What Happens after the Rare Earth Crisis: A Systematic Literature Review

1

College of Business Administration, Capital University of Economics and Business, Beijing 100070, China

2

School of Economics, Center for Studies of Modern Business, Zhejiang Gongshang University, Hangzhou 310018, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(5), 1288; https://doi.org/10.3390/su11051288

Submission received: 9 January 2019

/

Revised: 23 February 2019

/

Accepted: 26 February 2019

/

Published: 1 March 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:Rare earths (REs) play an important role in modern life, and have been the focus of global attention in recent years. As a result, the number of scientific publications has grown enormously, increasing the need for understanding the knowledge base of various research streams and their emerging branches. The economic analysis of REs has also augmented steadily. Nevertheless, the relevant literature is rather fragmented concerning the thematic topics. To respond to this, a systematic review in accordance with the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) and a bibliometric analysis were developed to offer a systematic and holistic literature review of the economic research on REs. This review incorporates studies of REs regarding aspects of supply, price, export policy, international trade, relationship with clean energy, and sustainability. The database of this review includes a set of 85 systemically selected state-of-the-art articles from five databases, including Web of Science, Science Direct, Springer, Proquest, and China National Knowledge Infrastructure (CNKI) that were published after the rare earth crisis, covering empirical and theory research conducted in different countries with different resource endowments. The results show that the majority of the economic research studies have been conducted in the past six years. Furthermore, among the six categories, the most popular research trend is sustainability. Some possible opportunities for future research are also illustrated in this paper.

1. Introduction

With the increasing concerns about climate change and reliability of supply of fossil fuels, it’s well acknowledged that growing attention has been drawn to the introduction and implementation of new energy, which mostly relies on the emerging technologies such as photovoltaics, fuel cells, and wind turbines. As a consequence, the materials that are required for the emerging technologies, which are indispensable or can hardly be substituted, have become the focus of concern. Among the materials, rare earths (REs) have become critical and important.

Rare earths (REs) refer to the 15 metallic elements of the lanthanide series, coupled with the chemically similar yttrium, and occasionally scandium [1]. Typically, REs are divided into two categories according to the separation process: light rare earths and heavy rare earths. The light rare earths are lanthanum (La), cerium (Ce), praseodymium (Pr), neodymium (Nd), and samarium (Sm), and the heavy rare earths include gadolinium (Gd), europium (Eu), terbium (Tb), dysprosium (Dy), thulium (Tm), ytterbium (Yb), lutetium (Lu), yttrium (Y), holmium (Ho), and erbium (Er) [2]. As a matter of fact, REs are not really rare in the crust of the earth. The abundance of REs in the earth’s crust is actually significantly higher than other commonly exploited elements, including the platinum group elements and mercury [1]. Most of these elements are as abundant as copper or lead. To date, more than 250 REs minerals have been discovered containing REs elements. Nevertheless, the concentrations of REs elements differ, varying from 10 to 300 ppm [3]. The real challenge lies at discovering REs that can be mined and processed economically.

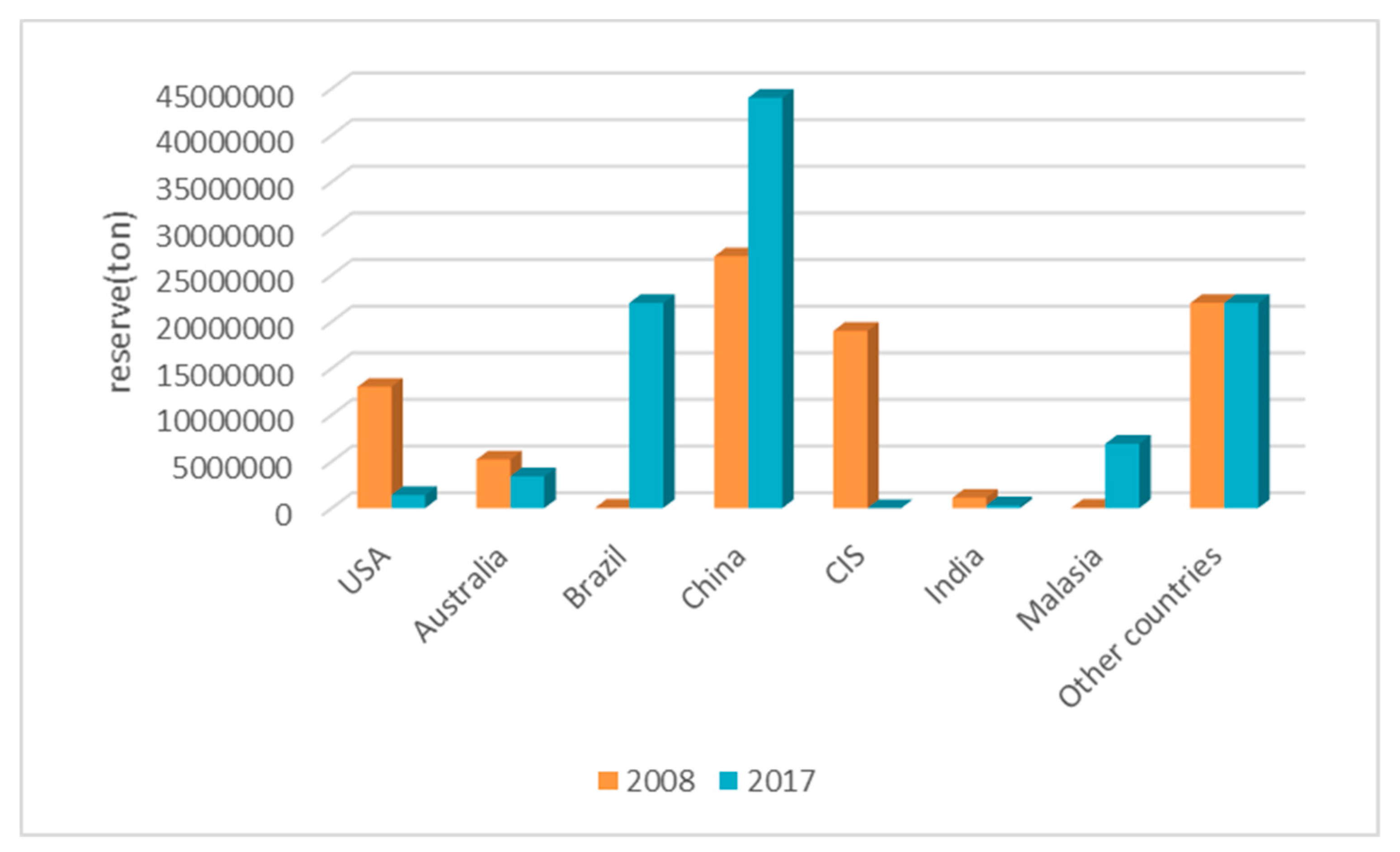

The reason why REs are indispensable and non-substitutable for the emerging technologies is their unique physical and chemical properties. On account of these unparalleled properties, REs have become significantly crucial in many fields. Originally, REs were widely used for traditional sectors, including metallurgy, petroleum, textiles, and agriculture. As the development of knowledge and technologies, a broad and rapidly expanding range of applications that rely upon their chemical, catalytic, electrical, magnetic, and optical properties emerge, especially in many high-tech applications such as hybrid cars, wind turbines, compact fluorescent lights, flat screen televisions, mobile phones, disc drives, and defense technologies, as shown in Table 1. Furthermore, it is their applications in clean energy technologies and defense systems that have brought global attention to REs. Given the growing economic and the persistent strategic importance of these sectors, there is no doubt that continuous access to these resources is strategically important, both in developing and developed countries. However, the distribution of REs all over the world is not even. Figure 1 shows the distribution of REs in different regions.

It is well-known that China possesses the most proven reserves of REs. Concurrently, China is the largest exporter and consumer of REs in the world. With approximately 23% of the world’s total rare earth reserves, China has satisfied more than 90% of the world’s demand for decades [6]. The rest of world has developed a strong reliance upon the exploitation and exportation of China’s REs, including the United States (US), Japan, and the European Union, which makes them concerned about the risk of the supply of REs in view of the dominant position of China in the world market of REs. Especially in 2010, China decided to implement a stringent exportation policy, which directly resulted in the surging of the price of RE products.

Research on the REs from an economic perspective has thrived in the recent decade on account of several reasons. To begin with, the global transition toward renewable energies and a low-carbon economy is an irresistible trend that has been accompanied by emerging technologies that cannot work without REs. Considering that REs currently have no known alternatives or substitutes [7], the world’s attention has grown. Furthermore, the words “Middle East has oil, but China has rare minerals”, which were said by Xiaoping Deng, reveal the political property of REs. This also explains why the rest of the world has ranked REs at the top of critical materials [8,9]. It is certain that REs, along with the resource management of drinking water, oil, and phosphorous (for fertilizers), will be crucial and decisive for the redefinition of the international global balances of the near future [10].

There are a few reviews and books concerning the social, historical, environmental, and technological aspects of REs [3,4,11,12,13,14,15,16,17,18,19,20,21]. Besides, some important reports conducted by countries such as the US, Japan, and India, have focused on the REs industry and supply chain in China [22,23,24,25]. This paper incorporates studies of REs regarding aspects of supply, price, export policy, international trade, relationship with clean energy, and sustainability to form a systematic review of the economics and demonstrate the research progress after the rare earth crisis. The first objective of this article is to explore the publications within the field of economics by carrying out a descriptive analysis, which identifies the numbers, countries of origin, and most popular sources. The second aim is to provide a detailed and holistic portrait of the current literature on the six topics worldwide in the past years. The last aim is to identify possible opportunities for future research, allowing us to advance some future lines of research.

The next section presents the method of the systematic review and describes all the steps taken in detail. Section 3 covers the search and categorization results of the review. Section 4 presents a discussion of the results and points out possible future research trends. Finally, the conclusion is summed up in Section 5.

2. Materials and Methods

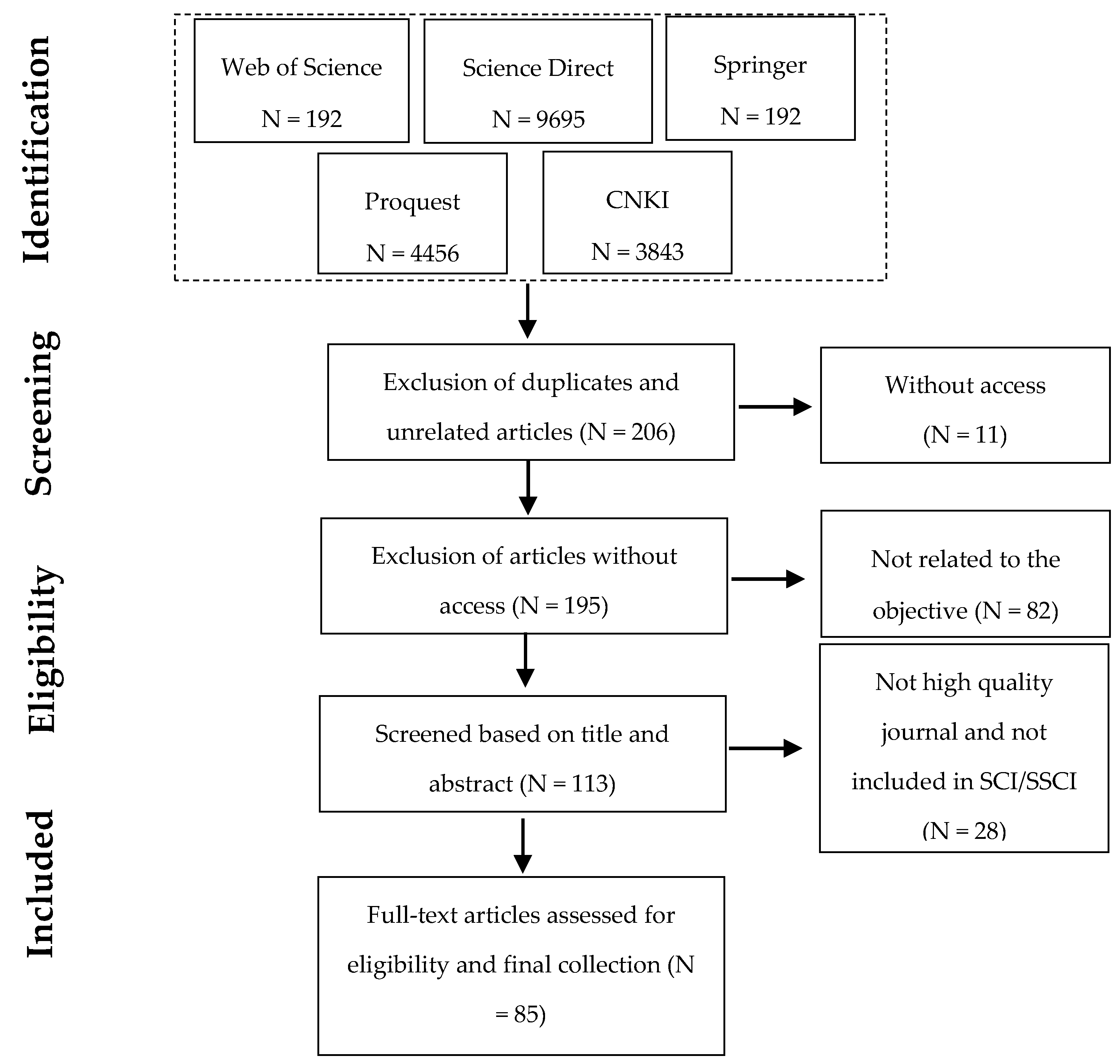

A literature review is a distinctive form of research that aims to facilitate theory development, contribute to closing possible gaps, and reveal areas where further research is needed using existing literature that covers this topic [26]. The objective of this paper is to provide a systematic and holistic portrait of economic research of REs worldwide over the last decade. To this end, a quantitative review based on the bibliometric analysis and a qualitative review through a systematic review in accordance with the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) statement [27], which mainly comprises four steps of literature research, quality assessment, eligibility and inclusion criteria, and studies included in qualitative synthesis of relevant studies is employed (Figure 2). Compared with descriptive literature reviews, a systematic review minimizes the bias in the identification, selection, synthesis, and summary of different studies [28]. A systematic review not only summarizes the results from prior literature, but also explains the differences among studies [29]. Bibliometrics is used in the study of a research topic’s evolution and trends, and applies different methodologies of quantitative analysis to assess the relative importance of publications in a specific field of study [30].

2.1. Literature Research

In order to collect as comprehensive related literature as possible, the Web of Science Core Collection of Thomson Reuters, Science Direct, Springer, Proquest, and China National Knowledge Infrastructure (CNKI) databases domestically and abroad were employed in this paper. Related papers in both English and Chinese were included in the consideration of difference research trends between China and the rest of the world in order to fulfill the intention of drawing a complete portrait of the research nowadays. Commonly used as a source of bibliometric data, the Web of Science Core Collection has had comprehensive coverage of over 3000 journals across 55 disciplines since 1956, and ensures the quality of the literature by using the commonly accepted citation indexing. Science Direct hosts over 12 million pieces of content from 3500 academic journals, and is especially famous for its section of Social Sciences and Humanities. The section “Business, management, and accounting” covers over 100 periodicals and lists potentially important new journals that are not yet included in the citation indexes. Besides, both Springer and Proquest are world-famous database, including plenty of research papers covering many disciplines. The China National Knowledge Infrastructure (CNKI) is the largest database in China for education, publication, and academia, containing almost all the disciplines and research. These five databases cover most of the studies in this field.

“Rare Earth”, “Rare Earth Price”, “Rare Earth Market”, “Rare Earth Policy”, and “Sustainability of Rare Earth” were chosen as keywords so as to search the papers in the field of economics. The article sample selection period was selected from 2009, because the majority of research emerged after the rare earth crisis. This worked as the first filter.

2.2. Quality Assessment

This paper includes original articles, excluding review articles to avoid duplication. Next, abstracts and conclusions were screened to further narrow down the records. In addition, the references cited in the selected papers were also checked, as well as the articles citing our sampled papers.

2.3. Eligibility and Inclusion Criteria

Among the identified pieces of literature, papers went through a stricter and more accurate selection according to the following criteria:

To assure the high quality of selected papers, articles in English were chosen only if they were published in the SCI\SSCI journals, while articles in Chinese were chosen only if they were published in high-quality peer-reviewed Chinese journals (Chinese Core Journals) that have been recognized by the majority.

This paper reviews the economic literature on the REs after the rare earth crisis, so only studies that were published after 2009 of REs regarding the aspects of supply, price, export policy, international trade, relationship with clean energy, and sustainability have been included.

During the selection, articles with no access to the full text were not included.

Most studies included quantitative results; a few articles with qualitative analysis of high value were included as well.

Duplicates studies from different databases were excluded.

2.4. Studies Included in Qualitative Synthesis

After selecting the 85 papers, the process included two different sequential steps. In the first step, the corresponding metadata was imported into Microsoft Excel 2013 so as to undergo a descriptive analysis of the literature on REs in the field of economics such as the distribution of year, distribution of fields, and distribution of countries. In the next step, an in-depth content analysis was undertaken to identify and analyze main research streams, reporting the state of the art of research across different topics and highlighting the possible challenges and opportunities for future research. Content analysis is a research approach to the analysis of documents and texts that seeks to describe and quantify the manifest content of communication in terms of predetermined categories, following a systematic approach, allowing replicable and valid inferences from texts [31].

3. Results

3.1. Descriptive Analysis

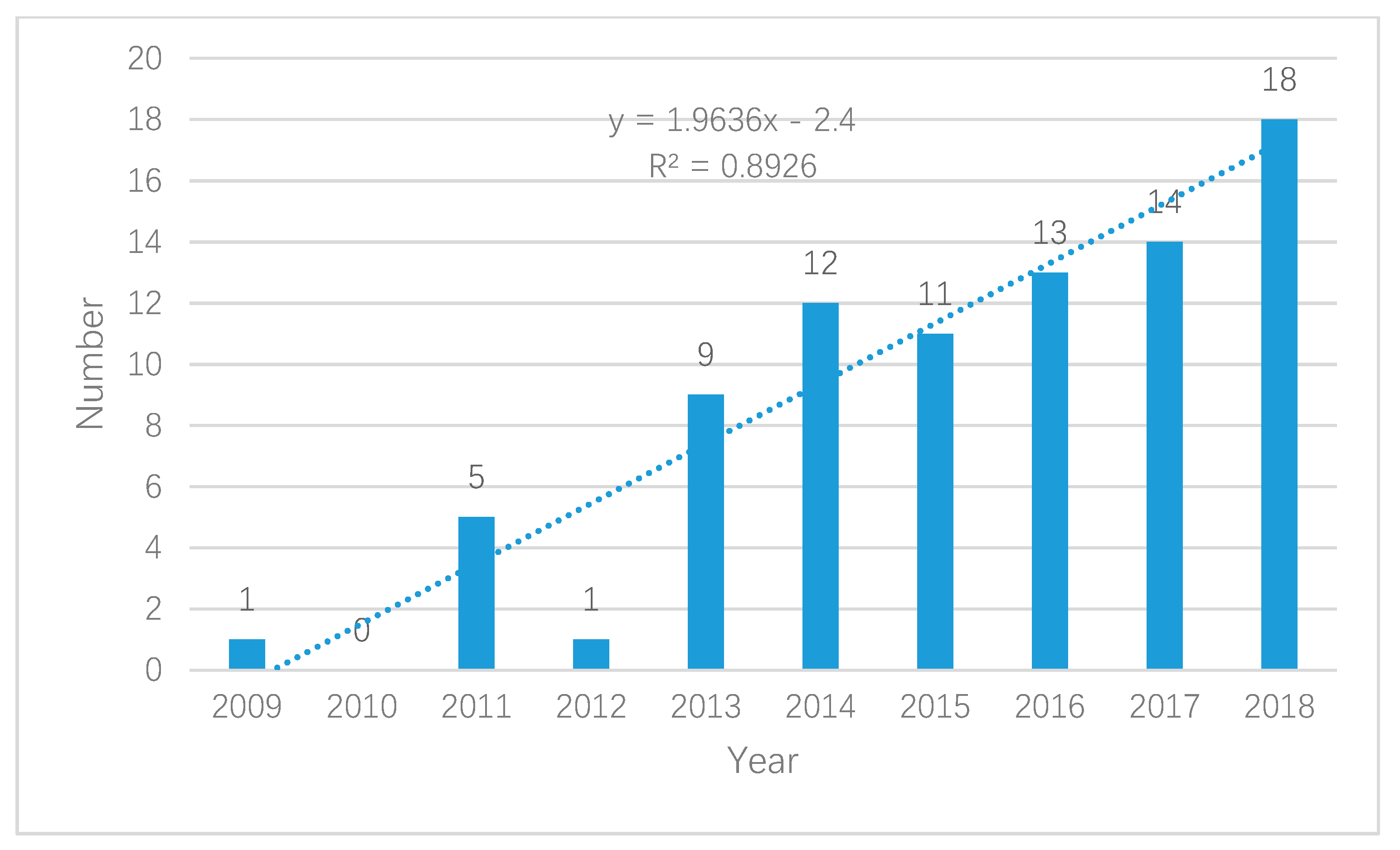

Figure 3 demonstrates the evolution of a number of publications per year on the economic research of REs. Before the rare earth crisis (2009–2010), there was little literature concerning economic research on REs. As time went by, the research in this field has grown steadily between the period of 2009–2018, reaching a peak in 2018. It can be noted that the majority of the selected articles have been published in the most recent years, precisely from 2013 to 2018, representing 92% of the total papers. This trend indicates that the study of REs from an economic perspective has increased significantly over the years.

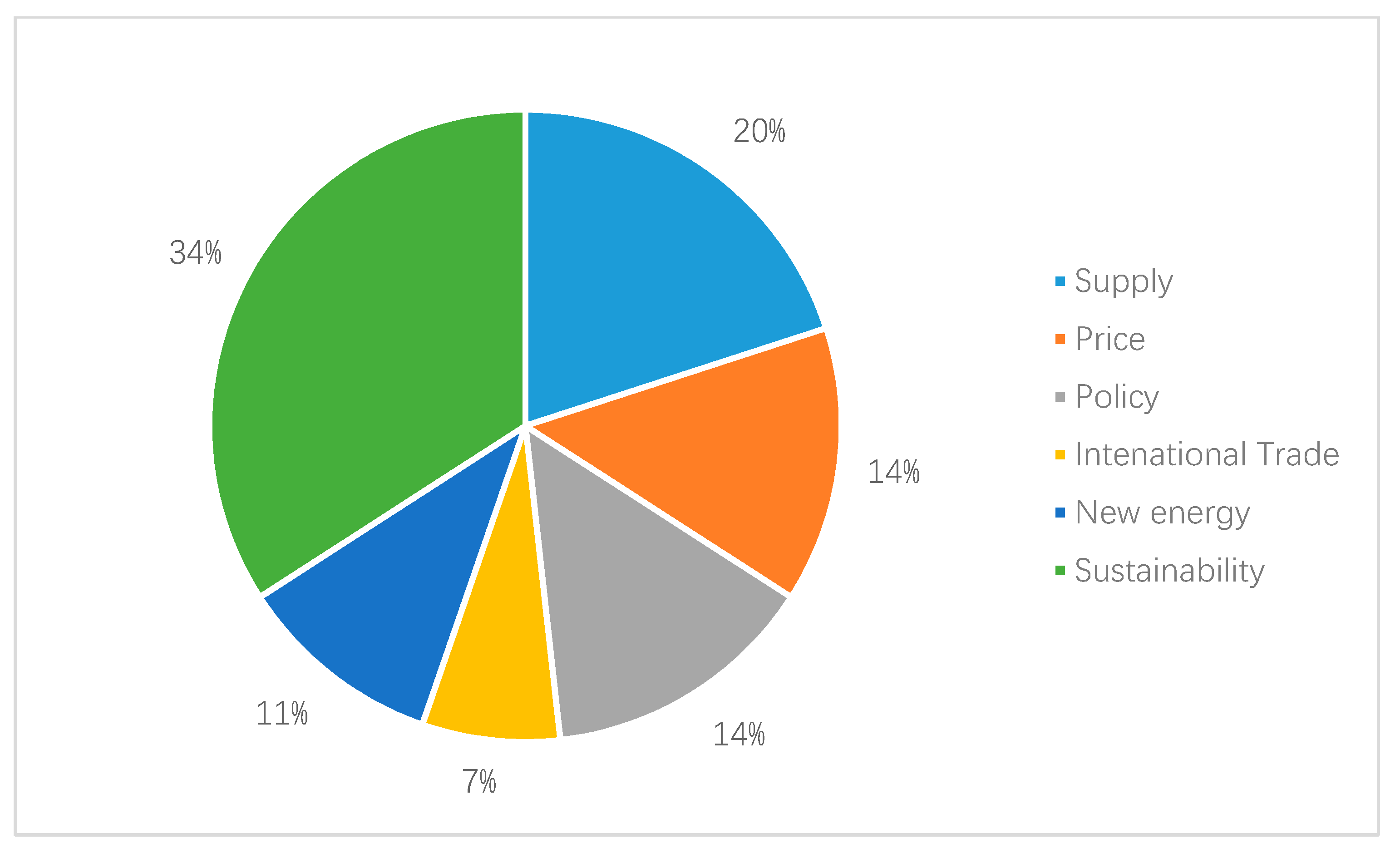

As shown in Figure 4, the main research fields on the economics of REs include research on the supply, price, international trade, policy, relationship with new energy, and sustainability. Among the fields, it is not surprising that sustainability accounts for the largest portion due to the exhaustible situation and irreplaceable position in the modern economy. Moreover, it is worth noting that recently, the number of analyses of REs in the field of renewable energy has increased, which has been a rarely explored field. This may be the result of the shift from the traditional economy to a low-carbon economy, the pressure of environmental issues, and the need for greater energy security. At the same time, concerns about the supply crisis of REs and the policy changes of the Chinese government have drawn the attention of researchers in the fields of policy and supply. In addition, the prices of REs are a key factor that determine the strategies between importing REs from China or investing in exploring other REs resource implemented by the countries outside China. Furthermore, it is also important for many corporations to decide whether it’s profitable to expand production. The field of price is also an interesting field that has a direct influence on international trade.

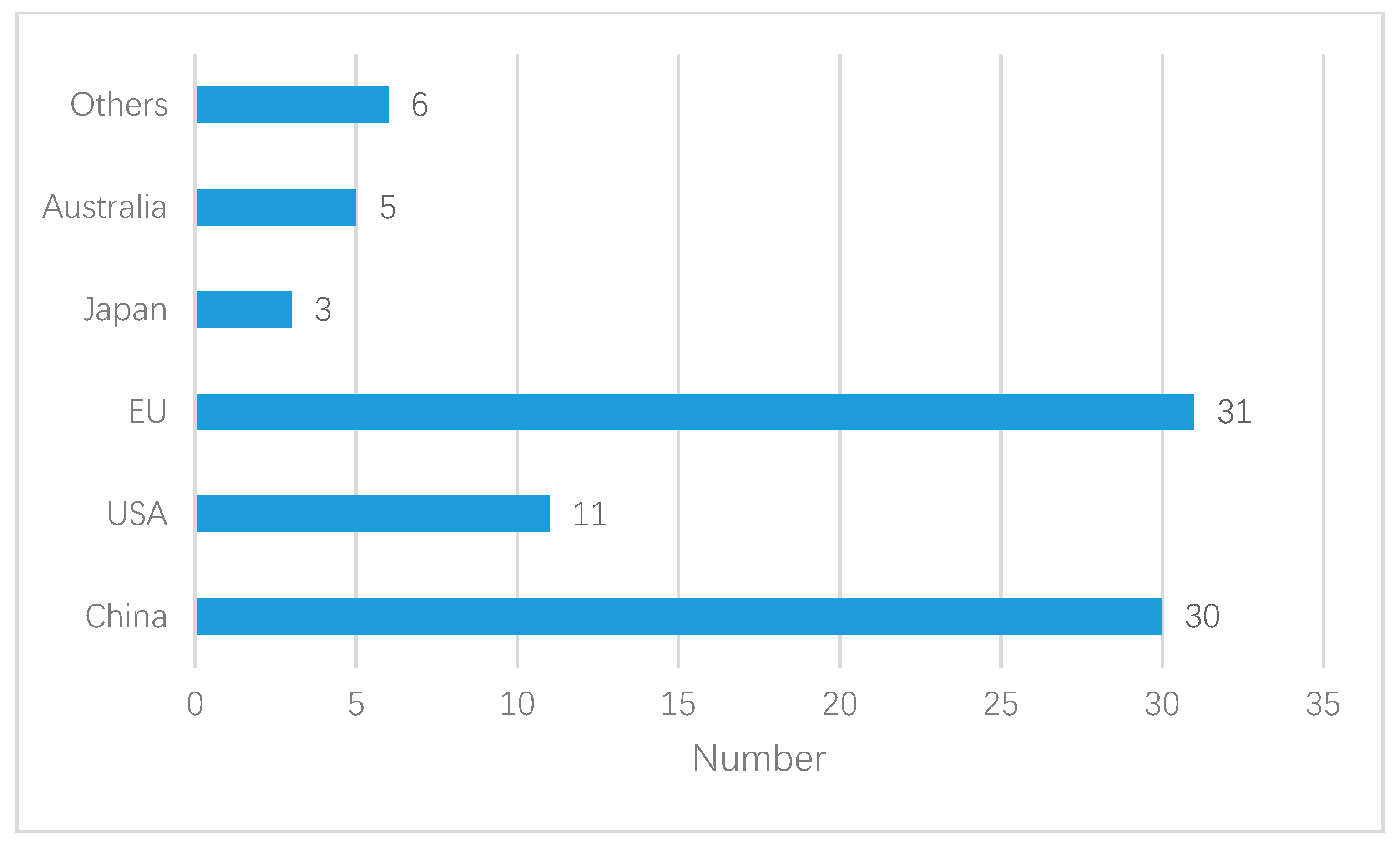

Concerning publications by country, Figure 5 reviews the top six most productive geographical areas. In the ranking, China and the European Union (EU) stand out as the top two countries. China has been the largest producer and consumer of REs, and plays an important role in the world market [32]. In the past years, disputes between China and Japan, the US, and the EU have caught the world’s attention, which makes research on the REs a hot topic. The European Union and the US Department of Energy have categorized RE materials as “critical materials”, while the British Geological Survey has also ranked them on the top of their "Metals Risk List” [8,9]. This seems to be consistent with the research performance of the EU and US in Figure 5.

Finally, as observed in Table 2, the journal publishing the most economic articles on REs in the field of economics is the journal of Resources Policy. The topics of this journal cover the broad discipline of mineral economics, include mineral market and price analysis, project evaluation and real options valuation, mining and sustainable development, mineral resource rents and the resource curse, mineral wealth and corruption, mineral taxation, and regulation.

3.2. Content Analysis

3.2.1. Issues about the Supply of REs

After the discovery of REs in 1794, intensive research in the sciences has been conducted ever since. Over the 20th century, major strides were made in understanding the chemistry and geochemistry of REs on Earth and in the cosmos, based on analyses of REs in meteorites [7]. Research into REs from an economic perspective emerged intensively worldwide after the crisis of REs occurred during 2009–2010.

Before 2009, the production of REs all over the world has transferred to China step by step since the 1980s on account of China’s dominant position in the REs market and the lower cost of the exploitation and process of REs [22]. However, given the non-renewable situation of REs, the deteriorating ecological environment, and the geopolitical dispute with Japan over the Diaoyu/Senkaku Islands, China decided to implement a more stringent export policy and significantly reduce the export quotas [25]. As a consequence, the REs market responded, and most of the RE elements encountered skyrocketing prices. It was not until then that the rest of world realized they developed a strong reliance on China due to its over 90% share of the world’s demand. From then on, increasing focus has been paid to the supply of REs.

After China announced its export quotas on REs, many counties awoke to the worry of whether there would be a supply crisis [33,34,35]. Considering that the shortage of REs could impact a number of industries, Nieto [33] chose to evaluate how critical REs are to petroleum refining through a supply–demand scenario and the key supply factors approach. This helped to understand the vulnerability of industries to price volatility in the US. The reason why petroleum refining was chosen is that the application of REs in fluid catalytic cracking (FCC) units for petroleum refining occupies the largest domestic use of REs (US Department of Energy [DOE], 2011), and FCC catalysts are a refinery’s second highest raw material cost behind crude oil. Instead of focusing on a particular industry, Vikström [34] considered this issue from the foundation of a historical perspective of Sweden. The author analyzed four reports and/or records of meetings from 1917, 1954, 1980, and 2014, which were years when the debate about resource scarcity flourished both in Sweden and internationally. In the author’s opinion, import dependence always played a crucial part in shaping Swedish perception of criticality, and the global political context was of immense importance. China’s dominance in the production of REs was the reason why numerous political and business actors began to fear the crisis. Moreover, a few methods were developed as more interest was drawn to the criticality assessment [35,36]. Jasiński [35] proposed a synergic combination of multi-criteria decision analysis (MCDA) methods to assess supply risks for non-fossil mineral resources. The robustness analysis, considering criteria weight constraints, determined that the REs have a high eventuality of supply chain disruption. In addition, the European Union has been one of the regions that pay the most attention to REs. Rabe [36] examined the dependence of the European Union’s solar and wind industries on the Chinese supply of five critical raw materials: tellurium, gallium, indium, neodymium, and dysprosium, and reviewed China’s industrial policies that shaped the supply of these materials abroad. Moreover, the author also assessed the short-term and long-term strategies of the European Union and European solar and wind industries to ameliorate potential supply bottlenecks, and found the existence of long-term risks of these strategies. Considering the renovation of the energy sector toward using renewable sources and zero-emission transport technologies, Valero [37] proposed a new methodology to identify possible bottlenecks of future demand versus geological availability. The author classified certain materials applied in green technologies as very high, high, or medium. Dysprosium and neodymium were identified as having a medium risk, which meant that the demand might at some point exceed production before 2050. Furthermore, attention was paid to investigate the constraints and opportunities of supply chain. Golev [38] overviewed REs supply chains outside of China, defined their environmental constraints and opportunities, and reflected on a broader range of technical, economic, and social challenges for both primary production and the recycling of REs. In addition, Sprecher [39] conducted research on the supply chain resilience of neodymium magnet (NdFeB) with the help of a novel approach based on resilience theory combined with a material flow analysis (MFA). The results showed that supply chain resilience was composed of various mechanisms, including resistance, rapidity, and flexibility, which originated from different parts of the supply chain, and it was recommended to improve the capacity of the NdFeB system to deal with future disruptions.

Another stream of studies in this field is to make a forecast for the production of REs in China. In 2012, the US, Japan, and the EU brought the dispute with China about its export restriction policy of REs to the World Trade Organization (WTO). It took two years to settle the case, which ended with China’s failure. Consequently, China canceled the export restriction policy in 2014, including the export quota and export tariff. The export license on REs was enforced in 2015, which drove the study of China’s supply trends to become a hot topic of the world. Various researchers have shown interest in the production forecast of China, among which Jianping Ge and Yalin Lei [6,40,41,42,43] have made significant contributions.

Previous research has focused on estimations of the supply and influence of REs, and have mainly been based on experiential judgment of the current and premonitory production capacity for new REs rather than quantitative modeling. Wang and Lei [40] employed the Generalized Weng model, which was a widely used quantitative model in exhaustible resource forecast to predict the production of the three major REs in China (namely, mixed rare earth, bastnasite, and ion-absorbed rare earth) before 2050. Furthermore, in consideration of changes in regulatory policies and the development of strategic emerging industries, it was critical to investigate the scene of RE supplies. Ge and Lei [41] forecasted the production, domestic supply, and export of China’s REs in 2025 by constructing a dynamic computable equilibrium (DCGE) model. From a policy perspective, they found that the elimination of export regulations, including export quotas and export taxes, did have a negative impact on China’s future domestic supply of REs. There are many models that can be applied to forecast the production of specific resources, whereas quantitative results differ from model to model on account of the disadvantages and advantages of different models. Table 3 shows the scope, advantages, and limitations of the applications of common models.

In the context of China strengthening its protection of RE resources and the environment, the rest of the world immediately took action to alleviate the Chinese domination in the REs sector. Countries with resources of REs have ramped up their domestic production of REs (e.g., Lynas Corporation, Australia). Countries without resource endowments have launched different projects. The European Commission has launched the “European Raw Materials Initiative” enforcing deeper links and cooperation contracts with other producing countries, particularly in Africa, to relieve the pressure of China’s decrease in RE exports [44]. The Japanese government has launched the support task “Reduction and replacement of rare earths and rare metals” in 2011, and companies that test low-dysprosium (Dy) NdFeB magnets have increased [45]. A series of papers aiming to examine the results of different programs and come up with different strategies for a stable supply of REs in different regions has appeared.

Japan controls about 23% of the global NdFeB supply [45]. Dysprosium (Dy) is an important component of advanced magnets that perform in high-temperature environments (around 200 °C) by raising their coercivity. It is also a heavy rare earth element (HREE) that is mostly found in ion adsorption, and is hardly found except for in southern China [45]. This situation poses a great risk to the supply of Dy. Seo [45] compared the effectiveness of two different strategies for reducing total demand for Dy in Japan during the period 2010–2030: development of low-Dy REE (NdFeB) magnets and a program to promote the recycling of REE magnets. The author found that the strategy of low-Dy magnet development would be much more effective at reducing Dy demand than promoting recycling. However, in the long term, both strategies should be pursued in a balanced approach. The potential impact of the re-emerging REs industry in the US on the future global supply and demand trends of REs was also explored by He and Lei [42] using the documentary research method after the US government announced the resumption of the production of domestic REs ores in 2012. Nonetheless, the global demand of HREEs, including the U.S., will still rely on China’s supply. Machacek and Kalvig [46] examined the proposed product volume supply of RE elements from six advanced RE-bearing mineral exploration projects, two of which were in Greenland, for RE demand by industrial users in the EU. Jamaludin [47] investigated whether Lynas could make a difference in the global political economy of REs elements in the future. The author argued that Lynas’ initiatives to expand REs production had merit for REs’ global market equity; however, the efforts were small compared to the production of China.

Comparing mining and resource recovery projects requires consideration of a range of complex parameters, including the geological profile and in situ value of resources, the technical feasibility of the project, the ecosystem’s sensitivity to and environmental impacts from main operations, potential social risks, and local community confrontation [38]. Thus, a better understanding of these projects and factors could help optimize the supply chain. Besides, different countries have different resource endowments; it’s crucial for resource-rich and resource-poor nations to respond differently to the supply problem. Europe has opted for policy dialogue with resource-rich countries, whereas Japan and the United States have a more hands-on approach in research and development initiatives. Meanwhile, Australia’s and China’s policies instead focus on the development of domestic mining activities and resource protection [48].

Supply and demand theory is the fundamental analysis of economics, whereas the existing literature mainly focuses on the supply side, and not much of the demand side [49,50]. The reason why there have been only a few papers that have explored the demand for REs is mainly because it is a rapidly changing market due to the fast progress in science and technology. Every extended application of REs can make a huge contribution to the consumed amount, which makes the forecast of the demand less meaningful in the long run. Generally, it’s well accepted that the demand of REs will increase in the future due to the transition toward low-carbon energy production, renewable energies, and a green economy in order to reduce climate change. Global demand for REs is slated to grow at an annual rate of 5% by 2020 [51].

3.2.2. The Price of REs

After the rare earth crisis, plenty of research has been devoted to the supply crisis. Concurrently, the prices of REs have experienced significant volatility (Table 4), which makes it a hot topic of world interest.

In order to alleviate the pressure of China’s dominance in the REs market, the rest of the world has developed mining projects outside China. It is said that there are about 200 projects on REs exploration that are under preparation and exploitation [52]. Nevertheless, the mining projects require vast investment, and many of them failed when the prices of REs fell. Hence, it’s of great value to forecast prices of REs for investors and policymakers, which leads to the strand of research on the forecast of the prices of REs.

In this field, limited research aiming at forecasting the prices has been conducted [53,54,55]. The method is confined to common time series, such as for example the autoregressive integrated moving average (ARIMA) model. Yang [53] adopted an ARIMA (1, 1, 2) model to describe and forecast the dynamic fluctuation of the price of REs neodymium oxide and dysprosium oxide. The prices of neodymium oxide and dysprosium oxide were forecasted and compared with the real values from 2006 to 2015. The results were of high accuracy, indicating the ARIMA (1, 1, 2) model was suitable for the forecast of prices in the medium and short term. Riesgo [54] applied autoregressive (AR) and moving average (MA) models to forecast the prices of dysprosium oxide in the first place. To achieve a more accurate forecast of dysprosium oxide prices by eliminating the anomalous phenomenon, the author considered the transformed historical prices as the DNA of the time series due to its similarity to a gene sequence. Riesgo [55] developed the theory of transgenic time series and applied it to the forecasting of several REs oxide prices, including: dysprosium, europium, terbium, neodymium, and praseodymium oxides. In addition to the forecast of price, Yang [56] noticed that the prices of RE products in China fluctuated periodically. The author used the X12 seasonal adjust method and the H-P (Hodrick and Prescott) filter model to analyze the periodic fluctuations of their price empirically, and acquired the periodic fluctuations of REs prices and products in the period from February 2006 to December 2014. The results showed that prices of REs oxide products experienced two periods during the test period. In consideration of the huge fluctuation of REs products prices in 2011, it was estimated that there would be a long-term fluctuation period, and the wave of the second fluctuation period of RE products would last for more than 43 months. Many different methods have been used to forecast the prices, and each one possesses diverse advantages and disadvantages. It’s worth applying other methods in the field of forecasting prices to help us understand the changes in price comprehensively.

In contrast to the research outside China, domestic researchers have been devoted to exploring why China has lost its pricing power in the REs market. Although it is well admitted that China has a monopoly position in the world market, China has failed to turn the monopoly advantage into profit. A lack of pricing power seems to be an important reason for this paradox.

There is plenty of literature involved in this topic studying the paradox [57,58,59,60,61,62,63,64]. Song [57], Yu [58], and Liao [59] investigated the reasons for this paradox. First, the excessive and disorderly and illegal exploitation of REs in China leads to the oversupply and low price of REs. Second, domestic RE enterprises are relatively scattered and the concentration of the RE industry in China is low, which makes it impossible to form a pricing alliance. However, exporters such as the US, Japan, and the EU, which account for over 80% of China’s exportation, have a strong market influence. Some papers mentioned that they often grasp the dominant and pricing power of REs in the international market through their own or joint ways [57,59,60]. Third, China lacks competitiveness in the world market of RE production even though China is the largest producer and exporter in the world, since the products are of low added value. The technologies required for high-end REs products are weak, and the innovation is insufficient, which to some degree restricts the acquisition of pricing power. A few authors have investigated the topic empirically. Based on the model of Knetter [61] and the Lerner index, Fang [60] confirmed the existence of the paradox and proved that China had limited market power only in Hong Kong, Indonesia, and Thailand among 17 export countries. Sun [62] analyzed the micro trade data, and found the market power of China RE exports was quite weak through empirical methods. Yu [63] manifested that the rise in the price of China’s RE exports did not indicate the rise of its international pricing status, considering the production and reserve status, price terms of trade, and business indexes. Zhu [64] developed the SMR model to study the international market power of China, and found that China lacked market power in the international REs trade export market. In addition, Deng [65] analyzed some Western developed countries’ successful experiences in seizing the commodity pricing power of metal, oil, and grain. The author suggested improving industry concentration, setting up a cartel system, developing an international pricing center, and establishing a national storage system to enhance China’s pricing power.

3.2.3. The Export Policy of China

As the largest producer and exporter of REs in the world, China has satisfied more than 90% of the world’s demand for decades [6]. There is no doubt that the policy of China on the production, exportation, revenue, stockpile, and industry of REs will significantly affect the RE market, which has attracted a deal of attention in this field domestically and abroad.

The attitude of the Chinese government toward REs has changed from encouraging exploitation to protection from a historical perspective. Back in the 1980s, China adopted positive policies to facilitate the exploitation with the guideline of “large mines deserve large-scale exploitation, small mines deserve small-scale exploitation” so as to exchange the resources for technologies and capital with developed countries. Leading by this guideline, RE resources suffered from predatory mining, which resulted in a chaotic situation of production. This chaos lasted for years, and it was not until stepping into the 21st century that China realized the importance of REs for the emerging technologies and the serious damage that the mining of REs has caused to the ecology. Afterwards, China amended a series of policies to protect the resources. Table 5 shows the evolutions of China’s RE export policies.

The frequently altered policies have inspired many scholars to evaluate the policy effects [6,43,65,67]. The main policies involved are environmental and export policies. Han [6] built a static game-theoretic model to analyze the resulting effects on firms at home and abroad in different scenarios where China abolished export restrictions, enhanced resource tax, and levied an environmental tax. Zhang [66] used the Lerner index and back propagation (BP) neural network to examine whether China’s REs export policies work. He [67] examined the effect of China abolishing the export rebates in 2005 using the DID (Differences-in-Differences) method. Considering China was particularly susceptible to ecological destruction, water pollution, and soil erosion, Wang [67] constructed a computable general equilibrium (CGE) model to investigate the market impacts of environmental regulation on the production of REs in China, with three scenarios used to simulate the different environmental regulatory intensities that the Chinese government might adopt in the near future. It was estimated that the domestic supply of REs was 168,000 tons in 2016, but the national quota was 105,000 tons. The conservative estimated number of illegal exploitation was 63,000 tons, accounting for 60% of the legal supply. This portion of the market has attracted little or no attention to the environmental damage of their mining actions, which depresses the market price such that external (and in some case internal) producers are having difficulties making or maintaining profit margins. Illegal mining, and the subsequent environment and economic implications of unregulated ionic clay RE mining, were investigated [68].

Furthermore, some scholars explored why China implemented export quotas and tariffs on REs and how the state is engaged in this sector domestically and abroad in view of the discriminating policies between domestic and foreign demand [69]. The main purpose of government is to lay the foundation for three other goals, namely: the establishment of integrated and innovative Chinese corporations that compete globally; the provision of incentives to attract high-tech foreign direct investment to China; and better environmental protection. Brown [70] developed a three-actor Stackelberg model of coproduction, and applied it to RE markets to explore the effects of Chinese RE stockpiling, environmental taxation, and improvements in recovery rates on RE markets. Through examining three narratives, Wübbeke [71] argued that the major driving motives of the changes of Chinese policies were domestic concerns for resource conservation and environmental protection, as well as the development of competitive downstream industries. In addition, in order to investigate how the policies affect the supply chain differently in China compared to the rest of the world, Mancheri [72] analyzed various policies (restrictions on trade between China and rest of world, Chinese influence on RoW supply chain, and the dynamics inside the Chinese supply chain) and focused on how prices responded to various resilience influencing mechanisms such as diversity of supply, legal and regulatory frameworks, and stockpiling. The results showed that the supply chain was a complex phenomenon, and the resilience of a system was not solely dependent on physical disruptions, but also on dynamic factors, including societal and geopolitical factors.

For years, the China’s reserve of REs remained first place in the world; however, the share has been declined. China accounted for 74% of the world’s total reserves in the 1970s, but the number dropped to 69% in the 1980s, and then in the 1990s, it was 45% [73]. It was reported that the proportion came to 23% according to the 12th Five-Year Plan white book of China’s RE conditions and policies. China is losing its non-renewable resources due to a lack of strategic arrangement. Furthermore, enough emphasis has been stressed on the environmental pollution caused by the exploitation and process of REs. Producing one ton of RE elements can make 60,000 m3 of waste gas that contains hydrofluoric acid, 200 m3 of acid-containing sewage water, and 1 to 1.4 tons of radioactive waste [5]. As a consequence, China lost the case and declared that it would cancel its export restriction policy, including the export quota and export tariff, in 2014. A few scholars suggested that China should implement a resource tax in place of the export tariff in order to alleviate the increasingly serious pollution situation. Wan [74] constructed a three-country trade model with an environmental damage function in order to examine the effects of three policies with different implications for the equilibrium quantities of dirty inputs and clean technologies: a downstream subsidy, an upstream export tariff, and an upstream pollution tax. The results of simulations suggested that the country could be better off if it significantly taxed the production of its resource, instead of using an export tariff, at least partly, as a strategic trade instrument. Ge [75] investigated the evolution of the resource tax and examined the effects of resource tax adjustments on the production and demand of REs through using a computable general equilibrium (CGE) model. Yang [76] investigated the effect of the resource tax on REs on their price under different tax rate schemes and different methods of tax collection with the method of a system dynamics approach that considered the price of REs and its influencing factors as a linear dynamic system. It was found that a resource tax that was calculated in accordance with the price of REs could better reflect the value of the resource tax regarding the price of REs and solve the negative externalities of REs resources in the process of mining. However, besides these articles, there is limited research in this field, and it is of great potential and value. It’s imperative to determine a reasonable tax rate on RE resources for the Chinese government. Furthermore, upon facing losing a reserve of resources and increasing industrial position, a stockpiling policy is of tremendous importance for healthy development. However, it requires more quantitative research on the scale of the stockpile, as well as more systematic policy.

3.2.4. International Trade of REs

The dispute between China and the rest of the world on RE resources has remained for a long time, and the WTO case caught the world’s focus. With the settlement of the case in 2014, some research is interested in investigating whether the announcement of a WTO dispute resolution case has the power to fundamentally change market dynamics. Through variance ratio tests and structural change tests, Proelss [77] found that RE prices exhibited a structural break around the announcement of the WTO dispute, and showed lower variance ratios for all tested REs afterward. Furthermore, the author found that the stock price informativeness of companies in the RE industry increased after the announcement, and the model uncertainty for option pricing models decreased. The other existing literature mainly focuses on the role of China in the world trade, including factors that may affect the world trade and world trade patterns [78,79,80,81,82] in consideration of China’s dominance in global RE reserves and production.

To investigate the influence of factors between China and the rest of the world on international trade, a gravity model has been widely applied in this field. The most concern is involved with institutional factors. Based on the Index of Economic Freedom from the Heritage Foundation, Pan [78] explored the effect of institutional distance between China and other 18 countries. Wei [79] introduced the institution variable into the gravity model to estimate its export potentials in an attempt to explain the underlying reasons for trade friction. Mancheri [80] focused on the Chinese export restriction and used the case of RE elements to evaluate Chinese export restrictions, reviewing China’s current monopoly over the industry and providing insights on how widely traded these minerals were and China’s position in international trade in terms of both volume and value. Recently, the patterns and structure of RE world trade have turned into another concern of researchers, and the complex network has become a popular method in this field. With the complex network method, one can investigate the relationship between countries and divide trading countries into several communities. Moreover, through conducting a series of different dimensions indices, such as degree centrality and strength centrality, we can explore the role that each country plays and the status of trading countries. Ge [81] used the complex network theory to analyze the world RE trade based on the trading data for 2011 to 2015. Hou [32] constructed an international RE trade network based on complex network theory to analyze the distribution of trading countries, the overall structure of trade, and the major countries and communities of the network.

With the settlement of the WTO case, the dispute between China and the rest of world seems to have come to an end. Nonetheless, the uneven distribution of RE resources makes the market structure and world trade more complicated. For years, the rest of the world has made efforts to change the monopoly position of China in the market. Enormous investment has been incentivized to explore the new mine resources; as aforementioned, there was around 200 mining projects outside China. Although many projects failed due to reasons varying from environmental concern to lack of investment, plenty of projects survived. Table 6 shows the major RE projects outside of China. It is believed that China can still retain its monopoly position for years because both mining and supply chain development require significant lead times [78]. However, with the finish and production of other projects, the world supply situation may be affected, which would subsequently affect the world trade situation considering the rapid decrease in the reserves of China. The world trade relations may be altered and need further research for the stable and healthy development of the industry.

3.2.5. Research about the Relationship with Clean Energy

To reduce the adverse effect of climate change and greenhouse gas emissions, enormous attention has been paid to the clean energy sector over the past 10 years. At the same time, investment in the clean energy segment has increased dramatically, which has contributed to the sector becoming one of the fastest-growing sectors. Recent estimates from the New Energy Finance (2016) suggest that the amount of money invested in renewables in 2015 has reached a new high of $285.9 billion [83].

The RE elements have wide applications in the clean energy technologies such as hybrid electric vehicles (HEVs), wind energy, and high-efficiency lighting, owing to their unique magnetic, optical, and catalytic properties. When added to autocatalysts and fluid catalytic cracking, La and Ce can transform heavy molecules into lighter compounds, increase gasoline output, and reduce emissions. Dy helps NdFeB, which constitutes a very important component in wind turbines and all-electric vehicles, increase the value of intrinsic coercivity and resistance to demagnetization, thus allowing the NdFeB magnets to be used at higher temperatures. Yttrium is mainly used in phosphors, which is the most important of its uses in the volume and the high demand for compact fluorescent light. Table 7 shows the common uses of different REs elements in clean energy and their level of criticality.

It’s widely accepted that REs play an important role in clean energy, but there are more problems that remain unsolved. The importance of REs to clean energy was illustrated and the main problems regarding REs, such as substitution, recycling, and environmental problems, have been pointed out [85]. Furthermore, by comparing the reserved RE resources, which was reported as 478 megatons (Mts) of RE oxides (REO), with REs demand from clean technologies, which was estimated as 51,900 metric tons (kt) of RE oxides in 2030, Zhou [86] proposed that Nd and Dy would strongly influence the development of exploring new REs projects and clean technologies in the next decades. Stegen [87] also sounded the alarm that a significant build-out of efficient lighting and renewable energy technologies might be endangered by shortages of REs and rare earth permanent magnets. Through four modeled scenarios, Habib [88] revealed that a Business As Usual Development (BAUD) projected primary supply was unable to meet the forecasted demand of Nd and Dy, and recycling did not seem to be in a position to close the wide gap between future demand and supply by 2050, which was mainly due to the long lifetime of key end-use products by 2050. Instead of treating REs as a whole, some scholars investigated the relationship between clean energy and one of the RE elements. Hoenderdaal [7] found that dysprosium demand would probably outstrip supply in the short term (up to 2020). Zhang [89] reviewed current yttrium supplies from the south and north of China, which accounted for the overwhelming majority of total world supply in the short term, as well as the potential resources outside of China, which might reduce the supply risk of yttrium in the long term. The review found that the supply of yttrium was not likely to be disturbed by the price changes of other co-products, because yttrium’s content was high in the ion adsorption clays in south China. While in North China (Baiyun Ebo), RE elements were usually produced as a by-product of iron, because the content of yttrium is lower. In the US, yttrium should be considered as a critical mineral for the US economy based on yttrium’s supply risk and importance to its uses. Besides, Apergis [90] focused on the long-run relationship between RE prices and the consumption of energy from renewables. The results denoted that in the long run, RE prices drove energy consumption for renewables in the majority of regions. A negative relationship between REs’ material price changes and the stock market performance of some clean energy indices was found using a multifactor market model from the perspective of finance [91].

3.2.6. Sustainability

The sustainability of REs has been the focus of study in recent years due to their contribution to the modern industry, environmental issues, the reality of REs as exhaustible resources, and the distorted structure of the international market. A “sustainability evaluation” for each element, including essential data about markets, applications, recycling, and possibilities for substitution has been summarized and analyzed [92]. Several studies have investigated the topic from the perspectives of different countries based on their resource endowment, financial perspective, resource governance, scarcity, and importance to the economy [10,93,94,95,96,97,98,99,100]. A few types of research have focused on the material flow analysis of REs and some other researchers have explored the damage to the environment related to processing and exploiting REs.

Massari [10] qualitatively illustrated the current situation of international markets, the availability of these strategic resources, the possibilities for substitution and recycling, and the possible solutions that could enhance the future supply security for the European countries. Schlinkert [93] introduced a clear and structured economic model that consisted of a sequence of four supply and demand models that gave explanations as to how the mining and separation step of the REs’ value chain could be concentrated in China. Furthermore, the sequence provided a coherent scenario for the future development of the REs market. The validity of this scenario was discussed and evaluated from the perspective of western countries, investors, and China. Zhü [94] provided an ANP-SWOT (Analytic Network Process and Strengths, Weaknesses, Opportunities and Threats) approach for an interdependent analysis that prioritized the REs industry in China. The internal and external environment factors, five short-term strategies, and four long-term strategies were analyzed to determine the optimal strategy for a REs industry development plan. The results showed that the protection of key resources and the integration of appropriate mining were the best short-term development strategies for China’s REs industry and the best long-term strategies were establishing a national strategic reserve system of REs and improving the technical innovation capacity. Charalampides [95] suggested that the EU would have to employ alternative measures to secure their supply of REs by adopting an admixture of trade policies, industrial adjustment, innovation, and budget allocations in the member states in order to limit their dependency on RE imports.

Rollat [96] proposed a forecast of certain RE flows in Europe at the 2020 horizon, based on an analysis of trends influencing various actors of the REs industry along the value chain. The results indicated that a significant shortage of REs supply in Europe at the 2020 horizon was not anticipated considering the balance between supply and demand, barring any new geopolitical crisis involving China. Machacek [97] developed a global value chain (GVC) framework to provide an understanding of value-adding segments of REs in their transformation from mine to market, and depicted the strategies of three Anglo-REE deposit developers (Molycorp, Lynas, and Great Western Minerals Group) who sought to establish alternative supplies to the dominant Chinese REs industry. Pavel [98] evaluated the substitution options for the REs permanent magnet-based wind turbines at the material and component levels to show that substitution has a real potential to alleviate the pressure on the supply of REs in the wind industry. Silva [99] introduced a new methodology of competitiveness analysis in mining with a focus on the REs mineral sector to examine the factors that had a great influence on the competitiveness of the RE projects in development, especially in Brazil. The results uncovered some real facts such as the resilience of the Mount Weld CLD Project (AUS), the weaknesses of the Mountain Pass Project (USA), and the competitive advantages and disadvantages of the best-classified project in Brazil.

Through analysis of a comprehensive set of data and demand forecasts, Ali [100] presented an interdisciplinary perspective on how best to ensure an ecologically viable continuity of global mineral supply over the coming decades. The author suggested that new links were needed between existing institutional frameworks to oversee the responsible sourcing of minerals, trajectories for mineral exploration, environmental practices, and consumer awareness of the effects of consumption. To study whether future generations possibly face a depletion of specific metals, for which metals, and to what extent the extraction rate would need to be reduced, Henckens [101] proposed an operational definition for the sustainable extraction rate of metals and divided 42 metals in four groups according to their geologic scarcity. The results showed that REs were not scarce. Koning [102] estimated the required extraction of metals until 2050 under several technology-specific low-carbon scenarios, and found that annual metal demand for the electricity and road transportation systems might rise dramatically for neodymium and dysprosium, by factors of more than three orders of magnitude.

In addition, some scholars examined the issue from a higher perspective, focusing on the financial performance and the systematic problems of the RE market in the world and the dilemma of choice between implementing alternative strategies and recycling the end-of-life applications. Fernandez [103] offered a historical perspective of the RE market by constructing and analyzing a time series of consumption, production, and oxide/metal prices, and provided a financial perspective of the RE market by presenting the evolution of market capitalization of leading REs companies, gauging the systematic risk of mining firms involved in the production and processing of REs worldwide, and measuring the co-movement of RE prices/indices with well-known commodity indices. The results discovered that the total market capitalization of RE companies was mostly driven by Chinese companies, and that REs oxide/alloy price returns generally displayed a positive correlation with commodity indices returns. Furthermore, the systematic risk of RE companies depended on the approximation to the market index, and might be riskier than the average S&P 500 constituent. Klossek [104] examined these distortions of the RE market with a systemic approach, and found that the systemic problems included competing for political–economic models, resource nationalism, market opacity, a lack of trust, weak cooperation, and short-term versus long-term approaches and profit orientation. These problems were interconnected and amplified each other. Then, four possible solutions were discussed accordingly. Lee [105] developed a game theoretical methodology that incorporated competition for limited resources to explicitly model a firm’s valuation and its decision regarding whether to adopt environmentally sustainable strategies. Furthermore, the author used a sample of firm-level data from the KLD (Kinder, Lydenberg and Domini) database, which includes firms’ sustainability policies, to find empirical support that competition for resources is positively correlated with a firm’s adoption of environmental strategies. An operation and inventory management strategy was developed to explore the profitability under uncertain market supply and with varying component/material values whose demand also faces significant uncertainties [106]. McLellan [107] reviewed four key areas of sustainability in the REs industry: technical, environmental, social, and economic. The author highlighted a broad range of areas needing consolidation with future research, and called for collaboration between industry and academia to understand the sustainability considerations of these critical elements in more depth.

Another hot topic in this stream is the material flow analysis. The material flow analysis (MFA) is a systematic assessment of the flows and stocks of materials within a defined system in space and time [108]. Application of the MFA approach to REs has highlighted the relative paucity of available information regarding the content of REs in products and content heterogeneity [109]. As a consequence, an increasing number of studies aimed at measuring the RE contents in various waste materials of different countries has emerged. Chen [110] provided SFA (Substance Flow Analysis) and generalized entropy analysis for neodymium in China in 2002 and 2011. Neodymium flow amounts and its generalized entropy value were calculated, respectively. The results demonstrated that the utilization efficiency of neodymium in the RE concentrates’ production stage increased by more than 69%, while the utilization efficiency of neodymium in the manufacturing stage increased by more than 28% in 2011 compared to 2002. The generalized entropy results indicated that the congregated degree of neodymium was larger in 2011 compared to 2002 after the concentrate production stage and manufacturing stage; the congregated degree increased by 45.5% and 12.5%, respectively. To solve the problem of the indirect effect and the network characteristics of REs, Wang [111] built an embodied RE network by combining both input–output analysis and complex network theory. The author found that an embodied REs flow network could reveal the small-world nature characteristics, and the chemicals and scrap sectors were the strongest sectors that benefited from direct effects, indirect effects, and intermediate effects based on a comprehensive analysis of the network’s degree centrality, eigenvector centrality, and betweenness centrality, respectively. Furthermore, the related sectors of infrastructure construction and the petrochemical industry were the focus of the establishment of embodied RE flow relations based on the analysis of each sector’s weighted edges that carry embodied RE flows.

Lee [112] investigated the material flow of terbium in 2011 using the integrated material flow analysis methodology (IMFAM), which combined the advantages of the top–down and bottom–up methods and overcame the limitations of each method in Korea. Guyonnet [109] explored the flows and stocks, at the scale of the European Union, of certain RE elements (Pr, Nd, Eu, Tb, Dy, and Y); the results provided estimates of flows of REs into use, in-use stocks, and waste streams. The results estimated that flows into the use of, e.g., Tb in fluorescent lamp phosphors, Nd and Dy in permanent magnets, and Nd in battery applications, were 35 tons, 1230 tons, 230 tons, and 120 tons, respectively, for the selected reference year 2010. Meanwhile, the amounts of Tb in fluorescent lamps and Nd in permanent magnets recycled each year in Europe could be in the order of 10 tons for Tb and between 170–230 tons for Nd. Swain [113] investigated the material flow analysis of neodymium, as well as the status of RE elements in the Republic of Korea. The author suggested that the recycling of end-of-life neodymium-bearing waste could be a feasible option to bring neodymium back to the supply stream. Shigetomi [114] examined specific economic drivers affecting the global flows of three critical metals: neodymium, cobalt, and platinum. The results revealed that economic scales, such as gross domestic product (GDP) per capita and population, as well as the distance between two regions, were statistically significant in terms of the global neodymium and platinum flow. Peiró [115] employed a material flow analysis (MFA) of the complex interrelationships between scarce metals. Nansai [116] quantified the global transfer of three critical metals (neodymium, cobalt, and platinum) that were considered vital for low-carbon technologies by means of material flow analysis (MFA), resolving the optimization problem to ensure the material balance of the metals within each country and region.

To achieve the development goal of REs, there is also another barrier to the sustainability of the REs industry: environment pollution. The biggest problem of REs, besides the low concentration of resources, is that these minerals are associated with radioactive elements (particularly thorium and uranium), which requires expensive mitigation measures to ensure adequate environmental protection and workers’ safety [8]. To date, most studies remain at the stage of qualitative research, because it is much more difficult to identify accurate quantitative figures on any environmental aspect of REs [108]. In order to solve this problem, future research requires interdisciplinary knowledge; for example, Yu [117] evaluated the environmental cost of REs refining in Baotou from 2000 to 2013 by the method of environmental abatement cost in order to provide scientific reference for the policy design of REs’ environment protection. Ma [118] quantitatively assessed the ecological and environmental cost of the exploitation of RE resources in three major production bases in China from 2001 to 2013 with remote sensing images.

It can be predicted that over the long term, some other technologies may be able to be substituted for REs in many current uses, such as for example in nanotechnology. However, in the near future, REs still possess an important position in the modern industry and economy. Therefore, the sustainability of REs remains an austere issue. It is worth noticing that sustainability research is transforming into a more transdisciplinary and heterogeneous form, often working at the science–policy–practice interface [119].

4. Discussion

This study contributes to the literature by providing an elaboration of a descriptive mapping of the existing literature on the studies of REs regarding the aspects of supply, price, export policy, international trade, relationship with clean energy, and sustainability to form a systematic review on the economics. The background and development process of research are also sorted out to present a better understanding of the research. Through merging the existing literature and dividing them into six categories, this paper offers a systematic and holistic portrait of the economic research of REs worldwide after the rare earth crisis; however, this article still has limitations. First, as it is often the case with qualitative research, subjective factors play a role. The development of the framework in this study is such a case. The researcher’s subjective evaluation of the articles when determining the areas and their classification must be considered. Nevertheless, a considerable degree of validity can be ensured, as the success dimensions rely on well-established scientific references [120]. The reference literature selected in this paper is published in peer-reviewed academic journals of high reputation and quality in their respective fields, which makes them very representative. The majority of the chosen papers encompass methodologies and empirical results, and those papers not including methodology and empirical results are also capable of offering a systematic picture of research in the corresponding field. Second, this paper takes mainly academic articles into account. Although some important books and reports have been mentioned in the paper, these books and reports have not been subject to in-depth analysis, and contributions have also been published in the form of other types of documents. Moreover, sometimes it’s difficult to precisely define the economics, so only studies of REs regarding the aspects of supply, price, export policy, international trade, relationship with clean energy, and sustainability were chosen to form a systematic review on the economics.

Furthermore, another contribution of this study is to point out the possible opportunities for future research. Based on the results of this systematic review, a research agenda can be set out for future studies. First, the balance between the demand of the economic markets and the natural abundance of the REs in ores is a major problem for the market [121]. As we know, all RE elements are separated from the RE ores, where dissimilar elements share different concentrations, whereas the applications and need of individual elements vary greatly in the market. That is to say, some elements, such as Dy and Nd, which have wider applications and are of more economic value, make up much less of the natural ores. To meet the demand of these elements, sufficient quantities of REs ores have to be exploited. As a consequence, other elements will be produced in larger quantities than required by the market, and subsequently, these elements have to be stockpiled, which comes at a cost. Preferentially, the REs market is driven by the demand for elements that are very abundant (cerium and lanthanum), since this will create fewer problems regarding the stockpiling of the elements that are available in excess. [122]. It’s crucial to comprehend that it is not the total amount of RE ores that are mined that is of importance, but rather the total amount of separated individual REs elements. It must be realized that much more research should be conducted on the current high-tech applications of REs elements that require the use of purified individual REs elements rather than mixtures of REs elements. For example, Binnemans [84] discussed the relationship between criticality and the balance problem, and showed how this relationship influenced the market for specific REs elements. The author suggested that the REs industry must find new uses for REs that were available in excess, and searched for substitutes for REs that had either limited availability or were high in demand.

Second, the prices of REs are important, not only because it’s an essential factor for industrial production, but also REs are common commodities that involve a large amount of investment. The investment, which is required both for the exploitation of REs as well as their research and development (R&D), mainly comes from two channels: government support and private capital. Regarding the part of private capital, financing from the stock market plays an important role, which means that the volatility and risk analysis of RE-related stocks may be a crucial issue. Previously, price information in China was not readily available, because RE contracts were generally negotiated rather than traded on spot or future markets [73]. At present, China’s REs products trade center, which mainly focuses on the spot trade, has been established, and the REs products exchange in Baotou was officially put into operation on 8 March 2014 [123]. Furthermore, it’s worth noticing that the SHFE (Shanghai Futures Exchange) and ACREI (Association of China Rare Earth Industry) have been cooperating on REs futures since 2014, and signed a strategic cooperation framework agreement on 30 March 2018, which indicates that the SHFE and ACREI stepped into the stage of comprehensive strategic cooperation. To some extent, it will accelerate the establishment of REs futures and the development of related derivatives. It can be predicted that research on the REs from a financial perspective will be the trend and a hot topic in the coming future in light of the research and development of other commodities such as copper and precious metals.

Third, a significant position in the research has considered the sustainability of REs, which is bound to be a promising avenue of future research. On one hand, it is worth noticing that the public acceptance or disapproval of controversial facilities, such as nuclear power plants, nuclear waste repositories, and incinerators, has often led to the abandonment of the proposed project or failure to operate the facility [124]. Research offering insights on how the public responds to potentially hazardous facilities may be of great potential regarding the need for policymakers to consider public sentiment, which can interfere with the further expansion of the REs industry. On the other hand, nowadays, it is of great concern for many countries that numerous clean energy technologies, such as wind turbines and electric vehicles, are constrained by the limitation of RE materials. Various strategies have been proposed in order to alleviate supply shortages, including increasing and diversifying primary production, developing substitutes, lowering material intensity, and recycling [125]. However, limited papers [126] have analyzed the effects of strategies quantificationally to get a more explicit understanding, which calls for further research.

5. Conclusions

In this paper, literature devoted to the economic research of REs in six fields after the rare earth crisis has been systematically reviewed to draw a holistic picture of the state of the art. A systematic review and bibliometric analysis have been carried out with an 85-article sample. The results show that the number of articles published per year has increased steadily after the crisis. Especially, a sharp increase in the published number of articles occurred in the past six years, representing 92% of the total papers. Furthermore, among the six categories of supply, price, export policy, international trade, clean energy, and sustainability, the most popular research trend is related to the sustainability, which accounts for 34%. The top two regions that contribute the most to the literature are China and the European Union, which is attributed to their stress on the criticality and importance of REs.

In addition, the background and changes of China’s policies are illustrated in the paper, as well as the development and evolution of research trends worldwide. After China declared more stringent export restrictions on REs in 2009, with the purposes of protecting REs resources and upgrading the REs industry, many countries showed greater concerns regarding the security of the supply chain and the volatility of the price, which contributed to a growing amount of research on the fields of supply and price. Furthermore, regarding the science and technological developments, REs play a vital role in the clean energy sector, leading to growing attention on the importance and criticality of REs. Nonetheless, facing the uneven distribution of the resources and distorted structure of the market, numerous countries have resumed domestic production and carried out new projects to reduce their dependence on China. This trend makes research on the evaluation of projects and strategies prevalent. After the failure of China in the WTO case, China canceled the export quota and export tariff, and began to enforce the export license on REs, which attracted a series of papers focusing on examining the effects of the policy and changes in the world market. At the same time, on account of the contribution to the modern industry, the serious pollution caused by the exploitation and production of REs, and the reality of REs as exhaustible resources, methods of realizing the sustainability of REs has become a hotspot appealing for more studies.

Finally, research into REs from an economic perspective will continue due to their contribution and importance to the economy. Future studies may vary from country to country in view of the different resource endowments of REs. For a resource-rich country such as China, considering the policy changes, it’s imperative to determine a reasonable tax rate on RE resources. Besides, how to better deal with the pollution and environmental issues, which requires more quantitative research, is another crucial step for the sustainable development of REs. Whereas for the European Union and Japan, which represent regions that are poor in RE resources, it is of importance to consider strategies among recycling, importing from other countries, and investing in the exploitation of new resources. That is to say, evaluation and comparison between these strategies is needed in order to achieve the optimum results.

Author Contributions

Y.C. designed the research framework; B.Z. collected the data and wrote the paper. Y.C. offered critical comments and participated in revising. All the authors read and approved the final manuscript.

Funding

This research was funded by National Natural Science Foundation of China (NSFC) under grant No. 71673250, Zhejiang Provincial Natural Science Foundation for Distinguished Young Scholar under grant No. LR 18G030001, Major Projects of the Key Research Base of Humanities under the Ministry of Education under grant No.14JJD 790019, and Zhejiang Social Science Foundation under grant No. 18NDJC184YB.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Gupta, C.K.; Krishnamurthy, N. Extractive metallurgy of rare earths. Int. Mater. Rev. 1992, 37, 197–248. [Google Scholar] [CrossRef]

- Moldoveanu, G.A.; Papangelakis, V.G. Recovery of rare earth elements adsorbed on clay minerals: I. Desorption mechanism. Hydrometallurgy 2012, 117–118, 71–78. [Google Scholar] [CrossRef]

- Jordens, A.; Cheng, Y.P.; Waters, K.E. A review of the beneficiation of rare earth element bearing minerals. Miner. Eng. 2013, 41, 97–114. [Google Scholar] [CrossRef]

- Xie, F.; Zhang, T.A.; Dreisinger, D.; Doyle, F. A critical review on solvent extraction of rare earths from aqueous solutions. Miner. Eng. 2014, 56, 10–28. [Google Scholar] [CrossRef]

- Hayes-Labruto, L.; Schillebeeckx, S.J.D.; Workman, M.; Shah, N. Contrasting perspectives on China’s rare earths policies: Reframing the debate through a stakeholder lens. Energy Policy 2013, 63, 55–68. [Google Scholar] [CrossRef]

- Han, A.; Ge, J.; Lei, Y. An adjustment in regulation policies and its effects on market supply: Game analysis for China’s rare earths. Resour. Policy 2015, 46, 30–42. [Google Scholar] [CrossRef]

- Hoenderdaal, S.; Tercero Espinoza, L.; Marscheider-Weidemann, F.; Graus, W. Can a dysprosium shortage threaten green energy technologies? Energy 2013, 49, 344–355. [Google Scholar] [CrossRef]

- Bristish Geological Survey. Risk List 2015; Bristish Geological Survey: Nottingham, UK, 2015. [Google Scholar]

- US Department of Energy. Critical Materials Strategy; US Department of Energy: Washington, DC, USA, 2011.

- Massari, S.; Ruberti, M. Rare earth elements as critical raw materials: Focus on international markets and future strategies. Resour. Policy 2013, 38, 36–43. [Google Scholar] [CrossRef]

- Ali, S.H. Social and Environmental Impact of the Rare Earth Industries. Resources 2014, 3, 123–134. [Google Scholar] [CrossRef]

- Anastopoulos, I.; Bhatnagar, A.; Lima, E.C. Adsorption of rare earth metals: A review of recent literature. J. Mol. Liq. 2016, 221, 954–962. [Google Scholar] [CrossRef]

- Cox, C.; Kynicky, J. The rapid evolution of speculative investment in the REE market before, during, and after the rare earth crisis of 2010–2012. Extr. Ind. Soc. 2018, 5, 8–17. [Google Scholar] [CrossRef]

- Klinger, J.M. Rare earth elements: Development, sustainability and policy issues. Extr. Ind. Soc. 2018, 5, 1–7. [Google Scholar] [CrossRef]

- Klinger, J.M. A historical geography of rare earth elements: From discovery to the atomic age. Extr. Ind. Soc. 2015, 2, 572–580. [Google Scholar] [CrossRef]

- Kiggins, R.D. The Political Economy of Rare Earth Elements: Rising Powers and Technological Change; Springer: Berlin, Germany, 2015. [Google Scholar]

- Klinger, J.M. Rare Earth Frontiers: From Terrestrial Subsoils to Lunar Landscapes; Cornell University Press: Ithaca, NY, USA, 2018. [Google Scholar]

- Wübbeke, J. China’s Rare Earth Industry and End-Use: Supply Security and Innovation; Palgrave Macmillan: London, UK, 2015. [Google Scholar]

- Chen, J.; Zhu, X.; Liu, G.; Chen, W.; Yang, D. China’s rare earth dominance: The myths and the truths from an industrial ecology perspective. Resour. Conserv. Recycl. 2018, 132, 139–140. [Google Scholar] [CrossRef]

- Jin, Y.; Kim, J.; Guillaume, B. Review of critical material studies. Resour. Conserv. Recycl. 2016, 113, 77–87. [Google Scholar] [CrossRef]

- Bailey, G.; Mancheri, N.; Acker, K.V. Sustainability of Permanent Rare Earth Magnet Motors in (H)EV Industry. J. Sustain. Metall. 2017, 3, 611–626. [Google Scholar] [CrossRef]

- Mancheri, N.; Sundaresan, L.; Chandrashekar, S. Dominating the World China and the Rare Earth Industry; National Institute of Advanced Studies: Bengaluru, India, 2013. [Google Scholar]

- Hurst, C. China’s Rare Earth Elements Industry: What Can the West Learn? Institute for the Analysis of Global Security: Washington, DC, USA, 2010. [Google Scholar]

- Humphries, M. Rare Earth Elements: The Global Supply Chain; Congressional Research Service: Washington, DC, USA, 2013.

- Mancheri, N.A.; Marukawa, T. Rare Earth Elements China and Japan in Industry, Trade and Value Chain; Institute of Social Science, University of Tokyo: Tokyo, Japan, 2016. [Google Scholar]

- Sahebalzamani, S.; Bertella, G. Business models and sustainability in nature tourism: A systematic review of the literature. Sustainability 2018, 10, 3226. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G. PRISMA Group. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. PLoS Med. 2009, 6, e1000097. [Google Scholar] [CrossRef] [PubMed]