Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China

1

International Exchange College, Ningbo University of Technology, Ningbo 315211, China

2

International Business School Suzhou, Xi’an Jiaotong-Liverpool University, Suzhou 215123, China

3

School of Economics and Management, Zhejiang Sci-Tech University, Hangzhou 310018, China

4

Design School, Xi’an Jiaotong-Liverpool University, Suzhou 215123, China

5

Department of Financial and Business Systems, Lincoln University, Lincoln 7647, New Zealand

6

The XIPU Institution, Xi’an Jiaotong-Liverpool University, Suzhou 215123, China

*

Author to whom correspondence should be addressed.

Sustainability 2024, 16(8), 3443; https://doi.org/10.3390/su16083443

Submission received: 21 January 2024

/

Revised: 1 April 2024

/

Accepted: 12 April 2024

/

Published: 19 April 2024

Abstract

:This paper examines whether the adoption of the Global Reporting Initiative (GRI) by listed firms could enhance the alignment between corporate sustainability reporting and stakeholders’ interests in China. Drawing on content analysis of the environmental, social, and governance (ESG) reports of 48 selected listed firms and a questionnaire survey of 409 respondents, this study shows that most of the sampled firms with GRI adoption have more sustainability activities identified in the content analysis than their peers that do not follow the GRI guidelines in the same industries; both groups of firms have a similar pattern of disclosure frequency in light of the six dimensions developed in this study; and there is a disconnect between the stakeholders’ needs and the sustainability reporting practice of the sampled listed firms. The findings reflect that the current corporate social responsibility reporting practice could be interpreted as a strategic response to the government’s policy priorities, rather than a direct attempt to address stakeholders’ concerns.

1. Introduction

Corporate sustainability reporting is a crucial non-financial disclosure of information to inform stakeholders of a corporation’s sustainable business performance to facilitate economic decision-making. It is related to CSR (corporate social responsibility) or ESG (environmental, social, and governance) reporting. CSR is a business model where companies aim to operate in a socially accountable manner, considering their impacts on the environment, employees, communities, and other stakeholders, beyond just maximizing profits. ESG refers to the three central factors in measuring the sustainability and societal impact of an organization’s operations, which investors and companies use to evaluate corporate behaviors and the long-term viability of a business. Studies have examined various aspects related to sustainability reporting, providing a holistic review of the motivations behind and the implications associated with ESG disclosure [1].

According to Stuart et al. (2023), one of the indicators proxying corporate sustainability disclosure is firms’ adoption of the Global Reporting Initiative (GRI) framework [2]. The GRI is an international independent standards organization that helps businesses, governments, and other organizations understand and communicate their impacts on sustainability issues such as climate change, human rights, and corruption. Various firms have adopted the GRI guidelines for their voluntary sustainability reporting, providing a bibliometric analysis for the GRI and identifying global trends in developed and developing economies [3]. One aspect of the research in this field examines whether the incorporation of GRI standards by firms could enhance the alignment between the contents of their sustainability disclosures and the interests or concerns of their stakeholders. For instance, using US companies’ sustainability reports as samples, Bradford et al. investigated whether the information reported by companies following the GRI aligns with stakeholders’ interests; they found that the GRI reporting framework does not provide information that aligns with consumers’ interests [4].

In China, the practice of corporate sustainability reporting has rapidly advanced [5]. First, according to the China Stock Market & Accounting Research (CSMAR) database, an increasing number of listed companies have voluntarily adopted GRI standards, with the percentage increasing from 20% in 2012 to 42% in 2021. Second, the Chinese government has a major role in economic growth, resource distribution, and promoting sustainability, in contrast to developed economies. For example, the Chinese government has officially set China’s “dual carbon” goals: to reach maximum carbon emissions by 2030 and to reach carbon neutrality by 2060. These goals guide businesses in sustainability. Third, the literature indicates that the COVID-19 pandemic has changed corporate social responsibility (CSR) practices. It is therefore important to investigate whether Chinese listed firms adopting GRI standards could enhance the alignment between corporate sustainability reporting and stakeholders’ interests, especially in China’s unique institutional environment and post-COVID-19 periods. Since few studies have examined this issue, our study fills a research gap.

In this paper, we use two groups of firms (i.e., firms with and without GRI framework adoption) to examine whether the adoption of GRI reporting guidelines by Chinese listed firms enhances the alignment between corporate sustainability reporting and stakeholders’ interests, from six dimensions including environment, economic, society, consumer, LA&HR (labor, decent work, and human rights), and governance-oriented risks. Using a sample of the selected 48 sample firms based on the 24 second-order industry classifications, we first conduct content analysis by a “goal-mining process” following the research of Anton and Earp (2004) and Bradford et al. (2017) [4,6]. We then design a sustainability survey instrument and compare the outcomes. We find that (1) most of the sampled firms with GRI standards adoption have more sustainability activities identified in the content analysis (i.e., disclose more) than their peers that do not follow the GRI guidelines in the same industries; (2) both groups of firms have a similar pattern of disclosure frequency in light of our developed six dimensions; and (3) there is a gap between what stakeholders want and the sustainability reporting provided by the sampled listed firms.

Our study contributes to the sustainability reporting literature by examining whether adopting the GRI reporting guidelines aligns with the stakeholders’ view of corporate sustainability’s dimensionality. While previous studies focused on developed economies, ours extends this line of research by examining the situation in China. The main findings reflect that the current CSR reporting practice could be interpreted as a strategic response to the government’s policy priorities, rather than a direct attempt to address stakeholders’ concerns.

2. Related Literature and Institutional Background

2.1. Stakeholders and Sustainability Reporting

Stakeholders are people or groups who can impact or be impacted by an organization’s goals [7]. According to stakeholder theory, management should consider the interests of stakeholders, encompassing more than merely the financial gains of shareholders [8]. Unlike shareholders who only care about financial success, stakeholders also care about the company’s social impact [9].

Sustainable activities are actions by companies that are beneficial to stakeholders and the environment in the long run [10]. These activities can improve a company’s performance, increasing its market value and reducing financing costs [11]. Companies with more robust sustainability performance often have lower bank loan rates. For example, companies that disclose their carbon emissions data often have lower debt costs [12,13].

Sustainability reporting (SR) is a process wherein companies share information about their sustainable activities. This can include their impact on the environment and society [14,15,16,17]. Companies may incorporate sustainability information into their annual reports or produce standalone SR documents [18,19]. Sustainability information is useful for decision-making by both internal and external stakeholders, as it can help predicate a firm’s overall risk and future benefits [20]. Intended users (i.e., stakeholders) of SR data usually include consumers, employees, suppliers, governments, communities, potential investors, and debt holders [21].

2.2. Uniqueness of Sustainability Reporting in China

SR has been significant in developed countries for several decades and is now gaining traction in developing countries [22,23]. China, being the world’s second largest economy, has a huge influence on global environmental sustainability [24]. Chinese investors are now considering a public company’s ESG ratings before investing, as these ratings can impact a company’s cost and brand value. Companies with higher ESG ratings are more likely to attract retail and institutional investors, as ESG ratings are seen as a predictor of better future financial performance [25,26].

SR in China is unique due to its political and economic context, in terms of its institutional, communication, and assurance practices. Firstly, differing from the institutional context in the US and European countries, the Chinese government plays a leading role in economic development and setting SR standards [24]. To pursue the general policy of a “harmonious society”, the Chinese government is incentivized to encourage more sustainable activities in state-owned companies because it wants to exercise ownership of the economic, political, and social dimensions within these companies [27]. Secondly, differing from the rule-based communication style and high communication quality in India, Chinese firms are more relation-based and lack multi-dimensional communication on SR motives, processes, and stakeholders’ concerns [28]. Thirdly, unlike Japan, China does not have third-party credibility assurance for SR [29,30,31]. Compared with Western companies, Chinese companies generally take on more social responsibilities, such as maintaining social stability and creating job opportunities. They also find ways to address shareholders’ interests [32]. Table 1 outlines the unique aspects of SR practice in China compared to the US, European countries, India, and Japan. The study of SR in emerging markets is a growing area of research. This is largely due to the unique challenges and opportunities presented by these markets that differ from those in more mature economies [33,34,35,36].

Although SR disclosure is not currently mandatory in China, global public companies are starting to engage in it. This includes disclosing information about economic, environmental, consumer, employee, societal, and corporate governance aspects [32]. In the economic dimension, Chinese companies report on wealth creation, economic growth, investment return, and taxes. The environmental dimension includes pollution reduction, resource utilization rate, and energy saving. In the consumers’ dimension, they ensure product quality and safety, uphold consumers’ rights, and maintain fair pricing [37]. In the employees’ dimension, companies disclose information about safe production, welfare, training and education, and promotion. The societal dimension denotes donations, poverty alleviation, and education support. The corporate governance dimension focuses on information about law and policy, risk management, and anti-corruption [37,38,39,40].

2.3. Sustainability Reporting Standards

Organizations provide voluntary reporting standards for CSR activities to improve reporting practices. One of these is the Global Reporting Initiative (GRI), which offers the world’s most widely used standards for sustainability reporting. These standards are designed to help organizations report on their sustainability performance such as biodiversity, emissions, waste, and tax. The GRI standards are updated regularly to reflect global best practices for sustainability reporting. Other players are the SASB (Sustainability Accounting Standards Board), the IFRS (International Financial Reporting Standards), the TCFD (Financial Stability Board’s Task Force on Climate-related Financial Disclosures), the CDSB (Climate Disclosure Standards Board), and the IIRC (International Integrated Reporting Council).

We use stakeholder theory and signaling theory to formulate theoretical arguments to show how adopting GRI standards can facilitate the quality of CSR reporting and mitigate the information gap between firms and their stakeholders.

From a stakeholder theory perspective, adopting GRI standards ensures coverage of all sustainability topics in a firm’s CSR reports and serves as a strategy tool. By following these standards, firms demonstrate their commitment to addressing the concerns and interests of all stakeholders, including employees, customers, suppliers, and the community. This comprehensive approach, aligned with the ethical and managerial branches of stakeholder theory, can help firms strategically manage stakeholder relationships by providing relevant information that stakeholders need to assess the firm’s sustainability performance.

From a signaling theory perspective, using GRI standards in CSR reporting signals the market about the firm’s dedication to transparency and accountability in sustainability matters. By voluntarily adhering to these globally recognized standards, firms send a positive signal that they are actively managing their environmental, social, and governance (ESG) impacts. This can reduce information asymmetry by providing stakeholders with standardized and reliable information, allowing for easier comparison and assessment of the firm’s sustainability performance. The signal is costly because the firm needs to invest resources into thorough reporting, which further boosts the signal’s trustworthiness.

2.4. The Connection between SR and Stakeholders’ Concerns

The literature indicates that it is important to check if SR matches stakeholders’ concerns or interests [2,4]. As SR holds the key to effective communication with stakeholders, the quality of information disclosed is critical. High-quality disclosures are complete, balanced, and relevant to the readers [2]. Using a well-structured framework like the GRI can help improve disclosure quality [41].

A few studies have examined whether using the GRI framework can help firms align their SR disclosure contents with stakeholders’ interests. For example, Bradford et al. (2017)’s research findings suggest a disconnect between the GRI framework and the information demands of consumers, implying that the GRI reporting framework does not provide information that aligns with consumers’ interests [4].

In China, despite the corporate SR practice being at an initial stage, stakeholders’ demand for SR is increasing rapidly [42,43]. Over the past two decades, an increasing number of Chinese listed firms have voluntarily applied the GRI framework to their SR practices [5]. Thus, it is worthwhile to examine whether GRI framework adoption by listed firms could facilitate corporate SR practices aligning with stakeholders’ interests. However, few studies examine this issue, particularly in the post-COVID-19 period, in which the literature has suggested a shift in corporate sustainability or CSR practices [44]. Therefore, this study fills the research gap.

3. Research Methodology

3.1. Sample Selection and Content Analysis

To answer our research questions, we conducted a content analysis of the selected CSR reports disclosed by Chinese firms listed on the Shanghai or Shenzhen Stock Exchanges. The steps of our sample selection were as follows: First, we used the WIND database for industry classification, including 10 first-order categories and 24 second-order categories. Second, we randomly selected a sizable, listed firm adopting the GRI framework in each second-order industry category to examine the impact of GRI adoption on CSR disclosure. These firms were each matched with another firm that had not adopted the GRI framework and had a similar market value to control for firm size. This resulted in a total of 48 listed firms (see Table A1 in Appendix A for details). We then downloaded the 2020 CSR reports from the 48 firms, which were released in 2021. The sampled CSR reports ranged from 5 to 133 pages in length.

The GRI framework suggests reporting on nearly 80 sustainability activities (or indicators) in six distinct dimensions, i.e., environment, economic, society, product responsibility (or consumer), human rights, and labor and decent work. In addition to these six dimensions, Bradford et al. (2017) [4] suggest that an additional indicator, i.e., risk and compliance, should stand alone as a separate dimension since the identification of such sustainability-related and governance-oriented risks matters for corporate governance and business success. The literature also suggests that the human rights-related challenges faced by firms often involve occupational health and safety, discrimination, child labor, forced or compulsory labor, and the right to collective bargaining [45,46]. Therefore, existing studies examine GRI-related issues by combining labor, decent work, and human rights into one indicator. For example, the impact of female managers on labor practice, decent work, and human rights (LA&HR) performance are examined [47]. Thus, our content analysis is based on the revised six GRI-oriented dimensions, i.e., environment, economic, society, consumer, LA&HR (labor, decent work, and human rights), and governance-oriented risks. Table 2 displays activities regarding the content analysis, including the definitions of the six revised dimensions and example sustainability activities based on our sampled ESG reports.

We used content analysis to examine the sampled ESG reports and identify sustainability activities that pertain to the revised GRI-oriented dimension. These actions were then evaluated both in terms of quality and quantity considering the company’s organizational profile, strategic design, corporate regulations, and specific sustainable actions disclosed in the ESG reports. Following Anton and Earp (2004) and Bradford et al. (2017), we used a technique known as a ‘‘goal-mining process”, which defines goals as the objectives and targets of achievement for a system and consists of three steps: goal identification, classification, and refinement [4,6]. Following these three steps, each sampled ESG report was first read to identify relevant activities or goals, which, in turn, were recorded and classified according to our six revised dimensions. We then refined all identified goals to remove synonymous/redundant goals and resolve inconsistencies within the goal set.

In the goal mining process, researchers separately categorized goals or activities, then compared their results. If disagreement appeared, then the issue was discussed and resolved. Researchers identified sustainability activities by the meaning in the text and counted how often (frequency) each activity was mentioned in the sampled ESG reports. Table 3 shows the frequency of all identified activities for each sampled firm/ESG report and classifies them according to the revised dimensions. It also includes the original 2205 activities identified, showing all the sustainability activities of the sampled firms.

In the goal refinement process, we then removed synonymous/redundant goals by reconciling dissimilar descriptions of similar activities from multiple companies into single activities [2,4,48]. Consequently, the original 2205 activities were categorized into 113 unique items. Next, we engaged a focus group to evaluate the 113 activities for clarity and to validate our categorizations. We asked for professional support from a CSR expert to evaluate the content validity of these items. The validity of classification for the 113 activities was then evaluated by five senior business students experienced in sustainability research. They classified the 113 items independently into six dimensions. We also utilized exploratory factor analysis for the pilot survey responses, removing items rated below 0.5. After refinement and exploratory factor analysis, 43 unique items/activities were included in our preliminary survey.

3.2. Survey Process

We designed a sustainability survey instrument to include statements with Likert-scale responses. Respondents were asked to assume the role of stakeholders (e.g., consumers) to rate the importance of each sustainability activity on a scale of 1 to 5, with 1 being not important, and 5 being very important. “How important do you think these activities are to a listed firm implementing corporate sustainability?” A pilot survey was tested on 409 respondents in the fall of 2021.

We utilized an online questionnaire survey to obtain a larger and more diversified sample of respondents to prevent manual data errors. We used WeChat to distribute the survey to 37 individuals, including government officials, academic researchers, entrepreneurs, enterprise managers and employees, medical personnel, college students of different majors, freelancers, and retirees. The survey was then distributed to their family members, colleagues, and friends. Finally, 409 respondents completed the survey. Table 3 shows the demographic information of all respondents, 84.1% of whom reside in the developed eastern regions of China, mainly in Shanghai, Zhejiang, and Jiangsu. Demographic results from the pilot study demonstrate good variability among respondents.

Table 4 presents the descriptive statistics and the reliabilities of each dimension/factor. The Cronbach’s alpha for 43 items in the survey is 0.973 and for each factor, it is above 0.7, which is acceptable for the internal consistency test [49]. In the KMO and Bartlett’s tests, the chi-squared result is 14,248 (df = 903; sig = 0.000). The KMO measure of sampling adequacy is 0.955, which indicates that the survey data are suitable for factor analysis. For the total variance explained, rotation sums of squared loadings are 68.96% for the six principal component analyses. The mean value of the governance-oriented risk factor is the highest at 4.66, while the society factor at 4.46 is the lowest but with the largest standard deviation.

As shown in Figure 1, content analysis and a questionnaire survey were employed to examine the disclosure quantity and quality of CSR reports. On the one hand, content analysis is utilized to investigate the disclosure quantity of CSR reports from the perspective of public companies to determine the disclosure frequency of different sustainability activities; on the other hand, it is used to clarify the degree of significance of each sustainability activity from the perspective of stakeholders. A questionnaire survey is used to collect the data of significance scores for various sustainable activities. The intention is to compare the distinct attention paid between CSR report preparers and CSR report users.

4. Results

4.1. Results of Content Analysis of the ESG Reports

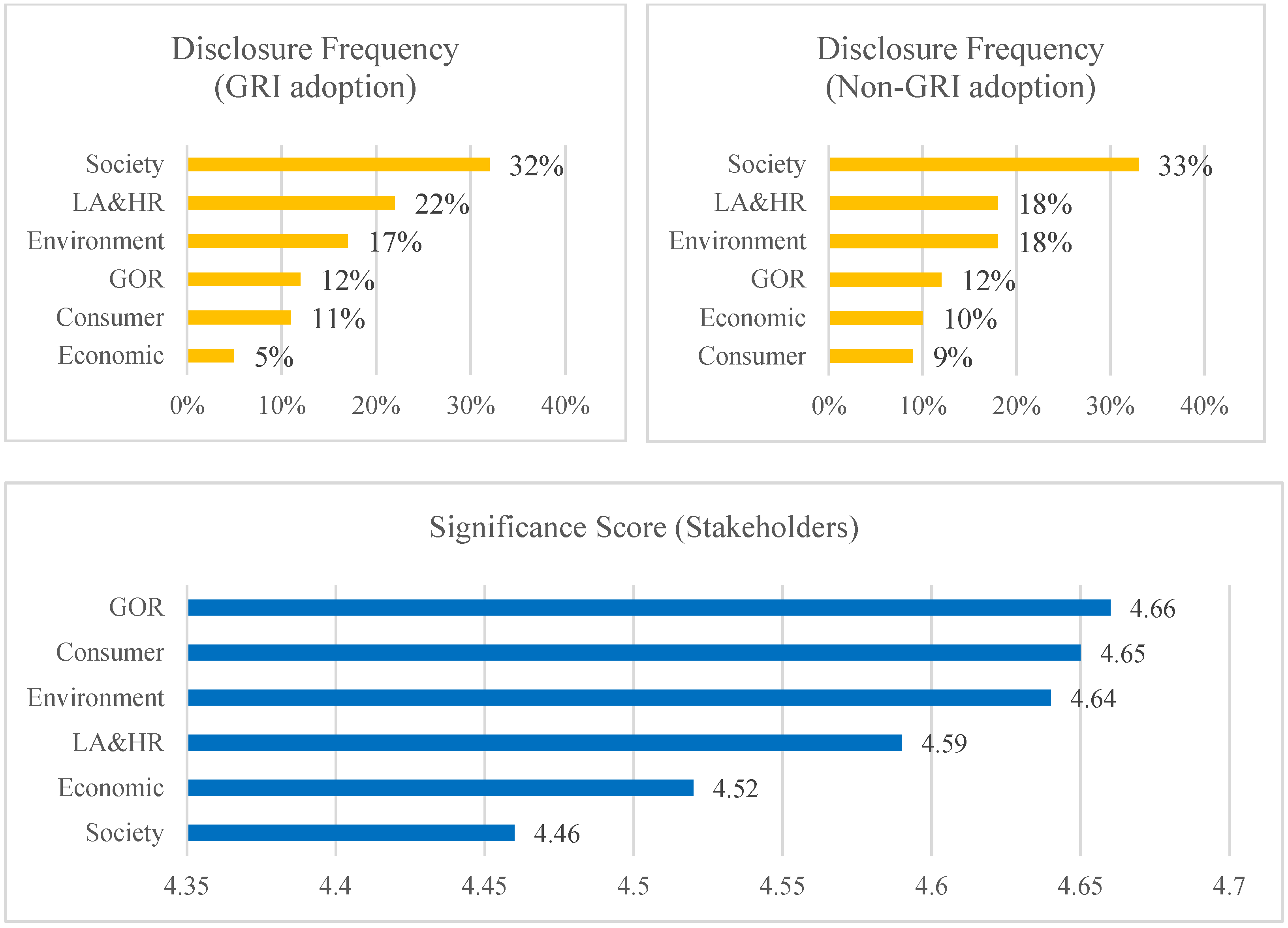

Table A1 in Appendix A presents the results of the content analysis of the sampled CSR reports based on the revised six GRI-oriented dimensions. First and overall, among the original 2205 sustainability activities identified in our content analysis across the 48 selected sampled firms, the majority of sustainability activities reported fall into the society dimension (33%). Others include the LA&HR (21%), environment (18%), governance-oriented risks (12%), consumer (10%), and economic dimensions (7%).

Second, the analysis indicates that companies in 22 out of the 24 industries that adopted GRI guidelines reported more sustainability activities than those that did not. For example, there are two state-owned enterprises (SOEs) in the utility industry (stock codes 003816.SZ and 600905.SH), with comparable firm size/market value, located in the developed regions in China. The former reported 105 sustainability activities in a 137-page ESG report, over twice as many as the latter, which reported 50 activities in a 94-page ESG report. Two non-SOEs (with stock codes 000156.SZ and 600959.SH) in the media industry and located in the developed regions also have a huge gap in terms of the number of sustainability activities reported in their ESG reports. The former reported 51 sustainability activities in a 55-page ESG report, which is four times as many as the latter, which reported 11 activities in a 5-page ESG report. Similarly, in the consumer durables and apparel industry, the firm with GRI adoption (stock code 600690.SH) disclosed 69 sustainability activities in a 133-page ESG report while its counterpart (stock code 000651.SZ) issued a 45-page ESG report with 39 sustainability activities.

Results from Table A1 suggest that firms with GRI adoption not only report more sustainability activities in their CSR reports but also produce longer reports compared to those not adopting GRI guidelines.

4.2. Results of Questionnaire Survey

To answer the research question “What sustainable activities do Chinese stakeholders find most significant?”, both Table 4 and Table A2 (in Appendix A) suggest that the governance-oriented risk (GOR) factor (factor mean = 4.66; std. dev. = 0.60) is considered by Chinese stakeholders the most significant dimension in corporate sustainability. This factor is followed by the consumer dimension (factor mean = 4.65; std. dev. = 0.62) and the environment dimension (factor mean = 4.64; std. dev. = 0.67). Other less important dimensions are LA&HR, economic, and society.

Results also indicate that Chinese stakeholders focus more on certain sustainability activities identified from 43 specific items earlier. For instance, in the governance-oriented risk dimension, “Protect data and network security” (factor mean = 4.78; std. dev. = 0.51) ranks first and “Implement anti-corruption and anti-bribery systems and whistleblower protection systems” (factor mean = 4.73; std. dev. = 0.54) ranks second. These items are related to corporations’ long-term security and ethics issues. For data security, companies are encouraged to engage in sustainable activities such as establishing information system and network security standards, data leakage prevention monitoring, and database encryption technique applications. For anti-corruption activities, companies could consider integrity training programs, violation reporting solutions, criticism by warnings, regulatory talks, and inquiry letters.

In the consumer dimension, “Protect customer privacy information and handle customer complaints properly” (factor mean = 4.74; std. dev. = 0.57) ranks first among the identified five activities. From the stakeholders’ (customers’) perspective, it is of great importance for corporate competence in information protection and handling consumer dissatisfaction. Primary information protection policy and consumer data collection authorization are encouraged. “Crackdown on fake products and implement product recall management” (factor mean = 4.67; std. dev. = 0.60) ranks second, which indicates that Chinese consumers attach importance to product safety and quality management.

In the environment dimension, Chinese consumers regard “Increase resource recycling rate and reduce resource consumption in operation process” (factor mean = 4.74; std. dev. = 0.55) as the most significant activity. “Control the release of pollution” (factor mean = 4.73; std. dev. = 0.60) ranks second and “Work on the national strategy of carbon neutrality and reduce carbon emissions” (factor mean = 4.72; std. dev. = 0.61) ranks third. Companies are suggested to increase their investment in clean energy promotion, resource recycling, pollution reduction, and carbon neutrality. Waste recovery process control, including collection, storage, transportation, and utilization, is also encouraged by Chinese consumers.

It should be noted that although the average score of the LA&HR dimension is not the highest compared with other dimensions, the item “Prohibit the use of child, forced or involuntary labor” (factor mean = 4.80; std. dev. = 0.51) ranks first among all 43 surveyed items. In the LA&HR dimension, Chinese stakeholders pay attention to “Eliminate discrimination on race, region, gender, disability, and nationality” (factor mean = 4.70; std. dev. = 0.60). The survey has revealed that legal and fair employment is considered the most crucial corporate employment issue. Moreover, since “Ensure vocational health and purchase insurance for health, damage, and accident” (factor mean = 4.66; std. dev. = 0.61) ranks third, it would appear that employees’ physical and mental health is of great concern to Chinese consumers.

In the society dimension, consumers assign importance to “Invest in high-tech innovations and enhance R&D competence” (factor mean = 4.62; std. dev. = 0.63) and “Participate in technological innovation projects, promote industry–university–institute cooperation, and global cooperation” (factor mean = 4.59; std. dev. = 0.65). Sci-tech innovation capability and R&D potential attract the most prominent consumers’ attention in this dimension. Companies are expected to take responsibility for technological innovation and popularization. Specifically, sustainability activities such as recruiting top-level sci-tech talent, providing R&D funding, and innovative reward policies should be stressed.

The mean values for the four items are numerically close in the economic dimension. This might be because most financial information is disclosed in annual reports instead of sustainability reports, resulting in less focus on this category.

4.3. Connection between Corporate Sustainability Reporting and Stakeholder Needs

Figure 2 compares the sample firms’ overall stakeholders’ needs regarding sustainability activities (i.e., the sustainability significance score assigned by the respondents) and CSR reporting practices (i.e., the disclosure frequency of each identified dimension). First, although our findings suggest that most of the sampled firms with GRI adoption have more sustainability activities identified in the content analysis than their peers that do not follow the GRI guidelines in the same industries, both groups of firms have a similar pattern of disclosure frequency of the revised six dimensions. That is, out of our six dimensions, the first four rankings of disclosure frequency are society, LA&HR, environment, and governance-oriented risk (GOR), respectively. For the firms with GRI adoption, the consumer dimension is ranked fifth, and the economic dimension is ranked last, while for the firms not following the GRI guidelines, the economic dimension is ranked fifth, and the consumer dimension is ranked last.

Second, from the perspective of stakeholder needs, the most important dimension is governance-oriented risk (with an overall score of 4.66), while the least important is the society dimension (4.46), even though it only scored slightly lower. The consumer dimension is second and the environment dimension is third.

The disparity between the needs of stakeholders and sustainability reporting by firms is illustrated in Figure 2. The sampled firms focus mostly on the society dimension, which stakeholders deem least important. Despite consumers ranking the consumer dimension as the second most important, firms are not paying it enough attention.

The survey divided respondents into male and female groups. Figure 3 illustrates the gender-based difference in stakeholder needs. Men ranked consumers’ needs as most important, followed closely by governance-related risks, then environmental concerns. Women, however, rated environmental and governance-related risks as equally important, followed by consumers’ needs.

We also conducted a two-step cluster analysis on SPSS software (version 24.0) to identify latent stakeholder clusters within the data. The silhouette measure of cohesion and separation of clusters is above 0.0, and the cluster quality is fair and valid.

The cluster analysis is based on respondents’ gender, age, and degree of emphasis on sustainability practice. Three clusters were discovered. They are named sustainability forerunners, sustainability supporters, and sustainability laggards. Table 5 shows the centroid analysis for the three clusters.

The sustainability forerunners cluster shown in Figure 4 is 100% female with 48.1% between 18 and 25 years. This group highly values all the aspects of sustainability, giving them the highest scores. The second cluster, sustainability supporters, is 100% male with 42.2% between 18 and 25 years. They regard all facets of sustainability as important but place special emphasis on the consumer dimension (with a mean of 4.87) and the governance-oriented risk dimension (with a mean of 4.85). The respondents under the sustainability laggards cluster are 71.1% female with 57.9% between 18 and 25 years old. This group does not value sustainability as much, as evident from the lower scores they gave to all dimensions compared to the other two groups.

Based on gender, age, and interest in sustainability practice, we discovered three stakeholder clusters: sustainability forerunners, sustainability supporters, and sustainability laggards. It is suggested that sustainability reporting stakeholders be subdivided into smaller groups. Besides gender and age, other demographic factors such as annual income, specialty, education, and residence region could also be considered. Further, we could investigate stakeholder sustainability interests based on two or more demographic factors.

5. Results Discussion and Policy Implications

5.1. Results Discussion

The main findings of our study suggest that the firms with GRI adoption have disclosed more sustainability content than their peers without GRI adoption in the same industries, and that neither group successfully aligns their sustainability practices with stakeholders’ interests, despite similar disclosure patterns.

The findings provide valuable insights into the sustainability reporting practices of Chinese listed firms and their relevance to stakeholders’ needs [50]. With reference to stakeholder theory and signaling theory, the results are discussed below.

5.1.1. Stakeholder Theory Perspective

From the stakeholder theory lens, companies are not aligning their sustainability efforts with their stakeholder priorities. While the firms with GRI adoption tend to report more sustainability information overall, both groups of firms (those with and without GRI adoption) exhibit a similar pattern in disclosure frequency across the six dimensions.

Notably, these firms focus more on the “society” dimension, likely due to China’s collectivist culture and government emphasis on poverty reduction and social welfare. However, this does not fully reflect the stakeholders’ priorities, who ranked the “governance-oriented risk” dimension as the most important. This indicates that the firms may be more attuned to fulfilling their social responsibilities as defined by the government and broader societal norms, than to addressing the informational needs of their diverse stakeholders.

The firms surveyed did not prioritize customer interests in their sustainability reports, despite stakeholders emphasizing its importance. This shows a misalignment between the firms’ priorities and those of the stakeholders. This suggests that the firms may not be adequately considering the interests of their customers and end-users in their sustainability reporting practices.

Moreover, all respondents focused on governance-oriented risks, possibly due to the COVID-19 pandemic. The pandemic presented a risk and uncertainty to society [44]. The literature suggests that CSR can be used to manage business risks [51]. Effective governance, including transparency, accountability, and strong leadership, can help companies navigate challenges and make informed decisions during a crisis. Effective governance also includes adhering to laws and regulations. Governments worldwide implemented new regulations and guidelines during the pandemic to manage the crisis. Stakeholders may closely monitor how companies follow these new rules, so good governance practices are important for legal and regulatory compliance. Despite being the world’s second largest economy, China’s corporate governance needs improvement compared to developed economies. Thus, Chinese stakeholders (as potential investors) probably expect further improvement in the quality of governance.

5.1.2. Signaling Theory Perspective

From the signaling theory standpoint, some firms use GRI standards to show their commitment to transparency and accountability in sustainability matters. However, the findings suggest that adopting GRI guidelines does not necessarily translate into a closer alignment between the firms’ reporting practices and stakeholders’ priorities.

The COVID-19 pandemic may have further influenced the firms’ sustainability reporting strategies as they navigated the challenging economic environment and shifting stakeholder expectations. While some firms may have doubled their sustainability commitments to signal their resilience and long-term orientation, others may have prioritized short-term financial concerns, leading to a potential divergence from stakeholders’ needs.

Moreover, the unique institutional environment in China, characterized by the pivotal role of the government in regulating reporting practices, may have shaped the firms’ signaling behaviors. As reflected in the high disclosure frequency of the “society” and “environment” dimensions, the emphasis on societal and environmental contributions could be interpreted as a strategic response to government policy priorities and expectations—for example, the Chinese government formally announced its commitment to the “dual carbon goal” in September 2020, in which China aims to achieve carbon neutrality (the net-zero carbon emissions goal) before 2060 and that China’s carbon emissions would peak before 2030)—rather than addressing stakeholder concerns.

5.2. Policy Implications and Recommendations

The findings of this study, combined with the recent regulatory efforts by Chinese authorities, provide valuable insights for policymakers and Chinese listed firms to enhance the quality and relevance of sustainability reporting practices.

Chinese authorities have recently taken significant steps to regulate CSR/ESG reporting for firms listed on China’s three major stock exchanges—the Shanghai Stock Exchange (SSE), Shenzhen Stock Exchange (SZSE), and Beijing Stock Exchange (BSE). On 8 February 2024, they published new sustainability reporting guidelines for listed companies. Starting in 2026, larger-cap and dual-listed companies in China are required to disclose information on a wide range of environmental, social, and governance (ESG) topics as part of corporate sustainability reporting guidelines. The new guidelines require companies to disclose sustainability-related information in reports covering various topics, including circular economy practices and their contribution to China’s national development strategy.

The Shanghai, Shenzhen, and Beijing Stock Exchanges introduced new guidelines for sustainability reporting. These guidelines show the Chinese government’s efforts to improve and standardize ESG disclosures among public companies. This move complements a study revealing the necessity for Chinese companies to enhance their sustainability reporting to meet the information needs of various stakeholders. Chinese listed firms should improve their sustainability reporting by considering both government regulations and stakeholders’ priorities. They should interact and address the concerns of customers, investors, and local communities. This could involve supplementing their GRI-based disclosures with additional information that directly addresses the concerns and interests of these stakeholders, as identified through regular engagement and feedback mechanisms.

By fostering a closer alignment between corporate sustainability reporting and stakeholder priorities, Chinese listed firms can enhance the credibility of their sustainability signals, improve transparency, and ultimately strengthen their relationships with key stakeholders. This, in turn, can contribute to these firms’ long-term sustainability and competitiveness in the evolving business landscape.

Policymakers should improve reporting rules to focus more on stakeholders. This could involve requiring businesses to disclose how they involve stakeholders and use their feedback in sustainability plans. They could also create standards for different industries or provide advice on how to evaluate sustainability issues that matter most to their stakeholders. If Chinese policymakers and firms make regulatory efforts that meet the needs of various stakeholders, they can foster a more transparent and accountable sustainability reporting ecosystem. This can ultimately contribute to the country’s broader sustainability goals and enhance the long-term resilience of its capital markets.

The findings of this study suggest that Chinese firms should improve their sustainability reports to meet the needs of various stakeholders, including the government, customers, investors, and local communities. This could be achieved by balancing the disclosure of their social responsibilities as required by the government while also addressing the concerns of other important stakeholders.

Furthermore, adopting GRI standards, while a positive step, may not be sufficient to ensure the quality and relevance of sustainability reporting. Firms should also provide additional information that meets their stakeholders’ needs and concerns, identified through regular interaction and feedback. By fostering a closer alignment between corporate sustainability reporting and stakeholder priorities, Chinese listed firms can enhance the credibility of their sustainability signals, improve transparency, and ultimately strengthen their relationships with key stakeholders. This will also help them remain sustainable and competitive in the ever-changing business world.

6. Conclusions

This study delves into the alignment between corporate sustainability reporting and stakeholder interests in China, particularly through the lens of GRI standards adoption by listed firms. By analyzing ESG reports from 48 companies and surveying 409 stakeholders, we unveil a notable misalignment: firms with GRI adoption report more on sustainability activities yet fail to align these reports with the actual interests of stakeholders. This misalignment suggests that firms’ sustainability efforts might lean more towards satisfying regulatory demands and government policies rather than addressing stakeholder needs. Our findings highlight the crucial need for Chinese firms to enhance their sustainability reporting practices by better aligning them with stakeholders’ priorities. This research provides insights for policymakers and corporate managers on the importance of bridging the gap between corporate sustainability efforts and stakeholders’ expectations, advocating for a balance between compliance and genuine stakeholders’ engagement to achieve societal sustainability goals within China’s regulatory and cultural setting.

Author Contributions

Conceptualization, L.X. (Lu Xu), L.X. (Li Xie), and Y.S.; methodology, L.X. (Lu Xu) and Y.Z.; formal analysis, L.X. (Lu Xu) and L.X. (Li Xie); investigation, L.X. (Lu Xu) and S.M.; data curation, L.X. (Lu Xu); writing—original draft preparation, L.X. (Lu Xu), Y.S. and J.H.; writing—review and editing, L.X. (Lu Xu), L.X. (Li Xie), Y.S. and J.H.; supervision, L.X. (Lu Xu) and Y.S.; project administration, L.X. (Lu Xu) and Y.S.; funding acquisition, L.X. (Lu Xu) and S.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Zhejiang Provincial Philosophy and Social Sciences Planning Project, grant number 23NDJC144YB and 22FNSQ77YB; the Fundamental Research Funds of Zhejiang Sci-Tech University, grant number 23096010-Y; the National Natural Science Foundation of China, grant number 71402170; and China National College Student Innovation and Entrepreneurship Project, grant number 202211058048X.

Institutional Review Board Statement

The study was conducted in accordance with the Declaration of Helsinki, and approved by the Ethics Committee of Xi’an Jiaotong-Liverpool University (protocol code No.: ER-LRR-11000123420240125135113 and date of approval: 29 January 2024).

Informed Consent Statement

Informed consent was obtained from all subjects involved in this study.

Data Availability Statement

Data are not available due to ethical restrictions.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Content analysis of sustainability activities.

| Industry | Stock Code | Location | GRI | SOE | Sustainability Dimensions | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Environment | Economic | Society | Consumer | LA&HR | GOR | Total | |||||

| Energy | 600792.SH | Yunnan | * | 3 | 3 | 3 | 1 | 11 | 8 | 29 | |

| 600387.SH | Zhejiang | 0 | 5 | 0 | 0 | 0 | 6 | 11 | |||

| Materials | 600019.SH | Shanghai | * | ** | 16 | 1 | 15 | 9 | 15 | 4 | 60 |

| 600585.SH | Anhui | 13 | 2 | 9 | 5 | 14 | 2 | 45 | |||

| Capital goods | 601766.SH | Beijing | * | ** | 9 | 1 | 29 | 0 | 7 | 1 | 47 |

| 600031.SH | Beijing | 6 | 3 | 14 | 2 | 10 | 0 | 35 | |||

| Commercial and professional services | 300012.SZ | Guangdong | * | 7 | 0 | 8 | 3 | 11 | 5 | 34 | |

| 603568.SH | Zhejiang | 7 | 1 | 3 | 0 | 4 | 2 | 17 | |||

| Transportation | 000507.SZ | Guangdong | * | 17 | 2 | 8 | 4 | 9 | 5 | 45 | |

| 000905.SZ | Fujian | 7 | 0 | 15 | 0 | 0 | 0 | 22 | |||

| Automobiles and components | 600104.SH | Shanghai | * | 12 | 5 | 28 | 4 | 11 | 3 | 63 | |

| 601633.SH | Hebei | 14 | 1 | 9 | 8 | 3 | 6 | 41 | |||

| Consumer durables and apparel | 600690.SH | Shandong | * | 13 | 2 | 21 | 8 | 21 | 4 | 69 | |

| 000651.SZ | Guangdong | 5 | 3 | 6 | 13 | 7 | 5 | 39 | |||

| Consumer services | 002033.SZ | Yunnan | * | 2 | 3 | 5 | 4 | 10 | 2 | 26 | |

| 300859.SZ | Xinjiang | 0 | 4 | 0 | 0 | 2 | 3 | 9 | |||

| Media | 000156.SZ | Zhejiang | * | 7 | 6 | 10 | 17 | 8 | 3 | 51 | |

| 600959.SH | Jiangsu | 0 | 0 | 8 | 1 | 0 | 2 | 11 | |||

| Retailing | 601828.SH | Shanghai | * | 8 | 6 | 10 | 10 | 17 | 2 | 53 | |

| 600739.SH | Liaoning | 3 | 4 | 6 | 0 | 11 | 3 | 27 | |||

| Food and staples retailing | 300783.SZ | Anhui | * | 8 | 0 | 23 | 4 | 6 | 7 | 48 | |

| 601116.SH | Zhejiang | 0 | 5 | 4 | 0 | 0 | 6 | 15 | |||

| Food, beverage, and tobacco | 600600.SH | Shandong | * | 12 | 4 | 12 | 3 | 9 | 5 | 45 | |

| 000596.SZ | Anhui | 3 | 4 | 3 | 2 | 6 | 2 | 20 | |||

| Household and personal products | 603605.SH | Zhejiang | * | 14 | 5 | 9 | 4 | 15 | 5 | 52 | |

| 300957.SZ | Yunnan | 16 | 4 | 9 | 3 | 9 | 7 | 48 | |||

| Healthcare equipment and services | 688139.SH | Shandong | * | 14 | 2 | 26 | 4 | 10 | 8 | 64 | |

| 688050.SH | Beijing | 4 | 5 | 18 | 1 | 12 | 3 | 43 | |||

| Pharmaceuticals, biotechnology, and life sciences | 000538.SZ | Yunnan | * | 10 | 3 | 18 | 6 | 5 | 14 | 56 | |

| 603392.SH | Beijing | 12 | 5 | 10 | 0 | 5 | 7 | 39 | |||

| Banks | 601665.SH | Shandong | * | 6 | 1 | 18 | 9 | 12 | 7 | 53 | |

| 601187.SH | Fujian | 4 | 5 | 21 | 7 | 7 | 0 | 44 | |||

| Diversified financials | 600837.SH | Shanghai | * | 6 | 5 | 30 | 10 | 7 | 10 | 68 | |

| 300033.SZ | Zhejiang | 7 | 4 | 7 | 4 | 7 | 3 | 32 | |||

| Insurance | 601318.SH | Guangdong | * | 7 | 4 | 22 | 16 | 8 | 5 | 62 | |

| 601628.SH | Beijing | ** | 3 | 4 | 23 | 18 | 4 | 11 | 63 | ||

| Software and services | 600570.SH | Zhejiang | * | 13 | 4 | 28 | 3 | 18 | 8 | 74 | |

| 600845.SH | Shanghai | ** | 0 | 5 | 8 | 2 | 13 | 5 | 33 | ||

| Technological hardware and equipment | 601138.SH | Guangdong | * | 15 | 5 | 10 | 0 | 23 | 15 | 68 | |

| 002415.SZ | Zhejiang | ** | 10 | 6 | 7 | 7 | 10 | 8 | 48 | ||

| Semiconductors and semiconductor equipment | 603501.SH | Shanghai | * | 9 | 0 | 6 | 3 | 18 | 10 | 46 | |

| 002459.SZ | Hebei | 16 | 4 | 11 | 6 | 15 | 9 | 61 | |||

| Telecommunication services | 600050.SH | Beijing | * | ** | 3 | 3 | 47 | 21 | 18 | 5 | 97 |

| 601698.SH | Beijing | ** | 3 | 5 | 62 | 0 | 9 | 5 | 84 | ||

| Utilities | 003816.SZ | Guangdong | * | ** | 22 | 5 | 33 | 0 | 22 | 23 | 105 |

| 600905.SH | Beijing | ** | 18 | 4 | 17 | 0 | 4 | 7 | 50 | ||

| Real estate | 600383.SH | Guangdong | * | 0 | 0 | 17 | 0 | 10 | 3 | 30 | |

| 600606.SH | Shanghai | 4 | 5 | 14 | 0 | 0 | 0 | 23 | |||

| Total | 388 | 158 | 720 | 222 | 453 | 264 | 2205 | ||||

| Average per report | 8.08 | 3.29 | 15.00 | 4.63 | 9.44 | 5.50 | 45.94 | ||||

| Range | 0–22 | 0–6 | 0–62 | 0–21 | 0–23 | 0–23 | 9–105 | ||||

| GRI adopters | 233 | 70 | 436 | 143 | 301 | 162 | 1345 | ||||

| Non-GRI adopters | 155 | 88 | 284 | 79 | 152 | 102 | 860 | ||||

| Percentage of GRI adopters | 17% | 5% | 32% | 11% | 22% | 12% | 100% | ||||

| Percentage of non-GRI adopters | 18% | 10% | 33% | 9% | 18% | 12% | 100% | ||||

| Percentage of total | 18% | 7% | 33% | 10% | 21% | 12% | 100% | ||||

Notes: * shows that ESG reports are prepared based on the GRI standard. ** indicates a state-owned enterprise. LA&HR denotes labor, decent work, and human rights. GOR denotes governance-oriented risk.

Table A2.

Significance score of survey items.

| Dimensions | Items | Mean | Std. Dev. |

|---|---|---|---|

| Environment | Work on national strategy of carbon neutrality and reduction of carbon emissions | 4.72 | 0.61 |

| Utilize clean and renewable energy and minimize the negative impact of climate change | 4.69 | 0.66 | |

| Control the release of pollution (e.g., wastewater, noise, greenhouse gas, and solid wastes) | 4.73 | 0.60 | |

| Increase resource recycling rate and reduce recourse consumption (e.g., water, electricity, natural gas, and petrol) in the operation process | 4.74 | 0.55 | |

| Increase facility investment on recourse and energy saving and protect the environment in the entire life cycle when providing products and services | 4.63 | 0.67 | |

| Establish a green energy data center for environmental detection and analysis | 4.52 | 0.74 | |

| Sustain biodiversity and conserve flora and fauna | 4.69 | 0.65 | |

| Establish an evaluation model for environmental performance | 4.54 | 0.75 | |

| Save paper and plastic through packaging, shipment, and daily office activity | 4.54 | 0.73 | |

| Economic | Preserve the value of shareholders’ assets and increase profit distribution | 4.44 | 0.80 |

| Increase market value | 4.55 | 0.73 | |

| Disclose financial performance (e.g., sales revenue, net income, EPS, ROE, and ROI) | 4.55 | 0.73 | |

| Contribution of tax payment | 4.55 | 0.71 | |

| Society | Donate during the COVID-19 period and rollout of volunteer and charity events | 4.33 | 0.81 |

| Provide poverty alleviation and critical illness assistance | 4.40 | 0.78 | |

| Assist in infrastructure in poor areas and purchase or help to sell agricultural products in poor areas | 4.36 | 0.80 | |

| Provide public education grants for children and support special education for autistic children | 4.39 | 0.81 | |

| Provide job opportunities for female, disabled, and ethnic minorities | 4.44 | 0.79 | |

| Participate in technological innovation projects, promote industry–university–institute cooperation and global cooperation | 4.59 | 0.65 | |

| Invest in high-tech innovations and enhance R&D competence | 4.62 | 0.63 | |

| Facilitate the development of SMEs and promote and lead industry development | 4.50 | 0.71 | |

| Initiate the perspective of healthy living | 4.54 | 0.71 | |

| Consumer | Establish a customer-oriented strategy and encourage product innovation and service efficiency | 4.60 | 0.64 |

| Detect fake products and implement product recall management | 4.67 | 0.60 | |

| Protect customer privacy information and handle customer complaints properly | 4.74 | 0.57 | |

| Process client review and survey on customer satisfaction | 4.63 | 0.64 | |

| Upgrade consumer experience and explore customer communication channels | 4.64 | 0.63 | |

| LA&HR | Establish employee representative commission and encourage employee involvement in decision-making | 4.43 | 0.78 |

| Provide regular training programs for career development with a fair performance evaluation system and compensation system | 4.62 | 0.62 | |

| Ensure vocational health and safety management and purchase insurance for health, damage, and accident | 4.66 | 0.61 | |

| Keep work–life balance and provide holiday time, festival celebration, sports and entertainment activities, and a recuperate program | 4.57 | 0.66 | |

| Provide medical examinations on a regular basis and provide psychological care | 4.61 | 0.64 | |

| Eliminate discrimination on race, region, gender, disability, and nationality | 4.70 | 0.60 | |

| Increase the proportion of female managers and take care of female employees | 4.58 | 0.71 | |

| Prohibit the use of child and forced labor | 4.80 | 0.51 | |

| Offer public rental housing benefits and rental allowance | 4.49 | 0.74 | |

| Provide financial assistance for employees with family difficulties | 4.45 | 0.78 | |

| Survey on employee satisfaction and build up a working environment that features diversity and fairness | 4.59 | 0.65 | |

| GOR | Evaluate ESG performance for customers, suppliers, and employees | 4.59 | 0.64 |

| Set up risk management and internal control commission and risk rating system | 4.60 | 0.63 | |

| Establish life cycle quality management system, emergency management system, and safety inspection and training system | 4.60 | 0.65 | |

| Protect data and network security | 4.78 | 0.51 | |

| Implement anti-corruption and anti-bribery systems and whistleblower protection systems | 4.73 | 0.54 |

References

- Tsang, A.; Frost, T.; Cao, H. Environmental, social, and governance (ESG) disclosure: A literature review. Br. Account. Rev. 2023, 55, 101149. [Google Scholar] [CrossRef]

- Stuart, A.C.; Fuller, S.H.; Heron, N.M.; Riley, T.J. Defining CSR disclosure quality: A review and synthesis of the accounting literature. J. Account. Lit. 2023, 45, 1–47. [Google Scholar] [CrossRef]

- Mougenot, B.; Doussoulin, J.P. A bibliometric analysis of the Global Reporting Initiative (GRI): Global trends in developed and developing countries. Environ. Dev. Sustain. 2024, 26, 6543–6560. [Google Scholar] [CrossRef]

- Bradford, M.; Earp, J.B.; Showalter, D.S.; Williams, P.F. Corporate sustainability reporting and stakeholder concerns: Is there a disconnect? Account. Horiz. 2017, 31, 83–102. [Google Scholar] [CrossRef]

- Shen, H.; Lin, H.; Han, W.; Wu, H. ESG in China: A review of practice and research, and future research avenues. China J. Account. Res. 2023, 16, 100325. [Google Scholar] [CrossRef]

- Anton, A.I.; Earp, J.B. A requirements taxonomy to reduce website privacy vulnerabilities, to appear. Requir. Eng. 2004, 9, 169–185. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stockholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Mgt. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Howarth, R.B.; Norgaard, R.B. Environmental valuation under sustainable development. Am. Econ. Rev. 1992, 82, 473–477. [Google Scholar]

- Benabou, R.; Tirole, J. Individual and corporate social responsibility. Economics 2010, 77, 1–19. [Google Scholar]

- Lins, K.V.; Servaes, H.; Tamayo, A. Social capital, trust, and firm performance: The value of corporate social responsibility during the financial crisis. J. Financ. 2017, 72, 1785–1824. [Google Scholar] [CrossRef]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Kleimeier, S.; Viehs, M. Carbon Disclosure, Emission Levels, and the Cost of Debt. Available online: https://www.researchgate.net/publication/314699310 (accessed on 7 January 2023).

- Nassos, G.P.; Avlonas, N. Practical Sustainability Strategies: How to Gain a Competitive Advantage; John Wiley & Sons: New York, NY, USA, 2020; pp. 243–274. [Google Scholar]

- Christensen, H.B.; Hail, L.; Leuz, C. Mandatory CSR and sustainability reporting: Economic analysis and literature review. Rev. Account. Stud. 2021, 26, 1176–1248. [Google Scholar] [CrossRef]

- Thoradeniya, P.; Lee, J.; Tan, R.; Ferreira, A. From intention to action on sustainability reporting: The role of individual, organizational and institutional factors during war and post-war periods. Br. Account. Rev. 2022, 54, 101021. [Google Scholar] [CrossRef]

- Deloitte. Sustainability Disclosure: Getting Ahead of the Curve. Available online: https://www2.deloitte.com/content/dam/Deloitte/us/Documents/risk/us-risk-sustainability-disclosure.pdf (accessed on 15 January 2023).

- Dingwerth, K.; Eichinger, M. Tamed transparency: How information disclosure under the global reporting initiative fails to empower. Glob. Environ. Politics 2010, 10, 74–96. [Google Scholar] [CrossRef]

- Bucaro, A.C.; Jackson, K.E.; Lill, J.B. The influence of corporate social responsibility measures on investors’ judgments when integrated in a financial report versus presented in a separate report. Contemp. Account. Res. 2020, 37, 665–695. [Google Scholar] [CrossRef]

- Grewal, J.; Serafeim, G. Research on corporate sustainability: Review and directions for future research. Found. Trends Account. 2020, 14, 73–127. [Google Scholar] [CrossRef]

- Lindgren, C.; Huq, A.M.; Carling, K. Who are the intended users of CSR reports? Insights from a data-driven approach. Sustainability 2021, 13, 1070. [Google Scholar] [CrossRef]

- Mion, G.; Loza Adaui, C.R. Mandatory nonfinancial disclosure and its consequences on the sustainability reporting quality of Italian and German companies. Sustainability 2019, 11, 4612. [Google Scholar] [CrossRef]

- Hamilton, S.N.; Waters, R.D. Mainstreaming standardized sustainability reporting: Comparing Fortune 50 corporations’ and US News & World Report’s top 50 global universities’ sustainability reports. Sustainability 2022, 14, 3442. [Google Scholar] [CrossRef]

- Ervits, I. CSR reporting by Chinese and western MNEs: Patterns combining formal homogenization and substantive differences. Int. J. Corp. Soc. Responsib. 2021, 6, 6. [Google Scholar] [CrossRef]

- Ammann, M.; Bauer, C.; Fischer, S.; Müller, P. The impact of the Morningstar Sustainability Rating on mutual fund flows. Eur. Financial Manag. 2019, 25, 520–553. [Google Scholar] [CrossRef]

- Hartzmark, S.M.; Sussman, A.B. Do investors value sustainability? A natural experiment examining ranking and fund flows. J. Financ. 2019, 74, 2789–2837. [Google Scholar] [CrossRef]

- See, G. Harmonious society and Chinese CSR: Is there really a link? J. Bus. Ethics 2009, 89, 1–22. [Google Scholar] [CrossRef]

- Lattemann, C.; Fetscherin, M.; Alon, I.; Li, S.; Schneider, A.M. CSR communication intensity in Chinese and Indian multinational companies. Corp. Gov. Int. Rev. 2009, 17, 426–442. [Google Scholar] [CrossRef]

- McKinnon, J. Cultural constraints on audit independence in Japan. Int. J. Account. 1984, 20, 17–43. [Google Scholar]

- Yamagami, T.; Kokubu, K. A note on corporate social disclosure in Japan. Account. Audit. Account. J. 1991, 4, 32–39. [Google Scholar] [CrossRef]

- Haider, M.B.; Kokubu, K. Assurance and third-party comment in sustainability reporting in Japan: A descriptive study. Int. J. Environ. Sustain. Dev. 2015, 14, 207–230. [Google Scholar] [CrossRef]

- Xu, S.; Yang, R. Indigenous characteristics of Chinese corporate social responsibility conceptual paradigm. J. Bus. Ethics 2010, 93, 321–333. [Google Scholar] [CrossRef]

- Salehi, M.; DashtBayaz, M.L.; Khorashadizadeh, S. Corporate social responsibility and future financial performance: Evidence from Tehran Stock Exchange. EuroMed J. Bus. 2018, 13, 351–371. [Google Scholar] [CrossRef]

- Sisaye, S. The influence of non-governmental organizations (NGOs) on the development of voluntary sustainability accounting reporting rules. J. Bus. Socio-Econ. Dev. 2021, 1, 5–23. [Google Scholar] [CrossRef]

- Bridges, C.M.; Harrison, J.A.; Hay, D.C. The ungreening of integrated reporting: A reflection on regulatory capture. Meditari Account. Res. 2022, 30, 597–625. [Google Scholar] [CrossRef]

- Elaigwu, M.; Abdulmalik, S.O.; Talab, H.R. Corporate integrity, external assurance and sustainability reporting quality: Evidence from the Malaysian public listed companies. Asia-Pac. J. Bus. Adm. 2024, 16, 410–440. [Google Scholar] [CrossRef]

- Maignan, I.; Ralston, D.A. Corporate social responsibility in Europe and the US: Insights from businesses’ self-presentations. J. Int. Bus. Stud. 2002, 33, 497–514. [Google Scholar] [CrossRef]

- Davis, K.; Blomstrom, R.L. Business and Society: Environment and Responsibility; McGraw-Hill: New York, NY, USA, 1975; pp. 23–45. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Sundin, H.; Brown, D.A. Greening the black box: Integrating the environment and management control systems. Account. Audit. Accoun. 2017, 30, 620–642. [Google Scholar] [CrossRef]

- Global Reporting Initiative (GRI). Integrated Reporting. Available online: https://www.globalreporting.org/information/currentpriorities/integratedreporting/Pages/default.aspx (accessed on 15 January 2023).

- Oberseder, M.; Schlegelmilch, B.B.; Murphy, P.E. CSR practices and consumer perceptions. J. Bus. Res. 2013, 66, 1839–1851. [Google Scholar] [CrossRef]

- Cheng, S.; Lin, K.Z.; Wong, W. Corporate social responsibility reporting and firm performance: Evidence from China. J. Manag. Govern. 2016, 20, 503–523. [Google Scholar] [CrossRef]

- Crane, A.; Matten, D. COVID-19 and the future of CSR research. J. Manag. Stud. 2021, 58, 280–284. [Google Scholar] [CrossRef]

- Ehnert, I.; Parsa, S.; Roper, I.; Wagner, M.; Muller-Camen, M. Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world’s largest companies. Int. J. Hum. Resour. Manag. 2016, 27, 88–108. [Google Scholar] [CrossRef]

- Hess, D. The transparency trap: Non-financial disclosure and the responsibility of business to respect human rights. Am. Bus. Law J. 2019, 56, 5–53. [Google Scholar] [CrossRef]

- Monteiro, A.P.; García-Sánchez, I.M.; Aibar-Guzmán, B. Labour practice, decent work and human rights performance and reporting: The impact of women managers. J. Bus. Ethics 2022, 180, 523–542. [Google Scholar] [CrossRef]

- Straub, D.W. Validating instruments in MIS research. MIS Q. 1989, 13, 147–169. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Sun, Y.; Wang, J.J.; Huang, K.T. Does IFRS and GRI adoption impact the understandability of corporate reports by Chinese listed companies? Account. Financ. 2022, 62, 2879–2904. [Google Scholar] [CrossRef]

- Smith, N.C. Corporate social responsibility: Whether or how? Calif. Manage. Rev. 2003, 45, 52–76. [Google Scholar] [CrossRef]

Figure 1.

Research process.

Figure 2.

Connection between stakeholders’ interests and corporate SR practices with and without GRI adoption. Notes: LA&HR denotes labor, decent work, and human rights. GOR denotes governance-oriented risk.

Figure 2.

Connection between stakeholders’ interests and corporate SR practices with and without GRI adoption. Notes: LA&HR denotes labor, decent work, and human rights. GOR denotes governance-oriented risk.

Figure 3.

Gender-based difference in stakeholder needs.

Figure 4.

Cell distribution in six dimensions for sustainability forerunners cluster.

Table 1.

Differences in SR practices.

| Country | Content | SR Practice | SR Uniqueness in China | Reference |

|---|---|---|---|---|

| US and European countries | Institutional context | The market plays a leading role in economic development, and companies have more stabilized SR-related regulation regimes. | The Chinese government plays a leading role in SR standards-setting and economic development. | Ervits (2021) [24] |

| Encourage all kinds of companies in sustainability practice | Encourage more sustainable activities in state-owned companies | See (2009) [27] | ||

| India | Communication style | Rule-based | Relation-based | Lattemann et al. (2009) [28] |

| Communication quality | Well-rounded and multi-dimensional communication on SR motives, processes, and stakeholder concerns | Limited communication on SR motives, processes, and stakeholder concerns | ||

| Japan | Assurance | Credibility assurance of SR from an independent third party | Absence of SR assurance | Yamagami and Kokubu (1991) [30]; Haider and Kokubu (2015) [31] |

Table 2.

GRI dimensions, descriptions, and examples.

| Dimensions | Description | Sample Sustainable Activity |

|---|---|---|

| Environment | Activities that specify the long-term sustainable impact of a company’s operations on climate and natural resources | Established photovoltaic power generation equipment to reduce carbon dioxide emissions (600019.SH in the materials industry) |

| Economic | Activities that describe a company’s economic value generated and distributed, financial implications, and financial assistance | Increased tax payment per share (600104.SH in the automobiles and components industry) |

| Society | Activities that indicate how a company affects areas and people locally, nationally, and globally | Donated 168 billion RMB to poverty-stricken areas in Guangxi and Gansu Provinces (601766.SH in the capital goods industry) |

| Consumer | Activities that describe how a company improves consumer experience | Encouraged internet-based instead of paper-based form filling to shorten the waiting time of consumers (600050.SH in the telecommunication services industry) |

| LA&HR | Activities that indicate how a company protects employees’ human rights and improves employee satisfaction | Provided 245 h of training for employees (601828.SH in the retail industry) |

| GOR | Activities that describe how a company identifies and avoids risks | Increased the proportion of independent directors in the performance evaluation commission and auditing commission (600383.SH in the real estate industry) |

Notes: LA&HR denotes labor, decent work, and human rights. GOR denotes governance-oriented risk.

Table 3.

Demographics of respondents.

| Number | Percentage | |

|---|---|---|

| Age: | ||

| 18–25 | 207 | 50.6% |

| 25–35 | 89 | 21.8% |

| 36–45 | 58 | 14.2% |

| above 45 | 55 | 13.4% |

| Gender: | ||

| Male | 143 | 35.0% |

| Female | 266 | 65.0% |

| Specialty: | ||

| Management | 219 | 53.5% |

| Economics | 70 | 17.1% |

| Engineering | 49 | 12.0% |

| Education | 27 | 6.6% |

| Computer science | 17 | 4.2% |

| Medicine | 11 | 2.7% |

| Others | 16 | 3.9% |

| Income: | ||

| Under 50,000 RMB | 178 | 43.5% |

| 50,000–100,000 RMB | 74 | 18.1% |

| 100,001–200,000 RMB | 75 | 18.3% |

| 200,001–300,000 RMB | 47 | 11.5% |

| Above 300,000 RMB | 35 | 8.6% |

| Education: | ||

| Below high school | 8 | 2.0% |

| Associate | 28 | 6.8% |

| Bachelor’s | 293 | 71.6% |

| Master’s and above | 80 | 19.6% |

| Region: | ||

| Eastern China | 344 | 84.1% |

| Northwest | 41 | 10.0% |

| Northern China | 11 | 2.7% |

| Southern China | 8 | 2.0% |

| Central China | 3 | 0.7% |

| Others | 2 | 0.5% |

Table 4.

Means and reliabilities of sustainability factors.

| Factor | Mean | Std. Dev. | Cronbach’s Alpha | Item Number |

|---|---|---|---|---|

| Factor 1: Environment | 4.64 | 0.67 | 0.91 | 9 |

| Factor 2: Economic | 4.52 | 0.74 | 0.79 | 4 |

| Factor 3: Society | 4.46 | 0.75 | 0.94 | 9 |

| Factor 4: Consumer | 4.65 | 0.62 | 0.87 | 5 |

| Factor 5: LA&HR | 4.59 | 0.68 | 0.93 | 11 |

| Factor 6: GOR | 4.66 | 0.60 | 0.89 | 5 |

| Total | 0.973 | 43 |

Table 5.

Centroid analysis.

| Environment | Economic | Society | Consumer | LA&HR | GOR | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | Mean | Std. Dev. | ||

| Cluster | Sustainability forerunners | 4.94 | 0.14 | 4.85 | 0.32 | 4.88 | 0.25 | 4.96 | 0.14 | 4.93 | 0.14 | 4.96 | 0.14 |

| Sustainability supporters | 4.81 | 0.31 | 4.69 | 0.43 | 4.64 | 0.46 | 4.87 | 0.24 | 4.78 | 0.31 | 4.85 | 0.27 | |

| Sustainability laggards | 4.20 | 0.56 | 4.04 | 0.58 | 3.87 | 0.52 | 4.16 | 0.52 | 4.08 | 0.51 | 4.19 | 0.53 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Xu, L.; Xie, L.; Mei, S.; Hao, J.; Zhang, Y.; Song, Y. Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China. Sustainability 2024, 16, 3443. https://doi.org/10.3390/su16083443

AMA Style

Xu L, Xie L, Mei S, Hao J, Zhang Y, Song Y. Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China. Sustainability. 2024; 16(8):3443. https://doi.org/10.3390/su16083443

Chicago/Turabian StyleXu, Lu, Li Xie, Shengjun Mei, Jianli Hao, Yuqian Zhang, and Yu Song. 2024. "Corporate Sustainability Reporting and Stakeholders’ Interests: Evidence from China" Sustainability 16, no. 8: 3443. https://doi.org/10.3390/su16083443

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.