the pipe. Some firms may see environmental practices as being marginal to their strategic and competitive objectives and adopt EMPs simply to provide an appearance of conformity, to demonstrate commitment to the environment and attain legitimacy with stakeholders. Such firms may adopt EMPs as a symbolic tool to manipulate their external image but not as being important for internal change in strategies to reduce pollution [

1,

2]. Other firms may have stronger commitments to the environment and see the benefits of taking a holistic approach to environmental management. They may be more likely to adopt EMPs and make investments in P2 activities.

We address the following two research questions: What is the role of pressures from external stakeholders perceived by firms vs. internal factors and managerial attitudes in determining the extent to which firms adopt EMPs and P2 activities? Do managers that perceive environmental issues as a significant concern respond differently to stakeholder pressures in terms of their adoption decisions, as compared to other facilities? In particular, we seek to analyze the role of internal drivers such as managerial attitudes and perceptions about costs of adoption and external pressures from stakeholders in shaping incentives to adopt EMPs and P2 practices. We compare these to the relative importance of perceived (subjective) pressures and those of objective incentives captured observable facility characteristics such as ownership, size, and type of product produced in motivating the adoption of EMPs and P2 practices. We also examine if the influence of these pressures differs across firms that considered environmental issues to be a significant concern for their facility or not. This research can inform the targeting of environmental policies that seek to encourage voluntary environmental management by identifying the types of firms and industries less likely to be motivated by market pressures alone to adopt EMPs and/or P2 practices.

Our analysis is based on survey data on a variety of EMPs and P2 activities adopted by 689 facilities located in Oregon in 2005 and operating in six different sectors. Public and private initiatives to foster improved business environmental management have proliferated in Oregon since the 1990s. Of the facilities responding, more than half had implemented at least one environmental management practice. The respondents include small facilities and those under private ownership. We use information on indicators of adoption of EMPs and P2 activities to construct an index for each that measures the intensity with which EMPs and P2 are being implemented within the facility using a combination of confirmatory factor analysis (CFA) and structural equation modeling (SEM). The empirical analysis uses a two-stage process in which the measurement models are first developed and confirmed using CFA to obtain latent constructs of EMP and P2 practice adoption and of perceived pressures from various stakeholders. In the second stage the measurement model and the SEM are estimated jointly to examine the determinants of EMP and P2 adoption using path analysis.

Several studies have empirically examined the factors that motivate some firms to voluntarily adopt one or more environmental management practices or to seek ISO 14001 certification using observable characteristics of firms to serve as objective measures of external regulatory and market pressures. This includes studies examining motivations for adopting a practice, such as total quality environmental management [

3], an environmental plan [

4], a firm-structured system of environmental management practices [

5,

6,

7,

8]. Studies examining the motivations for seeking ISO 14001 certification include [

9,

10,

11]. These studies show the importance of regulatory pressures in motivating the adoption of EMPs or the ISO 14001 standard [

6,

9,

11]. Firms that were larger in size [

7] and those producing final goods, particularly if they were small polluters, were also more likely to adopt more EMPs [

6].

Other studies have included both observable proxies and constructed measures of perceived pressures to explain adoption of EMPs and ISO 14001 standard [

4,

8,

10]. Henriques and Sadorsky [

4] find that customer pressure, shareholder pressure, regulatory pressure and community pressures, in addition to a lower sales-to-asset ratio motivates firms to adopt an environmental plan. Delmas and Toffel [

8] construct three broad groups of pressures (commercial, non-market and internal) faced by firms. They find that perceived pressures, particularly commercial pressures and internal pressures, have a stronger role in explaining adoption of EMPs than objective pressures. Similarly, Nakamura

et al. [

10] find that environmental values, beliefs and attitudes of managers are important in addition to observable proxies for costs and benefits of ISO certification. Banerjee

et al. [

12] find that regulatory pressures and public concern were strong determinants of top management commitment to the environment which, together with environmental orientation of the firm, are significant determinants of its environmental strategy.

Only a few studies have examined the motivations for adopting environmentally responsible practices and pollution prevention activities. Curkovic

et al. [

13] and Khanna

et al. [

14] show the influence of total quality management systems in inducing the adoption of pollution prevention techniques. Using observed firm characteristics as proxies for internal and external pressures, the latter study finds that firms that were larger polluters and larger in size, with the capacity to bear the costs of adoption, were more likely to adopt total quality environmental management systems. In contrast, firms facing more stringent environmental regulations were more likely to adopt P2 practices.

This study builds on previous work using the survey data from Oregon facilities analyzed here. Khanna

et al. [

15] analyzed the differential incentives for these firms to adopt EMPs and for participating in voluntary environmental programs and used observed facility characteristics as proxies for these incentives. They found that regulatory pressures were more likely to influence firms to adopt EMPs, whereas market (competitive) pressures were more likely to induce participation in voluntary environmental programs. Ervin

et al. [

16] integrated utility maximization with an institutional theory approach to analyze the relative roles of objective proxies and subjective (perceived) measures of various stakeholder pressures in influencing these firms to adopt EMPs and P2 practices. They used a two-step approach in which the first step involved constructing indices of the intensity of these pressures and of the intensity of adoption using principal component analysis (PCA) to convert the observed responses of facilities to Likert-scaled statements; these indices were then used as the variables in the second step estimation of a two-equation model with EMP and P2 adoption as the dependent variables. This approach assumes that the estimated indices are deterministic and without any error. PCA also does not provide a method for assessing the validity and goodness of fit of the resulting indices. Ervin

et al. [

16] found that competitive pressures and costs of implementation were more likely to influence EMP adoption, while regulatory pressures motivated P2 adoption. Management attitudes towards their environmental responsibility were positively associated with both EMP and P2 adoption. Their findings also indicated that the perceived pressures faced by facilities were correlated with their belief that environmental issues were of significant concern to the facility.

In this paper, we construct latent variables that measure intensity while recognizing that the information provided by the responses to the Likert scales include measurement error. We assess the reliability, consistency, and validity of each of the latent variables and the goodness of fit of the overall model to evaluate how closely our observed model fits the observed data. We then apply a model that simultaneously estimates both the latent variables and the relationship between the various explanatory variables and the dependent variable of interest. This approach recognizes that unobservable factors that affect the estimation of the latent constructs could be correlated with the unobservable factors that affect the impact of those latent variables on the dependent variable.

2. Conceptual Framework

We develop a simple conceptual model to explain the motivations for adoption of EMPs and P2 practices. We define EMPs as involving changes in operating policies, including setting environmental policies and standards that were more stringent than mandatory government requirements, conducting environmental audits, using cost-accounting methods that internalize environmental costs, training and rewarding employees to pursue environmentally friendly practices and annual reporting environmental achievements. We differentiate these from P2 practices, which are defined as those involving changes in production practices and methods of pollution control by reducing spills and leaks, changing raw materials, modifying production processes and products. While the former involves a change in the management system, the latter involves technological changes in production and pollution control processes. A survey by Florida and Davidson [

17] shows that, although there is overlap, EMP adoption and P2 practice adoption are distinct approaches to environmental management; they found that 42% (out of 214) of their sample adopted a formal EMP; 41% used some form of P2 practice; and 29% reported both. Several previous studies have made a distinction between EMPs and P2 practices and shown that formal environmental management systems (a construct similar to our EMPs) are associated, but not perfectly correlated with, the adoption of pollution prevention practices [

14,

18,

19] Deltas

et al. [

20] show that adoption of total quality environmental management systems induced adoption of selective P2 practices; specifically those that involved procedural changes or are of a customized nature and not those visible to consumers. We, therefore, consider EMPs and P2 practices to be two complementary but distinct approaches to environmental management and seek to examine if they were motivated by similar or different types of stakeholder pressures.

There are several theories that have been put forward to explain why firms voluntarily undertake actions to improve their environmental performance beyond compliance. Viewing the firm as a rational actor, environmental economists have suggested that firms may see it as being in their self-interest to proactively improve environmental management, because it could enable them to influence markets for their products, obtain higher prices for their products, and lower their costs of labor and capital and the costs of environmental regulations [

21]. This is in contrast to the more traditional view in environmental economics of a firm as being a competitive price taker in the output and input markets and maximizing profits while reacting passively to regulatory constraints. Environmental actions in this framework impose costs and divert productive resources; consequently, firms have no incentive to go beyond compliance with the regulatory constraints they face [

22,

23]. This literature suggests that the potential to preempt the threat of mandatory regulations, shape future regulations, gain competitive advantage and market share (by appealing to consumers and lowering costs and improving internal efficiency), build a corporate reputation with communities and environmental interest groups and lower the costs of capital by reducing risks of liabilities for lenders and stockholders can provide economic incentives for firms to voluntarily invest in environmental measures. Differences in adoption of EMPs can then be explained by differences in the extent to which individual firms expect to achieve these benefits and in the costs of adoption they have to incur, assuming they have perfect information on both. The underlying premise of economic models explaining corporate environmental behavior is that firms are profit maximizers; thus, preferences of the management for the environment and their moral beliefs and desire to be environmentally responsible are typically not incorporated in these models.

The resource-based view of the firm argues that firms will differ in the competitive advantage they might gain from proactive environmental management practices, depending on the internal capabilities of firms to implement such practices and their external environment, such as market structure. Christmann [

22] shows that the cost savings obtained through the adoption of P2 practices can vary across firms, depending on the presence of complementary assets in the form of an internal capability to be innovative. This suggests that incentives to adopt such practices will differ across firms that vary in their internal capacity and external drivers for technological change. The “new institutionalistic” theories of organizational behavior broaden the view of the firm from a rational actor influenced by objective economic costs and benefits to being influenced by complex motivations stemming from normative beliefs, desire for conformity, political and cultural values Institutional theorists go beyond the debate between “rational” models on the one hand and “normative” or “moral” models on the other to describe how rational, normative and cognitive decision processes can coexist [

24]. They view organizations as complex social actors whose behavior is shaped as much by their cultural environments as by rational calculations. By emphasizing the power of cultural systems to shape managerial behaviors, these theorists recognize that organizations may respond to social and moral norms and legitimacy, even when the threat of legal sanctions is remote. This literature, however, has been critiqued for placing too much emphasis on the homogeneity of organizations and not explaining the diversity in observed organizational response to similar institutional pressures [

25]. Several studies have emphasized the importance of applying institutional theory of firm behavior to explain environmental management decisions. Sarkis

et al. [

26] notes the importance of external drivers such as regulatory, competitive, customer, and stakeholder pressure in explaining supply chain management decisions. Simpson [

27] finds that external factors, specifically customer pressure and regulatory pressure, influence adoption of waste reduction practices. Heterogeneity in organizational response to institutional pressures could be due to internal forces within the firm that cause inertia or cultural barriers to change [

25] and in managerial attitudes and commitment towards environmental responsibility [

28]. This could influence how managers filter, interpret and prioritize the signals they receive from the external environment and respond to these by undertaking proactive environmental management [

29]. Cordano and Frieze [

30] find that managerial knowledge and attitudes towards environment were key determinants of their preference for P2 activities.

Our empirical framework recognizes that complex interactions between the institutional environment, organizational dynamics and managerial attitudes shape organizational behavior. Traditionally, firms were expected to undertake environmental protection only to the extent that they were coerced to do so by regulatory constraints or by citizen actions, such as private lawsuits or boycotts. Increasing concerns for environmental quality among consumers, investors, lenders, competitor firms and communities have created a more diverse cultural setting which induces firms to view environmental protection as being central to the core objectives of the firm and not as being external to the market environment [

25]. We seek to measure the effects of this expanding field of environmental pressures on two constructed measures of environmental behavior of a facility,

Intensity of EMP Adoption and

Intensity of P2 Practice Adoption. The former is measured using information provided by survey respondents about the extent to which environmental goals, policies, standards and a variety of other practices are implemented in the facility. These include environmental audits, environmental cost accounting, employee training in environmental management and compensation for contributions to environmental performance. The latter is measured by the extent to which respondents perceived that pollution prevention practices, raw material substitution and recycling were practiced at their facility. Specific survey questions included to elicit information on these two dependent variables are reported in

Table 1.

We postulate that each of these dependent variables is influenced by a combination of internal and external pressures as in [

28,

31]. The external pressures include those from external stakeholders of the firm, such as, regulators, consumers, interest groups and investors as well as observed characteristics of facilities that proxy for the types of pressures they might face. The internal pressures are proxied by constructed measures of the attitudes of the managers of the facility and of the parent company towards the environment and perceived barriers to implementation. Additionally, observed characteristics of facilities, such as their ownership (private or public) and size could also influence their decision to undertake innovative management. We test the following three hypotheses using the SEM framework.

Table 1.

Construction of Latent Dependent Variables (with summary statistics).

Table 1.

Construction of Latent Dependent Variables (with summary statistics).

| Latent Variable | Survey Question | Mean | Std. Dev. | N | CFA Indicator Loadings* |

|---|

| Environmental Management Practices | Environmental goals guide operational decisions (Q.12a) | 2.88 | 1.2 | 631 | 0.926 |

| Environmental responsibility is emphasized through well-defined environmental policies and procedures (Q.12b) | 2.84 | 1.3 | 640 | 1.108 |

| Our environmental standards are more stringent than mandatory governmental requirements (Q. 12c) | 2.85 | 1.3 | 616 | 0.986 |

| We conduct environmental audits for our own performance goals, not just for compliance (Q. 12d) | 2.66 | 1.4 | 619 | 1.163 |

| Employees receive incentives for contributions to environmental performance (Q. 12e) | 1.91 | 1.0 | 634 | 0.682 |

| We use environmental cost accounting (Q. 12f) | 1.96 | 1.1 | 604 | 0.804 |

| We make continuous efforts to minimize environmental impacts (Q. 12g) | 3.7 | 1.2 | 642 | 0.852 |

| We require our suppliers to pursue environmentally friendly practices (Q. 12h) | 2.53 | 1.3 | 614 | 0.959 |

| Employees are conscious of the importance of minimizing negative environmental impacts (Q.12i) | 3.58 | 1.2 | 635 | 0.863 |

| An adequate amount of training in environmental management is provided to all employees (Q. 12j) | 2.89 | 1.3 | 638 | 1.065 |

| Facility environmental achievements are given prominent coverage in facility annual reports (Q. 12k) | 2.16 | 1.2 | 602 | 1 |

| Pollution Prevention Practices | Pollution prevention is emphasized to improve environmental performance (Q. 14a) | 3.59 | 1.2 | 641 | 1.66 |

| Efforts have been made to reduce spills and leaks of environmental contaminants (Q. 14b) | 4.39 | 0.9 | 649 | 1.068 |

| We choose raw materials that minimize environmental impacts (Q. 14c) | 3.46 | 1.1 | 622 | 1.657 |

| We have modified our production systems to reduce waste and environmental impacts (Q. 14d) | 3.71 | 1.1 | 617 | 1.735 |

| We have modified our production to reduce environmental damage during production, consumption, and disposal (Q. 14e) | 3.47 | 1.2 | 609 | 1.802 |

| We have increased recycling and reduce landfilling of our solid waste (Q. 14f) | 4.21 | 1.0 | 642 | 1 |

Hypothesis 1: Firms that perceive stronger pressure from current and future regulations are more likely to adopt EMPs and P2 practices.

Firms may voluntarily adopt EMPs and P2 practices to achieve compliance with existing and anticipated regulations more cost-effectively by identifying innovative approaches to improve environmental performance by integrating it with operational decisions, as well as by reducing the likelihood of inspections and enforcement actions. Khanna and Kumar [

32] find that adoption of an environmental management system reduces the costs of abatement of toxic releases and increases environmental efficiency. Firms may also seek to preempt and shape future regulations by showing environmental stewardship and good faith efforts at improving environmental performance (see survey in [

21]). Regulatory pressures have been found to be an important motivator of voluntary environmental management by a number of studies and surveys of firms, notably [

4,

7,

9,

17]. Additionally, the threat of potential liability for Superfund sites and anticipated Clean Air Act regulations for hazardous air pollutants also motivated firms to adopt a more comprehensive environmental management system [

5,

6]. However, several recent studies find that regulatory pressures are not important for influencing certain practices (e.g., Total Quality Environmental Management [

3]) or in some industries (e.g., pulp mills [

33]) but they were a statistically significant determinant of P2 practice adoption [

14] Using the same dataset as this study, Ervin

et al. [

16] also find that regulatory pressures had a statistically significant effect in motivating P2, but not EMPs. We test this hypothesis by including a latent construct

Regulatory Pressures based on indicator variables listed in

Table 2.

Table 2.

Construction of Latent Explanatory Variables (with summary statistics).

Table 2.

Construction of Latent Explanatory Variables (with summary statistics).

| Latent Variable | Survey Question | Mean | Std. Dev. | N | CFA Indicator Loadings * |

|---|

| Regulatory Pressures (encouraging environmental management) | Complying with current government environmental regulations (Q. 4d) | 4.1 | 1.2 | 661 | 1.000 |

| Taking environmentally friendly actions to reduce regulatory inspections and make it easier to get environmental permits (Q. 4e) | 3.21 | 1.5 | 634 | 1.534 |

| Being better prepared for meeting anticipated environmental regulations (Q. 4f) | 3.29 | 1.4 | 644 | 1.459 |

| Preempting future environmental regulations by voluntarily reducing regulated pollution beyond compliance levels (Q. 4g) | 2.98 | 1.4 | 634 | 1.686 |

| Preempting future environmental regulations by voluntarily reducing unregulated impacts (Q.4h) | 2.68 | 1.4 | 618 | 1.526 |

| Investor Pressure | Satisfying investor or owner desires to reduce environmental risks and liabilities (Q. 4a) | 3.39 | 1.5 | 658 | 1.000 |

| Protecting or enhancing the value of the facility or parent firm for investors or owners (Q. 4b) | 3.31 | 1.5 | 649 | 1.074 |

| Satisfying lenders’ desires to reduce environmental risks and liabilities (Q. 4c) | 2.39 | 1.4 | 617 | 0.718 |

| Consumer Pressure | Customer desire for environmentally friendly products and services (Q. 3a) | 2.85 | 1.4 | 654 | 1.000 |

| Customer willingness to pay higher prices for environmentally friendly products/services (Q. 3b) | 2.34 | 1.3 | 636 | 0.826 |

| Ability to earn public recognition and customer goodwill with environmentally friendly actions (Q. 3c) | 2.72 | 1.4 | 662 | 0.806 |

| Interest Group Pressure | Environmental interest groups’ perception that environmental protection is a critical issue (Q. 3d) | 2.26 | 1.3 | 647 | 1.000 |

| Preventing boycotts or other adverse actions by environmental interest groups (Q. 3e) | 1.75 | 1.2 | 648 | 0.751 |

| Promoting an environmentally friendly image to environmental interest groups (Q. 3f) | 2.42 | 1.4 | 663 | 1.091 |

| Competitive Pressure | Investing in cleaner products and services differentiates our products or our facility (Q. 5a) | 2.84 | 1.4 | 650 | 1.000 |

| Improving environmental performance helps us keep up with competitors (Q. 5b) | 2.59 | 1.4 | 656 | 0.987 |

| Environmentally friendly actions result in product or process innovations (Q. 5c) | 2.51 | 1.3 | 642 | 1.024 |

| Environmentally friendly actions can reduce costs (Q. 5d) | 2.96 | 1.4 | 645 | 0.875 |

| Being environmentally responsible attracts quality employees and reduces employee turnover (Q. 5e) | 2.48 | 1.4 | 655 | 0.946 |

| Being environmentally responsible improves employee morale, motivation and productivity (Q. 5f) | 2.77 | 1.3 | 658 | 0.930 |

| Managerial Attitudes (of facility’s upper management) | Moral responsibility to protect the environment (Q. 7a) | 4.27 | 0.9 | 658 | 1.000 |

| Support for protecting the environment even if substantial costs are incurred (Q. 7b) | 3.42 | 1.2 | 653 | 1.388 |

| Improvements in environmental performance will improve long-term financial performance (Q. 7c) | 3.39 | 1.1 | 637 | 1.401 |

| Customers and other stakeholders care about the environmental impacts of its products (Q. 7d) | 3.72 | 1.0 | 641 | 1.291 |

| Advances in technology can solve environmental problems while increasing profits at the same time (Q. 7e) | 3.41 | 1.1 | 622 | 1.141 |

| Facility should help conserve society’s limited natural resources (Q. 7f) | 4 | 1.0 | 642 | 1.048 |

| Barriers to Implementation | High upfront investment expense (Q. 8a) | 3.63 | 1.4 | 615 | 1.000 |

| Availability of knowledgeable staff (Q. 8b) | 2.77 | 1.2 | 621 | 0.749 |

| High day-to-day costs (Q. 8c) | 3.29 | 1.3 | 605 | 1.059 |

| Significant upfront time commitment (Q. 8d) | 3.21 | 1.3 | 620 | 1.099 |

| Uncertain future benefits (Q. 8e) | 3.11 | 1.3 | 600 | 1.042 |

| Risk of downtime of delivery interruptions during implementation (Q. 8f) | 2.86 | 1.4 | 602 | 1.021 |

| | Degrees of freedom | | | | 1091 |

| | Number of estimated parameters | | | | 134 |

| | Chi-square; Chi-square/df | | | | 4925.52; 4.52 |

| | CFI; RMR | | | | 0.82; 0.086 |

Hypothesis 2: Firms that perceive stronger pressure from consumers, investors, competitors and environmental interest groups are more likely to adopt EMPs and P2 practices.

Facilities may implement EMPs and/or P2 practices to realize market opportunities through their interactions with external stakeholders, such as consumers and investors, with which firms have contractual relationships, as well as with communities and environmental interest groups that enforce the firm’s “social license to operate” [

28]. Consumers, stockholders and other investors can influence firm behavior by signals transmitted through product and capital markets. Facilities may also undertake environmental management and P2 to build reputational capital by showing good faith efforts at improving environmental performance and being accepted by local communities and interest groups. However, P2 practices may not be as visible as EMPs and some may even be more expensive to implement than EMPs. As a result, market-based pressures may have a stronger impact on adoption of EMPs as compared to P2 practices. Publicly owned firms may be more likely to face pressure from diverse stockholders to be environmentally responsible and less risky. They may also have greater access to financial resources and economies of scale since they are typically part of a multifacility operation. They are also more likely to be willing to bear risks since costs of bearing risks are spread over many investors. A detailed study of costs of adopting EMPs finds this to be the case [

34]. However, investors are also concerned about firm profitability and may be less willing to support investment in costly P2 practices. Henriques and Sadorsky [

4] find that pressure from shareholders was significant in motivating firms to adopt an environmental plan, whereas Khanna and Anton [

5] find that publicly traded firms with a higher ratio of capital assets per unit sales and that are therefore more dependent on capital markets were more likely to adopt a more comprehensive environmental management system. Firms in closer contact with consumers, or spending more on advertising per unit sales or more visible to the public, were found to be more likely to undertake some voluntary environmental initiatives [

5,

6,

35]. Khanna

et al. [

14], however, find that market pressures from consumers, environmental groups and communities had an insignificant effect on P2 activities of firms.

A few studies have examined whether firms in more competitive business environments were more likely to participate in voluntary programs in order to gain a competitive advantage by differentiating their product, or by lowering waste (pollution) and enhancing efficiency. Khanna and Anton [

5] find that firms operating in less concentrated industries, that is, under more competitive conditions, are more likely to adopt a more comprehensive environmental management system. This could suggest that such firms are seeking to lessen competition by differentiating their products through their environmental attributes and by acquiring a credible environmental reputation. Dasgupta

et al. [

7], on the other hand, did not find that a desire for international competitiveness, proxied by export orientation or multinational status, was a significant motivator for Mexican firms to adopt ISO 14001, while Harrington

et al. [

3] did not find any effect of market structure on adoption of total quality environmental management.

We include a latent variable that measures

Investor Pressure (see

Table 2) and a dummy variable,

Public, equal to one if the firm was publicly owned. We construct a latent variable as a proxy for

Consumer Pressure. We also include a dummy,

Retail, equal to one if the facility sells its output to final consumers. Communities and environmental interest groups demand social responsibility from firms and can affect a firm’s image and reputation through boycotts and negative publicity. Surveys suggest that firms that perceive these pressures and have a stronger desire to improve their relations with their communities and seek external recognition are more likely to adopt EMPs and P2 practices [

4,

17,

36]. We include a latent variable,

Interest Group Pressure, to capture these pressures.

We include two variables to capture the market environment of the facility. First we construct a latent variable, Competitive Pressure to capture the facility’s perceptions of the extent to which it influences environmental management. We also include the a dummy variable, Multinational, equal to one if the facility was part of a multinational parent company and thus exposed to global competition.

Hypothesis 3: Internal factors, such as strong pro-environment managerial attitudes and lower costs of adopting EMPs and P2 practices, are likely to lead to adoption of EMPs and P2 practices.

Following Ajzen’s [

37] theory of planned behavior to examine preferences for P2, Cordano and Frieze [

30] suggest that “attitudes towards a behavior arise from a person’s beliefs about the consequences resulting from its performance and that person’s affective response to those consequences.” As a person’s attitudes towards a behavior become more favorable, their intention and effort exerted to perform the behavior is likely to increase. These attitudes might be affected by beliefs about the benefits and costs of voluntary environmental management. They find that managerial attitudes influenced preferences for source reduction activities.

Coglianese and Nash [

36] find that facilities that had greater support from top management within the facility and from the parent company for participation in the National Performance Track program were more likely to participate. Nakamura

et al. [

10] found that perceptions of managers’ recognition of personal responsibility to protect the environment had a strong influence on the extent to which environmental policies were integrated into corporate policies and practices while Delmas and Toffel [

8] found that internal pressures from management, other facilities in the firm, employees and shareholders were important in determining the comprehensiveness of the environmental management system adopted. We include a latent variable,

Managerial Attitude, to capture these effects.

The availability of proven techniques for waste reduction and improved environmental management and pressures from stakeholders to adopt them do not guarantee that they will be adopted. While the above factors capture the benefits of environmental management, it is also important to consider the barriers to improving environmental performance, which might provide disincentives for adoption of EMPs and for undertaking P2 activities. Ashford [

38] identifies several barriers to adoption of waste reduction measures that include: lack of information about their impacts on future profitability, lack of managerial capacity and capital to incur transition costs of reorganizing production, and uncertainty about the performance of new technologies. We construct a latent variable,

Barriers to Implementation, to capture these disincentives for adopting EMPs and/or P2 practices (

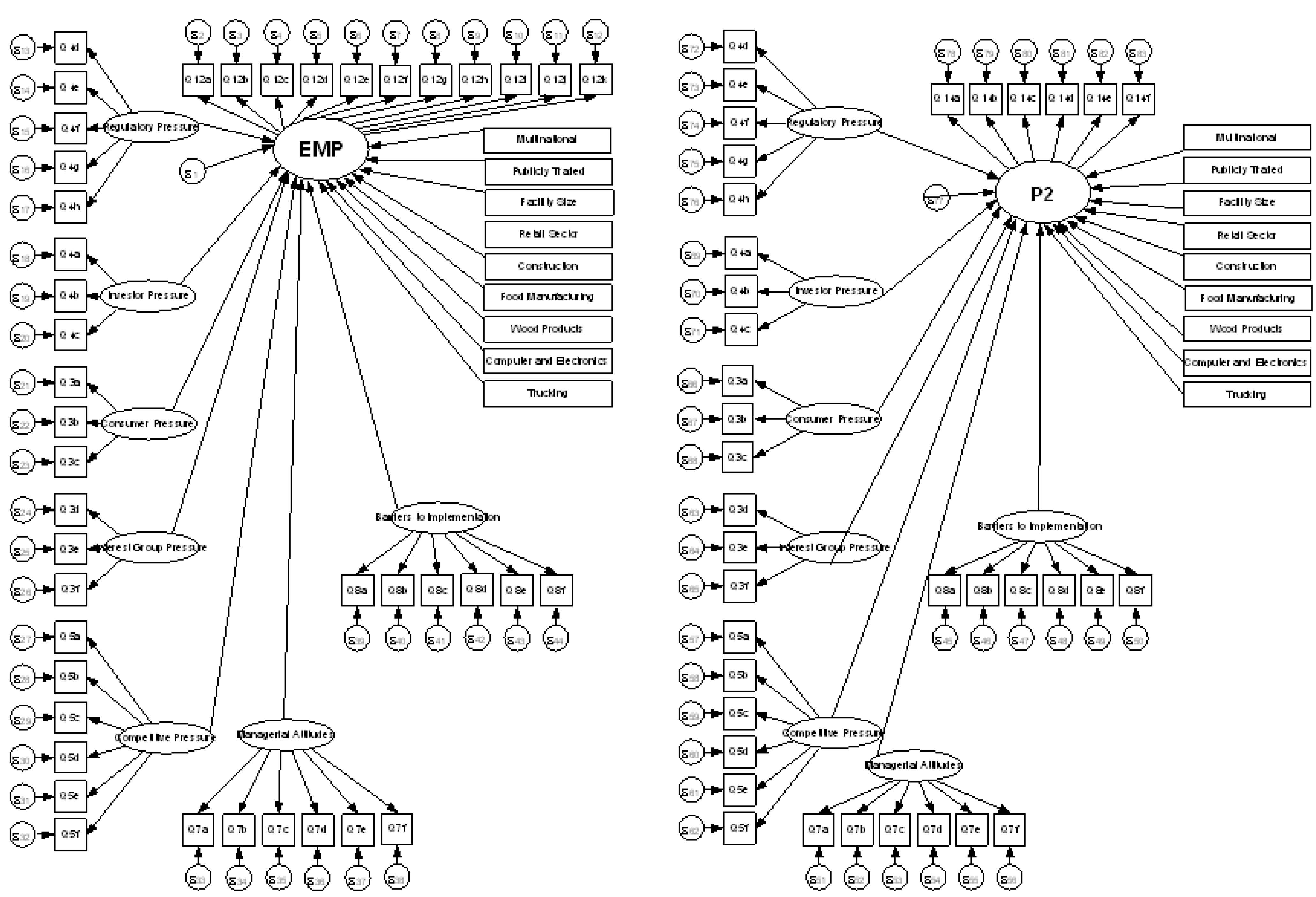

Table 2). Full path diagrams showing the relationship between the latent constructs and the dependent variables are shown in

Figure 1.

Figure 1.

Path diagrams for the models of EMP adoption and P2 practices adoption. Ovals represent latent variables, rectangles represent observed variables, and circles represent a random error component.

Figure 1.

Path diagrams for the models of EMP adoption and P2 practices adoption. Ovals represent latent variables, rectangles represent observed variables, and circles represent a random error component.

3. Data

The data were obtained from a survey of for-profit facilities that employed 10 or more employees and workers in primarily one of the following six industry sectors in Oregon in 2004. These sectors include: construction of buildings (NAICS 236), food manufacturing (NAICS 311), wood product manufacturing (NAICS 321), computer and electronic product manufacturing (NAICS 334), truck transportation (NAICS 484), and accommodation (NAICS 721). Names of all facilities in these sectors were obtained from the Oregon Employment Department (OED). The choice of industry sectors was based on careful consideration of several factors. This study was intended to provide a comprehensive view of business environmental management among facilities of varying sizes, characterized by a variety of organizational characteristics and voluntary environmental management approaches, and subject to varying environmental regulations. The selected sectors were chosen to capture both manufacturing and non-manufacturing industries of importance to the Oregon economy, in sufficient numbers to facilitate sector-specific analysis. The six sectors included in this study are among those that employ the greatest numbers of individuals, that operate the greatest numbers of facilities, and that generate the most substantial corporate tax revenues in Oregon. A total of 1,964 facilities meeting the size and sector criteria were identified to receive the survey after telephone contacts to identify the person with the most knowledge about facility environmental management. The survey was developed and administered using a Tailored Design Method (TDM) protocol [

39]. The survey asked questions in four general areas: environmental management, environmental practices, environmental performance, and facility characteristics (e.g., annual revenues). The Likert agreement scale was used to assess perceptions of upper management and parent company attitudes, the extent to which environmental management practices and P2 activities have been implemented. The Likert-type ordered-response scale was used to assess perceptions of customer, investor, lender, regulatory and competitive influences, barriers to environmental management, managerial attitudes, and parent company support. A five-point scale was chosen for this study for several reasons, based on determinations by Clark [

40] and Lehman and Hulbert [

41]. First, the five-point scale has been found to be approximately as effective as a continuous scale at estimating the mean response. With the addition of each point, the differences between continuous and discrete scales decrease rapidly up to the level where five or six points are included. After this, adding points results in less measurement improvement. Furthermore, due to the length and intensity of this survey, a seven-point scale was considered too detailed for respondents. Conversely, a three-point scale was considered too limited. Fewer points on the scale may not capture adequate variation, which increases the likelihood of a departure from the assumption of a normal distribution, a requirement for many statistical tests [

42].

Approximately 3.9% of eligible facilities declined to participate after the phone call. The facilities that declined had slightly smaller numbers of employees on average, 16 employees as compared to 24 for respondents. A total of 689 responses were obtained, representing an overall response rate of just over 35%. To test for potential self-selection bias, the OED list of facilities, the sample of 1,964 facilities identified to receive the survey, and the set of respondents were compared by facility size and geographic location. No bias was detected based on average or median employment levels, or proportions of facilities located in each county, between these groups. Additionally, the Oregon Department of Environmental Quality operates three geographic regulatory regions. No bias was detected based on comparisons of proportions of facilities located in these regions in the OED list, the survey sample, or the set of respondents.

Two follow-up mailings were sent to facilities that had not yet responded. A total of 403 facilities responded to the initial mailing, 151 facilities responded after the second mailing, and 75 facilities responded after the third and final mailing. To determine if the responses were biased according to mailing wave, we conducted a one-way analysis of variance with each of the survey questions as the response variable and mailing wave (first, second, or third) as the factor variable. The means of the survey responses to all questions included in this study obtained during the three mailing waves were compared and found to be statistically different for only three survey questions (out of 49 tested). In those three cases, these differences were very small in magnitude. We therefore conclude that the responses are not biased according to when the survey was returned.

Our dataset contains missing values because many survey respondents did not provide an answer for every question. Of the 689 surveys forms that were returned, 199 had responses for every question used in the present model. This means that 490 responses had missing values for at least one question. We estimate the model using the two most up-to-date methods for addressing the problem of missing values: the expectation maximization (EM) algorithm and the Full Information Maximum Likelihood (FIML) method. Imputation using the EM algorithm generates a complete dataset by estimating the missing values using other variables in the dataset. An advantage of imputing missing values is that we can bootstrap

p-values in our estimated model. Since our dataset consists of categorical indicator variables that are nonnormally distributed, bootstrapped

p-values provide a better measure of the significance of the estimated parameters than one based on the maximum likelihood method. The FIML estimation method does not impute missing values. Rather, parameters and standard errors are estimated directly using all of the observed data. In the course of the FIML procedure, a likelihood function for each individual observation is estimated based on the (non-missing) variables [

43]. The drawback of this method is that we cannot bootstrap significance levels for the parameter estimates using the AMOS software and hence only report the ML estimates. Use of two methods of estimation with missing values provides a useful robustness check.

Both the EM and FIML estimation methods assume the data are missing at random. In practice, this assumption is very difficult to test (see, for example, [

44], p. 152). To allow for the possibility that some data may not be missing at random, studies recommend using auxiliary variables to explain missing values (see [

45]). While our estimated model makes use of 45 or 50 observed variables (depending whether we are estimating the EMP or P2 practices model) to construct explanatory variables, our survey collected responses to 251 observed variables. We used many of these variables to impute missing values with the EM-algorithm to reduce the bias and increase the efficiency of estimates. Also, though a large portion of the observations are missing at least one variable, few observations are missing more than one or two observed variables per latent construct. This gives us additional confidence that our latent constructs are accurately measuring the explanatory variable of interest.

4. Empirical Framework

We employ SEM to assess the factors and facility characteristics that explain the

Intensity of EMPs and

P2 practice adoption by firms. SEM is a statistical technique for measuring relationships between latent variables,

i.e., variables that are not directly observed but measured by various indicators. SEM is particularly well suited to our study because many of the concepts we model are attitudes or beliefs (such as managerial attitudes or pressure from various stakeholder groups) that are measured using a series of survey questions. Bollen [

46] describes SEM as a set of regression equations that invoke less restrictive assumptions and allows for errors in measurement of explanatory and dependent variables, as well as for errors in the regression equations quantifying the relationships between those variables.

Many of the concepts we seek to include in our model are not directly observable (e.g., pressure from various stakeholder groups, management attitudes, and perceived barriers to adoption), so we use responses to between three and ten survey questions as indicators of the underlying concepts. By using SEM, rather than an alternative method like conventional regression analysis with factor scores as independent variables, we eliminate the problem of measurement error. Constructing factors scores for imperfectly measured concepts introduces an error-in-variables problem and can lead to biased coefficient estimates. SEM simultaneously estimates the relationship between the latent variable and the dependent variable and the correlation between indicator variables, thereby effectively estimating measurement error involved in constructing the latent variable apart from the effects of the independent variables on the dependent variables (see [

47], pp. 73–77 for an intuitive explanation, or [

48] for a more formal representation).

Maximum likelihood estimation of SEM’s using categorical variables or data that are nonnormal may produce chi-square goodness-of-fit statistics that are inflated (

i.e., reject too many true models) and biased standard errors for estimated parameters (

i.e., too many significant results) [

49,

50]. Univariate normality tests of each of our observed indicator variables suggest possible nonnormality in our data. We are primarily interested in the regression weights in the structural model (the coefficients on the variables that explain EMP adoption and P2 practices adoption), therefore we address the possible nonnormality by generating significance levels for our estimated parameters using nonparametric bootstrapping, as recommended in previous work [

51].

An SEM consists of two components: a measurement model and a structural model. These two components make up two sets of equations that are estimated simultaneously. We perform the analysis in three steps. First, we estimate the measurement model and assess reliability, consistency, and validity of each of the latent variables. Second, we assess the goodness of fit of the overall model to evaluate how closely our observed model fits the observed data. Third, we estimate the two-equation structural model with the latent variables Intensity of EMPs and P2 practice adoption as dependent variables and with the seven latent factors and four observed characteristics of the facility as explanatory variables.

4.1. Measurement Model

The measurement model connects a latent variable of interest to one or more indicator variables using a linear function. Each indicator variable is a continuous variable that is represented as having two causes, a single underlying latent variable that is not directly observed but is a formal representation of a concept and a measurement error. These errors are assumed to be independent of each other and of the latent factors. The measurement model does not analyze associations between latent variables. The measurement model is similar to factor analysis used to reduce many indicator variables to a few latent factors.

We first evaluate whether the latent variables we have constructed represent reasonable and identifiable distinct concepts. To do this, we perform a CFA and use the results to evaluate the measurement model based on three criteria: indicator reliability, internal consistency, and discriminant validity. The CFA estimates the unobserved latent variables as linear combinations of indicator variables. We use the indicator loadings (i.e., regression coefficients) and error term variances from the regressions in the CFA to construct the statistics described below.

Indicator reliability is a measure of how well an observed indicator variable explains variation in the latent construct it is measuring. We tested indicator reliability by assessing the significance, sign, and strength of each indicator loading on to the hypothesized latent variable. The indicator loadings for each latent construct are reported in

Table 1,

Table 2. Note that for each latent variable, the estimate of one indicator loading is set to one. This is because latent variables, being unobservable, have no natural scale. All of these indicators loadings are significant at the one percent level. We thus conclude that our measurement model has adequate indicator reliability.

Next, we assessed the internal consistency of the observed indicator variables used to measure each latent construct using three different methods. Internal consistency is the degree to which indicator variables that measure the same latent construct are correlated with each other. Internal consistency is also commonly referred to as convergent validity and is based on the premise that the observed indicator variables should co-vary highly if they measure the same latent variable [

52]. We use three ways to check internal consistency for a latent variable: Cronbach’s alpha, composite reliability, and average variance extracted. Results are presented in

Table 3.

Table 3.

Measures of Internal Consistency.

Table 3.

Measures of Internal Consistency.

| Latent Variable | Cronbach α | Composite Reliability | Average Variance Extracted |

|---|

| Customer Pressure | 0.774 | 0.695 | 0.584 |

| Interest Group Pressure | 0.905 | 0.756 | 0.751 |

| Investor Pressure | 0.892 | 0.694 | 0.601 |

| Regulatory Pressure | 0.851 | 0.842 | 0.959 |

| Competitive Pressure | 0.853 | 0.820 | 0.674 |

| Management Attitude | 0.922 | 0.845 | 0.813 |

| Barriers to Implementation | 0.821 | 0.802 | 0.619 |

| Implementation of EMPs | 0.905 | 0.893 | 0.708 |

| P2 Practices | 0.892 | 0.815 | 0.707 |

The first check of internal consistency is Cronbach’s alpha. As a rule of thumb, Cronbach’s greater than 0.70 indicates that a latent variable exhibits adequate internal consistency [

52]. The second check of internal consistency is composite reliability. We calculated the composite reliability for each latent construct by dividing the squared sum of the standardized factor loadings by the variance of the error terms in the measurement equations plus the squared sum of the standardized factor loadings. Composite reliability greater than 0.70 indicates the latent variable has adequate internal consistency [

2]. The third check of internal consistency is average variance extracted, defined as the proportion of the variance in the indicators that is explained by the latent variable. Note that the part of the variance in the indicators that is due to the latent variable is the sum of the squared standardized factor loadings. For each latent variable, the average variance extracted is calculated as the sum of the squared item standardized loadings divided by the sum of the variance of error terms and the squared item standardized loadings [

53]. The total variance of the observed indicator variables is made up of an unexplained portion (the variance of the measurement errors) and an explained portion (the variance in the indicators that is due to the latent variable). For an adequate measurement model, the average variance extracted should be greater than 0.50. This would indicate that the variance explained by the latent variable is greater than the variance due to measurement error [

53].

The results presented in

Table 3 indicate that our hypothesized latent constructs have good internal consistency. The composite reliability for each latent variable is above the accepted threshold of 0.70, except for customer pressure which is only slightly below. The average variance extracted for all nine latent variables is well above the accepted threshold of 0.50. We conclude that our observed indicator variables do an adequate job of measuring the latent constructs of interest in to our study.

Lastly, we tested the discriminant validity of our latent constructs, the degree to which measures of each of the latent variables are different. If the hypothesized latent variables in the measurement model truly are distinct concepts, then the latent variables should not be highly correlated [

52]. Following Delmas and Toffel [

2] we evaluate discriminant validity by comparing the shared variance between pairs of latent variables with the shared variance between the items that make up the latent variables. We compute the shared variance between two latent variables by squaring the correlation between the two latent variables. We compute the shared variance between the latent variables and their indicators as the average variance extracted (as described above). Discriminant validity is adequate if the shared variance between two latent variables is less than the shared variance between the latent variables and their indicators.

Table 4 is a matrix that is used to evaluate the degree of discriminant validity of our measurement model. Elements on the diagonal are the square root of the average variance extracted for each latent variable. These elements represent the shared variance between indicator variables within the same latent variable. Off-diagonal elements are the correlation between two latent variables. These elements represent the shared variance between distinct latent variables or between indicator variables of two distinct latent variables. In a measurement model with a high degree of discriminant validity, diagonal elements will be greater than all other elements in the same row or column. Put another way, this means that the indicator variables that make up any latent variable are more highly correlated with each other than with other latent variables. The results in

Table 4 show that our measurement model exhibits adequate discriminant validity because each diagonal element is greater than all other elements in its row and column.

Table 4.

Discriminant Validity Matrix.

Table 4.

Discriminant Validity Matrix.

| | Customer Pressure | Interest Group Pressure | Investor Pressure | Regulatory Pressure | Competitive Pressure | Managerial Attitudes | Barriers | EMP | P2 Practices |

|---|

| Customer Pressure | 0.764 | | | | | | | | |

| Interest Group Pressure | 0.705 | 0.866 | | | | | | | |

| Investor Pressure | 0.519 | 0.561 | 0.775 | | | | | | |

| Regulatory Pressure | 0.444 | 0.567 | 0.641 | 0.979 | | | | | |

| Competitive Pressure | 0.726 | 0.668 | 0.616 | 0.603 | 0.821 | | | | |

| Managerial Attitude | 0.486 | 0.482 | 0.583 | 0.456 | 0.706 | 0.902 | | | |

| Barriers to Implementation | 0.146 | 0.127 | 0.201 | 0.175 | 0.132 | –0.075 | 0.787 | | |

| Implementation of EMPs | 0.410 | 0.473 | 0.552 | 0.496 | 0.579 | 0.661 | –0.088 | 0.841 | |

| P2 Practices | 0.358 | 0.400 | 0.465 | 0.531 | 0.539 | 0.618 | 0.015 | 0.743 | 0.841 |

4.2. Structural Model

We estimate two structural models with intensity of EMP adoption and intensity of P2 adoption as dependent variables as illustrated by the path diagrams in

Figure 1. The explanatory variables in each model are the same and consist of seven latent variables and directly observed variables. The seven latent variables (listed in

Table 2) include regulatory pressure, investor pressure, consumer pressure, interest group pressure, competitive pressure, management attitudes towards environmental protection, and barriers to implementation of environmentally responsible practices. The nine directly observed explanatory variables are described in

Table 5 and include reported facility revenues, whether the facility is part of a publicly owned corporation, whether the facility is part of a multinational corporation, and dummy variables indicating the industry to which a facility belongs. The estimated coefficients on each of the explanatory variables allow us to test our three hypotheses on the determinants of EMP and P2 practice adoption.

Table 5.

Summary Statistics.

Table 5.

Summary Statistics.

| | Percent of Sample | Number of Responses | Standard Deviation |

|---|

| Facility Revenues | $16.8 million | 460 | 68.9 |

| Retail | 44.7% | 658 | 0.50 |

| Public Ownership | 10.4% | 641 | 0.31 |

| Multinational Status | 12.7% | 659 | 0.33 |

| Construction of Buildings (236) | 19.6% | 682 | 0.40 |

| Food Manufacturing (311) | 15.4% | 682 | 0.36 |

| Wood Product Manufacturing (321) | 17.3% | 682 | 0.38 |

| Computer and Electronics Manufacturing (334) | 7.4% | 682 | 0.26 |

| Truck Transportation (484) | 18.9% | 682 | 0.39 |

| Accommodation (721) | 20.5% | 682 | 0.40 |

{kind=link}