1. Introduction

Non-timber forest products (NTFPs) commercialization was promoted following the environmental movement of the 1980s with a view to improve the livelihood benefits of forest and forest fringe communities and thereby the sustainable use of forests [

1,

2,

3]. Since then, commercialization remains one of the major issues receiving research and development attention [

4]. The commercialization process has been largely dealt with in three related approaches: (i) domestication and management intensification; (ii) sustainable rural livelihood; and (iii) pro-poor (value chains). The domestication approach focuses on bringing plants from the wild to farms to improve productivity, quality, and marketability [

5,

6,

7]. The sustainable livelihood approach deals with the understanding of livelihood assets and income mainly at a local level [

8,

9,

10]. The value chain approach emerged in response to filling the limitations and complementing the previous approaches, which have a large rural focus and are weak in linking the various actors and processes in the production to consumption systems [

10,

11,

12,

13].

Commercialization involves the integration of a product or a household into a market economy. This integration may be expressed by an increased financial trade value [

11] or by the proportion of the sale to the total income [

14,

15]. When the proportion of production ending in the market is higher than a normal subsistence sale, the product is generally considered as commercialized. Similarly, commercialization may also be explained by the nature of the value chain strength and density. When a product or service attracts more demand, a concomitant increase in the value chain length and complexity may be observed. Commercialization may also occur at the input side, as manifested by increased use of purchased inputs [

16] and increased management investment in domesticated or wild systems [

17]. The success of product commercialization can be determined by factors external to small-scale farmers, including infrastructure, level of urbanization, technological change, and demand for the product [

11,

15,

16,

18,

19] as well as farm-level factors including size of landholding, extent of land use diversification, level of input use, and intensity of management [

15,

20,

21]. Thus, the commercialization of a product can be stimulated or deterred by factors ranging from household characteristics to broader institutional and policy environments.

Bamboo, generally considered to be a non-timber forest product, is a multipurpose resource with a great potential for commercialization. Several studies in Asia reveal that bamboo supports rural development, appeals to smallholder producers, and has several pro-poor characteristics [

22,

23,

24,

25,

26]. Moreover, bamboo has become a high-tech industrial raw material and substitute for wood with well-established markets and a wide range of production-to-consumption systems [

27,

28]. However, African bamboo utilization is still limited primarily to low value subsistence uses and local markets [

29,

30]. Similarly, in contrast to Africa, in many places in Asia both overall and commercial income contribution of bamboo is high and growing at a substantial rate [

22,

31,

32]. Yet, recent trends in bamboo-growing regions of Africa show that bamboo species are gradually drawing increased attention as a vehicle for development [

33], so that there is a good opportunity to enhance production.

Ethiopia has over 960,000 ha of bamboo [

34], corresponding to approximately 7% of the global bamboo resource. The country can sustainably produce three million cubic meters of dry weight annually [

24] from its two commercially important bamboo species:

Yushania alpina and

Oxytenanthera abyssinica. Despite this potential, current uses are primarily limited to construction of traditional houses, low-grade furniture, household utensils, beehives, fences, and handicrafts [

35]. However, several attributes of bamboo such as the abundant availability of commercially useful species of bamboo and their fast growth, adaptability on marginal lands, promising material properties, and potential to support rural development give high priority to the commercialization of bamboo species in Ethiopia. However, little research has been performed concerning the current state of bamboo commercialization and its determining factors in the Ethiopian context. This study aims to fill this gap by (i) examining the extent of bamboo commercialization through the analysis of management intensity, income ratios, and value chain strength, and (ii) empirically identifying factors contributing to differential levels of commercialization within and between the study regions.

2. Materials and Methods

2.1. Study Areas

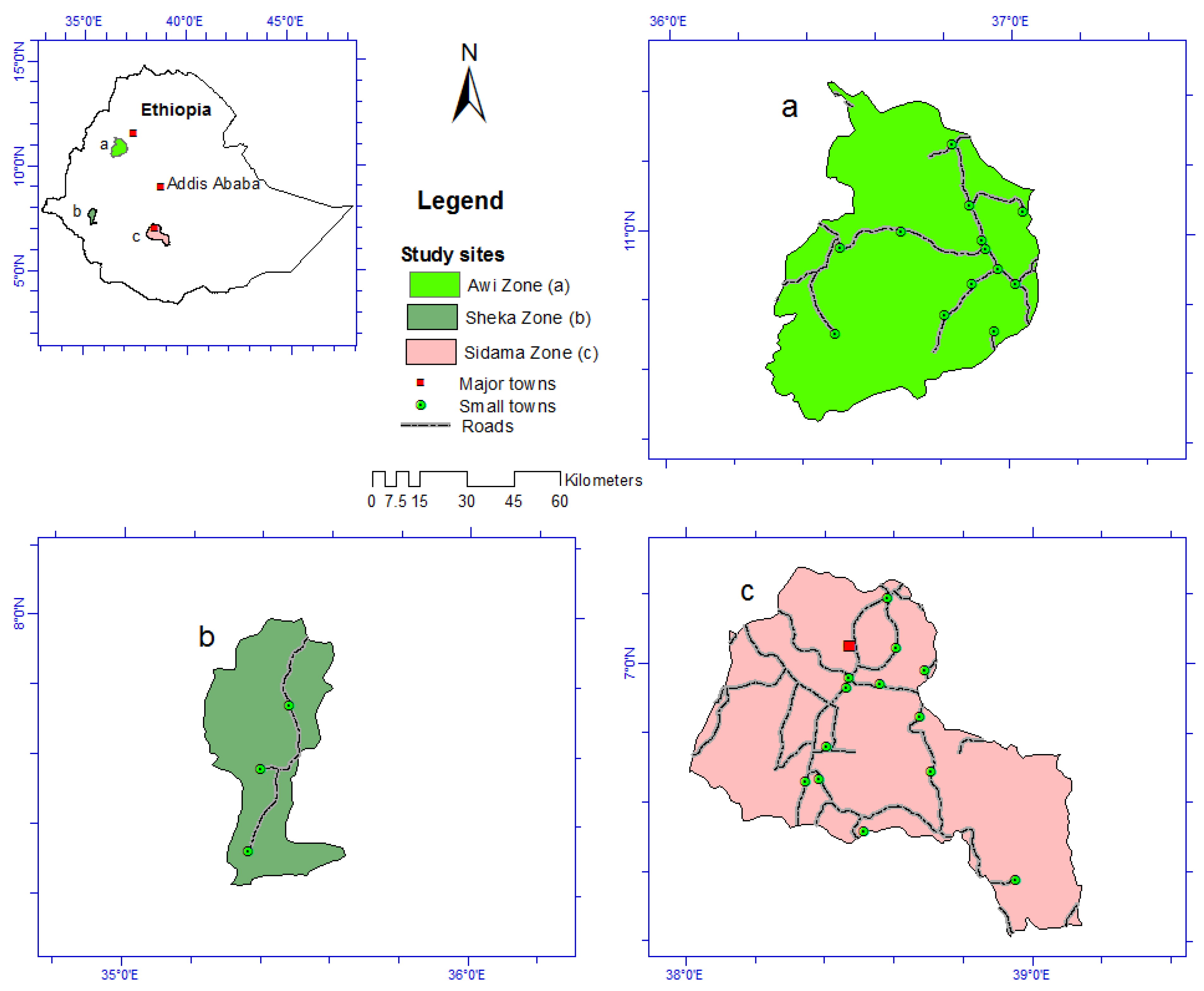

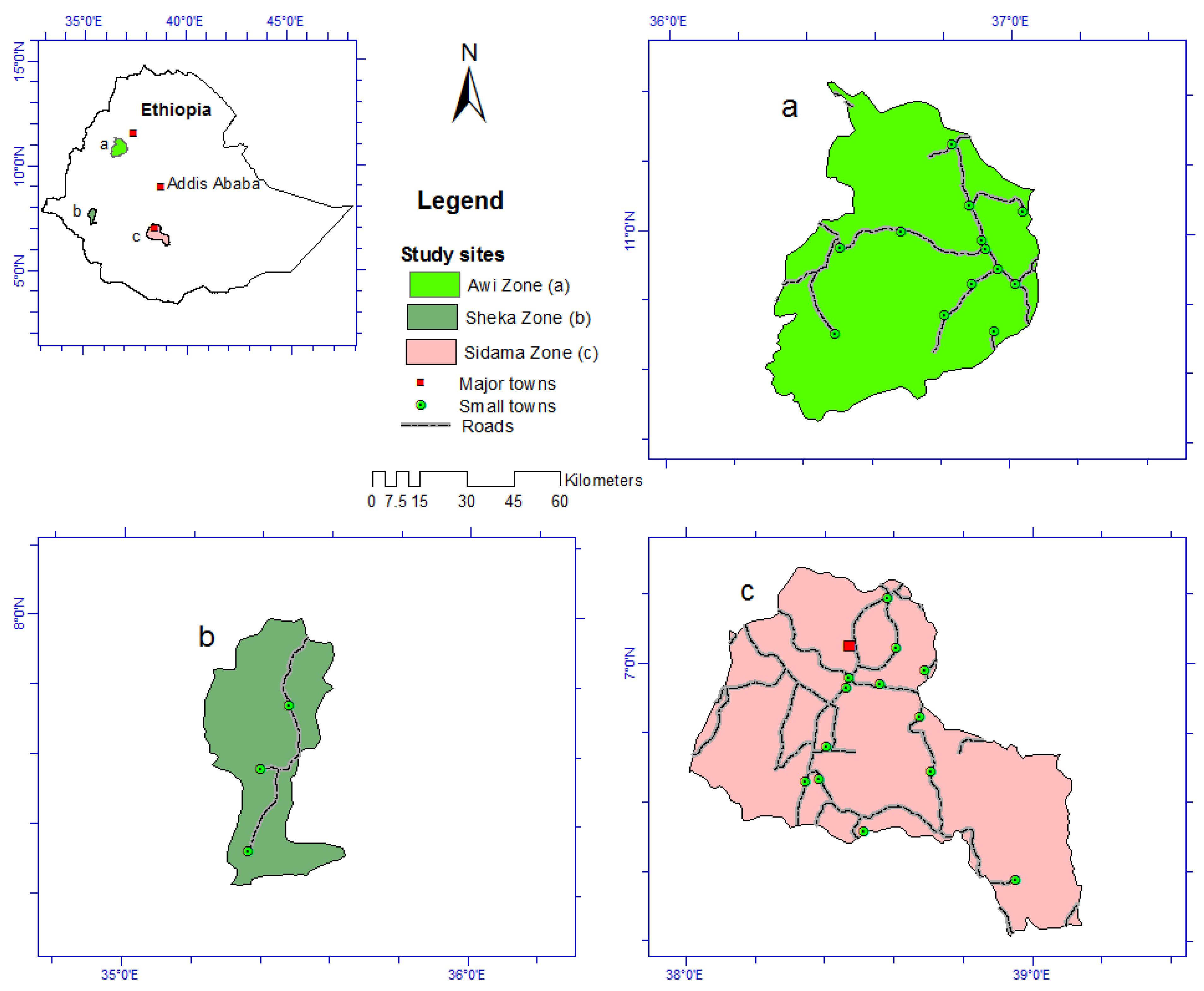

Three major bamboo-producing rural districts and four trading and consumption cities of Ethiopia were selected for this study. The rural districts studied are Awi, in the northwest; Sheka, in the southwest; and Sidama, in south-central Ethiopia (

Figure 1). In each of the three rural districts, the major bamboo-producing

kebeles (smallest political administration units in Ethiopia) were selected. The

kebeles lie in more or less similar agro-ecological and altitudinal locations ranging roughly between 2000 and 3000 m asl (above sea level). Bamboo producers and harvesters are all farmers who manage bamboo as part of their land use system in Awi and Sidama or extract from the forest as in the case of Sheka. All of them possess highland bamboo species (

Yushania alpina) and household characteristics such as family size, age, and education level and these are not significantly different among the

kebeles. However, there are several other biophysical and socioeconomic differences among the study districts, which are described here.

Figure 1.

Location of the study districts in relation to the country map.

Figure 1.

Location of the study districts in relation to the country map.

2.1.1. Awi

Awi has an area of 9148 km

2 and a population of 982,942 [

36]. It is located between 10°27' and 11°25' N latitude and 36°17' and 37°40' E longitude. Awi is located on the highway from Addis Ababa to Bahir Dar, a flourishing city in the northwestern part of the country. Altitude ranges from 1900 to 3300 m asl and the average temperature is approximately 18 °C with an annual average rainfall of 2206 mm. Bamboo grows in the highlands above 2200 m asl. Although Awi is 445 km from Addis Ababa, it is surrounded by other cities including Bahir Dar (120 km), Debremarkos (140 km), and Gondar (290 km), as well as Injebara, the district capital. The district is well networked with all-weather roads and local communities have easy access to transportation to move their products to markets and centers of consumption.

2.1.2. Sheka

Sheka has a population of 192,970 [

36] and an area of approximately 2175 km

2. Administratively, it is located within the Southern Nation, Nationalities and Peoples regional state (SNNPRS), and geographically the district lies between 7°24' and 7°52' N latitude and 35°13' and 35°35' E longitude. The altitudinal range of the district falls between 900 and 2700 m asl and it receives high amounts of rainfall, with an average of 1800–2200 mm annually [

37]. Bamboo is located in marshy areas at altitudes ranging between 2450 and 2750 m asl, as part of the montane forest system. Agricultural practices are the sole livelihood sources for most inhabitants. Enset and maize are major subsistence crops. Honey and coffee are major cash income sources. Livestock provides both subsistence use and cash income.

This district is one of the most remote in the country, with a poor road network and limited infrastructure connecting it with major urban centers. It is located 700 km southwest of Addis Ababa and 350 km from Jimma. The city of Jimma has other sources of bamboo and wood products at shorter distances and with better road networks. There are few other towns in the region that stimulate local-level trade and consumption of forest products.

2.1.3. Sidama

The Sidama district has an area of 7672 km

2 and a population of 2,954,136 [

36]. It is located between 5°45' and 6°45' N latitude and 38° and 39° E longitude. The altitude varies from 500 to 3500 m asl. Average annual temperature ranges from 15 to 20 °C and average annual rainfall lies between 800 and 1200 mm. In general the highlands are cooler and moister than the mid- or low-altitude parts of the districts. The areas above 2000 m asl are generally suitable for growing bamboo. The major agricultural crops include coffee, enset, chat, sugarcane, beans, maize, wheat, barley, and several vegetables and fruits occupying specific agro-ecological niches along the altitudinal gradient [

38].

Sidama is well connected with the main high-standard road that leads to the capital, with the exception of some remote highlands that have only gravel roads. Hawassa, which is the capital of Sidama and SNNPRS, is a dynamic city with a high density of educated inhabitants and is a center for local and international tourists. The city is a multipurpose city with high market transactions. The kebeles where data were collected lie 145 km from Hawassa.

2.1.4. Urban Study Sites

In addition to the rural districts, four towns were covered in this study. The towns with their respective populations are Masha (11,122), Hawassa (157,879), Bahir Dar (221,991), and Addis Ababa (2,739,551) [

36]. These towns are the major urban bamboo resource consumption centers in Ethiopia and were selected for the study owing to the presence of majority of bamboo processors (people who convert bamboo culms to different value-added products), traders, and related bamboo commercialization agents. Moreover, Hawassa is the regional capital for Sheka and Sidama, and Bahir Dar is the regional capital for Awi. Addis Ababa is the capital and the only metropolitan city in Ethiopia. The town of Masha was selected because it is the nearest town available for trade and consumption of bamboo resources originating in Sheka.

2.2. Data Collection

Three phases of field surveys were conducted. Preliminary data collection and field observations were performed in July 2010 and detailed household surveys using semi-structured questionnaires and group discussions with producers and harvesters were conducted between December 2011 and February 2012. Further surveys for other actors in the value chain (processors, traders, and institutional actors) were conducted during August–September 2012.

Production-level surveys were conducted in six kebeles, two in each district. Samples were selected by systematic random sampling by proportional allocation to size of the kebeles. A total of 133 producer and harvester household heads, among them 38 from Awi, 43 from Sidama, and the rest from Sheka, were interviewed. There were only two female household heads in the final sample. Two group discussions were conducted in each kebele with community elders and local bamboo processors selected by the assistance of development agents and chairman of respective kebeles. The survey questionnaires covered issues regarding basic household characteristics, bamboo production and management, total number of culms consumed and sold annually, prices and income, trade, value chain actors, and relationships. Similar types of issues were also covered during group discussions.

Income and price data were also collected at local markets and from additional actors along the value chain. Prices at the local market were collected from all interviewed households and their averages were used in the calculation of income and income ratios. Subsistence income was estimated by assigning cash income equivalents based on the average local bamboo price per culm during the survey year and multiplying it by the estimated number of bamboo culms consumed by the household.

Subsequent interviews were conducted along the bamboo value chain: traders (3), processors (35), and consumers (45). In these stages, interviewees were selected purposively following the value chain networks. Purposive sampling was used as the total population was not known. All trader interviewees were taken from Addis Ababa, as there were few formal traders in the other cities. Even the traders from Addis Ababa were engaged only on a part-time basis. Processor samples were taken from Addis Ababa (25), Hawassa (5), Bahir Dar (4), and Masha (1). Processing enterprises ranged from small, single-person family enterprises to medium sized enterprises with more than 150 employees. In each enterprise, the managers were interviewed. The data collection also benefited from informal interviews with employed craftsmen. The enterprise studied in the town of Masha was only recently established and conducted small-scale bamboo processing as a parastatal enterprise (a local prison enterprise). The interviewee was a police officer who was trained in bamboo craftsmanship and was responsible for managing the bamboo processing work at the prison.

2.3. Data Analysis

Collected data were analyzed using a combination of descriptive statistics, ANOVA, value chain, and regression analysis. Data collected through group discussions, observation, and qualitative interviews were analyzed qualitatively. Data regarding production-to-consumption systems, actors, and processes were mapped and described using the value chain analysis guidelines of Kaplinsky

et al. [

12] and Fasse

et al. [

39]. Bamboo income and commercialization margins at the producer level were analyzed using descriptive statistics and ANOVA. For analysis of income, average market prices of culms at the local market were used, given that bamboo-handling households provided data based on local market prices. Subsistence equivalents were derived from the selling price of products sold during the survey year. For analysis of variance, non-parametric Kruskal–Wallis one-way ANOVAs on ranks were used to accommodate the non-normally distributed data. Normality was checked using the Shapiro–Wilk test. Determinants of bamboo commercialization at various levels were analyzed using best subsets regression analysis where the rate of commercialization was taken as the dependent variable.

3. Results

3.1. Bamboo Production Systems and Management

According to the data from interviews and group discussions, bamboo management systems differ among regions. Sidama and Awi have a domesticated and relatively intensively managed bamboo production system as compared with Sheka, which is an entirely natural forest-based system. Furthermore, the household survey revealed that 100% of farmers in the domesticated system obtained their bamboo products from privately owned sources, whereas all of the Sheka farmers obtained products entirely from state-owned natural forest-based sources.

As shown in

Table 1, bamboo management in Sheka was limited to appropriate harvesting, which included cutting at appropriate height, using sharp blades and cutting mature bamboo culms. In Sidama the most common management practice for bamboo was tending of natural sprouts, weeding, digging around to improve soil porosity, weeding or slashing of other species, culling or removing old or diseased individuals, and shading of newly planted bamboo.

Table 1.

Bamboo management practices in Awi, Sidama, and Sheka districts of Ethiopia.

Table 1.

Bamboo management practices in Awi, Sidama, and Sheka districts of Ethiopia.

| Management type | Percentage of respondents |

|---|

| Awi (

n = 38) | Sidama (

n = 43) | Sheka (

n = 52) |

|---|

| Appropriate harvesting | 21 | 19 | 13 |

| Tending (thinning, weeding, digging, piling covers) | 29 | 77 | – |

| Protection against cattle | 34 | 40 | – |

| Fertilization | 34 | 16 | – |

| Introducing new variety | 3 | 7 | – |

| Protect from flooding | 8 | – | – |

| Total * | | | |

Table 1 also shows that fertilization (mostly practiced for crops) has been used for bamboo in Awi owing to lower soil fertility and demand for large diameter culms. There was also a need for protection of bamboo from cattle. This need was emphasized in both domesticated systems, as cattle can cause major damage through grazing and trampling especially during the period of shoot sprouting.

There was a difference between regions in the amount of labor (measured in days) allocated per year for bamboo management. Sidama invested the most (2.57), followed by Awi (2.26), whereas an average Sheka farmer invested almost nil. Similarly, the number of people who were involved in any one type of management was highest in Sheka (87%) compared with 5% and 3% at Sidama and Awi, respectively. The reasons interviewees mentioned for their limited engagement in Sheka were that bamboo does not require management (73%), it is an open access resource and there is no incentive for management (52%), the resource is state-owned (38%), and interviewees would cooperate if the government takes the initiative (35%).

In contrast, a majority of farmers in Sidama and Awi were involved in one or more types of bamboo management practices. Their reasons for investment in bamboo management were to increase their income (100%), to improve culm diameter (27%), to speed culm growth (11%), and to identify mother bamboos for vigorous stands (1%). The responses were inherently similar, in that all interviewees aimed to produce a high-quality culm that would fetch better income or provide for better provisioning services.

Differences were also observed in the interviewees’ valuation of bamboo for various provisioning services. Bamboo is the first and second preferred tree crop in Sidama and Awi, respectively, for construction of houses and other household utilities. It is also the second useful income source next to Eucalyptus species. In Sheka bamboo is the third most useful tree for house construction, owing primarily to its light weight for roofing.

3.2. Income and Income Ratios

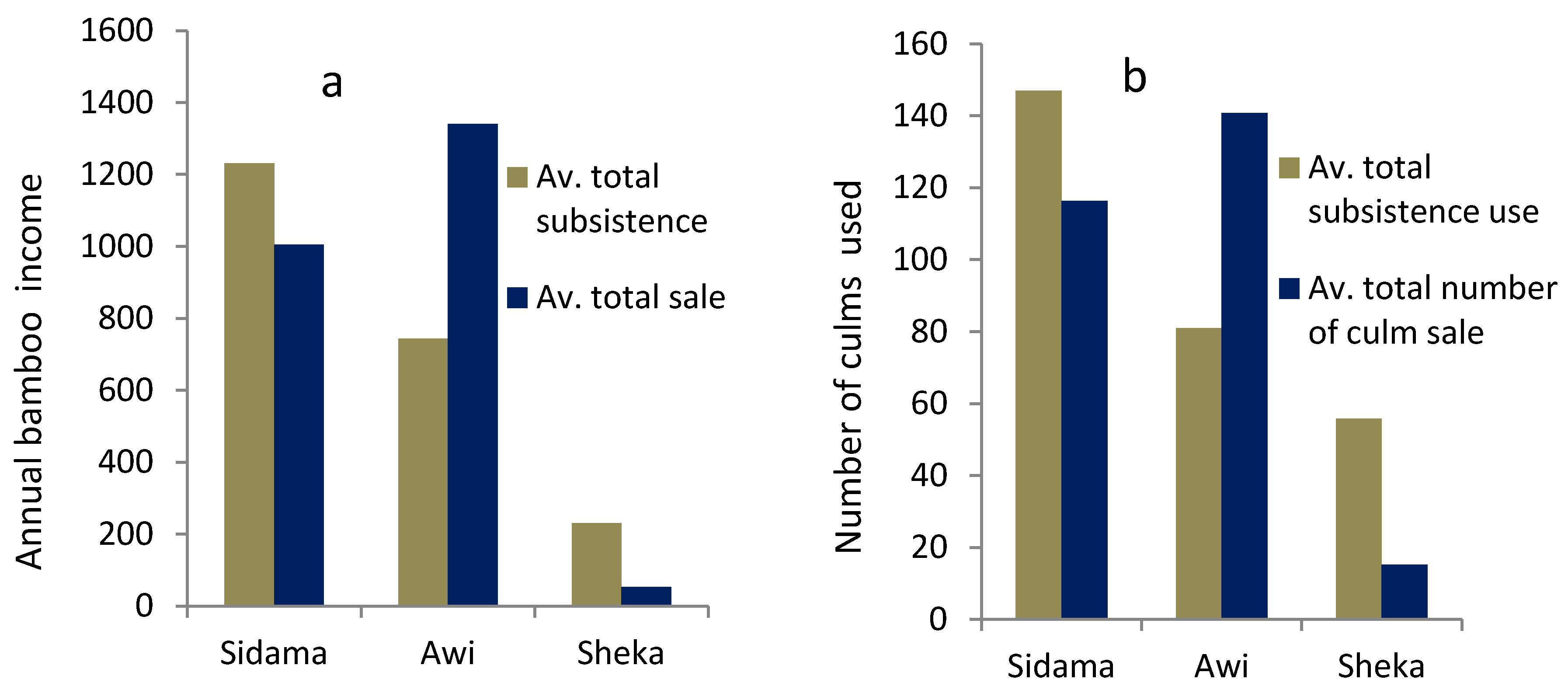

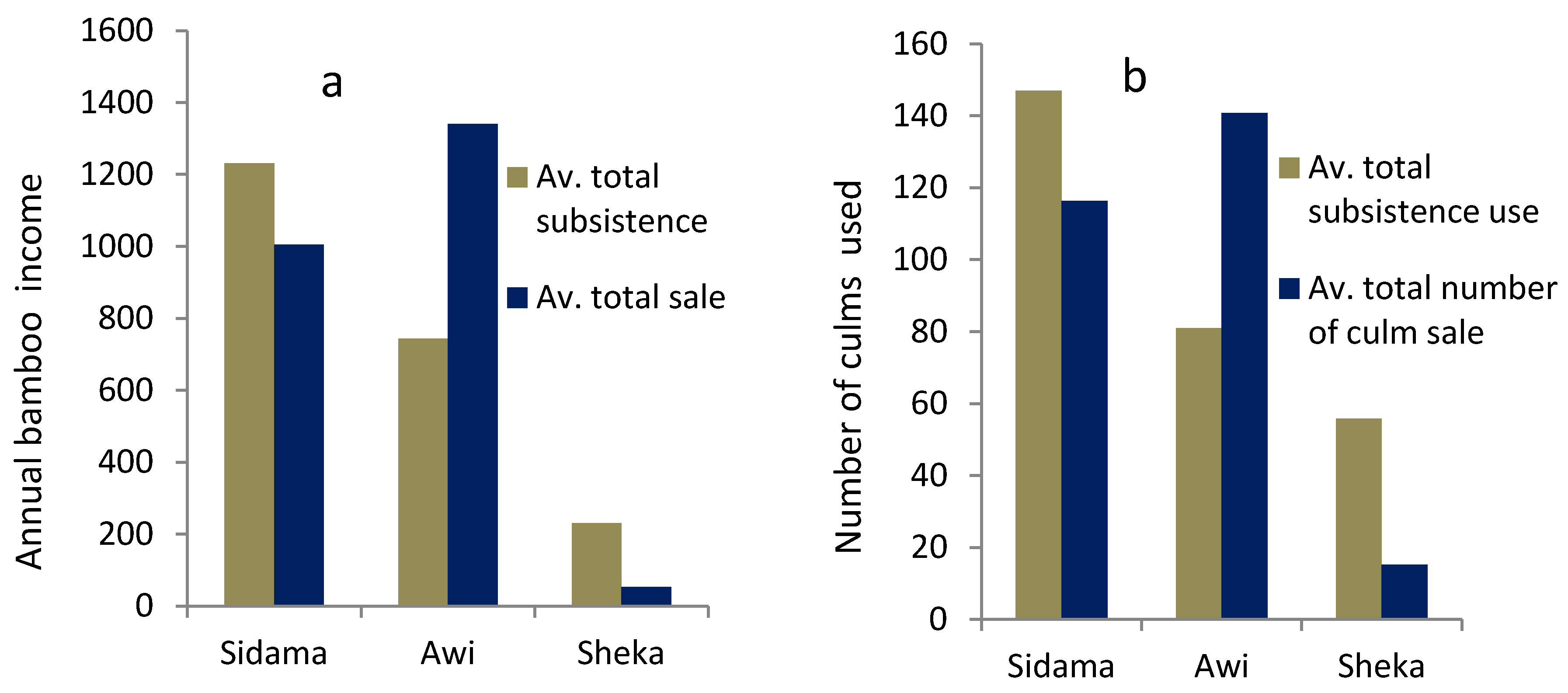

The average total income obtained from bamboo was 1534 birr (The exchange rate during data collection was 1 birr = $0.0572), of which 700 birr were obtained in cash and the remaining in subsistence form. Sidama households obtained the highest average total bamboo income of 2235 birr, followed by Awi with 2084 birr and Sheka with 284 birr (

Figure 2). In terms of cash income, Awi households obtained more than Sidama households. Of the average total annual income only 37.41% went to the market. However, regional differences were significant, reaching 60% in Awi and less than 10% in Masha. Moreover, of the traded volume, a good part of the trade was farmer-to-farmer; where about 20% from Sidama and 60% from Sheka ended with farmer-to-farmer transaction in trade and barter. Local trade in Awi was very limited.

Figure 2.

(a) Average total cash and subsistence income in birr; and (b) number of culms used for subsistence and sale, disaggregated by region.

Figure 2.

(a) Average total cash and subsistence income in birr; and (b) number of culms used for subsistence and sale, disaggregated by region.

In Awi, a relatively modest demand and encouraging market price was reported. Moreover, a large share of bamboo income was obtained in the form of cash (

Figure 2). It was reported that bamboo was the prime cash crop in this region. In contrast to Awi, Sheka farmers obtained majority of the bamboo income, which was smaller than that of the other two locales, in the form of subsistence. Despite relatively high total production in Sidama, cash income proportion was lower than in Awi. This difference was due to the high household consumption by producer-farmers in Sidama, which limited the amount supplied to the market (

Figure 2). Moreover, the price of culms was slightly lower in Sidama than in Awi.

Income varied among households from a minimum in Sheka to a maximum in Sidama. Both total and cash income of Sheka farmers were significantly different from those of Sidama and Awi farmers at 95% confidence. However, there was no difference between Sidamo and Awi at 95% confidence (

Table 2).

Table 2.

Variation in total bamboo consumption (in birr) and degree of commercialization in three Ethiopian study regions.

Table 2.

Variation in total bamboo consumption (in birr) and degree of commercialization in three Ethiopian study regions.

| Variables * | Sidama (

n = 43) | Awi (

n = 38) | Sheka (

n = 52) | Kruskal-Wallis ANOVA |

|---|

| Median | 25% | 75% | Median | 25% | 75% | Median | 25% | 75% |

|---|

| Cash income | 50 | 19 | 67 | 69 | 35 | 84 | 0 | 0 | 0 | ANOVA ranks | H = 45.56 | p < 0.001 |

| A | A | B | * Dunn’s multiple comparison | p < 0.05 | |

Total annual

income | 200 | 100 | 400 | 200 | 87.5 | 400 | 50 | 30 | 80 | ANOVA ranks | H = 29.95 | p < 0.001 |

| A | A | B | *Dunn’s multiple comparison | p < 0.05 | |

| Price per pole | 8 | 7 | 10 | 10 | 8 | 11 | 4 | 3 | 5 | ANOVA ranks | H = 86.75 | p < 0.001 |

| A | A | B | *Dunn’s multiple comparison | p < 0.05 | |

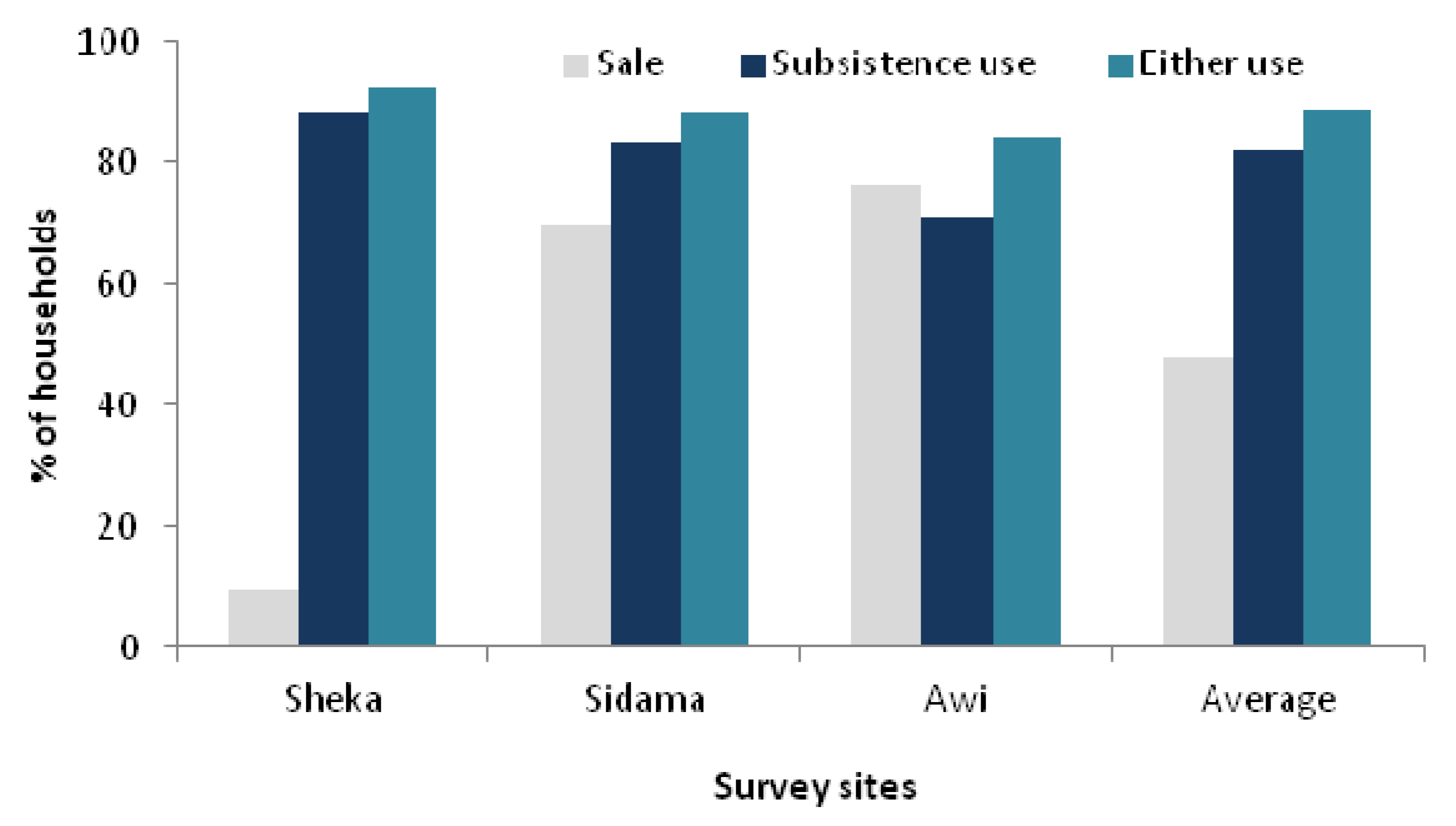

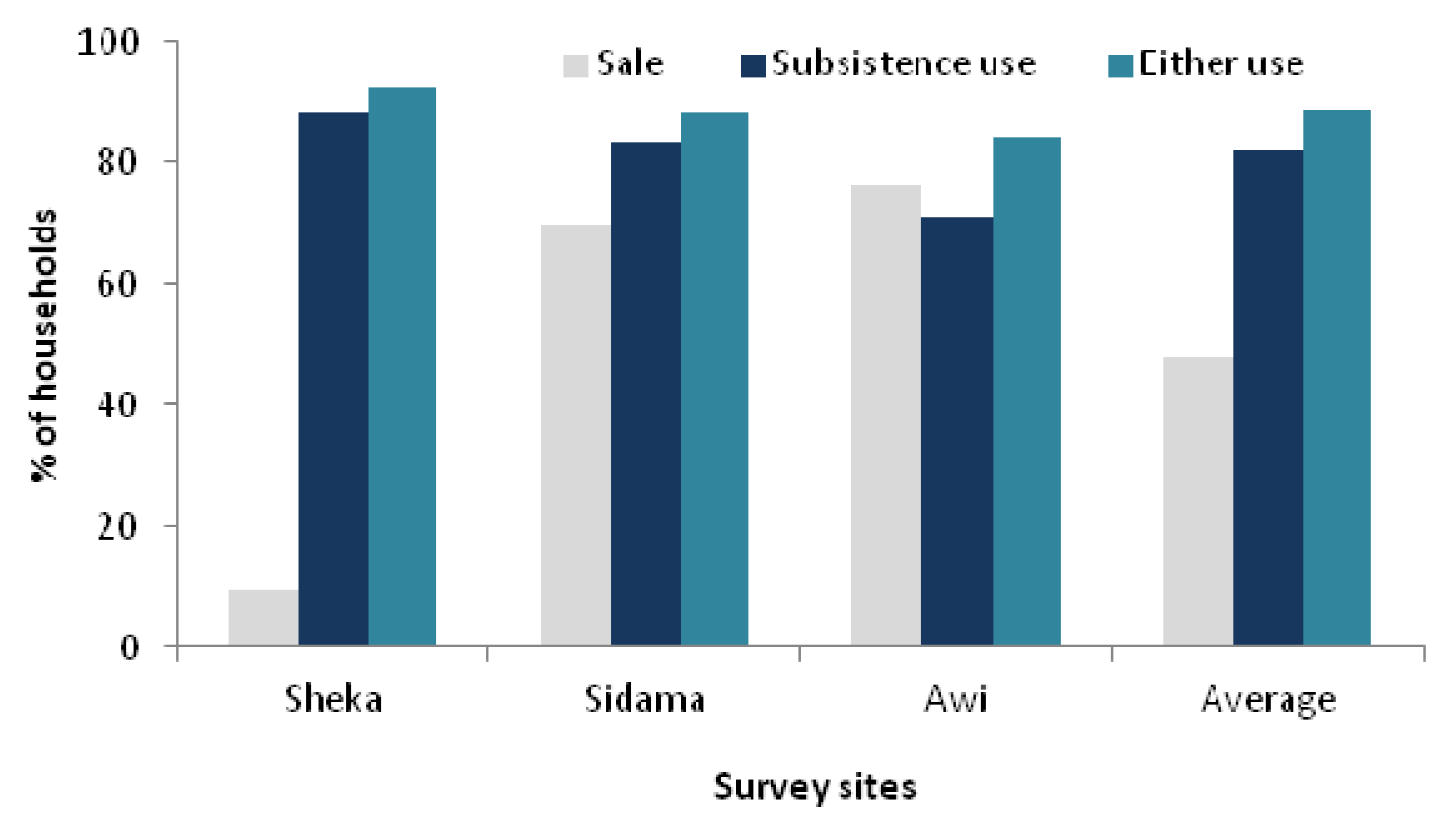

During the survey year, 90% of the interviewees from Sheka, 30% from Sidama, and 24% from Awi did not sell bamboo (

Figure 3).

Figure 3 further shows that there was no major difference between the three regions in terms of numbers of households using bamboo for subsistence purpose.

Figure 3.

Percentage of annual bamboo utilization by households in the districts.

Figure 3.

Percentage of annual bamboo utilization by households in the districts.

Within Sheka, further comparison of bamboo cash income relative to other livelihood sources revealed that it was the least commercialized product compared with cereal crops (14.1%), honey (85.4%), and spices (81%), where figures represent proportions of income obtained in cash. Consequently, the average total cash income of households was also higher than the average cash income from bamboo. Obviously, no tree species including bamboo were mentioned as important sources of cash income in this district.

3.3. Bamboo Value Chain

3.3.1. Production and Transportation

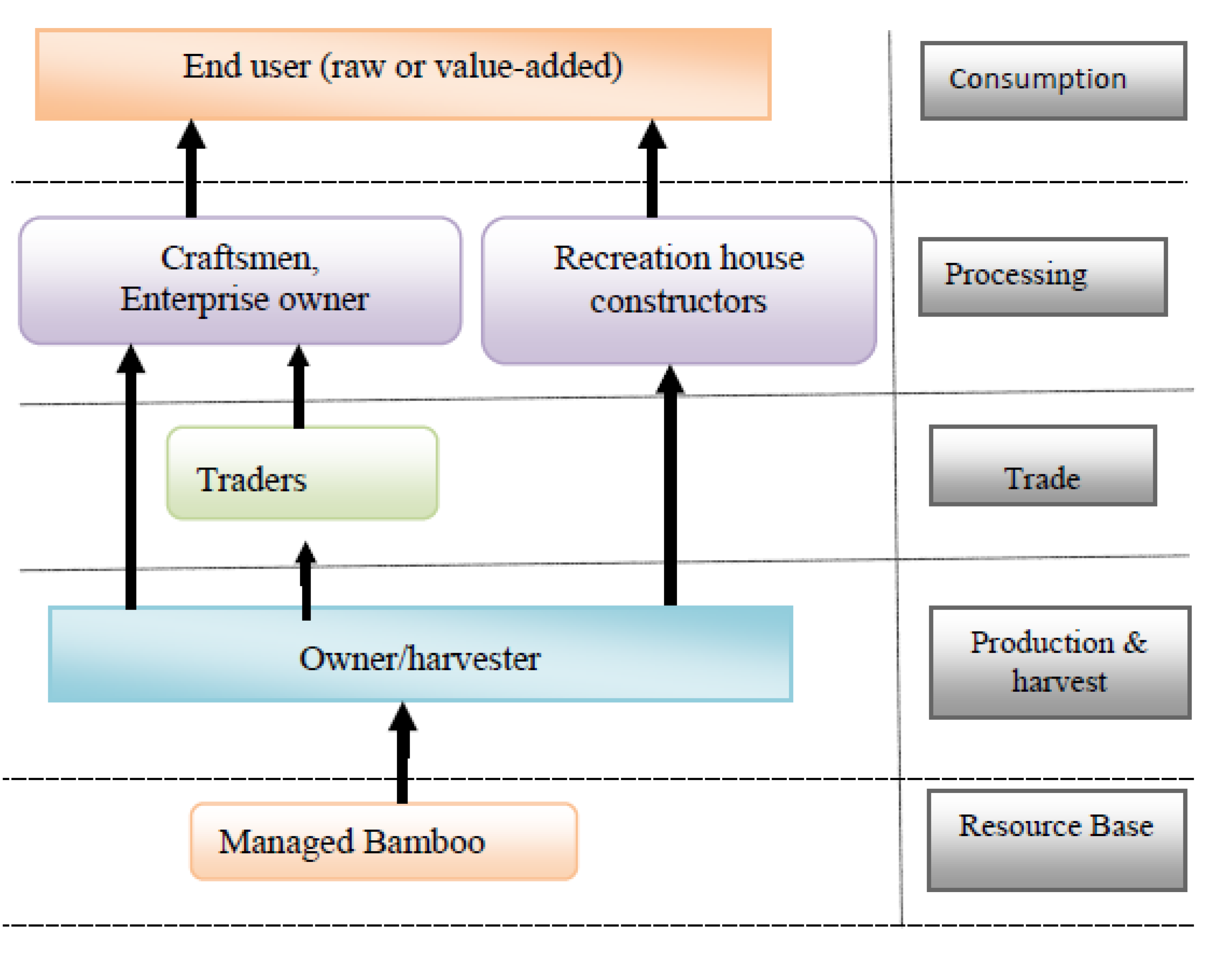

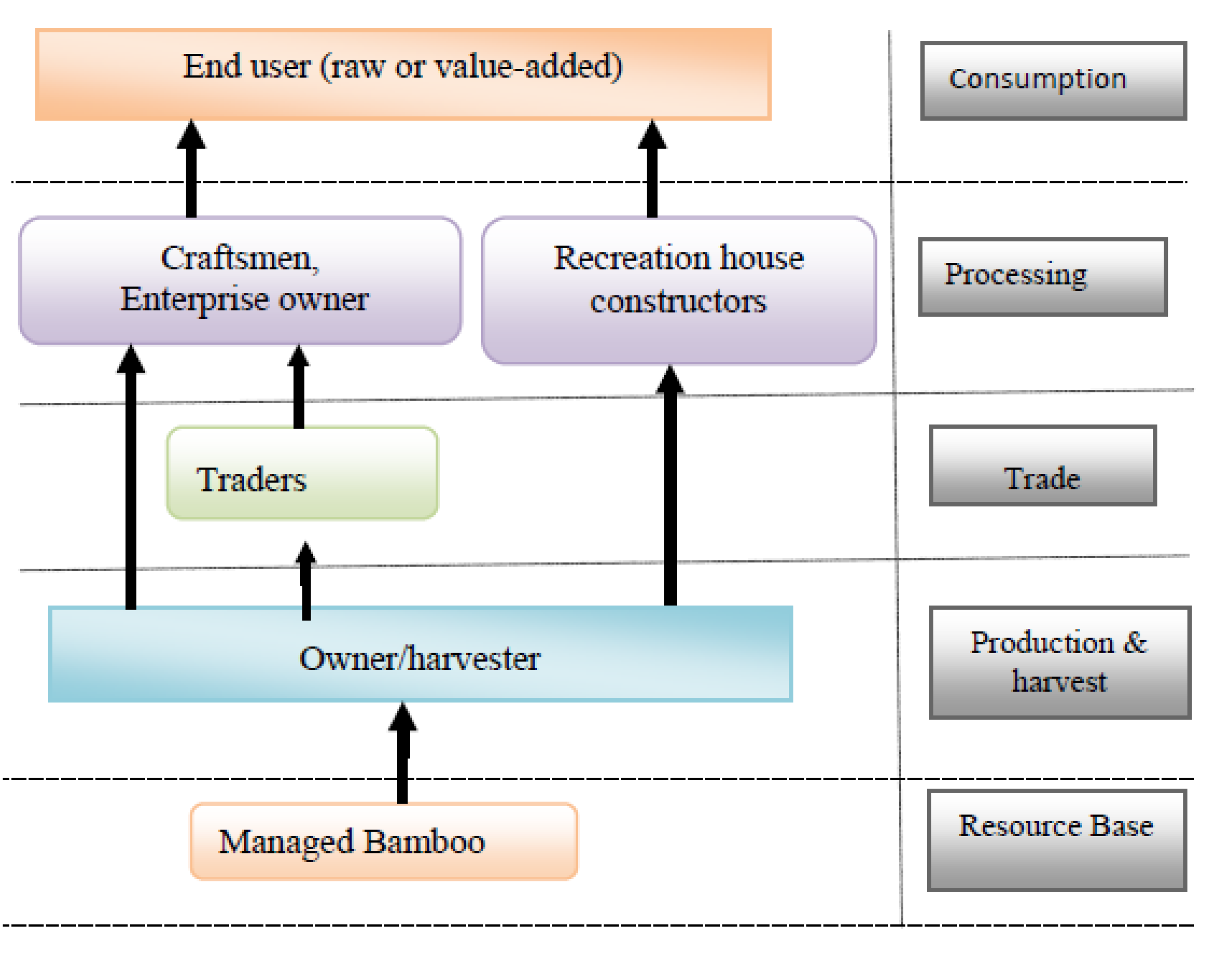

The bamboo value chain starts in culm production areas: the natural bamboo forest in Sheka and managed bamboos in Awi and Sidama. Farmers are the major actors as producers and harvesters. They harvest bamboo for their own consumption, for sale, or for bartering. Buyers also prefer to harvest bamboo culms by themselves directly from bamboo lots so that they can select mature and high-quality culms. However, farmers do not allow harvesting by buyers, claiming that they damage the stumpage value due to irresponsible harvesting practices. Major buyers of harvested culms were farmers, bamboo traders, bamboo craftsmen, and recreational house builders. Transactions were conducted at farm gates, roadsides, or local markets. Prices were fixed by negotiation between harvesters and buyers.

Culms are transported by four major actors: bamboo owners/harvesters, processors, traders, and tourist house constructors. Bamboo owners or, as in the case of Sheka, the collectors transport culms to nearby marketing centers. From marketing centers, processors transport the product to the processing cities. These same processors also travel deep inside the production area and collect products from the bamboo forest. Likewise, bamboo culms can also be transported by traders from production centers or local markets to their bamboo yards in the cities or directly to craft shops. Finally, bamboo recreational house construction companies or tourist house owners transport culms directly from the production area to the construction site. The means of transport are trucks.

3.3.2. Processing and Consumption

Processing of bamboo takes place both in the rural areas and in the urban selling center. Most households that own bamboo, process it to produce basic household utilities such as furniture, utensils, and equipment for consumption by the processors and their extended family members. Only some products (furniture and mats from Awi, mats from Sidama) are processed and traded. Most commercial processing takes place in urban areas with the largest concentration in the national capital, but regional capitals such as Hawassa and Bahir Dar each have more than 20 registered and unregistered processors who primarily produce furniture using traditional tools and equipments.

Processors have often developed skills through internships with other processors and/or formal training provided by different non-governmental organizations (NGOs). They usually produce products upon request from buyers. Most processors sell their products at centers of production, having no separate display and selling centers. Consumers are diverse, ranging from buyers interested in cheap products to buyers interested in relatively high-quality products combining traditional craft with modern furniture designs. In response to this demand, processors produce different types and quality-class products.

3.3.3. Value Chain Patterns and Relationships

The bamboo value chain from Awi was found to be relatively longer and more complex, following several forms and routes than bamboo originating from other areas of the country. The following describes the more common pattern: (i) culms are processed by farmers or by microenterprises in Ingebara for sale at the roadside or in the local market; (ii) raw culms are transported by traders to Addis Ababa and Bahir Dar to be processed by microenterprises or used for the construction of tourist houses; (iii) farmers produce traditional value-added products in Awi and transport the products themselves to Addis Ababa, Bahir Dar, Gondar and Mekele, Nekemt, Harar, and other cities to be purchased by traders and tourists; (vi) processors (craftsmen) from Awi travel to the above places to produce value-added products and sell them in a place where they temporarily reside, and then continue moving, following market demand; (v) processors from Awi are invited by urban bamboo product traders to cities and are paid on the basis of the number and type of value-added products they have produced.

Similarly, the bamboo value chain from Sidama follows the following pattern between production areas and consumption cities: (i) raw bamboo culms, low-grade mats, basketry, and handicraft products are processed in rural Sidama and bought by traders and consumers and transported to Hawassa, Addis Ababa, and other nearby cities; (ii) skilled farmers who design and construct Sidama houses travel to construction centers to assist constructors with selection of quality culms, construction of houses, and traditional insect pest treatment; (iii) private and organized bamboo processing associations producing bamboo furniture and craft products in Hawassa and Hula are dependent exclusively on Sidama bamboo and sell their products to consumers in the respective towns.

Thus, the Awi and Sidama farmers are involved in production, processing, trade, and technology transfer from rural to urban areas. The Sidama farmers tend to specialize in recreational area constructions, whereas the Awi farmers are well known for their furniture and bamboo-based decorations. Despite differences in specialization and volume of trade, the relationships and structures of the value chains originating in the two regions is more or less similar, as shown in

Figure 4.

Figure 4.

Typical value chain structure from Awi and Sidama.

Figure 4.

Typical value chain structure from Awi and Sidama.

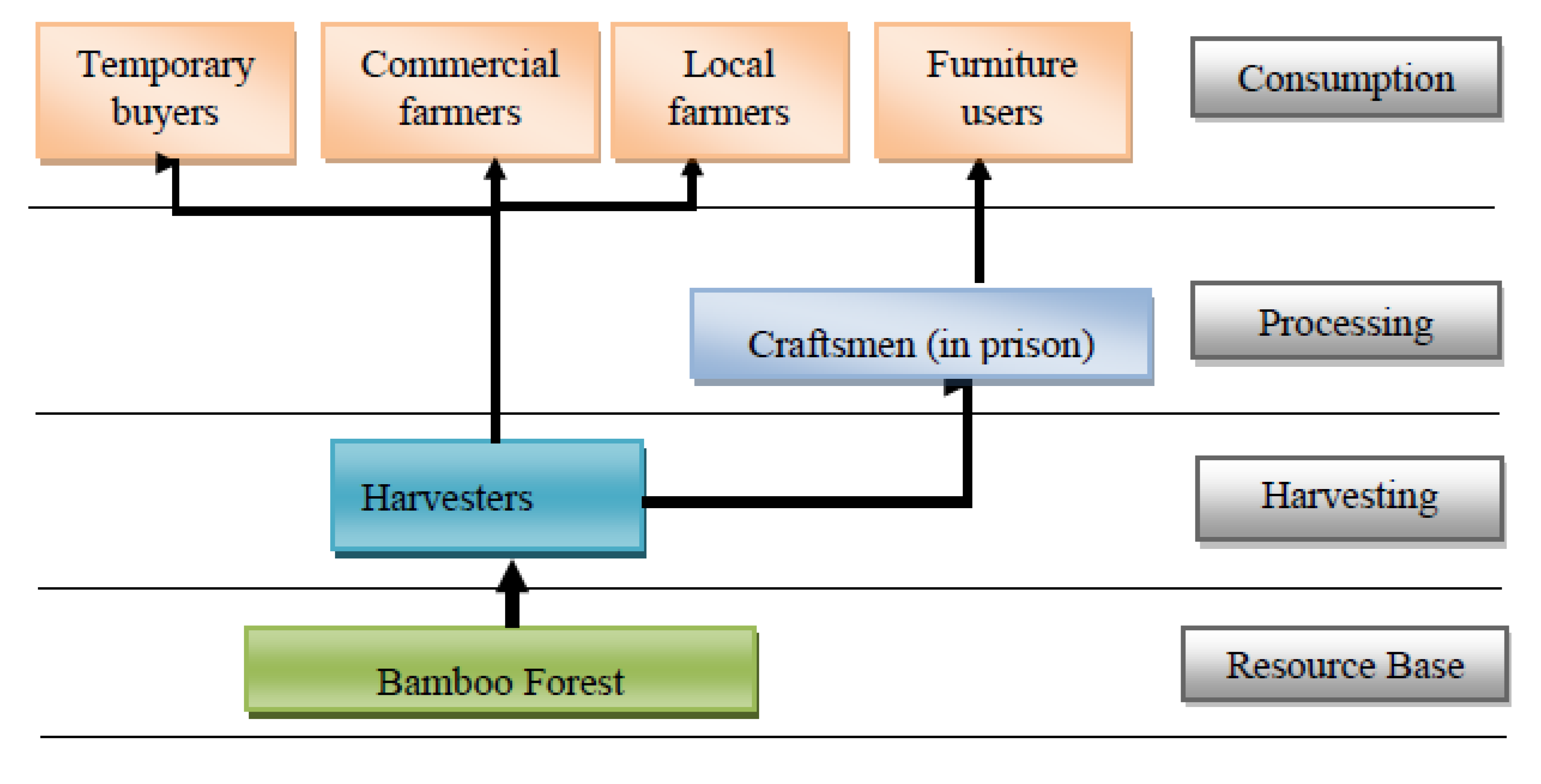

Sheka has the shortest value chain relationships of all the regions studied. In all of the chains except one, only harvesters and consumers were involved (

Figure 5). The longest chain relationship from Sheka was reported when a firm (the local prison) bought culms from collectors at roadsides to process them into furniture, which was sold to Masha city dwellers. The majority of the harvested bamboo was consumed by harvesters themselves. The remaining was sold to neighboring farmers, residents of Masha town, local prison, and private farm investors who use the culms for low-quality building structures, and supporting stakes for weak-stemmed fruits. Some were bought and transported to Gambella by the United Nations to construct temporary refugee houses. In all the transactions in Sheka, prices were fixed by buyers.

Figure 5.

Typical value chain structure from Sheka.

Figure 5.

Typical value chain structure from Sheka.

3.4. Causal Factors for Differential Levels of Bamboo Commercialization

A best subset regression analysis showed that the dependent variable “degree of commercialization” showed a significant and negative correlation with the distance to the market and a significant and positive correlation with management labor and management type (

Table 3). Of these variables, distance to the market was the strongest explanatory factor. Management labor and type were also significantly correlated with degree of commercialization. Other variables such as age, education, family size, distance to road, and gender were excluded because they were not correlated with degree of commercialization.

Table 3.

Factors significantly affecting bamboo commercialization in three Ethiopian sites (R² = 0.39, p < 0.05).

Table 3.

Factors significantly affecting bamboo commercialization in three Ethiopian sites (R² = 0.39, p < 0.05).

| Variable | Coefficient | Standard error | t | p |

|---|

| Constant | −294.2 | 121.72 | −2.42 | 0.017 |

| Distance to market | −0.84 | 0.23 | −3.02 | 0.003 |

| Management labor | 3.94 | 1.51 | 2.6 | 0.01 |

| Management type | 446.416 | 158.37 | 2.82 | 0.006 |

Separate regression analyses were also performed for each site to identify site-specific factors. No other significant influential factors were found for Awi and Sidama. However, in Sheka education level, family size, and training attendance positively and significantly affected commercialization (

Table 4).

Interviews with processors in Addis Ababa and Hawassa showed that despite ample resources in Sheka, it was not listed as a source of raw material by any of the interviewees. Their reason for not choosing Sheka as a raw material source was its remoteness and poor road conditions. Interviewees stated that they had no incentive to travel over long distance on poor roads when they could obtain sufficient raw materials from nearby areas with cheaper transportation costs. For this reason, Sheka has little share in the small but growing regional and national markets of the country. Our study further revealed that regional towns in southwest Ethiopia were not only small with limited service facilities and demand for bamboo resources, but they preferred to use and have relatively ample tropical hardwood timber for construction and furniture.

Table 4.

Factors significantly affecting bamboo commercialization in Sheka (R² = 0.29, p < 0.05).

Table 4.

Factors significantly affecting bamboo commercialization in Sheka (R² = 0.29, p < 0.05).

| Variable | Coefficient | Standard error | t | p |

|---|

| Constant | −39.06 | 17.44 | −7.44 | 0.03 |

| Education | 2.55 | 1.27 | 2.01 | 0.05 |

| Family size | 5.11 | 2.0 | 2.55 | 0.014 |

| Training | 99.2 | 25.7 | 3.86 | >0.001 |

In contrast, bamboo and its value-added products from Sidama and Awi either capture market share in local cities or are easily transported to Addis Ababa, the city that hosts the majority of bamboo-processing micro and family enterprises of Ethiopia. The pioneer medium-sized bamboo-manufacturing enterprise is also located in Addis Ababa. As a result, demand for bamboo culms is high in the capital. Although culms can be obtained from many other locations, Awi and Sidama were the second and third major sources of raw materials, respectively. Guragie was ranked first, owing to its relative proximity and better road access to the city. In terms of resources, these three regions together contribute only approximately 5%, compared with Sheka and its vicinity, which contribute approximately 20% of estimated highland bamboo resources.

The other factor that contributed to the disparities was the absence of bamboo technology development training and extension. The Federal Micro and Small Enterprise Development Agency (FEMSEDA), one of the major small and medium enterprise (SME) development and training government organizations, has provided several rounds of capacity building training in the country. Farmers from Awi and Sidama were frequent participants, whereas no training has been provided for Sheka farmers. NGOs and parastatal bamboo development projects have recently been operating in the country, but only one NGO has incorporated Sheka in its project. This NGO has offered training specifically in bamboo conservation and not in bamboo commercialization. This example demonstrates the large unequal access to technical training and market information among the districts.

4. Discussion

4.1. Management Systems and Commercialization

A domesticated production system is often preferred to afford a sustainable and adequate source of raw material with desired quality. As confirmed by earlier studies [

6,

40], successful commercialization of tree products depends on the domestication of product sources and the production system so as to ensure that supply can keep up with the growing demand of a developing market to overcome quality variability, uneven flow of raw material supply, inferior quality, and to stimulate local value addition [

7,

17,

41]. The Ethiopian bamboo production shows a similar pattern, where bamboo originating from domesticated systems such as in Sidama and Awi is more commercialized than the resources obtained from the remote, open-access bamboo forests of Sheka. This difference may be due to the incentivization of management investments by a comparatively higher income and presence of sufficient buyers. In contrast, in a place such as Sheka where markets are intermittent and prices are low owing to various factors described above, producers are discouraged from investing in management and trade. This observation is in line with Schippmann [

42], who states that economic feasibility is the main rationale for a decision to bring a species into domestic production. Producers decide to engage in domestic cultivation whenever there is an economic advantage relative to wild harvesting. Likewise, plant domestication is a market-led, farmer-driven process in which commercialization is the incentive for management of trees [

11,

43].

4.2. Cash Income and Income Ratios

This study showed that the cash income contribution of bamboo ranges from 9.48% in Sheka to 60% in Awi with an average value at 37.41%. This range shows that bamboo is less commercialized compared with other regions or products: for instance 93% for bamboo from Guanxi, China [

31] and 51% for

Adansonia digitata fruit products from Sudan [

44]. Compared with other livelihood products in Sheka, total and cash income contributions of bamboo were found to be lower than those of the major livelihood products such as crop and livestock productions. They were also lower than that reported for forest products from southeastern Ethiopia [

45].

The result further revealed that products such as livestock that have adequate local markets, as well as honey and spices, which have high value-to-weight ratios, tend to provide higher cash incomes than crop and forest products. This finding may imply that the remoteness of the region has less effect on products with a higher local demand and on those with higher price-to-weight ratios. Given the lower price-to-weight ratio and limited local preference for bamboo, it is unlikely that this product will fetch higher cash income under the existing infrastructural conditions.

The study reveals that lower prices for bamboo culms in Sheka have resulted in reduced contributions of bamboo to household income, further widening the difference between Sheka and other regions. Culm consumption in Sheka was three times lower than that in Awi and incomes were sevenfold lower. Thus, limited market integration resulting from remoteness and poor road conditions combined with other socioeconomic factors have led to reduced cash incomes and reduced overall contribution of bamboo to households in Sheka. In contrast, despite the relatively greater distance of Awi from Addis Ababa than from Sidama, higher prices and income-to-volume ratios in Awi imply that local value addition practices in Awi contributed to the differences. Therefore, limited value addition practices at the producer level not only kept prices low but also led to a reduced total income from the sector.

4.3. Value Chain System

Our results describing the functioning and structure of the bamboo value chains have shown a predominance of direct producer–consumer transactions, which exclude most intermediate actors. These features are similar to those of the medicinal plant trade reported by Booker

et al. [

43]. Low price of bamboo or bamboo products at the consumer level, which in turn could be the result of low value addition to bamboo products might have attributed for this weak value chain network. The price of value-added products is reported as small and is a mere summation of farm-gate price, labor and transportation costs. Higher prices, which lead to a higher cost for the consumer, may lead to the substitution of bamboo with other products, and correspondingly fewer opportunities to accommodate a large number of culm traders or brokers under the current level of consumer demand for bamboo products. In response to the low return and unstable demand and supply features, the bamboo trade is conducted in combination with other businesses and is often used as a stepping-stone to move to other sectors. These tendencies reduce the commercial development of the sector, in agreement with the analysis of Braun

et al. [

19], who assert that commercialization is the outcome of profit-based decision making behavior in the value chain.

It was observed that the market was the major governance feature in Awi and Sidama. In contrast, the functioning of the value chain from Masha was governed largely by buyers who were in a better position due to excess supply and few competitors. This observation is in agreement with the governance features discussed by Gereffi

et al. [

46]. In contrast with previous studies on extractive value chains [

1,

47], producers in the bamboo value chain of Awi and Sidama have a competitive position for negotiating prices. This advantage may be due to the awareness of farmers in these regions of the increasing demand and the presence of sufficient numbers of alternative buyers. Farmers sometimes even have exaggerated information regarding current prices of bamboo in the cities.

4.4. Determinants of Commercialization

Distance to major market centers is the most significant factor explaining the primary difference in commercialization among bamboo-producing regions. The distance and the quality of roads are identified as major deterrents for bamboo processors to buy culms from Sheka despite ample resources. The presence of a tourist destination, the high service-providing cities of Hawassa and Bahir Dar, complemented by a good-quality road network connecting the two cities to Addis Ababa, the capital, has increased the demand for bamboo and bamboo products in Sidama and Awi compared with Masha. This finding agrees with earlier findings that cities and associated urban functions stimulate product and service commercialization [

15,

48,

49]. Moreover, distance is the most pronounced factor for products with high weight-price ratios and perishable products. Thus, total culm price, which is a function of raw material and associated transportation costs to processing cities, has a direct influence on the choice of raw material source by bamboo-processing enterprises. The results also showed that management intensity was positively correlated with the degree of commercialization. However, the dependency was two-way; a situation called by Leakey [

50] the chicken and egg situation of domestication and commercialization.

Although commercialization differences among regions were not dictated by household characteristics and local factors such as age, education, income, gender, biophysical conditions, and related issues, some of them showed significant differences in bamboo trade engagement among Sheka households. Farmers who engaged in commercial harvesting were better educated and had access to market information. Better education often means denser networks in urban areas and more exposure to media based information. Such operators are less affected by local taboos that dictate that the selling of forest products belongs to poor households and marginalized groups. Thus, their knowledge and information positioning may help them to tap into meager market opportunities available in the regions. Large family size is probably a factor owing to the presence of sufficient labor to transport bamboo culms from distant forests, required in excess for household consumption, and such families may be motivated to sell what is left from their own consumption.

In the Awi and Sidama, given that the bamboo trade has operated for a long time, every household has sufficient information regarding marketing opportunities. Moreover, buyers travel house-to-house to purchase quality culms, and thereby promote market knowledge and information. They have also received repeated training, as explained above. Exposure to training may also increase their knowledge of bamboo utilization beyond traditional approaches. Unequal access to capacity development and marketing training among the study districts may also have contributed to the differential levels of commercialization. This hypothesis was in agreement with a previous study by teVelde [

18] comparing different NTFP commercialization in Mexico and Bolivia and another study comparing bamboo-growing villages in a remote region of China [

25].

5. Conclusions

This study shows that higher management intensity, integration in the value chain, and presence of marketing and knowledge infrastructure results in a higher rate of commercialization and correspondingly higher cash and total income from bamboo. The study reveals that the proportion of commercial use of bamboo is roughly a third of total consumption. However, micro differences are evident, reaching up to 60% in Awi and only 9.48% in Sheka. Moreover, despite the fact that the largest resource of the country is the natural bamboo forest, the majority of bamboo trade is dependent on managed bamboo resources. Consequently, the bamboo value chains originating from Awi and Sidama are longer and denser than that from Sheka, where only direct harvester and consumer transactions prevail. Moreover, some bamboo producers from Awi and Sidama are vertically integrated in the value chain as they are involved in processing and trade.

Commercial differences among regions are largely explained by distance to bamboo-processing and -marketing centers and abundance of preferred bamboo substituting materials. Another key finding, specifically from Sheka, is that higher educational attainment, attendance of training in bamboo, and large family size lead to a higher engagement in commercial harvesting and trade of bamboo. Thus, access to education and training together with the presence of sufficient labor to collect bamboo from forests may stimulate bamboo commercialization in the region. However, to further improve access to bamboo resource in the region by processors and traders from larger market centers, a better road network is crucial. Understanding of local differences in small-scale bamboo commercialization and the factors contributing to it can be used as a basis for further investigation of the pathways for the broader development of the bamboo value chain in Ethiopia.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}