Integrated Reporting Narratives: The Case of an Industry Leader

1

Department of Management Theory, Warsaw School of Economics, al. Niepodleglosci 162, 02-554 Warsaw, Poland

2

Department of Accounting, Faculty of Economics and Business, University of Groningen, Nettelbosje 2, 9747 AE Groningen, The Netherlands

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(4), 976; https://doi.org/10.3390/su11040976

Submission received: 29 December 2018

/

Revised: 8 February 2019

/

Accepted: 11 February 2019

/

Published: 14 February 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:In this paper, we investigate the integrated reporting practice of the second-largest Polish petroleum company. Using the qualitative research method of narrative analysis, the paper draws upon the practice of integrated reporting by the domestic and sector leader, the second-largest Polish petroleum company, LOTOS Group. By analyzing the content of integrated reports for the years 2006–2015, alongside the main actors and themes involved, we distinguish three main narrative strategies, including: legitimacy, shareholder-agency, and signaling. In addition, we reveal the evolutionary transition of integrated reporting and identify its phase of development. Reporting appears to be conjoined rather than integrated. The study’s results imply that the implementation of integrated reporting may be limited by its insufficient institutionalization in the organizational context and the lack of recognized standards.

1. Introduction

Since 1990, the terms “corporate sustainability” and “corporate social responsibility” (CSR) have been used interchangeably. The study of the determinants and consequences of CSR have become a relevant topic in the accounting and management literature. Researchers have applied various theoretical and empirical frameworks to study various dimensions of CSR. Some argue that slack resources enable firms to go for voluntary CSR disclosure [1], while others relate such initiatives with reputational risk [2] and a company’s value [3]. The literature focusing on the determinants of CSR disclosure argues that size, profitability, and a desire for legitimacy are the main determining factors of CSR disclosure (see for review [4]).

Contemporary debate on sustainable development among academics, consultants, and corporate executives has resulted in greater awareness of corporate sustainability. This poses emerging challenges for firms to do their business in a more humane, ethical, and responsible way. At the same time, communicating corporate sustainability efforts successfully to stakeholders is another challenge for managers. Non-financial reporting originated from CSR and environmental disclosure and evolved towards integrated reporting (IR) to provide a complete picture of multidimensional firm performance [5]. The existing literature views IR as “the latest development in sustainability reporting innovation” [6] (p. 1068), which promises “holistic, strategic, responsive, material, and relevant across multiple time frames” [7] (p. 292) disclosure of a company’s operation and performance.

The idea of extending traditional standalone reports and integrating sustainability and financial disclosure has recently gained considerable prominence [8,9], especially in the face of increasing regulatory interest in IR. South Africa became the first jurisdiction to mandate this form of disclosure in 2010. The driver for this was the King Code of Governance Principles for South Africa 2009 (King III) becoming a requirement for entities listed on the Johannesburg Securities Exchange. New mandatory reporting rules in Europe (Directive 2014/95/EU) and stock exchange listing rules in, inter alia, Copenhagen, Kuala Lumpur, London, Paris, and Singapore also require quoted companies to disclose non-financial information (still, however, not necessarily integrated with financial information).

From a pure economic perspective, full disclosure helps firms to reduce information asymmetry [10], which increases awareness about a firm’s existence and its investor base [11]. Superior quality disclosure increases operating cash flows [12] and decreases the cost of financing [13]. Yet, a significant amount of literature acknowledges the opportunistic use of sustainability reporting. In this regard, very little has been researched from IR perspectives in terms of what motivates managers to adopt IR and what objectives managers want to achieve through IR.

We add to this literature by investigating the practice of IR of the second-largest Polish petroleum company. With a weak institutional environment, where less than 1% of listed companies produce integrated reports and formally binding standards of CSR disclosure have been available only since 2017, Poland significantly lags behind the sustainability reporting trend. However, the country and the selected company, which had already started IR in 2009, provide an excellent context to investigate companies’ motivations (other than regulatory compliance and risk of falling behind competitors) in their transition towards IR. Operating within a sector associated with a negative environmental and societal impact, in its practice of IR LOTOS exemplifies the case of an early adopter and local leader in the under-examined Central European context.

Additionally, the government ownership (53%) of the case company provides an interesting context to study the political use of non-financial reporting. We view a company’s IR as strategic communication with external and internal stakeholders in the form of a story, which is not just recounted but which provides legitimacy and accountability for the firm’s actions. IR is not a simple disclosure of data and facts. It is a strategic device based on stories that constitute the social world [14], indicating the proactive role of the participants. IR does not only reflect processes but gives meaning to events, actions, and objects, shapes reality, and provides guidance to and an understanding of organizational processes [14]. We adopt the narrative as the research method to uncover the logics of the corporate communication. Using the narrative approach, we trace human behavior to identify the succession of choices, undertaken decisions, and the analytical process of actions. We decompose the story of IR to draw upon its content and wording and identify narrative strategies and the pace of disclosure integration.

Our findings reveal that the company follows three main strategies, namely legitimacy, shareholder-agency, and signaling. Each of these strategies addresses different group of stakeholders and serves a different purpose (sustaining a license to operate among the nearest constituencies, justifying CSR investment to mainstream investors, signaling a strategic approach towards CSR to socially responsible investors). The results indicate that the moral context of the reporting is predominantly focused on shareholder-value maximization and the business case for sustainability. Additionally, as reporting appears to be of a combined rather than integrated character, the practice illustrates the still peripheral role of CSR and the weaknesses of its incorporation into business strategy. The shortcomings of LOTOS IR are tied to the lack of recognized standards and poor institutionalization within the organizational context.

The remainder of the article is structured as follows. By reviewing the existing literature, we build a framework to explain the practice of IR as a tool for strategic communication in the next section. Then, we introduce the research method of narrative analysis that we employed to report the results of this exploratory research. Finally, we discuss the results and conclude by providing some useful guidelines for future researchers and corporate managers in the final section.

2. Integrated Reporting as a Strategic Corporate Communication

Our aim in this study is to explore the sense-making process through narrative analysis in the context of stakeholder theory. In this regard, the exiting research has explored the adoption and use of IR from an institutional theory perspective [8]. Stakeholder theory posits that a firm should not only take care of the owners of the firm but also the society, economy, and the environment in which the firm operates [15,16]. Furthermore, the adoption and use of IR can be seen as a tool to obtain approval to operate in the society and avoid negative campaigns from pressure groups [17]. These corporate goals are in line with the basic premises of legitimacy theory and stakeholder theory [15]. Therefore, we analyze the contents of IR of an industry leader in the context of stakeholder theory.

IR is defined as: “a concise communication about how an organization’s strategy, governance, performance, and prospects, in the context of its external environment, lead to the creation of value over the short, medium, and long term” [18] (p. 7). Although the primary purpose of IR is to indicate the organization’s ability to generate value for investors and to induce them to allocate capital efficiently, it is also intended to meet the expectations of stakeholders, enhance accountability, and foster sustainability transition [19]. IR helps firms provide an overview of their sustainability and economic performance at the same place that bridges the information gap between non-financial and financial information [15]. Literature in this vein argues that firms adopting IR can realize three main benefits. First, as a holistic communication to a broad group of constituencies, IR empowers stakeholders by incorporating the needs of a wider variety of stakeholders into business strategy [20]. The corporate decision to produce integrated reports exemplifies the reconciliation of stakeholder theory and offers a balance of opportunities and benefits for producers as well as users of accounting information [21,22]. In this sense, IR helps firms maintain a balance in addressing the cooperative and competitive interests of stakeholders [23].

Second, IR increases accountability by providing concise and complete disclosure of a company’s social, environmental, and financial performance [24]. However, at the current stage of development, IR is neither institutionalized in corporate practice nor follows universal standards [23]. Non-financial disclosure frameworks, such as the International IR Framework [18] or the Global Reporting Initiative (GRI), face criticism with respect to either the instrumental use of such frameworks [25] or insufficient coverage and a lack of connection with true company performance [26].

The main reason for a shift of corporate attention towards IR is the demand from stakeholders for non-financial performance information [16]. The traditional practices of preparing financial and non-financial (sustainability) reports do not fulfill this purpose [27]. Recent findings show that even the production of standalone sustainability reports does not meet the corporate purpose of informing stakeholders in general and investors in particular [15]. This has shifted managers’ attention towards new ways of reporting. As a result, many firms have recently adopted an IR framework [17]. To further inform stakeholders, the majority of large firms have started issuing standalone sustainability reports. Recent literature in this vein shows that the production of standalone sustainability reports is creating a disconnect between financial and non-financial information. Originally, IR evolved to overcome this disconnect [28].

The strategic perception about IR is to meet investors’ expectations and consequently enhance company value [29]. Since IR is believed to serve the interests of the capital providers far more than the wider public, its current practice is viewed as “‘a masterpiece of obfuscation and avoidance of any recognition of the prior 40 years of research and experimentation’ that (…) threaten to push us ‘even further away from any plausible possibility that sustainability might be seriously embraced by any element of business and politics’” [26] (p. 1121).

Third, IR represents a fundamental change in corporate communication, which offers an opportunity to improve transparency, governance, and decision-making [30] and balances short, medium, and long-term perspectives of information disclosure and management orientation [7]. The main objective of this reporting approach is to provide not only a combined report but to manage and create value: from IR to integrated thinking [31]. Therefore, it is a transition of corporate thinking from a short-term focus on financial gains and cost-cutting to a long-term, future-oriented, business-model and value-based approach to run a company [28,30,32,33]. To summarize, it drives (or is driven by) the sustainability transition, which is viewed as a fundamental revolution in business and represents firms’ shift of focus towards a low emission, resource-efficient economy.

Despite the fact that IR has received a lot of scholarly attention in recent accounting, finance, and management literature, very little is known from a corporate perspective as to what purpose firms want to achieve by adopting IR. Stubbs and Higgins [6] (p. 1069) argue that the process of IR adoption still remains a black box, since “it is unclear why companies pursue IR, what approaches and internal mechanisms early adopters use to implement it, and whether it is driving organizational change at this early stage”. Building on the framework of IR materiality and functions, our goal is to look inside this black box and identify the content, size, wording, actors, and themes addressed in IR in order to explain its “deep structure” [14] (p. 712) in addition to identifying corporate strategies of multidimensional performance disclosure.

3. Research Design

3.1. Data Collection

The LOTOS Group is one of the largest European petroleum companies (and the second largest in Poland), employing over 5000 people. As a vertically integrated business group with 15 affiliated firms, it specializes in the extraction and processing of crude oil and the wholesale and retail sale of petroleum products. Apart from the parent company LOTOS, which manages the refinery in Gdańsk, the LOTOS Group comprises 15 other companies under the LOTOS brand. Two of them are based outside Poland, in Lithuania and Norway. The refinery in Gdańsk is one of the newest and most advanced refineries in Europe in terms of applied technologies and environmental protection. Through LOTOS Petrobaltic S.A. and LOTOS Exploration and Production Norge AS, LOTOS is engaged in the exploration and production of crude oil from the Baltic Sea and the Norwegian Continental Shelf. It is the sole company producing hydrocarbons in the Polish Exclusive Economic Zone of the Baltic Sea, and has almost exclusive rights to carry out exploration and production work in the Baltic Sea. The company also has access to onshore hydrocarbon deposits in Lithuania through its subsidiary AB LOTOS Geonafta.

Since 2005, LOTOS has been listed on the Warsaw Stock Exchange with a majority stake of 53% of shares controlled by the government. These characteristics provide an interesting research setting, since LOTOS group operates in an environmentally sensitive industry in which firms encounter more pronounced stakeholder pressure to reduce their detrimental environmental impact and provide more transparent information about their policies and operations [16]. On the other hand, the government ownership of the selected firm can also help us complement the literature about the political use of CSR [34].

LOTOS is one of CSR leaders in Poland. Since November 2009, its shares have also been a constituent of the Warsaw Stock Exchange’s RESPECT Index of socially responsible companies, which is the first such index in Central and Eastern Europe. For 14 years (2002–2016), the company was run by Paweł Olechnowicz, under whose management the company’s revenues have increased fourfold. As a strong leader, highly supported by employees, he played a crucial role in LOTOS’s transition towards sustainability and IR.

We conduct a discourse and textual analysis of all available information disclosed by LOTOS group in the form of CSR and environmental reports, as well as integrated reports issued since 2009. Our study period is from 2006 to 2015. To study the case of LOTOS group in detail, we analyze the content of consolidated financial reports and public statements published over the study period. The supporting documents unraveling the LOTOS story include all publicly available information, constituting: press releases, corporate websites, LOTOS Development Strategy documents for 2011–2015, and LOTOS Effective and Rising Program documents for 2013–2015. Table 1 provides details of the data used in the analysis.

3.2. Narrative Analysis Methodology

Narrative analysis as a research approach is used in organizational studies to encode different data relevant to various phenomena of organizational life [35], and to understand the emergence and functioning of strategy [36]. In general, a narrative is defined as a form of experience to explain what has occurred [37]. The study of a narrative allows us to capture the explanations of “a story that describes the process, or sequence of events that connects the cause and effect” [14] (p. 711), indicating the order and making sense of a series of events.

This research method analyzes the language, which offers a structural analysis with a decisive concept indicating its organization and is essential for any system of sense-making. Narrative analysis requires not only the ability to follow “the unfolding of the story but also to recognize in it a number of strata, to project the horizontal concatenations of the narrative onto an implicitly vertical axis; to read a narrative or to listen to it is not only to pass from one word to the next, but also from one level to the next” [38] (p. 243). Pentland (1999), whose approach we follow for this analysis, stresses a four-level structure in narrative, including: text, story, fabula, and meaning-generating mechanisms, and enumerates relationships of narrative properties covering sequence, focal actors, moral context, and other indicators. Adopting the narrative methodology to analyze IR not only mirrors the organizational reality but also allows us to deconstruct the firm’s internal and external powers, strategies and tactics, perceptions, and identities with its participants. Stories are referred to as trajectories that people follow and, in line with their constant evolution, re-create, and that are much more than data since they help to explain decision-making patterns and reasoning and power structures [14].

The capability of examining the contents of corporate communication to internal and external constituencies and its links to strategic and organizational actions provided by narrative analysis is useful to understand the process of adoption and implementation of IR [19]. In this study, we follow the approach proposed in the strategy by [36], which is also adopted in explaining succession in family firms by [39]. We assume that narrative analysis of integrated reports “is a strategic device—a set of carefully constructed stories—that organizational actors use to influence the understanding of others with respect to a particular person, event, or potential future” [39] (p. 1378). The communication dimension of narrative emphasizes the importance of readership and interpretation [36]. In this way, narrative analysis of IR is a form of sense-making, referring “to thematic sequenced accounts that convey meaning from implied authors to implied reader” and encompassing “both the telling and the told” [36] (pp. 431–432) embedded in organizational contexts [40], stories, legends, myths, rhetoric, and metaphors. On the operational level, we adopt the structural framework proposed by [14], following the ‘from description to explanation’ process of narrative. We view integrated reports as stories told by organizations that encompass their financial, social, and environmental performance, in which the sequence, actors, and moral context are covered. Integrated reports turn words and facts into stories, revealing underlying structures of organizational processes [7].

3.3. Data Analysis

We analyze the data in three steps. First, to understand the context in which narratives of IR are produced [39], we trace the company characteristics, strategy, and performance exemplified in the company’s corporate and investor relations websites, its statute, and its development strategy documents. Second, we look at the 2006–2008 environmental and CSR reports that represent the company’s non-financial disclosures, followed by an analysis of the 2009–2014 integrated reports. This part of the analysis is complemented with data derived from media communications, public statements, and financial reports.

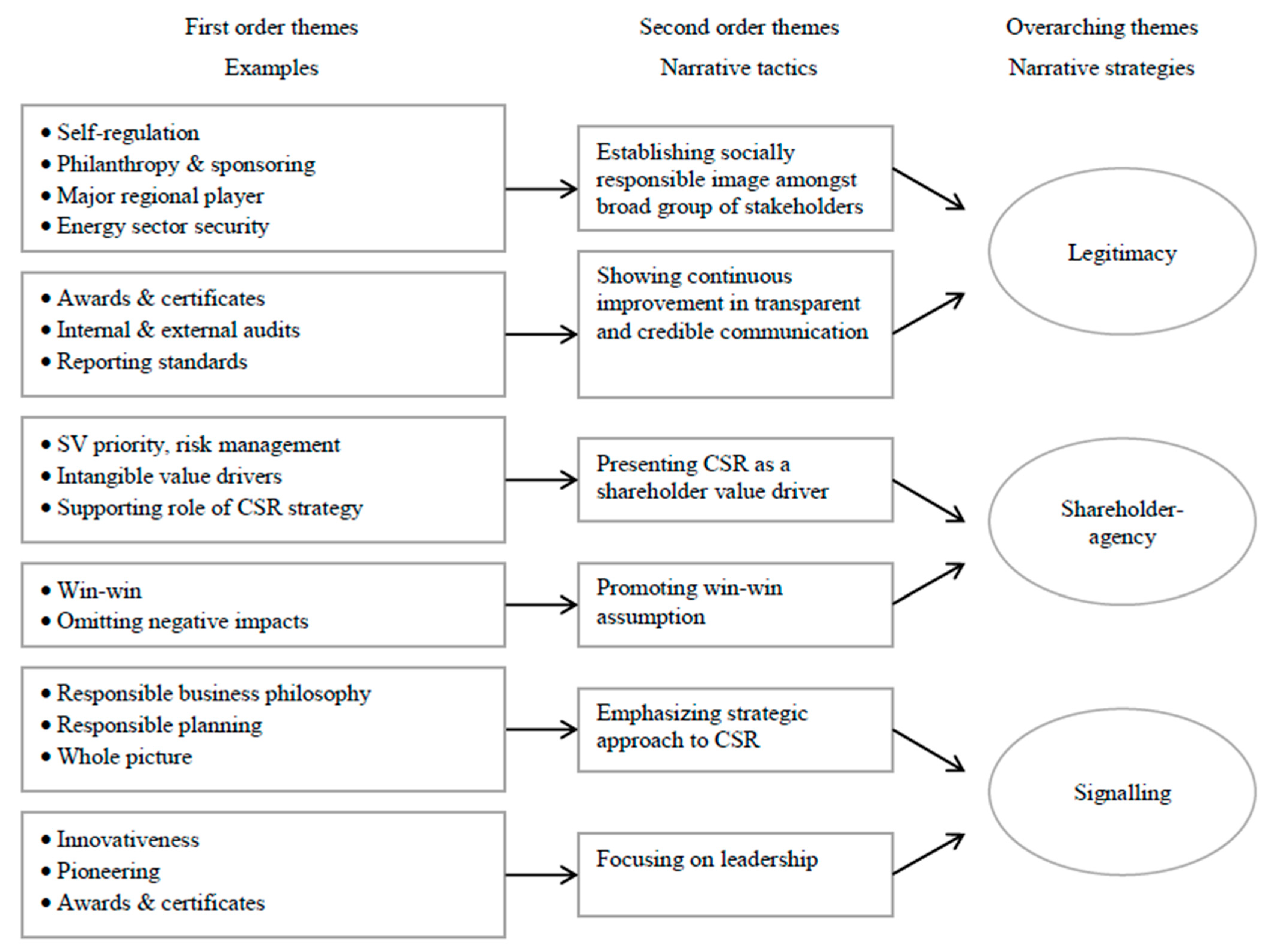

Adopting a functional approach to narrative analysis [39], we intend to uncover the message and the meanings of particular stories behind the simple collection of words. With the support of ATLAS.ti (the qualitative data analysis software), we adopt a coding process of paragraphs and sentences to perform a thematic analysis of the text in three stages: identifying first-time themes, identifying narrative tactics, and identifying narrative strategies [39]. This could be referred to as the what, how, and why, as recounted by LOTOS in its environmental, CSR, and integrated reports. First, we analyze the 2006–2014 reports to develop inductive codes to trace the story of the motivation, adoption, and practice of IR. These first-order themes are grounded in data and exemplified by the operational communication. They show what is disclosed with respect to LOTOS’s performance. Second, we aggregate first-order themes to deliver more abstract codes tracing related story lines. These second-order themes represent how the stories of IR are developed and are referred to as narrative tactics. Third, we assign these narrative tactics to broader concepts of why LOTOS implements IR to develop aggregated, over-reaching themes that represent narrative strategies.

4. Major Findings

Our analysis reveals that LOTOS adopts three narrative strategies in its IR: legitimacy, signaling, and shareholder-agency. Figure 1 presents the results of the analysis.

4.1. Legitimacy

Legitimacy strategy involves conveying the idea that LOTOS operations are beneficial for the local community and entails two tactics, addressed mainly to nongovernmental organizations (NGOs) and public authorities: establishing a socially responsible image and showing continuous improvement in transparency.

4.1.1. Establishing a Socially Responsible Image

LOTOS establishes an image of a company committed to ecology and the development of local communities and the national economy. This activity is a part of its “license to operate” strategy. It is aware of its impact on society and the environment [41] (p. 5) and “by operating in accordance to CSR and sustainable development principles, the company meets the expectations of its stakeholders” [42] (p. 4).

LOTOS offers holistic communication to a broad group of constituencies, addressing concerns about the safety of its production processes and products, and it repeatedly emphasizes self-regulation regarding environmental principles and product safety, far more stringently than standards imposed by Polish and European laws. For example, the chief executive officer (CEO) letter in the 2006 Environmental Report contains the following:

“We are able to meet the highest standards of environmental protection and environmental quality norms long before they become generally applicable, and above all to strictly follow the requirements of both national and international regulations in the field of environmental protection”.[41] (p. 5)

In the 2009 Annual Report, LOTOS informs that “in order to reduce the likelihood of adverse events” [43] (p. 28) self-imposed standards were also extended to the area of work safety. LOTOS also declares its intention to systematically implement new technical and organizational solutions to increase the awareness and involvement of employees and ensure safe working conditions for all persons residing and/or working at its premises [43] (p. 28). This positively impacts business practices in the region and industry [43] (p. 29).

The company’s community involvement is presented as a tool to gain support from its nearest constituencies. Through sponsoring and community involvement, LOTOS builds upon relationships with empowered stakeholders, specifically local communities, based on trust and the confidence that the close proximity of its plants may positively affect the development of particular regions [42] (p. 91).

4.1.2. Showing Continuous Improvement in Transparent and Credible Communication

The story is centered around continuous improvements in transparency and credibility, which are perceived as crucial elements for business success:

“Open information policy and dialogue with society, especially our closest neighbors, are key for the LOTOS Group’s future development”.[41] (p. 8)

LOTOS builds its “credibility story” by adopting the most commonly accepted reporting frameworks. Over time, the company has repeatedly been introducing improvements in this area, starting from the simple adoption of Global Reporting Initiative (GRI) standards in the 2006–2007 CSR Report and full compliance in the 2008 CSR Report, followed by the external verification of non-financial data in the 2011 Integrated Annual Report, the use of a GRI Sector Supplement in the Integrated Annual Report in 2012, and finally referring to the International IR Council (IIRC)’s framework in the 2013 Integrated Annual Report. Further support for this story is provided by the third-party recognition gained for outstanding reporting practices.

4.2. Shareholder-Agency

Recently, socially responsible investing (SRI) has gained popularity globally as the emphasis has shifted from shareholders’ value creation to stakeholder orientation. With this shift, informed investment decisions need credible sustainability/CSR information. The extant investment literature highlights the pivotal role of CSR performance information in reducing the analysts’ forecast errors, information asymmetry, cost of capital, financial constraints, and stock price crash risk. Despite the availability of such findings, managers often struggle with the best strategies to communicate their CSR engagements. Recently, some studies have highlighted the disconnect between financial and nonfinancial reporting [15]. This disconnect undermines the effectiveness of a firm’s dialogue with its stakeholders. The struggle to develop a connection between economic and noneconomic performance information has given rise to the IR. Even though IR is in its infancy, its adopters, such as LOTOS, are already able to use it as a strategic communication tool to inform current and future investors.

In this strategy, LOTOS presents its social responsibility efforts as complementary to its core strategy, with the underlying assumption of win-win stakeholder–shareholder relations. This narrative, initially outlined in the environmental and CSR reports, has developed with the adoption of IR in 2009. Before this, neither financial statements nor directors’ reports presented any information on the company’s social and environmental performance. With IR, LOTOS is able to present the connection between non-financial and financial performance data and to convey the “doing well by doing good” message to its shareholders.

4.2.1. Presenting CSR as a Shareholder Value Driver

Shareholder value maximized in line with sustainable development principles is the main corporate goal:

“The LOTOS Group has remained committed to its overarching strategic objective of building shareholder value through optimal use of available intellectual resources and assets (…) The strategy underscores the importance of developing those areas in compliance with the principles of sustainable development…”.[44] (p. 26)

CSR is not viewed as an unnecessary cost that decreases shareholder value [45] but remains a means for increasing accountability and an investment that drives long-term value creation. Addressing social and environmental concerns in the investment decision-making process (since 2009) may lower the investment risk by one third [46]. Since firm value is highly dependent on intangible assets, LOTOS emphasizes the need to take responsibility for environmental and social impacts.

“In the modern economy, a company’s value is derived not only from its ability to generate earnings, but also from how it is perceived by its external and internal stakeholders”.[47] (p. 279)

CSR strategy supports the core business strategy. In both periods (2008–2012 and 2012–2015), business goals were set earlier and served as a motivation to strategically define social and environmental activities. This suggests that these aspects are nevertheless not integrated but rather conjoined.

4.2.2. Promoting the Win-Win Assumption in Business–Society Relationships

LOTOS links increased disclosure with enhancing shareholder value. The CEO stresses that “one can say that its biggest responsibility is to be effective and efficient as, in fact, there is nothing worse for stakeholders than having to deal with an unprofitable company which does not pay its dues on time and cannot provide a decent work environment for its employees due to its poor standing” [47] (p. 108). While the company prioritizes maximizing shareholder value in accordance with sustainable development principles, it does not disclose its policy concerning a potential conflict between these objectives. Negative social or environmental performance is not openly communicated.

4.3. Signaling

This strategy refers to conveying a signal to socially responsible investors about CSR practices to reduce information asymmetries, distinguish itself from competitors, and maintain good relations with SRI capital providers. It comprises two tactics: emphasizing a strategic approach to CSR and focusing on leadership to optimize financing costs and to increase company value.

4.3.1. Emphasizing a Strategic Approach to CSR

LOTOS underlines its strategic commitment to CSR, which is presented as its business philosophy and exemplified in the following quote:

“LOTOS believes in doing business responsibly. We understand CSR as a way of doing business with due consideration for the needs of our environment. Our business operations and strategy are successfully aligned with social and environmental concerns, ethics, as well as human and customer rights”.[48] (p. 4)

Although the strategic approach to CSR, especially in the environmental dimension, had already been signaled in separate non-financial disclosures, it was the introduction of IR that built a strong case for this story. IR is presented as a result of integrated thinking that links financial and non-financial goals [49]. In a sense, this exemplifies a significant change in corporate communication. The following quote explains some of the motivations behind the change in reporting format:

“Responsibility, ethics and openness are the fundamentals of our business activity principles. These are the premises, which affected the current decision on changing the reporting model.”.[43] (p. 21)

The integrated disclosure to stakeholders delivers data on financial condition as well as social and environmental performance and provides a comprehensive picture of the company’s CSR strategies (2008–2012 and 2012–2015). Such transparent communication is seen as an important driver of competitive advantage [50].

The strategic approach to CSR correlates with corporate values of transparency, openness, innovation, responsibility, and its mission statement, which was redeveloped in 2010:

“Our mission is to pursue innovation-oriented sustainable development in the areas of exploration, production and processing of hydrocarbons and marketing of high-quality products, which is conducive to creating lasting value for shareholders, fully meeting customer expectations, enhancing and leveraging the employee potential, and which is carried out in compliance with the energy security policy, with due regard paid to the welfare of local communities and the natural environment”.[44] (p. 75)

CSR is described as a planning doctrine. Activities aimed at minimization of the Group’s social and environmental impacts are communicated as an integral part of LOTOS development plans that are set to benefit not only the company but also its key stakeholders:

“The 2011–2015 strategy provides for the consolidation of the LOTOS Group’s position as a strong, innovative, and successfully developing entity, which plays a crucial role in ensuring Poland’s energy security and operates in compliance with the principles of social responsibility and sustainable growth” [48] (p. 7). Although strategic goals do not make any explicit reference to social or environmental issues, LOTOS declares its intention to relate “all the business decisions to the prospect of development in three key dimensions”: long-term economic growth, protection of the natural environment, and social development [43] (pp. 21–22). Incorporating CSR into strategy and addressing stakeholder expectations provide an opportunity for enhanced communication to improve transparency, governance, and decision-making, and will serve as a means to manage and create value. However, once the analysis of LOTOS’s reporting is moved from the declarative level to actual initiatives and their results (both economic and social), integrated reports provide little information on interdependencies between non-financial and financial data.

Statements on the integration of non-financial and financial aspects of business are not reflected in the structure of reports that separate business performance from sustainability goals. In 2013, LOTOS introduced the notion of six capitals principles influencing the firm’s value and made an attempt to show interdependencies between them. In the following year, however, it returned to the previous structure of the report.

4.3.2. Emphasis on Leadership

LOTOS emphasizes its market leader image, implementation of management systems, and effective CSR strategy:

“Our ability to maintain the market lead will inextricably depend on our respect for the principles of sustainable development, in particular the rational use of natural resources, as well as minimizing the impact of all the LOTOS Group members on the natural environment”.[48] (p. 99)

LOTOS reports outline the link between CSR and innovation. The responsible and transparent approach towards stakeholders and the environment encompassing heavy investment in the newest technology is “cited as a paragon of modern business practices” [47] (p. 2).

A number of CSR activities are described as innovative and pioneering. LOTOS was the first in its sector to introduce an Integrated Management System that includes quality, environmental, and work safety management systems [41] (p. 6), and the first Polish company to produce a CSR report with an ‘A’ level application of the GRI framework [51]. The Group is also a pioneer of IR in Poland, which is described as evidence not only for its corporate responsibility, but also its degree of innovation [52]. Reinforcing this image as a leader are the awards and certificates that illustrate external recognition and are cited as proof of “its competitive position” [43] (p. 11).

5. Discussion

Table 2 offers a summary description of strategies with the identification of company voice, purpose to be met, primary benefits, and main theme, as well as a decomposition of the moral context emerging from the communication.

LOTOS uses three narrative strategies in its IR: legitimizing, shareholder-agency, and signaling. With the legitimization strategy, LOTOS seeks to sustain “the license to operate” and to gain acceptance from holistic communication to its broad range of stakeholders. The findings of this study clearly contribute towards legitimacy and stakeholder theory by showing that the enforcement of the social contract [53] drives LOTOS to construct CSR and sustainable development as a counterweight to the negative impact of the company on society and environment, stressing the moral context of the self-regulation and pro-active approach. IR is a tool for establishing a socially responsible image, introducing incremental improvements in corporate disclosures and building transparent and credible communication [7,30]. It appears to be the manifestation of acting within the bounds and norms expected by various stakeholders and a formal means of incorporating the expectations of wider stakeholder groups into its business practices [19,20]. The holistic communication offered by IR balances the cooperative and competitive interests of stakeholders [46] and legitimizes the company’s operation [54]. With the purpose to obtain the license to operate, LOTOS, as a government-controlled company, remains consistent “with the domestic institutional structure and the political values” [34] (p. 811). Offsetting the negative environmental impact as the national leader in IR, the company addresses political pressure and societal norms [34].

We identify the shareholder-agency approach as the second narrative strategy. This strategy’s goal is to emphasize the win-win assumption which, as we argue, is an instrumental approach that undermines the idea of sustainability to leverage the expectations of shareholders and the primacy of financial performance [25,26]. Previous research suggests that by providing a holistic view on the firm’s operations, IR addresses shareholders’ growing demand for information on non-financial value drivers [16]. However, LOTOS, being a pioneer in a weak institutional environment, appears to be more mature in balancing financial versus social and environmental issues than the majority of its shareholders. Due to insufficient knowledge about SRI and its effectiveness and performance compared with mainstream investment, Polish investors show low interest in socially responsible companies (EUROSIF). Thus, in its shareholder-agency strategy, the company uses the connection of non-financial and financial data offered by IR to justify its engagement in CSR and sustainability programs and avoid conflict with mainstream investors. The stories on reducing business risk and positive synergic effects between social/environmental and shareholder value communicate the primacy of shareholder value, supporting the role of CSR and the win-win assumption.

Finally, with a signaling narrative strategy, LOTOS uses IR to show the entire picture of multidimensional company performance [55]. The strategy is based on the underlying idea that organized and deliberative communication reduces information asymmetry and satisfies SRI capital providers’ demand for information on interlinkages between non-financial and financial performance. According to the tone of the discourse, LOTOS pursues a signaling strategy underlying a strategic approach to CSR and constructing CSR as driver of innovation, openness, and competitive advantage [56]. The company emphasizes being a national leader, which is expected to support the rational and efficient decision-making of investors [5]. LOTOS states that the decision to shift towards IR was driven by its CSR-based management orientation: a natural consequence of this new business philosophy.

Generally, the legitimacy and signaling theories are presented as opposite approaches. Legitimacy theory primarily argues for firms’ ethical behavior to attain a license to operate in a given economy, while signaling theory tries to explain firms’ actions that are not necessarily rooted in the company’s culture. The signaling actions are not the true representation of a company’s values and are sometimes linked to masking actions. In our analysis, we find that LOTOS not only is committed to the integration of nonfinancial aspects into its core economic activities but also promotes its voluntary actions to send a positive signal to the current and future investors.

Thus, similar to [57], we reveal that integrated thinking within the organization is the driver of IR and not the other way round, as suggested by some authors [28,30,32,33]. The introduction of IR is used as a signal that supports the company’s integrated thinking narrative. However, the analyzed documents provide little evidence for any actual sustainability transition, as financial and non-financial data are presented in more of a conjoined than integrated manner. CSR strategy and core business strategy are not integrated and treated equally, but it is rather CSR strategy supports the latter. Additionally, integrated reports present business and CSR performance separately and provide little information on interdependencies between non-financial and financial data.

The IR story is centered around shareholders, either assuring them control over reputational risk (legitimacy), establishing links towards financial performance and shareholder value (shareholder-agency), or securing capital for future investments (signaling). The documents analyzed indicate that LOTOS managers are motivated by the numerous benefits of IR. The goals of attaining legitimacy and gaining accountability to empowered stakeholders who demand holistic communication are accompanied by the desire to manage risk, reduce information asymmetry [10] (Martínez-Ferrero et al., 2015), and attract investors [11] by signaling competitive advantages stemming from a strategic approach to CSR. This leads us to the observation that the moral context of the LOTOS narrative is predominantly centered around the business case, rather than on the idea of sustainability [26].

Nevertheless, our analysis reveals that the transition towards IR is a process based on continuous incremental improvements instead of a revolutionary change. Thus, we see the dynamics of IR not as a linear process but as multifaceted synergistic evolution. LOTOS IR remains at an early stage of development. At this stage, we note the evidence for the opportunistic use of sustainability reporting that has already been acknowledged in prior studies. LOTOS keeps on communicating its motivations for IR, though more by increasing its intensity and improving the content’s quality rather than dramatically changing the tone of the message. Additionally, we reveal the reporting to be of a combined rather than integrated character [31], which mirrors the peripheral role of CSR and the weaknesses of its incorporation into business strategy.

The narrative analysis reveals that IR is not an overnight organizational innovation but is a long process over which a company learns how it wishes to express itself and what it wants to communicate. First, the idea behind the holistic disclosure of company performance originates from the voluntary disclosure of social and environmental activities, which evolve towards integrated reports covering financial and non-financial data [7]. IR starts with separate financial and non-financial disclosure and develops into a holistic information policy with a well-defined structure. Meeting the demand for holistic disclosure regarding company operations may be viewed as a response to the deficiencies in links between financial and non-financial information [28]. LOTOS addresses this to a wide group of stakeholders [29], mostly to shareholders, NGOs, public authorities, and local communities. As revealed in our analysis, integrated reports may become unwieldy in size, jumping in the case of LOTOS from 164 pages in 2009 to 337 pages a year later and peaking at 468 pages in 2014, thus hindering user-friendly communication.

Second, our findings support the criticism regarding the lack of widely recognized standards for IR and the insufficiency of specific CSR measures [25,26,58]. LOTOS follows the IIRC’s conceptualization of IR, which is built around a notion of value that is generated from six categories of capital, not necessarily owned by the company: financial, manufactured, intellectual, human, social, and natural [16]. However, in terms of the evolution of reporting for 2014, we observe a slight regress. Instead of identifying the links between the measures of the six kinds of capital with business strategy and financial performance, due to a lack of appropriate tools and instruments LOTOS seems to draw back and focus on shareholder value as the most important and widely understood measure of a company’s performance. The lack of strong institutionalized support in the form of clear guidelines and standards appears to force the company to rethink their integrated management and reporting [57].

6. Concluding Remarks and Future Research Directions

IR is attracting increasing attention from both academics and business practitioners. It offers fundamental qualitative progress in adopting and operationalizing the concepts of CSR and sustainability in business, and forces companies to identify the links between social, environmental, and financial performance, redeveloping managerial processes and procedures. It offers complete and strategic forward-looking materials as an instrument for transforming traditional businesses into sustainable, future-oriented enterprises that provide benefits to various stakeholders. Nonetheless, with the dominance of traditional reporting regimes and the prevalence of financial measures for corporate performance, communicating sustainability efforts to stakeholders remains a challenge for managers.

On the operational level, IR represents a story that the company tells to its constituencies, translating external expectations and pressures into organizational reality. We adopt the method of narrative analysis to capture the explanations of the story of IR by LOTOS Group. By studying CSR, environmental, financial, and integrated reports, as well as a number of additional documents, we identify the story of what happened. We reveal the practice with respect to its content, length, and wording, alongside the main actors and themes of IR, and distinguish three narrative strategies employed by LOTOS: legitimacy, shareholder-agency, and signaling motivations for adopting IR. The three strategies identified are discussed from the perspective of company voice, purpose to be met, primary benefits, and the main theme, in addition to the moral context emerging from the communication. Finally, we trace the dynamics of IR, emphasizing the evolutionary transition of LOTOS’s reporting practices and the combination of strategies rather than an integration of them. Our observations indicate the shortcomings of adopting IR, which are tied to the lack of recognized standards and the opportunistic use of sustainability communication.

Our study offers an analysis of the deep structure of IR by LOTOS. Simultaneously, it reveals limitations related to the qualitative study and the single-company case approach. A quantitative analysis over a large sample would reveal the bigger picture of IR practice. We suggest directions for further research that address the role of the organizational context with political pressure by governments and the positive spillover by the leader in the process of IR development. Finally, we view the operationalization of IR in the form of a balanced scorecard that integrates social, environmental, and financial performance as an essential direction for further studies.

Author Contributions

M.A., N.H. and M.R.-M. contributed equally to this paper.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Fodio, M.I.; Oba, V.C. Boards’ gender mix and extent of environmental responsibility information disclosure in Nigeria: An empirical study. Eur. J. Bus. Manag. 2012, 4, 163–169. [Google Scholar]

- Herda, D.N.; Taylor, M.E.; Winterbotham, G. The Effect of Board Independence on the Sustainability Reporting Practices of Large US Firms. Issues Soc. Environ. Account. 2012, 6, 178–197. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate governance and firm value: The impact of corporate social responsibility. J. Bus. Ethics 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Frias-Aceituno, J.V.; Rodríguez-Ariza, L.; Garcia-Sánchez, I.M. Explanatory Factors of Integrated Sustainability and Financial Reporting: Explanatory Factors of Integrated Sustainability Reporting. Bus. Strategy Environ. 2014, 23, 56–72. [Google Scholar] [CrossRef]

- Stubbs, W.; Higgins, C. Integrated Reporting and internal mechanisms of change. Account. Audit. Account. J. 2014, 27, 1068–1089. [Google Scholar] [CrossRef] [Green Version]

- Adams, S.; Simnett, R. Integrated Reporting: An Opportunity for Australia’s Not-for-Profit Sector: Integrated Reporting for Not-for-Profit Sector. Aust. Account. Rev. 2011, 21, 292–301. [Google Scholar] [CrossRef]

- Jensen, J.C.; Berg, N. Determinants of traditional sustainability reporting versus integrated reporting. An institutionalist approach. Bus. Strategy Environ. 2011, 21, 299–316. [Google Scholar] [CrossRef]

- Fifka, M.S. Corporate Responsibility Reporting and its Determinants in Comparative Perspective—A Review of the Empirical Literature and a Meta-analysis. Bus. Strategy Environ. 2013, 22, 1–35. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; Ruiz-Cano, D.; García-Sánchez, I.-M. The Causal Link between Sustainable Disclosure and Information Asymmetry: The Moderating Role of the Stakeholder Protection Context. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 319–332. [Google Scholar] [CrossRef]

- Merton, R.C. A Simple Model of Capital Market Equilibrium with Incomplete Information. J. Financ. 1987, 42, 483–510. [Google Scholar] [CrossRef] [Green Version]

- Lambert, R.; Leuz, C.; Verrecchia, R.E. Accounting Information, Disclosure, and the Cost of Capital. J. Account. Res. 2007, 45, 385–420. [Google Scholar] [CrossRef] [Green Version]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Corporate social responsibility disclosure and the cost of equity capital: The roles of stakeholder orientation and financial transparency. J. Account. Public Policy 2014, 33, 328–355. [Google Scholar] [CrossRef]

- Pentland, B.T. Building process theory with narrative: From description to explanation. Acad. Manag. Rev. 1999, 24, 711–724. [Google Scholar] [CrossRef]

- Hussain, N.; Rigoni, U.; Cavezzali, E. Does it pay to be sustainable? Looking inside the black box of the relationship between sustainability performance and financial performance. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1198–1211. [Google Scholar] [CrossRef]

- Hussain, N.; Rigoni, U.; Orij, R.P. Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J. Bus. Ethics 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Cavezzali, E.; Hussain, N.; Rigoni, U. The Integrated reporting and the conference calls content. In Integrated Reporting; Palgrave Macmillan: London, UK, 2016; pp. 231–252. [Google Scholar]

- International Integrated Reporting Council. The International <R> Framework; International Integrated Reporting Council: London, UK, 2013. [Google Scholar]

- Sierra-García, L.; Zorio-Grima, A.; García-Benau, M.A. Stakeholder Engagement, Corporate Social Responsibility and Integrated Reporting: An Exploratory Study: Corporate Social Responsibility and Integrated Reporting. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 286–304. [Google Scholar] [CrossRef]

- Higgins, C.; Stubbs, W.; Love, T. Walking the talk(s): Organisational narratives of integrated reporting. Account. Audit. Account. J. 2014, 27, 1090–1119. [Google Scholar] [CrossRef] [Green Version]

- Ioana, D.; Adriana, T.-T. Research Agenda on Integrated Reporting: New Emergent Theory and Practice. Procedia Econ. Financ. 2014, 15, 221–227. [Google Scholar] [CrossRef] [Green Version]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Donaldson, T.; Preston, L. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Steyn, M. Organisational benefits and implementation challenges of mandatory integrated reporting. Perspectives of senior executives at South African listed companies. Sustain. Account. Manag. Policy J. 2014, 5, 476–503. [Google Scholar] [CrossRef]

- Flower, J. The International Integrated Reporting Council: A story of failure. Crit. Perspect. Account. 2015, 27, 1–17. [Google Scholar] [CrossRef]

- Brown, J.; Dillard, J. Integrated reporting: On the need for broadening out and opening up. Account. Audit. Account. J. 2014, 27, 1120–1156. [Google Scholar] [CrossRef]

- Bernardi, C.; Stark, A.W. Environmental, social and governance disclosure, integrated reporting, and the accuracy of analyst forecasts. Br. Account. Rev. 2018, 50, 16–31. [Google Scholar] [CrossRef]

- Adams, C.A. The International Integrated Reporting Council: A call to action. Crit. Perspect. Account. 2015, 27, 23–28. [Google Scholar] [CrossRef]

- Doni, F.; Gasperini, A. Sustainability reporting and value relevance. Empirical evidence from the Beverage industry in the European Union. In Proceedings of the Global Cleaner Production and Sustainable Consumption, Sitges Barcelona, Spain, 1–4 November 2015. [Google Scholar]

- Eccles, R.G.; Krzus, M.P. One Report: Integrated Reporting for a Sustainable Strategy; John Wiley and Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Demartini, P.; Paoloni, P. Managing sustainability through the IC practice lens. In Proceedings of the International Forum on Knowledge Asset Dynamics, Zagreb, Croatia, 12–14 July 2013. [Google Scholar]

- Ballou, B.; Casey, R.J.; Grenier, J.H.; Heitger, D.L. Exploring the Strategic Integration of Sustainability Initiatives: Opportunities for Accounting Research. Account. Horiz. 2012, 26, 265–288. [Google Scholar] [CrossRef]

- Beattie, V.; Smith, S.J. Value creation and business models: Refocusing the intellectual capital debate. Br. Account. Rev. 2013, 45, 243–254. [Google Scholar] [CrossRef] [Green Version]

- Detomasi, D.A. The Political Roots of Corporate Social Responsibility. J. Bus. Ethics 2008, 82, 807–819. [Google Scholar] [CrossRef]

- Robert, D.; Shenhav, S. Fundamental Assumptions in Narrative Analysis: Mapping the Field. Qual. Rep. 2014, 19, 1–17. [Google Scholar]

- Barry, D.; Elmes, M. Strategy Retold: Toward a Narrative View of Strategic Discourse. Acad. Manag. Rev. 1997, 22, 429–452. [Google Scholar] [CrossRef] [Green Version]

- Bamberg, M. Narrative analysis. In APA Handbook of Research Methods in Psychology; Cooper, H., Ed.; APA Press: Washington, DC, USA, 2012; pp. 85–102. [Google Scholar]

- Barthes, R.; Duisit, L. An introduction to the structural analysis of narrative. New Lit. Hist. 1975, 6, 237–272. [Google Scholar] [CrossRef]

- Dalpiaz, E.; Tracey, P.; Phillips, N. Succession Narratives in Family Business: The Case of Alessi. Entrep. Theory Pract. 2014, 38, 1375–1394. [Google Scholar] [CrossRef]

- Ewick, P.; Silbey, S.S. Subversive Stories and Hegemonic Tales: Toward a Sociology of Narrative. Law Soc. Rev. 1995, 29, 197–226. [Google Scholar] [CrossRef]

- Grupa LOTOS. LOTOS Environmental Report 2006; Grupa LOTOS S.A.: Gdańsk, Poland, 2007. [Google Scholar]

- Grupa LOTOS. LOTOS Social Responsibility Report 2006–2007; Grupa LOTOS S.A.: Gdańsk, Poland, 2008. [Google Scholar]

- Grupa LOTOS. LOTOS Integrated Annual Report 2009. Sustainable Development in the 10+ Perspective; Grupa LOTOS S.A.: Gdańsk, Poland, 2010. [Google Scholar]

- Grupa LOTOS. LOTOS Integrated Annual Report 2010. Decade of Growth; Grupa LOTOS S.A.: Gdańsk, Poland, 2011. [Google Scholar]

- Klein, J. Społeczna odpowiedzialność przedsiębiorstw to nie filantropia. [Corporate social responsibility is not philanthropy]. Interview with Paweł Olechnowicz, CEO of LOTOS Group. Dziennik Bałtycki, 6 September 2011. [Google Scholar]

- Grupa LOTOS. Raport Roczny 2011 na A+ [The Annual Report 2011 for A+]; Grupa LOTOS S.A.: Gdańsk, Poland, 2012. [Google Scholar]

- Grupa LOTOS. LOTOS Integrated Annual Report 2013. Win the Furture; Grupa LOTOS S.A.: Gdańsk, Poland, 2014. [Google Scholar]

- Grupa LOTOS. LOTOS Integrated Annual Report 2011. Responsible Decisions; Grupa LOTOS S.A.: Gdańsk, Poland, 2012. [Google Scholar]

- Twardowska, J. Raportowanie danych finansowych to za mało, [Disclosure of financial data is not enough], podcast during presentation of LOTOS. Available online: https://www.youtube.com/watch?v=PNF2rb89tAc (accessed on 13 February 2019).

- Grupa LOTOS. LOTOS Zmienił Model Raportowania [LOTOS Changes Its Reporting Model]; Grupa LOTOS S.A.: Gdańsk, Poland, 2010. [Google Scholar]

- Grupa LOTOS. Pierwszy Raport CSR [The First CSR Report]; Grupa LOTOS S.A.: Gdańsk, Poland, 2008. [Google Scholar]

- Grupa LOTOS. Dekada Wzrostu [Decade of Growth]; Grupa LOTOS S.A.: Gdańsk, Poland, 2011. [Google Scholar]

- Deegan, C. Introduction: The legitimising effect of social and environmental disclosures—A theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Freeman, R.E.; McVea, J. A Stakeholder Approach to Strategic Management. Working Paper, 1-2. SSRN Electron. J. 2001. [Google Scholar] [CrossRef]

- Frias-Aceituno, J.V.; Rodriguez-Ariza, L.; Garcia-Sanchez, I. The Role of the Board in the Dissemination of Integrated Corporate Social Reporting. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 219–233. [Google Scholar] [CrossRef]

- Nidumolu, R.; Prahalad, C.K.; Rangaswami, M.W. Why sustainability is now the key driver of innovation. Harv. Bus. Rev. 2009, 87, 56–64. [Google Scholar]

- Lodhia, S. Exploring the Transition to Integrated Reporting Through a Practice Lens: An Australian Customer Owned Bank Perspective. J. Bus. Ethics 2015, 129, 585–598. [Google Scholar] [CrossRef]

- Oprisor, T. Auditing Integrated Reports: Are there Solutions to this Puzzle? Procedia Econ. Financ. 2015, 25, 87–95. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

The data structure.

{kind=link}

Table 1.

Overview of reports used in the analysis.

| Relevance for the Analysis | Corporate Document (no. of pages/length) | Component of Narrative Strategy |

|---|---|---|

| Primary relevance | 2006–2007 CSR report (124) 2008 CSR report (132) | The story told in CSR reports |

| 2006 Environmental report (44) | The story told by the company in an environmental report | |

| 2009 Integrated report (164) 2010 Integrated report (337) 2011 Integrated report (402) 2012 Integrated report (483) 2013 Integrated report (469) 2014 Integrated report (468) | The story told by the company in integrated reports | |

| Secondary relevance | 2006 Consolidated Annual Report (174) 2007 Consolidated Annual Report (216) 2008 Consolidated Annual Report (225) 2009 Consolidated Annual Report (269) 2010 Consolidated Annual Report (268) 2011 Consolidated Annual Report (243) 2012 Consolidated Annual Report (205) 2013 Consolidated Annual Report (260) 2014 Consolidated Annual Report (271) | The account of relations between core strategy/financial performance and CSR/sustainability activity |

| 2008 press release (1) 2009 press release (1) 2010 press release (2) 2011 press release (2) 2012 press release (2) 2013 press release (1) 2014 press release (1) 2015 press release (1) | The story told by company representatives on the relations between core strategy/financial performance and to CSR/sustainability. The firm’s motivation for IR explained | |

| 2011 CSR Director’s presentation (1) 2011 CSR Director’s presentation (13 slides) | ||

| 2014 Interview with CEO (1:21 minutes) | ||

| Third tier relevance | LOTOS statute (13) | Additional communication |

| LOTOS development strategy 2011–2015 (22) | ||

| Effective and Rising Program 2013–2015 (49 slides) |

CSR, corporate social reponsibility; IR, integrated reporting; CEO, chief executive officer.

Table 2.

Narrative strategies of integrated reporting.

| Strategy | Company Voice | Company Purpose to be Met | Actors Stakeholder Addressed | Moral Context |

|---|---|---|---|---|

| Legitimizing | CSR outbalances negative impact | License to operate | Stakeholders, Ecology, development, safety, national energy policy | Self-regulation and pro-active approach |

| Shareholder-agency | CSR is a strategic shareholder value driver | Justification for CSR programs | Mainstream investors performance, business risk, shareholder value | Increasing shareholder value and improving financial performance |

| Signaling | Strategic approach to CSR CSR is a driver for innovativeness and competitive advantage. | Attracting investors | SRI investors Long term growth, planning, six capitals | Strategic CSR, stakeholder management |

SRI, socially responsible investing.

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Aluchna, M.; Hussain, N.; Roszkowska-Menkes, M. Integrated Reporting Narratives: The Case of an Industry Leader. Sustainability 2019, 11, 976. https://doi.org/10.3390/su11040976

AMA Style

Aluchna M, Hussain N, Roszkowska-Menkes M. Integrated Reporting Narratives: The Case of an Industry Leader. Sustainability. 2019; 11(4):976. https://doi.org/10.3390/su11040976

Chicago/Turabian StyleAluchna, Maria, Nazim Hussain, and Maria Roszkowska-Menkes. 2019. "Integrated Reporting Narratives: The Case of an Industry Leader" Sustainability 11, no. 4: 976. https://doi.org/10.3390/su11040976

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.