Managing Multiple Logics: The Role of Performance Measurement Systems in Social Enterprises

1

Department of Business and Economics University of Southern Denmark, Universitetsparken 1, 6000 Kolding, Denmark

2

Institute of Finance and Accounting, Leuphana University, Universitätsallee 1, 21335 Lüneburg, Germany

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(8), 2327; https://doi.org/10.3390/su11082327

Submission received: 8 March 2019

/

Revised: 7 April 2019

/

Accepted: 8 April 2019

/

Published: 18 April 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:This systematic literature review explores the role of performance measurement systems (PMSs) in managing multiple logics in social enterprises. Social enterprises are hybrid organizations that simultaneously pursue a social mission (social logic) and financial sustainability (commercial logic). Satisfying multiple logics often leads to tensions, which are addressed and managed through PMSs. For this, we conduct a systematic literature review to derive our conclusions. PMSs in social enterprises may assume the roles of mediator, disrupter and symbolizer. The PMS works as a mediator in combination with sincere stakeholder involvement when both logics are represented in the PMS. If a PMS represents only one logic, it increases tensions and the PMS becomes a disrupter. When the PMS is used to enhance legitimacy, the PMS assumes the role of a symbolizer. In particular, we find that PMSs are most useful for monitoring performance and enhancing legitimacy. The role of PMSs in decision-making is limited due to difficulties of integrating social and commercial logics into a single PMS. Several factors—such as decision-makers’ influence—further shape the role of PMSs.

1. Introduction

1.1. Problem Statement

Hybrid organizations blur the boundaries between the private, public and non-profit sectors [1]. Hybrid organizations incorporate elements from different institutional logics and are by nature exposed to contradictions [2,3]. Social enterprises, whose objectives are to achieve a social mission (social logic) through commercial activities (commercial logic), are a prime example of a hybrid organization [1,3]. Social enterprises must therefore manage a range of diverse activities, objectives and stakeholder expectations simultaneously [3,4,5]. Over recent decades, social enterprise as a distinct form of organization has received increasing attention from researchers [1,6,7]. Early research on social enterprises emphasizes the advantage of funding social activities by generating income from commercial activities and defining and characterizing the concepts of social enterprise and social entrepreneurship [8,9,10,11,12,13].

Recent studies focus on the tensions that arise due to the hybrid nature of social enterprises [1]. Tensions arise as a result of contradictions relating to performing, organizing, belonging and learning [14]. If tensions are not managed carefully, social enterprises may become too focused on one logic and lose their hybridity [1,8,15,16,17,18,19]. Different corporate governance systems influence how organizations manage these tensions, such as market competition [20], CEO tournaments [21] and incentives [22]. The literature emphasizes the importance of, but also the challenge caused by, measuring performance in social enterprises [15,16,23]. Performance measurement systems (PMSs) are important for monitoring performance, strategic decision-making, attention focusing and legitimacy [24]. A new strand of literature emphasizes the important role of PMSs in compensation [25]. In social enterprises, multiple logics cause conflicting objectives and demands that complicate performance measurement and result in performing tensions [14]. Performing tensions emerge due to difficulties of agreeing on objectives and performance measurement. Difficulties of representing both social and commercial logics because of different evaluation principles therefore increase performing tensions [14]. Measuring social performance often involves qualitative, ambiguous and non-standardized evaluation principles, whereas commercial performance is measured according to specific, quantitative and standardized indicators [14]. A recently emerged strand of literature develops relative performance evaluation, which is also interesting in relation to compensation of management and thereby management’s initiatives for focusing on both social and commercial performance [26]. Relative performance evaluation may be a fundamentally new way of measuring performance and is especially suitable for improving the way in which social enterprises measure social performance.

Performing tensions in social enterprises correlate with a lack of appropriate PMSs, which creates problems for managing logics. A lack of appropriate PMSs can lead to mission drift (viz., the commercial logic overriding the social logic), loss of legitimacy and difficulties of meeting the stakeholders’ demands for transparency [15,27,28]. Even though the literature acknowledges the importance of PMSs, it is still not clear whether and, if so, how PMSs influence performing tensions and contribute to managing logics in a hybrid context [1,15,16,17,29]. This leads to the following research question: What is the role of performance measurement systems (PMSs) for managing multiple logics in social enterprises?

1.2. Literature Review

To address this question, we conduct a systematic literature review, which synthesizes the extant body of knowledge and develops suggestions that future research may use to contribute to this topic. We review 64 journals, ranked levels 3–4* in the 2015 Association of Business Schools (ABS) Academic Journal Guide. The review identifies 94 articles on hybrid, social enterprises and performance measurement. We focus on 16 articles that are specific enough to cover the posed research question.

Based on the findings, we present three roles of PMSs in social enterprises: the PMS serving as a mediator, disrupter and symbolizer. When a PMS functions as a mediator (positive connotation), it helps to balance different views, values and demands by representing logics. Second, a PMS functioning as a disrupter (negative connotation) constitutes a barrier because of incomplete PMSs that only capture parts of the performance and thereby increase tensions. Third, a PMS in the role of a symbolizer (neutral connotation) has the purpose of enhancing legitimacy. PMSs have different uses, such as monitoring performance or enhancing legitimacy. We find that PMSs have different roles, such as mediating or symbolizing, depending on what the PMS is used for. We state that understanding the role that PMSs play in different uses in social enterprises can lead to an understanding of the conditions under which PMSs help to manage performing tensions and multiple logics. Our first finding is that—under certain conditions—PMSs can function as a mediator that prevents mission drift and re-balances logics. Second, we find that the main use of PMSs is to enhance legitimacy. Third, PMSs assume the role of a disrupter if not both logics are represented in the PMSs. Fourth, several factors influence the role of PMSs. These factors are decision-makers’ influence, situation-specific interdependence, institutional factors, stakeholder interpretation of PMSs and design characteristics of PMSs. Finally, the analysis shows that there is a lack of research on the four different uses of PMSs in social enterprises. The literature mainly analyses the use of PMSs for monitoring and enhancing legitimacy. The body of research on the use of PMSs for strategic decision-making and attention focusing in social enterprises is quite limited.

The literature review makes three novel contributions. First, it improves our understanding of the situations in which PMSs help managers in social enterprises with monitoring, decision making, attention focusing and gaining legitimacy. Second, it provides a systematic examination of factors that influence the use of PMSs (decision-makers’ influence, situation-specific interdependence, institutional factors, stakeholder interpretation of PMSs and design characteristics of PMSs). Third, it identifies several important gaps such as how PMSs mediate decision-making, how and which factors influence the role of PMSs and how corporate governance systems affect PMSs. In addition, we need more research on when and how PMSs is a mediator in managing multiple logics.

In the next subsection, the paper presents the theoretical background with the purpose of developing a framework for the analysis. The second section explains the methodology used in this study and gives a descriptive analysis. The third section synthesizes the findings from the articles. The paper discusses the findings in the fourth section. Finally, the paper makes concluding remarks, gives suggestions for future research, and discusses limitations of the study in the fifth section.

1.3. Theoretical Background

1.3.1. Institutional Logics

Definitions and uses of institutional logics vary in the literature [30]. Thornton and Ocasio [31] (p. 804) define institutional logics as “the socially constructed, historical pattern of material practices, assumptions, values, beliefs and rules by which individuals produce and reproduce their material subsistence, organize time and space and provide meaning to their social reality.” Logics “provide the formal and informal rules of action, interaction and interpretation that guide and constrain decision makers in accomplishing the organization’s tasks and in obtaining social status, credits, penalties and rewards in the process.” Institutional logics can help explain pluralism, complexity and competing demands based on a system of values and beliefs that shape behaviour [31]. Institutional complexity can arise from the coexistence of logics that present varied and incompatible prescriptions leading to uncertainty and conflicts [14,18,30,32]. Logics are important because they explain connections that create a common purpose and unity within the organizational field [33]. Researchers within this field refer to organizations that embed such competing logics within their core features as hybrids [14].

1.3.2. The Social Enterprise as a Distinct Form of Organization

The social enterprise is a subcategory of the hybrid organization [2]. A hybrid organization is defined as having at least two different sectoral paradigms (e.g., public, private or non-profit sector), logics (e.g., social, market or business logic) and value systems (e.g., social impact or profit generation) [1,7]. Hybrid organizations therefore face highly diverse stakeholders as well as multiple and often conflicting objectives [17]. Most organizations may face cumbrous trade-offs between objectives, such as varying demands from strategic and institutional investors. Hybrid organizations differ from other organizations in that multiple logics are an inherent characteristic of hybrid organizations. In a hybrid organization it is important that no single logic dominates [3,34]. Governance systems, such as market competition [20], CEO tournaments [21] and compensation incentives [22] influence how social enterprises manage multiple logics.

The structure of social enterprises is described as an appropriate organizational form to solve social problems in society by combining social and commercial activities [13,35]. Previously, research on social enterprises has mainly focused on three aspects: management based on mission, access to financial resources and mobilization of stakeholder groups [1,8]. However, recent studies emphasize the challenge of managing multiple logics [1,14]. One definition of a social enterprise is “a business with primarily social objectives whose surpluses are principally reinvested for that purpose in the business or in the community, rather than being driven by the need to maximize profit for shareholders and owners” [36] (p. 13). Social enterprises combine elements of a social logic (non-profit sector) and a commercial logic (private sector) in their core business models [1,4]. Private companies are guided by a commercial logic to maximize shareholders’ returns, whereas non-profit organizations are guided by a social logic to generate social benefits [1,4,17,37]. Social enterprises offer goods and services to obtain a financial return (commercial logic). However, the objective is not to maximize shareholders’ profits but to have a financially sustainable business model that generates income for social objectives (social logic). Aligning these logics can lead to ambiguity and create tensions both within the social enterprise and among stakeholders [5,37].

1.3.3. Tensions in Social Enterprises

Smith et al. [14] define four categories of tensions in social enterprises: performing, organizing, belonging and learning tensions. Performing tensions arise from challenges related to PMSs, which makes it natural to focus on performing tensions in the analysis. The analysis will only involve organizing, belonging and learning tensions if findings indicate that PMSs have an influence on these tensions.

Performing tensions arise from the challenge of integrating the objectives of social and commercial logics and evaluating the overall performance of the social enterprise [5,14,38]. One of the main tensions in social enterprises arises from the pursuit of simultaneously being financially sustainable and fulfilling social objectives [1]. This can result in a discussion of whether to invest scarce resources in commercial or social objectives [13]. Measuring performance in social enterprises creates tensions due to the challenges of combining short-term quantitative measures for commercial performance with measures for social performance, which often involves qualitative, ambiguous and non-standardized metrics [39,40]. Performing tensions also arise in the process of gaining legitimacy from diverse stakeholders [6,18]. PMSs should prevent one logic from becoming dominant because it can lead either to financial losses or to mission drift. Mission drift is a situation where the social enterprise becomes too focused on generating income and fulfilling customer demands while neglecting its social objectives [8,28,41,42]. In contrast, social enterprises may face financial losses if they become too focused on their social objectives [28]. However, it is not clear what role PMSs play in managing performing tensions or how they can help to maintain the balance between multiple logics. Fulfilling both social and commercial objectives also creates organizing, belonging and learning tensions due to different cultures, skills and employees within the social enterprise [2].

Organizing tensions arise because of the existence of diverse organizational structures, cultures and practices within the same enterprise. Stakeholders demand different actions from social enterprises, which increases the complexity of appropriate governance structures. Organizing tensions can be reduced by separating activities into sub-units or independent organizations according to their logics [43].

Belonging tensions arise when stakeholders feel attached to different logics and therefore make sense of the social enterprise and its activities differently [44]. Belonging tensions may appear because stakeholders focus on different logics and therefore have different expectations about how objectives should be prioritized. This makes it difficult for decision-makers to prioritize and allocate resources among different objectives [2,15].

Learning tensions emerge from different time horizons, such as short-term financial outcomes and long-term social impact. For example, the short-term objectives of producing and selling goods can conflict with the long-term objectives of changing or benefitting society [14]. Learning tensions also arise from difficulties of determining the appropriate growth and size of the social enterprise [14].

1.3.4. The Use of PMSs

Social enterprises need to measure both social and commercial performance. However, it is often difficult to integrate the two types of performance and define the overall success of the social enterprise [29]. In the short term, financial measures can report on commercial performance. Social performance is more difficult to measure and it takes longer time to see the effects. Furthermore, it is challenging to develop cause-and-effect chains from activities of social value creation [45,46]. Even though many new PMSs that integrate social and commercial performance have been developed in recent decades (e.g., Balanced Scorecard, social return on investment (SROI), triple bottom-line and relative performance evaluation [26,45,47,48]), their usefulness is still limited [29,45,49]. The fact that social enterprises differ as to their organization, structure, funding, social objectives, time perspectives and stakeholders makes it difficult to develop a PMS that is broad enough to capture these diverse characteristics but narrow enough to establish a generally accepted standard [4,14,16,48,50].

Understanding the different uses of PMSs in social enterprises makes it possible to get a deeper understanding of the situations and purposes in which PMSs play a role. Henri [24] proposes four uses of performance measurement systems (PMSs): Monitoring, attention focusing, strategic decision making and legitimacy. Monitoring performance refers to creating an overview of how the social enterprise performs and whether the enterprise achieves its objectives. PMSs have a diagnostic purpose both for internal and external use.

Attention focusing refers to the use of PMSs to align stakeholders with organizational activities and objectives. Senior management can use PMSs to signal priorities and direct attention to critical aspects of performance. Another possibility for attention focusing is to tire the compensation of management to PMSs. Studies have shown that doing so increases the focus on social performance and results in higher social performance [25].

Strategic decision-making refers to the fact that PMSs should create the optimal basis for strategic decisions and, by that, for choosing the best alternatives. Information from PMSs supports management in analytical processes and in analysing cause-effect relations. PMSs improve learning and, therefore, future performance by giving structure and access to information on past performance and predictions of future opportunities.

Legitimacy refers to the justification and validation of current and future performance. PMSs can be used to enhance organizational legitimacy by improving transparency and representing information about performance, which makes it possible for the social enterprise to show the value of activities to stakeholders or underpin claimed value generation. Figure 1 summarizes the analytical framework based on the literature outlined in this section with the purpose of describing and analysing the role of PMSs in managing multiple logics.

2. Material and Method

2.1. Systematic Literature Review

We used a systematic approach to identify relevant articles for the analysis of the role of PMSs in social enterprises [51,52]. In the first step of the literature search, we set the research objectives and in the second step, we defined key theories and terms; see Figure 2. In the third step, we identified relevant journals. Our focus was on the most impactful and highest quality research journals. The search therefore included the highest-rated journals according to the 2015 Association of Business Schools (ABS) Academic Journal Guide. The search was restricted to journals ranked 3–4* and the four research fields: accounting; entrepreneurship and small business management; general management, ethics and social responsibility; and public sector and health care. We selected these research fields because of an interest in combining research in PMSs and social enterprises. Based on these criteria, the review includes 64 journals.

In the fourth step, the search included English-language peer-reviewed academic journal articles containing a combination of the search words social enterprise*, social venture*, social entrepreneurs*, hybrid [1,23] AND accounting, management control system*, performance measurement, reporting, costing, budget*, performance evaluation. The literature search was restricted to looking for keywords in titles, in the lists of keywords and in abstracts. This resulted in 94 articles.

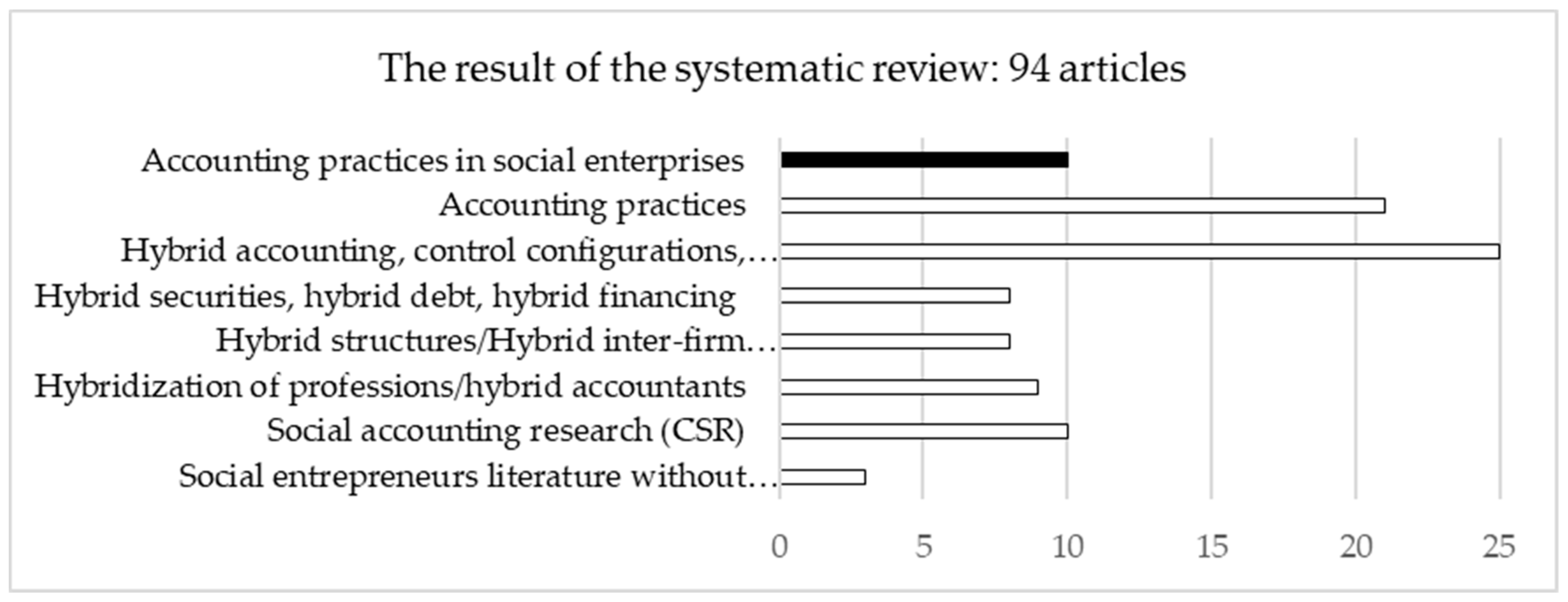

In the fifth step, we read the abstract, title, keywords and introduction of all 94 articles in full. In the remaining sections of the articles, we searched for key terms. We only included empirical articles in the further analysis because the purpose is to understand how PMSs work in practice. This resulted in 10 articles; see Table 1. The remaining 84 articles [53,54,55,56,57,58,59,60,61,62,63,64,65,66,67,68,69,70,71,72,73,74,75,76,77,78,79,80,81,82,83,84,85,86,87,88,89,90,91,92,93,94,95,96,97,98,99,100,101,102,103,104,105,106,107,108,109,110,111,112,113,114,115,116,117,118,119,120,121,122,123,124,125,126,127,128,129,130,131,132,133,134,135,136] do not deal with PMSs in a hybrid context; see Figure 3. Most excluded articles deal with accounting in general or with hybrid practices, hybrid financing, hybrid structures or hybrid professions, which have no value for the analysis of our research question.

Finally, to ensure that we had included all relevant articles published in other fields or lower ranked journals, we went through the reference lists of all 10 studies from the systematic search to identify articles not discovered through the systematic search. Finally, we searched Google Scholar to find articles that cite articles from the literature search. It is our conviction that articles in the field have cited the highly-ranked articles from the search and we therefore included all relevant articles in this last step, even if they are not published by our selected journals. We found six additional published articles that also stem from journals ranked 3–4* in ABS; see Table 1.

2.2. Descriptive Analysis of the Material

This section outlines several characteristics of the sample. First, as Figure 4 shows, most of the articles in the sample are published in accounting journals. It is remarkable that only five articles have been published in other fields than accounting given search terms such as social enterprise and reporting.

Second, it is notable that only two articles were published before 2009 and nearly 40% of all articles were published after 2014; see Figure 5.

Third, as shown in Figure 6, the type of case in the articles varies significantly, which provides advantages but, at the same time, limits comparability.

Fourth, most articles deal with legitimacy. Only three articles focus on strategic decision-making, even though decision-making is a controversial activity in a context of multiple logics. Figure 7 presents an overview of how social enterprises use PMSs.

3. Results: The Four Uses of PMSs

As discussed above, we synthesize the articles based on Henri’s [24] four categories: monitoring, strategic decision-making, attention focusing and legitimacy. The main purpose is to understand which role PMSs play in social enterprises and whether PMSs increase or reduce performing tensions and help manage multiple logics in social enterprises.

3.1. Monitoring

One of the four ways PMSs can be used in organizations is to continuously monitor performance. However, in social enterprises it is more complicated because PMSs must balance between measuring commercial and social performance. In a study of how accounting can facilitate dialogue among stakeholders and integrate different perspectives on how to evaluate performance, PMSs increase performing tensions by creating a productive friction among stakeholders, which was found to be beneficial for the social enterprise [137]. Productive friction refers to an ongoing debate on how to define and evaluate good performance. However, productive friction is only achieved if PMSs integrate different aspects of performance and stakeholders have the chance to discuss and adjust the PMS [137,138]. Based on the findings from the case, Chenhall et al. [137] present three processes that are important in creating productive friction and managing logics. First, it is important to create an acceptance among stakeholders that PMSs are inherently incomplete. However, PMSs still have a mediating role if different evaluative principles are included [137]. Second, it is necessary to make the attributes of accounts (e.g., numbers, indicators and narrative descriptions) visible, so that stakeholders understand how PMSs measure performance so as to challenge and discuss how to measure and integrate performance [137]. Third, the type of responses in situations where tensions increase is important. A productive response is a debate among stakeholders that focuses on the principles of PMSs, whereas debates over the mechanics of PMSs are unproductive and can in some cases lead to “stuckness” [137] (p. 269). In a study of a social enterprise (WISEs), Battilana et al. [139] study factors that influence social performance. They find that an effective approach to improve performance is to separate social and commercial activities but create “spaces of negotiation,” which they define as “arenas of interaction that allow all staff members to discuss and agree on how to handle the daily trade-offs that they face across social and commercial activities” [139] (p. 1660).

Furthermore, PMSs can—by mediating transparency between the social enterprise and its stakeholders—help the social enterprise to stay focused on multiple logics. Busco et al. [34] study a social enterprise that sells technical products on the commercial market and have a social objective of developing new technology. Information from the PMS tells employees which projects (social and commercial) to prioritize. Furthermore, the enterprise shares access to the PMS with its stakeholders. Sharing access to the PMS helps the social enterprise not only to create legitimacy but also to secure a balance between logics because it allows stakeholders to keep track of how the social enterprise performs and prioritizes logics. Furthermore, the case shows that the PMS reduces performing tensions because all projects (social and commercial) are prioritized in the PMS [34]. As a side effect, the study also finds that by having the right indicators for measuring performance, PMSs can increase innovation in social enterprises because integrating social and commercial projects forces employees to think differently, which results in innovative solutions and increases effectiveness [34].

In other situations, PMSs increase performing tensions that are unfavourable [48,50]. First, performing tensions increase because it is possible to quantify and compare commercial performance in the short term, whereas social performance is uncertain and will mostly accrue in the long term, which makes it easier for stakeholders to focus on measures for commercial performance [48]. This increases performing tensions because it is unclear how the social logic comes into play and is measured. Millar and Hall [50] study the use of SROI in social enterprises and find several implications and barriers when trying to measure social performance, such as the problem of using standardized measures, the fact that SROI is time- and resource-intensive to use, conflicting assumptions, difficulties of obtaining non-financial outcomes, lack of comparability, high complexity and lack of acceptance among stakeholders.

Second, implementing PMSs as a consequence of external demands and without involving internal stakeholders might increase tensions. Christiansen and Skærbæk [140] follow a process of implementing a PMS. The PMS is implemented due to external demands. The PMS increases tensions because employees perceive the PMS as reducing their influence on their work and limiting their possibility for creativity. Instead, the PMS enhances the power of the external stakeholders and management, who gain access to information because processes become transparent.

3.2. Attention Focusing

PMSs can emphasize critical aspects of performance and help management align stakeholders to the strategy by measuring and reporting on selected indicators, which reduces both performing and belonging tensions [137]. First, PMSs can help managers re-balance logics and enhance legitimacy if PMSs are combined with stakeholder engagement [41]. PMSs can reduce performing and belonging tensions by mediating a sense-making process of reducing multiple interpretations of organizational identity and securing that stakeholders have the same perception of what the objectives of the social enterprise are. PMSs can reduce belonging tensions by constructing a shared organizational identity and create a feeling of belonging if they represent both logics [8,44].

However, PMSs have several limitations that reduce their usefulness for drawing attention to multiple logics. First, PMSs alone cannot balance logics if social enterprises become too focused on commercial performance (mission drift). Ramus and Vaccaro [141] show how senior management tries to shift its focus from commercial performance to social performance. The PMS is not helpful for mediating the process. Instead, the PMS only becomes a marketing tool because employees dismiss it as a monitoring tool and instead focus on commercial objectives.

Second, performing tensions can arise when stakeholders interpret information from PMSs differently. PMSs tell different stories depending on the person who looks at the information. In a study of budget carry-forwards in schools, Ezzamel et al. [142] find that budget information is interpreted differently depending on stakeholders’ logics. Some interpret budget carry-forwards positively, while others find that a surplus is bad. Finally, PMSs increase tensions and reduce the usefulness for attention focusing when stakeholders use PMSs to support their own logics [41,142].

Social enterprises can secure attention to logics by separating social and financial activities [43]. To reduce performing tensions, resources can be allocated once a year to sub-units. This can be an advantage, as it leads to a limited need for prioritizing between logics during the year. However, it does not help decision-makers at the time of the resource allocation [43,139].

3.3. Strategic Decision-Making

PMSs can help organizations identify opportunities to increase value [96]. Evidence on how PMSs influence decision-making in social enterprises is scarce but three main findings appear from the literature. First, decision-making is conditional on the specific situation [43]. In a study of a Swedish football club, senior managers use three different measures for decision-making: league-table position (sports-related), financial result (business-related) and the amount of equity (business-related). The study shows that the relationship between logics depends on the specific situation. In situations with poor commercial performance, commercial performance is given priority over sports performance. In situations where both commercial and sports performances are satisfactory from a management perspective, logics are not perceived to be incompatible or to create tensions from a management point of view. Finally, the case also illustrates that even when senior managers knew that giving priority to sports performance would affect the commercial result, they gave priority to sports performance if the commercial performance was adequate and the sports performance was poor [43]. In some situations tensions did not exist, whereas in other situations discussions about what to give priority to created tensions.

The second main finding is that to benefit from using PMSs in decision-making it is crucial to involve stakeholders [41], which can be done by creating “spaces of negotiation” [139], giving access to information from the PMS [34] and using different measures representing different logics [43]. In a study by Chenhall et al. [137], stakeholders discuss how to create a PMS for strategic decision-making and monitoring. It is this dialogue that creates productive friction, improves the PMS, and, by that, performance.

Thirdly, decision-making is often decoupled from formal reporting because of high complexity and conflicts among decision-makers due to decision-makers’ individual backgrounds, professions and values that cannot be represented in PMSs [143]. In such a situation, PMSs increase performing tensions.

3.4. Legitimacy

Social enterprises have to develop PMSs if they face demands for transparency from external stakeholders [144,145]. However, it does not necessarily mean that social enterprises also use PMSs for internal purposes. Instead of reducing tensions, PMSs developed for enhancing legitimacy often increase performing and belonging tensions [140,142,146].

Social enterprises adapt PMSs from the private sector to gain legitimacy, even though conventional PMSs fail to show the hybrid value creation of social enterprises [48]. The result is that PMSs become window-dressing rather than a source to improve organizational learning and effectiveness [146]. Nicholls [48] (p. 766) notes in her study that “as a result, they often reflect larger power structures and normative social pressures rather than internal processes.” This often increases performing tensions because PMSs are decoupled from decisions and activities performed in the social enterprise. It can be challenging to use PMSs to enhance legitimacy due to the lack of standards for PMSs in social enterprises. PMSs are used strategically in various ways by social enterprises according to their specific objectives [48]. This can be an advantage because social enterprises can adjust PMSs to their context but it is also problematic because the information provided is often limited, fragmented and therefore of little value for users because of the lack of standardization and comparability [48]. In the study by Ezzamel et al. [142], budgeting brings the commercial logic into schools, which many actors find difficult to manage. Employees create buffers in the system, trying to avoid the commercial logic but still gain legitimacy by using budgets.

4. Discussion

4.1. The Role of PMSs

It is the objective of this paper to gain a deeper understanding of the role of PMSs in social enterprises. In Figure 8, we present the analytical framework extended by findings from the analysis. Based on the findings, we present three roles that PMSs have in social enterprises to manage multiple logics. PMSs can assume the roles of a mediator, a disrupter and a symbolizer. It is important to note that PMSs can have several roles simultaneously. It is therefore not a continuum from mediator to disrupter to symbolizer.

The analysis shows that performing tensions do not always have to be reduced but that it can be beneficial to increase performing tensions as long they create productive friction. Therefore, the role of PMSs does not correlate with how successfully PMSs reduce tensions. The role of PMSs partially correlates with their uses but different factors influence the role of PMSs.

PMSs must represent different aspects of performance as well as different stakeholder values to function as a mediator. Furthermore, stakeholders have to accept PMSs as being a valuable and fair tool. PMSs can have a mediating role in several ways. First, PMSs can mediate innovation by forcing employees to focus on both social and commercial activities simultaneously, which can improve creativity and performance [34]. Second, PMSs mediate dialogue and alignment among stakeholders if they are designed to capture both social and commercial performance [41,137,141,145]. Third, PMSs have their strongest role in enhancing legitimacy [144]. The use of PMSs to create legitimacy often conflicts with the use of PMSs for decision-making, creating a dysfunctional decoupling. One example is the PMSs in a Swedish football organization [43]. The organization has budgets and PMSs for each unit to avoid endless discussions related to trade-offs between sport and business. These PMSs are league-table position (sports-related), financial result (business-related) and the amount of equity (business-related). It is a help to decision-makers that both logics are represented in the PMSs but it is still trade-offs and discussions among top management that help the organization move forward, while the PMSs help each manager to represent his unit.

PMSs disrupt the relation between logics and increase tensions if the only outcome of PMSs is a discussion about how and what to measure [147]. These discussions tend to be unproductive and lead to “stuckness” [137] (p. 269). Developing an appropriate PMS can be challenging, as social enterprises are accountable across multiple logics and toward a range of stakeholders [145]. A PMS can create friction among stakeholders if it does not represent their logics, which is disruptive and increases tensions. The challenge is biggest when PMSs have to integrate commercial performance with social performance. In a situation where the demand for measurement comes from external stakeholders, while internal stakeholders try to avoid it, PMSs are disruptive and often increase tensions [140,141,142,146]. “When interests conflict, PM becomes more complicated and decoupled, because it is not clear what is wanted and consequently, what should be done or measured” [35] (p. 386). In some organizations, PMSs fail to include important aspects of performance. There, stakeholders will try to work against PMSs that do not represent their values. A study of the Royal Danish Theatre finds that the PMS creates frustrations and discussions among a group of artists, because they feel that the PMS does not take their position and priorities into account [140]. Instead, they lose their artistic freedom and the PMS is a tool implemented by government agencies to enforce control and their own interests. In another case, the PMS is subject to endless discussions on how to measure performance, which results in the organization getting “stuck” [137].

In some cases, the use of PMSs enhances legitimacy. In such a situation, the PMSs function as a symbolizer. This may lead to the PMSs also becoming a disrupter, because a decoupling of the PMS and decision-making can increase all four types of tensions, which in this context is disadvantageous. In one Italian social enterprise, management tried to implement a new PMS because the social enterprise had been focusing too much on commercial activities [141]. The PMS was implemented without stakeholder involvement and was seen as a marketing tool that was not useful for monitoring or decision-making. The result was that the organization used commercial measures, while the PMS was only used for external reporting.

4.2. Factors Influencing the Use of PMSs

In the course of our analysis, we discovered that the role of PMSs is affected by several factors: decision-makers’ influence, situation-specific interdependence, institutional factors, stakeholder interpretation of PMSs and design characteristics of PMSs. The factors are added to the framework to give us a deeper understanding of the role of PMSs; see Figure 8. The analysis shows that there is no unique way of modelling the role of PMSs because of the influence from these factors. We discuss their ambivalent effects on managing tensions in the following subsections.

4.2.1. Decision-Makers’ Influence

Decision-makers influence the role of PMSs to a great extent [138]. If decision-makers give priority to one logic, they might exploit PMSs to give priority to their preferred logic while neglecting others [48,147,148]. In a study of two theatres, it is clear how the personal values held by the directors are an important driver for balancing between the art and commercial logic [138]. In another study, the PMS is decoupled from decision-making due to pressure, conflicts and personal values [143]. It is not possible to generalize about whether the influence from decision-makers makes PMSs function as mediators or disrupters. However, the analysis indicates that it is uncommon for PMSs to function as an independent tool to secure a balance between social and commercial logics, because PMSs will either be shaped to fit decision-makers’ expectations or will be reduced to a symbolizer, decoupled from decision-making.

4.2.2. Situation-Specific Interdependence

Findings from the analysis show that there is a dynamic relationship among logics inside social enterprises, which differs from the dominant perception in the literature. Carlsson-Wall et al. [43] find that logics are prioritized differently within the same social enterprise and, more importantly, logics are not incompatible per se but may only conflict based on the situation. In a football club, a good sports performance often leads to good commercial performance due to higher ticket sales, more lucrative TV licenses and increased revenue from advertising and sponsorships [43]. In such a situation, logics do not conflict but create mutual value. It is difficult to say whether PMSs mediate when logics are prioritized differently in different situations. PMSs mediate by giving separate information about sports and commercial performance. However, PMSs do not integrate numbers from each unit, so it is up to decision-makers to prioritize and decide which logic should be given priority in a given situation. Based on these limited findings, PMSs cannot reduce performing tensions when it comes to decision-making as long as separate PMSs exist and logics are measured separately.

4.2.3. Institutional Factors

The analysis shows that the role of PMSs depends on different factors. In one study, the funding situation influences whether the role of PMSs was an informative tool (symbolizer) or an implicative tool (mediator) [138]. Gooneratne and Hoque [146] show how external institutions play a vital role in the adaption of PMSs. A desire for legitimacy also influences the adoption of structures and practices. External demands for PMSs can increase tensions because PMSs are adopted only in the role of a symbolizer with no relation to monitoring, strategic decision-making and attention focusing.

4.2.4. Stakeholder Interpretation of PMSs

Stakeholders’ different logics influence how they perceive and use PMSs [48,140,142,145]. Ezzamel et al. [142] study budget carry-forwards and find that the interpretations of budget carry-forwards vary among stakeholders. Some stakeholders see them as safeguarding and securing resources for the next year, while other stakeholders consider this money as being spent for the current year. Still other stakeholders perceive budget carry-forwards as a signal that schools have too large budgets [142]. Finally, PMSs are perceived differently among stakeholders because PMSs can change power positions and enhance or reduce power, autonomy and control among stakeholders [140].

4.2.5. Design Characteristics of PMSs

In many situations, the characteristics of PMSs will affect whether PMSs mediate, disrupt, symbolize, reduce or increase tensions. It is therefore crucial to develop measures representing both logics [137]. The imperfection of PMSs and the difficulties of measuring social performance make it important to render the attributes of PMSs visible [137]. PMSs can then cause different logics to materialize and create a space for negotiation relating to monitoring and attention focusing [137,139,140]. However, if PMSs only represent one logic, performance will be measured according to norms, criteria and standards appropriate only for that logic and PMSs will disrupt and increase tensions [140]. One approach is to integrate social and commercial performance through frameworks, such as Blended Value Accounting and Social Return on Investment. However, these systems still have to be developed further [48,50].

Social enterprises can choose to divide the organization into sub-units, which is called “structural differentiation” [43] (p. 48). Sub-units then have their own PMS for monitoring and do not have to integrate logics. This allows stakeholders to focus on their own objectives without the risk of creating tensions [43,138,139]. When social enterprises are divided into sub-units, decisions about resource allocation only have to be taken once a year during the budgeting phase. In the course of the year, sub-units can prioritize the use of resources [16,138]. However, it is not always possible to separate logics and if logics are separated, there is a risk of counteractions and undetected contradictions [16]. In a Swedish football club, logics were separated among the sub-units [43]. However, senior management still had to combine logics for strategic decision-making. Tensions arose, since it is not easy to combine measures and because measures are used to support managers’ preferred logics [35]. Therefore, when decision-makers prioritize logics differently, tensions can be difficult to manage. Hence, separating logics by splitting PMSs is by definition not beneficial. However, there is some evidence that it helps to reduce tensions in monitoring and attention focusing and secures resources for each logic during the year but also that PMSs have limited influence on decision-making.

PMSs can be designed to emphasize a logic, while other logics are given priority in decision-making. In such a situation, the role of PMSs is reduced to that of a symbolizer [24,41]. The role of a PMS can also be reduced to a symbolizer if employees avoid it and management focuses on using it for gaining legitimacy by showing commitment to social and commercial logics, while other measures are used for monitoring performance [41]. Busco et al. [34] argue that tensions do not exist among logics if both logics are represented in the PMS. In such a situation, no logic becomes dominant because stakeholders can follow the social enterprise and interact with it though the PMS. However, this study only discusses a PMS in relation to monitoring and legitimacy.

5. Conclusions

5.1. Synthesis of the Findings

Findings from the analysis show that PMSs can have a mediating, disruptive and symbolizing role. A PMS is a mediator when it is capable of presenting information about performance and keeping track of critical success indicators for different aspects of performance with respect to different values. However, there are several situations in which PMSs are disruptive. First, when PMSs increase tensions because of uncertainty about what and how to measure. Second, when stakeholders have different interpretations of PMSs and what PMSs show. Third, when PMSs change the power structures among stakeholders [140,142]. Fourth, when PMSs are associated with one specific logic, making it difficult for other logics to use it as a material tool [142]. Fifth, when PMSs are not adjusted to the hybrid nature of social enterprises. Sixth, when one logic has already become dominant [41]. Finally, when social enterprises try to fit into traditional financial reporting developed for commercial use.

It is therefore crucial to adjust PMSs to the hybrid nature of social enterprises because it will help these social enterprises to meet the increasing demand for being transparent. Furthermore, to reduce tensions, social enterprises may separate social and commercial activities into units or independent organizations. However, to make decisions about resource allocation, logics must be integrated. A major finding is that very few articles deal with how PMSs mediate or disrupt decision-making in social enterprises. It is even more remarkable that suggestions for how PMSs can mediate in decision-making are scarce. In particular, it is unclear how decision-makers handle multiple logics in a situation where giving priority to one logic has a negative impact on the other logic. Findings show that most cases studied have the advantage that logics correlate, which means that commercial performance leads to social performance and vice versa. In other types of social enterprises, we expect to find a clear trade-off between commercial and social performance.

The role of PMSs becomes more complex because in some situations PMSs mediate by increasing performing tensions, whereas in other situations they disrupt and increase tensions. Furthermore, the role of PMSs is influenced by different factors; see Figure 8. It is thus difficult to say what the role of PMSs is in a specific social enterprise because of the influence from these factors.

One clear finding from the analysis is that PMSs in social enterprises need to facilitate a dialogue among stakeholders [41]. This is only possible if performance is evaluated according to different criteria. It is important that PMSs can visualize different aspects of performance to prevent mission drift, construct identity and ensure that the social enterprise maintains its legitimacy among stakeholders. A PMS is not able to integrate all aspects of social and commercial performance. However, by combining multiple evaluation principles and involving stakeholders in discussing and developing measures, it helps to create “productive friction” [137] (p. 269). This also helps social enterprises to come up with new ideas and combine logics in ways that create innovation [34,137].

Our goal was to increase the understanding of how social enterprises can benefit from using PMSs. The review contributes to the existing literature in three ways. First, we provide insight about the situations in which PMSs help social enterprises in monitoring, attention focusing, decision making and creating legitimacy. Developing three roles of PMSs helps us to get a better understanding of the situations and circumstances in which PMSs help social enterprises. This insight may help practitioners to a better understanding of how they can benefit from using PMSs but, more importantly, we also show that PMSs are not always useful for all purposes and have to be used in conjunction with other mechanisms, such as stakeholder involvement. We show that it is not always beneficial to use PMSs to minimize tensions but that PMSs can create tensions that lead to a productive dialogue and thereby improve performance. From our analysis, we see a relation between the role of PMSs and the expectations of uses and incentives behind the PMSs—such as PMSs supporting hidden agendas—often end up being disruptive. Second, the paper defines factors (decision-makers’ influence, situation-specific interdependence, institutional factors, stakeholder interpretation of PMSs and design characteristics of PMSs) influencing the role of PMSs. Third, we show that despite the rapidly increasing number of social enterprises and their predicted future impact on society, there is a lack of research on how these organizations balance and manage multiple logics. Especially, it is important to get a deeper understanding of how PMSs mediate decision-making and which additional factors influence the role of PMSs. The paper demonstrates that only 16 articles have studied the role of PMSs in social enterprises. Next, we provide suggestions for future research since we still need to learn more about how PMSs can contribute to managing multiple logics and tensions in social enterprises.

5.2. Future Research

Future research could therefore look at several aspects. First, social enterprises look for PMSs that have adjusted to their hybrid nature and can combine social and commercial performance. Tools such as Blended Value Accounting and Balanced Scorecard have moved the field forward [48]. However, these frameworks still need further development in order to gain broad acceptance. Relative performance evaluation is a new concept, which could change the way social enterprises measure performance. Future research could be carried out as a case study to see whether social enterprises can benefit from using relative performance evaluation. Further research could look deeper into why, besides wanting to satisfy external demands, social enterprises adapt PMSs. If social enterprises define the purpose of PMSs more clearly, it may be easier to find suitable frameworks that match either the demand for informing stakeholders or the need for detailed information for decision-making. More research is also needed to understand the role of PMSs in decision-making and the ways in which PMSs can mediate and help social enterprises manage multiple, and especially conflicting, logics in decision-making. Within the Corporate Social Responsibility (CSR) literature [110], a new strand of literature discusses whether compensation of managers linked to CSR increases the focus on CSR [25]. There is a lack of research focusing on the relation between management compensation and PMSs. Future research should investigate the opportunities for using PMSs in social enterprises as a mechanism for coupling social performance and incentives. The analysis shows that different factors influence the role of PMSs. Further research could look for other factors that influence the role of PMSs equally well or look at whether the role of PMSs changes from mediator to disrupter because of the influence from certain factors. It is especially interesting to look at how corporate governance systems influence the development and use of PMSs in social enterprises. Future research could also look at the relation between decoupled PMSs and decision-making to get a deeper understanding of the situations in which PMSs become decoupled from monitoring and decision-making. Another avenue for future research could be to look at the use of PMSs and whether social or commercial logics dominate different uses of PMSs. Finally, future research could elaborate on the findings from Carlsson-Wall et al. [43] and shed light on the situation-specific relations among logics. In the case study of the football club, giving priority to sports performance did benefit commercial performance in the long term. However, in many social enterprises this is not the case. It could therefore be interesting to see how a social enterprise takes decisions in a situation where benefitting one logic results in bad performance in the other.

5.3. Limitations

This review has several limitations. First, the analysis of studies relies on a qualitative subjective evaluation and criterion for analysis based on the researchers’ interpretations. Second, the search was limited to certain key words, which may have limited the number of articles found. Third, the review excludes theoretical articles. Studies of organizations within the public or non-profit sector could potentially have contributed to the analysis. Many of the studies included in the review had different ways of studying the phenomenon. The analyses try to solve these ambiguities. However, nuances in the comparison of studies may have been lost. Even though the number of articles is limited and it is not possible to generalize about the role of PMSs, the literature review still contributes with important knowledge and understanding.

Author Contributions

Conceptualization, J.G.N., R.L. and D.V.L.; Methodology, J.G.N., R.L. and D.V.L.; Validation, R.L.; Formal Analysis, J.G.N.; Investigation, J.G.N.; Writing-Original Draft Preparation, J.G.N.; Writing-Review & Editing, J.G.N., R.L. and D.V.L.; Visualization, J.G.N.; Supervision, R.L. and D.V.L.; Project Administration, R.L. and D.V.L.

Funding

J.G.N. Ph.d.project was funded by Innovationsfonden Denmark. The APC was funded by University of Southern Denmark.

Acknowledgments

We would like to thank the following colleagues for their numerous excellent comments on earlier versions of this paper: Albrecht Becker, Sirle Bürkland and Martin Messner.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses or interpretation of data; in the writing of the manuscript or in the decision to publish the results.

References

- Doherty, B.; Haugh, H.; Lyon, F. Social enterprises as hybrid organizations: A review and research agenda. Int. J. Manag. Rev. 2014, 16, 417–436. [Google Scholar] [CrossRef]

- Battilana, J.; Dorado, S. Building sustainable hybrid organizations: The case of commercial microfinance organizations. Acad. Manag. J. 2010, 53, 1419–1440. [Google Scholar] [CrossRef]

- Pache, A.-C.; Santos, F. Inside the hybrid organization: Selective coupling as a response to competing institutional logics. Acad. Manag. J. 2013, 56, 972–1001. [Google Scholar] [CrossRef]

- Mair, J.; Marti, I. Social entrepreneurship research: A source of explanation, prediction and delight. J. World Bus. 2006, 41, 36–44. [Google Scholar] [CrossRef]

- Tracey, P.; Phillips, N.; Jarvis, O. Bridging institutional entrepreneurship and the creation of new organizational forms: A multilevel model. Organ. Sci. 2011, 22, 60–80. [Google Scholar] [CrossRef]

- Lumpkin, G.; Moss, T.W.; Gras, D.M.; Kato, S.; Amezcua, A.S. Entrepreneurial processes in social contexts: How are they different, if at all? Small Bus. Econ. 2013, 40, 761–783. [Google Scholar] [CrossRef]

- Wilson, F.; Post, J.E. Business models for people, planet (& profits): Exploring the phenomena of social business, a market-based approach to social value creation. Small Bus. Econ. 2013, 40, 715–737. [Google Scholar]

- Austin, J.; Stevenson, H.; Wei-Skillern, J. Social and commercial entrepreneurship: Same, different or both? Entrep. Theory Pract. 2006, 30, 1–22. [Google Scholar] [CrossRef]

- Chell, E. Social enterprise and entrepreneurship: Towards a convergent theory of the entrepreneurial process. Int. Small Bus. J. 2007, 25, 5–26. [Google Scholar] [CrossRef]

- Dacin, P.A.; Dacin, M.T.; Matear, M. Social entrepreneurship: Why we don’t need a new theory and how we move forward from here. Acad. Manag. Perspect. 2010, 24, 37–57. [Google Scholar]

- Dees, J.G. Enterprising nonprofits. Harv. Bus. Rev. 1998, 76, 54–69. [Google Scholar]

- Diochon, M.; Anderson, A.R. Social enterprise and effectiveness: A process typology. Soc. Enterp. J. 2009, 5, 7–29. [Google Scholar] [CrossRef]

- Zahra, S.A.; Gedajlovic, E.; Neubaum, D.O.; Shulman, J.M. A typology of social entrepreneurs: Motives, search processes and ethical challenges. J. Bus. Ventur. 2009, 24, 519–532. [Google Scholar] [CrossRef]

- Smith, W.K.; Gonin, M.; Besharov, M.L. Managing social-businnes tensions: A review and research agenda for social enterprise. Bus. Ethics Q. 2013, 3, 407–442. [Google Scholar] [CrossRef]

- Battilana, J.; Lee, M. Advancing research on hybrid organizing—Insights from the study of social enterprises. Acad. Manag. Ann. 2014, 8, 397–441. [Google Scholar] [CrossRef]

- Ebrahim, A.; Battilana, J.; Mair, J. The governance of social enterprises: Mission drift and accountability challenges in hybrid organizations. Res. Organ. Behav. 2014, 34, 81–100. [Google Scholar] [CrossRef]

- Mair, J.; Mayer, J.; Lutz, E. Navigating institutional plurality: Organizational governance in hybrid organizations. Organ. Stud. 2015, 36, 713–739. [Google Scholar] [CrossRef]

- Pache, A.C.; Santos, F. When Worlds Collide: The Internal Dynamics of Organizational Responses to Conflicting Institutional Demands. Acad. Manag. Rev. 2010, 35, 455–476. [Google Scholar]

- Teasdale, S. Negotiating tensions: How do social enterprises in the homelessness field balance social and commercial considerations? Hous. Stud. 2012, 27, 514–532. [Google Scholar] [CrossRef]

- Giroud, X.; Mueller, H.M. Corporate governance, product market competition and equity prices. J. Financ. 2011, 66, 563–600. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z.; Wang, A.Y. Industry tournament incentives. Rev. Financ. Stud. 2017, 31, 1418–1459. [Google Scholar] [CrossRef]

- Li, Z.F. Mutual monitoring and corporate governance. J. Bank. Financ. 2014, 45, 255–269. [Google Scholar]

- Hlady-Rispal, M.; Servantie, V. Deconstructing the way in which value is created in the context of social entrepreneurship. Int. J. Manag. Rev. 2018, 20, 62–80. [Google Scholar] [CrossRef]

- Henri, J.-F. Organizational culture and performance measurement systems. Account. Organ. Soc. 2006, 31, 77–103. [Google Scholar] [CrossRef]

- Hong, B.; Li, Z.; Minor, D. Corporate governance and executive compensation for corporate social responsibility. J. Bus. Ethics 2016, 136, 199–213. [Google Scholar] [CrossRef]

- Bizjak, J.M.; Kalpathy, S.L.; Li, Z.F.; Young, B. The Role of Peer Firm Selection in Explicit Relative Performance Awards. 2018. Available online: https://ssrn.com/abstract=2833309 (accessed on 21 March 2019).

- Goddard, A.; Juma Assad, M. Accounting and navigating legitimacy in Tanzanian NGOs. Account. Audit. Account. J. 2006, 19, 377–404. [Google Scholar] [CrossRef]

- Luke, B.; Barraket, J.; Eversole, R. Measurement as legitimacy versus legitimacy of measures: Performance evaluation of social enterprise. Qual. Res. Account. Manag. 2013, 10, 234–258. [Google Scholar] [CrossRef]

- Siti-nazariah, A.Z.; Siti-nabiha, A.K.; Azhar, Z. Managing Social and Economic Performance in Social Enterprise: A Review of Literature. J. Bus. Manag. Account. 2016, 6, 47–73. [Google Scholar]

- Deephouse, D.L.; Suchman, M. Legitimacy in organizational institutionalism. In The Sage Handbook of Organizational Institutionalism; Greenwood, R., Oliver, C., Suddaby, R., Sahlin, K., Eds.; SAGE: Thousand Oaks, CA, USA, 2008; pp. 1–46. [Google Scholar]

- Thornton, P.H.; Ocasio, W. Institutional logics and the historical contingency of power in organizations: Executive succession in the higher education publishing industry, 1958–1990. Am. J. Sociol. 1999, 105, 801–843. [Google Scholar] [CrossRef]

- Thornton, P.H. The rise of the corporation in a craft industry: Conflict and conformity in institutional logics. Acad. Manag. J. 2002, 45, 81–101. [Google Scholar]

- Reay, T.; Hinings, C.R. Managing the rivalry of competing institutional logics. Organ. Stud. 2009, 30, 629–652. [Google Scholar] [CrossRef]

- Busco, C.; Giovannoni, E.; Riccaboni, A. Sustaining multiple logics within hybrid organisations: Accounting, mediation and the search for innovation. Account. Audit. Account. J. 2017, 30, 191–216. [Google Scholar] [CrossRef]

- Mason, C.; Doherty, B. A fair trade-off? Paradoxes in the governance of fair-trade social enterprises. J. Bus. Ethics 2016, 136, 451–469. [Google Scholar] [CrossRef]

- DTI. Social Enterprise: A Strategy for Success; DTI Department of Trade and Industry: London, UK, 2002.

- Santos, F. A positive theory of social entrepreneurship. J. Bus. Ethics 2012, 111, 335–351. [Google Scholar] [CrossRef]

- Jay, J. Navigating paradox as a mechanism of change and innovation in hybrid organizations. Acad. Manag. J. 2013, 56, 137–159. [Google Scholar] [CrossRef]

- Ebrahim, A.S.; Rangan, V.K. The limits of nonprofit impact: A contingency framework for measuring social performance. Soc. Enterp. Initiat. Harv. Bus. Sch. 2010, 8, 1–6. [Google Scholar] [CrossRef]

- Smith, W.K.; Lewis, M.W. Toward a theory of paradox: A dynamic equilibrium model of organzining. Acad. Manag. Rev. 2011, 36, 381–403. [Google Scholar]

- Ramus, T.; Vaccaro, A.; Brusoni, S. Institutional complexity in turbulent times: Formalization, collaboration and the emergence of blended logics. Acad. Manag. J. 2017, 60, 1253–1284. [Google Scholar] [CrossRef]

- Santos, F.; Pache, A.-C.; Birkholz, C. Making hybrids work. Calif. Manag. Rev. 2015, 57, 36–59. [Google Scholar] [CrossRef]

- Carlsson-Wall, M.; Kraus, K.; Messner, M. Performance measurement systems and the enactment of different institutional logics: Insights from a football organization. Manag. Account. Res. 2016, 32, 45–61. [Google Scholar] [CrossRef]

- Grimes, M. Strategic sensemaking within funding relationships: The effects of performance measurement on organizational identity in the social sector. Entrep. Theory Pract. 2010, 34, 763–783. [Google Scholar] [CrossRef]

- Ebrahim, A.; Rangan, V.K. What impact? A framework for measuring the scale and scope of social performance. Calif. Manag. Rev. 2014, 56, 118–141. [Google Scholar] [CrossRef]

- Lueg, R.; Nørreklit, H. Performance measurement systems—Beyond generic strategic actions. In The Routledge Companion to Cost Management; Mitchell, F., Nørreklit, H., Jakobsen, M., Eds.; Routledge: New York, NY, USA, 2012; pp. 342–359. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard: Translating Strategy into Action; Harvard Business School Press: Boston, MA, USA, 1996. [Google Scholar]

- Nicholls, A. ‘We do good things, don’t we?’: ‘Blended Value Accounting’ in social entrepreneurship. Account. Organ. Soc. 2009, 34, 755–769. [Google Scholar] [CrossRef]

- Kroeger, A.; Weber, C. Developing a conceptual framework for comparing social value creation. Acad. Manag. Rev. 2014, 39, 513–540. [Google Scholar] [CrossRef]

- Millar, R.; Hall, K. Social return on investment (SROI) and performance measurement: The opportunities and barriers for social enterprises in health and social care. Public Manag. Rev. 2013, 15, 923–941. [Google Scholar] [CrossRef]

- Denyer, D.; Tranfield, D.; Van Aken, J.E. Developing design propositions through research synthesis. Organ. Stud. 2008, 29, 393–413. [Google Scholar] [CrossRef]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a methodology for developing evidence: Informed management knowledge by means of systematic review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Agndal, H.; Nilsson, U. Different open book accounting practices for different purchasing strategies. Manag. Account. Res. 2010, 21, 147–166. [Google Scholar] [CrossRef]

- Alawattage, C.; Fernando, S. Postcoloniality in corporate social and environmental accountability. Account. Organ. Soc. 2017, 60, 1–20. [Google Scholar] [CrossRef]

- Barrett, M.; Gendron, Y. WebTrust and the “commercialistic auditor” The unrealized vision of developing auditor trustworthiness in cyberspace. Account. Audit. Account. J. 2006, 19, 631–662. [Google Scholar] [CrossRef]

- Bedford, D.S.; Malmi, T. Configurations of control: An exploratory analysis. Manag. Account. Res. 2015, 27, 2–26. [Google Scholar] [CrossRef] [Green Version]

- Bhimani, A. Accounting and the emergence of “economic man”. Account. Organ. Soc. 1994, 19, 637–674. [Google Scholar] [CrossRef]

- Boland, R.J., Jr.; Sharma, A.K.; Afonso, P.S. Designing management control in hybrid organizations: The role of path creation and morphogenesis. Account. Organ. Soc. 2008, 33, 899–914. [Google Scholar] [CrossRef]

- Botes, V. Flight of fantasy: Writing a full proof “code” for ethics. Account. Audit. Account. J. 2012, 25, 927–928. [Google Scholar] [CrossRef]

- Bugg-Levine, A.; Kogut, B.; Kulatilaka, N. A new approach to funding social enterprises. Harv. Bus. Rev. 2012, 90, 118–123. [Google Scholar]

- Burns, J.; Baldvinsdottir, G. An institutional perspective of accountants’ new roles—The interplay of contradictions and praxis. Eur. Account. Rev. 2005, 14, 725–757. [Google Scholar] [CrossRef]

- Callahan, C.M.; Smith, R.E.; Spencer, A.W. The valuation and reliability implications of FIN 46 for synthetic lease liabilities. J. Account. Public Policy 2013, 32, 271–291. [Google Scholar] [CrossRef]

- Caperchione, E.; Demirag, I.; Grossi, G. Public sector reforms and public private partnerships: Overview and research agenda. Account. Forum 2017, 41, 1–7. [Google Scholar] [CrossRef]

- Carnes, G.A.; Guffey, D.M. The influence of international status and operating segments on firms’ choice of bonus plans. J. Int. Account. Audit. Tax. 2000, 9, 43–57. [Google Scholar] [CrossRef]

- Caron, M.; Turcotte, M.B. Path dependence and path creation. Account. Audit. Account. J. 2009, 22, 272–297. [Google Scholar] [CrossRef]

- Chua, W.F.; Poullaos, C. The Empire Strikes Back? An exploration of centre-periphery interaction between the ICAEW and accounting associations in the self-governing colonies of Australia, Canada and South Africa, 1880–1907. Account. Organ. Soc. 2002, 27, 409–445. [Google Scholar] [CrossRef]

- Cooper, C.; Graham, C.; Himick, D. Social impact bonds: The securitization of the homeless. Account. Organ. Soc. 2016, 55, 63–82. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M. An examination of social and environmental reporting strategies. Account. Audit. Account. J. 2001, 14, 587–617. [Google Scholar] [CrossRef]

- Covaleski, M.A.; Dirsmith, M.W.; Weiss, J.M. The social construction, challenge and transformation of a budgetary regime: The endogenization of welfare regulation by institutional entrepreneurs. Account. Organ. Soc. 2013, 38, 333–364. [Google Scholar] [CrossRef]

- Cowton, C.J. Accounting and the ethics challenge: Re-membering the professional body. Account. Bus. Res. 2009, 39, 177–189. [Google Scholar] [CrossRef]

- Craig, R.; Amernic, J. A privatization success story: Accounting and narrative expression over time. Account. Audit. Account. J. 2008, 21, 1085–1115. [Google Scholar] [CrossRef]

- Dai, N.T.; Tan, Z.S.; Tang, G.; Xiao, J.Z. IPOs, institutional complexity and management accounting in hybrid organisations: A field study in a state-owned enterprise in China. Manag. Account. Res. 2017, 36, 2–23. [Google Scholar] [CrossRef]

- Davie, S.S.; McLean, T. Accounting, cultural hybridisation and colonial globalisation: A case of British civilising mission in Fiji. Account. Audit. Account. J. 2017, 30, 932–954. [Google Scholar] [CrossRef]

- Davison, J. Photographs and accountability: Cracking the codes of an NGO. Account. Audit. Account. J. 2007, 20, 133–158. [Google Scholar] [CrossRef]

- Dossi, A.; Patelli, L.; Zoni, L. The missing link between corporate performance measurement systems and chief executive officer incentive plans. J. Account. Audit. Financ. 2010, 25, 531–558. [Google Scholar] [CrossRef]

- Edwards, J.R.; Dean, G.; Clarke, F. Merchants’ accounts, performance assessment and decision making in mercantilist Britain. Account. Organ. Soc. 2009, 34, 551–570. [Google Scholar] [CrossRef]

- Fischer, M.D.; Ferlie, E. Resisting hybridisation between modes of clinical risk management: Contradiction, contest and the production of intractable conflict. Account. Organ. Soc. 2013, 38, 30–49. [Google Scholar] [CrossRef]

- Funnell, W.; Robertson, J. Capitalist accounting in sixteenth century Holland: Hanseatic influences and the Sombart thesis. Account. Audit. Account. J. 2011, 24, 560–586. [Google Scholar] [CrossRef]

- Funnell, W.; Williams, R. The religious imperative of cost accounting in the early industrial revolution. Account. Audit. Account. J. 2014, 27, 357–381. [Google Scholar] [CrossRef]

- Giovannoni, E.; Pia Maraghini, M. The challenges of integrated performance measurement systems: Integrating mechanisms for integrated measures. Account. Audit. Account. J. 2013, 26, 978–1008. [Google Scholar] [CrossRef]

- Hazgui, M.; Gendron, Y. Blurred roles and elusive boundaries: On contemporary forms of oversight surrounding professional work. Account. Audit. Account. J. 2015, 28, 1234–1262. [Google Scholar] [CrossRef]

- Heard, J.E.; Bolce, W.J. The political significance of corporate social reporting in the United States of America. Account. Organ. Soc. 1981, 6, 247–254. [Google Scholar] [CrossRef]

- Hopkins, P.E. The effect of financial statement classification of hybrid financial instruments on financial analysts’ stock price judgments. J. Account. Res. 1996, 34, 33–50. [Google Scholar] [CrossRef]

- Hyvönen, T.; Järvinen, J.; Pellinen, J.; Rahko, T. Institutional logics, ICT and stability of management accounting. Eur. Account. Rev. 2009, 18, 241–275. [Google Scholar] [CrossRef]

- Jacobs, K. Hybridisation or polarisation: Doctors and accounting in the UK, Germany and Italy. Financ. Account. Manag. 2005, 21, 135–162. [Google Scholar] [CrossRef]

- Kahn, R.L. Discussion of an empirical study of the role of accounting data in performance evaluation. J. Account. Res. 1972, 10, 183–186. [Google Scholar] [CrossRef]

- Kastberg, G.; Siverbo, S. The role of management accounting and control in making professional organizations horizontal. Account. Audit. Account. J. 2016, 29, 428–451. [Google Scholar] [CrossRef]

- Kimmel, P.; Warfield, T.D. Variation in attributes of redeemable preferred stock: Implications for accounting standards. Account. Horiz. 1993, 7, 30. [Google Scholar]

- King, G. The implications of an organization’s structure on whistleblowing. J. Bus. Ethics 1999, 20, 315–326. [Google Scholar] [CrossRef]

- King, T.E.; Ortegren, A.K.; King, R.M. A reassessment of the allocation of convertible debt proceeds and the implications for other hybrid financial instruments. Account. Horiz. 1990, 4, 10. [Google Scholar]

- Kosmala, K. True and fair view or rzetelny i jasny obraz? A survey of Polish Practitioners. Eur. Account. Rev. 2005, 14, 579–602. [Google Scholar] [CrossRef]

- Kurunmäki, L. A hybrid profession—The acquisition of management accounting expertise by medical professionals. Account. Organ. Soc. 2004, 29, 327–347. [Google Scholar] [CrossRef]

- Kurunmäki, L.; Miller, P. Regulatory hybrids: Partnerships, budgeting and modernising government. Manag. Account. Res. 2011, 22, 220–241. [Google Scholar] [CrossRef]

- Lee, C.-W.J. Financial restructuring of state owned enterprises in China: The case of Shanghai Sunve Pharmaceutical Corporation. Account. Organ. Soc. 2001, 26, 673–689. [Google Scholar]

- Levi, S.; Segal, B. The impact of debt-equity reporting classifications on the firm’s decision to issue hybrid securities. Eur. Account. Rev. 2015, 24, 801–822. [Google Scholar] [CrossRef]

- Lingane, A.; Olsen, S. Guidelines for social return on investment. Calif. Manag. Rev. 2004, 46, 116–135. [Google Scholar] [CrossRef]

- Macintosh, N.B.; Baker, C.R. A literary theory perspective on accounting: Towards heteroglossic accounting reports. Account. Audit. Account. J. 2002, 15, 184–222. [Google Scholar] [CrossRef]

- Mathews, M.R. A suggested classification for social accounting research. J. Account. Public Policy 1984, 3, 199–221. [Google Scholar] [CrossRef]

- Mattessich, R. Accounting reconsidered. Calif. Manag. Rev. 1959, 2, 85–91. [Google Scholar] [CrossRef]

- Maydew, E. Discussion of Firms’ off-balance sheet and hybrid debt financing: Evidence from their book-tax reporting differences. J. Account. Res. 2005, 43, 283–290. [Google Scholar] [CrossRef]

- Mihret, D.G.; Alshareef, M.N.; Bazhair, A. Accounting professionalization and the state: The case of Saudi Arabia. Crit. Perspect. Account. 2017, 45, 29–47. [Google Scholar] [CrossRef]

- Mikesell, J.L.; Mullins, D.R. Reforming budget systems in countries of the former Soviet Union. Public Adm. Rev. 2001, 61, 548–568. [Google Scholar] [CrossRef]

- Miller, P.; Kurunmäki, L.; O’Leary, T. Accounting, hybrids and the management of risk. Account. Organ. Soc. 2008, 33, 942–967. [Google Scholar] [CrossRef] [Green Version]

- Milliron, V.; Toy, D. Tax compliance: An investigation of key features. J. Am. Tax. Assoc. 1988, 9, 84–104. [Google Scholar]

- Mills, L.F.; Newberry, K.J. Firms’ off-balance sheet and hybrid debt financing: Evidence from their book-tax reporting differences. J. Account. Res. 2005, 43, 251–282. [Google Scholar] [CrossRef]

- Newberry, S.; Barnett, P. Negotiating the network: The contracting experiences of community mental health agencies in New Zealand. Financ. Account. Manag. 2001, 17, 133–152. [Google Scholar] [CrossRef]

- Moerman, L.C.; van der Laan, S.L. Risky business: Socializing asbestos risk and the hybridization of accounting. Crit. Perspect. Account. 2012, 23, 107–116. [Google Scholar] [CrossRef]

- Moody-Stuart, M. Discussion of Does sustainabililty reporting improve corporate behavior?: Wrong question? Right time? Account. Bus. Res. 2006, 36, 89–94. [Google Scholar] [CrossRef]

- Sabeti, H. The for-benefit enterprise. Harv. Bus. Rev. 2011, 89, 98–104. [Google Scholar]

- O’Dwyer, B. Conceptions of corporate social responsibility: The nature of managerial capture. Account. Audit. Account. J. 2003, 16, 523–557. [Google Scholar] [CrossRef]

- Ouibrahim, N.; Scapens, R. Accounting and financial control in a socialist enterprise: A case study from Algeria. Account. Audit. Account. J. 1989, 2. [Google Scholar] [CrossRef]

- Preston, A.M.; Vesey, A.M. The construction of US utility accounting: 1882–1944. Account. Organ. Soc. 2008, 33, 415–435. [Google Scholar] [CrossRef]

- Rayman, R.A. Fair value accounting and the present value fallacy: The need for an alternative conceptual framework. Br. Account. Rev. 2007, 39, 211–225. [Google Scholar] [CrossRef]

- Rubenstein, D.B. Bridging the gap between green accounting and black ink. Account. Organ. Soc. 1992, 17, 501–508. [Google Scholar] [CrossRef]

- Ryan, S.G.; Herz, R.H.; Iannaconi, T.E.; Maines, L.A.; Palepu, K.; Schrand, C.M.; Skinner, D.J.E.A. Evaluation of the FASB’s proposed accounting for financial instruments with characteristics of liabilities, equity or both. Account. Horiz. 2001, 15, 387–400. [Google Scholar] [CrossRef]

- Sample, V.A. Resource planning and budgeting for national forest. Public Adm. Rev. 2017, 52, 339–346. [Google Scholar] [CrossRef]

- Shaoul, J.; Stafford, A.; Stapleton, P. Accountability and corporate governance of public private partnerships. Crit. Perspect. Account. 2012, 23, 213–229. [Google Scholar] [CrossRef]

- Sikka, P. Enterprise culture and accountancy firms: New masters of the universe. Account. Audit. Account. J. 2008, 21, 268–295. [Google Scholar] [CrossRef]

- Skousen, C.R.; Yang, J.L. Western management accounting and the economic reforms of China. Account. Organ. Soc. 1988, 13, 201–206. [Google Scholar] [CrossRef]

- Skærbæk, P.; Thorbjørnsen, S. The commodification of the Danish defence forces and the troubled identities of its officers. Financ. Account. Manag. 2007, 23, 243–268. [Google Scholar] [CrossRef]

- Szulanski, G.; Winter, S. Getting it right the second time. Harv. Bus. Rev. 2002, 80, 62–69. [Google Scholar]

- Thomson, I.; Grubnic, S.; Georgakopoulos, G. Exploring accounting-sustainability hybridisation in the UK public sector. Account. Organ. Soc. 2014, 39, 453–476. [Google Scholar] [CrossRef] [Green Version]