Environmental Risk Management Strategies and the Moderating Role of Corporate Social Responsibility in Project Financing Decisions

Abstract

:1. Introduction

Study Objectives

- To examine the relationship between different risks assessment aspects in decision making related to project financing.

- Discussing several approaches towards environmental management in mega projects financing. How are financial institutions undertaking environmental management policies in the decision-making process?

- To study environmental risk management strategies and their impacts on financial decision-making.

2. Theoretical Background

2.1. Stakeholder Theory

2.2. Triple Bottom Line Theory

2.3. Environmental Risk Assessment (ERA)

2.4. Corporate Social Responsibility (CSR) and Project Financing

2.5. Stakeholder Assessment

2.6. Credit Risk Assessment

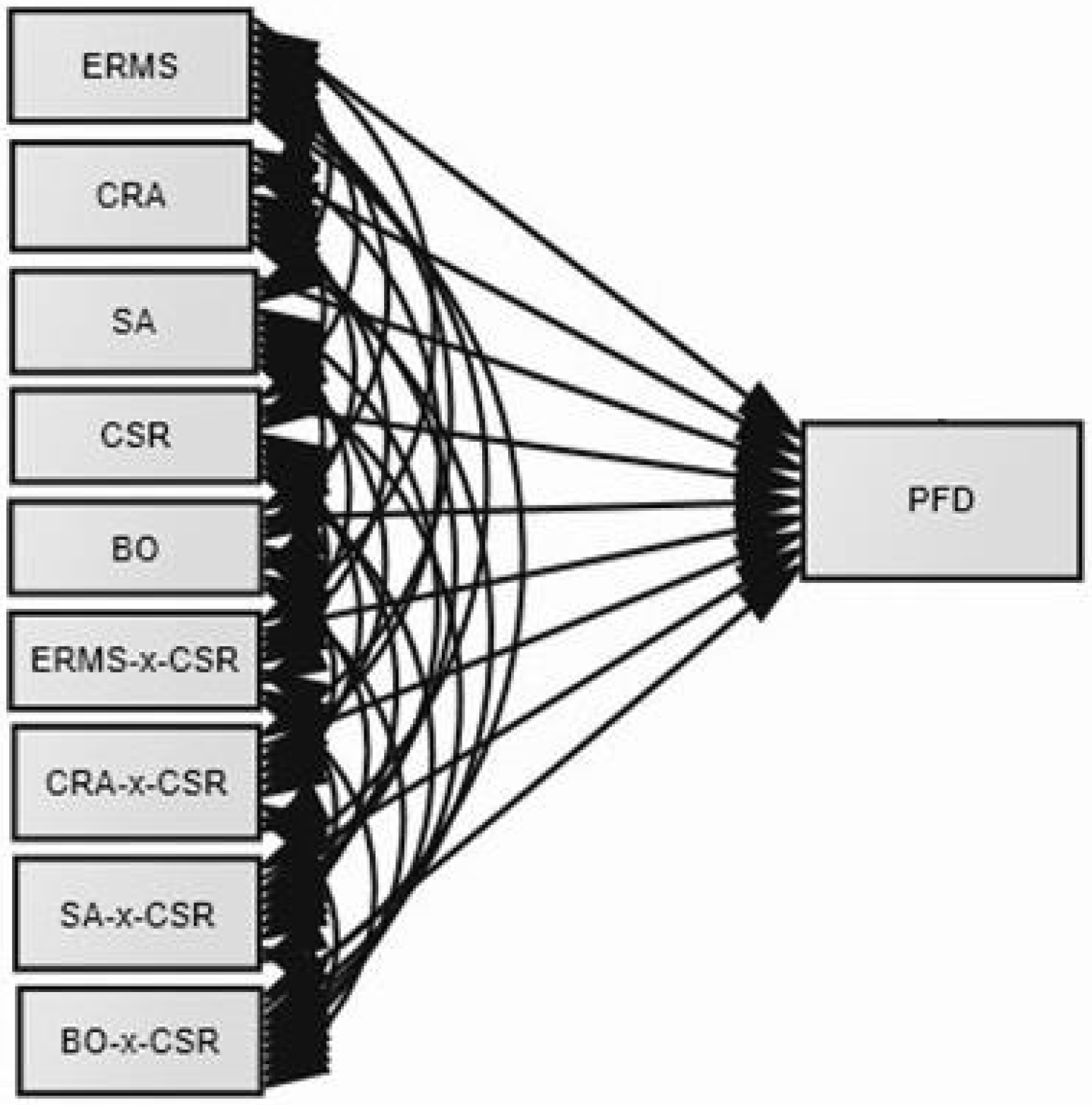

3. Conceptual Framework and Hypotheses Development

3.1. Hypothesis Development

3.1.1. Environmental Assessment

3.1.2. Credit Risk Assessment

3.1.3. Stakeholder Assessment

3.1.4. CSR Assessment

4. Research Methodology

5. Results and Discussion

5.1. Description

5.2. Preliminary Analysis: Reliability Test

5.3. Exploratory Factor Analysis

5.4. Hypothesis Testing

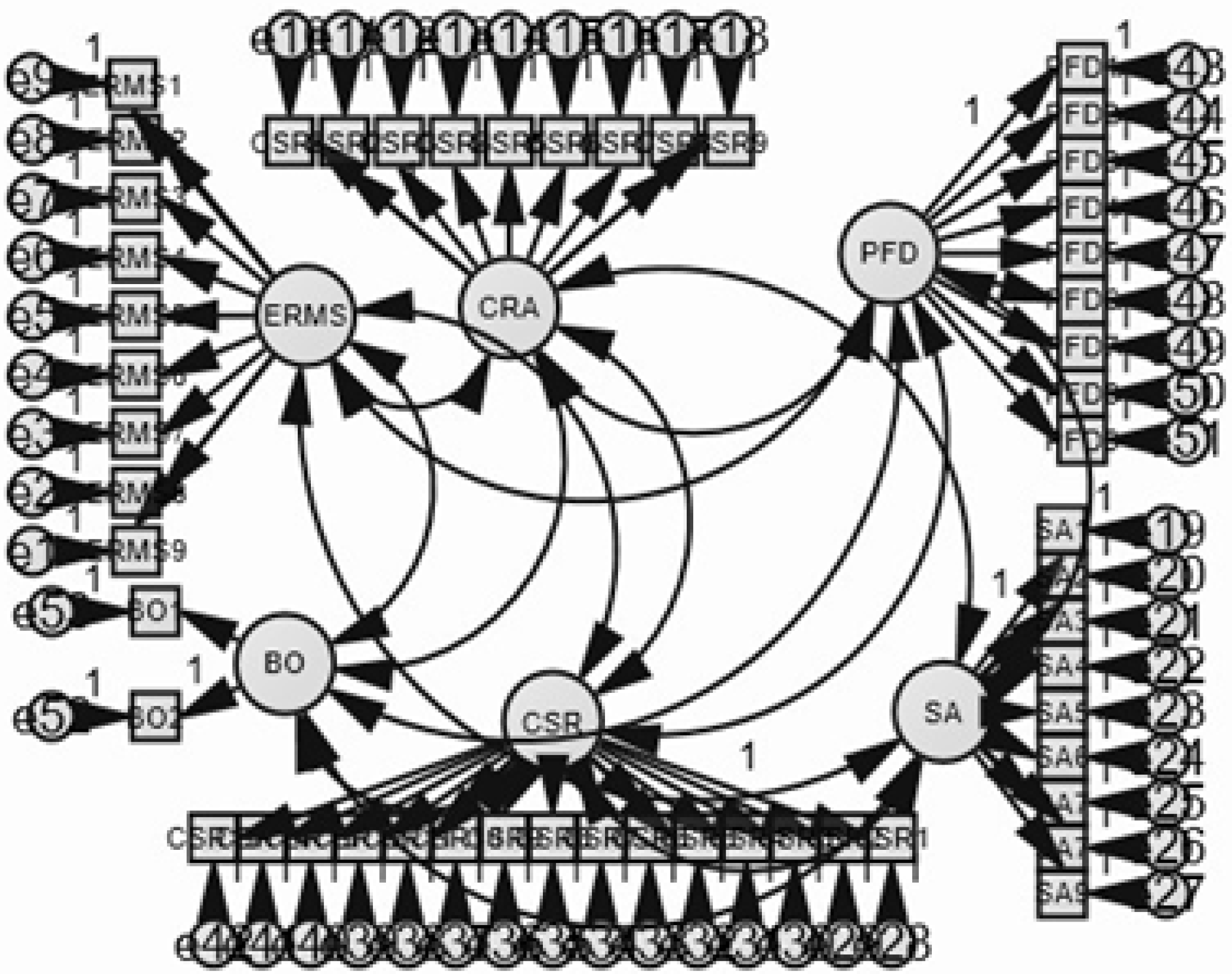

5.5. Structural Equation Model (SEM)

5.6. Structural Equation Model (Path Analysis)

5.7. Moderation

6. Conclusions

Implications for Policy Markers

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Sarokin, D.; Schulkin, J. Environmental Concerns and the Business of Banking. J. Commer. Bank Lend. 1991, 74, 6–19. [Google Scholar]

- Orlitzky, M.; Siegel, D.S.; Waldman, D.A. Strategic Corporate Social Responsibility and Environmental Sustainability. Bus. Soc. 2011, 50, 6–27. [Google Scholar] [CrossRef]

- Henriques, I.; Sadorsky, P. The relationship between environmental commitment and managerial perceptions of stakeholder importance. Acad. Manag. J. 1999, 42, 87–99. [Google Scholar]

- Clemens, B.; Bamford, C.E.; Douglas, T.J. Choosing strategic responses to address emerging environmental regulations: Size, perceived influence and uncertainty. Bus. Strategy Environ. 2008, 17, 493–511. [Google Scholar] [CrossRef]

- Annandale, D.; Bailey, J.; Ouano, E.; Evans, W.; King, P. The potential role of strategic environmental assessment in the activities of multi-lateral development banks. Environ. Impact Assess. Rev. 2001, 21, 407–429. [Google Scholar] [CrossRef]

- Coulson, A.B. How should banks govern the environment? Challenging the construction of action versus veto. Bus. Strategy Environ. 2009, 18, 149–161. [Google Scholar] [CrossRef]

- Ali Basah, M.Y. Corporate Social Responsibility and Natural Environmental Risk Management in the Context of the Banking Sector of Malaysia. Ph.D. Thesis, Cardiff University, Cardiff, UK, 2012; pp. 1–336. [Google Scholar]

- Scholtens, B. Finance as a driver of corporate social responsibility. J. Bus. Ethics 2006, 68, 19–33. [Google Scholar] [CrossRef]

- Hategan, C.-D.; Sirghi, N.; Curea-Pitorac, R.-I.; Hategan, V.-P. Doing Well or Doing Good: The Relationship between Corporate Social Responsibility and Profit in Romanian Companies. Sustainability 2018, 10, 1041. [Google Scholar] [CrossRef]

- Badulescu, A.; Badulescu, D.; Saveanu, T.; Hatos, R. The Relationship between Firm Size and Age, and Its Social Responsibility Actions—Focus on a Developing Country (Romania). Sustainability 2018, 10, 805. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals With Folks: The Triple Bottom Line of 21st Century Business; Wiley: Hoboken, NJ, USA, 1997. [Google Scholar]

- Sarfraz, M.; Qun, W.; Abdullah, M.I.; Alvi, A.T. Employees’ Perception of Corporate Social Responsibility Impact on Employee Outcomes: Mediating Role of Organizational Justice for Small and Medium Enterprises (SMEs). Sustainability 2018, 10, 2429. [Google Scholar] [CrossRef]

- Buysse, K.; Verbeke, A. Proactive environmental strategies: A stakeholder management perspective. Strateg. Manag. J. 2003, 24, 453–470. [Google Scholar] [CrossRef]

- Pijourlet, G. Corporate Social Responsibility and Financing Decisions. In Proceedings of the European Financial Management Association 2013 Annual Meetings, Reading, UK, 26 June 2013. [Google Scholar]

- Van de Velde, E.; Vermeir, W.; Corten, F. Corporate social responsibility and financial performance. Corp. Gov. Int. J. Bus. Soc. 2005, 5, 129–138. [Google Scholar] [CrossRef]

- Sen, S.; Bhattacharya, C.B.; Korschun, D. The role of corporate social responsibility in strengthening multiple stakeholder relationships: A field experiment. J. Acad. Mark. Sci. 2006, 34, 158–166. [Google Scholar] [CrossRef]

- Mishra, S.; Suar, D. Does corporate social responsibility influence firm performance of Indian companies? J. Bus. Ethics 2010, 95, 571–601. [Google Scholar] [CrossRef]

- Clarkson, M.E. A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Starik, M. Should trees have managerial standing? Toward stakeholder status for non-human nature. J. Bus. Ethics 1995, 14, 207–217. [Google Scholar] [CrossRef]

- Dechant, K.; Altman, B. Environmental leadership: From compliance to competitive advantage. Acad. Manag. Perspect. 1994, 8, 7–20. [Google Scholar] [CrossRef]

- Lavastre, O.; Spalanzani, A. Comment Gérer les Risques Liés à la Chaîne Logistique? Une Réponse par les Pratiques de SCRM. 2010. Available online: https://halshs.archives-ouvertes.fr/halshs-00534733/document (accessed on 22 July 2018).

- Mazouni, M.H. Pour une Meilleure Approche du Management des Risques: De la Modélisation Ontologique du Processus Accidentel au Système Interactif d’Aide à la Décision. Ph.D. Thesis, Institut National Polytechnique de Lorraine-INPL, Nancy, France, 2008. [Google Scholar]

- Scholtens, B.; Dam, L. Banking on the Equator. Are banks that adopted the Equator Principles different from non-adopters? World Dev. 2007, 35, 1307–1328. [Google Scholar] [CrossRef]

- Amalric, F. The Equator Principles: A Step towards Sustainability; Center for Corporate Responsibility and Sustainability: Zurich, Switzerland, 2005. [Google Scholar]

- Cowton, C.J.; Thompson, P. Do codes make a difference? The case of bank lending and the environment. J. Bus. Ethics 2000, 24, 165–178. [Google Scholar] [CrossRef]

- Watchman, P.Q.; Delfino, A.; Addison, J. EP 2: The revised Equator Principles: Why hard-nosed bankers are embracing soft law principles. Law Financ. Mark. Rev. 2007, 1, 85–113. [Google Scholar] [CrossRef]

- Sprengel, D.; Busch, T. Stakeholder Engagement and Environmental Strategy—The Case of Climate Change. Bus. Strategy Environ. 2010, 20, 351–364. [Google Scholar] [CrossRef]

- Billiot, M.J.; Daughtrey, Z.W. Evaluating environmental liability through risk premiums charged on loans to agribusiness borrowers. Agribusiness 2001, 17, 273–297. [Google Scholar] [CrossRef]

- Thompson, P.; Cowton, C.J. Bringing the environment into bank lending: Implications for environmental reporting. Br. Account. Rev. 2004, 36, 197–218. [Google Scholar] [CrossRef]

- Carroll, A.B. A Three-Dimensional Conceptual Model of Corporate Performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Moon, J. The contribution of corporate social responsibility to sustainable development. Sustain. Dev. 2007, 15, 296–306. [Google Scholar] [CrossRef]

- Carroll, A.B. The Pyramid of Corporate Social Responsibiiity: Toward the Moral Management of Organizational Stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Gallardo-Vázquez, D.; Sanchez-Hernandez, M.I. Measuring Corporate Social Responsibility for competitive success at a regional level. J. Clean. Prod. 2014, 72, 14–22. [Google Scholar] [CrossRef]

- Lee, M.; Kim, H. Exploring the Organizational Culture’s Moderating Role of Effects of Corporate Social Responsibility (CSR) on Firm Performance: Focused on Corporate Contributions in Korea. Sustainability 2017, 9, 1883. [Google Scholar] [CrossRef]

- Abdullah, M.I.; Ashraf, S.; Sarfraz, M. The organizational identification perspective of CSR on creative performance: The moderating role of creative self-efficacy. Sustainability 2017, 9, 2125. [Google Scholar] [CrossRef]

- Sarfraz, M. Do Consumers Consider CSR, A Case of Cellular Companies in Pakistan? Glob. J. Manag. Bus. Res. 2014, 14. Available online: https://journalofbusiness.org/index.php/GJMBR/article/view/1318 (accessed on 22 July 2018).

- Kemper, J.; Schilke, O.; Reimann, M.; Wang, X.; Brettel, M. Competition-motivated corporate social responsibility. J. Bus. Res. 2013, 66, 1954–1963. [Google Scholar] [CrossRef]

- Fijałkowska, J.; Zyznarska-Dworczak, B.; Garsztka, P. Corporate Social-Environmental Performance versus Financial Performance of Banks in Central and Eastern European Countries. Sustainability 2018, 10, 772. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 1984; Volume 1. [Google Scholar]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Braun, B.; Starmanns, M. A stakeholder model in economic geography: Perception and management of environmental stakeholders in German manufacturing companies. BELGEO 2009, 65–81. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Shrivastava, P. The role of corporations in achieving ecological sustainability. Acad. Manag. Rev. 1995, 20, 936–960. [Google Scholar] [CrossRef]

- Berman, S.L.; Wicks, A.C.; Kotha, S.; Jones, T.M. Does stakeholder orientation matter? The relationship between stakeholder management models and firm financial performance. Acad. Manag. J. 1999, 42, 488–506. [Google Scholar]

- Banerjee, S.B.; Iyer, E.S.; Kashyap, R.K. Corporate Environmentalism: Antecedents and Influence of Industry Type. J. Mark. 2003, 67, 106–122. [Google Scholar] [CrossRef]

- Bessis, J. Risk Management in Banking; Section 6; John Wiley & Sons: Hoboken, NJ, USA, 2011. [Google Scholar]

- Duffie, D.; Singleton, K.J. Credit Risk: Pricing, Measurement, and Management; Princeton University Press: Princeton, NJ, USA, 2012. [Google Scholar]

- Bassen, A.; Meyer, K.; Schlange, J. The Influence of Corporate Responsibility on the Cost of Capital an Empirical Analysis; Mimeo: New York, NY, USA; University of Hamburg: Hamburg, Germany, 2006; pp. 4–40. [Google Scholar]

- Van Greuning, H.; Brajovic Bratanovic, S. Analyzing Banking Risk: A Framework for Assessing Corporate Governance and Finacial Risk Management; The World Bank: Washington, DC, USA, 2009. [Google Scholar]

- Saunders, A.; Allen, L. Credit risk measurement. In New Approaches to VaR and Other Paradigms; John Wiley & Sons: Hoboken, NJ, USA, 2002. [Google Scholar]

- Chepkwony, P.K.; Kemboi, A.; Muange, R.M. Moderating effect of csr orientation on the relationship between internal csr practices and employee job satisfaction. Glob. J. Hum. Resour. Manag. 2015, 3, 1–16. [Google Scholar]

- Thomas, A.B. Research Skills for Management Studies; Routledge: Abingdon, UK, 2004. [Google Scholar]

- Dowell, G.; Hart, S.; Yeung, B. Do Corporate Global Environmental Standards Create or Destroy Market Value? Manag. Sci. 2000, 46, 1059–1074. [Google Scholar] [CrossRef]

- Fang, S.-R.; Huang, C.-Y.; Huang, S.W.-L. Corporate social responsibility strategies, dynamic capability and organizational performance: Cases of top Taiwan-selected benchmark enterprises. Afr. J. Bus. Manag. 2010, 4, 120–132. [Google Scholar]

- Bryman, A. Social Research Methods Bryman; Oxford University Press: Oxford, UK, 2013. [Google Scholar]

- Creswell, J.W. Research Design Qualitative Quantitative and Mixed Methods Approaches; Sage Publications: Thousand Oaks, CA, USA, 2003; pp. 3–26. [Google Scholar]

- Nunnally, J.C. Psychometric theory 25 years ago and now. Educ. Res. 1978, 4, 7–21. [Google Scholar]

- Neuman, L.W. Basics of Social Research Pnie; Pearson Education Limited: Harlow, UK, 2014. [Google Scholar]

- Dusuki, A.W. Corporate Social Responsibility of Islamic Banks in Malaysia: A Synthesis of Islamic and Stakeholders’ Perspectives. Ph.D. Thesis, Loughborough University, Leicestershire, UK, 2005. [Google Scholar]

- Pallant, J. SPSS Survival Manual: A Step by Step Guide to Data Analysis Using SPSS; Open University Press: Milton Keynes, UK, 2010. [Google Scholar]

- Agle, B.R.; Mitchell, R.K.; Sonnenfeld, J.A. Who matters to CEOs? An investigation of stakeholder attributes and salience, corporate performance, and CEO values. Acad. Manag. J. 1999, 42, 507–525. [Google Scholar]

- Maignan, I.; Ferrell, O.C. Measuring corporate citizenship in two countries: The case of the United States and France. J. Bus. Ethics 2000, 23, 283–297. [Google Scholar] [CrossRef]

- Driscoll, C.; Starik, M. The primordial stakeholder: Advancing the conceptual consideration of stakeholder status for the natural environment. J. Bus. Ethics 2004, 49, 55–73. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate Social Responsibility: Strategic Implications. J. Manag. Stud. 2005, 43, 1–18. [Google Scholar] [CrossRef]

- Mittal, R.K.; Sinha, N.; Singh, A. An analysis of linkage between economic value added and corporate social responsibility. Manag. Decis. 2008, 46, 1437–1443. [Google Scholar] [CrossRef]

- Abdullah, N.I. Maqasid al-Shari’ah. Maslahah, and Corporate Social Responsibility. Am. J. Islam. Soc. Sci. 2007, 24, 25–44. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Variable | Category | Frequency | Percent |

|---|---|---|---|

| Gender | Male | 320 | 65.17 |

| Female | 171 | 34.82 | |

| Respondents Age | 21–30 | 129 | 26.27 |

| 31–40 | 151 | 30.75 | |

| 41–50 | 110 | 22.45 | |

| 51 years or above | 101 | 20.57 | |

| Respondents‘ Work Profiles | Executives | 70 | 14.256 |

| Chief Executive Officer (CEO) | 4 | 0.814 | |

| Managers | 245 | 49.89 | |

| Board of Directors | 52 | 10.59 | |

| Senior Manager | 75 | 15.27 | |

| Others | 45 | 9.164 |

| N-Statistics | Maximum Statistics | Mean Values | Skewness | |

|---|---|---|---|---|

| Environment Risk Management Strategies | 491 | 5 | 3.19 | −8.41 |

| Credit Risk Assessment | 491 | 5 | 3.81 | −8.17 |

| Stakeholder Risk Assessment | 491 | 5 | 3.56 | −9.05 |

| Corporate Social Responsibility | 491 | 5 | 3.95 | −8.78 |

| Project Financing Decision | 491 | 5 | 4.14 | −7.12 |

| Valid N | 491 | 5 |

| Variables | Number of Items | Cronbach’s Alpha |

|---|---|---|

| Environmental risk management | 9 | 0.881 |

| Credit Risk assessment | 9 | 0.896 |

| Stakeholder risk assessment | 9 | 0.850 |

| Project finance decision | 9 | 0.908 |

| CSR assessment | 15 | 0.781 |

| Kaiser–Meyer–Olkin Measure of Sampling Adequacy | 0.869 | |

| Bartlett’s Test of Sphericity | Approx. Chi-Square | 1987.676 |

| df | 10 | |

| Sig. | 0.000 | |

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

|---|---|---|---|---|

| 1 | 0.750 a | 0.563 | 0.562 | 0.593 |

| Model | Sum of Squares | Mean Square | F | Sig. | |

|---|---|---|---|---|---|

| 1 | Regression | 221.780 | 221.780271 | 630.05 | 0.000 |

| Residual | 172.12 | 0.352001 | |||

| Total | 393.909 | ||||

| Model | R | R Square | Adjusted R Square | Std. The Error of the Estimate |

|---|---|---|---|---|

| 1 | 00.793 a | 0.629 | 0.628 | 0.546 |

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|---|

| 1 | Regression | 247.834288 | 1 | 247.834288 | 829.653164 | 0.000 |

| Residual | 146.074254 | 489 | 0.298720 | |||

| Total | 393.908541 | 490 | ||||

| Model | R | R Square | Adjusted R Square | Std. The Error of the Estimate | Sig. |

|---|---|---|---|---|---|

| 1 | 0.660 | 0.435 | 0.43 | 0.674467 | 0.000 |

| Model | R | R Square | Adjusted R Square | Std. The Error of the Estimate |

|---|---|---|---|---|

| 1 | 0.575 a | 0.330 | 0.329 | 0.734 |

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|---|

| 1 | Regression | 130.076807 | 1 | 130.076807 | 241.09138 | 0.000 b |

| Residual | 263.831734 | 489 | 0.539533 | |||

| Total | 393.908541 | 490 | ||||

| SEM | GFI | RMR | CFI | NFI | TFI | RMSEA |

|---|---|---|---|---|---|---|

| 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.15 |

| Estimate | S.E. | C.R. | P | |||

|---|---|---|---|---|---|---|

| PFD | <--- | ERMS | 0.16 | 0.06 | 3.27 | *** |

| PFD | <--- | CRA | 0.28 | 0.05 | 4.43 | *** |

| PFD | <--- | SRA | 0.15 | 0.04 | 3.39 | *** |

| PFD | <--- | CSR | 0.22 | 0.03 | 6.09 | *** |

| PFD | <--- | ERMS_x_CSR | 0.17 | 0.07 | 2.19 | 0.04 |

| PFD | <--- | CRA_x_CSR | 0.11 | 0.07 | 1.20 | 0.12 |

| PFD | <--- | SRA_x_CSR | 0.04 | 0.05 | 0.69 | 0.44 |

| PFD | <--- | BO | 0.02 | 0.05 | 0.27 | 0.72 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sarfraz, M.; Qun, W.; Hui, L.; Abdullah, M.I. Environmental Risk Management Strategies and the Moderating Role of Corporate Social Responsibility in Project Financing Decisions. Sustainability 2018, 10, 2771. https://doi.org/10.3390/su10082771

Sarfraz M, Qun W, Hui L, Abdullah MI. Environmental Risk Management Strategies and the Moderating Role of Corporate Social Responsibility in Project Financing Decisions. Sustainability. 2018; 10(8):2771. https://doi.org/10.3390/su10082771

Chicago/Turabian StyleSarfraz, Muddassar, Wang Qun, Li Hui, and Muhammad Ibrahim Abdullah. 2018. "Environmental Risk Management Strategies and the Moderating Role of Corporate Social Responsibility in Project Financing Decisions" Sustainability 10, no. 8: 2771. https://doi.org/10.3390/su10082771