How Do Verified Emissions Announcements Affect the Comoves between Trading Behaviors and Carbon Prices? Evidence from EU ETS

Abstract

:1. Introduction

2. Data

3. Methods

3.1. Determination of Event Windows

3.2. Modeling of Comoves

4. Results

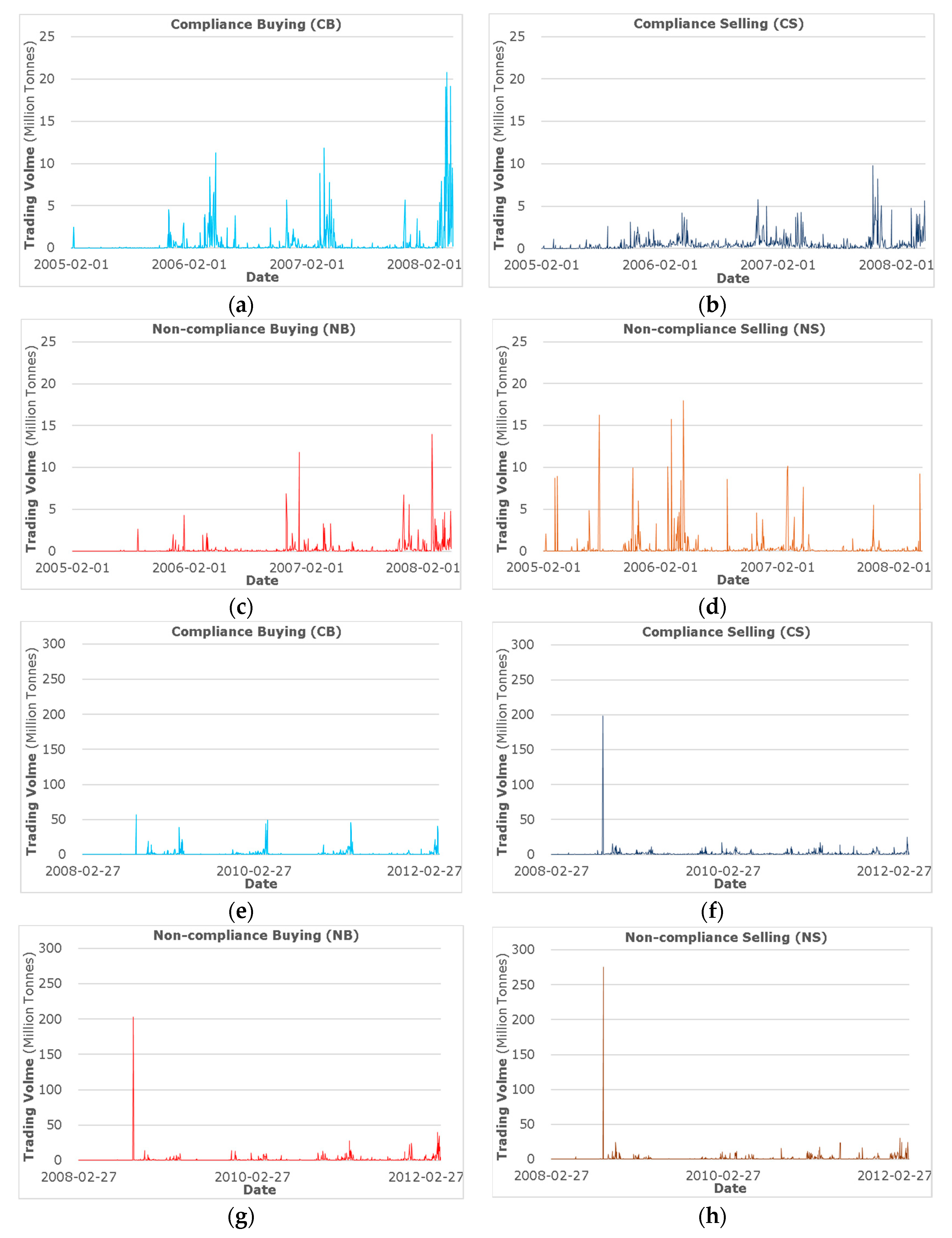

4.1. Observational Results

4.2. Empirical Results

5. Discussion

5.1. Full Impacts on Comoves

5.2. Ex-Ante and Ex-Post Impacts

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Nomenclature

| Abbreviations | |

| ACF | Autocorrelation function |

| ADF | Augmented Dickey–Fuller |

| AR | Autoregressive |

| ARMA | Autoregressive and moving average |

| CB | Compliance buying |

| CITL | Community Independent Transaction Log |

| CS | Compliance selling |

| EU ETS | European Union emissions trading scheme |

| EUA | European Union Allowance |

| EUTL | European Union Transaction Log |

| GARCH | Generalized autoregressive conditional heteroskedastic |

| GHG | Greenhouse gas |

| ICSS | Iterated cumulative sums of squares |

| MA | Moving average |

| NB | Non-compliance buying |

| NS | Non-compliance selling |

| PACF | Partial autocorrelation function |

| Symbols | |

| CP | Carbon price |

| Di | Dummy variable |

| RCP | Logarithm return of the carbon price |

| VCB | Volume of compliance buying |

| VCS | Volume of compliance selling |

| VNB | Volume of non-compliance buying |

| VNS | Volume of non-compliance selling |

| Z | ARCH, autoregressive conditional heteroskedastic |

| σ | GARCH |

| θ | Coefficient |

| β | Coefficient |

| γ | Coefficient |

| λ | Coefficient |

| Superscripts | |

| A | The announcement period |

| C | The complete period |

| I | Phase I |

| II | Phase II |

| PP | The pre- and post-announcement periods |

| Subscripts | |

| a, b, c | Count |

| i | Count |

| t | Time point |

References

- Newell, R.G.; Pizer, W.A.; Raimi, D. Carbon market lessons and global policy outlook. Science 2017, 343, 1316–1317. [Google Scholar] [CrossRef] [PubMed]

- Green, J.F. Don’t link carbon markets. Nature 2017, 543, 484–486. [Google Scholar] [CrossRef] [PubMed]

- Christiansen, A.C.; Wettestad, J. The EU as a frontrunner on greenhouse gas emissions trading: How did it happen and will the EU succeed? Clim. Policy 2003, 3, 3–18. [Google Scholar] [CrossRef]

- Fell, H.; Maniloff, P. Leakage in regional environmental policy: The case of the regional greenhouse gas initiative. J. Environ. Econ. Manag. 2018, 87, 1–23. [Google Scholar] [CrossRef]

- Passey, R.; MacGill, I.; Outhred, H. The governance challenge for implementing effective market-based climate policies: A case study of The New South Wales Greenhouse Gas Reduction Scheme. Energy Policy 2008, 36, 3009–3018. [Google Scholar] [CrossRef]

- Zhang, J.; Zhang, L. Impacts on CO2 emission allowance prices in China: A quantile regression analysis of the Shanghai emission trading scheme. Sustainability 2016, 8, 1195. [Google Scholar] [CrossRef]

- Dai, F.; Xiong, L.; Ma, D. How to set the allowance benchmarking for cement industry in China’s carbon market: Marginal analysis and the case of the Hubei emission trading pilot. Sustainability 2017, 9, 322. [Google Scholar] [CrossRef]

- Yang, B.; Liu, C.; Gou, Z.; Man, J.; Su, Y. How will policies of China’s CO2 ETS affect its carbon price: Evidence from Chinese pilot regions. Sustainability 2018, 10, 605. [Google Scholar] [CrossRef]

- Oh, I.; Yeo, Y.; Lee, J.-D. Efficiency versus Equality: Comparing design options for indirect emissions accounting in the Korean Emissions Trading Scheme. Sustainability 2015, 7, 14982–15002. [Google Scholar] [CrossRef]

- Zhang, Z.; Zhao, Y.; Su, B.; Zhang, Y.; Wang, S.; Liu, Y.; Li, H. Embodied carbon in China’s foreign trade: An online SCI-E and SSCI based literature review. Renew. Sustain. Energy Rev. 2017, 68, 492–510. [Google Scholar] [CrossRef]

- De Perthuis, C.; Trotignon, R. Governance of CO2 markets: Lessons from EU ETS. Energy Policy 2014, 75, 100–106. [Google Scholar] [CrossRef]

- Zeng, Y.; Weishaar, S.E.; Vedder, H.H.B. Electricity regulation in the Chinese national emissions trading scheme (ETS): Lessons for carbon leakage and linkage with EU ETS. Clim. Policy 2018. [Google Scholar] [CrossRef]

- Christiansen, A.C.; Arvanitakis, A.; Tangen, K.; Hasselknippe, H. Price determinants in the EU emissions trading scheme. Clim. Policy 2005, 5, 15–30. [Google Scholar] [CrossRef]

- Sanin, M.E.; Violante, F.; Mansanet-Bataller, M. Understanding volatility dynamics in the EU-ETS market. Energy Policy 2015, 82, 321–331. [Google Scholar] [CrossRef] [Green Version]

- Jia, J.; Xu, J.; Fan, Y. The impact of verified emissions announcements on the European Union emissions trading scheme: A bilaterally modified dummy variable modelling analysis. Appl. Energy 2016, 173, 567–577. [Google Scholar] [CrossRef]

- Fan, Y.; Jia, J.J.; Wang, X.; Xu, J.H. What policy adjustments in EU ETS truly affected the carbon prices? Energy Policy 2017, 103, 145–164. [Google Scholar] [CrossRef]

- European Commission. Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a scheme for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC. Off. J. Eur. Union 2003, 46, 32–46. [Google Scholar]

- Chevallier, J.; Lelpo, F.; Mercier, L. Risk aversion and institutional information disclosure on the European carbon market: A case-study of the 2006 compliance event. Energy Policy 2009, 37, 15–28. [Google Scholar] [CrossRef]

- Alberola, E.; Chevallier, J.; Chèze, B. Price drivers and structural breaks in European carbon prices 2005–2007. Energy Policy 2008, 36, 787–797. [Google Scholar] [CrossRef]

- Hintermann, B. Allowance price drivers in the first phase of EU ETS. J. Environ. Econ. Manag. 2010, 59, 43–56. [Google Scholar] [CrossRef] [Green Version]

- Miclãus, P.G.; Lupu, R.; Dumitrescu, S.A.; Bobircã, A. Testing the efficiency of the European carbon futures market using event-study methodology. Int. J. Energy Environ. 2008, 2, 121–128. [Google Scholar]

- Hitzemann, S.; Uhrig-Homburg, M.; Ehrhart, K.M. The impact of the yearly emissions announcement on CO2 prices: An event study. Inf. Manag. Mark. Eng. 2010, 2, 77–92. [Google Scholar]

- Brouwers, R.; Schoubben, F.; van Hulle, C.; van Uytbergen, S. The initial impact of EU ETS verification events on stock prices. Energy Policy 2016, 94, 138–149. [Google Scholar] [CrossRef]

- Convery, F.J. Origins and development of EU ETS. Environ. Resour. Econ. 2009, 43, 391–412. [Google Scholar] [CrossRef]

- Liu, Y.; Guo, J.; Fan, Y. A big data study on emitting companies’ performance in the first two phases of the European Union Emission Trading Scheme. J. Clean. Prod. 2017, 142, 1028–1043. [Google Scholar] [CrossRef]

- Zaklan, A. Why do emitters trade carbon permits? Firm-level evidence from the European Emission Trading Scheme. In DIW Discussion Papers; DIW Berlin: Berlin, Germany, 2013; p. 32. [Google Scholar]

- Jaraitėkažukauskė, J.; Kažukauskas, A. Do transaction costs influence firm trading ehavior in the European emissions trading system? Environ. Resour. Econ. 2015, 62, 583–613. [Google Scholar] [CrossRef]

- Betz, R.A.; Schmidt, T.S. Transfer patterns in Phase I of the EU Emissions Trading Ssystem: A first reality check based on cluster analysis. Clim. Policy 2016, 16, 474–495. [Google Scholar] [CrossRef]

- Fan, Y.; Liu, Y.; Guo, J. How to explain carbon price using market micro-behaviour? Appl. Econ. 2016, 48, 4992–5007. [Google Scholar] [CrossRef]

- Martin, R.; Muûls, M.; Wagner, U.J. Trading Behavior in the EU Emissions Trading Scheme. Social Science Research Network, 2014. Available online: https://ssrn.com/abstract=2362810 (accessed on 15 April 2018).

- Hepburn, C. Climate change economics: Make carbon pricing a priority. Nat. Clim. Chang. 2017, 7, 389–390. [Google Scholar] [CrossRef]

- Du, S.; Tang, W.; Song, M. Low-carbon production with low-carbon premium in cap-and-trade regulation. J. Clean. Prod. 2016, 134, 652–662. [Google Scholar] [CrossRef]

- Hamilton, J.T. Pollution as news: Media and stock market reactions to the toxics release inventory data. J. Environ. Econ. Manag. 1995, 28, 98–113. [Google Scholar] [CrossRef]

- Bali, T.G.; Bodnaruk, A.; Scherbina, A.; Tang, Y. Unusual news flow and the cross section of stock returns. Manag. Sci. 2017, 64, 3971–4470. [Google Scholar]

- Gabaix, X.; Gopikrishnan, P.; Plerou, V.; Stanley, H.E. Institutional investors and stock market volatility. Q. J. Econ. 2006, 121, 461–504. [Google Scholar] [CrossRef]

- Milunovich, G.; Joyeux, R. Testing market efficiency in EU carbon futures markets. Appl. Financ. Econ. 2010, 20, 803–809. [Google Scholar]

- Creti, A.; Jouvet, P.-A.; Mignon, V. Carbon price drivers: Phase I versus Phase II equilibrium? Energy Econ. 2012, 34, 327–334. [Google Scholar] [CrossRef]

- Ellerman, D.; Buchner, K. Over-allocation or abatement? A preliminary analysis of EU ETS based on the 2005–06 emissions data. Environ. Resour. Econ. 2008, 41, 267–287. [Google Scholar] [CrossRef]

- Anderson, B.; Di Maria, C. Abatement and allocation in the pilot phase of EU ETS. Environ. Resour. Econ. 2011, 48, 83–103. [Google Scholar] [CrossRef]

- Grubb, M.; Azar, C.; Persson, U.M. Allowance allocation in the European emissions trading system: A commentary. Clim. Policy 2005, 5, 127–136. [Google Scholar] [CrossRef]

- Fan, Y.; Xu, J. What has driven oil prices since 2000? A structural change perspective. Energy Econ. 2011, 33, 1082–1094. [Google Scholar] [CrossRef]

- Inclan, C.; Tiao, G.C. Use of cumulative sums of squares for retrospective detection of changes of variance. J. Am. Stat. Assoc. 1994, 89, 913–923. [Google Scholar]

- Aggarwal, R.; Inclan, C.; Leal, R.P. Volatility in emerging stock markets. J. Financ. Quant. Anal. 1999, 34, 33–55. [Google Scholar] [CrossRef]

- Zhu, B.; Chevallier, J.; Ma, S.; Wei, Y. Examining the structural changes of European carbon futures price 2005–2012. Appl. Econ. Lett. 2015, 22, 335–342. [Google Scholar] [CrossRef]

- Ji, Q.; Guo, J. Oil price volatility and oil-related events: An Internet concern study perspective. Appl. Energy 2015, 137, 256–264. [Google Scholar] [CrossRef]

- Efimova, Q.; Serletis, A. Energy markets volatility modelling using GARCH. Energy Econ. 2014, 43, 264–273. [Google Scholar] [CrossRef]

- Guo, J.; Ji, Q. How does market concern derived from the Internet affect oil prices? Appl. Energy 2013, 112, 1536–1543. [Google Scholar] [CrossRef] [Green Version]

- Mi, Z.; Zhang, Y. Estimating the ‘value at risk’ of EUA futures prices based on the extreme value theory. Int. J. Glob. Energy Issues 2011, 35, 145–157. [Google Scholar] [CrossRef]

- Mi, Z.; Wei, Y.; Tang, B.; Cong, R.; Yu, H.; Cao, H.; Guan, D. Risk assessment of oil price from static and dynamic modelling approaches. Appl. Econ. 2017, 49, 929–939. [Google Scholar] [CrossRef]

- Zhang, Y.; Liu, Z.; Yu, X. The diversification benefits of including carbon assets in financial portfolios. Sustainability 2017, 9, 437. [Google Scholar] [CrossRef]

- Balcılar, M.; Demirer, R.; Hammoudeh, S.; Nguyen, D.K. Risk spillovers across the energy and carbon markets and hedging strategies for carbon risk. Energy Econ. 2016, 54, 159–172. [Google Scholar] [CrossRef] [Green Version]

- Daskalakis, G. On the efficiency of the European carbon market: New evidence from Phase II. Energy Policy 2013, 54, 369–375. [Google Scholar] [CrossRef]

- Farmer, J.D. Market efficiency and the long-memory of supply and demand: Is price impact variable and permanent or fixed and temporary? Quant. Financ. 2006, 6, 107–112. [Google Scholar] [CrossRef]

- Daskalakis, G. Temporal restrictions on emissions trading and the implications for the carbon futures market: Lessons from the EU emissions trading scheme. Energy Policy 2018, 115, 88–91. [Google Scholar] [CrossRef]

- Grubb, M.; Neuhoff, K. Allocation and competitiveness in the EU emissions trading scheme: Policy overview. Clim. Policy 2006, 6, 7–30. [Google Scholar] [CrossRef]

- Benz, E.; Loschel, A.; Sturm, B. Auctioning of CO2 emission allowances in Phase 3 of the EU Emissions Trading Scheme. Clim. Policy 2010, 10, 705–718. [Google Scholar] [CrossRef]

- Joltreau, E.; Sommerfeld, K. Why Does Emissions Trading under the EU Emissions Trading System (ETS) Not Affect Firms’ Competitiveness? Empirical Findings from the Literature. Joltreau, Eugénie and Sommerfeld, Katrin, Why Does Emissions Trading under the EU Ets Not Affect Firms’ Competitiveness? Empirical Findings from the Literature. IZA Discussion Paper No. 11253. Available online: https://ssrn.com/abstract=3097371 (accessed on 15 April 2018).

- Ang, B.W.; Su, B. Carbon emission intensity in electricity production: A global analysis. Energy Policy 2016, 94, 56–63. [Google Scholar] [CrossRef]

- Su, B.; Ang, B.W. Multiplicative structural decomposition analysis of aggregate embodied energy and emission intensities. Energy Econ. 2017, 65, 137–147. [Google Scholar] [CrossRef]

- Zhang, M.; Su, B. Assessing China’s rural household energy sustainable development using improved grouped principal component method. Energy 2016, 113, 509–514. [Google Scholar] [CrossRef]

{kind=link}

| Mean | Std. dev | Skewness | Kurtosis | Maximum | |||

|---|---|---|---|---|---|---|---|

| Phase I | Complete Period | CB | 0.515 | 1.867 | 6.713 | 58.889 | 20.793 |

| CS | 0.552 | 0.922 | 4.291 | 28.492 | 9.829 | ||

| NB | 0.412 | 1.730 | 7.210 | 61.974 | 17.985 | ||

| NS | 0.243 | 0.895 | 8.982 | 110.484 | 13.955 | ||

| Announcement period | CB | 0.924 | 1.990 | 3.198 | 14.246 | 11.831 | |

| CS | 0.710 | 0.811 | 2.776 | 11.013 | 4.297 | ||

| NB | 0.826 | 2.421 | 4.736 | 27.658 | 17.985 | ||

| NS | 0.218 | 0.505 | 4.306 | 23.141 | 3.305 | ||

| Pre-announcement period | CB | 1.148 | 2.396 | 2.832 | 11.008 | 9.831 | |

| CS | 0.815 | 0.834 | 2.448 | 8.969 | 4.213 | ||

| NB | 1.302 | 3.182 | 3.505 | 15.611 | 13.965 | ||

| NS | 0.279 | 0.587 | 3.397 | 14.759 | 3.305 | ||

| Post-announcement Period | CB | 0.708 | 1.425 | 2.797 | 11.152 | 7.747 | |

| CS | 0.627 | 0.826 | 3.049 | 12.349 | 4.297 | ||

| NB | 0.313 | 0.910 | 6.523 | 51.567 | 7.682 | ||

| NS | 0.155 | 0.387 | 6.420 | 50.994 | 3.277 | ||

| Phase II | Complete Period | CB | 0.585 | 1.893 | 6.090 | 46.328 | 12.025 |

| CS | 0.568 | 2.236 | 25.823 | 762.295 | 4.189 | ||

| NB | 0.614 | 3.119 | 17.510 | 351.245 | 4.289 | ||

| NS | 0.599 | 3.429 | 24.226 | 649.108 | 5.811 | ||

| Announcement period | CB | 1.046 | 2.278 | 3.881 | 20.482 | 8.212 | |

| CS | 0.711 | 1.177 | 4.613 | 32.619 | 3.589 | ||

| NB | 0.847 | 1.708 | 4.089 | 23.243 | 2.213 | ||

| NS | 0.806 | 1.432 | 3.229 | 15.934 | 2.183 | ||

| Pre-announcement period | CB | 1.201 | 2.441 | 3.790 | 19.164 | 9.694 | |

| CS | 0.872 | 1.179 | 3.518 | 18.238 | 3.329 | ||

| NB | 1.140 | 2.029 | 3.435 | 16.650 | 3.839 | ||

| NS | 1.088 | 1.600 | 2.771 | 12.804 | 5.459 | ||

| Post-announcement Period | CB | 0.598 | 1.673 | 4.785 | 30.448 | 9.694 | |

| CS | 0.432 | 0.754 | 3.943 | 22.566 | 3.178 | ||

| NB | 0.321 | 0.611 | 3.043 | 12.854 | 3.387 | ||

| NS | 0.298 | 0.553 | 3.096 | 13.972 | 5.646 | ||

| Variable | Coefficient | Z-Statistic | Pr. | |||

|---|---|---|---|---|---|---|

| Phase I | Complete Period | Mean Equation (Equation (2)) | ||||

| θ1I,C | 7.04 × 10−4 | 0.141 | 0.888 | |||

| θ2I,C | −0.205 | −3.115 | 0.002 *** | |||

| θ3I,C | 2.54 × 10−3 | 2.879 | 0.004 *** | |||

| θ4I,C | −4.73 × 10−3 | −1.744 | 0.081 * | |||

| Variance Equation (Equation (4)) | ||||||

| β1I,C | 2.10 × 10−3 | 4.779 | 0.000 *** | |||

| β2I,C | 0.145 | 3.641 | 0.000 *** | |||

| β3I,C | 0.550 | 6.608 | 0.000 *** | |||

| γ1I,C | −1.38 × 10−4 | −743.052 | 0.000 *** | |||

| γ2I,C | −4.70 × 10−4 | −14.844 | 0.000 *** | |||

| Announcement Period | Mean Equation (Equation (2)) | |||||

| θ1I,A | 1.30 × 10−3 | 0.268 | 0.789 | |||

| θ2I,A | −0.196 | −3.080 | 0.002 *** | |||

| θ3I,A | 2.53 × 10−3 | 3.010 | 0.002 *** | |||

| θ4I,A | −4.92 × 10−3 | −1.880 | 0.060 * | |||

| Variance Equation (Equation (6)) | ||||||

| β1I,A | 2.07 × 10−3 | 4.487 | 0.000 *** | |||

| β2I,A | 0.143 | 3.757 | 0.001 *** | |||

| β3I,A | 0.540 | 6.195 | 0.000 *** | |||

| γ1I,A | −8.47 × 10−5 | −0.413 | 0.680 | |||

| γ2I,A | −4.34 × 10−4 | −1.701 | 0.089 * | |||

| λ1I,A | −5.95 × 10−5 | −0.296 | 0.768 | |||

| λ2I,A | −6.24 × 10−4 | −1.698 | 0.090 * | |||

| Phase II | Complete Period | Mean Equation (Equation (3)) | ||||

| AR(1)II,C | 2.76 × 10−2 | 0.036 | 0.971 | |||

| MA(1)II,C | −1.59 × 10−2 | −0.021 | 0.984 | |||

| Variance Equation (Equation (4)) | ||||||

| β1II,C | 9.92 × 10−6 | 3.045 | 0.002 *** | |||

| β2II,C | 0.128 | 8.267 | 0.000 *** | |||

| β3II,C | 0.862 | 51.658 | 0.000 *** | |||

| γ1II,C | −8.11 × 10−4 | −1.624 | 0.105 | |||

| γ2II,C | 1.61 × 10−3 | 1.997 | 0.046 ** | |||

| Announcement Period | Mean Equation (Equation (3)) | |||||

| AR(1)II,A | 0.968 | 25.979 | 0.000 *** | |||

| MA(1)II,A | −0.971 | −26.478 | 0.000 *** | |||

| Variance Equation (Equation (6)) | ||||||

| β1II,A | 9.83 × 10−6 | 2.943 | 0.003 *** | |||

| β2II,A | 0.119 | 7.904 | 0.000 *** | |||

| β3II,A | 0.868 | 53.023 | 0.000 *** | |||

| γ1II,A | −1.84 × 10−4 | −0.189 | 0.850 | |||

| γ2II,A | 2.14 × 10−3 | 1.109 | 0.268 | |||

| λ1II,A | −2.97 × 10−3 | −2.344 | 0.019 ** | |||

| λ2II,A | 1.53 × 10−3 | 0.693 | 0.488 | |||

| Variable | Coefficient | Z-Statistic | Pr. | ||

|---|---|---|---|---|---|

| Phase I | Pre- and Post-Announcement Periods | Mean Equation (Equation (2)) | |||

| θ1I,PP | 9.69 × 10−4 | −0.207 | 0.836 | ||

| θ2I,PP | −0.196 | −3.095 | 0.002 *** | ||

| θ3I,PP | 2.50 × 10−3 | 2.954 | 0.003 *** | ||

| θ4I,PP | −4.99 × 10−3 | −1.905 | 0.057 * | ||

| Variance Equation (Equation (9)) | |||||

| β1I,PP | 2.07 × 10−3 | 4.513 | 0.000 *** | ||

| β2I,PP | 0.143 | 3.741 | 0.000 *** | ||

| β3I,PP | 0.542 | 6.245 | 0.000 *** | ||

| γ1I,PP | −1.33 × 10−4 | −6.812 | 0.000 *** | ||

| γ2I,PP | −4.22 × 10−4 | −5.581 | 0.000 *** | ||

| λ1I,PP | −6.11 × 10−4 | −2.532 | 0.011 ** | ||

| λ2I,PP | −1.01 × 10−3 | −2.277 | 0.023 ** | ||

| Phase II | Pre- and Post-Announcement Periods | Mean Equation (Equation (3)) | |||

| AR(1)II,PP | −1.96 × 10−2 | −0.027 | 0.978 | ||

| MA(1)II,PP | 3.13 × 10−2 | 0.043 | 0.966 | ||

| Variance Equation (Equation (10)) | |||||

| β1II,PP | 6.68 × 10−6 | 2.138 | 0.033 ** | ||

| β2II,PP | 0.103 | 7.409 | 0.000 *** | ||

| β3II,PP | 0.885 | 58.115 | 0.000 *** | ||

| γ1II,PP | 3.87 × 10−3 | 3.501 | 0.001 *** | ||

| γ2II,PP | −8.45 × 10−4 | −1.247 | 0.212 | ||

| λ1II,PP | −2.73 × 10−3 | −3.544 | 0.000 *** | ||

| λ2II,PP | −7.77 × 10−5 | −0.043 | 0.966 | ||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guo, J.; Su, B.; Yang, G.; Feng, L.; Liu, Y.; Gu, F. How Do Verified Emissions Announcements Affect the Comoves between Trading Behaviors and Carbon Prices? Evidence from EU ETS. Sustainability 2018, 10, 3255. https://doi.org/10.3390/su10093255

Guo J, Su B, Yang G, Feng L, Liu Y, Gu F. How Do Verified Emissions Announcements Affect the Comoves between Trading Behaviors and Carbon Prices? Evidence from EU ETS. Sustainability. 2018; 10(9):3255. https://doi.org/10.3390/su10093255

Chicago/Turabian StyleGuo, Jianfeng, Bin Su, Guang Yang, Lianyong Feng, Yinpeng Liu, and Fu Gu. 2018. "How Do Verified Emissions Announcements Affect the Comoves between Trading Behaviors and Carbon Prices? Evidence from EU ETS" Sustainability 10, no. 9: 3255. https://doi.org/10.3390/su10093255