1. Introduction

Housing is a substantial economic force. In the United States, spending on housing and housing services has tended to represent 15% of GDP. In China, the focus of this paper, housing spending has grown to 8% of GDP. Rapidly increasing home prices are problematic and raise concerns against sustainable development [

1], such as increased financial pressure on households and large real-estate bubbles. These high prices have resulted in a disproportional price-to-income ratio that largely exceeds the international guard line [

2] and threatens a healthy housing market. An average household looking to buy a house in Shanghai would pay 25 years of income for a 90 m

2 apartment. Furthermore, as housing price booms typically lead to busts, a financial crisis may be triggered [

3].

Housing is a complex bundled good and changes in pricing indicate the weighted average change in the value of its constituent components [

4,

5]. Housing has important connections to household behavior, local and national policy, and the environment [

6]. A user of all factors of production, housing is routinely associated with consumption of land, energy, and materials. Importantly, as housing has a fixed location, its relative location ties it both to filtering processes [

7] and to transportation and the related expenses and externalities [

8,

9].

Given the complex connectivity between these issues, sustainability in housing has typically been examined as a function of resource and location efficiency. Studies have examined sustainable construction product selection [

10]; energy efficiency and the role of eco-certification schemes [

11,

12]; as well as traditional neighborhood design [

13] and walkability [

14]. However, as variation in housing supply and home prices, which are metrics describing the bundled consumption of land, housing, and their requisite energy and materials, are associated with inflation [

15], there is an opportunity to study sustainability in housing markets as a function of variation in macro-economic conditions such as central government monetary policy. This opportunity is exploited here.

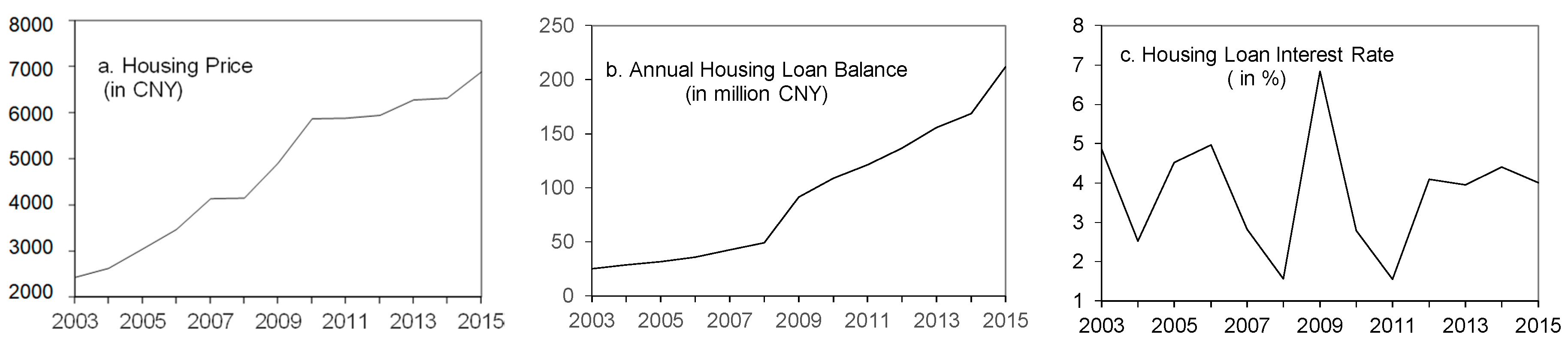

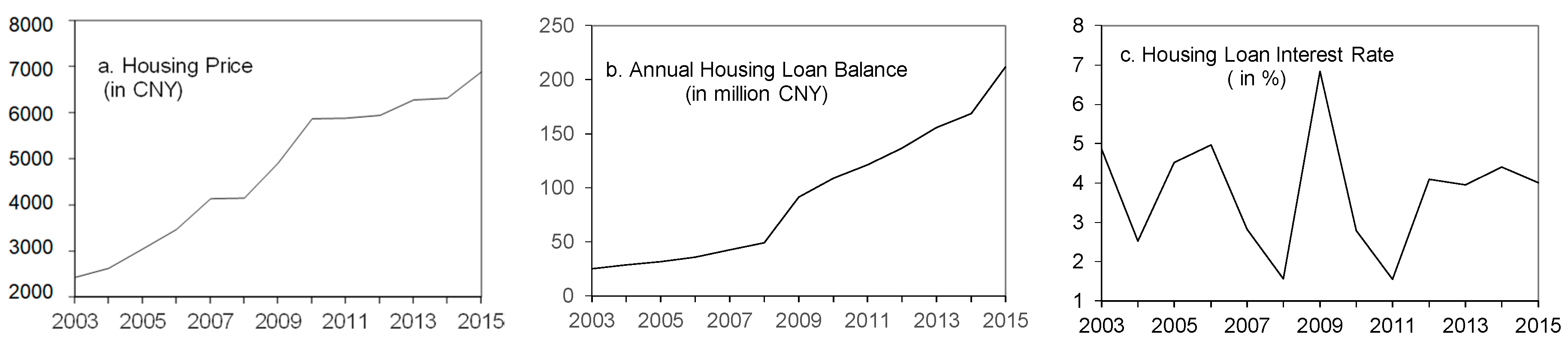

The People’s Bank of China, the central bank, uses monetary controls as primary macroeconomic means to cool overheated housing prices. Limiting the housing loan supply (i.e., bank lending) and increasing the borrow rate are two common monetary policies used to ensure price stability [

16]. The central bank can increase the interest rate or reserve requirements to reduce the liquidity of commercial banks. In response, the banks cut back on the supply of mortgages and loans and effectively limit lending [

17]. The central bank adjusted the borrowing rate for housing loans 24 times from 2003 to 2015 and gradually raised the down payment baseline for a second home from 30% to 60% in the same period. However, housing prices in China continued to increase for decades.

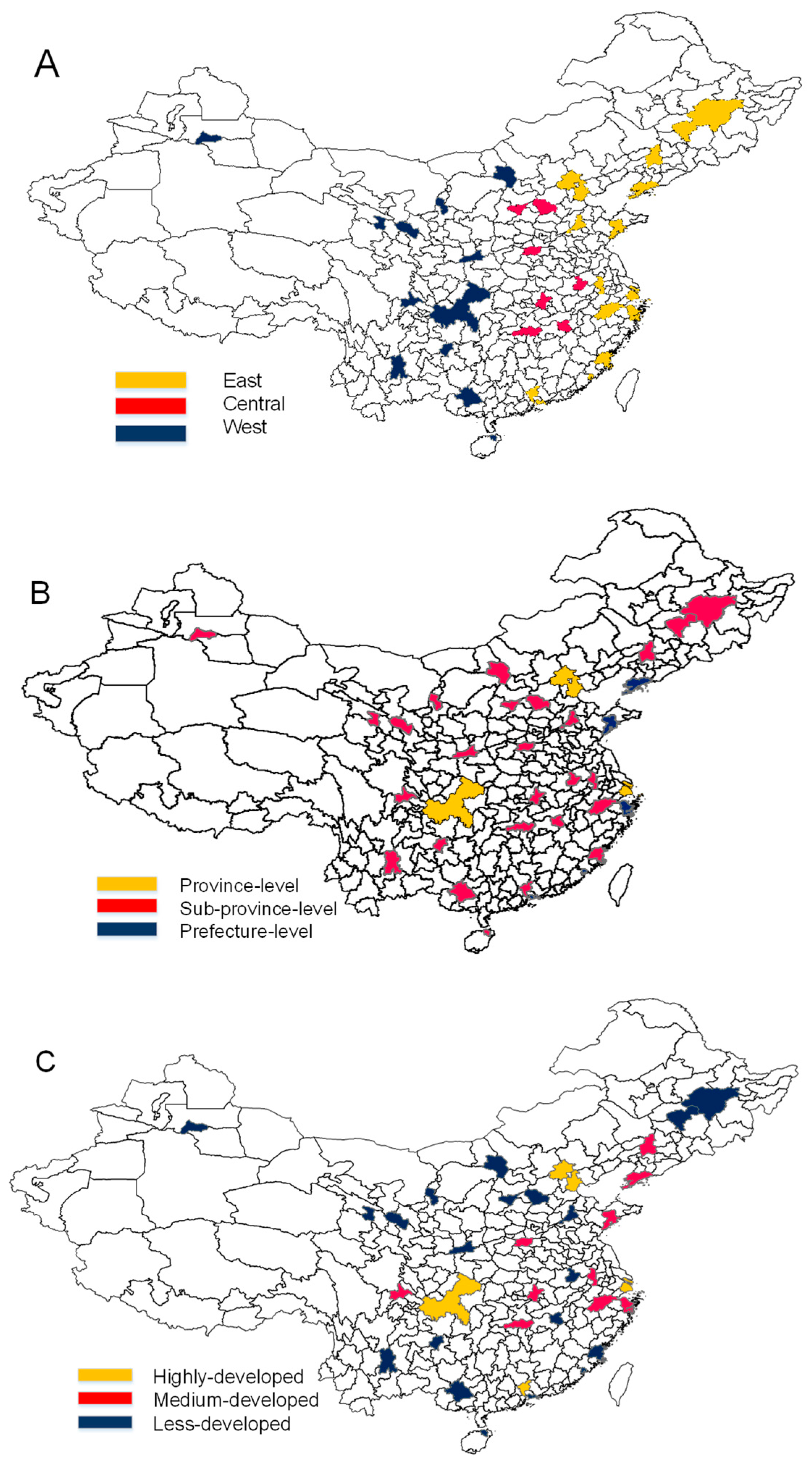

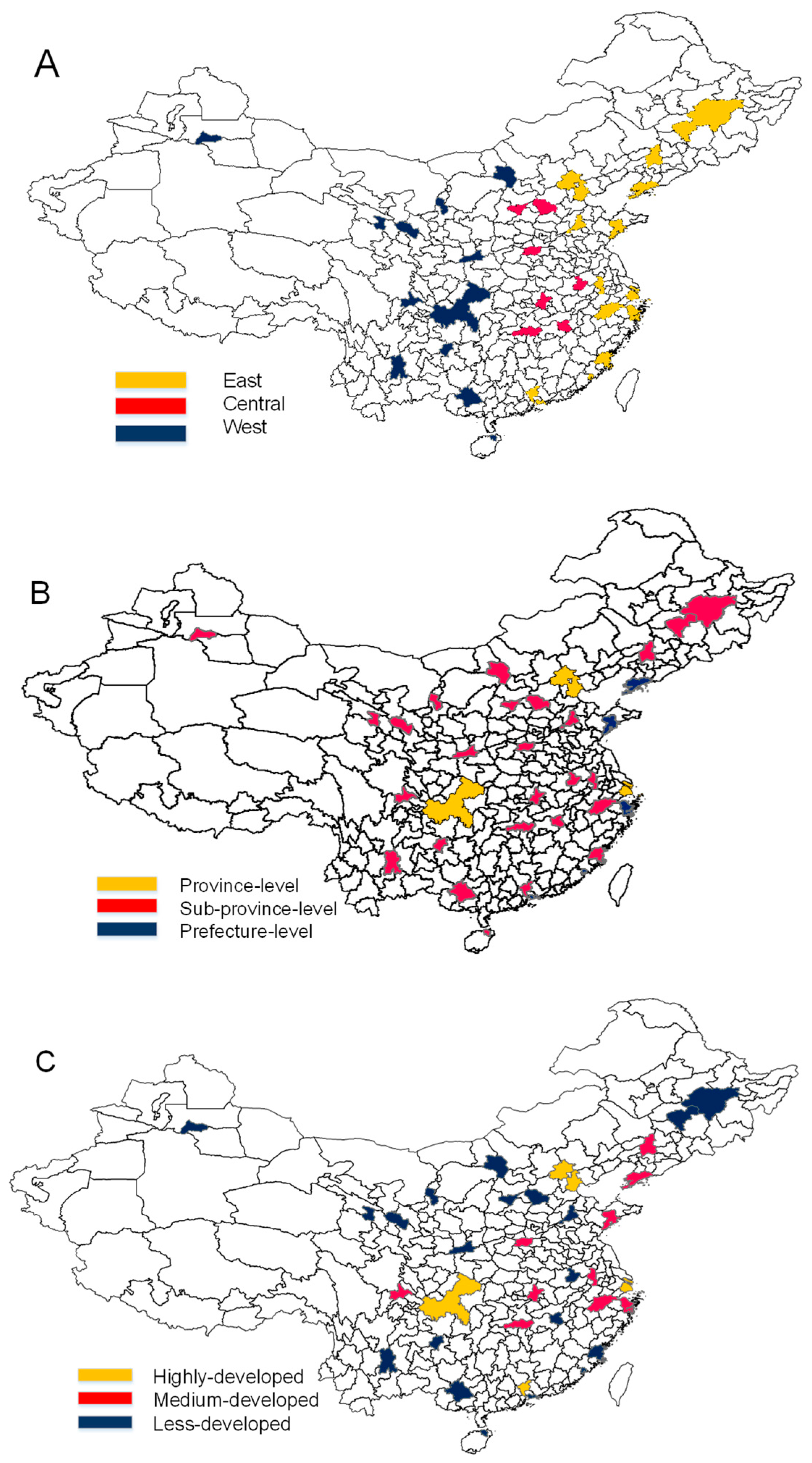

Exploring the inflation-housing supply-housing consumption-sustainability relationship, the objective of this research is to identify the causal effects of bank lending on urban housing prices at city level across varying periods. Unlike extant research mainly focuses on nation-level effects, this study examines such effects of bank lending at national, regional, and city levels. We hypothesize that the causality between bank lending and housing prices varies at city level. We believe that a centralized bank lending policy at the national level is less effective for a sustainable urban housing market. In the context of recent examinations of the influence of various economic policies on housing prices, this paper uses the Chinese property market as the lens through which we examine the effectiveness of central bank monetary policy. More specifically, we investigate whether and how the lending supply through housing loans and the lending rate through interest rates affect housing prices in 35 major Chinese cities. Our argument is that in influencing home prices, the central bank can help to create a more sustainable future for China by shaping the housing supply—and as a result, the utilization of land, materials, and energy.

2. Literature Review

Housing markets and prices are complex and connected to a myriad of factors and forces. Consequently, the literature review below summarizes literature germane to housing price variation in Chinese markets and the role of monetary policy in shaping home prices in a global context. It also describes how sustainability in housing has typically been studied and the opportunity that this paper seizes related to macro-economic forces and their ability to shape a sustainable future in housing. Otrok and Terrones (2005) studied the dynamic properties of house prices, interest rates and macroeconomic for 13 industrial countries. The results showed housing price comovement in 13 industrial countries was related with interest rates, but the response of housing price on U.S. monetary shocks is different between the U.S. and the rest of the world [

18]. Beltratti and Morana (2010) investigated the linkage between housing prices and macroeconomic developments for the G-7. The results showed the linkage between house prices and macroeconomic developments is bidirectional, with investment showing in general a stronger reaction than consumption and output to real house price shocks [

19]. Tsatsaronis and Zhu (2004) studied the impact of macroeconomic factors on housing prices dynamics for several industrialized countries. The results showed house prices were more sensitive to short-term rates, and more aggressive lending practices are associated with stronger feedback from prices to bank credit [

15]. Manganelli et al. (2014) used VAR model to investigate the relationships between selling and rental prices of the Italian housing market. The results showed housing prices were highly responsive to short-term real interest rates [

20]. Manganelli and Tajani (2015) used VAR model to analysis the impact of economic system on housing prices trend in the USA and in Italy. The results showed the lending rate can contribute to explaining the variability of the Italian housing prices, but has no effect in the American model [

21].

The Chinese property markets and government interventions used to guide and manage them have been the subject of a growing body of scholarship [

22,

23,

24]. From gentrification patterns [

25], to the role of city mayors in moderating environmental externalities [

26], to the creation of repeat sales indices using emerging data [

27], researchers have investigated and explored the complexities of one of the fastest growing residential markets on the planet. One vein of the extant literature has sought to explain factors associated with variation in Chinese home prices. Zheng at el. [

26] analyzed home price changes using foreign direct investment, ambient air pollution, and wage metrics—finding evidence of a shift from producer cities to consumer cities. Li and Mao [

22] provided a summary of housing policy interventions and observed patterns of mobility within residential markets. Shen [

28] examined the significant price to income ratio growth relative to other developed nations and observed that affordability in Chinese markets remained strong. Further, Ren et al. [

29] applied an auto-regression test for the presence of a housing market bubble and found no evidence that prices exceeded intrinsic values. Wu et al. [

25] analyzed supply and demand factors associated with price movements and noted the importance of land in rising housing prices. Zhou et al. [

30] observed evidence of anchoring behavior in the Chengdu housing market as non-local investors tended to over-pay for similar quality housing units.

Relatedly, both in and out of the Chinese context, scholars have specifically investigated whether monetary controls effectively affect overhead housing prices in the long term, with varying results. Some have asserted that the bank lending supply causes housing price changes [

3,

31,

32,

33,

34]. In other words, housing prices are sensitive to mortgage rates, credit capacity, loan supply, and loan-to-value ratios. Contrasting studies [

35,

36,

37] highlight that housing prices lead to changes in the lending supply through the wealth effect. Moreover, some point out a mutual dependence between housing prices and the lending supply [

38], whereas others underline the lending rate as the cause of housing price increases rather than the lending supply [

39,

40]. The effect of the lending rate on housing prices varies depending on investment need, metropolitan area [

41], city administration, and geographic region [

26,

41]. Specifically focused on the role of central bank economic policy in moderating Chinese housing prices, Li and Xu [

42] found restrictive loans and prices to be effective pricing controls while restricted purchases were not. Chiang [

43] identified a strong association between the role of expansionist monetary policy and rising residential rents. It is from this foundation, that our paper seeks to extend and contribute to the conversation on the influence of central bank policy on housing prices by focusing on monetary policy—namely, lending supply and interest rates at the city level.

Given that housing is a substantial consumer of all factors of production—specifically land, building materials, labor, and energy (both with respect to production and operation)—scholars have tended to study sustainability in housing with resource efficiency questions. Broadly, the resource efficiency questions have focused on the demand for and the value proposition of sustainable housing. For example, analyses examined the diffusion patterns (and as a result the demand for) sustainable construction technologies [

10] and housing in the U.S. [

11]—observing that demand was influenced by climate, policy, and economic conditions. Relatedly, studies have suggested that homes with sustainable features and locations created competitive advantage for owners [

13,

44,

45,

46,

47,

48]. This competitive advantage has carried over to lenders as borrowers on energy efficient homes and homes in more walkable areas tended to be less likely to default on their mortgages than borrowers on similar traditional homes [

12,

14]. Naturally, these connect with research that noted geography and location [

6,

8,

9], taxation schemes [

49], and local policy [

50] are all associated with variation in home prices. Moreover, there are signals from outside of housing suggesting that urban spatial structure and urban form shape transportation patterns, greenhouse gas emissions, and public health [

51,

52].

In the context of the observed relationships between housing supply, housing prices, policy, and sustainability, this paper utilizes a non-traditional pathway. Instead of focusing on the micro-economic choices of individuals and firms and how each of those reflect elements of resource efficiency, this paper focuses on the role of macro-economic effects—namely, central government monetary and lending policies and their ability to influence housing supply and prices. The premise of the argument is a resource efficiency one; that is, to the extent monetary policy controls can shape housing prices and supply (demand for housing), central governments can reduce the production of housing and the land, energy, and materials included therein.

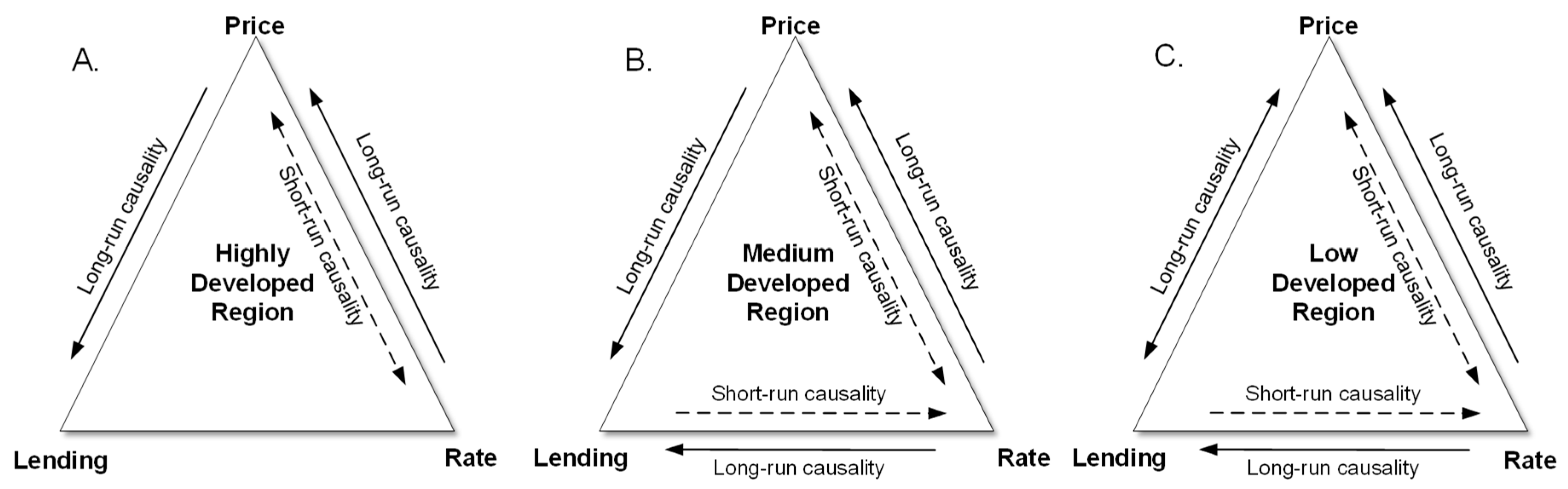

5. Conclusions

We conducted a cross-sectional time-series study to identify the effects of two primary monetary controls—lending supply and the lending rate—on housing prices in urban China. Unlike studies that isolate their analysis to nation-level effects, we analyzed the long-run and short-run causality of lending at national, regional, and city levels. Our data were from 35 major cities in China over the period 2003–2015. Particularly, we examined region-level effects by geographic location, administrative hierarchy, and level of economic development. The major contribution of this study is that we have identified the variance of lending policy on housing prices at the city-level. That is, sustainable urban development relies a more innovative and city-tailed bank lending policy [

65]. In other words, city and local banks should have more authorities to develop effective lending policies.

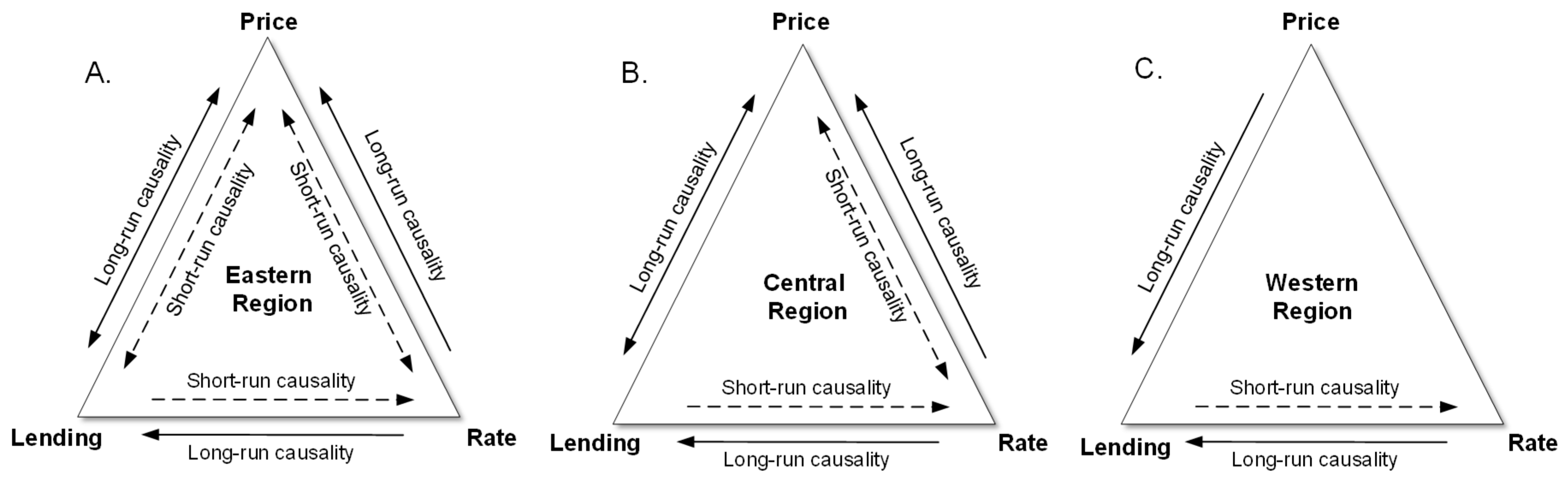

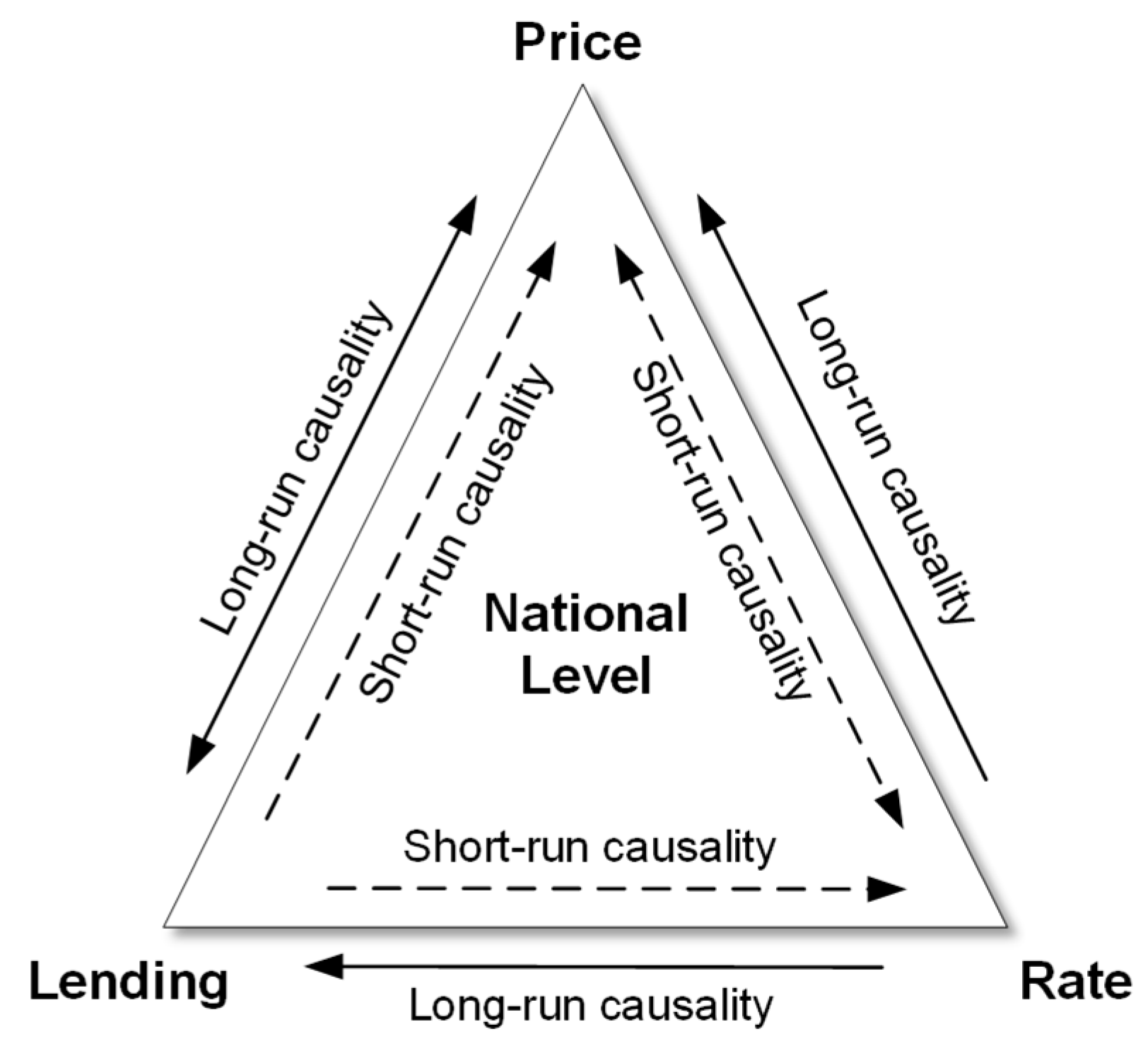

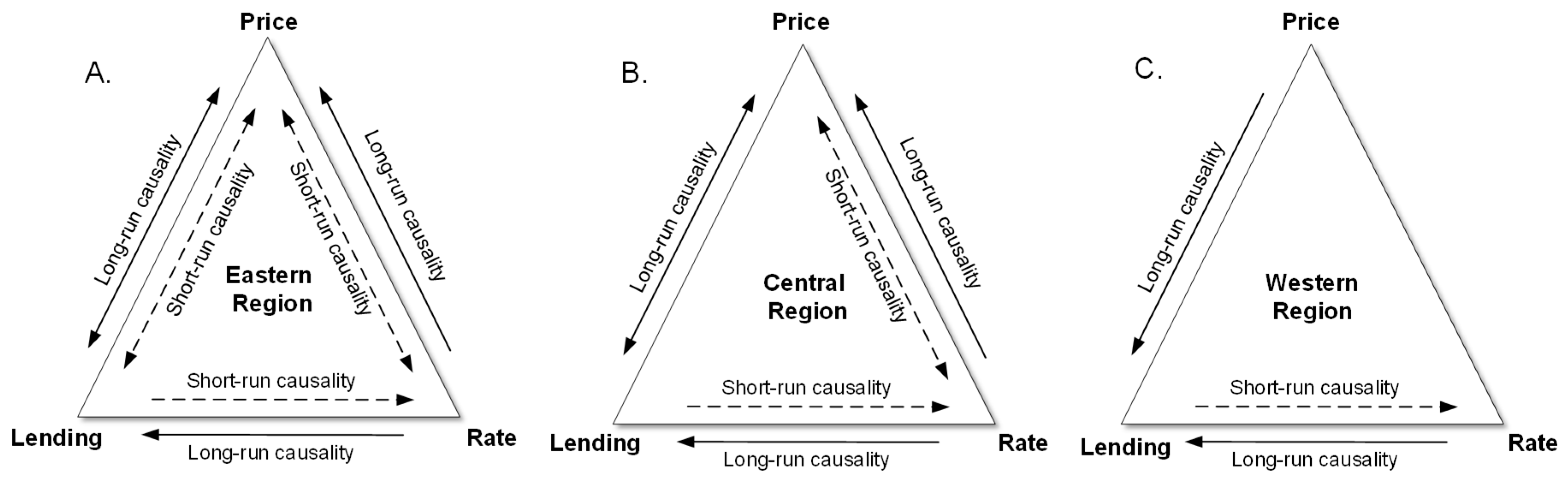

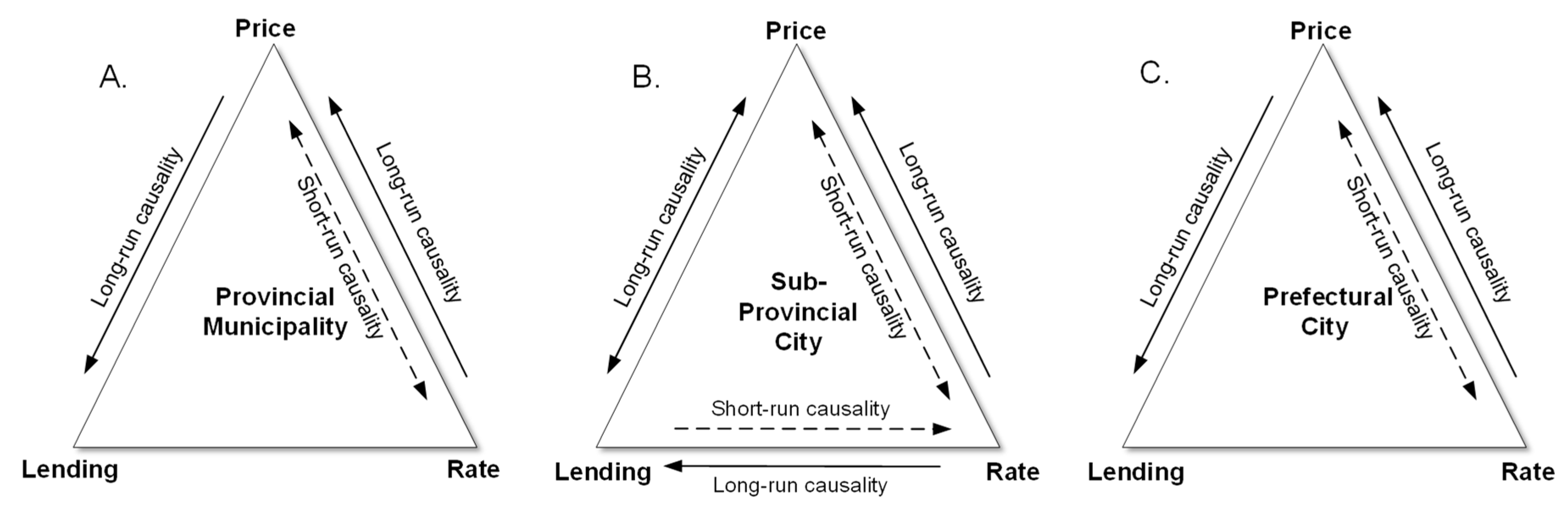

Our results confirm that to cool overheated housing prices in China, controlling lending rates is more effective than controlling the lending supply as a long-term measure. Specifically, at the national level, controls on both the lending supply and the lending rate are effective on housing prices, but they work differently. That is, controlling the lending supply is more effective in the short run, whereas controlling the lending rate is more effective in the long run. At the regional level, controlling the lending rate is effective in eastern and central China, whereas controlling the lending supply is not effective in all geographic regions. Furthermore, controlling the lending rate is effective in all administrative regions, whereas controlling the lending supply does not work well; in addition, controlling the lending rate is effective in highly, medium-, and less-developed economic regions, whereas controlling the lending supply is not. However, adjusting either the lending supply or the lending rate are not an effective approach to short-term controls at the regional level. At the city level, we found that controlling the lending rate is more effective than controlling the lending supply but affects fewer cities.

We found that in many regions, housing prices cause changes in housing loan supply in the long run. This finding suggests that credit policies (e.g., loan constraints) often lag in response to housing price increases. Homebuyers expect higher returns from real-estate investments, implying that policymakers should control the housing loan supply more proactively and systematically in response to such situations. In China, especially in big cities, housing has become an investment rather than solely a consumption good; thus, households are willing to borrow more when they expect housing prices to remain constant or increase [

66]. Housing is also valuable collateral, so banks are willing to lend more during housing price increases [

67]. Moreover, given State ownership of land, it is critical to view the results here in their legal and property rights context—which differs from foils such as that of the United States [

65].

We found considerable variances in the effectiveness of controls across cities. In particular, monetary controls are not effective for 20 out of 35 cities in China. This finding shows the weakness of city-level controls when fighting “hot money” controlled by cross-regional investors seeking short-term returns from the housing market in China. In other words, a centralized macroeconomic regulation at national level seems less sustainable and effective to cities. Therefore, this finding provides practical implications for policymakers in China and similar developing countries [

68] for sustainable urban development while retaining a healthy housing market.

Many future studies can extend this research. First, intelligent simulation tools that can be used to predict housing price changes given certain monetary controls should be developed. These tools will be informative and productive for decision makers when planning monetary control strategies. Second, the effects of monetary controls on a segmented housing market should be investigated. For example, some controls may be especially effective on certain type of properties.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}