The Study of the Impact of Carbon Finance Effect on Carbon Emissions in Beijing-Tianjin-Hebei Region—Based on Logarithmic Mean Divisia Index Decomposition Analysis

Abstract

:1. Introduction

2. A Brief Overview of Literature

2.1. The Cost of Carbon Reduction

2.2. The Impact of Financial Development on Carbon Emissions

2.3. The Construction of Carbon Finance Market

2.4. The Stock Market in Promoting Renewable or Clean Energy Projects and Reducing Carbon Emissions

3. Methodology and Data

3.1. Constructing an LMDI Model

3.2. Basic Data

4. An Empirical Analysis of the Effects of Carbon Finance on Carbon Emissions

4.1. An Empirical Study on the Impact of Carbon Finance Effect on Carbon Emissions from the Beijing-Tianjin-Hebei Region

4.1.1. The Effects of Green Credit on Carbon Emissions

4.1.2. The Effects of Carbon Trading on Carbon Emissions

4.2. An Empirical Analysis of the Effects of Carbon Finance on Carbon Emissions in the Sub-Region

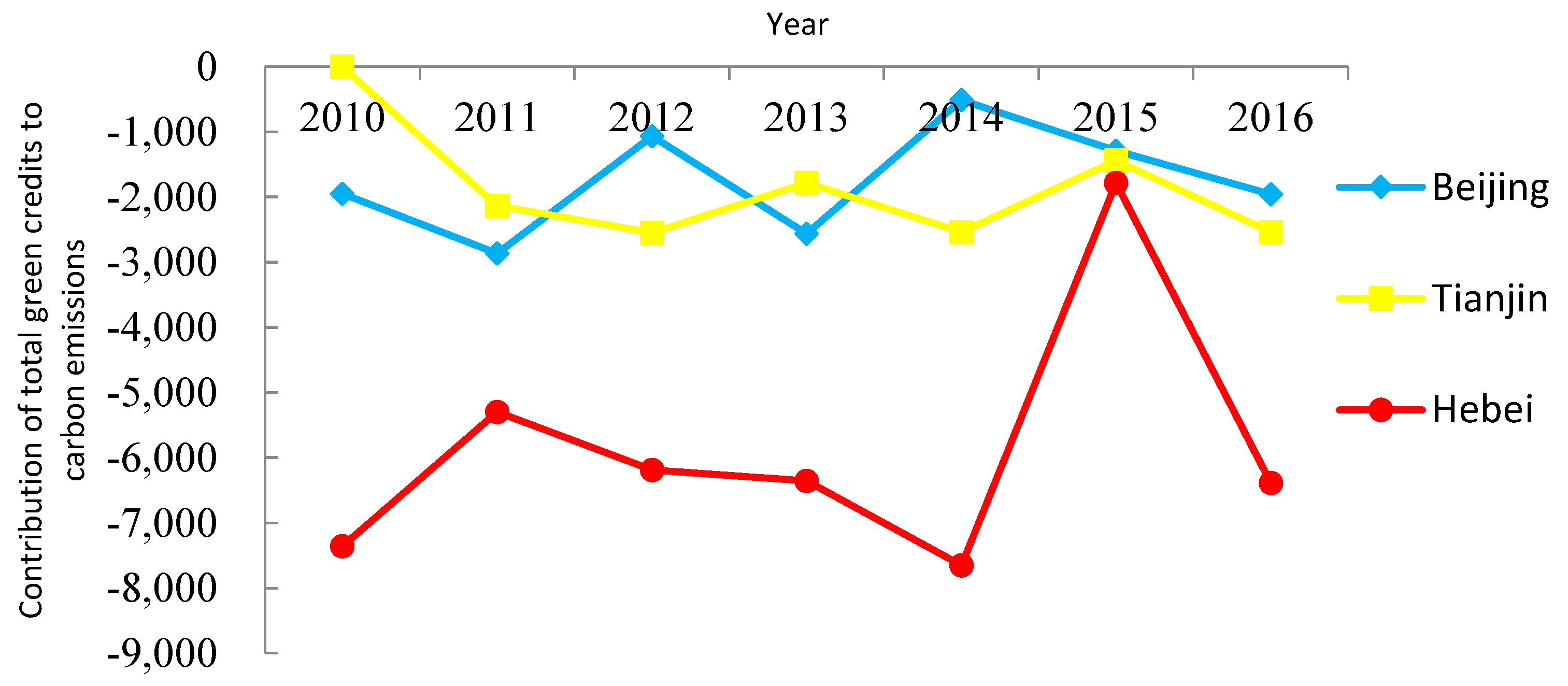

4.2.1. Contribution of the Total Green Credit Effect of Each Region to Carbon Emissions

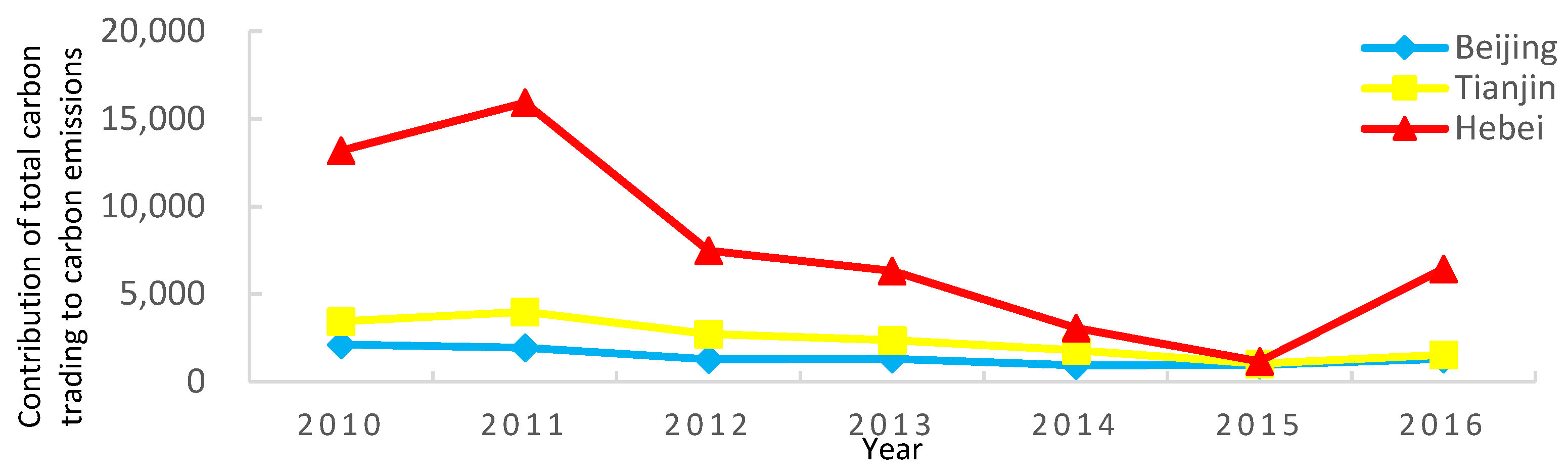

4.2.2. Contribution of the Total Carbon Trading Effect of Each Region to Carbon Emissions

5. Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

References

- Intergovernmental Panel on Climate Change. Climate Change 2007: The Physical Science Basis. Available online: http://www.ipcc.ch/report/ar5/wg1/ (accessed on 13 November 2017).

- World Bank, 2018. Available online: https://data.worldbank.org/indicator/EN.ATM.CO2E.KT (accessed on 10 January 2019).

- Shi, Q.; Chen, J.; Shen, L. Driving factors of the changes in the carbon emissions in the Chinese construction industry. J. Clean. Prod. 2017, 166, 615–627. [Google Scholar] [CrossRef]

- Zhang, S.M.; Wang, L.Y. Relationship between carbon emission reduction and carbon finance-a study on promoting carbon emission reduction through carbon financing. In Proceedings of the International Conference on Manufacture Engineering and Environment Engineering (MEEE), Hong Kong, China, 26 November 2013. [Google Scholar]

- United Nations Conference on Environment and Development. United Nations Framework Convention on Climate Change. 1992. Available online: http://legal.un.org/avl/ha/ccc/ccc.html (accessed on 21 February 2019).

- Chen, J.; Shen, L.; Song, X.; Shi, Q.; Li, S. An empirical study on the CO2 emissions in the Chinese construction industry. J. Clean. Prod. 2017, 168, 645–654. [Google Scholar] [CrossRef]

- Zhang, Y.; Shen, L.; Shuai, C.; Bian, J.; Zhu, M.; Tan, Y.; Ye, G. How is the environmental efficiency in the process of dramatic economic development in the Chinese cities? Ecol. Indic. 2019, 98, 349–362. [Google Scholar] [CrossRef]

- Pan, L.F. For the First Time, China’s per Capita Carbon Emissions Have Exceeded Those of the European Union and Exceeded Those of Europe and the United States Combined. Wall Street Journal 2014. Available online: https://wallstreetcn.com/articles/208487 (accessed on 21 February 2019).

- Yu, Q. Global carbon project report: global carbon emissions rebounded strongly in 2017. Available online: http://www.sohu.com/a/204132842_313745 (accessed on 1 March 2019).

- Cohen, G.; Jalles, J.T.; Loungani, P.; Marto, R.; Wang, G. Decoupling of Emissions and GDP: Evidence from Aggregate and Provincial Chinese Data; Social Science Electronic Publishing: Rochester, NY, USA, 2018. [Google Scholar]

- Zhou, P.; Zhou, X.; Zhou, D.Q. A survey of studies on Estimating CO2 mitigation costs. Manag. Rev. 2014, 26, 20–27. [Google Scholar]

- Ellerman, A.D.; Decaux, A. Analysis of Post-Kyoto CO2 Emissions Trading Using Marginal Abatement Curves; MIT Working Paper: Cambridge, MA, USA, 1998. [Google Scholar]

- Schelling, T.C. Intergenerational Discounting. Energy Policy 1995, 23, 395–401. [Google Scholar] [CrossRef]

- Goulder, L.H.; Parry, I.W.H.; Williams, R.C., III; Burtraw, D. The cost-effectiveness of alternative instruments for environmental protection in a second-best setting. J. Public Econ. 1999, 72, 329–360. [Google Scholar] [CrossRef]

- Chaurey, A.; Kandpal, T.C. Carbon abatement potential of solar home systems in India and their cost reduction due to carbon. Energy Policy 2009, 37, 115–125. [Google Scholar] [CrossRef]

- Wu, L.B.; Qian, H.Q.; Tang, W.Q. Selection Mechanism between Emission Trading and Carbon Tax based on Simulation of Dynamic Marginal Abatement Cost. Econ. Res. J. 2014, 49, 48–61. [Google Scholar]

- Ma, Y.M.; Gao, S.; Qiu, S. Foreign Direct Investment, Financial Deepening and Carbon Emission-Based on 1995–2011 Provincial Panel Data Financial. Sci. Technol. Manag. Res. 2014, 13, 214–218. [Google Scholar]

- Rahman, S.M.; Kirkman, G.A. Costs of certified emission reductions under the Clean Development Mechanism of the Kyoto Protocol. Energy Econ. 2015, 47, 129–141. [Google Scholar] [CrossRef]

- Linares, P.; Pérez-Arriaga, I.J. A sustainable framework for biofuels in Europe. Energy Policy 2013, 52, 166–169. [Google Scholar] [CrossRef]

- Shahbaz, M.; Solarin, S.A.; Mahmood, H. Does Financial Development Reduce CO2 Emissions in Malaysian Economy? A Time Series Analysis. Econ. Model. 2013, 35, 145–152. [Google Scholar] [CrossRef]

- Sadorsky, P. The impact of financial development on energy consumption in emerging economies. Energy Policy 2010, 38, 2528–2535. [Google Scholar] [CrossRef]

- Jalil, A.; Feridun, M. The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Econ. 2011, 33, 284–291. [Google Scholar] [CrossRef]

- Gu, H.M.; He, B. Study on Chinese Financial Development and Carbon Emission. China’s Popul. Resour. Environ. 2012, 22, 22–27. [Google Scholar]

- Yan, C.L.; Li, T.; Lan, W. Financial Development, Innovation and Carbon Emission. J. Financ. Res. 2016, 1, 14–30. [Google Scholar]

- Xiong, L.; Qi, S.Z. Financial development and China’s provincial carbon emissions—Based on STIRPAT model and dynamic panel data analysis. J. China Univ. Geosci. 2016, 2, 63–73. [Google Scholar]

- Shao, H.H.; Liu, Y.B. The Nonlinear Relationship between Financial Development and Carbon Emission--Based on Panel Smooth Transition Regression Model. Soft Sci. 2017, 31, 80–84. [Google Scholar]

- Yang, Z.; Chen, B. Establishing a regional carbon trading market in China is imperative. Acad. Mon. 2010, 7, 65–77. [Google Scholar]

- Chen, B.; Liu, Z. Research on Global Carbon Trading Market. J. Inn. Mong. Univ. 2010, 3, 22–26. [Google Scholar]

- Zhang, J.H. The path of carbon trading market construction. China Financ. 2011, 10, 26–28. [Google Scholar]

- Yang, S.C.; Zhang, R.P. System design for the development of carbon financial market. Explor. Econ. Probl. 2012, 9, 103–106. [Google Scholar]

- Mei, X.H.; Xu, C.Z. Research on the construction of China’s carbon financial system. Explor. Econ. Probl. 2015, 10, 89–96. [Google Scholar]

- Zhang, Z.Q. Development strategy of carbon finance in China under the background of low carbon economy. Educ. Dev. Res. 2017, s1, 10–12. [Google Scholar]

- Paramati, S.R.; Mo, D.; Gupta, R. The effects of stock market growth and renewable energy use on CO2 emissions: Evidence from G20 countries. Energy Econ. 2017, 66, 360–371. [Google Scholar] [CrossRef]

- Paramati, S.R.; Bhattacharya, M.; Ozturk, I.; Zakari, A. Determinants of energy demand in African frontier market economies: An empirical investigation. Energy 2018, 148, 123–133. [Google Scholar] [CrossRef]

- Kutan, A.M.; Paramati, S.R.; Ummalla, M.; Zakari, A. Financing renewable energy projects in major emerging market economies: Evidence in the perspective of sustainable economic development. Emerg. Mark. Financ. Trade 2018, 54, 1761–1777. [Google Scholar] [CrossRef]

- Paramati, S.R.; Apergis, N.; Ummalla, M. Financing clean energy projects through domestic and foreign capital: The role of political cooperation among the EU, the G20 and OECD countries. Energy Econ. 2017, 61, 62–71. [Google Scholar] [CrossRef]

- Paramati, S.R.; Alam, M.S.; Apergis, N. The role of stock markets on environmental degradation: A comparative study of developed and emerging market economies across the globe. Emerg. Mark. Rev. 2018, 35, 19–30. [Google Scholar] [CrossRef]

- Ang, B.W.; Zhang, F.Q.; Choi, K.H. Factorizing Changes in Energy and Environmental Indicators through Decomposition. Energy 1998, 23, 489–495. [Google Scholar] [CrossRef]

- Ang, B.W.; Liu, F.L. A New Energy Decomposition Method: Perfect in Decomposition and Consistent in Aggregation. Energy 2001, 26, 537–548. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Year | ∆C | ∆Cu | ∆Cq | ∆C1 | ∆Cd | ∆Ccer | ∆C2 |

|---|---|---|---|---|---|---|---|

| 2010 | 9438.72 | −11,214.65 | 1906.02 | −9308.63 | 51,145.45 | −32,398.10 | 18,747.35 |

| 2011 | 11,562.49 | −10,849.28 | 559.77 | −10,289.51 | −69,941.03 | 91,793.02 | 21,851.99 |

| 2012 | 1645.84 | −6839.19 | −2966.30 | −9805.49 | −41,509.76 | 52,961.08 | 11,451.33 |

| 2013 | −673.35 | −38,564.35 | 27,866.81 | −10,697.54 | 313,758.78 | −303,734.58 | 10,024.20 |

| 2014 | −4915.56 | −17,580.54 | 6882.57 | −10,697.97 | 89,836.97 | −84,054.56 | 5782.41 |

| 2015 | −1390.25 | −35,588.53 | 31,078.91 | −4509.61 | −67,851.01 | 70,970.37 | 3119.36 |

| 2016 | −1595.16 | −15,823.34 | 4938.13 | −10,885.21 | −31,852.09 | 41,142.14 | 9290.05 |

| 2010-2016 | 14,072.73 | −136,459.87 | 70,265.92 | −66,193.96 | 243,587.31 | −163,320.62 | 80,266.68 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, L.; Liu, D.; Hou, J.; Xu, D.; Chao, W. The Study of the Impact of Carbon Finance Effect on Carbon Emissions in Beijing-Tianjin-Hebei Region—Based on Logarithmic Mean Divisia Index Decomposition Analysis. Sustainability 2019, 11, 1465. https://doi.org/10.3390/su11051465

Li L, Liu D, Hou J, Xu D, Chao W. The Study of the Impact of Carbon Finance Effect on Carbon Emissions in Beijing-Tianjin-Hebei Region—Based on Logarithmic Mean Divisia Index Decomposition Analysis. Sustainability. 2019; 11(5):1465. https://doi.org/10.3390/su11051465

Chicago/Turabian StyleLi, Li, Di Liu, Jian Hou, Dandan Xu, and Wenbo Chao. 2019. "The Study of the Impact of Carbon Finance Effect on Carbon Emissions in Beijing-Tianjin-Hebei Region—Based on Logarithmic Mean Divisia Index Decomposition Analysis" Sustainability 11, no. 5: 1465. https://doi.org/10.3390/su11051465

APA StyleLi, L., Liu, D., Hou, J., Xu, D., & Chao, W. (2019). The Study of the Impact of Carbon Finance Effect on Carbon Emissions in Beijing-Tianjin-Hebei Region—Based on Logarithmic Mean Divisia Index Decomposition Analysis. Sustainability, 11(5), 1465. https://doi.org/10.3390/su11051465