1. Introduction

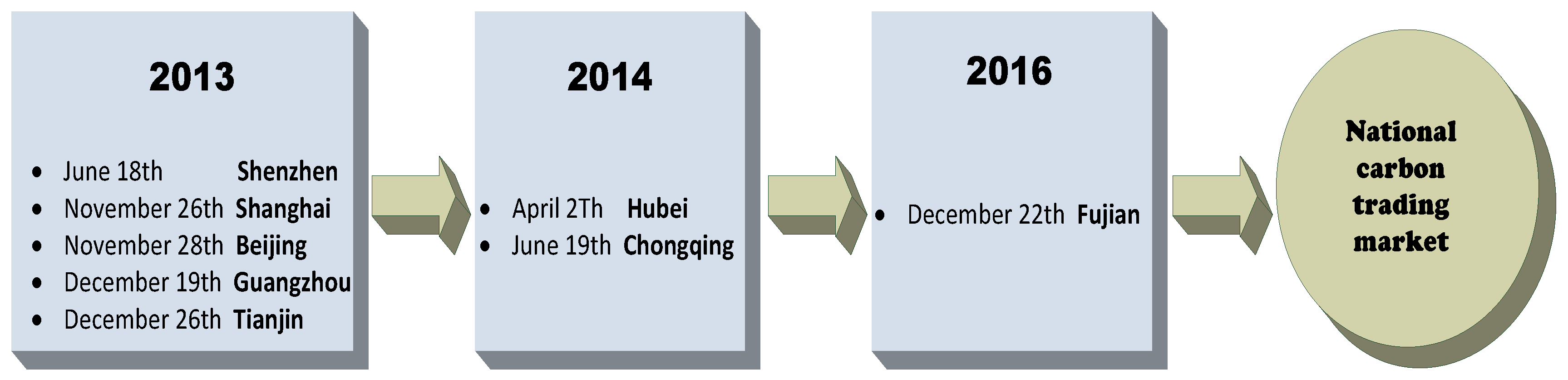

Energy structure adjustment, the development of energy conservation, and emission reduction have all become an important part of sustainable development strategy in China. In order to achieve effective control of total carbon emissions and guide enterprises to actively participate in emission reduction work, China’s carbon trading market has developed rapidly. Since October 2011, China has successively established trials of carbon emissions trading in seven provinces and cities, including Shenzhen and Shanghai, as shown in

Figure 1. The carbon emissions trading system officially opened in December 2017 in the country. As of the end of October 2017, a total of 13.325 million tons of quota transactions had been completed, and the cumulative carbon trading volume exceeded 2.7 billion yuan. China has become the second largest carbon market in the world [

1].

Thermal power enterprises are one of the main targets of carbon emission control in China, and they are also important participants in the carbon trading market [

2]. According to the “National Carbon Emissions Trading Market Construction Plan (Power Generation Industry)” issued by the National Development and Reform Commission in December 2017, the power generation industry is the leading pilot industry for the development of the national carbon trading market. As a result, the participation of coal-fired power companies in carbon trading which occupies up to 64.04% in the power structure has great potential for development. As shown in

Figure 2, the total amount of carbon emissions from thermal power generation in the country from 2010 to 2016 was more than 3 billion tons, accounting for more than 20% of the country’s total carbon emissions [

3,

4,

5]. Carbon quota trading will be a significant means for thermal power enterprises to control carbon emissions actively in the future.

Under the development requirements of carbon emission reduction control, thermal power enterprises urgently need to improve their business performance through environmental cost management. Some studies have found that between 2003 and 2011, the proportion of eco-environmental costs in developing countries to GDP was approximately 20.79% to 23.02%, and that of developed countries was only 3.99% to 4.22%. So the issue of environmental costs has become a considerable constraint factor for the development of high-energy-consuming enterprises. The national emission reduction control intensity has been gradually strengthened, and the pressure on enterprises to reduce emissions continues to increase. It is of utmost importance for thermal power enterprises to manage business performance considering the environmental costs, including their operating results, development potential, and business management level. Therefore, under the market environment where carbon trading is actively developing, the design of environmental cost composite measurement indicators, and then the analysis of operating performance considering environmental costs, can provide important support for corporate strategy formulation and sustainable development [

6]. At the same time, in-depth analysis of the relationship between environmental costs and business performance, mining business efficiency, data envelopment analysis (DEA) efficiency considering environmental costs and putting forward business performance optimization strategies, can provide theoretical and methodological references for thermal power companies to better adapt to the development of the carbon trading market and to support corporate environmental cost management and business performance optimization.

2. Literature Review

In recent years, the issue of environmental costs has received widespread attention. The United States Environmental Protection Agency (USEPA) formally proposed the concept of environmental costs in 1995 and divided it into four categories: traditional costs, potential costs, contingent costs, and relationship and image costs. In terms of environmental cost accounting, management, and disclosure, Takanobu Kosugi combined a life cycle impact assessment model, an optimal economic growth model, and a comprehensive assessment model to conduct an econometric analysis of corporate costs. Chou designed and developed the evaluation system of carbon emissions and the special calculation method of environmental cost in the construction industry [

7]. More and more scholars have made different statements on the significance and quantitative relationship of environmental cost to firm performance. After investigation, Mokhtar et al. found that Malaysian listed companies have incorporated environmental information into performance measurement, control and report [

8]. Haggard and other scholars point out that, voluntary disclosure of environmental accounting information by enterprises enhances the transparency of enterprises, and effectively reduces the cost of obtaining environmental accounting information for investors, which is very beneficial for reducing the volatility of stock prices and maintaining the stability of the market value of the company [

9]. With transfer costs, competition intensity, interaction theory and the interactive perspective, Taiwen and other scholars found that financial performance is positively related to the environmental management system, and found that the in-depth study of environmental costs and the construction of a good environmental management system have positive significance for business performance [

10]. Ramos-Real et al. used data envelopment analysis to evaluate the business performance of 18 power companies in Brazil from 1998 to 2005 [

11].

After 2002, with global warming and the signing of the Kyoto Protocol, the situation of carbon trading and carbon information disclosure in enterprises gradually attracted the attention of researchers in accounting circles. Larrinaga and Bebbington think that controlling carbon emissions is an important part of enterprise environmental management. Therefore, enterprises need to disclose carbon information [

12]. Schaltegger suggests that in the context of a low-carbon economy, new management methods and models are needed to predict and meet new carbon information needs [

13]. Brawn et al. believe that companies should recognize the carbon emission obtained free of charge from the government as intangible assets at the market price at the time of acquisition, followed by amortization, and the book value of carbon emission rights should be adjusted at the end of the period according to the market price of the carbon emission rights. When sold, the difference between income and book value of carbon emission rights should be recognized as liabilities [

14].

With the development of a low-carbon economy, the problem of carbon emission control in thermal power enterprises is becoming more and more prominent. Zhai, H. adopts a power plant modelling tool to reduce the unit CO

2 emission rate by 30% through the carbon capture, utilization, and storage (CCUS) modification of the existing US coal-fired generating units (EGUs). [

15]. Cristóbal, J. used a mixed integer nonlinear programming (MINLP) model to optimize the power production of coal-fired power plants with carbon management [

16]. Having studied, SQ, Jiang found that coal-fired power plants installed in China between 1993 and 2013 will lead to 106 Gt of carbon dioxide emissions during their average lifetime, more than three times the global carbon dioxide emissions from fossil fuels in 2010 [

17]. Wang, J. analyzed the impact of coal-fired power generation on the environment in China by using the life-cycle assessment (LCA) method, and the cost of resource consumption and external environmental cost of coal-fired power generation was further calculated by using the related cost theory [

18]. Du, L. found that Chinese coal-fired power plants have great opportunities to reduce carbon dioxide emissions, and older and larger power plants have lower environmental efficiency and marginal carbon dioxide emission reduction costs [

19]. In the aspect of business performance research in Thermal Power Enterprises, a new two-stage network DEA model was proposed by Bi, G.B. to evaluate the performance of coal-fired power generation in China by improving the link constraints which is different from the traditional network DEA method [

20]. To evaluate the performance and output level of coal-fired power plants in the United States, Färe, R. constructed the environmental performance index (EPI) [

21].

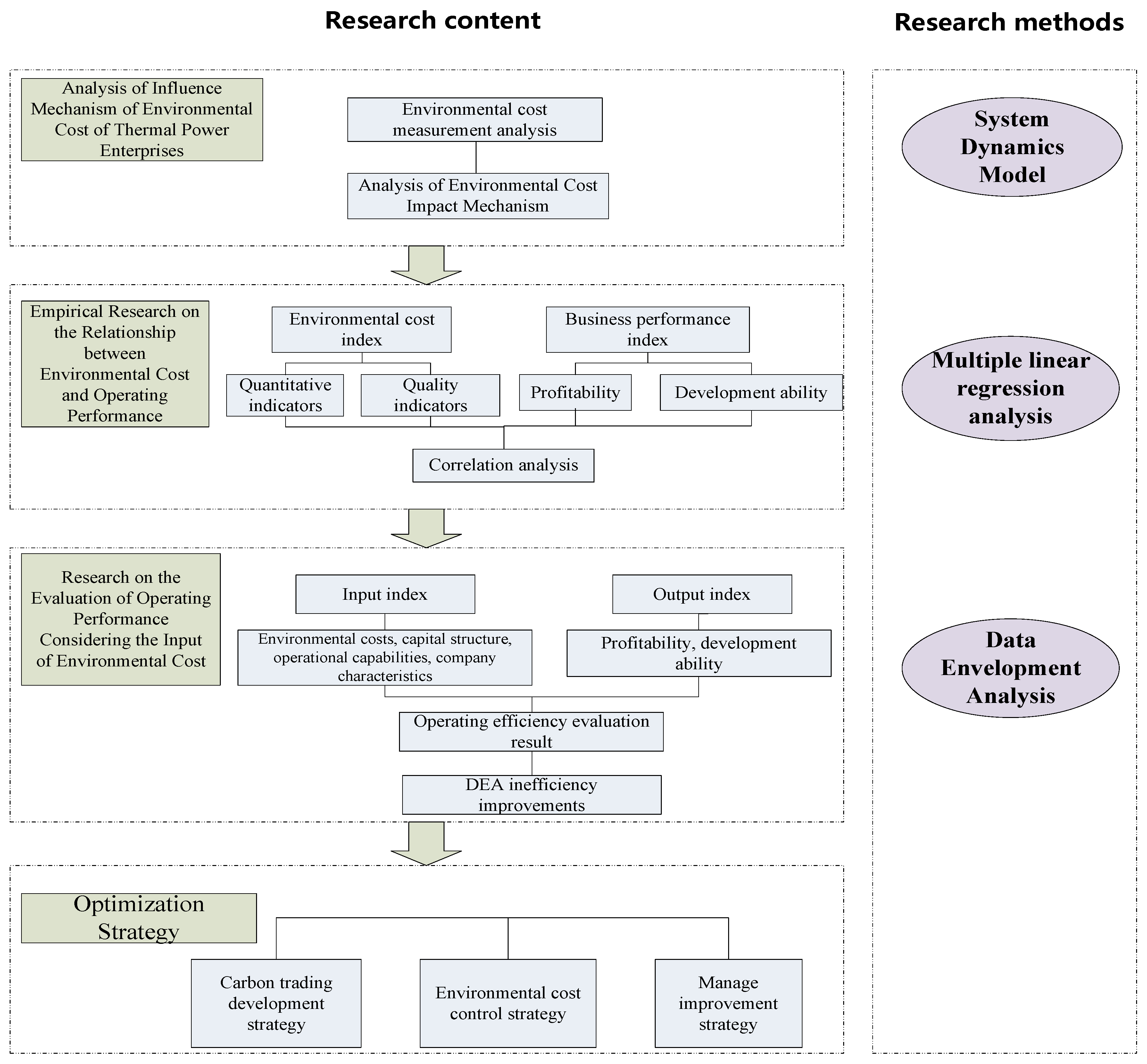

In summary, the academic community has carried out certain exploration research on the environment cost, enterprise carbon trading, and carbon emission, and has also carried out certain analysis on thermal power enterprise carbon emission reduction and management performance. However, under the development of the carbon trading market, the research on relationship analysis and evaluation of environmental cost and operating performance of thermal power enterprises is relatively lacking, and the measurement research of the environmental cost index is limited to the quantitative index and index design and measurement of environmental cost quality need to be deeply studied. Therefore, this paper selects thermal power generation enterprises as the research object, carries out measurement analysis on its environmental cost from the quality and the quantity aspect, modeling studies on the correlation between the environmental cost and management performance, scientifically assessing the level of business performance considering environmental costs, and then puts forward the optimization of management and the control strategy to enhance the sustainable development ability of thermal power enterprises under the background of carbon trading, which has a certain theoretical research value.

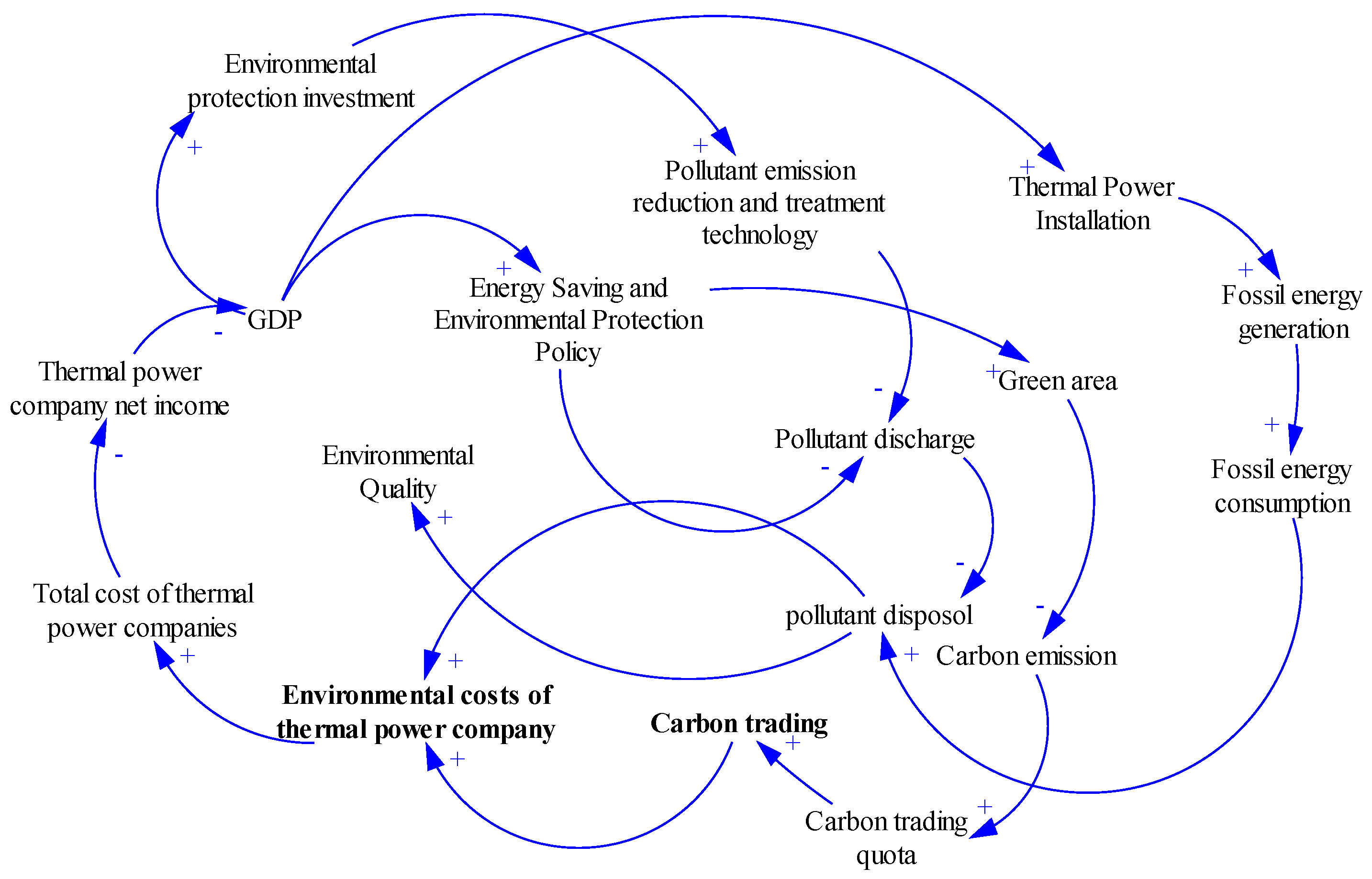

5. Analysis of the Correlation between Environmental Costs and Business Performance of Thermal Power Enterprises

5.1. Index Design and Correlation Analysis Model Construction

Business performance is a very broad concept. It refers to the contribution made by the company’s strategy and its implementation and execution to the final business performance of the company within a certain period. It shows the strength of the company in terms of asset profitability, operations, debt repayment, anti-risk, and growth, and it is an important part of the company’s overall strength. In the context of a low-carbon economy and sustainable development, according to previous research results and the characteristics of production and operation of thermal power companies, this paper defines the thermal power company’s operating performance as follows. In a certain period of time, thermal power companies fully and rationally use their various resources for production, which is based on the principle of maximizing corporate value and shareholder value, and through the provision of low-carbon, green, stable, high-quality power products, demonstrate the operating results, development potential and management level. The level of operating profit and the growth of operating income can more intuitively reflect the business performance of the company.

Thermal power enterprises are asset-intensive enterprises, their own profitability and growth ability is the focus of business performance. Therefore this paper chooses Rate of Return on Common Stockholders’ Equity (ROE) as the index to measure the profitability of power generation enterprises and chooses Increasing Rate of Sales Income (ORIR) as the index to measure the growth ability of power generation enterprises. In order to measure the environmental cost level of thermal power enterprises in an all-round way, two indexes of quantity and quality are set up in this paper, that is, the environmental cost is evaluated by using the Environmental Cost Index (EC) and the Environmental Cost Disclosure Quality Index (ECQ) is used to measure the quality of environmental cost information disclosure. In addition, this paper introduces Asset-liability Ratio (DEBT), Total Assets Turnover (ATAR), Firm Size (SIZE), and Firm Age (AGE), taking them as control variables, because they are considered to be more important influencing factors of business performance. The model variables are summarized in

Table 4 below.

The indicators are calculated as follows.

5.1.1. Environmental Cost Numerical Index (EC)

, where C1 is the cost for pollution discharge and C2 is the purchase cost of the carbon dioxide emission quota. The two calculation methods were explained in the previous article, and OC is the total operating cost of the enterprise.

5.1.2. Environmental Cost Disclosure Quality Index (ECQ)

In order to obtain the Environmental Cost Disclosure Quality Index (ECQ), this paper designs an evaluation system of environmental cost disclosure quality index, which is analyzed from two aspects: Disclosure method aspect and disclosure content aspect. As is shown in

Table 5, the system consists of 13 sub-items. With regard to the method, environmental costs are disclosed, a score of 0 for non-disclosure of environmental cost information in any public report; a score of 1 for disclosure of environmental cost related information only in enterprise annual reports; and a score of 2 for disclosure of environmental cost related information in social responsibility report or sustainable development report in addition to its annual report. With regard to the content, environmental costs are disclosed, score for disclosure of environmental costs if no information is disclosed publicly is 0; score for the project only carried on the text description is 1; score for the project carried on the text and digital disclosure is 2; score for the project fully disclosed and share the list description is 3. For the convenience of statistics, we multiply the obtained quality evaluation score by 100/38 to convert the total score from 38 to 100.

5.1.3. Rate of Return on Common Stockholders’ Equity (ROE)

ROE = Profit after tax/average net assets

5.1.4. Increasing Rate of Sales Income (ORIR)

ORIR = Sales growth/total prior year sales × 100%

5.1.5. Asset-Liability Ratio (DEBT)

DEBT = Total liabilities at end/total assets at end × 100%

5.1.6. Total Assets Turnover (ATAR)

ATAR = Net operating income/average total assets

5.1.7. Firm Size (SIZE)

SIZE = Ln(Total assets of enterprises)

5.1.8. Firm Age (AGE)

AGE = Enterprise listing year − Reporting year + 1.

To sum up, this paper constructs the following two empirical analysis models:

The relationship between environmental cost and ROE of thermal power enterprises (A) is as follows:

The relationship between environmental cost and ORIR of thermal power enterprises (B) is as follows:

where α is model intercept term, β is the regression coefficient of the model, Ɛ is the stochastic error.

5.2. Sample Selection

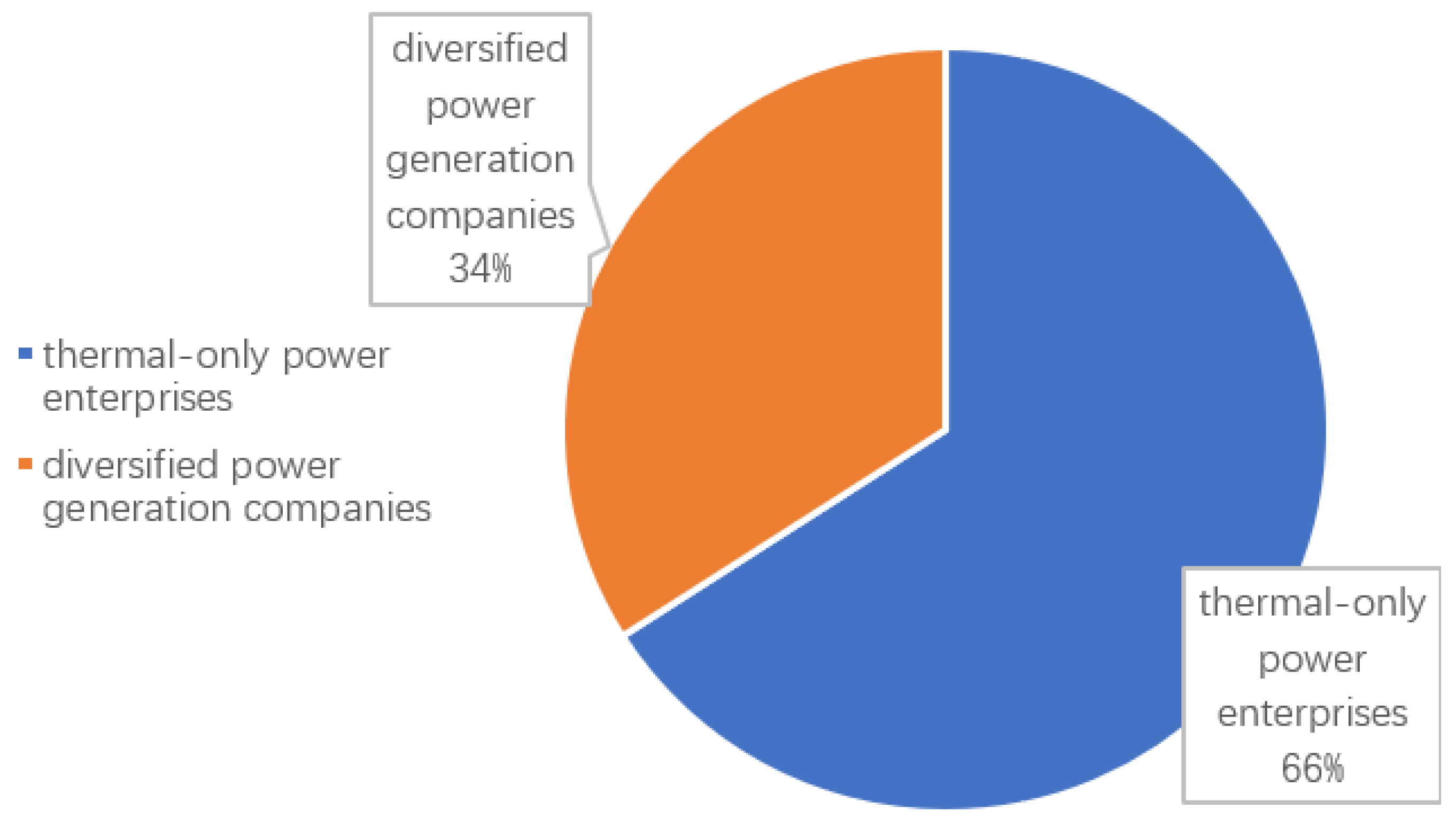

This paper selects listed companies of A share power of thermal power generation listed in the power plate of Sina Finance, excluding *ST enterprises and those whose data are incomplete or abnormal in the reporting period; because carbon trading officially opened the pilot project in 2013, considering there is a certain time lag of its influence on the actual production and operation of power generation enterprises, we finally selected the effective sample values from 2014–2016 of 36 listed thermal power companies, as Datang Co., Ltd. (601991), Huadian Power International Co., Ltd. (600027), with a total sample capacity of 108. The imperfection disclosure mechanism of environmental cost information in thermal power enterprises leads to incomplete cost information and scattered distribution. Therefore, in addition to the annual report, this paper also carries out artificial data collection and statistical analysis on the enterprise social responsibility report, the sustainable development report, the electricity generation completion announcement etc. Social responsibility reports and sustainable development reports are from the data center of Eastmoney.com. Financial data are from the Reese Database (RESSRT) and CCER Database.

5.3. Research Hypothesis

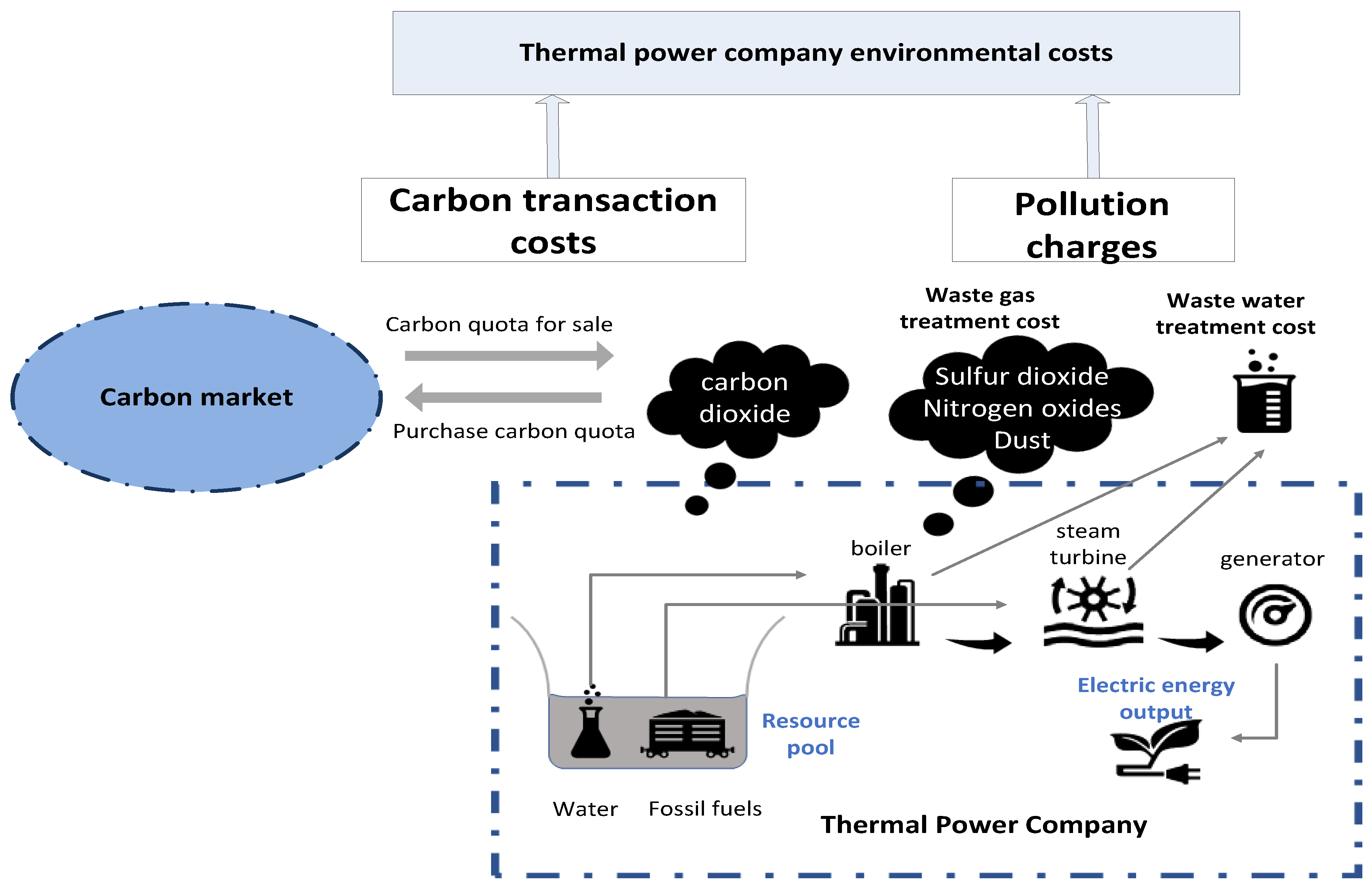

Thermal power companies, like other companies, are economic organizations that seek to maximize profits. Only by reducing its own production and operating costs can there be more room for profit. Therefore, in line with the principle of cost-effectiveness, companies are committed to continuously reducing costs to increase revenue. Its own technological process and production and operation characteristics have determined that thermal power companies are facing enormous environmental pressure. In order to reduce the impact on the environment, thermal power companies need to pay higher environmental costs throughout their entire life cycle. Under the background of the near-completion of the carbon trading market, the purchase expenditures for CO

2 emission right quotas will also be gradually included in the environmental costs that thermal power plants need to pay and lead to the direct outflow of money, which may further reduce corporate profits. However, environmental costs do not only lead to the direct outflow of economic benefits. The environmental prevention costs that companies actively pay for, such as the R&D of clean power generation technologies and the construction of environmental protection facilities, may increase the power generation efficiency of enterprises and reduce the emission levels of pollutants, which will have a positive and positive impact on business performance in the future. At the same time, the relatively high cost of post-environment compensation paid by the company may stimulate the company to strengthen its energy-saving transformation work, strengthen management, improve the company’s operating efficiency, and actively carry out development and transformation, thus ultimately promoting improvement of the company’s operating performance. Darnall N. et al. analyzed the samples from more than 100 listed companies in different industries and found that there was a significant positive correlation between environmental costs and business performance [

30]. Based on the above analysis, this paper proposes Hypothesis 1:

Hypothesis 1 (H1). There is a positive correlation between environmental cost and business performance.

Business performance is the embodiment of the company’s operating results over a period of time and the management of the business operators. It can be evaluated in terms of profitability, dividends, and development capabilities. Therefore, for thermal power companies, Han F. et al. believe that profitability and growth ability are key factors in evaluating their operating performance [

31]. Based on Hypothesis 1, this article proposes the following two sub-hypotheses:

Hypothesis 1.1 (H1.1). The environmental cost of the enterprise is positively related to the profitability of the enterprise.

Hypothesis 1.2 (H1.2). The environmental cost of the enterprise is positively related to the development ability of the enterprise.

The Environmental Cost Quantity Index and Environmental Cost Disclosure Quality Index are two aspects of the composite measurement of environmental costs. They show the relationship between environmental costs and business performance indicators from two dimensions. The environmental cost disclosure refers to the enterprise’s disclosure of corporate information such as corporate annual reports, social responsibility reports, and sustainable development reports: the process of revealing the outflow of economic benefits generated. Thermal power companies need to pay high costs every year for the environment. Also, because environmental cost information is scattered and difficult to gather, disclosure of environmental cost information also requires a certain cost. Given the established level of income, the increased cost of the disclosure of environmental cost information will lead to a decline in the profitability of the company. However, based on the concept of social responsibility, corporate disclosure of environmental cost information is a manifestation of the active implementation of social responsibility. The quality of the disclosure of the company’s environmental cost information will help improve the corporate reputation. On the other hand, the disclosure of environmental cost information also urges high-emission and high-pollution power generation enterprises to accelerate the pace of energy conservation and emission reduction, and actively innovate to promote the development of enterprises. In summary, this article proposes Hypothesis 2:

Hypothesis 2 (H2). There is a positive correlation between the quality of environmental cost disclosure and business performance.

Based on profitability and growth ability which are the key factors for evaluating the performance of power generation companies, this paper puts forward two sub-hypotheses based on Hypothesis 2:

Hypothesis 2.1 (H2.1). There is a positive correlation between the quality of Environmental Cost Disclosure and the profitability of Enterprises.

Hypothesis 2.2 (H2.2). There is a positive correlation between the quality of Environmental Cost Disclosure and Enterprise Development ability.

5.4. Empirical Calculation and Conclusion Analysis

5.4.1. Descriptive Statistics

The descriptive statistics of selected samples are shown in

Table 6. The level of operating performance and environmental cost of thermal power enterprises is uneven and the difference is obvious. The enterprise environmental cost quantity index is generally small; the maximum value is only 2.24%. The difference in the environmental cost disclosure quality index is significant, which indicates that the environmental cost disclosure of enterprises is not standardized and not unified. According to the operating performance, the difference of ORIR data is obvious, and the sales income of power generation enterprises is declining. The ROE gap of different enterprises is also large, but it still shows a positive growth trend from the average point of view. From the point of view of control variables, the value of asset-liability ratio of different enterprises fluctuates greatly, and the asset size is large, but the gap is small. The largest age difference between enterprises reached 22, indicating that there are emerging enterprises which keep on joining the power industry.

5.4.2. Correlation Analysis and Regression Test

According to the above hypothesis, we first choose Rate of Return on Common Stockholders’ Equity (ROE) as dependent variables to carry out regression analysis. The results are shown in

Table 7. The test value of model (A)

F is 3.074, passed the significance test. The DW test is 1.830, which indicates that there is no sequence auto-correlation. Since the focus of this study is on the correlation between environmental costs and operating performance, close to 70% of the goodness of fit is considered acceptable. In summary, this paper holds that model (A) has a certain accuracy and can be used in empirical analysis. From the regression results of model (A), both EC and ECQ passed the significance test. There was a significant positive correlation between the Environmental Cost Numerical Index (EC) and the Rate of Return on Common Stockholders’ Equity (ROE), and the coefficient was 4.3. The rise of environmental cost as a proportion of operating cost will significantly stimulate firms to increase their ROE, so the assumption of H

1a is verified. The Environmental Cost Disclosure Quality Index (ECQ) is also positively correlated with the Rate of Return on Common Stockholders’ Equity (ROE), with a coefficient of 0.481. This shows that the improvement of environmental information disclosure quality will promote the profitability of enterprises to a certain extent, so the assumption of H

2.1 is verified.

This paper chooses Increasing Rate of Sales Income (ORIR) as the dependent variable, the result is shown in

Table 8. The test value of model (B)

F is 2.275, passing the significance test. The DW test is 2.077, which indicates that there is no sequence auto-correlation. Model (B) can be applied to empirical analysis. From the regression results, only EC and firm size (SIZE) passed the significance test. There was a significant positive correlation between the Environmental Cost Numerical Index (EC) and the Increasing Rate of Sales Income (ORIR), and the coefficient was 9.936. An increase in the proportion of environmental costs to operating costs will stimulate enterprises’ diversification and transformation and will have a positive effect on the growth of overall sales income of power generation enterprises, and promote the sustained growth of revenue, so the assumption H

1b has been verified. Although the correlation coefficient between ECQ and ROE is positive, neither of these two variables has passed the significance test, which may be related to the low quality of environmental cost information disclosure in thermal power enterprises at present. Therefore, it is assumed that H

2b cannot be verified from model (B) for the time being.

The conclusion of empirical analysis of model (A) and model (B) shows that Hypothesis 1.1, Hypothesis 1.2, and Hypothesis 2.1 are all verified, that is, environmental cost has a positive correlation with business performance, environmental cost information disclosure quality, and profitability.

5.4.3. Conclusion Analysis

Based on the empirical analysis of the correlation between environmental cost and business performance of thermal power enterprises, this paper draws the following conclusions:

- ●

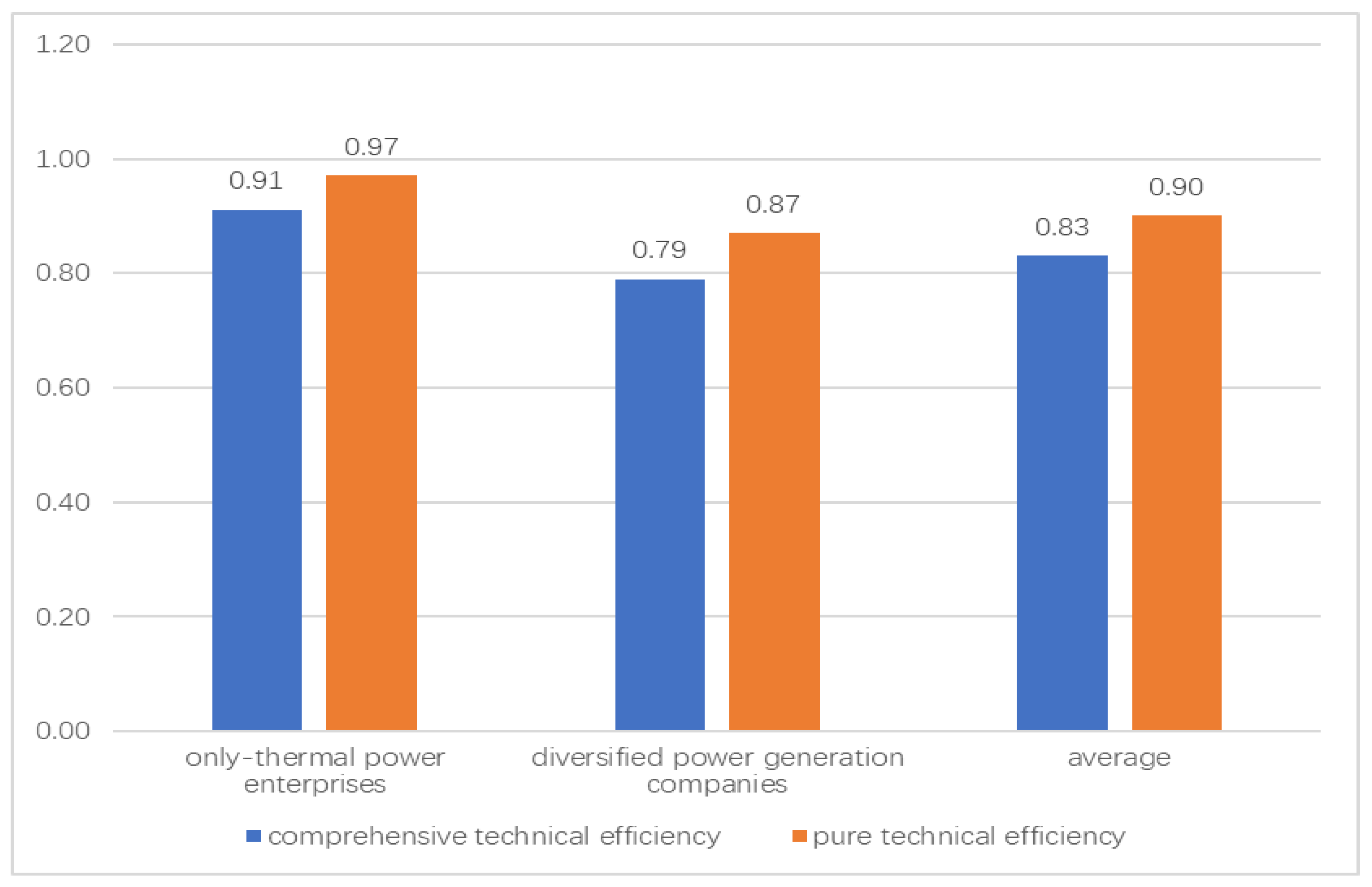

There are significant differences in environmental costs among different power generation enterprises. From the aspect of Environmental Cost Numerical Index (EC), the environmental cost of the power generation enterprise with the thermal power plant accounts for a large proportion of the operating cost. Reducing the proportion of thermal power installed, and diversifying development helps power generation enterprises to reduce environmental costs. Judging from the ECQ, many enterprises do not consider environmental costs, such as greening costs, and the disclosure of carbon trading information is also relatively lacking.

- ●

There is a significant positive correlation between the level of environmental cost and business performance. (1) Environmental Cost Numerical Index is positively correlated with the business performance of power generation enterprises. The high environmental cost expenditure level of power generation enterprises stimulates enterprises to improve their technical level and management ability. It has a positive effect on the profitability and growth ability of power generation enterprises. (2) The Environmental Cost Disclosure Quality Index is positively correlated with the profitability of power generation enterprises. The higher the quality of environmental cost information disclosure, the stronger is the profit of power generation enterprises. In summary, this paper holds that environmental costs and business performance show a positive correlation.

8. Conclusions

This paper explores the relationship between environmental costs and operational performance of thermal power companies in the context of carbon trading through system dynamics, multiple linear regression analysis, and the DEA model, and uses environmental costs as input factors to evaluate the company’s operating performance. This basis provides a strategic reference for thermal power companies to improve their operating performance.

The main contributions of the paper are as follows:

In this paper, the carbon transaction costs are included in the environmental costs for quantitative analysis, which enriches the connotation of thermal power companies’ environmental costs. Based on the research of experts and scholars and the era of the background of carbon trading development, the paper sorts out and summarizes public information of power generation enterprises such as the annual reports and sustainable development reports, so as to include carbon transaction costs in the environmental costs of power generation companies and carries out empirical research and analysis to provide new ideas for companies to conduct more comprehensive and detailed environmental cost management.

Construction of a Composite Index of Environmental Costs Considering Carbon Transaction Costs. In the construction of the indicators of environmental cost for the correlation analysis, this paper constructs an environmental cost evaluation index from a quantitative level and a quality level. Based on the company’s actual power generation, the paper calculated the environmental costs including wastewater discharge, waste gas emissions, and carbon dioxide emission costs, and established an environmental cost quantity level evaluation index. Disclosure of 13 major environmental cost sub-projects, such as equipment investment, monitoring costs, greening costs, and carbon trading conditions, is the basis for evaluation, to construct a more comprehensive evaluation system for public disclosure of environmental cost information. The composite index more comprehensively and clearly shows the environmental cost of power generation companies, which helps to more accurately reveal the relationship between environmental costs and business performance and lays a good foundation for empirical evaluation research.

Research on the evaluation and optimization strategy of power generation companies’ operating performance based on the input of factors such as environmental costs was carried out, and the content of correlation analysis was supplemented and improved, making the research conclusions more quantitative and specific. This paper takes the quantity and quality of environmental costs, and the size of corporate assets as input factors, analyzes the extent of actual impact on the thermal performance of thermal power companies, and proposes the direction and degree of improvement of each input factor based on the projection analysis method. The evaluation study supplements the correlation between environmental costs and operating performance and proposes corresponding strategies for effectively improving the performance of power generation enterprises in the context of carbon trading.

Based on this, the main conclusions of this paper are:

- ●

There is a positive correlation between environmental costs and operational performance of thermal power companies. The increase in corporate environmental cost input has a certain role in promoting the improvement of business performance. This provides certain theoretical support for thermal power companies to increase their investment in environmental protection and better fulfill their social responsibilities.

- ●

The increase in environmental costs and other inputs of production factors are the direction of important measures for improving the operating efficiency of thermal power companies. The analysis of the relaxation degree of input–output indicators of thermal power companies based on projection analysis shows that insufficient input of major factors such as environmental costs and financial leverage leads to insufficient output factors of power generation enterprises.

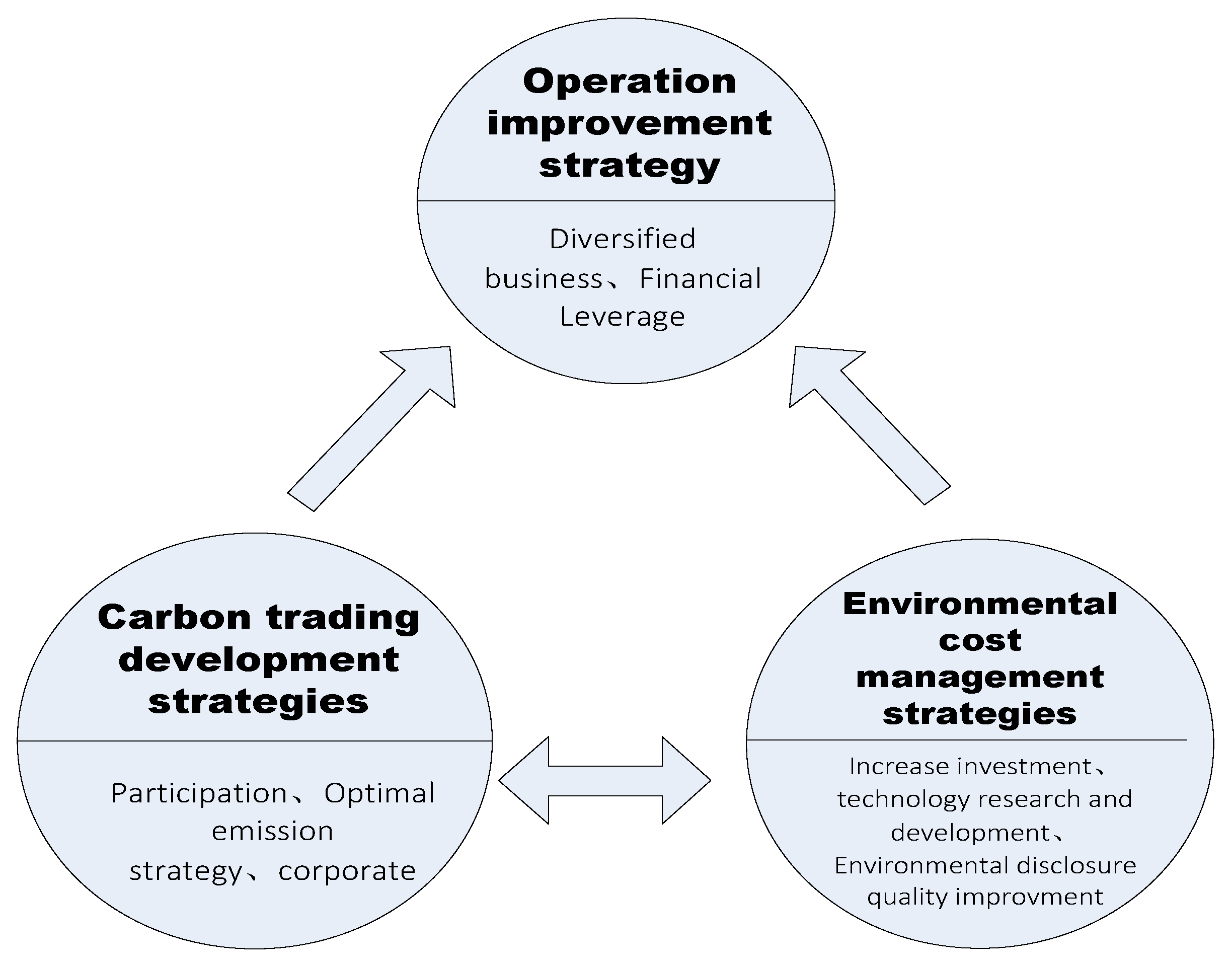

- ●

Thermal power companies should formulate optimization strategies for business performance from the aspects of carbon trading participation, environmental cost management, and operation management, and achieve improvement of business performance.

The above conclusions are innovative and enriching and expand the research results of existing literature. First of all, from the perspective of the selection of research objects, most of the existing literature separately conducts a quantitative analysis of the environmental cost elements of thermal power companies, establishes an environmental cost measurement model, and taps its sensitivity factors to determine the optimal pollutant emission reduction optimization program [

32]. There is also literature on the performance indicators of the polluting industries, including thermal power companies. In the context of energy conservation and emission reduction, thermal power companies’ business performance is evaluated from the perspective of R&D investment [

33,

34]. The comprehensive development of China’s carbon trading market will inevitably have an important impact on thermal power companies’ environmental costs and operating performance. Few literature works have studied the relationship between the two in the new development of carbon trading. This article combines the environmental background of carbon trading with the environmental costs of thermal power companies and business performance, explores the correlation between the two, and concludes that the environmental costs are positively related to business performance, achieving the extension and supplementation of previous research conclusions. Second, as far as the selection of research methods is concerned, in the previous literature, when the environmental cost was measured and analyzed, it was mostly limited to measurement and accounting on a quantitative dimension, and the combination of environmental cost accounting and environmental cost indicators was studied in order to make business decisions as reference for sustainable development [

35]. However, this article innovatively introduced environmental quality indicators, to construct a more comprehensive environmental quality information disclosure quality evaluation system, which together with quantitative indicators constitute a more scientific and reasonable environmental cost compound measurement indicator. When existing literature conducts business performance research, it mainly analyzes and evaluates financial aspects, and performs cost-benefit assessment and poor performance management improvement for the company considering electricity price and power generation cost [

30]. However, this paper analyzes the DEA efficiency of business performance, and focuses on the impact of the input cost of environmental costs on business performance. It was found that the lack of input in major factors, such as environmental costs and financial leverage, causes the output elements of the power generation enterprises to be insufficient. In addition, in the field of thermal power companies’ business performance improvement and sustainable development optimization strategies, the existing literature mainly seeks corporate performance improvement strategies from the perspective of the main business [

36]. However, the strategy of this article highlights the important factor of environmental costs, and encourages companies to actively participate in carbon trading, which has effectively expanded and enriched existing strategies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}