Impact of Sustainability Balanced Scorecard Types on Environmental Investment Decision-Making

Department of Accounting, Faculty of Business & Accountancy, University of Malaya, Jalan Universiti, 50603 Kuala Lumpur, Malaysia

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(2), 541; https://doi.org/10.3390/su10020541

Submission received: 14 January 2018

/

Revised: 8 February 2018

/

Accepted: 13 February 2018

/

Published: 17 February 2018

Abstract

:Investment decision-making based on aspects of sustainability is gaining importance among organizations around the globe. In this context, there is a need for quality investment decisions, which require sufficient knowledge among organizational managers about managing sustainability information to achieve environmental objectives that meet stakeholder expectations. This has led to the emergence of organizational performance measuring tools such as the Sustainability Balanced Scorecard, which integrates the environmental perspective into the traditional Balanced Scorecard. Using experimental research method, the objective of this study is to investigate the indirect effect of Eco-efficiency knowledge and Sustainability Balanced Scorecard knowledge as mediators influencing the relationship between Sustainability Balanced Scorecard types and their impact on environmental investment decision-making. Findings of the current research are based on 60 respondents who were randomly assigned to one of the following two types of Sustainability Balanced Scorecard architecture: (1) environmental data embedded within the traditional Balanced Scorecard perspectives; and (2) standalone environmental data as an additional fifth perspective along with the traditional Balanced Scorecard architecture. The traditional Balanced Scorecard without any information on environmental perspective is included in the experiment as the control condition. The findings indicate that the combined effect of eco-efficiency knowledge and Sustainability Balanced Scorecard knowledge has a significant positive influence on the relationship between the Balanced Scorecard type versus Sustainability Balanced Scorecard type and environmental investment decision-making.

1. Introduction

Environmental decision-makers are struggling mainly with social and political issues, which have arisen due to the views held on how to properly conduct investment decision-making and what the outcomes should be [1]. A broad consensus has been established that the Sustainability Balanced Scorecard (SBSC) is one of the most effective tools in evaluating potential investments and initiatives by better integration of the environmental, social and economic aspects of corporate sustainability measurement and management [2,3]. The SBSC evolved from the traditional Balanced Scorecard (BSC). SBSC types are generally organized in one of two ways: (a) sustainability data embedded within the four perspectives scorecard; or (b) adding the sustainability perspective as an additional fifth perspective to the scorecard [2].

Scholarly debate about SBSC types focuses on whether additional performance perspectives should be used to address sustainability objectives or whether sustainability issues should be integrated into the existing performance perspectives [4,5]. Corporate sustainability is increasingly becoming a knowledge-based practice to improve the quality of sustainable development and environmental investment decision-making [6]. The SBSC was developed to support the corporate sustainability effort, although there still exists a lack of clarity on what aspects constitute the SBSC and how to best achieve it [7].

The incremental SBSC improvement has added new environmental data which requires knowledge to transfer the data to the valuable information that could reduce resource intensity and minimize the environmental impact of production; together with value creation. In this regard, eco-efficiency is an improved measure of sustainability because it links environmental impacts directly with some kind of economic performance [8] and it works as a valuable tool towards evaluating investment opportunities [9,10].

However, inadequate knowledge regarding eco-efficiency processes such as a lack of knowledge regarding the selection and composition of appropriate environmental data granularities and regarding the model quality to improve investment decision-making [11] negatively influence the evaluation of sustainability goals and their achievement [10]. The two types of knowledge established as being important for environmental decision-making are eco-efficiency knowledge and SBSC knowledge [9,12]. Eco-efficiency knowledge means the knowledge of all the processes related to the product lifecycle to properly prioritize a list of likely interventions of efficient sources and to make better environmental investment decisions to achieve a higher level of sustainability [13]. Furthermore, this knowledge is also related to what people know and are concerned about regarding the natural environment, their responsibilities towards environmental protection and the relationship between the economy and sustainable development [14]. With eco-efficiency knowledge, decision-makers are expected to process data (SBSC indicators), know what can be done about the environmental problems (action-related knowledge), and understand the benefits and effectiveness of environmentally responsible actions [15] in enhancing environmental investment decision-making.

Hence, knowledge of eco-efficiency indicators may guide managers to design products using fewer environmentally harmful or resource-depleting raw materials which could significantly reduce direct manufacturing costs and increase inventory savings [9]. Therefore, a better understanding of the efficient use of environmental data will guide the appropriate use of SBSC measures to enhance environmental investment decision-making [7].

For SBSC type knowledge, the lack of such knowledge is said to cause insufficient use of the SBSC measurements [16]. SBSC proponents have also found that managers’ knowledge deficiency regarding the unique measures (leading indicators) and common measures (lagging indicators) will confound their decision- making [4,17]. As such, insufficient understanding of the SBSC metrics can negatively affect decision-making. The level of knowledge and understanding of the SBSC metrics is likely to influence how evaluators use common and unique measures to evaluate the performance [18].

Accordingly, weighting SBSC measures equally leads to SBSC disruption [19]. Dilla and Steinbart [20] argued that each measure must be properly understood to achieve the targets of a firm, as each business unit must acquire knowledge and receive training on the scorecard measures. In this context, it is likely that the lack of knowledge on SBSC measures may pose obstacles for the effective decision-making of managers, consequently seriously limiting their view of business performance. An example of this is when supervisors evaluate the performance of managers using the SBSC based only on common measures across different units and not on the measures that were unique to particular business unit [17,21]. Extant literature on SBSC and eco-efficiency has highlighted that knowledge about sustainable development may enhance environmental investment decision-making [7,22]. However, there is a lack of literature that examines the impact of the mediating role of eco-efficiency knowledge and SBSC knowledge on the relationship between SBSC types and environmental investment decision-making, signifying that this aspect may have been overlooked.

This study aims to examine the serial mediation effect of eco-efficiency knowledge and SBSC knowledge on the relationship between SBSC type and environmental investment decision-making. With this aim in mind, this study employs the experimental method by building on work done by Alewine and Stone [2], with the target experimental method being a between-subjects study (3 × 1). This study contributes to the SBSC type and environmental investment literature by providing insights into how eco-efficiency knowledge and SBSC knowledge contribute to achieving a firm’s environmental objectives.

2. Literature Review and Development of Hypotheses

In building the proposed framework, four interlaced bodies of literature were reviewed: SBSC type and environmental investment decision-making; SBSC type and eco-efficiency knowledge; SBSC type and SBSC knowledge; and eco-efficiency knowledge and SBSC knowledge.

2.1. Sustainability Balanced Scorecard (SBSC) Types and Environmental Investment Decision-Making

Scholars have developed extended scorecard architectures under the name of SBSC [23], possibly for two reasons: (1) to allow management to address goals in all three dimensions of sustainability by integrating economic, environmental, and social aspects; and (2) the SBSC integrates these three dimensions in a single integrated management system instead of a parallel system. Based on these considerations, the SBSC differs from the balanced scorecard (BSC) explicitly by recognizing sustainability-related objectives and performance measures and it is an appropriate tool for integrating strategically relevant environmental, social, and ethical goals [24]. The SBSC measures an organization’s performance from four or five perspectives, which are: financial, customer, internal business process, learning and growth, and environmental perspectives [25].

Past scholarly works [26,27] have explored the relationship between the SBSC and decision outcomes when analyzing environmental data. Epstein and Wisner demonstrated that integrating social and environmental metrics into the scorecard outcomes group of benefits mainly helps managers improve corporate decision-making and accountability by including both leading and lagging measures of performance, as well as guiding senior managers to reposition their organizations towards improved corporate responsibility [24]. Alewine and Miller [4] assert that the SBSC metrics have a significant influence on the willingness of managers to incorporate environmental considerations into investment decision-making. Kaplan and Wisner examined the effective use of environmental data. Thus, they used experimental methods where the data manipulation included a four-perspective scorecard in which environmental data were embedded within the traditional four-perspective and a five-perspective scorecard in which the stand-alone fifth perspective was isolated and grouped along with environmental data, so that the latter might lead to a less weighted decision compared to spreading the data throughout the traditional perspectives. Their findings provide a guideline for managers on the more effective SBSC architecture in which the environmental data was embedded within the traditional perspectives [5].

Meanwhile, Alewine reviewed and synthesized the environmental accounting literature and concluded that the experimental designs can help explicate the behavioral and cognitive processes that underlie the effects of information displays on the successful and unsuccessful use of environmental accounting information. Therefore, he confirmed that the data quality must be considered carefully when constructing SBSCs. This was because it influences the evaluation effectiveness of environmental decision-making [26]. This issue requires the awareness of the decision-makers that provide contexts to the attribute being analyzed. The reason behind this is because analysing attributes that lack this knowledge may lead to inaccurate assessments, improper weighting of the attributes, and, consequently, inaccurate evaluations and decisions.

Jiangtao and Pin for one, sought to determine how the SBSC aids in evaluation and investment decisions. They carried out an experiment to examine whether the environmental data integrated into the BSC would change investment decisions, whether the presentation of the environmental data would affect investment decisions, and why these factors produce different outcomes. The results indicated that participants chose the more environment-friendly investment option when the environmental data were added as a fifth perspective [3]. Likewise, Alewine and Stone investigated the most influential SBSC type that would impact investment decision-making and found in their experimental study that investments undertaken in achieving environmental stewardship objectives were better with the SBSC four perspectives whereby participants spent less time on them [2].

The studies discussed above are examples of an ongoing debate among scholars on which type of SBSC architecture is the most effective when it comes to implementing management strategies for achieving financial and environmental objectives [28]. However, these studies did not highlight the role of environmental-related knowledge in the relationship between SBSCs and environmental investment decision-making. Therefore, this study focuses on the influence of knowledge on the SBSC type in terms of achieving environmental objectives.

2.1.1. The Role of Knowledge in the Relationship between Data and Decision-Making

Due to the fast-changing environment of today, businesses need strategies to examine whether all the relevant information is available to the people who need them to make effective and more informed decisions. Data alone does not lead to effective decision-making, as it has no inherent association with the possible consequences of an action beyond its existing form. Information is defined as data processed into a form that has meaning to the user and is of real or perceived value to current or prospective actions or decisions [29].

Sarker and Burritt conducted an experimental research in the Australian offshore petroleum industry to examine the effect of environmental accounting information on environmental investment decision-making. Their results indicated that environmental accounting information has a more significant influence on the willingness of managers to incorporate environmental considerations into investment decisions [1].

The link between the information received by managers and the decisions taken by them is influenced by the knowledge possessed by these managers [13]. Information without adequate knowledge to synthesize the information into actionable plans will not translate into efficient and effective decision-making [30]. Modern day tools and techniques used in managerial processes need to be well understood by decision-makers to achieve their intended goals [4]. In fact, knowledge based on expertise in the domain of the problem significantly affects how that information is processed for better decision-making [31]. Therefore, successful organizations invest a sizeable amount of their resources on the training and capacity building of their managers and employees. However, decision making is the least developed process in the companies mostly because of the lack of awareness and importance of explicit knowledge [10].

The lack of knowledge in implementing sustainability strategies can affect the outcomes of environmental programs [32]. Thus, in this study, two types of knowledge that are important in implementing sustainable strategy are examined. These two types of knowledge—eco-efficiency knowledge and SBSC knowledge—may explain the relationship between the SBSC type and better environmental investment decision-making. The next part of this study highlights the influences of these knowledge types and how they will possibly mediate the relationship between the SBSC type and environmental investment decision-making.

2.1.2. The Mediating Role of Eco-Efficiency Knowledge

Eco-efficiency has become a consistent tool towards the transition to sustainable development. The efforts of eco-efficiency indicators have been used for comparative studies and decision-making, providing better financial, environmental, and social performance [8,9]. However, Ehrenfeld asserted, “if eco-efficiency is to become a useful indicator for determining choice, it must be coupled with other indicators and tools” [33]. In this regard, various works [34,35,36] have highlighted a possible link between the SBSC and eco-efficiency to influence decision-makers.

Möller and Schaltegger discussed the relationship between the SBSC and eco-efficiency analysis. They found that eco-efficiency is an instrument for estimating and controlling the appropriate key performance indicators for two major aspects of sustainability; namely, environmental and economic issues. Eco-efficiency analysis can be considered a bridge between the SBSC and environmental management information systems, particularly those systems that rely on material and energy flow analysis and life-cycle assessment approaches [35].

Ranđelović and Stevanović found that SBSCs are able to incorporate eco-efficiency by reducing resource intensity, minimizing the environmental impact of production, and facilitating continuous incremental improvement. They identified two approaches to integrate eco-efficiency into the SBSC framework. The first is through the financial and non-financial variables in the SBSC. Items such as specialized knowledge or quality of the process could be incorporated in the SBSC. The second is including indirect economic outcomes of eco-efficiency. They found that eco-efficiency analysis can play an important role in the selection of investment projects for sustainable development [37].

Moreover, literature has proposed a mathematical model to improve eco-efficiency that seeks to support environmental decision-making and help managers to make trade-offs between green and lean management practices which contribute to the reduction if the environmental negative impact of companies and improvement of their economic performance [12]. Thus, eco-efficiency is considered the goal of managerial decision-making in an environmental context because it reconciles the use of capital and the efficient use of environmental resources. Figge and Hahn found that managers need knowledge to expand the role of environmental efficiency considerations in business decision-making, which can create sustainability value [38].

Lozano and Lozano highlighted that eco-efficiency could be used as a decision-making tool to choose between transformation processes by combining the scientific and technical issues with the economic ones. For instance, eco-efficiency analyses have been applied to compare two alternative routes to convert residual biomass into energy or chemicals. For example, to reduce the energy consumption and emissions at the industry level, it is important to better understand the factors that influence these indicators in the various industrial sectors [39]. To perform these analyses, sometimes detailed data and the application of models or methods are necessary to generate reliable and consistent information to support making effective environmental investment decisions. Many industries are global, so local analyses need to be complemented with an overall analysis of the global trends within each specific industry [40]. Uhlman and Saling found that eco-efficiency analyses harmonize two of the three pillars that a company must measure to manage and quantify sustainability. It can make strategic decision-making along the entire value chain easier and it helps to produce innovative sustainable products [36].

Based on several works of literature [9], it can be inferred that eco-efficiency indicators help firms to monitor the level of achievement of environmental objectives at a glance. These indicators generate feedback regarding the differences between environmental and economic aspects and help focus attention on areas that require improvement. Hence, they provide the knowledge and learning necessary to support effective environmental investment decision-making.

Furthermore, knowledge of eco-efficiency helps decision makers achieve quality environmental investment decision-making [41]. In fact, eco-efficiency knowledge improves weak sustainability performance, which should be understood in consideration for better environmental investment decision-making [6]. There is a lack of studies that examine the impact of eco-efficiency knowledge on environmental investment decision-making [10]. There appears to be no specific literature with a comprehensive study of the mediating effect of eco-efficiency knowledge on the relationship between scorecard types and environmental investment decision-making whilst emphasizing sustainability aspects.

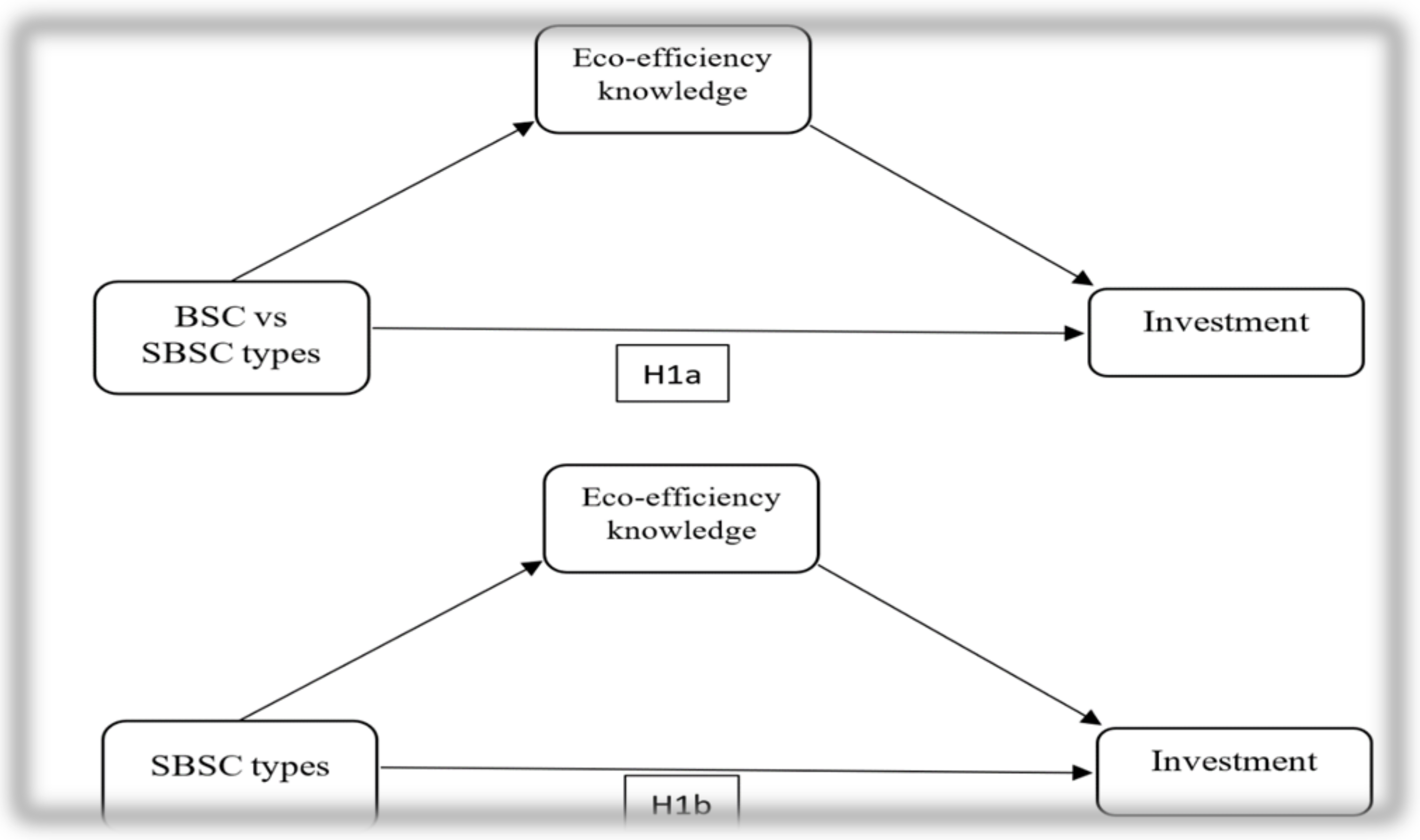

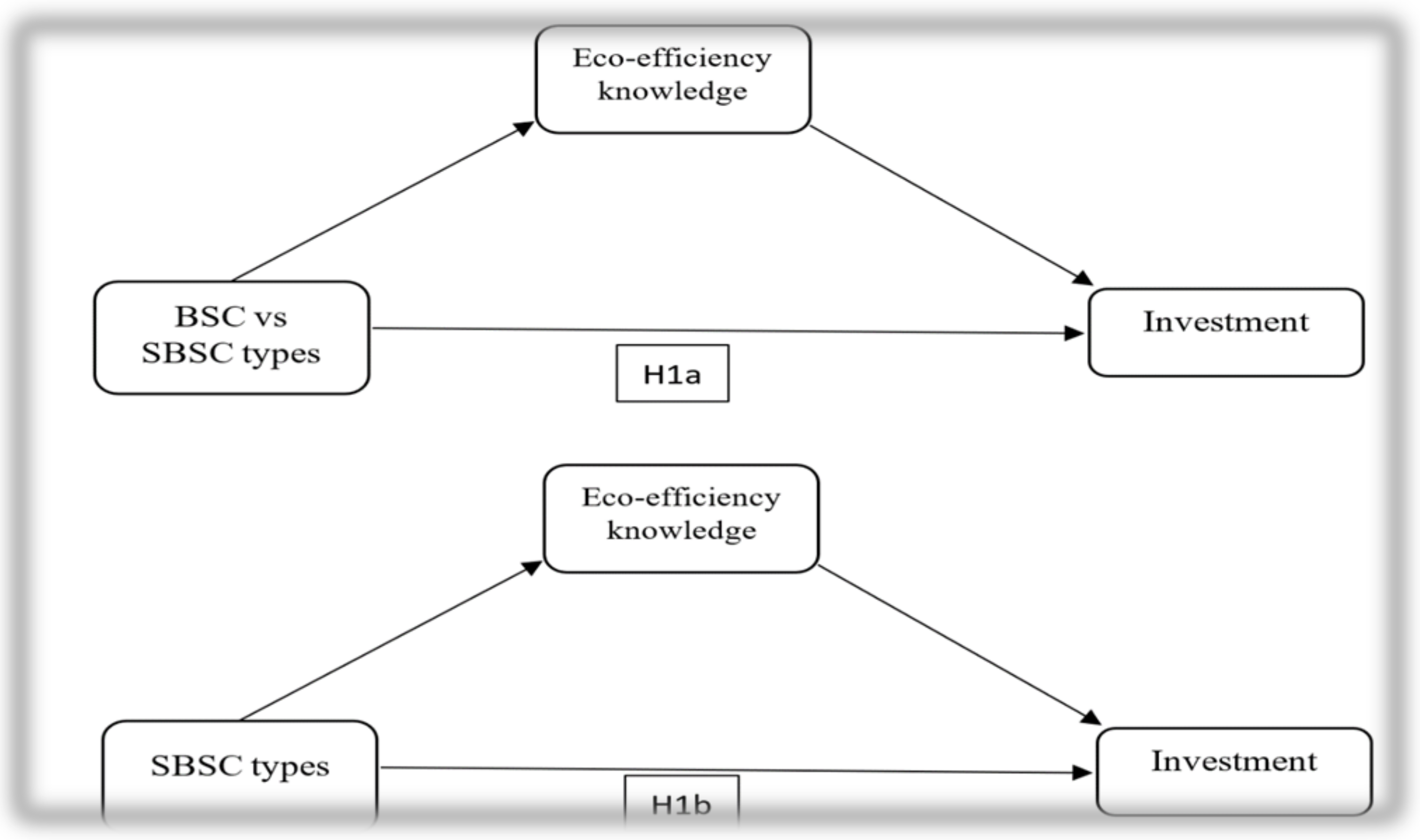

Thus, this is where the current study attempts to fill those gaps by introducing eco-efficiency knowledge as a bridge to explain the different impacts of changing the BSC type to the SBSC type on investment decision-making whilst prioritizing environmental aspects. This is because eco-efficiency interacts with the SBSC through the sustainability perspective. Therefore, it is hypothesized (Figure 1. Hypothesis 1) that:

H1a:

SBSC has a greater effect on the environmental investment decision-making when eco-efficiency knowledge is introduced.

Understanding the impact of the SBSC with four perspectives and the SBSC with five perspectives on environmental investment decision-making requires the introduction of specific knowledge regarding environmental information. This is because this knowledge helps distinguish between the influence of embedded and stand-alone environmental data on investment decision-making and on how environmental accounting information gets processed to help ensure that the data are used as intended in a decision setting [26].

However, the literature seems to have overlooked the examination of the mediating role of eco-efficiency knowledge on the relationship between the SBSC types and environmental investment decision-making. Therefore, the following hypotheses are posited (Figure 1. Hypothesis 1):

H1b:

Eco-efficiency knowledge mediates the relationship between the SBSC types (four-perspective versus five-perspective) on environmental investment decision-making.

2.1.3. The Mediating Role of SBSC Knowledge

An essential aspect of the SBSC is that it offers management with a holistic framework that translates a firm’s strategy into a coherent set of performance measures. It links performance measures with organizations’ strategic objectives [42]. SBSCs translate strategic objectives into actionable measures to help organizations improve their performance. Thus, the employees’ understanding of SBSCs is critical to facilitate the development and implementation process of SBSCs [43]. The better the employees understanding of the firm’s strategy, the better they will be able to use strategically linked performance measures to guide their decisions and actions [42].

Several studies [20,44] have observed how different aspects of SBSC knowledge could improve organizational performance. Wu and Haasis asserted that knowledge is an enabler for the appropriate application of SBSCs. They examined the embedded knowledge with the four consecutive perspectives of SBSCs (learning, processes, stakeholders, and sustainability) [7]. Furthermore, they investigated how knowledge of SBSC metrics that resided in the environment, people, processes, and stakeholder relationships made contributions to create value from top to the lower management and enhance the decision-making quality to achieve environmental objectives.

Literature found that different ways of presenting information can lead to differences in the organization of knowledge. Thus, SBSC knowledge is essential to make the use of SBSC seamlessly and effectively. Their findings showed that the knowledge of SBSC measures had the most impact on facilitating successful decision-making [16]. Consistent with recent studies, they have experimentally explored how the SBSC format and reputation from the environmental performance come together to influence performance evaluations. They found that a better understanding of how environmental reputation and SBSC format interacted impacted decisions [4]. A lack of the SBSC measurements usage knowledge may lead to inappropriate decision-making due to the fact that when organizations aim to achieve environmental objectives by using SBSC, they must possess the knowledge on how to organize environmental measures within the scorecard and how to analyze the sustainability information [28].

Another important aspect of SBSC knowledge is the common (the same across business units) and unique measures (differing across business units) that are used to evaluate organizational performance. Managers with limited knowledge in using SBSC types based their performance evaluations on common measures across units and ignored any unique strategy measures of each unit [17,21]. Dilla and Steinbart found that after participants had training and experience in designing SBSCs, those who were knowledgeable about the SBSC emphasized both common and unique measures [20]. Kang and Fredin evaluated the performance of two managers under either feedback or non-feedback conditions and found that when evaluators were given task property feedback—a form of cognitive feedback—they tended to use more unique measures than if they were not given any feedback information. This feedback led to better decision-making [44]. Thereby, this study asserts that sufficient knowledge of SBSC measurements has a rigid effect on performance evaluation.

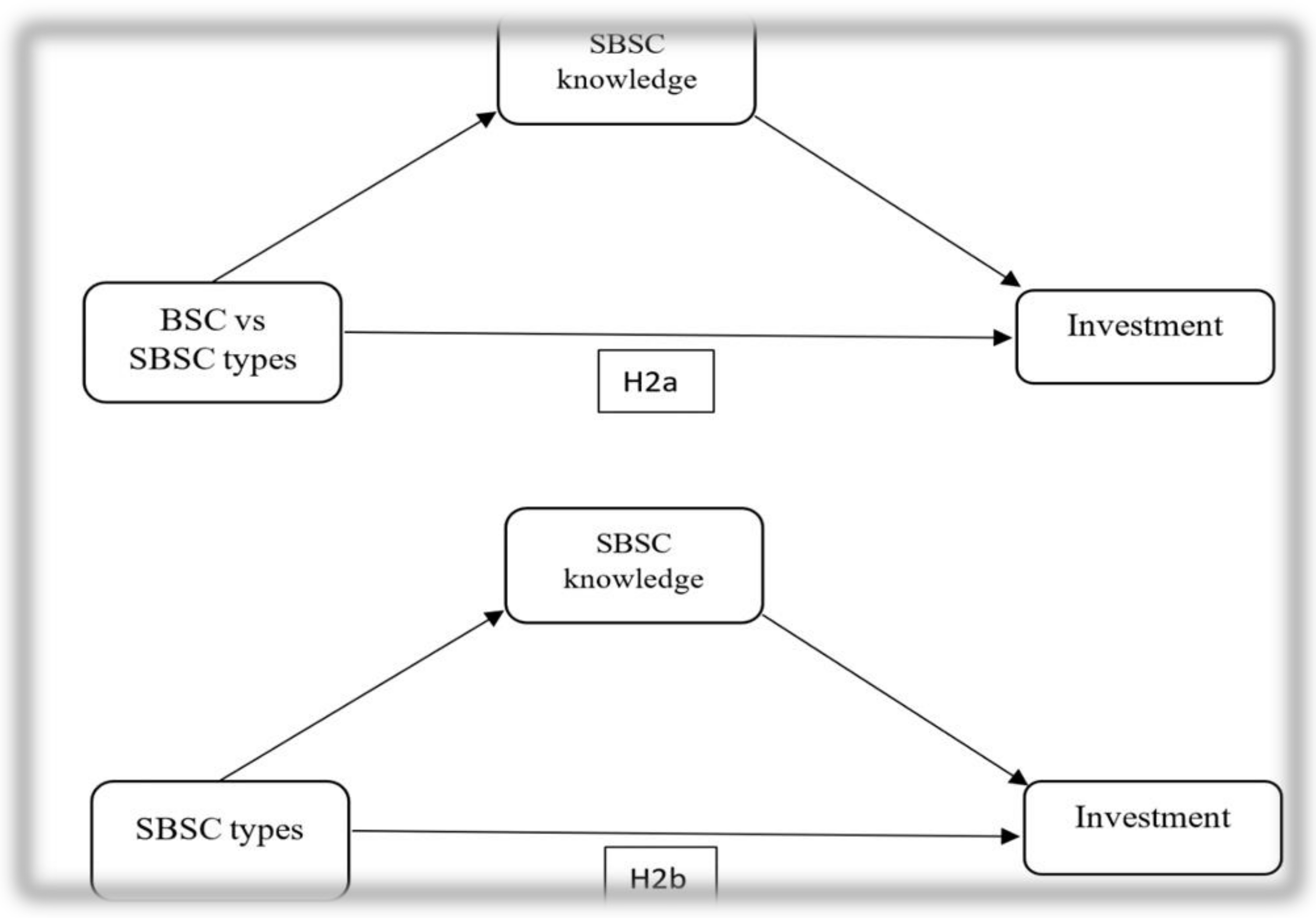

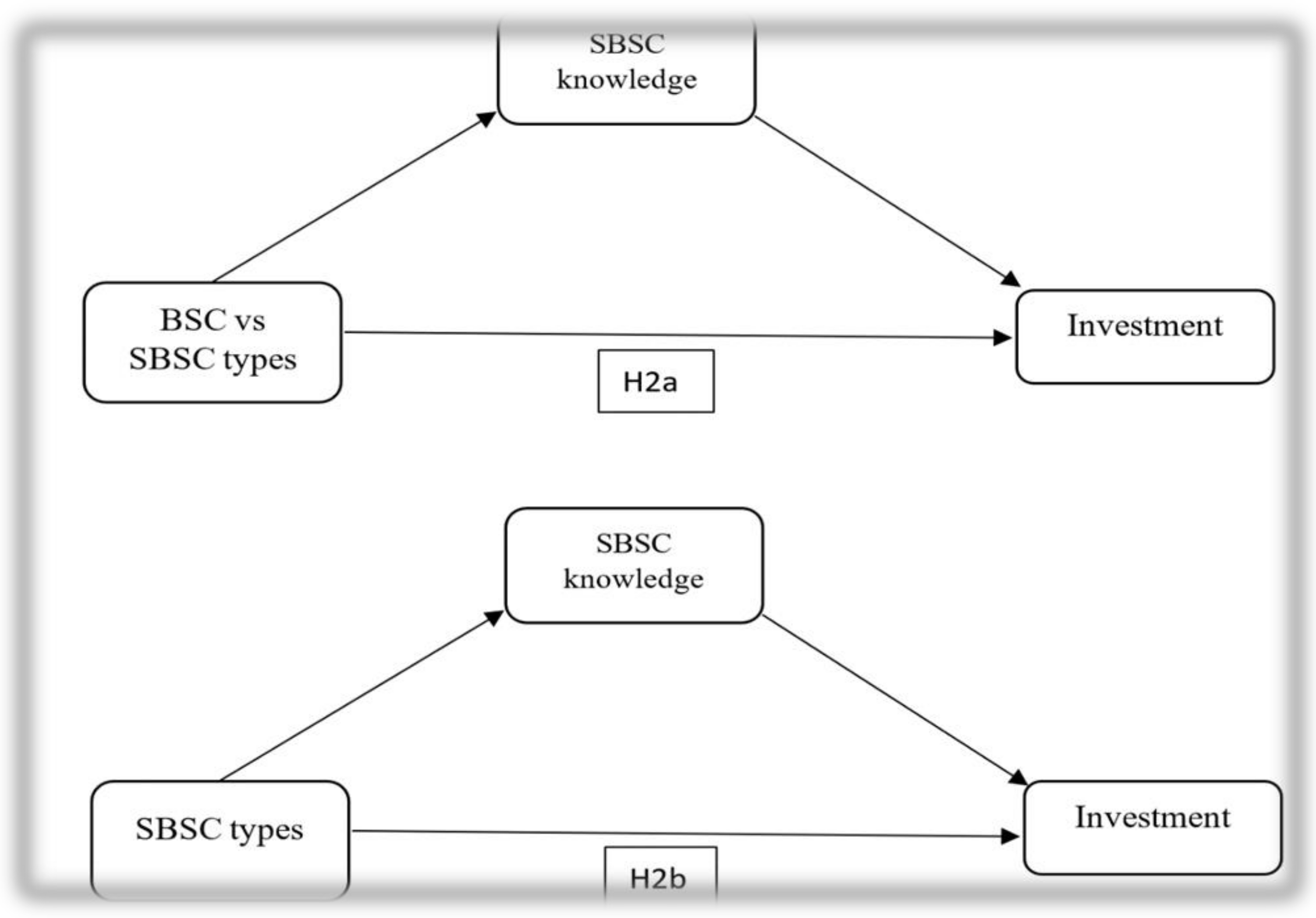

SBSC knowledge helps provide insights into how and when parts of scorecard data should effectively be integrated into decision-making. This includes environmental investment decisions. Therefore, managers who do not possess sufficient SBSC knowledge may make poor investment decisions. Based on this literature, this study hypothesizes that SBSC knowledge will increase awareness of the SBSC type measures that will lead to better environmental investment decision-making [19]. Moreover, SBSC knowledge can reduce the confusion between SBSC types, since increasing the quantity of information in a five-perspective SBSC may increase the chance of an information overload more than the information in a four-perspective SBSC [2]. The following hypotheses are proposed as represented in Figure 2. Hypothesis 2).

H2a:

SBSC knowledge mediates the relationship between the BSC versus SBSC and environmental investment decision-making to achieve environmental objectives.

H2b:

SBSC knowledge mediates the relationship between the SBSC type (four-perspective versus five-perspective) and investment decision-making to achieve environmental objectives.

2.1.4. The Serial Mediating Role of Eco-Efficiency Knowledge and SBSC Knowledge

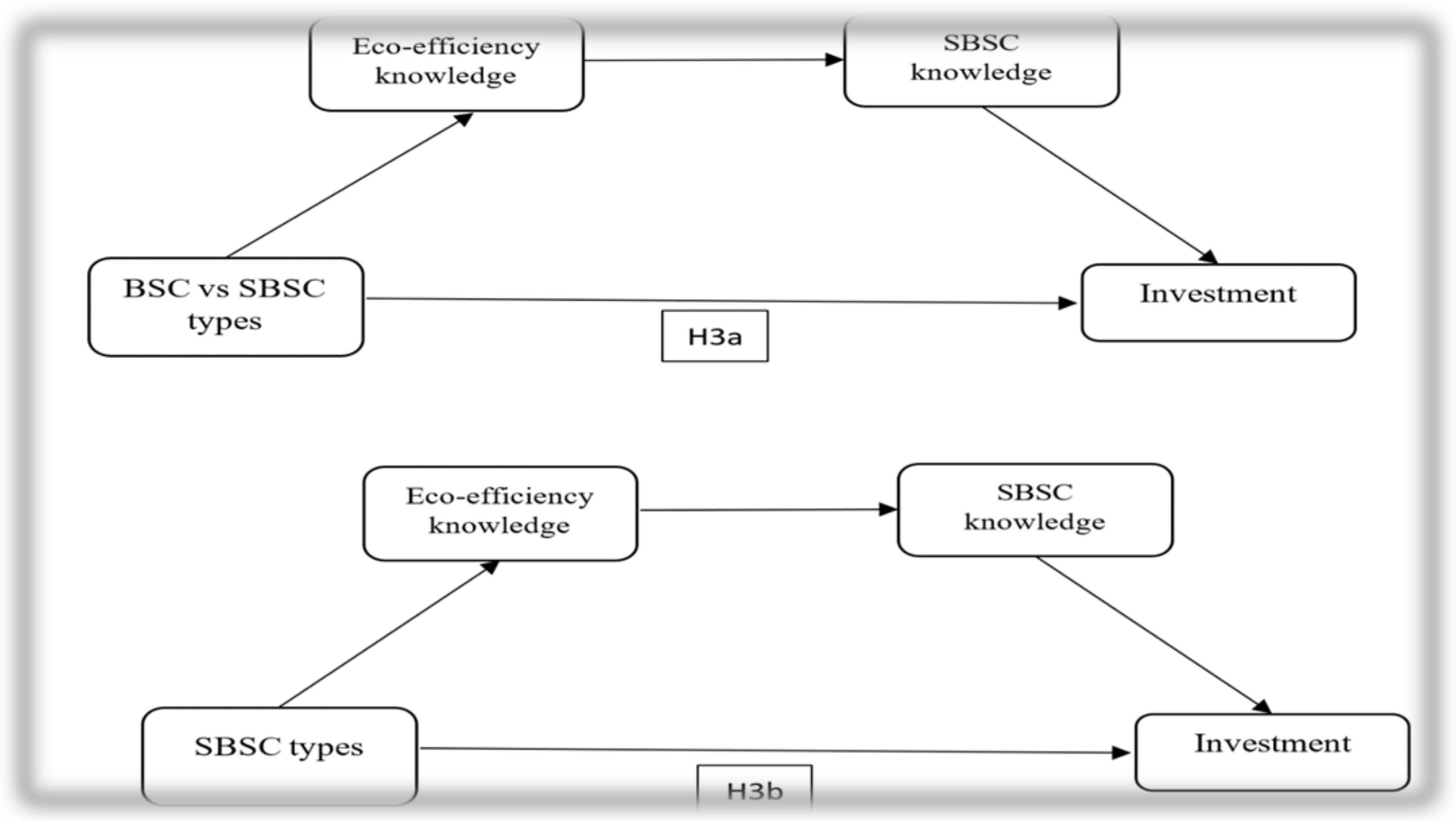

The previous sections discussed the idea that eco-efficiency knowledge and SBSC knowledge could individually mediate the relationship between the SBSC type and environmental investment decision-making that aims to achieve environmental objectives. However, it is unclear whether eco-efficiency knowledge could subsequently influence SBSC knowledge and whether these variables could function together as mediators to increase the influence of the SBSC type on environmental investment decision-making. The following literature suggests that eco-efficiency knowledge may have an effect on the SBSC knowledge.

Ullah and others found that integrating both economic and environmental information may help increase SBSC knowledge [45]. Figge and Hahn investigated a causal relationship between the economic value creation and environmental impact that influenced sustainable value creation [38]. Alewine also stated that a better understanding on the part of the decision-maker of the processing of non-environmental information would be conducive to environmental investment decision-making [26]. Therefore, eco-efficiency knowledge can be considered a bridge between the SBSC type and SBSC knowledge.

Consequently, based on the knowledge-based information (KBI) [30], the current study proposes that eco-efficiency knowledge provides information to assess and control the SBSC type measures by interpreting efficiency in each measure. This type of information strengthens environmental awareness and improves the SBSC measurements usage for better investment decisions that emphasize environmental objectives. This knowledge could also have an effect on the BSC versus SBSC and the investment decision-making that emphasizes environmental objectives. The reason behind this could be due to the fact that organizations can use the SBSC for eco-efficiency knowledge to link between the conventional BSC and corporate environmental accounting systems [35]. Hence, the effect of the eco-efficiency effectiveness may be clearly observed due to the absence of the traditional BSC. Thus, this study proposes the following hypotheses represented in Figure 3. Hypothesis 3).

H3a:

BSC versus SBSC leads to better investment decisions that achieve environmental objectives through increased eco-efficiency knowledge, which consequently leads to increased SBSC knowledge.

H3b:

The SBSC type (four-perspective versus five-perspective) has an effect on the investment decisions that achieve environmental objectives through increased eco-efficiency knowledge, which consequently leads to increased SBSC knowledge.

3. Methods

This study deploys experimental research design building upon the work of [2]. A between-subjects experimental study was used to investigate whether eco-efficiency knowledge and SBSC knowledge affected the direct relationship between BSC architectures (traditional four-perspective BSC, four-perspective SBSC, or five-perspective SBSC) and environmental investment decision-making. The procedure and instruments used in this study were adapted from [2]. The experimental manipulation was conducted based on the two different SBSC types mentioned earlier. The traditional BSC architecture represented a control group with four perspectives, which were: financial, customer, internal business, and learning growth. For the SBSC type, there was a four-perspective SBSC and a five-perspective SBSC architecture. The former had environmental data embedded into the traditional four perspectives, while the latter contained the traditional four perspectives and environmental concerns as a stand-alone fifth perspective. The participants were randomly assigned to one of the three experimental conditions. In this study, the participants applied four metrics for each perspective, derived from [17,46,47].

In total, 71 postgraduate students participated. This number of participants was precisely chosen according to suggestions by Hair and others who stated that the most acceptable way of determination in an experimental research is with a 10:1 ratio (10 samples for one variable) [46]. Of those, 60 participants (80%) completed the instrument. The remaining participants, with incomplete answers, were discarded. The number of female students (55%) exceeded that of male students (45%). The participants were mostly between the ages 20 and 34 (62%). The mean work experience of the participants was 2.5 years, while most (65%) of the participants had more than three years of experience.

First, the participants were randomly assigned to one of the three conditions. Next, they were required to complete a demographic section which requested the following information: years of work experience, age, gender, tertiary education, and any past accounting courses taken at a tertiary level. The participants were also required to provide an e-mail address and were given a raffle ticket to participate in a draw. Five winners from the draw were awarded prizes. Next, the participants were given a summary of how the eco-efficiency concept is linked to an organization’s strategic objectives and tested on their understanding of this information. They were also given a summary of how the SBSC concept is linked to an organization’s strategic objectives (environmental information was not introduced at this stage) and tested on their understanding of this information. Both of the tests conducted above are further explained in Section 3.1.

Then, the participants were required to assume the role of the manager for a hypothetical organization—Company ABC. As managers, they had to decide how to allocate $20 million to two proposed investment projects (Investments A and B). The amount of money invested in each project had to be aligned with the company’s two strategic objectives: financial success and environmental stewardship. Additionally, the participants were given the SBSC instrument which contained four or five perspectives (depending on the randomized condition presented to them). Each perspective contained four measurement metrics. Table 1 presents these perspectives and their measurement metrics.

Under each metric (presented side by side), the company’s goals for each metric and projected metric values for Investments A and B were included. The projected metric values for the two investment projects differed. One investment showed projected metric values that would achieve better financial goals, and the other showed values that would better achieve environmental goals. Specifically, one investment project would achieve three of the four metrics in the financial perspective, whereas the other project would only achieve one of the four financial metrics. For the environmental metrics in the SBSC conditions, the investment project that was better at achieving financial metrics would only achieve one of the four environmental metrics, whereas the investment project that was worse at achieving financial metrics would achieve three of the four environmental metrics. For the projected metric values in the customer, internal business, and learning growth perspectives, both investments were equally attractive and were projected to not influence the participants’ evaluation of the two investments. This case was designed to create a tension between the two strategic objectives (financial success and environmental stewardship) of a hypothetical Company ABC [2]. The instrument for this study took approximately 10–20 min to complete.

3.1. Measurement of Variables

BSC and SBSC type. There were three sets of conditions (20 respondents in each condition): a four-perspective BSC, a four-perspective SBSC, and a five-perspective SBSC. The perspectives in the four-perspective BSC were financial, customer, internal business, and learning and growth, with no environmental perspective. The four-perspective SBSC condition embedded the environmental perspectives within the traditional four-perspective scorecard. The five-perspective SBSC had the traditional four-perspective scorecard and the environmental perspective as a stand-alone fifth perspective. The measures for the SBSC type was based on Alewine and Stone [2]. Their measurement was based on various scorecard research such as [17,47,48]. Based on the sequence in [2], a value of one was given to the four-perspective BSC conditions, a value of two to the four-perspective SBSC conditions, and a value of three to the five-perspective SBSC conditions.

Eco-efficiency knowledge. The participants were given a summary of how the eco-efficiency concept is linked to an organization’s strategic objectives. Then, they were tested on this understanding. Eco-efficiency was measured using six true/false questions that had been adopted from literature [41]. The participants were given a value of zero for incorrect answers and a value of one for correct answers. Two questions were dropped because of low inter-item correlation.

SBSC knowledge. The participants were given a summary of how the SBSC concept is linked to an organization’s strategic objectives. Then, they were tested on this understanding. The SBSC knowledge was measured using four true/false questions that had been adopted from Alewine and Stone [2]. The participants were given a value of zero for incorrect answers and a value of one for correct answers.

Environmental Investment Decision-making. To measure investment decision-making, the participants were asked to indicate amounts between $0 and $20 million for the two investment projects: Investments A and B. For the four-perspective scorecard conditions, Investment B was seen as the superior financial alternative to Investment A, whereas in the four-perspective and five-perspective SBSC conditions, Investment A was seen as the superior environmental alternative.

3.2. Testing Serial Mediators

The model with two serial mediators was tested using Hayes’ PROCESS macro [49]. PROCESS is a computational tool for SPSS that can be used for mediation analyses. It utilizes an ordinary least squares logistic regression-based analytical framework to estimate the direct and indirect effects in mediator models. Additionally, the macro applies bootstrap methods of 5000 samples to estimate the bias-corrected bootstrap confidence intervals and makes inferences about the indirect effects in mediation models. As the PROCESS macro provides a formal test of indirect effects, it is suited for the serial multiple mediation model deployed in this study.

4. Research Results

Manipulation check questions related to perspectives were included in the scorecard. Twenty-two participants did not identify the number of perspectives correctly on the scorecard. The same results were obtained after excluding those participants who failed this manipulation check question.

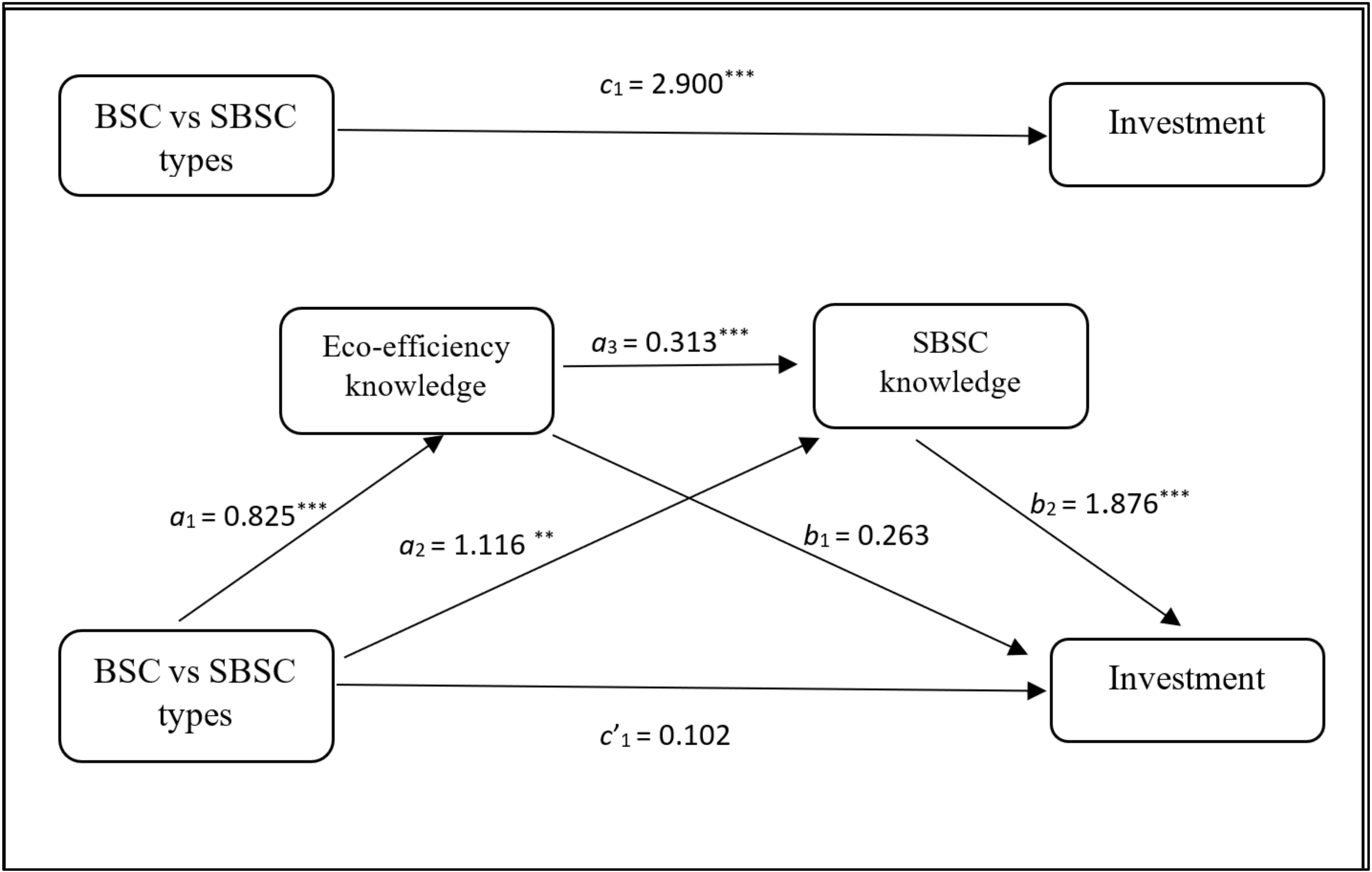

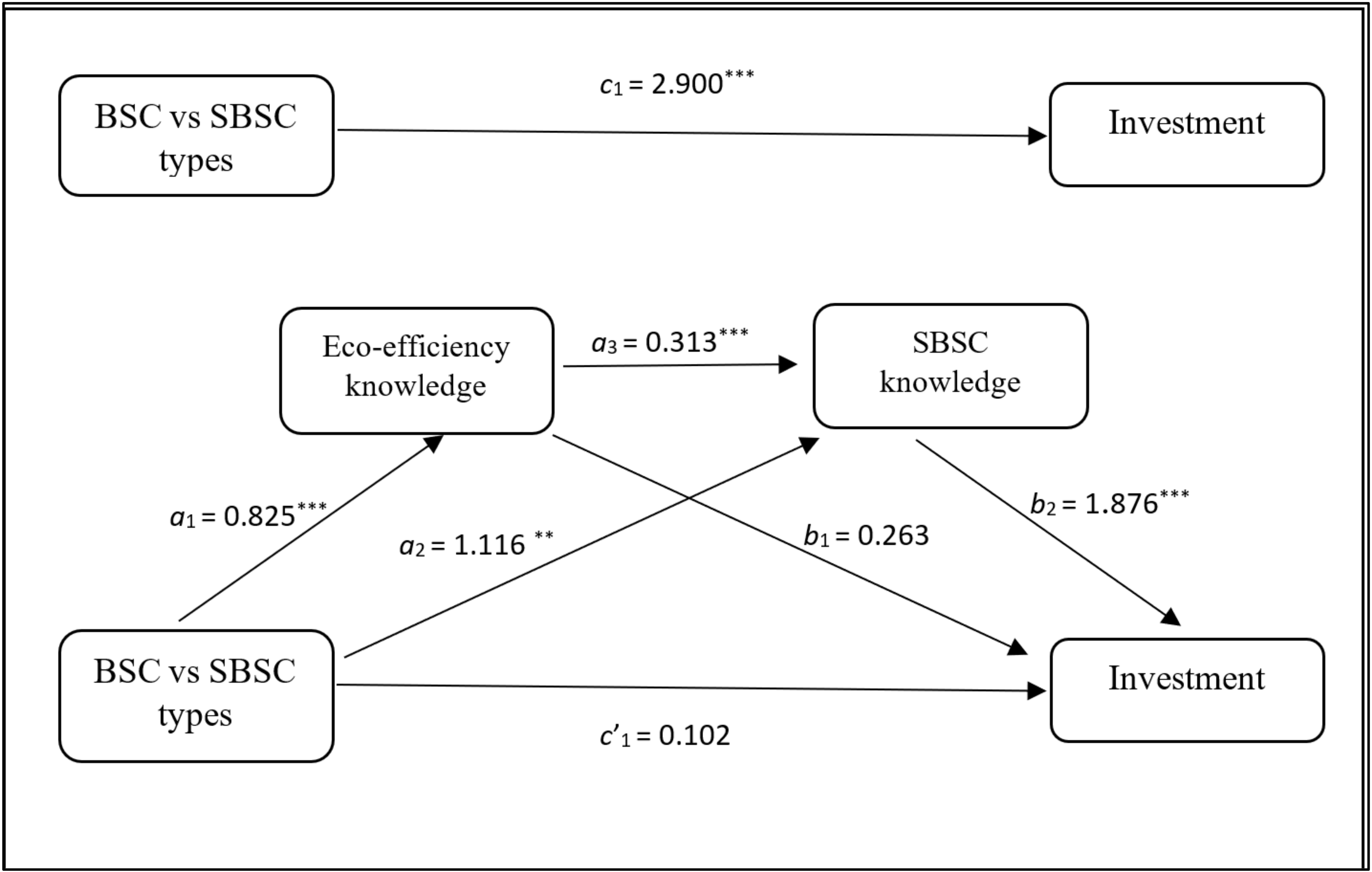

To test the effect of the SBSC types on environmental investment decision-making, serial multiple mediation analyses were run. Figure 4 and Figure 5 represent the tested serial multiple mediation model for the BSC versus SBSC and the SBSC type (four-perspective versus five-perspective), respectively. The c-path in the model includes the direct effect of the BSC versus SBSC on environmental investment decision-making, independent of the effect of the mediators (c1) and the total effect of the BSC versus SBSC on environmental investment decision-making that attempts to achieve environmental objectives (c), which is the sum of the direct effect and the indirect effect via the mediators [49].

The total effect remains c1 = 2.900 (p < 0.001), as it is not influenced by the variables that are proposed as intervening between the BSC versus SBSC (BSC: n = 20, mean = 9.050, SD = 2.742) (SBSC: n = 40, mean = 11.950, SD = 3.281) and investment decisions that achieve environmental objectives. The direct effect of c′1 = 0.102 is not statistically significant (p = 0.941). One specific indirect effect is not significant, however, there are two specific indirect effects that are significant, as evidenced by the bootstrap confidence intervals that do not contain zero. The first indirect effect, H1a, is not significant. It carries the effect of the BSC versus SBSC through eco-efficiency knowledge only, bypassing SBSC knowledge. This indirect effect is the product of a1 = 0.825 and b1 = 0.263, with a 95% bootstrap confidence interval of −0.457–1.396. Eco-efficiency knowledge did not have any effect on the BSC versus SBSC and this did not result in better environmental investment decision-making, independent of SBSC knowledge. Therefore, H1a is not supported.

The next indirect effect, H2a, flows from the BSC versus SBSC directly to the SBSC knowledge and then to investment decisions that achieve environmental objectives, bypassing eco-efficiency knowledge, and is defined as the product of a2 = 1.116 and b2 = 1.876, with a 95% bootstrap confidence interval of 0.328–4.439. Therefore, for those who were given SBSCs with the environmental aspects and who had more SBSC knowledge (1.116 units more) than those who were not given SBSCs, this increased the SBSC knowledge associated with better investment decisions that achieved environmental objectives, independent of eco-efficiency knowledge. Hence, H2a is supported.

The last indirect effect of the BSC versus SBSC passes through both the eco-efficiency knowledge and the SBSC knowledge, which is H3a. It is estimated as the product of a1, a3 = 0.313, and b2, with a 95% bootstrap confidence interval of 0.020–1.953. Greater eco-efficiency knowledge resulting from the BSC versus SBSC translated into an increased SBSC knowledge, which in turn led to better investment decisions that achieved environmental objectives. Hence, H3a is supported. Thus, the evidence is consistent with the claim that eco-efficiency and SBSC knowledge influences the relationship between the BSC versus SBSC and investment decisions that achieve environmental objectives, indirectly through two of the three pathways.

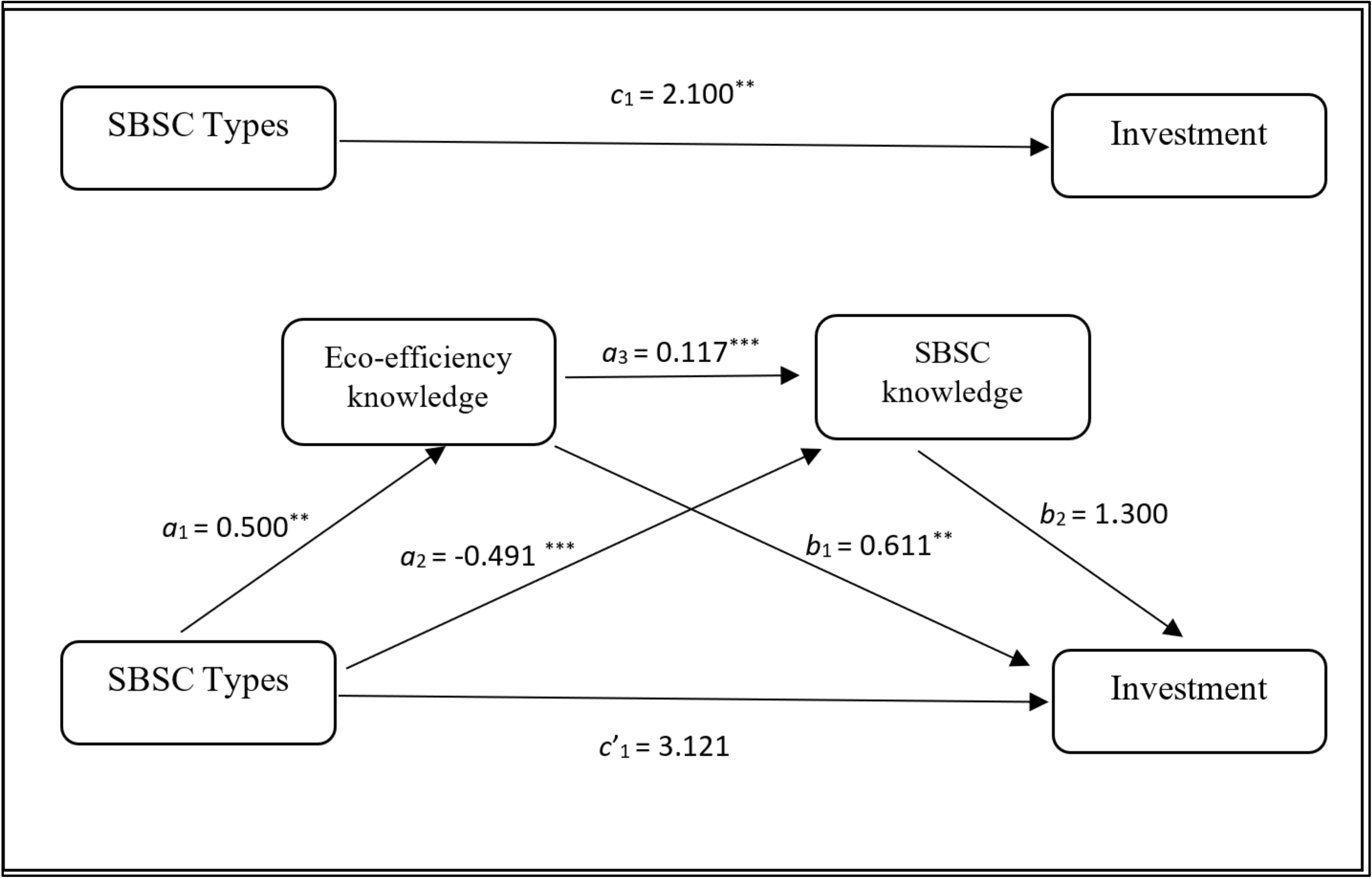

The direct effect of c’1 = 3.121 is statistically significant (p = 0.03), for it is not affected by the variables that are proposed as intervening between the SBSC type (four-perspective versus five-perspective) (four-perspective SBSC: n = 20, mean = 11.000, SD = 1.025 or the five-perspective SBSC: n = 20, mean = 13.100, SD = 4.228) and investment decision-making that achieves environmental objectives. Two specific indirect effects are not significant. However, one specific indirect effect is significant, as evidenced by the bootstrap confidence intervals that do not contain zero. The first indirect effect, H1b, is not significant. It carries the effect of the SBSC type (four-perspective versus five-perspective) through eco-efficiency knowledge only, bypassing SBSC knowledge. This indirect effect is the product of a1 = 0.500 and b1 = 0.611, with a 95% bootstrap confidence interval of −1.132–0.232. Eco-efficiency knowledge did not have any effect on the SBSC type and this did not result in better investment decision-making that achieved environmental objectives, independent of SBSC knowledge. Therefore, H1b is not supported.

The next indirect effect, H2b, flows from the SBSC type (four-perspective versus five-perspective) directly to the SBSC knowledge and then to investment decision-making that achieves environmental objectives, bypassing eco-efficiency knowledge. It is defined as the product of a2 = −0.491 and b2 = 1.300, with a 95% bootstrap confidence interval of −1.639 to −0.141. Therefore, those who were given SBSC with five perspectives and had more SBSC knowledge made better investment decisions that achieved environmental objectives. H2b is supported.

In contrast, the last indirect effect of the four-perspective versus five-perspective SBSC passes through both the eco-efficiency knowledge and SBSC knowledge, which is H3b. It is estimated as the product a1, a3 = 0.117, and b2, with a 95% bootstrap confidence interval of −0.267–0.061. Thus, the combined effect of eco-efficiency knowledge and SBSC knowledge had no effect on the relationship between the SBSC type (four-perspective vs. five-perspective) and investment decision-making that achieved environmental objectives. This leads us to conclude that H3b is not supported.

5. Discussion and Conclusions

The purpose of the current study is to investigate whether eco-efficiency knowledge and SBSC knowledge mediate the relationship between the BSC versus SBSC or the SBSC type (SBSC four-perspective versus five-perspective) and environmental investment decision-making. Our findings lead us to conclude that eco-efficiency knowledge alone does not mediate the relationship between the BSC versus SBSC (H1a), the SBSC type (SBSC four-perspective versus five-perspective) (H1b) and investment decision-making that aims to achieve environmental objectives. This result is inconsistent with the findings of literature [39] that proved that increasing the knowledge of the efficient use of capital and environmental resources guides better decision-making, thereby asserting that it is essential that information should be managed properly to enhance eco-efficiency knowledge for better investment decision-making [13]. This conflicting result may be because knowledge of the efficient use of the process is not enough to interpret the data from the BSC and SBSC types unless it is combined with a knowledge of the SBSC architecture as well (e.g., [28]).

In relation to the SBSC knowledge, this study confirms the findings of prior studies (e.g., [5,7,20,44]) which observed that knowledge of SBSC measures impacts the weight of investment decision-making that places importance on environmental performance. This knowledge, as predicted, improves the relationship between the BSC/SBSC types and environmental investment decision-making by enabling proper attention to be given to the different SBSC measures, (H2a and H2b). Thus, decision-makers who have no innate knowledge of the complex environmental measures may struggle to evaluate the decision relevance of such complex measures. Hence, there is a need for managers to have sufficient knowledge of SBSC measures and design to make good environmental investment decisions. SBSC knowledge also reduces the confusion of SBSC types by enabling the SBSC metrics to stand out by recognizing the most appropriate SBSC measures when choosing between alternatives (for example, the Common and Unique measures) [4].

The combined effect of eco-efficiency knowledge and SBSC knowledge significantly influences the relationship between the BSC versus SBSC and better investment decision-making that achieves environmental objectives, (H3a). This is because eco-efficiency knowledge stands to expresses a relationship between the positive and negative effects of a decision. Besides that, eco-efficiency knowledge reflects the trade-offs between the economic and the environmental business performances and can be used to promote improvements along the value chain and the sustainability of products, processes, and services [12], which in turn facilitates an increase of SBSC knowledge. However, these knowledge combinations did not have an impact on the relationship between the SBSC type and environmental investment decisions (H3b).

A reason for this result could be due to the way that environmental interrelated knowledge functions when changing from four to five SBSC perspectives and the way it has an impact on environmental investment decision-making. Since the literature has found that the way that the SBSC data are presented has different levels of influence on the decision-maker to make environmental decisions which require knowledge based on experience and practices instead of academic knowledge, Frick and Wilson [15] argued that different forms of environmental knowledge do not work together unless knowledgeable participants are included. Therefore, this result could be quite motivational for researchers to conduct experimental methods with people such as a manager who have sufficient knowledge of SBSC architecture and knowledge related to environmental issues to examine the serial mediation effect of eco-efficiency knowledge and SBSC knowledge on the relationship between SBSC type and environmental investment decision-making and to compare the results to each conclusions which is necessary for successful environmental investment decision-making.

Consistent with previous research (e.g., [12,38,48]), eco-efficiency knowledge and SBSC knowledge both influence environmental investment decision-making. This theory may be useful in explaining how environmental investment decision-making processes evolve with the increasing knowledge of eco-efficiency processes and SBSC metrics.

Consequently, this study can be useful in understanding the effect of knowledge, particularly eco-efficiency knowledge and SBSC knowledge, and in explaining the association between the BSC versus SBSC and investment decision-making that achieves environmental objectives. The results of the mediation effects show that appropriate sequential implementation of eco-efficiency knowledge and SBSC knowledge may enable manufacturers to reap environmental, economic, and investment benefits. In addition, its guide as a decision maker depends on the SBSC architecture (four or five perspectives) to achieve a better investment decision that achieves environmental objectives.

Based on this study, it can be concluded that knowledge on the quality of performance evaluation is essential to enhance investment decision-making and achieve environmental objectives. A lack of effective knowledge on the efficient use of environmental information and SBSC type can negatively affect the outcomes of environmental investment decisions. Thus, the current study uses the experimental method to demonstrate the role of eco-efficiency knowledge and SBSC knowledge in the relationship between SBSC types and environmental investment decision-making that emphasize environmental objectives. The results indicate that the direct proportional relationship between SBSC types and environmental investment decision-making is most significant with the presence of both eco-efficiency knowledge and SBSC knowledge. Meanwhile, the indirect impact of eco-efficiency knowledge and SBSC knowledge on the direct effect of SBSC type and environmental investment decision-making has not been seen. This is perhaps because eco-efficiency knowledge and SBSC knowledge are not specified as a set of measurements.

This study has certain limitations. Firstly, in determining the scope of the study, motivation by a real-world phenomenon is challenging. It can be difficult to identify appropriate measures for a certain construct. This study measured the SBSC knowledge by using four true/false questions that were adopted from [2] and six true/false questions that were adopted from [41] to examine eco-efficiency knowledge. These questions may not have addressed the different aspects of eco-efficiency knowledge and SBSC knowledge. The reason behind this is simply because knowledge is quite a broad aspect and thus the number of questions that have been used in the current study may not have been enough. Measuring knowledge requires a greater variety of questions to increase the reliability of the results obtained. However, there is an unavailability of studies that measure eco-efficiency knowledge and SBSC knowledge that could be adopted from. Thus, there is need to develop this study’s scales with more aspects to measure the individual’s knowledge of eco-efficiency and SBSC and figuring out its outcomes.

Another limitation of this study is that the participants were postgraduate students with very low levels of knowledge about the SBSC utilization in the real world and, probably, with no experience at all on allocating such an amount of money into competing projects. If the same experiment were conducted on participants who were experienced managers that utilize these tools in their work and are familiar with these concepts in their daily decision-making, the results could be improved.

Furthermore, this study adds to the SBSC and environmental investment literature [2] by examining how eco-efficiency knowledge and SBSC knowledge impacts the relationship between the outcomes in a sustainability scorecard type context and environmental investment decision-making. Regarding the implication for the practice many organizations tend to adopt new ideas without providing adequate levels of training to their operational decision makers. Hence, a superficial understanding of concepts such as Eco Efficiency and SBSC architecture may not be able to link SBSC with decision-making that are geared towards fulfilling environmental objectives. Furthermore, the testing of the two mediators, Eco efficiency knowledge and SBSC knowledge, has practical significance because organizations would then realize that gearing up the depth and breadth of their managerial training programs is likely to create significantly higher results.

Further research may be contributed by answering which type of SBSC has more impact on environmental decision-making with the introduction of eco-efficiency knowledge and SBSC knowledge as mediators, as well as other factors such as risk management that may ultimately impact the evaluative effectiveness of decisions involving environmental accounting information to bring to conclusion the current debate regarding SBSC architecture [50].

Author Contributions

All authors contributed equally in the paper according to their strength in the area of sustainability and carrying out the research.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Sarker, T.K.; Burritt, R.L. An Empirical Examination of the Role of Environmental Accounting Information in Environmental Investment Decision-Making; Springer Science & Business Media: Berlin, Germany, 2008; Volume 24, p. 457. [Google Scholar]

- Alewine, H.C.; Stone, D.N. How does environmental accounting information influence attention and investment? Int. J. Account. Inf. Manag. 2013, 21, 22–52. [Google Scholar] [CrossRef]

- Jiangtao, L.; Pin, Z. Analysis of sustainability balanced scorecard influences on decision processes and investment decisions. Proceedings of 2nd IEEE International Conference Information Management and Engineering (ICIME), Chengdu, China, 16–18 April 2010; pp. 111–116. [Google Scholar]

- Alewine, H.C.; Miller, T.C. How Balanced Scorecard Format and Reputation Related to Environmental Objectives Influence Performance Evaluations. In Advances in Management Accounting; Emerald Group Publishing Limited: Bingley, UK, 2016; pp. 123–165. [Google Scholar]

- Kaplan, S.E.; Wisner, P.S. The judgmental effects of management communications and a fifth balanced scorecard category on performance evaluation. Behav. Res. Account. 2009, 21, 37–56. [Google Scholar] [CrossRef]

- Nicolăescu, E.; Alpopi, C.; Zaharia, C. Measuring corporate sustainability performance. Sustainability 2015, 7, 851–865. [Google Scholar] [CrossRef]

- Wu, J.; Haasis, H.D. Knowledge management-enabled application of the sustainability balanced scorecard. In Proceedings of the 2011 IEEE Asia-Pacific Power and Energy Engineering Conference (APPEEC), Wuhan, China, 25–28 March 2011; pp. 1–4. [Google Scholar]

- Müller, K.; Holmes, A.; Deurer, M.; Clothier, B.E. Eco-efficiency as a sustainability measure for kiwifruit production in New Zealand. J. Clean. Prod. 2015, 106, 333–342. [Google Scholar] [CrossRef]

- Caiado, R.G.G.; de Freitas Dias, R.; Mattos, L.V.; Quelhas, O.L.G.; Leal Filho, W. Towards sustainable development through the perspective of eco-efficiency-A systematic literature review. J. Clean. Prod. 2017, 165, 890–904. [Google Scholar] [CrossRef]

- Beljić, M.; Panapanaan, V.; Linnanen, L.; Uotila, T. Environmental knowledge management of Finnish food and drink companies in eco-efficiency and waste management. Interdiscip. J. Inf. Knowl. Manag. 2013, 8, 99–119. [Google Scholar] [CrossRef]

- Doorasamy, M.; Garbharran, H. The role of environmental management accounting as a tool to calculate environmental costs and identify their impact on a company’s environmental performance. Asian J. Bus. Manag. 2015, 3, 8–30. [Google Scholar]

- Carvalho, H.; Govindan, K.; Azevedo, S.G.; Cruz-Machado, V. Modelling green and lean supply chains: An eco-efficiency perspective. Resour. Conserv. Recycl. 2017, 120, 75–87. [Google Scholar] [CrossRef]

- Cagno, E.; Micheli, G.J.; Trucco, P. Eco-efficiency for sustainable manufacturing: An extended environmental costing method. Prod. Plan. Control 2012, 23, 134–144. [Google Scholar] [CrossRef]

- Huang, P.S.; Shih, L.H. Effective environmental management through environmental knowledge management. Int. J. Environ. Sci. Technol. 2009, 6, 35–50. [Google Scholar] [CrossRef]

- Frick, J.; Kaiser, F.G.; Wilson, M. Environmental knowledge and conservation behavior: Exploring prevalence and structure in a representative sample. Personal. Individ. Differ. 2004, 37, 1597–1613. [Google Scholar] [CrossRef]

- Banker, R.D.; Chang, H.; Pizzini, M. The judgmental effects of strategy maps in balanced scorecard performance evaluations. Int. J. Account. Inf. Syst. 2011, 12, 259–279. [Google Scholar] [CrossRef]

- Banker, R.D.; Chang, H.; Pizzini, M.J. The balanced scorecard: judgmental effects of performance measures linked to strategy. Account. Rev. 2004, 79, 1–23. [Google Scholar] [CrossRef]

- Grevinga, K. Common Measure bias in the Balanced Scorecard: An Experiment with Undergraduate Students. Master’s Thesis, University of Twente, Enschede, The Netherlands, 2013. [Google Scholar]

- Gering, M.; Mntambo, V. Parity politics; Chartered Institute of Management Accountants: London, UK, 2002; pp. 36–37. [Google Scholar]

- Dilla, W.N.; Steinbart, P.J. Relative weighting of common and unique balanced scorecard measures by knowledgeable decision makers. Behav. Res. Account. 2005, 17, 43–53. [Google Scholar] [CrossRef]

- Lipe, M.G.; Salterio, S. A note on the judgmental effects of the balanced scorecard’s information organization. Account. Organ. Soc. 2002, 27, 531–540. [Google Scholar] [CrossRef]

- Rashidi, K.; Saen, R.F. Measuring eco-efficiency based on green indicators and potentials in energy saving and undesirable output abatement. Energy Econ. 2015, 50, 18–26. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. Pursuing Sustainability with the Balanced Scorecard: Between Shareholder Value and Multiple Goal Optimization; Centre for Sustainability Management: Lüneburg, Germany, 2012. [Google Scholar]

- Epstein, M.J.; Wisner, P.S. Using a balanced scorecard to implement sustainability. Environ. Qual. Manag. 2001, 11, 1–10. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The Sustainability Balanced Scorecard–Management to Business Strategy. Bus. Strateg. Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Alewine, H.C. A model for conducting experimental environmental accounting research. Sustain. Account. Manag. Policy J. 2010, 1, 256–291. [Google Scholar] [CrossRef]

- Tsai, W.H.; Chou, W.C.; Hsu, W. The sustainability balanced scorecard as a framework for selecting socially responsible investment: An effective MCDM model. J. Oper. Res. Soc. 2009, 60, 1396–1410. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. The Sustainability Balanced Scorecard: A Systematic Review of Architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Davis, G.B.; Olson, M.H. Management Information Systems: Conceptual Foundations, Structure, and Development; McGraw-Hill, Inc.: New York, NY, USA, 1984. [Google Scholar]

- Kettinger, W.J.; Li, Y. The infological equation extended: Towards conceptual clarity in the relationship between data, information and knowledge. Eur. J. Inf. Syst. 2010, 19, 409–421. [Google Scholar] [CrossRef]

- Payne, J.W.; Bettman, J.R.; Johnson, E.J. The Adaptive Decision Maker; Cambridge University Press: Cambridge, UK, 1993. [Google Scholar]

- Kaplan, S.E.; Petersen, M.J.; Samuels, J.A. An examination of the effect of positive and negative performance on the relative weighting of strategically and non-strategically linked balanced scorecard measures. Behav. Res. Account. 2011, 24, 133–151. [Google Scholar] [CrossRef]

- Ehrenfeld, J.R. Eco-efficiency. J. Ind. Ecol. 2005, 9, 6–8. [Google Scholar] [CrossRef]

- Dias-Sardinha, I.; Reijnders, L.; Antunes, P. From environmental performance evaluation to eco-efficiency and sustainability balanced scorecards. Environ. Qual. Manag. 2002, 12, 51–64. [Google Scholar] [CrossRef]

- Möller, A.; Schaltegger, S. The Sustainability Balanced Scorecard as a Framework for Eco-Efficiency Analysis. J. Ind. Ecol. 2005, 9, 73–83. [Google Scholar] [CrossRef]

- Uhlman, B.W.; Saling, P. Measuring and communicating sustainability through Eco-efficiency analysis. Chem. Eng. Prog. 2010, 106, 17–29. [Google Scholar]

- Ranđelović, M.P.; Stevanović, T. Sustainability Balanced Scorecard and Eco-Efficiency Analysis. Facta Univ.-Econ. Organ. 2012, 2, 257–270. [Google Scholar]

- Figge, F.; Hahn, T. Value drivers of corporate eco-efficiency: Management accounting information for the efficient use of environmental resources. Manag. Account. Res. 2013, 24, 387–400. [Google Scholar] [CrossRef]

- Lozano, F.J.; Lozano, R. Assessing the potential sustainability benefits of agricultural residues: Biomass conversion to syngas for energy generation or to chemicals production. J. Clean. Prod. 2017, 172, 4162–4169. [Google Scholar] [CrossRef]

- Martínez, C.I.P.; Silveira, S. Energy efficiency and CO2 emissions in Swedish manufacturing industries. Energy Effic. 2013, 6, 117–133. [Google Scholar] [CrossRef]

- Ravi, V. Analysis of interactions among barriers of eco-efficiency in electronics packaging industry. J. Clean. Prod. 2015, 101, 16–25. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Using the Balanced Scorecard as a strategic management system. Harvard Bus. Rev. 1996, 1, 75–85. [Google Scholar]

- Falle, S.; Rauter, R.; Engert, S.; Baumgartner, R.J. Sustainability Management with the Sustainability Balanced Scorecard in SMEs: Findings from an Austrian Case Study. Sustainability 2016, 8, 545. [Google Scholar] [CrossRef]

- Kang, G.; Fredin, A. The balanced scorecard: The effects of feedback on performance evaluation. Manag. Res. Rev. 2012, 35, 637–661. [Google Scholar] [CrossRef]

- Ullah, A.; Perret, S.R.; Soni, P. Eco-efficiency of cotton-cropping systems in Pakistan: An integrated approach of life cycle assessment and data envelopment analysis. J. Clean. Prod. 2016, 134, 623–632. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis; Prentice Hall: Upper Saddle River, NJ, USA, 1998; Volume 5, pp. 207–219. [Google Scholar]

- Libby, T.; Salterio, S.E.; Webb, A. The balanced scorecard: The effects of assurance and process accountability on managerial judgment. Account. Rev. 2004, 79, 1075–1094. [Google Scholar] [CrossRef]

- Lipe, M.G.; Salterio, S.E. The balanced scorecard: Judgmental effects of common and unique performance measures. Account. Rev. 2000, 75, 283–298. [Google Scholar] [CrossRef]

- Hayes, A.F. PROCESS: A Versatile Computational Tool for Observed Variable Mediation, Moderation, and Conditional Process Modelling; Scientific Research Publishing Inc.: Wuhan, China, 2012. [Google Scholar]

- Hansen, E.G.; Schaltegger, S. Sustainability Balanced Scorecards and their Architectures: Irrelevant or Misunderstood? J. Bus. Ethics 2017. [Google Scholar] [CrossRef]

Figure 1.

Hypothesis 1.

Figure 2.

Hypothesis 2.

Figure 3.

Hypothesis 3.

Figure 4.

A serial multiple mediation model with eco-efficiency knowledge and SBSC knowledge as proposed mediators of the influence of the traditional Balanced Scorecard (BSC) versus Sustainability Balanced Scorecard (SBSC) on environmental investment decision-making. Notes: * p < 0.05, ** p < 0.01, *** p < 0.001.

Figure 4.

A serial multiple mediation model with eco-efficiency knowledge and SBSC knowledge as proposed mediators of the influence of the traditional Balanced Scorecard (BSC) versus Sustainability Balanced Scorecard (SBSC) on environmental investment decision-making. Notes: * p < 0.05, ** p < 0.01, *** p < 0.001.

Figure 5.

A serial multiple mediation model with eco-efficiency knowledge and SBSC knowledge as proposed mediators of the influence of SBSC types on environmental investment decisions. Notes: * p < 0.05, ** p < 0.01, *** p < 0.001.

Figure 5.

A serial multiple mediation model with eco-efficiency knowledge and SBSC knowledge as proposed mediators of the influence of SBSC types on environmental investment decisions. Notes: * p < 0.05, ** p < 0.01, *** p < 0.001.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

The measurement metrics for each perspective in the three traditional Balanced Scorecard (BSC) type manipulations.

Table 1.

The measurement metrics for each perspective in the three traditional Balanced Scorecard (BSC) type manipulations.

| Perspective | Metrics |

|---|---|

| Financial | • Return on Investment |

| • Annual cash flow increase | |

| • Sales growth | |

| • Payback period | |

| Customer | • Customer satisfaction rating |

| • Percentage of sales to new customers | |

| • Customer referrals | |

| • New product offers to customers | |

| Internal Business Processes | • Time to process customer order |

| • Annual number of stock outs for an order | |

| • On-time deliveries as a percentage of all deliveries | |

| • Time to launch new products to market | |

| Learning and Growth | • Employee turnover |

| • Number of employee training certifications | |

| • Employee satisfaction | |

| • Annual production employee work-related accidents | |

| Environmental | • Energy cost savings |

| • Number of community complaints about the company’s pollutant emissions | |

| • Annual tons of nitrogen dioxide emissions | |

| • Number of training hours per factory employee for environmental emergency responses |

Note: The BSC condition only contains four perspectives: financial, customer, internal business, and learning growth. The environmental perspective was only included in the SBSC condition as its fifth perspective. In the four-perspective SBSC condition, the four metrics in the environmental perspectives were distributed into the traditional four perspectives as follows: an energy cost savings metric was included in the financial perspective; the number of community complaints about company pollutant emissions metric was included in the customer perspective; the annual tons of nitrogen dioxide emissions metric was included in the internal business processes perspective; and the number of training hours per factory employee for environmental emergency responses metric was included in the learning and growth perspective.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Jassem, S.; Azmi, A.; Zakaria, Z. Impact of Sustainability Balanced Scorecard Types on Environmental Investment Decision-Making. Sustainability 2018, 10, 541. https://doi.org/10.3390/su10020541

AMA Style

Jassem S, Azmi A, Zakaria Z. Impact of Sustainability Balanced Scorecard Types on Environmental Investment Decision-Making. Sustainability. 2018; 10(2):541. https://doi.org/10.3390/su10020541

Chicago/Turabian StyleJassem, Suaad, Anna Azmi, and Zarina Zakaria. 2018. "Impact of Sustainability Balanced Scorecard Types on Environmental Investment Decision-Making" Sustainability 10, no. 2: 541. https://doi.org/10.3390/su10020541

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.