Economic Policy Uncertainty, National Culture, and Corporate Debt Financing

1

School of Economics and Finance, Xi’an Jiaotong University, Xi’an 710049, China

2

La Trobe Business School, La Trobe University, Melbourne, VIC 3083, Australia

3

Department of Business Management, University of Johannesburg, Johannesburg 2092, South Africa

4

Department of Commerce, University of Kotli Azad Jammu and Kashmir, Muzaffarabad 11100, Pakistan

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(20), 11179; https://doi.org/10.3390/su132011179

Submission received: 28 August 2021

/

Revised: 4 October 2021

/

Accepted: 5 October 2021

/

Published: 11 October 2021

(This article belongs to the Special Issue Application of Quantitative Methods in Modelling Sustainability in Economics and Finance)

Abstract

:Financial innovation vis-à-vis economic policy uncertainty (EPU) without due regards being given to debt financing. This paper fills this gap and unveils the dynamic role of national culture in defining debt financing via EPU. We use a sample of 3831 non-financial firms of Asian economies and employ the System Generalized Method of Moments to estimate the regression coefficients. Our findings reveal an inverse relationship between the EPU and debt financing, which suggests that debt finance mitigation strategies are successfully executed in the region. The potential reasons for this include the policies by businesses to reduce business activities and avoid the unfavorable rising financing cost through EPU. On the supply side, the rising EPU induces the banks to accelerate their interest rate due to increased default risk. Similarly, we observe that high uncertainty avoidance (UND) has a negative and significant link with debt financing due to an unpleasant behavior of corporate managers towards debt when they have an alternate source of financing instruments instead of accepting long-term obligations. However, we find that the UND and EPU interaction has a significantly positive impact on debt financing due to the rigid behavior of managers, which forces them to consider cultural traits and converts their risk-averse attitude into risk-friendly behavior. This implies that corporate managers should reflect the sensitivity of the national culture while considering debt financing.

1. Introduction

Recent literature on economic policy uncertainty (EPU) and sustainable economic growth has mostly addressed issues related to financial stability without due regards being given to debt financing instruments. For example, Phan et al. [1], Ashraf and Shen [2], Xu et al. [3], and Guedhami et al. [4] are among those who considered various EPU models and financial stability. However, the issue of EPU on sustainable economic growth under debt financing practices vis-à-vis a socioeconomic structure based on cultural values is ignored. This paper fills this gap in the literature and unveils interesting dynamic characteristics of national culture, which play a defining role in debt financing under EPU. Phan et al. [1] investigated the impact of EPU on financial stability, demonstrating a significantly negative impact. This motivated the idea to redefine EPU as an assortment of economic risk, which converts an evolution into an ambiguous position, e.g., monetary, and fiscal policy uncertainty, tax regime uncertainty, and other regulatory institution uncertainty. Furthermore, it is defined as the discrepancies confronted by economic mediators in forecasting the future course of fiscal policies, regulatory, monetary, and trade policy [5]. Many academic scholars and other policy makers have admitted the dreadful outcomes of economic policy uncertainty on sustainable economic growth. Baker et al. (2016) highlight that the industrial production of the USA during 2005 to 2012 decreased by 1.1 percent due to an increment in economic policy uncertainty. According to Business media, there was a wave of 1 percent in gross domestic product (GDP), and 1 million employees were sacked during the year 2011 to 2012 after a huge positive economic policy uncertainty shock in the USA [6]. The economies where economic policy uncertainty exists change their behaviors and decisions dynamically.

Hofstede [7] defined the term “culture” as the collectively programming of the human mind that separates the masses of one country, group, or region from the other countries, regions, or groups. He also debates that anyone can demonstrate the culture of a state by following six cultural dimensions. However, this study has taken uncertainty avoidance as a proxy of national culture, which means that having a high uncertainty avoidance culture leads to managers’ risk-averse and non-flexible behaviors. The managers eradicate obscurities before making any decisions and prefer those decisions which have minimum risk. Moreover, in an ardent, contemporary, and vigorous business environment, the purpose of gaining economic efficiency in the firm is not only attached to technical novelty, but it is also associated with national-level factors, i.e., country-level culture. The research has acknowledged the significant impact of EPU on firm financing policy [8,9]. These studies recognized that there exist negative links between EPU and firm financing decisions, but this study encompasses national culture affect for bending risk-averse behavior into risk-friendly behavior. Does culture play a moderating role in enhancing debt financing with high EPU economies? The culture plays a vital contribution in the vigorous planning of business. The numerous tools and techniques of management at the firm level apply according to cultural values which can modify the firm manager’s decision. The valuation of human behavior (which becomes cultural values) differs across borders (countries).

The most familiar debate in finance literature is firm financing decisions despite vast research on the topic. Although there are various finance theories for advocating efficient capital structure, there is no theory which generalizes this trend. The companies have two sources which are used to fulfill their funding needs, i.e., interior, and exterior sources of funding. The interior basis financing comprises of retained earnings or capital reserves. As per the pecking order theory, the firms prefer to use their inside funding first, and if they do not have enough internal funds, then they seek external funding sources. The external funds are further separated into equity and debt sources of financing. The theories of capital structure, i.e., pecking order theory, trade-off theory, and agency cost theory, argue about equity and debt financing. Generally, firms follow financing opportunities according to the pecking order theory, i.e., capital reserve, debt sources of financing, and equity sources of financing. According to Modigliani and Miller’s [10] trade-off theory, the firms prefer more economical fund sources, i.e., high EPU leads to spreading information asymmetry, which creates biases and hence firms prefer debt financing over economical financing. Most of the firms prefer debt financing because it curbs the important information to spread. Moreover, Jensen and Meckling [11] highlighted that agency cost theory is applicable during high EPU, convincing the management towards debt financing as it increases firms’ wealth by mitigating the conflict between managers and shareholders. The managers try to eliminate the agency conflict by adopting debt financing. Thus, Myers and Majluf [12] used pecking order theory, which proclaims that the firms do not focus to use their internal source of financing due to high EPU and which indicates firms to consider debt as source of financing.

This research attempts to reveal the contribution of EPU in firm financing decisions through the channel of national culture. It inspires to record how EPU influences firm financing decisions with the existence of national culture. The earlier studies have confirmed the effect of EPU on firm financing options and have verified from the literature that the change in national culture has an influence on firm financing decisions. In addition, the national culture has direct influence on firm financing decisions due to the attitude of managers. Furthermore, this research pursues to investigate the moderating effect of national culture with EPU and leverage financing by applying 10 years of data (2007–2016). The System Generalized Method of Moments (GMM) was employed with appropriate instruments due to the problem of endogeneity. The outcomes of this research indicate the vigorous influence of EPU on leverage financing through the moderating effect of national culture. The findings further state that the executives should consider the sensitivity of national culture while making financing decisions with high EPU.

More precisely, this research ascribes to enrich empirical literature on both EPU and financing decisions by accumulating the national level culture. A recent study demonstrated how culture played a moderating role with tax evasion, religiosity, and social norms [13]. Another recent study considered financing decisions as a moderating variable with national culture and firm financial performance [3,4,14]. However, no research has been conducted to explore this relationship. There is plenty of literature available on the most used determinants of firm financing decisions. Nevertheless, no research has been found which depicts such arrangement of variables, particularly in those economies where the EPU is high. It highlights new understandings of how EPU affects firm financing decisions via channels of national culture. It covers the prevailing literature on EPU and firm debt financing options to national culture and strengthens the results of prior studies which forecasted the influence of EPU on firm debt financing decisions. Moreover, the research holds empirical and practical implications. The empirical outcomes of the research demonstrate how EPU and UND empirically affect debt financing. This study verifies empirically the appearance of national culture to determine debt financing with high EPU economies. Practically, this study advocates for managers to consider the sensitivity of culture while making debt financing decisions with high EPU economies. This aspect (national culture) is non-financial and non-firm specific.

The rest of the paper is organized as follows. In Section 2, we encompass the theoretical and empirical aspects of the literature and briefly describe the hypotheses development. Section 3 discusses the data, materials, and methodology used and the research framework and econometrics model implemented in our study. Section 4 presents some important results obtain from this study. The Section 5 contains some concluding remarks in outlining the policy implications.

2. Literature Review

This section contains a brief literature review to motivate the problem and build theoretical and historical background regarding EPU. This research aims to link EPU and DF in the presence of national-level culture. During periods of high EPU, corporate firms are unable to acquire debt financing due to default risk faced by the banking sector. They obtain equity financing or internal financing for their businesses; however, national level culture serves as a factor which averts managers toward debt financing. The managers prefer leverage financing because of their rigidness and cultural traits [15]. Let us begin to understand the linkage between EPU and DF by reviewing the literature in the following subsections.

2.1. Economic Policy Uncertainty and Firm Debt Financing Decision

An enormous literature exists which deliberates an inter-relationship between EPU and financing options [8,9,16]. These studies concentrated on the ups and downs of EPU and examined the influence of EPU on firm financing decisions. More explicitly, the upshots of earlier studies quantified that corporations employ more conservative strategy in high EPU economies due to high cost of borrowing [17,18,19]. Consequently, the corporations spend not as much on capital [20]. The EPU negatively influenced firm level financing [8]. An increment in EPU means that the firms hardly choose debt financing options, which states a negative relationship between EPU and leverage financing [15]. Recently, alternative debt financing via Sukuk (Islamic Bond) has offered ownership in tangible assets to investors. For example, Alam, Bhatti, and Wong [21] showed that Sukuk are not riskier than conventional bonds, whereas [22] demonstrated Sukuk as an instrument for raising funds. Balli, Ghassan, and Al Jeefri [23] addressed the issue of Sukuk and bond spreads, while Uluyol [24] reviewed the current literature on the subject. This research explicates that the data of rivalry movements and political climate should be considered while making leverage financing decisions in determining a company’s idyllic capital structure. For economies which are confronting EPU conditions, business entities decide sagaciously regarding their financing decision. Most of the studies have indicated that there is an inverse influence of EPU on firm financing [8,9]. Despite the unfavorable influence of EPU on firm financing, there are some economies (e.g., India, Pakistan) where high EPU exists but business entities prefer more debt for financing [15]. Pástor and Veronesi [25] depicted that high EPU deteriorates the demand for leverage financing. The uncertainties are further alienated into two forms, e.g., macro uncertainties and micro uncertainties. Furthermore, uncertainty negatively influences households’ needs and investment decisions [26]. In addition, EPU affects the entire economy by dropping economic growth [27]. The consumers can postpone some essential and non-essential consumption relatively due to high uncertainty [28]. There is an inverse relation between EPU and financing cost [17,18,19]. The following hypothesis can be assumed by pursuing previous studies’ outcomes:

Hypothesis 1 (H1).

There is a negative relationship between economic policy uncertainty and debt financing decisions.

2.2. National Culture and Firm Debt Financing Decision

The word “culture” has an enduring influence on managers’ planning and choices, which are diverse across borders. The main involvement in finding the notions and understandings of culture was introduced by Hofstede. He also considered the culture of numerous regions and highlighted the various cultural dimensions, which present cultural trends of specific regions. He has covered the different measures of culture at the national level in research, which were organized in different countries [5,7]. Arosa et al. [29] stated that there is a negative affiliation between leverage financing and uncertainty avoidance. The literature has demonstrated that national-level culture may influence the decision of firm financing [30]. A voluminous literature exists which stated the national level culture as an important determinant of various firm-level decisions [31,32]. Similarly, there is an influence of national-level culture on leverage financing, which is proven by the literature. Moreover, according to prior studies, we can hypothesize the H2 hypothesis stated below:

Hypothesis 2 (H2).

There exists a negative and significant link between the national-level culture and firm financing decisions.

2.3. Economic Policy Uncertainty, National Culture, and Firm Debt Financing Decision

Businesses are not concerned about debt for financing due to their risk-averse behavior in high uncertainty economies. In earlier research, researchers and scholars have corroborated that there is a negative link between EPU and financing decisions. The corporate executives pursue risk-adverse notions which lead to harmless financing. Similarly, some high uncertainty economies adopt more risky behaviors and prefer more debt for financing due to their norms and values. Few researchers have also confirmed the contribution of culture on decision making regarding firm-level financing [33,34]. Thus, these researchers are restricted to firm-level cultural negotiations. Additionally, few studies were explored in the literature that described the separate connection of EPU with financing decisions and national-level culture with firm financing decisions. So, this research attempts to fill this gap in the following way: The research is innovative in a way that it takes the national culture as a moderating variable between the EPU and firm financing decisions. To the best of our knowledge, no such study was found in the literature on such relationships, which led us to test the hypothesis H3 below:

Hypothesis 3 (H3).

There exists a positive link between EPU and corporate financing decisions when there is high uncertainty avoidance.

2.4. Firm-Specific, Country-Specific, and Firm Debt Financing

Despite the main explained and explanatory variables, the rest of the variables are known as the control variables, which are encompassed into two further categories, i.e., firm-specific variables and country-specific variables. The firm-specific variables are the tangibility of the total assets, firm size, and sales growth ratio. The enormous firms may obtain debt financing effortlessly, which states that the size of the firm has a positive influence on leverage financing. Similarly, the business which holds more tangible assets may obtain debt easily due to less stringent covenant problems and by using assets as loan collateral, which also highlights that the tangibility of the total assets has a positive link with debt financing. Moreover, sales growth interacts negatively with leverage source of financing because debt hoists volatility and firms feel hesitation in growth [3,14,35,36,37,38]. On the other side, the country-level variables are as follows: inflation rate, interest rate, and financial sector development. Moreover, the minimum rate of interest tends to make it easier for business corporations to acquire external finance, which demonstrates a negative link between interest rate and leverage. An upsurge in the inflation rate leads to an increment in interest rate, which discourages external financing due to the high interest rate. Booth et al. [30] suggested that there is negative and significant association between inflation and external financing. The financial sector development leads to the improved obtainability of more funds for businesses in any country at the minimum debt financing cost, which shows that the financial sector development has a positive relationship with leverage financing [30,39].

2.5. Research Framework

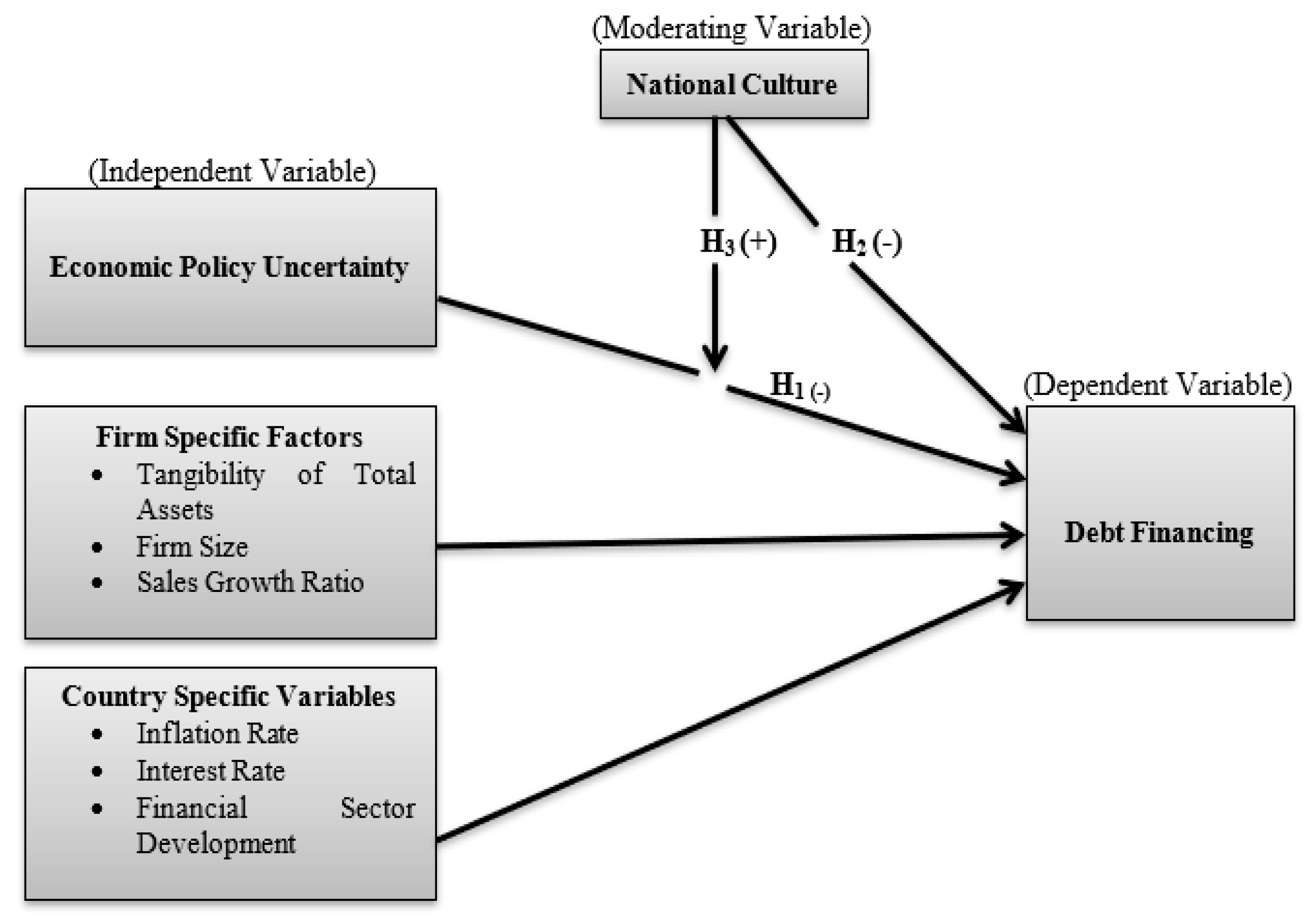

Figure 1 exposes the relationships of the variables. The variable displayed on right side (debt financing) is called the dependent variable, which is influenced by the left-hand-side variables, i.e., EPU (independent variable), firm-specific variables (tangibility, firm size, sales growth ratio), and country-specific variables (interest rate, inflation rate, financial sector development). The variable which is displayed in the center is known as the moderating variable (national culture).

3. Material and Methods

3.1. Description of Data

The data of non-financial firms were obtained from [Thomson Reuters DataStream] and Financial Statements. The official data site which is titled as “Hofstede Insight” helped to acquire data of Hofstede cultural dimensions. The data regarding different macroeconomic variables were obtained from the World Development Indicators (WDI) maintained by The World Bank (https://data.worldbank.org/topic/economy-and-growth accessed on 3 October 2021). The economies were opted by using technique of random sampling with total population 5722, but sample size comprises 3831 non-financial firms of 6 Asian economies, i.e., Pakistan, India, Singapore, China, South Korea, and Japan, which start from 2007 to 2016. We deleted the financial sector firms which are under the SIC code 6000–6999. The missing data for five or more than five years were deleted from the sample. These economies provide clear validation of how culture affects firms’ financing decisions in economies of the same region. The chosen economies are a mixture of developed and developing economies. It also discloses that neighboring economies’ culture has not that much difference. Culture significantly articulates cross-country difference in financing decision [40].

3.2. Variable Specification

In this research, leverage financing is considered as an explained variable, which is denoted as total debt divided by total assets [8,9,14]. The leverage financing is linked with trade-offs between benefit and costs. This financing is relaxed to the businesses from tax, which leads to encouraging them. An accomplishment of debt level is an alarming situation for any business entity because it increases the obligations of the business in this competitive environment. Similarly, the explanatory variable, which is known as the EPU, is measured by taking the natural log of EPU index. This EPU index consists of uncertainty from policy, news, market, and economic indicators [8,41]. The corporate firms have an astigmatic approach during high uncertainty, and thus they move themselves towards the comfort zone by minimizing economic activities. Moreover, the moderating variable, which is called national culture, is indicated with the help of six dimensions as declared and defined by Hofstede [7]. The rigid culture forces managers to take critical decisions, but good cultural values augment the businesses sustainability. Furthermore, tangibility of total assets is used as a firm-specific variable, which is measured as total fixed assets divided by total assets. The other firm-specific variable is firm size, which is calculated as log of total sales. The sales growth ratio is also taken as control variable and is measured as current year sales minus last year sales divided by last year sales [14,35,36,37,38]. The rest of the variables are country-specific variables, which are called macroeconomic variables. The inflation is calculated by consumer price index, whereas interest rate is measured as annual real interest rate and financial sector development is measured with aggregate of systematic measurement by IMF [30,39]. Moreover, the following previous studies have employed the GMM mode [15,42,43]. Table 1 is as follows:

3.3. Econometric Model

In Equation (1), above is for explained variables (debt financing), MV is moderating variable, is for firm-specific variables, and represents the countr-specific variables. Furthermore, the subscript “i” denotes firm change, whereas “t” is the time change and “j” represents country change. Similarly, DF in Equation (2) below is expressed as:

This Equation (2) expresses the relationship of EPU with DF in the presence of firm-specific and country-specific variables.

Similarly, DF depends on UND and is given in Equation (3), which highlights the connection between UND and the DF. Moreover, Equation (4) below DF is expressed as a function of UND, EPU, SGR, FS, FSD, IFR, and NC:

Note that Equation (4) above introduces the interaction term of UND in the shape of moderating variables, which means that the EPU has significant role on DF in the presence of UND. Moreover, the DF stands for debt financing and EPU is for economic policy uncertainty. Similarly, the TT is tangibility of total assets and FS is firm size. The SGR shows sales growth ratio and IFR represents inflation rate. In the same way, IR is interest rate and FSD is financial sector development. Thus, NC is abbreviation of national culture and UND expresses uncertainty avoidance.

3.4. Methodological Discussion

This research used different methodologies and tests. The econometric model comprises country-specific variables (macroeconomic variables). Thus, there may be probabilities that the data are stationary or not. To find out the stationarity of data, we practiced unit root test. The outcomes of Augmented Dickey–Fuller test stated that the data are stationary.

According to Table 2, the Augmented Dickey–Fuller test signifies that the alternate hypothesis is accepted, which is verified by its probability values (p < 0.5). After identification of data stationarity, we moved towards endogeneity, which builds the assumption that macro variables are endogenous with error terms or not. To identify this problem, we have applied a Wald test, which expresses the presence of endogeneity.

In Table 3, the probability values of restriction terms have portrayed the presence of endogeneity. There are number of techniques which deal with the problem of endogeneity. However, this study has used System GMM to resolve the issue of endogeneity because the data are panel and GMM is an appropriate methodology for panel data. The fitness of model relies upon nature of data. In this research, System Generalized Method of Moments has practiced for regression estimation purpose, which is developed by Griliches and Hausman [46]. This research comprises panel data, which encompassed both time series and cross-section data and confronted the endogeneity problem which authenticates the applicability of the GMM method. In finance and economics literature, most of the independent variables are not perfectly exogenous, which hoists the problem of endogeneity. Therefore, to sort this problem out, the generalized method of moments is compulsory with its appropriate tools and instruments [47]. The thing which verifies the implication of GMM is that the dependent variable should depend upon its own lag. We have functioned GMM model with 1st rank instrument, which revealed the problem of endogeneity. The p value of J-stat is insignificant, which shows the acceptability of the alternate hypothesis.

4. Results and Findings

This section demonstrates the findings of the current study on how economic policy uncertainty determines the choice of debt source financing in the presence of national culture. This is performed by computing descriptive statistics for all the variable, which are shown in Table 4 below.

Table 4 represents the overall reactions of respondent firms in the shape of mean, median, and standard deviation. The leverage ratio has 0.283 as its mean value, which articulates that firms have 28.3 percent debt financing in their capital structure. The digit 0.271 states the median value of the leverage ratio, which is closer to the mean value and reveals the debt financing behavior of firms. Moreover, the standard deviation of LR is 0.174, which shows the level of scattering from its mean value. The skewness and kurtosis have values of 0.381 and 2.508, respectively, which verify the normality of data. Furthermore, the economic policy uncertainty has 129.0 as its mean value and 127.9 as its median value. The EPU has 0.047 as its standard deviation value, which shows the dispersion of data from its mean value. Furthermore, the skewness has a value of 0.378 and kurtosis has a value of 12.22, and these show that the data are stationary at normal. The mean, median, and standard deviation values of the firm-specific variables exhibit the responses of firms in their firm-specific form. The 2.487 percent is the average interest rate of the mentioned countries. Similarly, an average inflation rate is 2.745 percent, which is normal. The financial sector development has 0.696 as its mean value, which shows that the mentioned countries are advanced because, according to the IMF, economies having more than 0.60 FSD statistics are considered as developed. The next section is about the correlation analysis.

The results of the correlation analysis among the variables are given in Table 5. The statics’ values corroborate the degree of association among variables. The EPU has positively correlated with the leverage ratio, but UND has a negative correlation with the LR. Similarly, the tangibility and sales growth ratios are positively correlated with the leverage ratio because when the asset tangibility and sales growth ratio enhance, the firms increase the debt ratio. Moreover, the firm size has negatively correlated with leverage ratio because when managers expand their businesses, they obtain financial stability and have enough funds to use. The interest rate and inflation rate are positive correlated with leverage ratio which means that they both are moving in same direction with debt financing. However, financial sector development is negatively correlated with the LR, which also reveals an inverse relation with the LR. The values of the VIF imply that there is no multicollinearity in the data as the values are less than 10 (benchmark is 10).

Table 6 signifies the outcomes of the regression model, which replies to the research query of how EPU effects debt financing. The economic policy uncertainty has −0.009 as its coefficient value, which describes that EPU has a negative and significant link with leverage financing, which also means that the businesses will not prefer debt financing with high uncertainty. Additionally, firms minimize their business activities which will mitigate funds need. Therefore, the probabilities of default debts increase, which forces financial institutions and banks to upsurge their rate of interest. Moreover, tangibility has 0.357 as its coefficient value, which shows a positive relation with debt financing, which also defines that more tangible assets can be used as loan collateral to obtain the debt easily. Similarly, firm size also has a positive coefficient value (0.083), which shows that larger firms are more stable firms, and they may acquire debt for their financing needs. The sales growth ratio has negative coefficient value (−0.013), which means that the debt increases volatility and risk of the firm which will stop risk averse firms from debt financing, and they feel hesitation in growth [14,36]. The country-specific variables, i.e., interest rate, has a negative and significant coefficient value (−0.001), which means that there is an inverse relationship between EPU and debt financing because, in high uncertainty economies, the banks and other financial institutions increase their interest rate and the rational managers do not prefer to take debt for financing. Similarly, inflation rate also has an inverse relationship with debt financing, which means that an increment in inflation rate leads to an increase in interest rate, which will expel finance managers in complexities regarding their debt financing. Moreover, the financial sector development has a positive and significant link with debt financing because the businesses in developed economies may obtain the debt on the minimum rate, and they prefer debt for financing.

The adjusted R-square value is 0.559, which represents the degree of cohesiveness with economic policy uncertainty. It also means that the independent variables explain 55.9 percent dependent variable. The value of the standard error is 0.115, which shows responses of contributed firms are just 11.5 from the actual line of regression. The probability value of the J-statistic is 0.165, which is insignificant and shows the valid instruments of GMM.

Table 7 represents the outcomes of the regression analysis, which reply to the research question of how uncertainty avoidance influences debt financing. The coefficient value of the uncertainty avoidance is −0.007, which is less than 0.05 and shows that the uncertainty avoidance has a significant but negative impact on debt. It means that there is an inverse relationship between the uncertainty avoidance and debt financing, which expresses that high uncertainty leads to the pessimistic behavior of corporate managers about debt financing. Furthermore, when firm managers find substitutes and safe ways to finance their businesses, they show an offensive attitude for leverage financing. The rest of the variables, including firm-specific and country-specific variables, are the same relationship as the Table 6 results. Moreover, the adjusted R-square is 12.9, which is low because the uncertainty avoidance is a non-financial nature of variable.

Table 8 portrays the results of the regression analysis. The EPU has a positive and significant impact on debt financing due to an interaction term in the form of uncertainty avoidance. In addition, the rigid behavior of corporate managers’ expelling them to consider culture importance, which leads to an optimistic behavior towards debt financing. It transforms their risk-adverse behavior into risk-friendly behavior. The norms and values insist that they think optimistically about debt despite high economic policy uncertainty. The other variables, i.e., firm-specific and country-specific variables, have a similar relationship as the Table 6 and Table 7 results. Furthermore, the value of the adjusted R-square is 0.726, whereas the value of the standard error is 0.052. The p value of the J-stat is 0.173 (see Table 9). Briefly, the study summarizes that there is a significant effect of EPU and UND on debt financing, and it also authenticates the presence of uncertainty avoidance to determine leverage financing in high EPU economies.

We have checked the robustness by using the system GMM model with another proxy of national-level culture (Indulgence) and obtained sustainable outcomes as mentioned in the previous Table 8. All our outcomes are reliable to a series of robustness checks and offer useful information.

5. Concluding Remarks

This study examines the influence of economic policy uncertainty on debt financing in the presence of national-level culture by using data of non-financial firms from six Asian economies (Pakistan, India, Singapore, China, South Korea, and Japan) from the period of 2007 to 2016. Considering the potential endogeneity problem, we used the generalized method of moments. The overall findings validated the first hypothesis that the economic policy uncertainty negatively drives the corporate debt financing in our sample because uncertainty creates an anonymous situation for the industries to equip capital structure with debt. Similarly, the uncertainty avoidance has an inverse relationship with debt financing due to the pessimistic and risk-averse approach of corporate managers regarding debt financing. Interestingly, we find that national culture positively moderates the negative impact of economic policy uncertainty on debt financing because managers demonstrate rigidity to preserve the culture while opting for debt as a financing source. It implies that the national culture converts risk-averse behavior into risk-tolerant behavior. Moreover, the findings of this study signify that economic policy uncertainty has a significant impact on debt financing via the channel of uncertainty avoidance (national culture).

5.1. Implications

This study offers some empirical and practical implications, which are as follows:

- The empirical findings show that economic policy uncertainty and uncertainty avoidance affect debt financing. It authenticates the importance of national culture in diffusing the negative impact of high economic policy uncertainty in financing decisions may not be overlooked in selected Asian economies. It also participates in the literature.

- This research practically guides corporate managers by considering the sensitivity of uncertainty avoidance while deliberating about leverage financing with high economic policy uncertainty economies. This aspect (national culture) is non-financial and non-firm specific.

5.2. Limitations and Future Research

- The current study has not reflected all Asian economies due to data constraints.

- It is time-consuming to consider all the variables that determine debt financing.

- This study can be extended by considering primary and secondary sources of financing with six dimensions of culture as determinants of financing.

Author Contributions

Conceptualization, B.H.S., U.F., M.I.B. and M.A.K.; methodology, B.H.S., U.F. and M.I.B.; formal analysis, B.H.S., U.F., M.I.B. and M.A.K.; original draft preparati, B.H.S., U.F., M.I.B. and M.A.K.; review and editing, M.I.B.; supervision, M.I.B. and M.A.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

We are thankful to handling editor, four anonymous referees for excellent comments which improved the article in its present form. We take all the responsivities of any error.

Conflicts of Interest

All the contributing authors declare no conflict of interest.

References

- Phan, D.; Iyke, B.N.; Sharma, S.S.; Affandi, Y. Economic policy uncertainty and financial stability—Is there a relation? Econ. Model. 2020, 94, 1018–1029. [Google Scholar] [CrossRef]

- Ashraf, B.N.; Shen, Y. Economic policy uncertainty and banks’ loan pricing. J. Financ. Stab. 2019, 44, 100695. [Google Scholar] [CrossRef]

- Xu, S.; Qamruzzaman, M.; Adow, A.H. Is Financial Innovation Bestowed or a Curse for Economic Sustainably: The Mediating Role of Economic Policy Uncertainty. Sustainability 2021, 13, 2391. [Google Scholar] [CrossRef]

- Guedhami, O.; Mansi, S.; Reeb, D.; Yasuda, Y. Economic policy uncertainty and allocative distortions. J. Financ. Stab. 2021, 56, 100923. [Google Scholar] [CrossRef]

- Hofstede, G. Cultural dimensions in management and planning. Asia Pac. J. Manag. 1984, 1, 81–99. [Google Scholar] [CrossRef]

- McNabb, B. Uncertainty is the Enemy of Recovery; Wall Street Journal: New York, NY, USA, 2013. [Google Scholar]

- Hofstede, G. Culture’s Consequences: Comparing Values, Behaviours, Institutions and Organizations Across Nation, 2nd ed.; Sage Publication: Thousand Oaks, CA, USA, 2001. [Google Scholar]

- Xiao, S.-Y.; Lee, C.-C. Does Economic Policy Uncertainty Affect Firm-Level Financing in China? Atlantis Press: Hohhot, China, 2018; pp. 183–186. [Google Scholar] [CrossRef] [Green Version]

- Liu, G.; Zhang, C. Economic policy uncertainty and firms’ investment and financing decisions in China. China Econ. Rev. 2019, 63, 101279. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H. Corporate income taxes and the cost of capital: A correction. Am. Econ. Rev. 1963, 53, 433–443. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Myers, S.; Majluf, N. Corporate Financing and Investment Decisions When Firms Have Information That Investors Do Not Have. J. Financ. Econ. 1984, 13, 187–222. [Google Scholar] [CrossRef] [Green Version]

- Sutrisno, T.; Dularif, M. National culture as a moderator between social norms, religiosity, and tax evasion: Meta-analysis study. Cogent Bus. Manag. 2020, 7, 1–20. [Google Scholar]

- Farooq UAhmed, J.; Ashfaq, K.; Hassan Khan, G.U.; Khan, S. National culture and firm financial performance: A mediating role of firm financing decision. Cogent Bus. Manag. 2020, 7, 1–21. [Google Scholar]

- Makololo, P.; Seetharam, Y. The effect of economic policy uncertainty and herding on leverage: An examination of the BRICS countries. Cogent Econ. Financ. 2020, 8, 1–21. [Google Scholar] [CrossRef]

- Al-Thaqeb, S.A.; Algharabali, B.G. Economic policy uncertainty: A literature review. J. Econ. Asymmetries 2019, 20, e00133. [Google Scholar] [CrossRef]

- Çolak, G.; Durnev, A.; Qian, Y. Political Uncertainty and IPO Activity: Evidence from U.S. Gubernatorial Elections. J. Financ. Quant. Anal. 2017, 52, 2523–2564. [Google Scholar] [CrossRef] [Green Version]

- Jens, C.E. Political uncertainty and investment: Causal evidence from U.S. gubernatorial elections. J. Financ. Econ. 2017, 124, 563–579. [Google Scholar] [CrossRef] [Green Version]

- Kelly, B.; Pástor, Ľ.; Veronesi, P. The Price of Political Uncertainty: Theory and Evidence from the Option Market. J. Financ. 2016, 71, 2417–2480. [Google Scholar] [CrossRef]

- Gulen, H.; Ion, M. Policy Uncertainty and Corporate Investment. Rev. Financ. Stud. 2015, 29, 523–564. [Google Scholar] [CrossRef]

- Alam, N.; Bhatti, M.; Wong, J.T. Assessing Sukuk defaults using value-at-risk techniques. Manag. Financ. 2018, 44, 665–687. [Google Scholar] [CrossRef]

- Khawaja, M.; Bhatti, M.I.; Ashraf, D. Ownership and control in a double decision framework for raising capital. Emerg. Mark. Rev. 2019, 41, 100657. [Google Scholar] [CrossRef]

- Balli, F.; Ghassan, H.; Al Jeefri, E.H. Sukuk and bond spreads. J. Econ. Financ. 2021, 45, 529–543. [Google Scholar] [CrossRef]

- Uluyol, B. A comprehensive empirical and theoretical literature survey of Islamic bonds (sukuk). J. Sustain. Financ. Invest. 2021, 1–23. [Google Scholar] [CrossRef]

- Pástor, Ľ.; Veronesi, P. Political uncertainty, and risk premia. J. Financ. Econ. 2013, 110, 520–545. [Google Scholar] [CrossRef] [Green Version]

- Bernanke, B.S. Irreversibility, uncertainty, and cyclical investment. Q. J. Econ. 1983, 98, 85–106. [Google Scholar] [CrossRef]

- Bloom, N. The Impact of Uncertainty Shocks. Econometrica 2009, 77, 623–685. [Google Scholar] [CrossRef] [Green Version]

- Eberly, J.C. Adjustment of Consumers’ Durables Stocks: Evidence from Automobile Purchases. J. Politi-Econ. 1994, 102, 403–436. [Google Scholar] [CrossRef]

- Arosa, C.M.V.; Richie, N.; Schuhmann, P.W. The impact of culture on market timing in capital structure choices. Res. Int. Bus. Financ. 2014, 31, 178–192. [Google Scholar] [CrossRef]

- Booth, L.; Aivazian, V.; Kunt, A.D.; Maksimovic, V. Capital structures in developing countries. J. Financ. 2001, 56, 87–130. [Google Scholar] [CrossRef]

- Haq, M.; Hu, D.; Faff, R.; Pathan, S. New evidence on national culture and bank capital structure. Pac. -Basin Financ. J. 2018, 50, 41–64. [Google Scholar] [CrossRef] [Green Version]

- Shao, L.; Kwok, C.C.; Guedhami, O. National culture and dividend policy. J. Int. Bus. Stud. 2010, 41, 1391–1414. [Google Scholar] [CrossRef]

- Karim, S.; Qameuzzaman, M.D. Corporate culture, management commitment, and HRM effect on operation performance: The mediating role of just-in-time. Cogent Bus. Manag. 2020, 7, 1–27. [Google Scholar] [CrossRef]

- Srisathan, W.A.; Ketkaew, C.; Naruetharadhol, P. The intervention of organizational sustainability in the effect of organizational culture on open innovation performance: A case of thai and chinese SMEs. Cogent Bus. Manag. 2020, 7, 1717408. [Google Scholar] [CrossRef]

- de Jong, A.; Kabir, R.; Nguyen, T.T. Capital structure around the world: The roles of firm- and country-specific determinants. J. Bank. Financ. 2008, 32, 1954–1969. [Google Scholar] [CrossRef] [Green Version]

- Petrunia, R.J.; Huynh, K.P. Age effects, leverage, and firm growth. J. Econ. Dyn. Control. 2020, 34, 1003–1013. [Google Scholar]

- Salim, M.; Yadav, R. Capital Structure and Firm Performance: Evidence from Malaysian Listed Companies. Procedia-Soc. Behav. Sci. 2012, 65, 156–166. [Google Scholar] [CrossRef] [Green Version]

- Vy, L.T.P.; Nguyet, P.T.B. Capital structure and firm performance: Empirical evidence from a small transition country. Res. Int. Bus. Financ. 2017, 42, 710–726. [Google Scholar]

- Farooq, U.; Ahmed, J.; Khan, S. Do the macroeconomic factors influence the firm’s investment decisions? A gener-alized method of moments (GMM) approach. Int. J. Financ. Econ. 2021, 26, 790–801. [Google Scholar] [CrossRef]

- Khan, M.A.; Gu, L.; Meyer, N. The effects of national culture on financial sector development: Evidence from emerging and developing economies. Borsa Istanb. Rev. 2021. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring Economic Policy Uncertainty*. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Al-Malkawi HA, N.; Bhatti, M.I. Are tests of dividend policy robust to estimation techniques: The case of an emerging economy? Phys. A Stat. Mech. Its Appl. 2020, 541, 123216. [Google Scholar] [CrossRef]

- Iqbal, U.; Gan, C.; Nadeem, M. Economic policy uncertainty and firm performance. Appl. Econ. Lett. 2019, 27, 765–770. [Google Scholar] [CrossRef]

- Suyuan, W.L.; Khurshid, A. The effect of interest rate on investment; empirical evidence of Jiangsu Province, China. J. Int. Stud. 2015, 8, 81–90. [Google Scholar] [CrossRef] [PubMed]

- Castro, F.; Kalatzis, A.E.; Filho, C.M. Financing in an emerging economy: Does financial development or financial structure matter? Emerg. Mark. Rev. 2015, 23, 98–123. [Google Scholar] [CrossRef]

- Griliches, Z.; Hausman, J.A. Errors in variables in panel data. J. Econ. 1986, 31, 93–118. [Google Scholar] [CrossRef] [Green Version]

- Akhtar, M.R.; Anwar, M.M. Do peer firms impact corporate investment policies? Pak. J. Commer. Soc. Sci. 2018, 12, 363–378. [Google Scholar]

Figure 1.

Theoretical Framework.

{kind=link}

Table 1.

Abbreviations and variables’ details.

| Sr. No. | Variables | Used As | Definition | Measurement | References |

|---|---|---|---|---|---|

| 1 | DF | DV | Debt Financing | Debt to asset ratio = total debt/total assets | [8,14] |

| 2 | TT | CV (Firm-specific) | Tangibility of Total Assets | Fixed assets/total assets | [14] |

| 3 | FS | CV (Firm-specific) | Firm Size | Log of sales | [37] |

| 4 | SGR | CV (Firm-specific) | Sales Growth Ratio | C. year sales—L. year sales/last year sale | [36] |

| 5 | IFR | CV (Country-specific) | Inflation Rate | Consumer price index | [39] |

| 6 | IR | CV (Country-specific) | Interest Rate | Annual real interest rate | [44] |

| 7 | FSD | CV (Country-specific) | Financial Sector Development | Aggregate of systematic measurement by IMF | [45] |

| 8 | EPU | IV | Economic Policy Uncertainty | Natural log of EPU index, amassed based on news by Baker | [8,41] |

| 9 | NC | MV | National Culture | Hofstede Insights | [7] |

Note: This table portrays the detail of variables, acronyms, and relevant calculations obtained from the mentioned studies.

Table 2.

Panel unit root test.

| Method | Statistic | Prob. |

|---|---|---|

| Levin, Lin, and Chu t | −59.069 | 0.000 *** |

| Im, Pesaran, and Shin W-stat | −7.393 | 0.000 *** |

| ADF—Fisher Chi-square | 8978.61 | 0.000 *** |

| PP—Fisher Chi-square | 1087.3 | 0.000 *** |

Note: The asymptotic assumption of unit root test shows that the data are stationary at normal. *** significance at 1% level.

Table 3.

Wald test results.

| Test Statistic | Value | Df | Probability |

|---|---|---|---|

| Panel Estimation | |||

| F-statistic | 55.927 | (9, 29280) | 0.000 |

| Chi-square | 50.351 | 9 | 0.000 |

| Individual Estimation | |||

| Normalized Restriction (=0) | Probability | Std. Err. | |

| C(1) | 0.011 *** | 0.039 | |

| C(2) | −0.033 *** | 0.002 | |

| C(3) | −0.010 *** | 0.006 | |

| C(4) | 0.081 *** | 0.047 | |

| C(5) | −0.039 *** | 0.026 | |

| C(6) | 0.093 ** | 0.007 | |

| C(7) | 0.042 *** | 0.018 | |

| C(8) | −0.055 *** | 0.006 | |

| C(9) | −0.012 *** | 0.010 | |

Note: Restrictions are linear in coefficients. ** significance at 5% level; *** significance at 1%.

Table 4.

Descriptive statistics of the chosen variables.

| Mean | Median | Std. Dev. | Skewness | Kurtosis | Range | |

|---|---|---|---|---|---|---|

| LR | 0.283 | 0.271 | 0.174 | 0.381 | 2.508 | 0.899 |

| EPU | 129.0 | 127.9 | 0.047 | 0.378 | 12.22 | 311.9 |

| UND | 67.26 | 85.00 | 0.028 | −0.498 | 1.493 | 84.00 |

| TR | 0.357 | 0.341 | 0.095 | 0.335 | 2.486 | 0.899 |

| FS | 2.517 | 2.472 | 0.075 | 0.338 | 3.265 | 5.660 |

| SGR | 0.062 | 0.042 | 0.222 | 0.457 | 4.581 | 1.834 |

| INF | 2.745 | 1.437 | 0.053 | 1.276 | 4.288 | 21.63 |

| IR | 2.487 | 2.631 | 0.082 | −0.235 | 2.876 | 13.40 |

| FSD | 0.695 | 0.812 | 0.180 | −0.760 | 2.131 | 0.693 |

Abbreviations: LR = leverage ratio, EPU = economic policy uncertainty, UND = uncertainty avoidance, TR = tangibility ratio, FS = firm size, SGR = sales growth ratio, INF = inflation rate, IR = interest rate, FSD = financial sector development.

Table 5.

Cross-correlation among various variables.

| LR | EPU | UND | TR | FS | SGR | INF | IR | FSD | |

|---|---|---|---|---|---|---|---|---|---|

| LR | 1.000 | ||||||||

| EPU | 0.062 | 1.000 | |||||||

| UND | −0.191 | −0.229 | 1.000 | ||||||

| TR | 0.339 | 0.002 | −0.070 | 1.000 | |||||

| FS | −0.041 | 0.111 | 0.159 | −0.063 | 1.000 | ||||

| SGR | 0.003 | 0.024 | −0.149 | −0.002 | 0.053 | 1.000 | |||

| INF | 0.190 | −0.017 | −0.563 | 0.148 | −0.332 | 0.148 | 1.000 | ||

| IR | 0.089 | −0.020 | −0.213 | 0.043 | −0.115 | −0.080 | 0.006 | 1.000 | |

| FSD | −0.214 | −0.029 | 0.790 | −0.151 | 0.286 | −0.151 | −0.796 | −0.247 | 1.000 |

| Multicollinearity Diagnostic Test | |||||||||

| VIF | 6.761 | 7.178 | 4.731 | 9.831 | 4.761 | 8.021 | 5.768 | 8.889 | 4.851 |

Note: The variance inflation factor results have described on the bottom of this correlation table. Abbreviations: LR = leverage ratio, EPU = economic policy uncertainty, UND = uncertainty avoidance, TR = tangibility ratio, FS = firm size, SGR = sales growth ratio, INF = inflation rate, IR = interest rate, FSD = financial sector development, VIF = variance inflation factor.

Table 6.

Effect of economic policy uncertainty on corporate debt financing.

| Variables | Coefficients | Standard Eror | Probability |

|---|---|---|---|

| Explanatory variable | |||

| EPU (Economic Policy Uncertainty) | −0.009 *** | 0.005 | 0.000 |

| Firm-specific variables and macro variables (used as control variables) | |||

| TR (Tangibility Ratio) | 0.357 *** | 0.018 | 0.000 |

| FS (Firm Size) | 0.083 *** | 0.023 | 0.000 |

| SGR (Sales Growth Ratio) | −0.019 *** | 0.028 | 0.477 |

| INF (Inflation Rate) | −0.056 *** | 0.004 | 0.000 |

| IR (Interest Rate) | −0.033 *** | 0.002 | 0.000 |

| FSD (Financial Sector Development) | 0.079 *** | 0.052 | 0.134 |

| Adjusted R-square | 0.559 | ||

| S.E of regression | 0.115 | ||

| Prob. J-stat | 0.165 | ||

Note: *** significance at 1% level; Abbreviations: LR = leverage ratio, EPU = economic policy uncertainty, UND = uncertainty avoidance, TR = tangibility ratio, FS = firm size, SGR = sales growth ratio, INF = inflation rate, IR = interest rate, FSD = financial sector development.

Table 7.

Impact of uncertainty avoidance on corporate debt financing.

| Variables | Coefficients | Standard Error | Probability |

|---|---|---|---|

| Explanatory variable | |||

| UND (Uncertainty Avoidance) | −0.007 *** | 0.061 | 0.000 |

| Firm-specific variables and macro variables (used as control variables) | |||

| TR (Tangibility Ratio) | 0.291 *** | 0.004 | 0.000 |

| FS (Firm Size) | 0.007 *** | 0.001 | 0.000 |

| SGR (Sales Growth Ratio) | −0.013 *** | 0.042 | 0.002 |

| INF (Inflation Rate) | −0.002 *** | 0.008 | 0.007 |

| IR (Interest Rate) | −0.001 *** | 0.001 | 0.293 |

| FSD (Financial Sector Development) | 0.058 *** | 0.017 | 0.000 |

| Adjusted R-square | 0.129 | ||

| S.E of regression | 0.162 | ||

| Prob. J-stat | 0.116 | ||

Note: *** significance at 1% level.

Table 8.

Moderating Effect of EPU and UND on corporate debt financing.

| Variables | Coefficients | Standard Error | Probability |

|---|---|---|---|

| Explanatory variable | |||

| EPU (Economic Policy Uncertainty) | −0.017 *** | 0.002 | 0.000 |

| UND (Uncertainty Avoidance) | −0.057 *** | 0.007 | 0.000 |

| EPU×UND | 0.042 *** | 0.033 | 0.000 |

| Firm-specific variables and macro variables (used as control variables) | |||

| TR (Tangibility Ratio) | 0.248 *** | 0.014 | 0.000 |

| FS (Firm Size) | 0.023 *** | 0.004 | 0.000 |

| SGR (Sales Growth Ratio) | −1.358 *** | 0.210 | 0.000 |

| INF (Inflation Rate) | −0.045 *** | 0.008 | 0.000 |

| IR (Interest Rate) | −0.080 *** | 0.012 | 0.000 |

| FSD (Financial Sector Development) | 1.169 *** | 0.158 | 0.000 |

| Adjusted R-square | 0.726 | ||

| S.E of regression | 0.052 | ||

| Prob. J-stat | 0.173 | ||

Note: *** significance at 1% level.

Table 9.

Checked robustness with another proxy of national culture (Moderating effect of EPU and IDG on corporate debt financing).

Table 9.

Checked robustness with another proxy of national culture (Moderating effect of EPU and IDG on corporate debt financing).

| Variables | Coefficients | Standard Error | Probability |

|---|---|---|---|

| Explanatory variable | |||

| EPU (Economic Policy Uncertainty) | −0.000 *** | 0.000 | 0.000 |

| IDG (Indulgence) | −0.007 *** | 0.001 | 0.002 |

| EPU×IDG | 0.003 *** | 0.012 | 0.000 |

| Firm-specific variables and macro variables (used as control variables) | |||

| TR (Tangibility Ratio) | 0.289 *** | 0.012 | 0.000 |

| FS (Firm Size) | 0.005 *** | 0.003 | 0.005 |

| SGR (Sales Growth Ratio) | −1.086 *** | 0.022 | 0.000 |

| INF (Inflation Rate) | −0.001 *** | 0.001 | 0.000 |

| IR (Interest Rate) | −0.000 *** | 0.000 | 0.000 |

| FSD (Financial Sector Development) | 1.045 *** | 0.024 | 0.000 |

| Adjusted R-square | 0.726 | ||

| S.E of regression | 0.052 | ||

| Prob. J-stat | 0.173 | ||

Note: *** significance at 1% level.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Subhani, B.H.; Farooq, U.; Bhatti, M.I.; Khan, M.A. Economic Policy Uncertainty, National Culture, and Corporate Debt Financing. Sustainability 2021, 13, 11179. https://doi.org/10.3390/su132011179

AMA Style

Subhani BH, Farooq U, Bhatti MI, Khan MA. Economic Policy Uncertainty, National Culture, and Corporate Debt Financing. Sustainability. 2021; 13(20):11179. https://doi.org/10.3390/su132011179

Chicago/Turabian StyleSubhani, Bilal Haider, Umar Farooq, M. Ishaq Bhatti, and Muhammad Asif Khan. 2021. "Economic Policy Uncertainty, National Culture, and Corporate Debt Financing" Sustainability 13, no. 20: 11179. https://doi.org/10.3390/su132011179

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.