A Study on the Sustainable Growth of SMEs: The Mediating Role of Organizational Metacognition

1

Department of Industrial Engineering, Konkuk University, 120 Neungdong-ro, Gwangjin-gu, Seoul 05029, Korea

2

Department of Advanced Industry Fusion, Konkuk University, 120 Neungdong-ro, Gwangjin-gu, Seoul 05029, Korea

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(8), 2829; https://doi.org/10.3390/su10082829

Submission received: 28 June 2018

/

Revised: 4 August 2018

/

Accepted: 6 August 2018

/

Published: 9 August 2018

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:This study investigates a method to improve small- and medium-sized enterprises’ (SMEs’) business performance and organizational effectiveness for sustainable growth. This study hypothesizes that technological innovation capabilities have a positive impact on business performance and organizational effectiveness and that metacognition at the organizational level has a mediating role in the relationship. To verify the relationship, this study conducts an empirical analysis using a survey questionnaire. The findings are as follows. First, technological innovation capability has a positive effect on both business performance and organizational effectiveness. Second, organizational metacognition has a partial mediating effect on the effect of technological innovation capability on business performance and organizational effectiveness. The results suggest that chief executive officer (CEO) and middle managers contemplate the methodology of metacognition at the organizational level and that they should focus more on enhancing business performance by developing technological innovation capability and organizational metacognition.

1. Introduction

Amplified uncertainty in the business environment in recent times has added to the difficulty of improving performance and securing a competitive advantage for sustainable growth. According to Consumer News and Business Channel’s Global Uncertainty Index, which measures the degree of uncertainty, 2016 witnessed the most uncertainty since the global financial crisis in 2009. In addition, both large firms as well as small- and medium-sized enterprises (SMEs) faced adverse business environments, such as Brexit and the strong dollar policy of the U.S. in overseas markets. In particular, compared with the industry ecosystem for SMEs in Europe, the industry ecosystem in Korea is not favorable to SMEs. SMEs in Korea face more difficult problems and need strategies to ensure sustainable growth at the company level [1].

To overcome these adverse circumstances and pursue sustainable growth, both SMEs and large companies prepare long-term growth strategies to strengthen their technological innovation capability. A firm’s survival is based on its business performance, which is fundamental for economic growth [2]. However, a firm’s sustainable growth is not the result of a single, specific factor but rather a combination of company strategy, structure, and processes that fit together [3].

Although SMEs would like to become more competitive and sustainable by reinforcing their technological innovation capabilities to survive and grow in an era of uncertainty, it is difficult for them to link their innovation capabilities to performance due to limitations such as firm size and a lack of resources compared with large firms [4,5,6,7]. From the resource-based view, firm size is an important resource that influences profitability and performance [8]. Large firms have superior advantages in term of resources and capabilities compared with SMEs [9]. Firm size, as a description of a firm’s resource endowment, generally has an important link to planning, because forming and implementing the firm’s strategies requires a commitment of scarce resources [10]. Implementing technological innovation and strategy generally relies on planning, problem-solving, and the firm’s innovative behavior—areas that are affected by the firm size. In addition, empirical research shows that the revenue of small firms decreases in production innovation [11].

Overall, SMEs are in a relatively unfavorable condition to improve their performance and pursue continuous growth through technological innovation. To address these limitations, SMEs would like to manage and establish the metacognition of the workforce as an internal strategic resource that can lead to innovative behaviors and solve problems [12]. In particular, metacognition is the process of thinking using the concept of cognition; it is a function of understanding the cognitive process [13]. It also refers to planning and checking the process of thinking in order to solve problems. It plays a pivotal role in problem-solving and influences the performance and creativity of the task [14,15,16,17,18]. According to OECD studies, SMEs that provide employees with opportunities to develop problem-solving skills and make use of their knowledge are more likely than others to succeed in developing new products or processes [19]. Thus, metacognition utilized in the process of solving problems can help SMEs’ technological innovation capabilities lead to performance. In other words, metacognition in the problem-solving process helps employees identify the problem rationally and implement the appropriate strategy.

Although some prior research (e.g., [12,20,21]) investigates the relationship between metacognition and SME performance, they focus on the metacognition of the CEO and top management at the individual level. Thus, this study aims to address the limitations of prior studies by considering the metacognition of SMEs’ human resources at the organizational level.

In all, this study posits the relationship between SMEs’ technological innovation capability and business performance and organizational effectiveness. Specifically, this study hypothesizes that technological innovation capability increases business performance and organizational effectiveness, and this relationship is mediated by organizational metacognition.

This study was designed to complement and bridge the gap in the literature by analyzing the relationship between technological innovation capability and SME performance. Although many studies on SMEs’ technological innovation capabilities exist, they are relatively limited to the technology itself, and there is little extant research on metacognition at the organizational level. Thus, this study will contribute to our understanding of the mechanism by which metacognition at the organizational level plays an important role in enhancing technological innovation and performance in SMEs. This study will help CEOs and managers to enhance their firms’ competitiveness.

2. Materials and Methods

2.1. Concepts and Theoretical Background

2.1.1. Technological Innovation Capability

Technology innovation capability is a combination of technology innovation and capability; it is the organizational ability to carry out the process of developing, introducing, and adopting ideas and technologies for new products, services, and production processes [21]. According to the resource-based view, technological innovation capability is a very important resource for securing a firm’s competitive advantage as a set of firm characteristics that promote and support technological innovation [22]. Burgelman, Christensen, and Wheelwright [23] emphasize that technological innovation capability that promotes and supports corporate innovation strategies is an important internal resource. The Korean government and research institutes advise that SMEs should strive for technological innovation and build innovation capabilities to survive and grow continuously during the Fourth Industrial Revolution [24,25].

Although various studies on technological innovation capability exist, they focus mainly on output—such as R&D expenditures—and the number of inputs and new products—such as the number of researchers and the economic evaluation of innovative technologies. However, some authors criticize this type of measurement for being limited to the consequences of disembodied innovation activities and ignoring the importance of innovation activities, accumulated knowledge, and improved organizational capabilities [26]. Thus, these superficial methods cannot accurately measure the technological innovation capabilities of SMEs.

On the other hand, technological innovation is difficult to achieve in a short time, and firms must invest significant time and money. In this regard, some studies [27,28] advise that firms should manage the process of technological innovation activities effectively and argue that the organization’s strategic and management capability is important for generating performance. In other words, the technical view alone cannot explain technological innovation performance and successful technology innovation activities.

2.1.2. Organizational Metacognition

Metacognition refers to the process of thinking via a concept of cognition and a function of understanding the cognitive process [13]. It also includes planning and checking the process of thinking in order to solve the problem. Metacognition in the problem-solving process makes it possible to identify the problem rationally and to implement the appropriate strategy [14,15,16,17,18]. Metacognition is a higher-dimensional heuristic method individuals apply to process information about their environment [29]. In other words, it is the ability to regulate and control the use of knowledge and experience in an unfamiliar environment and situation [30].

In general, metacognition consists of two main functions: monitoring and control [30,31]. Metacognitive monitoring refers to the processes that allow the individual to observe, reflect on, or experience his or her own cognitive processes [32]. Monitoring includes processes such as identifying the task, checking and evaluating one’s progress, and predicting the outcomes of that progress [30]. Metacognitive control refers to the conscious and nonconscious decisions that an individual makes, based on the output of his or her monitoring processes [30]. The metacognitive control process is critical to learning, making effective judgments, and sharing knowledge [33]. In these primary functions of metacognition, monitoring and control work in tandem and thereby enable an individual to regulate his or her information processing based on the requirements of the task at hand.

In summary, authors argue consistently that metacognition plays an essential role in individual learning and problem-solving processes, and is an important variable that influences performance, the creativity of the task, and innovation [20,21,22,23,30,31,32,33]. Thus, metacognition utilized in the process of solving problems can enable SMEs’ technological innovation capability to lead to performance improvement. In other words, metacognition in the problem-solving process helps to identify the problem rationally and implement the appropriate strategy.

Despite the general understanding that metacognition helps learning and problem-solving, it is still inconclusive in terms of SME performance. Some prior research works (e.g., [13,20,21]) study the relationship between metacognition and SME performance; however, they focus on the metacognition of the CEO and top management at the individual level. Although other research on metacognition investigates collaborative metacognition [34] and socially shared metacognition [35], the studies were conducted on students. Thus, this study adopts and expands Brown’s metacognition measurement approach and tool [15] to examine the influence of organizational metacognition on business performance and organizational effectiveness. The content validity and face validity were secured through experts in business administration, management engineering, psychology, and education engineering.

2.1.3. Business Performance

Business performance refers to achievements due to the firm’s management activities. In general, measurements of business performance are divided into financial and nonfinancial methods [36]. Financial performance refers to the quantitative results of management activities. Gupta and Govindarajan [37] use the increase in sales, profit growth, and market share to measure financial performance. However, short-term financial performance has a limited ability to assess corporate competitiveness in a competitive environment, and others emphasize the importance of nonfinancial information [38,39]. Therefore, this study defines the concept of business performance due to management activities as a combination of financial and nonfinancial performance to consider in SMEs’ long-term growth based on previous studies [37,38,39]. This study focuses on the sales growth rate, return rate, and cash flow to measure financial performance, and customer growth, market share, company image, and brand awareness to assess nonfinancial performance.

This study utilizes a subjective assessment as a proxy indicator of economic performance following previous research [36,40], showing that it is possible to measure a firm’s economic performance through subjective evaluation. These measures consider that SMEs are also increasingly reluctant to disclose performance-related indicators such as financial statements because of information security.

2.1.4. Organizational Effectiveness

Organizational effectiveness is the degree to which an organization achieves its goals [41] or the degree to which it meets the needs of its members and participants in a balanced manner [42]. In other words, how well the organization achieves its desired situation can explain organizational effectiveness. The concept of organizational effectiveness is still in the nascent stage, and despite much research on organizational effectiveness, there are no agreed conclusions on consistent goals, determinants, and measurements [43]. Steer [44], who studied organizational effectiveness over a long period and established measures of organizational effectiveness, describes 14 factors of organizational effectiveness such as adaptability, flexibility, productivity, job satisfaction, organizational commitment, intended turnover, and so on.

In this study, the core factors of organizational effectiveness are composed of creativity and work performance following preceding studies. As noted above, metacognition can be an influential factor in creativity, innovative behavior, and work performance [13,20,21] because it is more relevant to the cognitive process than other factors of organizational effectiveness are. Creativity is a concept that identifies the ability to create new, innovative, and useful ideas, processes, services, and products. In particular, creativity is assuming an even more important role in the Fourth Industrial Revolution [24], as it accelerates digital transformation [4,45]. Work performance is the concept of how successful an organization is in performing its tasks.

2.2. Hypotheses

2.2.1. Effect of SMEs’ Technological Innovation Capability on Business Performance

Technological innovation capability is a very important resource for securing competitive advantage in both large firms and SMEs. It is a set of firm characteristics that promote and support technological innovation strategies [22]. Specially, innovation, including technology and management, is a key determinant of productivity and long-term growth. On average, SMEs are less innovative and have less access to resources. Thus, technological innovation is difficult for SMEs to achieve in a short time, because they must invest significant time and money. Moreover, the technology life cycle is getting shorter and more uncertain [26].

However, some SMEs are highly innovative and can enhance productivity levels. Companies that develop and use their internal strategic resources effectively (e.g., managerial and workforce skills, Information and Communications Technologies, R&D, etc.) have better performance [19]. Some prior studies [26,46] demonstrate empirically that technological innovation capability indicators such as R&D expenditures have a positive effect on business performance. However, others criticize this type of measurement for being limited to the consequences of disembodied innovation activities and ignoring the importance of innovation activities, accumulated knowledge, and improved organizational capabilities [47].

In contrast to the positive effect of technological innovation capability on SMEs, some studies argue that such capability does not affect the sales growth rate, even if R&D investment and external technology cooperation levels are high [48]. Dowling and McGee [49] also find that capabilities such as external technology cooperation are not significant for sales growth. Therefore, this study develops the following hypotheses to address the research gap and explore the empirical relationships between technological innovation capabilities and business performance.

Hypothesis 1.

Technological innovation capability has a positive impact on business performance.

Hypothesis 1.1.

Technological innovation capability has a positive impact on financial performance.

Hypothesis 1.2.

Technological innovation capability has a positive impact on nonfinancial business performance.

2.2.2. Effect of SMEs’ Technological Innovation Capability on Organizational Effectiveness

A firm’s competitive advantage can arise from its efficiency and capability to develop new products [50]. As mentioned above, SMEs are in a relatively unfavorable condition compared with large firms. Specially, in the context of the Fourth Industrial Revolution, where competition between countries and companies is fierce, the capability to innovate and implement new technology is growing more important [51]. Technological innovation capability is a comprehensive set of firm characteristics that facilitate and support technological innovation strategies [24]. They are special assets or resources that include technology, product, process, knowledge, experience, and organization [52]. Consequently, these characteristics of technological innovation capability could affect the organization overall. Various researchers and institutions develop different approaches and demonstrate the positive effect of technological innovation capability on organizational and SME performance [26,47,53,54,55].

Despite the fact that technological innovation capability could influence an organization thoroughly, previous studies [53,54,55] on the effect of technological innovation capability mainly lean toward consequence-oriented measurements such as sales performance, product performance, and so on. Therefore, this study develops the following hypotheses to investigate the empirical relationships between technology innovation capability and organizational effectiveness factors, and to bridge the research gap.

Hypothesis 2.

Technological innovation capability has a positive impact on organizational effectiveness.

Hypothesis 2.1.

Technological innovation capability has a positive impact on creativity.

Hypothesis 2.2.

Technological innovation capability has a positive impact on work performance.

2.2.3. Mediating Role of Organizational Metacognition

As the life cycle of technologies becomes shorter and more uncertain, and their development directions uncertain, firms’ technology planning capabilities have become increasingly important [26]. Implementing technology innovation and strategy generally relies on the firm’s planning, problem-solving, and innovative behavior. However, firm size can affect this ability. Thus, SMEs are in a relatively unfavorable condition to implement and achieve technological innovation. Metacognition refers to the process of thinking via a concept of cognition and is a function of understanding the cognitive process [13]. It also includes planning and checking the process of thinking in order to solve the problem. Metacognition in the problem-solving process makes it possible to identify the problem rationally and to implement the appropriate strategy [14,15,16,17,18]. Metacognition is a higher-dimensional heuristic method individuals apply to process information about their environment [29]. In other words, it is the ability to regulate and control the use of knowledge and experience in unfamiliar environments and situations [30]. From this point of view, metacognition will have a major impact on processes involving the introduction and execution of ideas in the previous and process stage of technological innovation.

Successful technological innovation does not stem from technology alone. In this regard, some studies [27,28] argue for recognizing the importance of activities such as planning and managing the process of technological innovation implementation. Specifically, it is more likely that SMEs will control many unexpected problems in the technology innovation process and implementation. Metacognition also plays a pivotal role in problem-solving and influences the performance and creativity of the task [14,15,16,17,18]. In addition, metacognition is an important factor in enhancing innovation [12]. In this regard, metacognition applied to the process of problem-solving and innovation can allow SMEs’ technological innovation to enhance their performance.

Hypothesis 3.

Organizational metacognition has a mediating effect on the relationship between technological innovation capability and business performance.

Hypothesis 4.

Organizational metacognition has a mediating effect on the relationship between technological innovation capability and organizational effectiveness.

2.3. Method

2.3.1. Research Model

The factors used in this study are technological innovation capability (independent variable), organizational metacognition (mediator), and business performance and organizational effectiveness (dependent variables). Figure 1 presents the research model.

2.3.2. Sampling and Analysis of Respondents’ Demographic Factors

This research focuses on SMEs. In general, SMEs in Korea are enterprises with no more than 500 employees. The Korean government and organizations (e.g., Ministry of SMEs and Startups, Small and Medium Business Corporation) usually work according to this criterion. To test the hypotheses, this study used a survey targeting Korean SMEs from April 2017 to July 2017. The survey was conducted in training and education centers, fairs, and convention centers, even in the factories. A door-to-door system could be applied in order to increase the response rate (response rate: 90%). Consequently, a total of 415 copies were collected and used in the data analysis. Table 1 presents the key characteristics of the sample, including the respondents’ gender, age, position, industry, and the number of employees.

2.3.3. Measurement of Variables

This study focused on four major variables: technological innovation capability, organizational metacognition, business performance, and organizational effectiveness. The survey items to examine the main factors and subfactors were based on modified and revised questions in prior research. The exploratory factor analysis was conducted to confirm whether or not the measurement tools used in this research are validly measuring the actual concept.

As a result of setting factor extraction method as a principal component and applying the Varimax rotation for rotating factors, 6 factors having a factor loading above 0.5 were extracted. The accumulation rate of the rotation sums of squared loadings came out to be 69.055. It can be seen that 7 factors under which 47 variables are categorized have an explanatory power of 69%.

As shown in Table 2, the fit value of the Kaiser–Meyer–Olkin (KMO) measure is 0.949 and this means that the factor analysis is highly appropriate and fair. Barlett’s sphericity test is used to determine the correlation between the variables while conducting the factor analysis. In this research, the significant percentage came out to be 0.000; thus, the independence is suitable for the factor analysis. The Cronbach’s alpha value used for verifying reliability verifies the internal consistency of the variables measured through various items relating to one concept. The Cronbach’s alpha values calculated from the survey items measured in this research ranged from 0.889 to 0.969 as shown in Table 3. This finding means that the reliability is high because of the fact that the values were all above 0.7.

Technological Innovation Capability

In this study, technological innovation capability is an organizational capability that is essential for companies to implement technology innovation strategies. To examine technological innovation capability comprehensively, this study used 18 questions verified in Bowen’s [56] measurement development study to assess three subfactors: R&D capability, technology accumulation capability, and technology innovation system. Each item consisted of a 5-point Likert scale.

Organizational Metacognition

Metacognition refers to the knowledge of cognitive processes or the ability to control or adjust cognitive processes. It plays a key role in planning, checking, and controlling the problem-solving process. This study adopted and expanded Brown’s metacognition measurement approach and tool [15] to examine organizational metacognition. In this study, organizational metacognition is defined as the aggregate of metacognition that organizational members utilize in the problem-solving process to achieve performance. This study used 10 verified questions and constructed the questionnaire items using metacognition factors such as planning, evaluation, and regulation, which play a major role in the problem-solving process. Each item consisted of a 5-point Likert scale.

Business Performance

Business performance refers to the sum of financial and nonfinancial performance resulting from management activities. Financial performance includes factors such as the sales growth rate, return rate, and cash flow. Nonfinancial performance includes the increase in customers, market share, company and brand image, and awareness as the main factors. In this study, 12 items were selected based on previous studies [28,31,40] and measured using 5-point Likert scales.

Organizational Effectiveness

Organizational effectiveness is the extent to which an organization achieves its goals. Several studies examine the factors and measurement standards of organizational effectiveness. This study defined creativity and work performance as the key factors and measured each using 5-point Likert scales [44].

2.3.4. Assessing Common Bias

While the researchers collected questionnaires at regular intervals to address common method bias, this bias cannot be removed perfectly because all items in the questionnaire were measured using the same method (a survey) [57]. Consequently, to assess the likelihood of common method bias, confirmatory factor analysis (CFA) and was performed. The results were as follows: x2 = 2013.312 (df = 1012, p = 0.000), x2/df = 1.989, goodness-of-fit-index (GFI) = 0.840, adjusted goodness-of-fit-index (AGFI) = 0.811, normed fit index (NFI) = 0.883, turker-lewis index (TLI) = 0.970, comparative fit index (CFI) = 0.938, root mean square residual (RMR) = 0.037, root mean square error of approximation (RMSEA) = 0.049, and p of close fit (PCLOSE) = 0.718. These results show no statistical significance; that is, it was not seriously fit for the analysis.

Through the CFA, the standardized loading (factor loading) and average variance extracted were calculated. All variables used in this research indicated that both the standardized loading value and the average variance extracted are above 0.5, and construction reliability is above 0.7. Therefore, the results confirm convergent validity.

In addition, the discriminant was verified. As Table 4 shows, the correlation square among all factors was less than the average variance extracted per factor. Therefore, the results confirm that the factors in this research model have discriminant validity.

3. Analysis and Results

3.1. Measurement Model Results

In this study, the research model of the hypothesis set technological innovation capability as the exogenous variable, and organizational metacognition, business performance, and organizational effectiveness as endogenous variables. Specifically, technological innovation capability is an independent variable; organizational metacognition is a mediating variable; and creativity, work performance, financial performance, and nonfinancial performance are dependent variables.

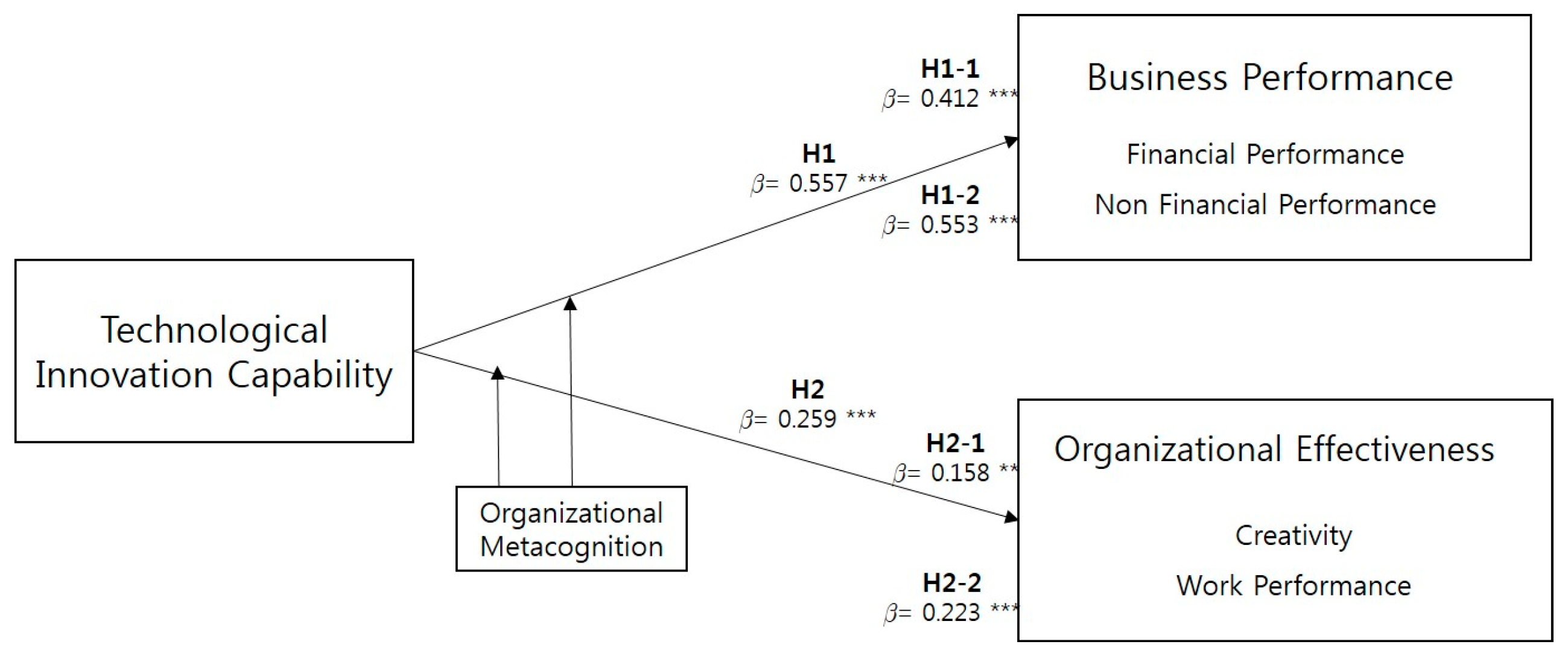

AMOS 20 was used to verify the magnitude, influence, and moderating effect among the variables in the research model. Figure 2 presents the results of the path coefficient calculations. A CFA was conducted to verify the validity of the items through the exploratory factor analysis and reliability verification. In the CFA model, the Chi-square value was 2013.312, the df was 1012, the p-value was 0.000, and chi-square divided by degrees of freedom (CMIN/DF) was 1.989. The Chi-square statistic is used to check if a model is suitable for the data. The p-value and the Chi-square value are inversely proportional to each other. The fit is considered high if the p-value is more than 0.05. Although p-value is below 0.05, the model is considered fit when the CMIN/DF is below 3.0.

In this model, the Chi-square value is 2460.511, the df value is 10225, the p-value is 0.000, the CMIN/DF value is 2.089, the GFI value is 0.820, the AGFI value is 0.800, the RMR value is 0.038, the RMSEA value is 0.051, the PCLOSE value is 0.242, the NFI value is 0.877, the IFI value is 0.038, the RFI value is 0.869, the TLI value is 0.927, the CFI value is 0.931, the PGFI value is 0.739, the PNFI value is 0.825, and the PCFI value is 0.8761. The fit of the structural equation models is thus appropriate.

3.2. Hypothesis Testing

3.2.1. Hypotheses 1 and 2

Table 5 shows the results of the structural equation modeling analysis to test the hypotheses.

For Hypothesis 1, that technological innovation capability has a positive impact on business performance, the size of the influence is 0.557, which confirms that technological innovation capability has a significantly (critical ratio (C.R). = 8.406 > 1.96, p = 0.000 < 0.001) positive (+) influence on business performance. This indicates that SMEs’ technological innovation capabilities increase business performance. Accordingly, H1 was proved.

For Hypothesis 2, that technological innovation capability has a positive impact on organizational effectiveness, the size of the influence is 0.259, which confirms that technological innovation capability has a significantly (C.R. = 3.37 > 1.96, p = 0.000 < 0.001) positive (+) influence on organizational effectiveness. In other words, the higher the technology innovation capability, the higher is its positive contribution to organizational effectiveness. Accordingly, H2 was also proved.

In Hypothesis 1, the subfactors of business performance can be classified into financial and nonfinancial performance. Therefore, this study can verify H1.1 that technological innovation capability has a positive impact on financial performance and H1.2 that technological innovation capability has a positive impact on nonfinancial performance. The results in Table 5 indicate that technological innovation capability has a positive (+) influence on both financial and nonfinancial performance. Accordingly, both H1.1 and H1.2 were adopted. Thus, technological innovation capability can increase both financial and nonfinancial performance in SMEs.

The subfactors of organizational effectiveness in Hypothesis 2 can be classified into creativity and work performance. Thus, this study can test H2.1 that technological innovation capability has a positive impact on creativity and H2.2 that technological innovation capability has a positive impact on creativity. The results in Table 5 show that technological innovation capability has a positive (+) influence on both creativity and work performance. Accordingly, H2.1 and H2.2 were proved.

3.2.2. Hypotheses 3 and 4

Hypotheses 3 and 4 examine the mediating effects of organizational metacognition. To verify the mediating effects, the Sobel test, which calculates the z value using path coefficients and standard errors, was performed.

The Sobel z test of H3, that organizational metacognition has a mediating effect on the relationship between technological innovation capability and business performance, indicates that the mediation is statically significant at the 5% level (Z = 2.245 ≥ 1.96, p = 0.014 < 0.05). The Sobel z test of H4, that organizational metacognition has a mediating effect on the relationship between technological innovation capability and organizational effectiveness, indicates a statistically significant effect at the 1% level (Z = 3.959 ≥ 1.96, p = 0.0000 < 0.001).

To identify the full and partial mediating effect, 2000 samples were randomly extracted using the bootstrapping method. As Table 6 shows, organizational metacognition has a partial mediation effect in the relationship between technological innovation capabilities and business performance.

Table 6 suggests that organizational metacognition partially mediates the relationship between technological innovation capability and organizational effectiveness as well. In other words, organizational metacognition has a positive mediating role in the effect of technological innovation capability on organizational effectiveness.

4. Conclusions

4.1. Summary and Implications

To help SMEs achieve sustainable growth, this study examines the relationships between technological innovation capability, business performance, and organizational effectiveness. A firm’s competitive advantage could arise from its capability and efficiency in developing new products [50]. When competition is fierce, the capability to innovate and implement new technology is important [51]. Moreover, technological innovation capability is a kind of special asset or resource that includes technology, product, process, knowledge, experience, and organization [52]. Consequently, these characteristics of technological innovation capability could influence the organization overall. Therefore, SMEs could establish a long-term strategy for sustainable growth by building technological innovation capability.

In addition, this study investigates the mediating effect of metacognition at the organizational level. Metacognition plays an essential role in individual learning and problem-solving processes, and is an important variable that influences performance, the creativity of the task, and innovation [20,21,22,23,30,31,32,33]. Technology innovation inevitably involves many unexpected problems. Thus, metacognition in the problem-solving process can help SMEs’ technological innovation capability improve performance and enable sustainable growth. This study has several results. SMEs’ technological innovation capability improves financial and nonfinancial performance in line with arguments in previous studies [46,47]. SMEs could become more competitive and sustainable by reinforcing technological innovation capabilities. In addition, this study finds that SMEs’ technological innovation capability improves creativity and work performance, which are factors of organizational effectiveness. In other words, maintaining or enhancing SMEs’ technological innovation capability can accelerate their achievement of goals and improve management performance in a competitive environment. This study also finds that organizational metacognition partially mediates the relationship between technological innovation capability and business performance. It usually takes much time and effort for SMEs’ technological innovation capabilities to produce performance, because SMEs face unfavorable conditions, such as a lack of resources and unexpected problems. This result indicates that metacognition in the problem-solving process helps them adopt the appropriate strategy when implementing technological innovation and improves their performance. Lastly, organizational metacognition partially mediates the relationship between technological innovation capability and organizational effectiveness. Successful technology innovation should be accompanied by efforts by the organization and its members, such as technology innovation activities, organizational learning in the process, and problem-solving. These features of technological innovation capability could affect the organization overall. Therefore, metacognition is an important leading factor that influences organizational effectiveness. The findings in the present study support results from various studies demonstrating the positive effect of technological innovation capability on organizational and firm performance [22,46,53,54,55].

This study provides several implications for SMEs through its systematic approach and empirical verification of the impact of technological innovation capability on business performance and organizational effectiveness.

First, even during uncertainty and recession, SMEs should continue to make strategic efforts to reinforce technological innovation capability in terms of sustainable growth, as it has a positive effect on business performance. Therefore, efforts to improve technological innovation capabilities that create valuable, rare, difficult-to-imitate, and low-substitution technologies will be a good strategy for SMEs to improve their corporate performance. Thus, CEOs and managers should be actively interested in improving technological innovation capability.

Second, CEOs and managers of SMEs should use their technological innovation capability strategically to enhance organizational effectiveness in areas such as creativity and task performance. SMEs face intense competition. However, this study indicates that technological innovation capability has a positive effect on organizational effectiveness. If CEOs and managers of SMEs aim to maintain their technological innovation capability, their efforts will allow their firms to achieve organizational goals and improve management performance.

Third, this study verifies a new fact: organizational metacognition mediates the effects of technological innovation capabilities on business performance and organizational effectiveness. This finding directly or indirectly verifies the initial expectation and thinking that it is possible to expand metacognition to the organizational level, and that it influences SME performance [13,20,21,34,35]. This result implies that organizational metacognition helps solve various problems that may arise in the process of technology innovation.

Technology innovation capability is a very important resource to promote sustainable success by promoting innovation strategies [24]. Thus, SMEs also aim to become more competitive by reinforcing technological innovation capabilities to survive and grow in an era of uncertainty. However, it is more difficult for SMEs to link their innovation capabilities to performance due to limitations such as firm size and a lack of resources [4,5,6,7] compared with large firms [4,5,6,7]. Firm size as a description of its resource endowment generally has an important link to planning and monitoring capabilities [10]. Implementing technology innovation and strategy generally relies on planning, problem-solving, and innovation behavior, which firm size can affect. Metacognition plays a pivotal role in problem-solving and influences the performance and creativity of the task [14,15,16,17,18]. Considering these facts, if SMEs manage their metacognition properly and make use of it in the problem-solving process, they can successfully improve business performance and be more competitive. In other words, SMEs’ metacognition could help to identify a problem rationally and implement the appropriate strategy when implementing technological innovation. OECD studies show that SMEs that provide employees with opportunities to develop problem-solving skills and use their knowledge are more likely to succeed compared to others in developing new products or processes [19].

Finally, training and education for SME employees could allow them to adopt the perspective of metacognition. National and local governments are developing policies to support SMEs. They aim to help SMES adopt technology and managerial innovation. This study’s results show that organizational metacognition has a mediating effect on both business and organizational effectiveness. Therefore, education and training that strengthens metacognition will be an effective means to improve SME competitiveness.

4.2. Limitations and Future Work

Although this study contributes to the understanding of metacognition at the organizational level and its effect on a firm’s performance, this study has several limitations. This analysis is mainly based on SMEs, and the results therefore have limited generalizability to large and/or global corporations. Accordingly, future research should expand the subjects to include large companies and global corporations. In addition, a majority of the sample is SMEs in Korea, which limits the size of the company and the region in scope. It is necessary to conduct further research to complement the cross-sectional study limitations and perhaps conduct a comparative study of companies in Asian and Western countries. Moreover, it is better to use a stricter significance level than 5% when multiple tests are performed. This study followed the general criteria used in Korean social sciences. Thus, the results are difficult to expand and generalize to SMEs around the world. Future research will require more systematic and multivariate empirical studies and striker method. Last, technological innovation capability (R&D, Technology Accumulation Capability, and Technological Innovation System) does not fully reflect technology and capability of industry 4.0. Accordingly, future research will require more advanced factors of the technological innovation capability SMEs need.

Author Contributions

W.-J.Y. carried out the empirical studies and the literature review, and drafted the manuscript; H.H.C. participated in the design of the study and the statistical analysis; S.J.L. helped to draft and review the manuscript and communicate with the editor of the journal. All authors have read and approved the final manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Ik Seung, K. A study on the business ecosystem of German SMEs and its implications for Korean SMEs: Focusing on the hidden champion enterprises in Germany. Korean J. Econ. Manag. 2014, 32, 69–95. [Google Scholar]

- Hopenhayn, H.A. Entry, exit, and firm dynamics in long run equilibrium. Econ. Soc. 1992, 60, 1127–1150. [Google Scholar] [CrossRef]

- Normann, R. Reframing Business: When the Map Changes the Landscape; John Wiley & Sons: Hoboken, NJ, USA, 2001. [Google Scholar]

- Petruzzelli, A.M.; Ardito, L.; Savino, T. Maturity of knowledge inputs and innovation value: The moderating effect of firm age and size. J. Bus. Res. 2018, 86, 190–201. [Google Scholar] [CrossRef]

- McDougall, P.P.; Oviatt, B.M.; Shrader, R.C. A comparison of international and domestic new ventures. J. Int. Entrep. 2003, 1, 59–82. [Google Scholar] [CrossRef]

- Weerawardena, J.; Mort, G.S.; Liesch, P.W.; Knight, G. Conceptualizing accelerated internationalization in the born global firm: A dynamic capabilities perspective. J. World Bus. 2007, 42, 294–306. [Google Scholar] [CrossRef] [Green Version]

- Roni, M.; Jabar, J.; Muhamad, M.R.; Murad, M. Sustainable manufacturing drivers and firm performance: Moderating effect of firm size. Int. J. Adv. Appl. Sci. 2017, 4, 243–249. [Google Scholar] [CrossRef] [Green Version]

- Grant, R.M. The resource-based theory of competitive advantage: Implications for strategy formulation. Knowl. Strateg. 1999, 3–23. [Google Scholar] [CrossRef]

- Murad, A.M.; Ithnin, H.S.; Jabar, J. Conceptual study of readiness factors for AMT implementation in manufacturing SMEs. In Proceedings of the 2015 International Conference on Technology Management and Tehnopreneurship (IC-TMT 2015), Melaka, Malaysia, 5–6 August 2015. [Google Scholar]

- Temtime, Z.T. The moderating impacts of business planning and firm size on total quality management practices. TQM Mag. 2003, 15, 52–60. [Google Scholar] [CrossRef]

- Corsino, M.; Espa, G.; Micciolo, R. R&D, firm size and incremental product innovation. Econ. Innov. New Technol. 2011, 20, 423–443. [Google Scholar]

- Kim, D.; Lee, D. Impacts of metacognition on innovative behaviors: Focus on the mediating effects of entrepreneurship. J. Open Innov. Technol. Mark. Complex. 2018, 4, 18. [Google Scholar] [CrossRef]

- Jacobs, J.E.; Paris, S.G. Children’s metacognition about reading: Issues in definition, measurement, and instruction. Educ. Psychol. 1987, 22, 255–278. [Google Scholar] [CrossRef]

- Costa, A.L. Mediating the metacognitive. Educ. Leadersh. 1984, 42, 57–62. [Google Scholar]

- Brown, A. Metacognition, executive control, self-regulation, and other more mysterious mechanisms. In Metacognition, Motivation, and Understanding; Lawrence Erlbaum: Hillsdale, NJ, USA, 1987; pp. 65–116. [Google Scholar]

- Osman, M.E.; Hannafin, M.J. Metacognition research and theory: Analysis and implications for instructional design. Educ. Technol. Res. Dev. 1992, 40, 83–99. [Google Scholar] [CrossRef]

- Kaufman, J.C.; Beghetto, R.A. In praise of Clark Kent: Creative metacognition and the importance of teaching kids when (not) to be creative. Roeper Rev. 2013, 35, 155–165. [Google Scholar] [CrossRef]

- Park, I.S. Development and Implementation of Science Programs Enhancing Creative Problem Solving Skills Applying Meta-Cognition. Ph.D. Thesis, The Graduate School of Ewha Womans University, Seoul, Korea, 2010. [Google Scholar]

- OECD. Skills and Learning Strategies for Innovation in SMEs; OECD Working Party on SMEs and Entrepreneurship; OECD: Paris, France, 2015. [Google Scholar]

- Rhodes, J.; Lok, P.; Sadeghinejad, Z. The impact of metacognitive knowledge and experience on top management team diversity and small to medium enterprises performance. World Acad. Sci. Eng. Technol. Int. J. Soc. Behav. Educ. Econ. Bus. Ind. Eng. 2016, 10, 2842–2846. [Google Scholar]

- Rhodes, J.; Cheng, V.; Sadeghinejad, Z.; Lok, P. The relationship between management team (TMT) metacognition, entrepreneurial orientations and small and medium enterprises (SMEs) firm performance. Int. J. Manag. Pract. 2018, 11, 111–140. [Google Scholar] [CrossRef]

- Burgelman, R.A.; Maidique, M.A.; Wheelwright, S.C. Strategic Management of Technology and Innovation; Irwin: Chicago, IL, USA, 1996; Volume 2. [Google Scholar]

- Burgelman, R.A.; Christensen, C.M.; Wheelwright, S.C. Integrating technology and strategy: A general management perspective. In Strategic Management of Technology and Innovation; McGraw-Hill Education: New York, NY, USA, 2008. [Google Scholar]

- Kim, J.H.; Korea Institute of Science Technology Evaluation and Planning (KISTEO). The Era of the Fourth Industrial Revolution, Seeking Strategic Responses to Future Social Change; KISTEO: Seoul, Korea, 2016. [Google Scholar]

- Chung, M.; Hyundai Research Institute (HRI). The Korean Economy through the Fourth Industrial Revolution Leads to the Economic Powerhouse—Describes the Present and Future of the Korean Economy VIP; HRI: Seoul, Korea, 2017. [Google Scholar]

- Park, J.J.; Kim, T.T.; Son, Y.R. A study on the influence of technology innovation ability of SMEs on business performance. Korean Comp. Account. Rev. 2016, 14, 93–115. [Google Scholar]

- Nelson, R.R. An Evolutionary Theory of Economic Change; Harvard University Press: Cambridge, UK, 2009. [Google Scholar]

- Choi, S.B.; Ha, G.R. A study of critical factors for technological innovation of Korean manufacturing firms. J. Ind. Econ. Bus. 2011, 24, 1–24. [Google Scholar]

- Kozhevnikov, M. Cognitive styles in the context of modern psychology: Toward an integrated framework of cognitive style. Psychol. Bull. 2007, 133, 464. [Google Scholar] [CrossRef] [PubMed]

- Perfect, T.J.; Schwartz, B.L. Applied Metacognition; Cambridge University Press: Cambridge, UK, 2004. [Google Scholar]

- Blume, B.D.; Covin, J.G. Attributions to intuition in the venture founding process: Do entrepreneurs actually use intuition or just say that they do? J. Bus. Ventur. 2011, 26, 137–151. [Google Scholar] [CrossRef]

- Flavell, J.H. Metacognition and cognitive monitoring: A new area of cognitive–developmental inquiry. Am. Psychol. 1979, 34, 906. [Google Scholar] [CrossRef]

- Schmidt, A.M.; Ford, J.K. Learning within a learner control training environment: The interactive effects of goal orientation and metacognitive instruction on learning outcomes. Pers. Psychol. 2003, 56, 405–429. [Google Scholar] [CrossRef]

- Kwon, S.H.; Park, K.A. The effects of the collaborative metacognition support on the task performance of group and learning attitude in computer supported collaborative learning. J. Korean Assoc. Educ. Inf. Media 2004, 10, 193–219. [Google Scholar]

- Iiskala, T.; Vauras, M.; Lehtinen, E.; Salonen, P. Socially shared metacognition of dyads of pupils in collaborative mathematical problem-solving processes. Learn. Instr. 2011, 21, 379–393. [Google Scholar] [CrossRef]

- Venkatraman, N.; Ramanujam, V. Measurement of business performance in strategy research: A comparison of approaches. Acad. Manag. Rev. 1986, 11, 801–814. [Google Scholar] [CrossRef]

- Gupta, A.K.; Govindarajan, V. Business unit strategy, managerial characteristics, and business unit effectiveness at strategy implementation. Acad. Manag. J. 1984, 27, 25–41. [Google Scholar]

- Roure, J.B.; Keeley, R.H. Predictors of success in new technology based ventures. J. Bus. Ventur. 1990, 5, 201–220. [Google Scholar] [CrossRef]

- Birley, S.; Norburn, D. Owners and managers: The Venture 100 vs. the Fortune 500. J. Bus. Ventur. 1987, 2, 351–363. [Google Scholar] [CrossRef]

- Dess, G.G.; Robinson, R.B. Measuring organizational performance in the absence of objective measures: The case of the privately-held firm and conglomerate business unit. Strat. Manag. J. 1984, 5, 265–273. [Google Scholar] [CrossRef]

- Robbins, S.P. Organizational Behavior: International Edition; Prentice Hall: New Jersey, NJ, USA, 2003. [Google Scholar]

- Coulter, P.B. Organizational effectiveness in the public sector: The example of municipal fire protection. Adm. Sci. Q. 1979, 24, 65–81. [Google Scholar] [CrossRef]

- Miles, R.H. Resource Book in Macro Organizational Behavior; Scott Foresman: Glenview, IL, USA, 1980. [Google Scholar]

- Steers, R.M. Problems in the measurement of organizational effectiveness. Adm. Sci. Q. 1975, 20, 546–558. [Google Scholar] [CrossRef]

- Finance, Audit Tax Consulting Corporate. Industry 4.0 Challenges and Solutions for the Digital Transformation and Use of Exponential Technologies; Finance, Audit Tax Consulting Corporate: Zurich, Swiss, 2015. [Google Scholar]

- Jang, S.G.; Shin, Y.S.; Jung, H.H. Relationship between R&D investment, technology management capability, and firm performance. Korean Manag. Rev. 2009, 38, 105–132. [Google Scholar]

- Schoenecker, T.; Swanson, L. Indicators determining FTC. Assessing a firm’s technological capability. IEEE Potentials 2002, 21, 12–17. [Google Scholar] [CrossRef]

- Park, S.M.; Lee, B.H. The effects of the utilization of external resources on the performances of the technological innovation in Korean small and medium-sized enterprises. Korean Strateg. Manag. Soc. 2006, 7, 181–206. [Google Scholar]

- Dowling, M.J.; McGee, J.E. Business and technology strategies and new venture performance: A study of the telecommunications equipment industry. Manag. Sci. 1994, 40, 1663–1677. [Google Scholar] [CrossRef]

- Guan, J. Comparison study of industrial innovation between China and some European countries. Prod. Invent. Manag. J. 2002, 43, 30–46. [Google Scholar]

- Geissbauer, R.; Vedso, J.; Schrauf, S. Industry 4.0: Building the Digital Enterprise; PwC: London, UK, 2016. [Google Scholar]

- Guan, J.; Ma, N. Innovative capability and export performance of Chinese firms. Technovation 2003, 23, 737–747. [Google Scholar] [CrossRef]

- Charles, A. The Impact of technological innovation on organizational performance. Ind. Eng. Lett. 2014, 4, 3. [Google Scholar]

- Lau, K.W.; Yam, R.C.; Tang, E.P. The impact of technological innovation capabilities on innovation performance: An empirical study in Hong Kong. J. Sci. Technol. Policy China 2010, 1, 163–186. [Google Scholar] [CrossRef]

- Reichert, F.M.; Zawislak, P.A. Technological capability and firm performance. J. Technol. Manag. Innov. 2014, 9, 20–35. [Google Scholar] [CrossRef]

- Bowen, H.K.; Clark, K.B.; Holloway, C.A.; Wheelwright, S.C. Development projects: The engine of renewal. Harv. Bus. Rev. 1994, 72, 110–120. [Google Scholar]

- Podsakoff, P.M.; Organ, D.W. Self-reports in organizational research: Problems and prospects. J. Manag. 1986, 12, 531–544. [Google Scholar] [CrossRef]

Figure 1.

Research model.

Figure 2.

Result of structural equation model analysis.

{kind=link}

{kind=link}

Table 1.

Sample characteristics.

| Variable | Number | Percentage |

|---|---|---|

| Gender | ||

| Male | 314 | 75.7 |

| Female | 101 | 24.3 |

| Age | ||

| 20~29 years | 60 | 14.5 |

| 30~39 years | 191 | 46.0 |

| 40~49 years | 125 | 30.1 |

| 50 years and over | 39 | 9.4 |

| Position | ||

| Staff | 112 | 26.9 |

| Assistant manager | 109 | 26.3 |

| Manager | 121 | 29.2 |

| General manager | 33 | 7.9 |

| Executives | 24 | 5.8 |

| Chief executive officer | 16 | 3.9 |

| Industry | ||

| Electronics | 58 | 14.0 |

| Machinery & Automobile | 106 | 25.5 |

| Construction | 77 | 18.6 |

| Petrochemicals | 23 | 5.5 |

| Textile | 6 | 1.4 |

| Food, beverage, & medicine | 5 | 1.2 |

| Cosmetics | 6 | 1.4 |

| Lumber | 16 | 3.9 |

| Agricultural, fisheries, & mining | 4 | 0.9 |

| Other manufacturing | 58 | 14.0 |

| Service | 56 | 13.5 |

| Number of Employees | ||

| 1~49 | 169 | 40.8 |

| 50~99 | 79 | 19.0 |

| 100~299 | 79 | 19.0 |

| 300~499 | 88 | 21.2 |

Table 2.

Kaiser–Meyer–Olkin (KMO) and Bartlett’s test.

| Kaiser–Meyer–Olkin Measure of Sampling Adequacy | 0.949 | |

| Bartlett’s test of sphericity | approx. chi-square | 9114.971 |

| df | 16,546.590 | |

| p | 0.000 | |

Table 3.

Exploratory factor analysis and reliability analysis.

| Factor | Variables | Descriptive Statistics | Communalities | Rotated Component Matrix | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | SD | Initial | Extraction | 1 | 2 | 3 | 4 | 5 | 6 | ||

| Technological Innovation Capability | R&D Capability 1 | 3.22 | 1.178 | 1.000 | 0.708 | 0.770 | 0.105 | 0.074 | 0.085 | 0.065 | 0.140 |

| R&D 2 | 3.26 | 1.082 | 1.000 | 0.744 | 0.794 | 0.158 | 0.123 | 0.138 | 0.108 | 0.123 | |

| R&D 3 | 3.30 | 1.098 | 1.000 | 0.686 | 0.756 | 0.170 | 0.160 | 0.150 | 0.117 | 0.151 | |

| R&D 4 | 3.04 | 0.990 | 1.000 | 0.643 | 0.750 | 0.086 | 0.164 | 0.141 | 0.037 | 0.090 | |

| R&D 5 | 3.07 | 0.979 | 1.000 | 0.633 | 0.757 | 0.172 | 0.127 | 0.073 | 0.092 | 0.007 | |

| Technology Accumulation Capability 1 | 3.22 | 1.012 | 1.000 | 0.776 | 0.774 | 0.175 | 0.050 | 0.110 | 0.093 | 0.138 | |

| TAC 2 | 3.00 | 0.984 | 1.000 | 0.778 | 0.717 | 0.212 | 0.202 | 0.095 | −0.005 | 0.132 | |

| TAC 3 | 3.12 | 0.953 | 1.000 | 0.769 | 0.745 | 0.145 | 0.060 | 0.105 | 0.069 | 0.184 | |

| TAC 4 | 3.25 | 0.909 | 1.000 | 0.726 | 0.749 | 0.212 | 0.135 | 0.034 | 0.166 | 0.139 | |

| TAC 5 | 3.10 | 0.910 | 1.000 | 0.752 | 0.776 | 0.253 | 0.127 | 0.066 | 0.148 | 0.098 | |

| TAC 6 | 3.14 | 0.967 | 1.000 | 0.742 | 0.765 | 0.196 | 0.170 | 0.086 | 0.128 | 0.160 | |

| TAC 7 | 3.18 | 1.050 | 1.000 | 0.699 | 0.789 | 0.169 | 0.023 | 0.082 | 0.162 | 0.102 | |

| Technological Innovation System 1 | 3.06 | 1.000 | 1.000 | 0.711 | 0.772 | 0.225 | 0.188 | 0.085 | 0.123 | 0.085 | |

| TIS 2 | 3.05 | 0.925 | 1.000 | 0.630 | 0.668 | 0.255 | 0.120 | 0.082 | 0.077 | 0.134 | |

| TIS 3 | 3.00 | 1.010 | 1.000 | 0.724 | 0.740 | 0.185 | 0.197 | 0.066 | 0.067 | 0.143 | |

| TIS 4 | 3.07 | 0.980 | 1.000 | 0.699 | 0.741 | 0.191 | 0.232 | 0.107 | 0.126 | 0.142 | |

| TIS 5 | 3.20 | 0.949 | 1.000 | 0.688 | 0.761 | 0.216 | 0.206 | −0.003 | 0.122 | 0.051 | |

| TIS 6 | 2.91 | 0.959 | 1.000 | 0.708 | 0.772 | 0.197 | 0.232 | 0.122 | 0.034 | 0.011 | |

| Organizational Metacognition | OM 1 | 3.36 | 0.770 | 1.000 | 0.649 | 0.221 | 0.729 | 0.089 | 0.047 | 0.148 | 0.165 |

| OM 2 | 3.44 | 0.774 | 1.000 | 0.721 | 0.258 | 0.752 | 0.159 | 0.065 | 0.134 | 0.194 | |

| OM 3 | 3.48 | 0.770 | 1.000 | 0.672 | 0.263 | 0.733 | 0.083 | 0.060 | 0.183 | 0.149 | |

| OM 4 | 3.33 | 0.790 | 1.000 | 0.670 | 0.167 | 0.753 | 0.112 | 0.092 | 0.125 | 0.047 | |

| OM 5 | 3.29 | 0.747 | 1.000 | 0.713 | 0.228 | 0.769 | 0.079 | 0.157 | 0.108 | 0.024 | |

| OM 6 | 3.29 | 0.766 | 1.000 | 0.680 | 0.228 | 0.762 | 0.148 | 0.096 | 0.081 | −0.023 | |

| OM 7 | 3.27 | 0.786 | 1.000 | 0.652 | 0.287 | 0.707 | 0.161 | 0.171 | 0.066 | 0.056 | |

| OM 8 | 3.23 | 0.810 | 1.000 | 0.525 | 0.307 | 0.605 | 0.090 | 0.142 | 0.047 | 0.007 | |

| Organizational Effectiveness | Creativity1 | 3.23 | 0.795 | 1.000 | 0.719 | 0.112 | 0.193 | 0.008 | 0.792 | 0.181 | 0.084 |

| Creativity2 | 3.25 | 0.790 | 1.000 | 0.740 | 0.115 | 0.119 | 0.009 | 0.796 | 0.257 | 0.103 | |

| Creativity3 | 3.03 | 0.823 | 1.000 | 0.787 | 0.089 | 0.142 | −0.028 | 0.866 | 0.078 | 0.034 | |

| Creativity4 | 3.14 | 0.779 | 1.000 | 0.778 | 0.122 | 0.048 | −0.004 | 0.851 | 0.182 | −0.013 | |

| Creativity5 | 3.02 | 0.747 | 1.000 | 0.825 | 0.119 | 0.102 | −0.004 | 0.878 | 0.159 | −0.039 | |

| Creativity6 | 3.15 | 0.751 | 1.000 | 0.725 | 0.187 | 0.051 | 0.062 | 0.781 | 0.252 | −0.094 | |

| Work performance1 | 3.59 | 0.650 | 1.000 | 0.680 | 0.226 | 0.104 | 0.053 | 0.288 | 0.722 | 0.063 | |

| WP 2 | 3.59 | 0.692 | 1.000 | 0.729 | 0.141 | 0.105 | 0.099 | 0.275 | 0.777 | 0.075 | |

| WP 3 | 3.64 | 0.684 | 1.000 | 0.779 | 0.146 | 0.180 | 0.085 | 0.299 | 0.789 | 0.069 | |

| WP 4 | 3.56 | 0.692 | 1.000 | 0.708 | 0.104 | 0.172 | 0.097 | 0.230 | 0.776 | 0.012 | |

| WP 5 | 3.73 | 0.669 | 1.000 | 0.720 | 0.180 | 0.175 | 0.081 | 0.113 | 0.789 | 0.098 | |

| Business Performance | Financial Performance 1 | 3.37 | 0.959 | 1.000 | 0.690 | 0.146 | 0.078 | 0.780 | 0.039 | 0.028 | 0.223 |

| Financial Performance 2 | 3.23 | 0.899 | 1.000 | 0.606 | 0.213 | 0.124 | 0.671 | 0.050 | 0.040 | 0.302 | |

| Financial Performance 3 | 3.12 | 0.976 | 1.000 | 0.771 | 0.186 | 0.124 | 0.827 | 0.006 | 0.107 | 0.158 | |

| Financial Performance 4 | 2.86 | 0.903 | 1.000 | 0.763 | 0.160 | 0.113 | 0.845 | −0.016 | 0.078 | −0.018 | |

| Financial Performance 5 | 3.03 | 0.911 | 1.000 | 0.739 | 0.256 | 0.146 | 0.798 | −0.034 | 0.044 | 0.105 | |

| Financial Performance 6 | 3.27 | 0.980 | 1.000 | 0.614 | 0.246 | 0.171 | 0.682 | 0.001 | 0.123 | 0.189 | |

| Non-Financial Performance 1 | 3.41 | 0.855 | 1.000 | 0.729 | 0.333 | 0.159 | 0.341 | −0.003 | 0.088 | 0.676 | |

| Non-Financial Performance 2 | 3.43 | 0.871 | 1.000 | 0.780 | 0.312 | 0.168 | 0.464 | 0.020 | 0.087 | 0.647 | |

| Non-Financial Performance 3 | 3.44 | 0.877 | 1.000 | 0.694 | 0.265 | 0.155 | 0.280 | 0.026 | 0.121 | 0.705 | |

| Non-Financial Performance 4 | 3.39 | 0.821 | 1.000 | 0.802 | 0.333 | 0.121 | 0.389 | 0.019 | 0.097 | 0.717 | |

| Eigenvalue | 11.649 | 5.277 | 4.714 | 4.708 | 3.591 | 2.515 | |||||

| Cumulative variance | 24.786 | 36.014 | 46.045 | 56.062 | 63.703 | 69.055 | |||||

| Cronbach’s α | 0.969 | 0.916 | 0.932 | 0.899 | 0.906 | 0.889 | |||||

Table 4.

Discriminant validity.

| Correlation (a ↔ b) | r | r 2 | AVE (a) | AVE (b) |

|---|---|---|---|---|

| Organizational Metacognition ↔ Technological Innovation Capability | 0.628 | 0.394 | 0.626 | 0.913 |

| Technological Innovation Capability ↔ Business Performance | 0.652 | 0.425 | 0.913 | 0.831 |

| Organizational Metacognition ↔ Business Performance | 0.508 | 0.258 | 0.626 | 0.831 |

| Business Performance ↔ Organizational Effectiveness | 0.351 | 0.123 | 0.831 | 0.808 |

| Organizational Metacognition ↔ Organizational Effectiveness | 0.514 | 0.264 | 0.626 | 0.808 |

| Technological Innovation Capability ↔ Organizational Effectiveness | 0.479 | 0.229 | 0.913 | 0.808 |

Table 5.

Hypothesis results.

| Category | Estimate | S.E. | C.R. | p | Result | |||

|---|---|---|---|---|---|---|---|---|

| Technological Innovation Capability | → | Business Performance | 0.557 | 0.046 | 7.338 | *** | H1 | adopted |

| Technological Innovation Capability | → | Organizational Effectiveness | 0.259 | 0.031 | 3.37 | *** | H2 | adopted |

| Technological Innovation Capability | → | Financial Performance | 0.412 | 0.053 | 6.251 | *** | H1.1 | adopted |

| → | Non-Financial Performance | 0.553 | 0.055 | 8.882 | *** | H1.2 | adopted | |

| Technological Innovation Capability | → | Creativity | 0.158 | 0.044 | 2.373 | 0.018 ** | H2.1 | adopted |

| → | Work Performance | 0.223 | 0.036 | 3.449 | *** | H2.2 | adopted | |

* Significant at the 5% level, ** significant at the 1% level, *** significant at the 0.1% level.

Table 6.

Mediating effect of organizational metacognition.

| Category | Total Effect | Direct Effect | Indirect Effect | Result | ||

|---|---|---|---|---|---|---|

| Technology Innovation Capability | → | Organizational Metacognition | 0.616 *** | 0.616 *** | - | |

| → | Business Performance | 0.654 ** (p = 0.001) | 0.557 ** (p = 0.001) | 0.097 * (p = 0.021) | Partial Mediation | |

| → | Organizational Effectiveness | 0.477 ** (p = 0.002) | 0.259 ** (p = 0.003) | 0.218 ** (p = 0.002) | Partial Mediation | |

* Significant at the 5% level, ** significant at the 1% level, *** significant at the 0.1% level.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Yoo, W.-J.; Choo, H.H.; Lee, S.J. A Study on the Sustainable Growth of SMEs: The Mediating Role of Organizational Metacognition. Sustainability 2018, 10, 2829. https://doi.org/10.3390/su10082829

AMA Style

Yoo W-J, Choo HH, Lee SJ. A Study on the Sustainable Growth of SMEs: The Mediating Role of Organizational Metacognition. Sustainability. 2018; 10(8):2829. https://doi.org/10.3390/su10082829

Chicago/Turabian StyleYoo, Wang-Jin, Hyun Ho Choo, and Sang Jin Lee. 2018. "A Study on the Sustainable Growth of SMEs: The Mediating Role of Organizational Metacognition" Sustainability 10, no. 8: 2829. https://doi.org/10.3390/su10082829

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.