Encouraging Environmentally Friendlier Cars via Fiscal Measures: General Methodology and Application to Belgium

Abstract

:1. Introduction

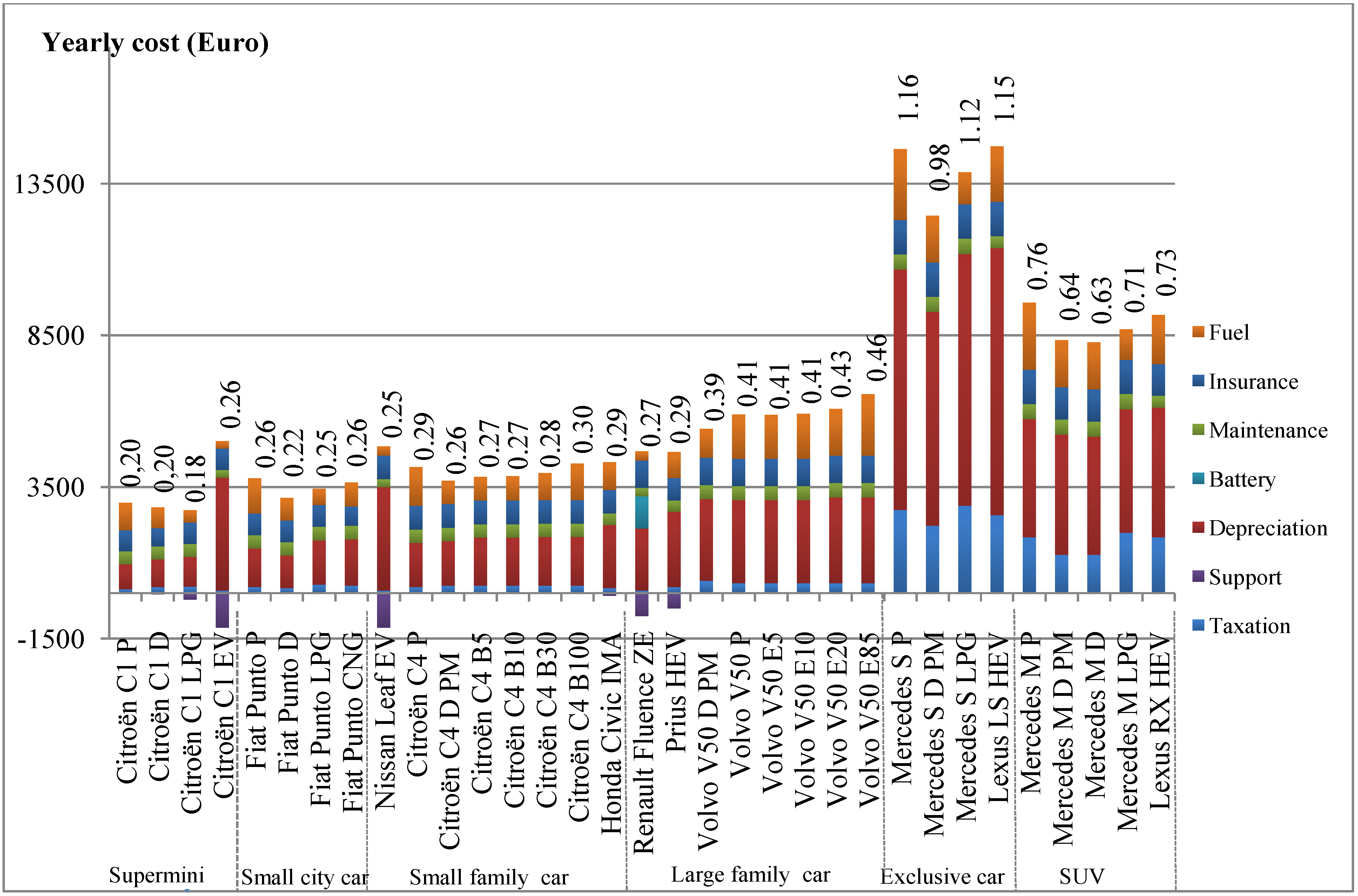

2. Life Cycle Cost Analysis

2.1. Methodology

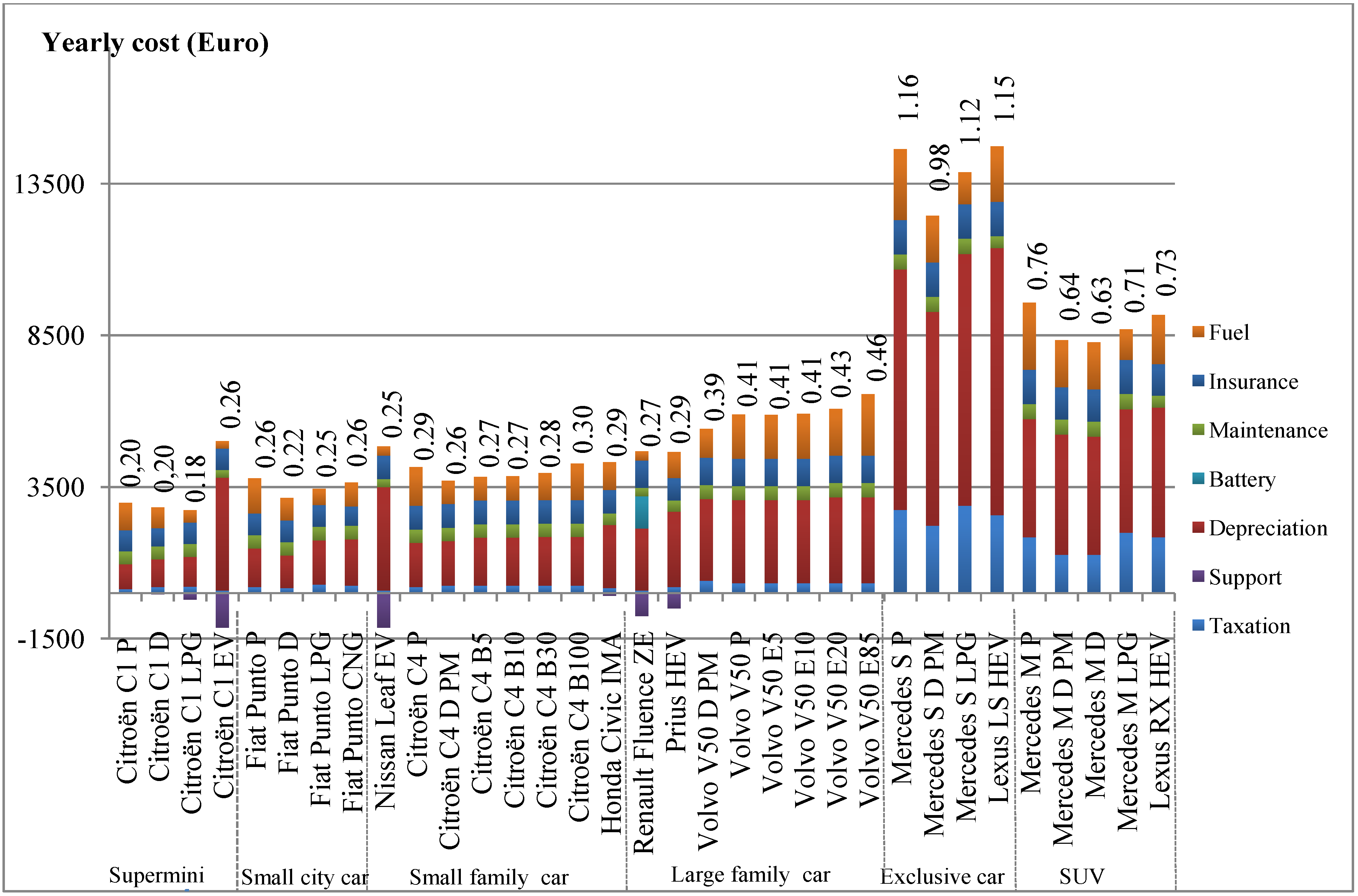

| Vehicle type | Make/model | Fuel | Purchase price (€) | VRT (€) | ACT (€/year) | Fuel consumption (l/100 km; m3/km; kWh/km) | Insurance (€/year) | Maintenance (€/year) |

|---|---|---|---|---|---|---|---|---|

| Supermini | Citroën C1 | P | 9,446 | 62 | 126 | 4.5 | 793 | 1,067 |

| Supermini | Citroën C1 | D | 11,896 | 62 | 204 | 4.1 | 680 | 1,067 |

| Supermini | Citroën C1 | LPG | 11,446 | 0 | 215 | 5.7 | 793 | 1,127 |

| Supermini | Citroën C1 | EV | 35,756 | 62 | 70 | 0.12 | 793 | 846 |

| Small city car | Fiat Punto | P | 14,720 | 62 | 204 | 5.8 | 804 | 1,074 |

| Small city car | Fiat Punto | D | 14,300 | 62 | 165 | 4.5 | 804 | 1,084 |

| Small city car | Fiat Punto | LPG | 14,560 | 0 | 254 | 7.4 | 804 | 1,144 |

| Small city car | Fiat Punto | CNG | 16,810 | 62 | 254 | 6.5 | 725 | 1,144 |

| Small family car | Nissan Leaf | EV | 32,829 | 62 | 70 | 0.15 | 881 | 941 |

| Small family car | Citroën C4 | P | 16,586 | 62 | 204 | 6.4 | 881 | 1,162 |

| Small family car | Citroën C4 | D PM | 18,286 | 123 | 243 | 4.7 | 881 | 1,162 |

| Small family car | Citroën C4 | B5 | 18,286 | 123 | 243 | 4.7 | 881 | 1,162 |

| Small family car | Citroën C4 | B10 | 18,286 | 123 | 243 | 4.8 | 881 | 1,162 |

| Small family car | Citroën C4 | B30 | 18,486 | 123 | 243 | 4.8 | 881 | 1,162 |

| Small family car | Citroën C4 | B100 | 18,486 | 123 | 243 | 5.2 | 881 | 1,162 |

| Small family car | Honda Civic IMA | HEV | 22,390 | 62 | 165 | 4.6 | 878 | 1,097 |

| Large family car | Renault Fluence | EV | 20,000 | 62 | 70 | 0.15 | 1021 | 1,036 |

| Large family car | Toyota Prius | HEV | 26,830 | 62 | 204 | 4.3 | 833 | 1,170 |

| Large family car | Volvo V50 | D PM | 33,050 | 495 | 373 | 5.7 | 1,021 | 1,275 |

| Large family car | Volvo V50 | P | 30,600 | 495 | 281 | 7.3 | 1,021 | 1,275 |

| Large family car | Volvo V50 | E5 | 30,600 | 495 | 281 | 7.5 | 1,021 | 1,275 |

| Large family car | Volvo V50 | E10 | 30,600 | 495 | 281 | 7.6 | 1,021 | 1,275 |

| Large family car | Volvo V50 | E20 | 31,600 | 495 | 281 | 7.9 | 1,021 | 1,275 |

| Large family car | Volvo V50 | E85 | 31,600 | 495 | 281 | 9.9 | 1,021 | 1,275 |

| Exclusive car | Mercedes S | P | 106,722 | 4,957 | 2,368 | 11.7 | 1,272 | 1,422 |

| Exclusive car | Mercedes S | D PM | 98,978 | 4,957 | 1,784 | 9.4 | 1,272 | 1,422 |

| Exclusive car | Mercedes S | LPG | 107,722 | 4,659 | 2,576 | 14.8 | 1,272 | 1,482 |

| Exclusive car | Lexus LS | HEV | 113,750 | 4,957 | 2,173 | 9.2 | 1,272 | 1,304 |

| SUV | Mercedes M | P | 57,354 | 4,957 | 1,351 | 11.1 | 1,272 | 1,422 |

| SUV | Mercedes M | D | 55,055 | 4,957 | 700 | 9.4 | 1,206 | 1,422 |

| SUV | Mercedes M | D PM | 55,781 | 4,957 | 700 | 9.4 | 1,206 | 1,422 |

| SUV | Mercedes M | LPG | 58,354 | 4,659 | 1,567 | 14.1 | 1,272 | 1,482 |

| SUV | Lexus RX | HEV | 61,180 | 4,957 | 1,351 | 8.1 | 1,172 | 1,304 |

2.1.1. Depreciation Costs

2.1.2. Insurance

2.1.3. Vehicle Taxes

2.1.4. Maintenance Costs

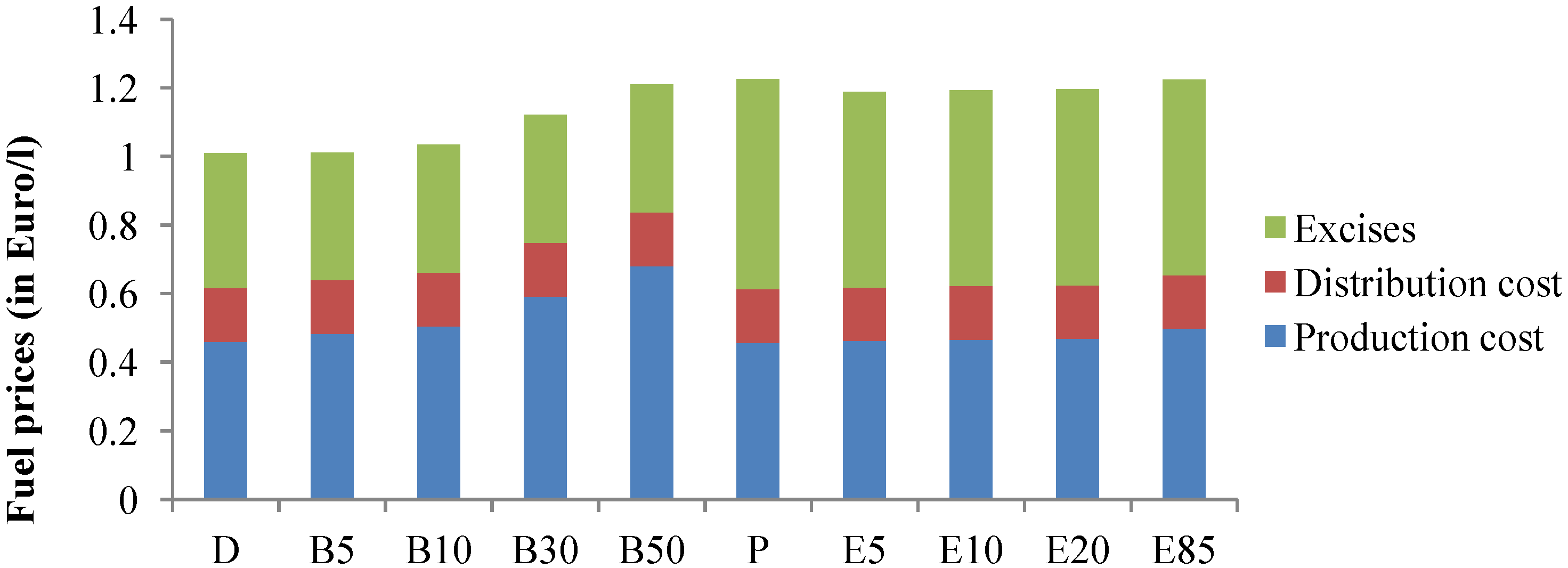

2.1.5. Fuel Costs

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

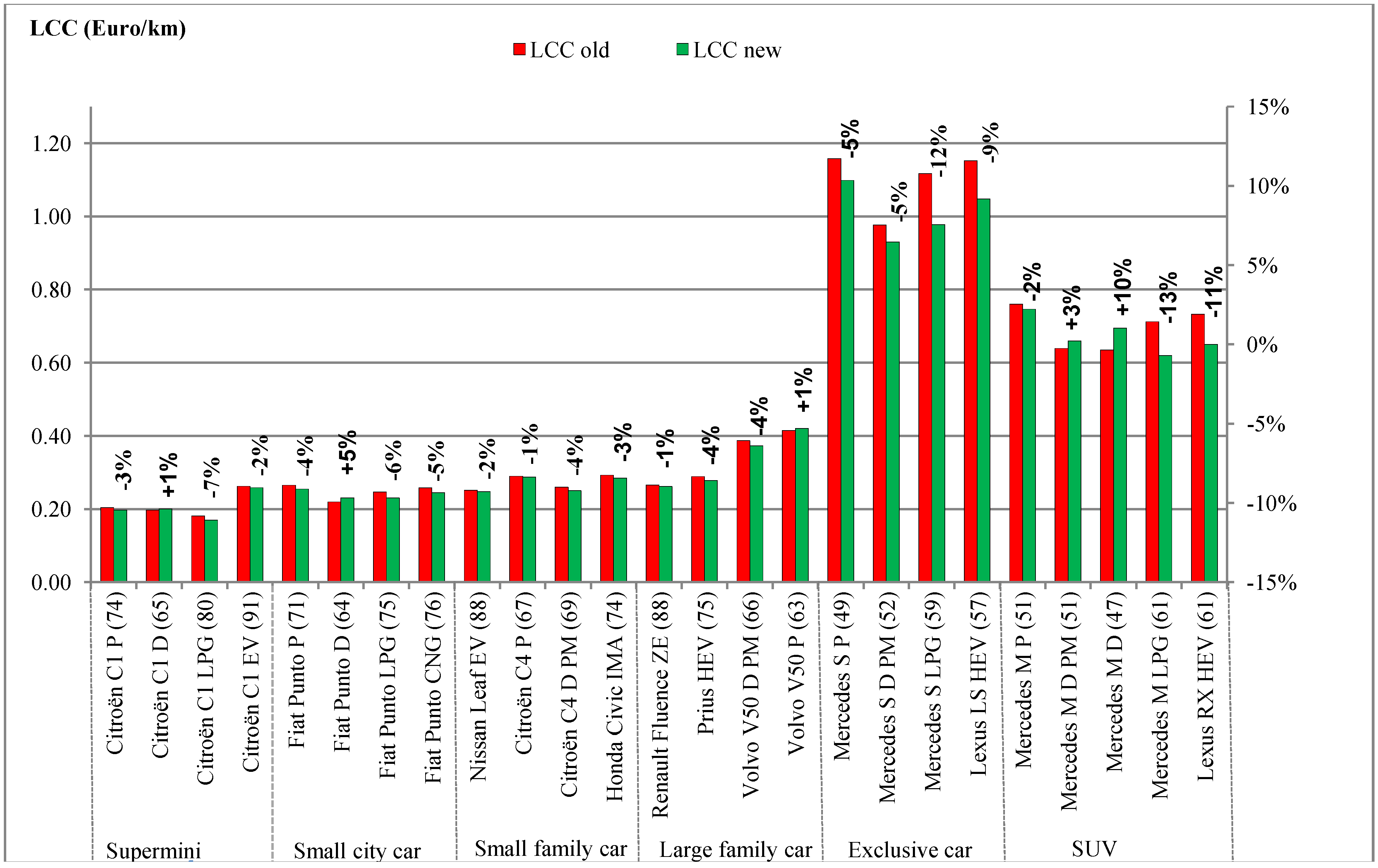

2.2. Results

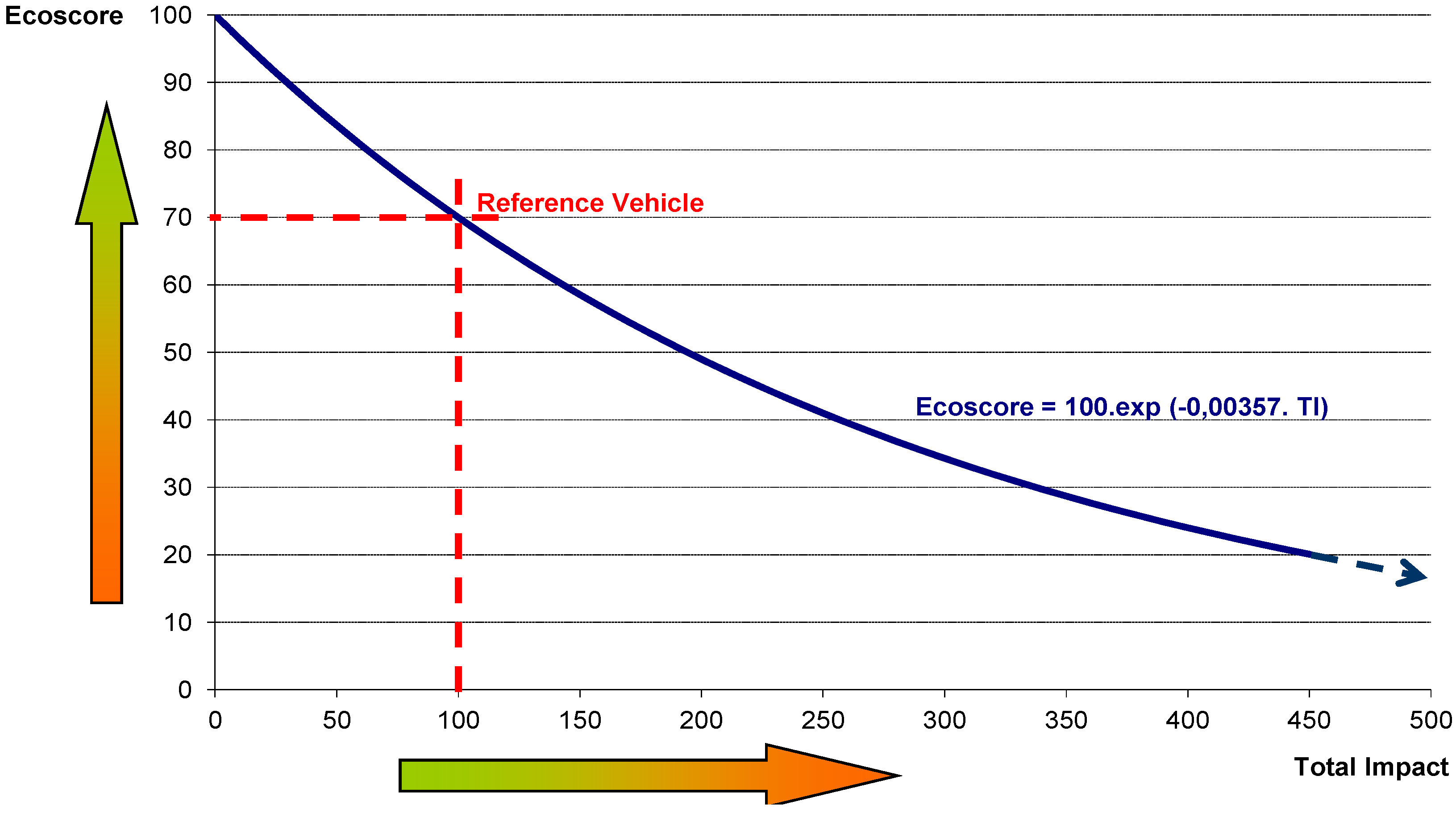

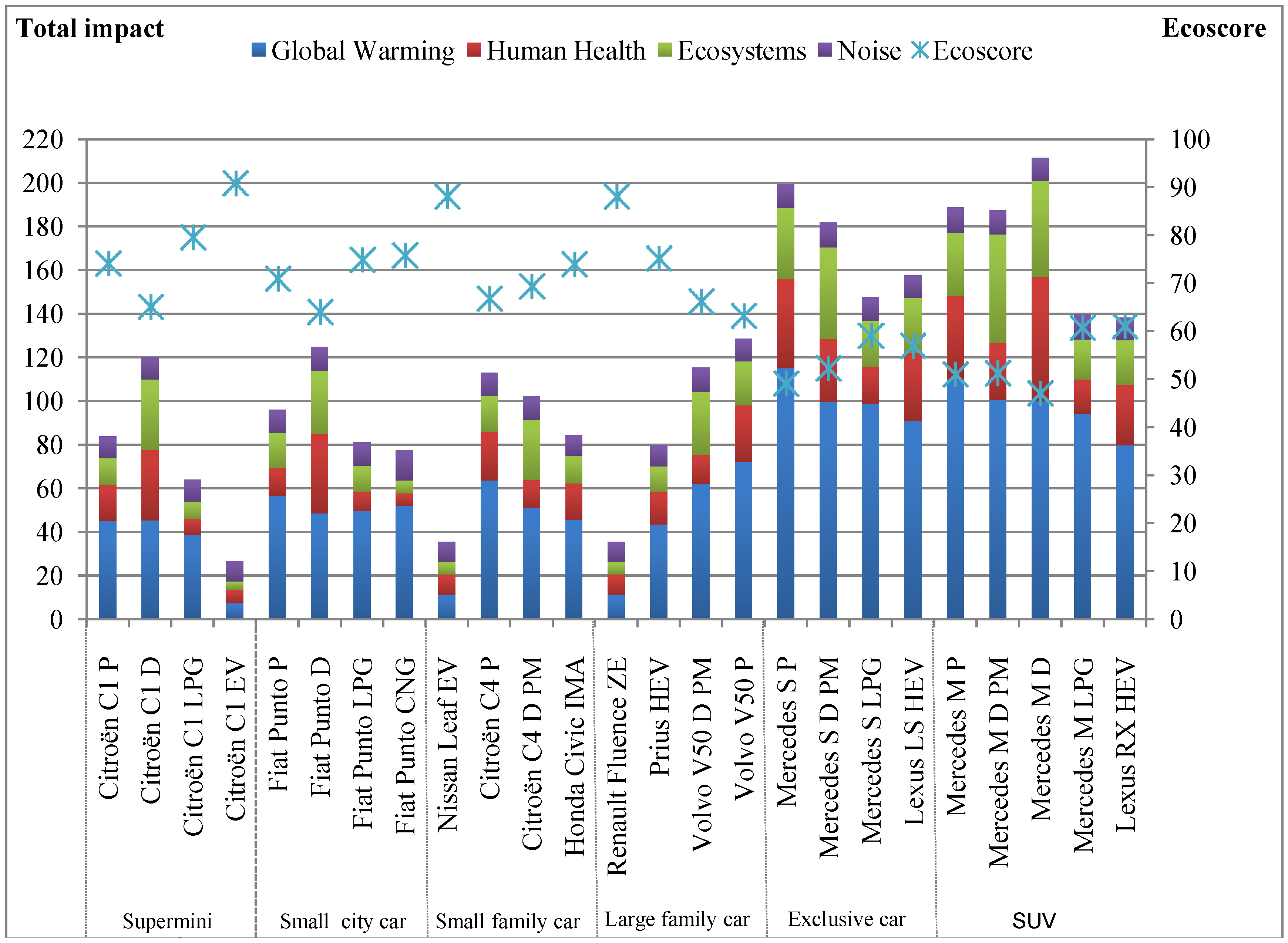

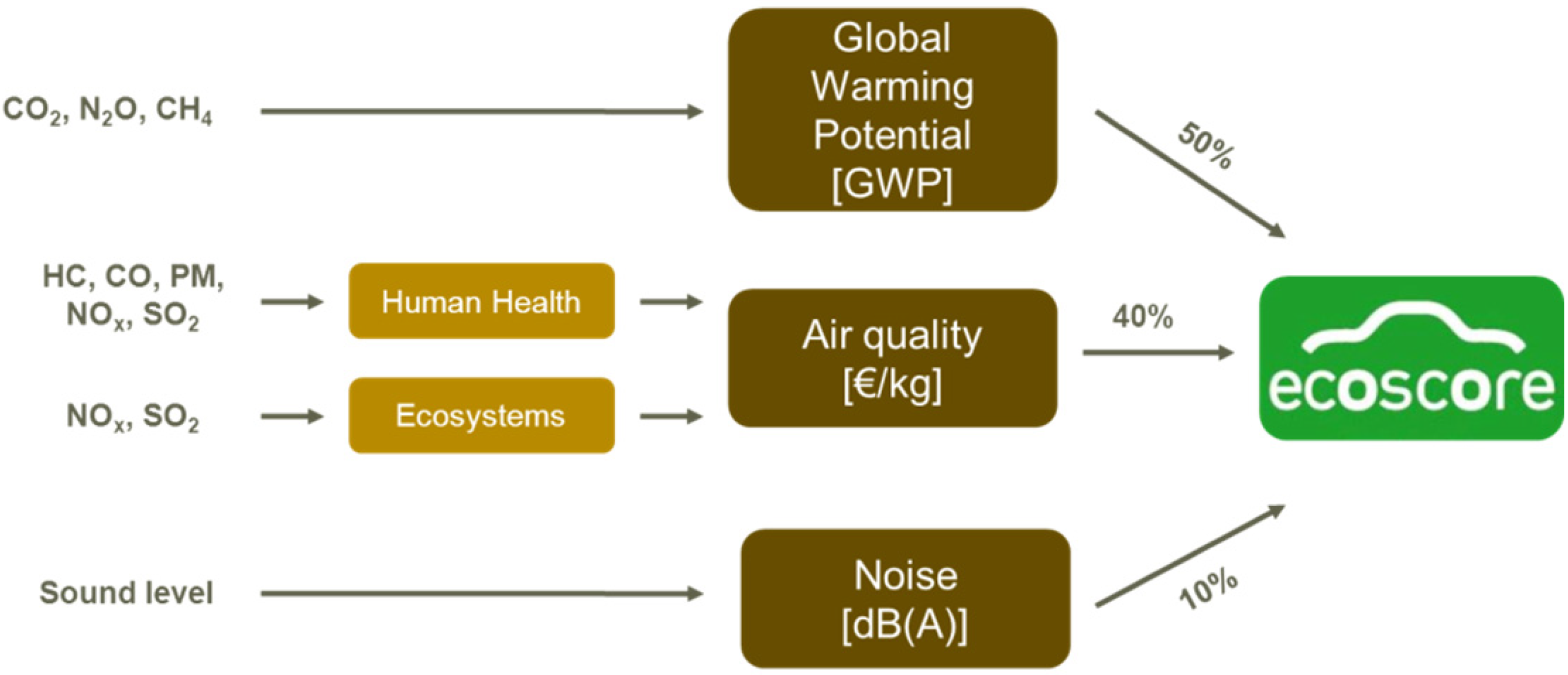

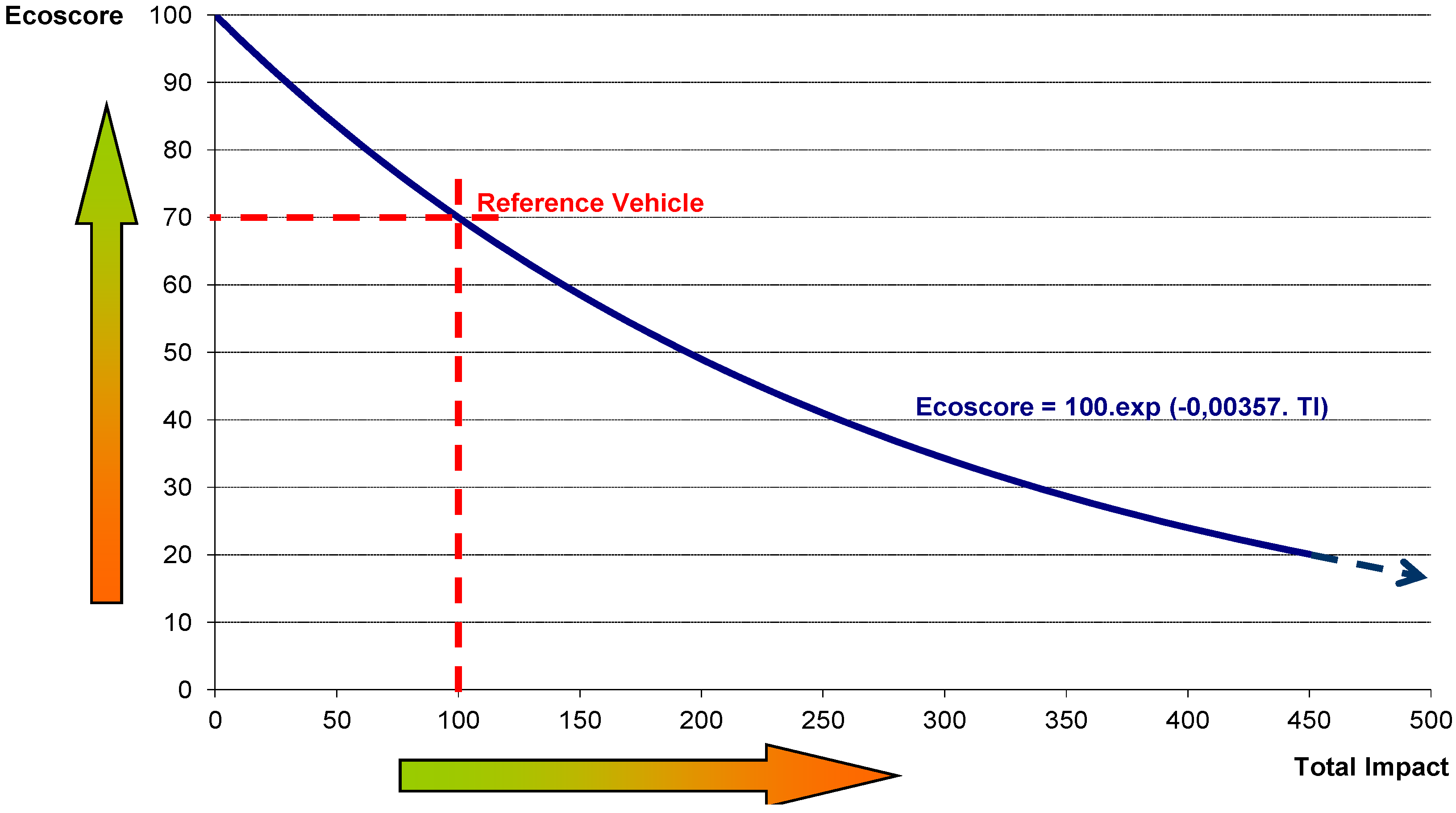

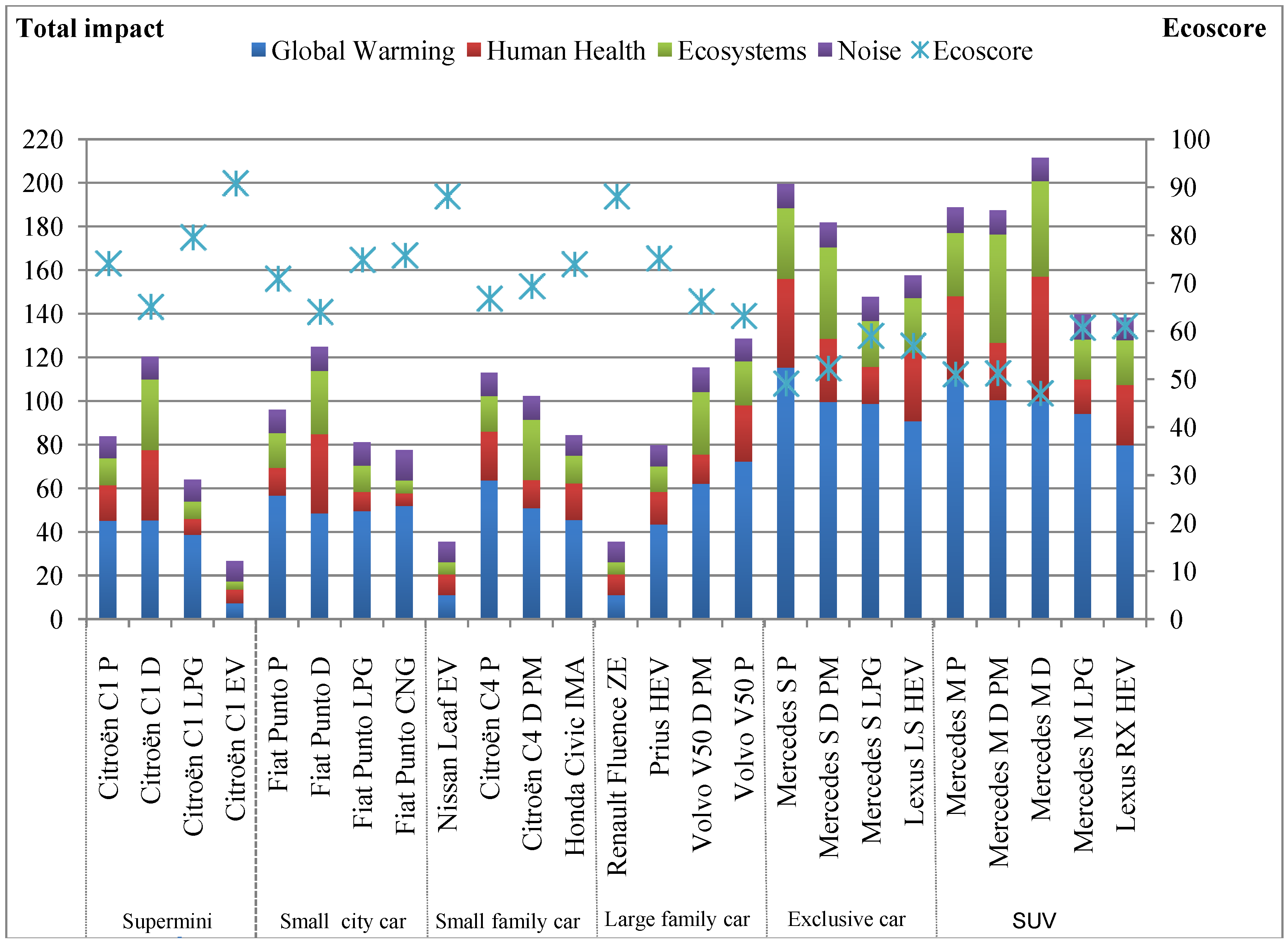

3. Ecoscore

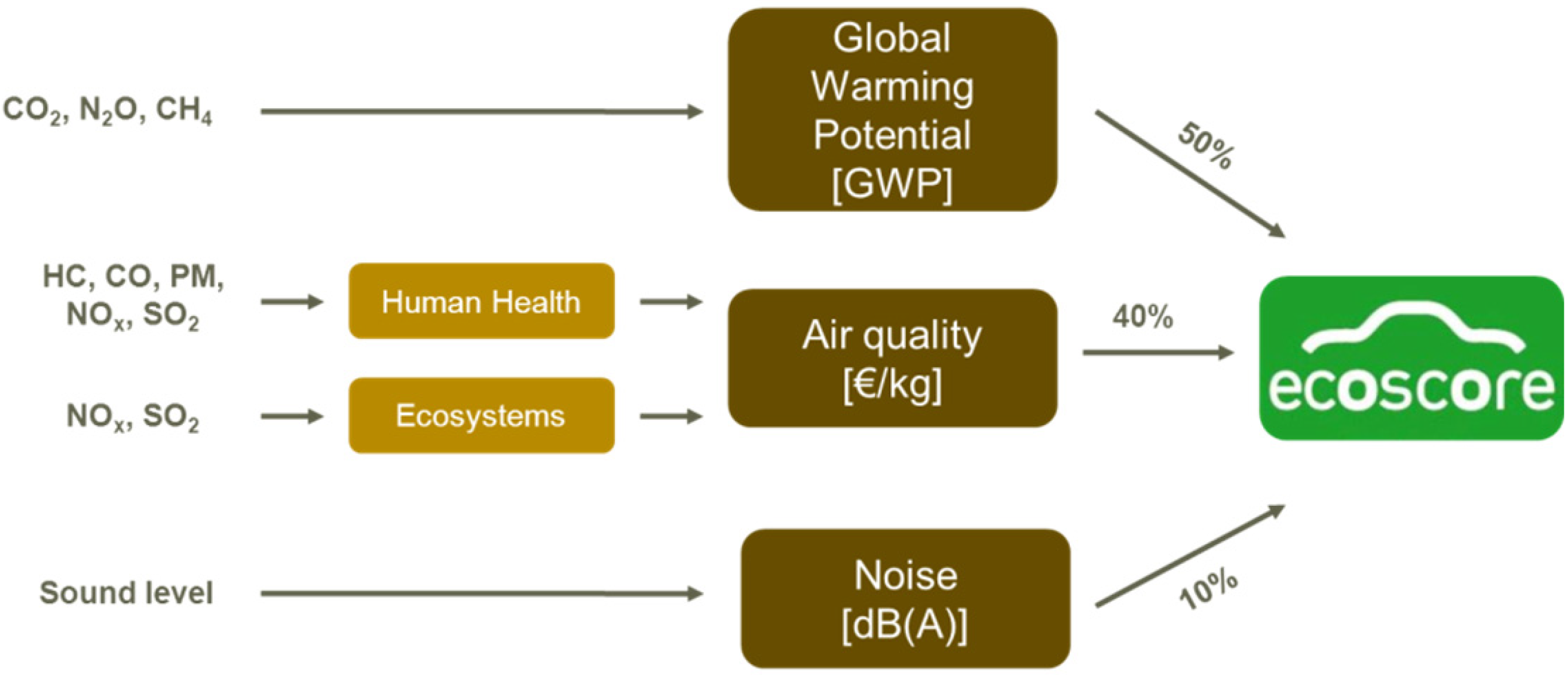

3.1. Methodology

3.2. Results

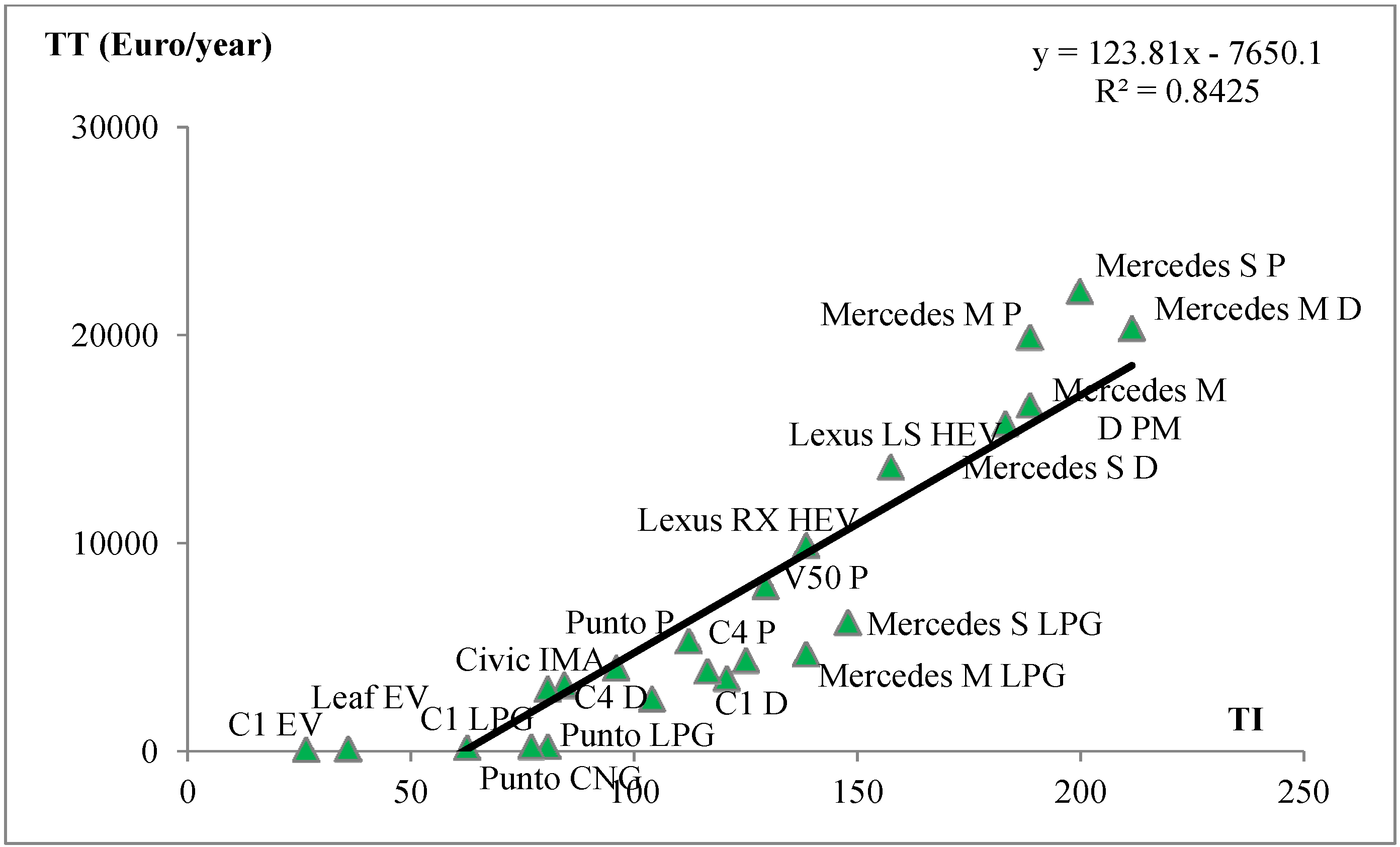

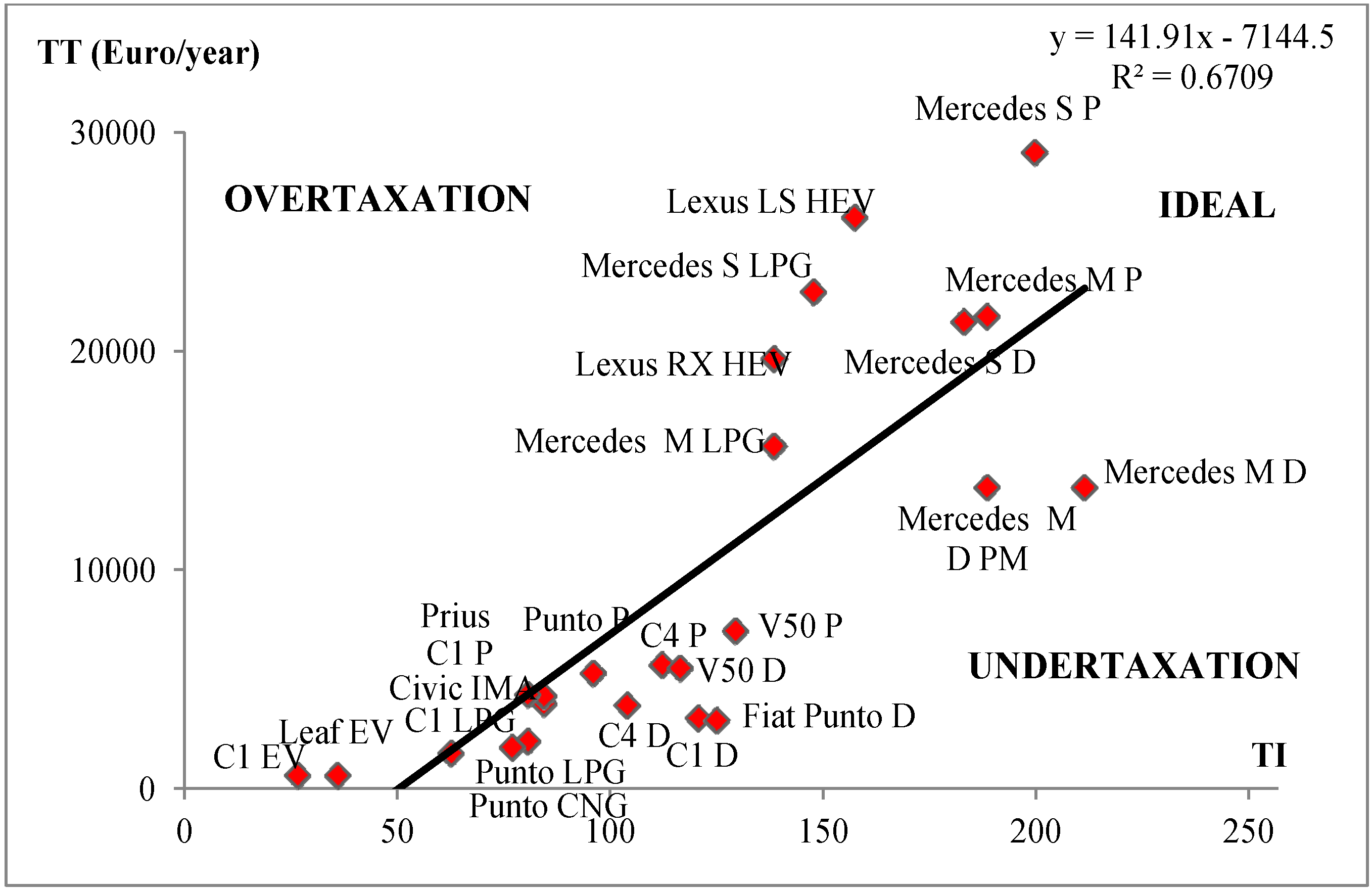

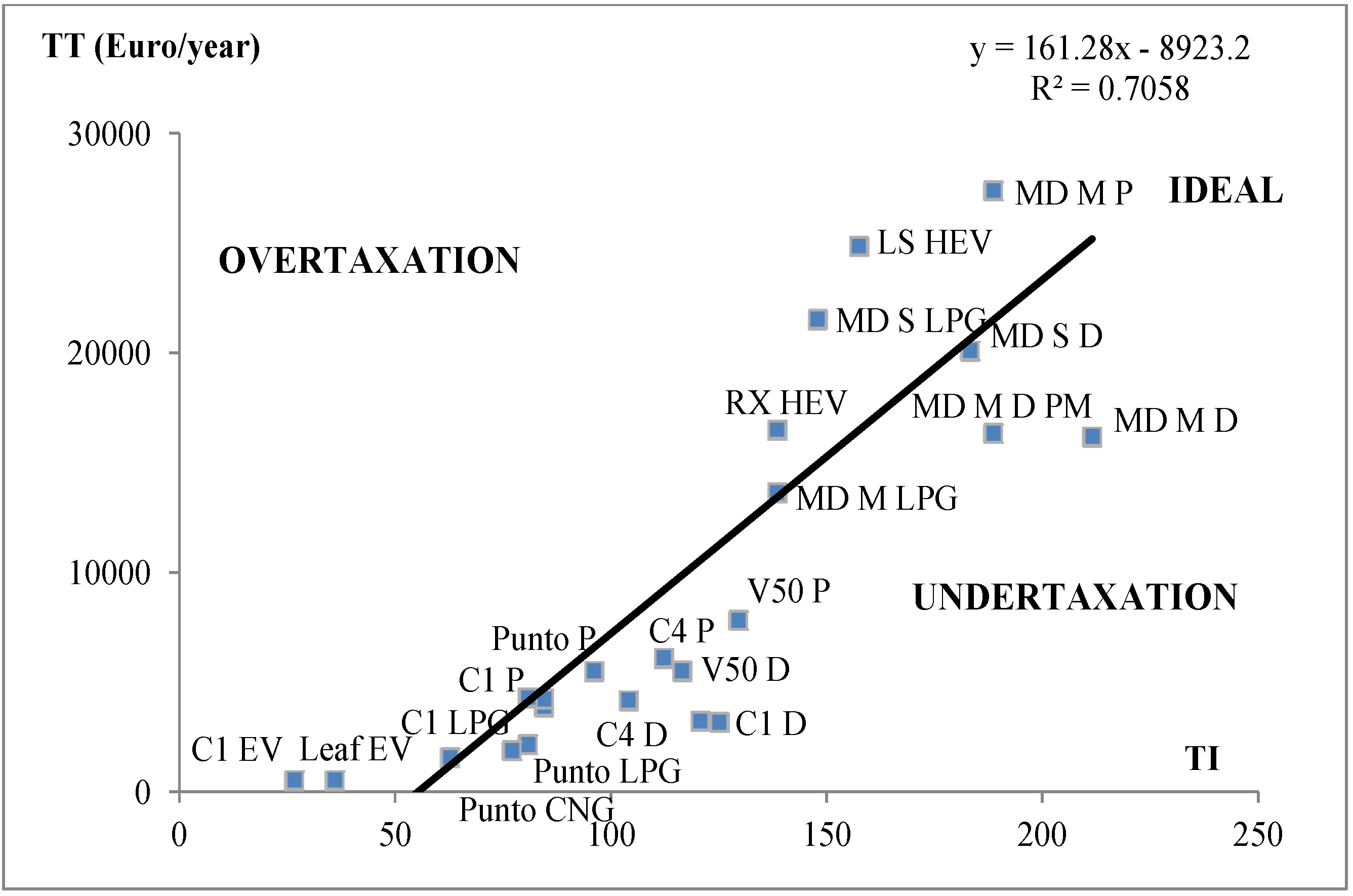

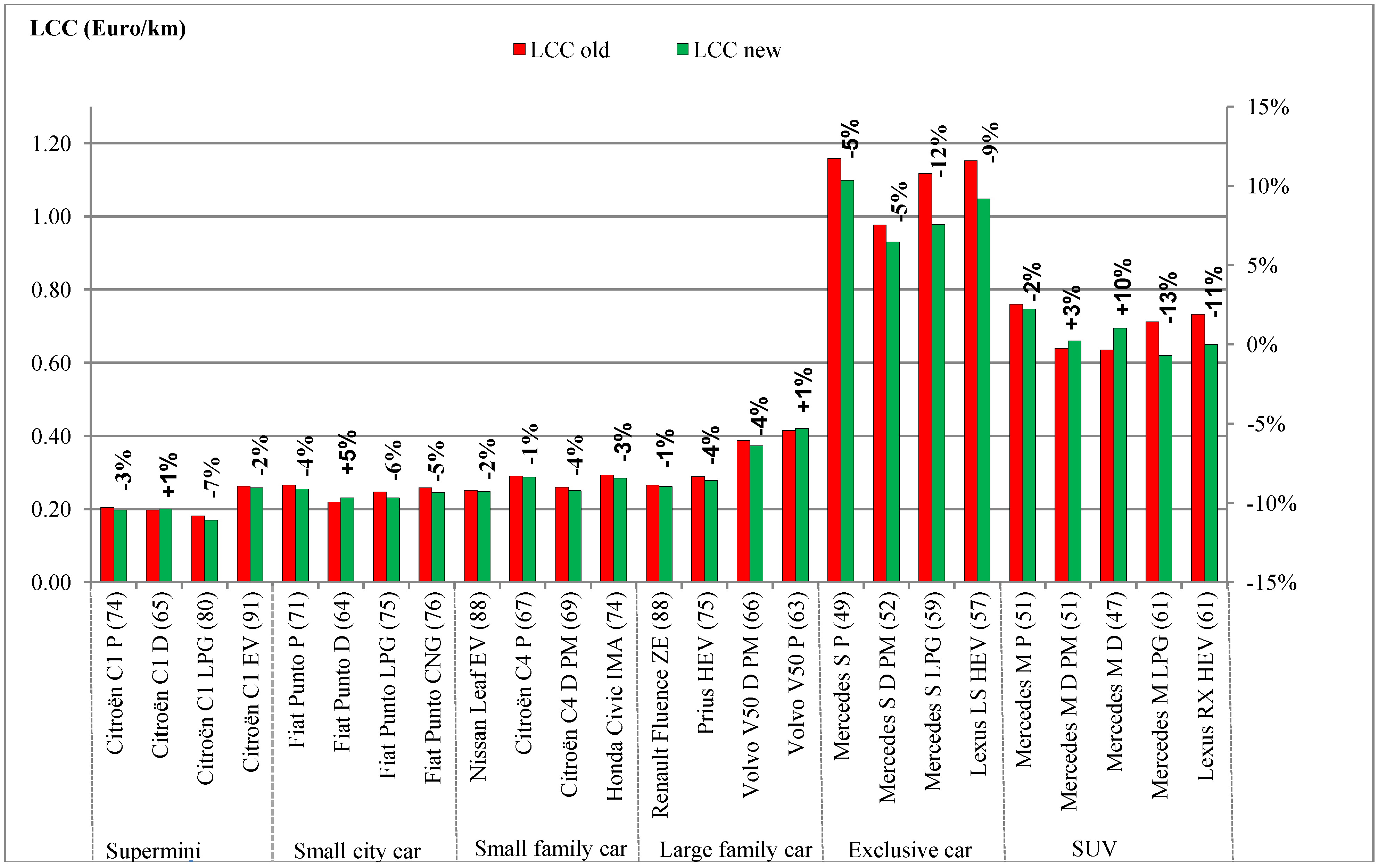

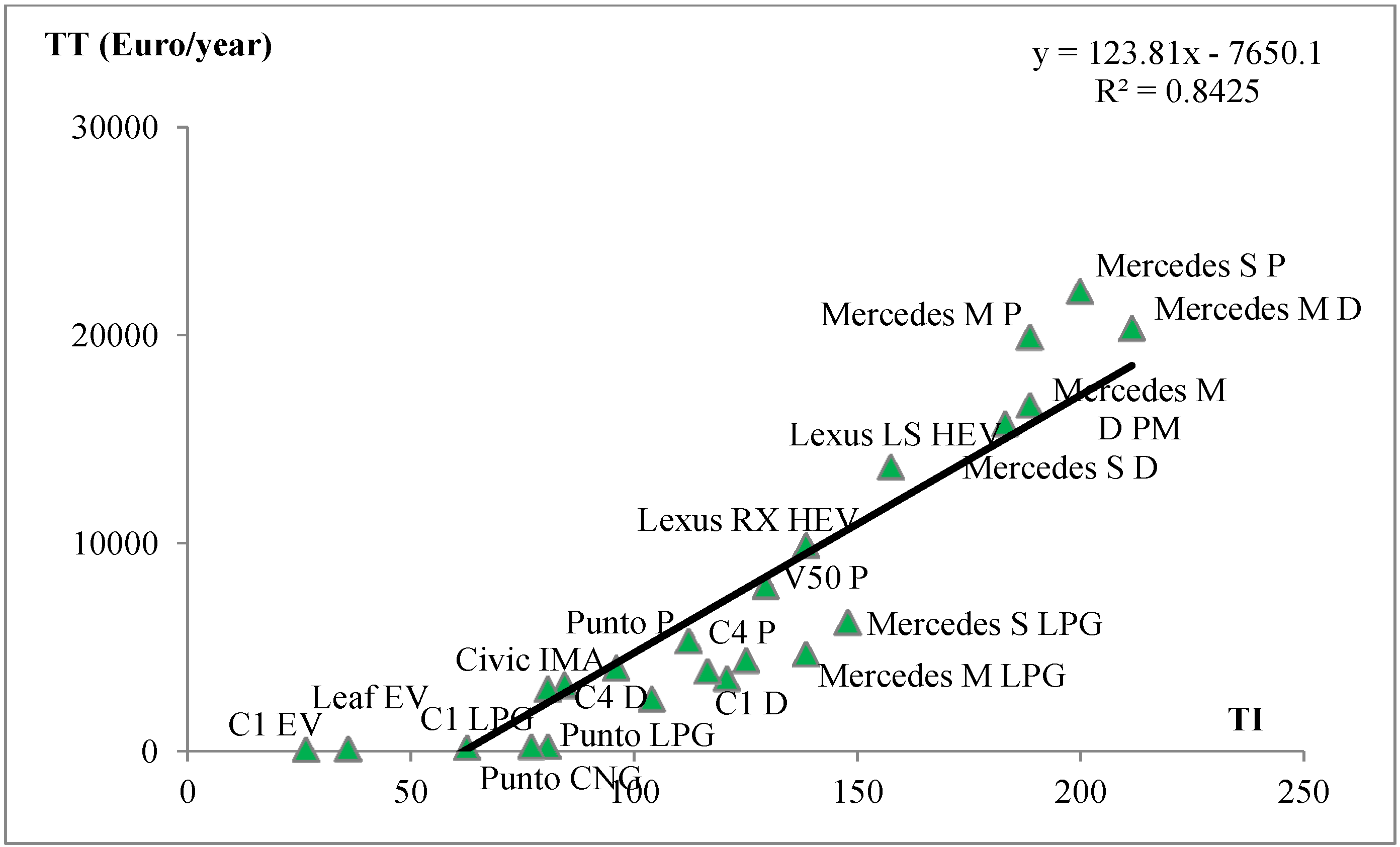

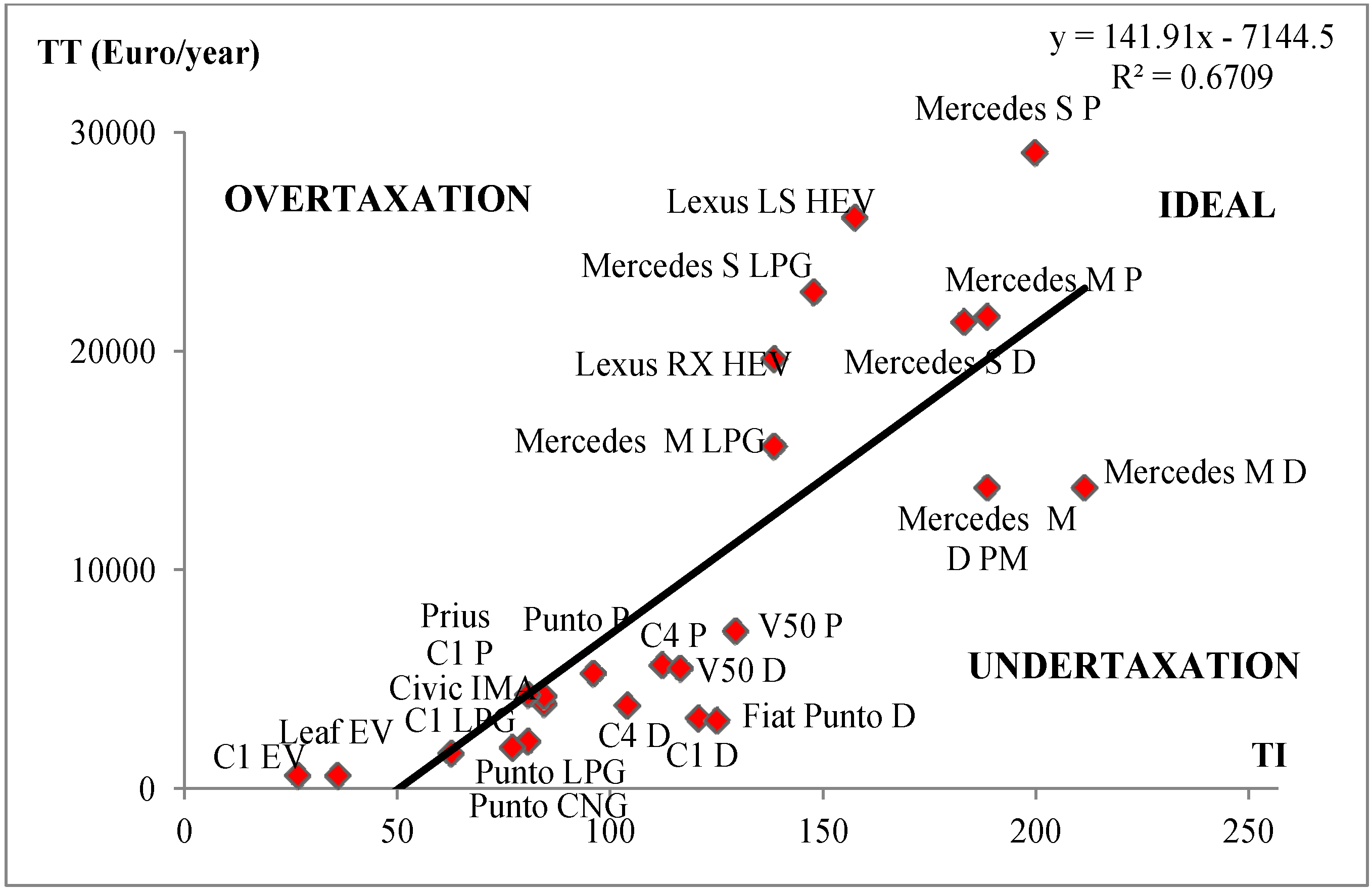

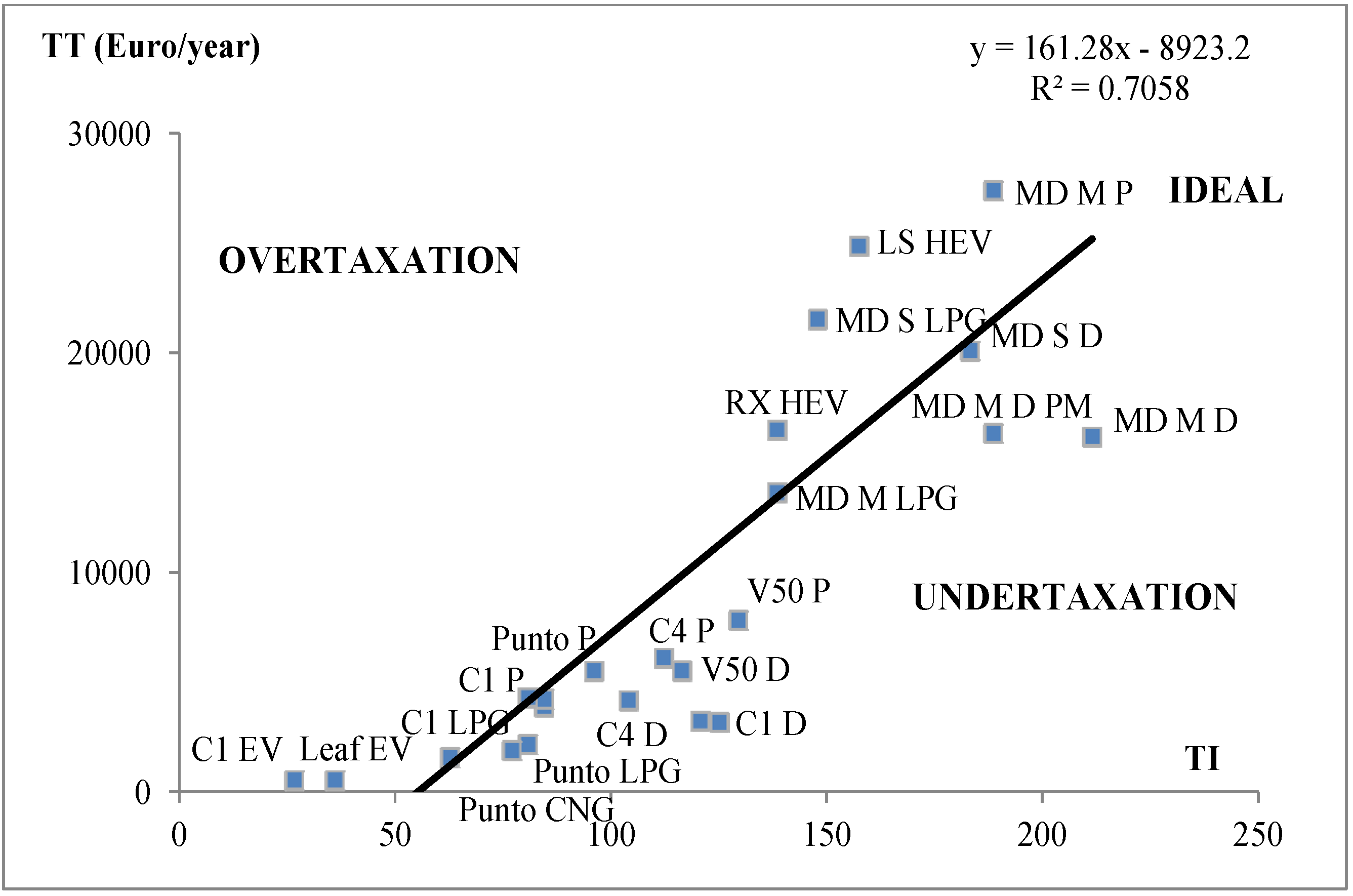

4. Tax Reform

4.1. Methodology

4.2. Results

5. Discussion and Conclusions

Abbreviations

| B5 | 5% biodiesel |

| B10 | 10% biodiesel |

| B30 | 30% biodiesel |

| B50 | 50% biodiesel |

| B100 | 100% biodiesel |

| CNG | compressed natural gas |

| D | diesel |

| D PM | diesel with PM-filter |

| E5 | 5% ethanol |

| E10 | 10% ethanol |

| E20 | 20% ethanol |

| E85 | 85% ethanol |

| EV | electric vehicle |

| HEV | hybrid electric vehicle |

| LPG | liquified petroleum gas |

| P | petrol |

Acknowledgements

References

- European Commission. Directive 2009/33/EC of the European Parliament and the Council of 23 April 2009 on the promotion of clean and energy-efficient road transport vehicles. Off. J. Eur. Union 2009, L120, 5–12. [Google Scholar]

- European Commission. Proposal for a Council Directive on Passenger Car Related Taxes; SEC(2005)809; European Commission: Brussels, Belgium, 2005. [Google Scholar]

- European Commission. Impact Assessment Guidelines; European Commission: Brussels, Belgium, 2009. Available online: http://ec.europa.eu/governance/impact/commission_guidelines/docs/iag_2009_en.pdf (accessed on 14 January 2013).

- ACEA (European Automobile Manufacturers’ Association). European Automotive Industry Advocates Harmonized CO2-Related Taxation of Cars and of Alternative Fuels in the EU. Available online: http://www.acea.be/ (accessed on 14 January 2013).

- Federal Public Service (FPS) Finance. Fiscality Related to Purchase of New Vehicles. Available online: http://www.minfin.fgov.be/portail2/nl/themes/transport/vehicles-purchase.htm#C1 (accessed on 13 January 2012).

- Kunert, U.; Kuhfeld, H. The diverse structures of passenger car taxation in Europe and the EU Commissions proposal for reform. Transp. Policy 2007, 14, 306–316. [Google Scholar] [CrossRef]

- Timmermans, J-M.; Matheys, J.; van Mierlo, J.; Lataire, P. Environmental rating of vehicles with different fuels and drive trains: A univocal and applicable methodology. Eur. J. Transp. Infrastruct. Res. 2006, 6, 313–334. [Google Scholar]

- Mairesse, O.; Verheyen, H.; Turcksin, L.; Macharis, C. Groene auto’s ? We willen ze wel maar kopen ze (nog) niet (in German). Verkeersspecialist 2008, 149, 12–15. [Google Scholar]

- Lipman, T.E.; Delucchi, M.A. A retail and lifecycle cost analysis of hybrid electric vehicles. Transp. Res. Part D 2006, 11, 115–132. [Google Scholar] [CrossRef]

- Goedecke, M.; Therdthianwong, S.; Gheewala, S.H. Life cycle cost analysis of alternative vehicles and fuels in Thailand. Energy Policy 2007, 24, 3236–3246. [Google Scholar] [CrossRef]

- Lee, J.Y.; Yoo, M.; Cha, K.; Won Lim, T.; Hur, T. Life cycle cost analysis to examine the economical feasibility of hydrogen as an alternative fuel. Int. J. Hydrog. Energy 2009, 34, 4243–4255. [Google Scholar] [CrossRef]

- Werber, M.; Fischer, M.; Schwartz, P.V. Batteries: Lower cost than gasoline? Energy Policy 2009, 27, 2465–2468. [Google Scholar] [CrossRef]

- Van Vliet, O.P.R.; Kruithof, T.; Turkenburg, W.C.; Faaij, A.P.C. Techno-economic comparison of series hybrid, plug-in hybrid, fuel cell and regular cars. J. Power Sources 2010, 195, 6570–6585. [Google Scholar] [CrossRef]

- National Institute for Statistics (NIS). Mobility Statistics. Available online http://www.statbel.fgov.be (accessed on 14 January 2013).

- Federal Public Service (FPS) Transport and Mobility. Statistieken van het Wegverkeer [in German]. Available online: http://www.mobilit.fgov.be/nl/index.htm (accessed on 14 January 2013).

- EPA (US Environmental Protection Agency). United States Environmental Protection Guidelines for Preparing Economic Analysis; EPA: Washington, DC, USA, 2000. [Google Scholar]

- Pearce, D.; Atkinson, G.; Mourato, S. Cost Benefit Analysis and the Environment; OECD (Organisation for Economic Co-operation and Development): Paris, France, 2006. [Google Scholar]

- LNE (Flemish Government, Department Environment, Nature and Energy). Environmental Costs: Definitions and Calculation Methods; LNE: Brussels, Belgium, 2008. [Google Scholar]

- Van Hulle, C.; Dutordoir, M.; Smedts, K.; de Cock, K.; Drijkoningen, H.; Lievens, T. Bank- en Financiewezen [in Dutch]; Acco Uitgeverij: Leuven, Belgium, 2006. [Google Scholar]

- Lebeau, K.; van Mierlo, J.; Lebeau, P.; Mairesse, O.; Macharis, C. The market potential for plug-in hybrid and battery electric vehicles in Flanders: A choice-based conjoint analysis. Transp. Res. Part D 2012, 17, 592–597. [Google Scholar] [CrossRef]

- Federal Public Service (FPS) Finance. Consumption Price Indices. 2010b. Available online: http://statbel.fgov.be/nl/statistieken/cijfers/economie/consumptieprijzen/consumptieprijsindexen/ (accessed on 15 January 2013). [Google Scholar]

- Autogids. Available online: http://www.autogids.be/ (accessed on 12 January 2013).

- Spitzley, D.V.; Grande, D.E.; Keoleian, G.A.; Kim, H.C. Life cycle optimization of ownership costs and emission reduction in US vehicle retirement decisions. Transp. Res. Part D 2005, 10, 161–175. [Google Scholar] [CrossRef]

- Van Mierlo, J.; Maggetto, G.; Meyer, S.; Hecq, W. Schone Voertuigen (in Dutch); Final Report; BIM-IBGE (The Brussels Institute for Management of the Environment): Brussels, Belgium, 2001. [Google Scholar]

- Keppens, M. Modelling Private Road Transport of Flemish Households: The Mobility and Welfare Effects of Fuel Taxes versus Tradable Fuel Rights. Ph.D. Dissertation, University of Hasselt, Hasselt, Belgium, 2006. [Google Scholar]

- Testaankoop. Vehicles and Transportation. Available online: http://www.test-aankoop.be/auto-en-vervoer/p139937.htm (accessed on 12 January 2013).

- GOCA (Groepering van Erkende Ondernemingen voor Autokeuring en Rijbewijs). Tariffs Car Inspection. Available online: http://www.goca.be (accessed on 14 January 2013).

- Stadsregio Amsterdam. Market Consultation Environmentally Friendly Material in the Framework of the Zaan Region. Available online: http://www.verkeerskunde.nl/marktconsultatie (accessed on 14 January 2013).

- Petroleum Federation (Petrolfed). Composition of the Maximum Price of Fuels. Available online: http://www.petrolfed.be/dutch/cijfers/maximumprijs_voornaamste_petroleumproducten.htm (accessed on 12 January 2013).

- Federal Public Service (FPS) Finance. Law Concerning Biofuels. Available online: http://economie.fgov.be (accessed on 12 January 2013).

- Lievens, E.; Jossart, J.-M. Micro-Economic Cost Overview of Biofuels; Report for Bioses Project (Biofuels Sustainable End Use); Belgian Science Policy: Brussels, Belgium, 2010. [Google Scholar]

- Stroomtarieven. Available online: http://www.stroomtarieven.be (accessed on 14 January 2013).

- H2moves.eu. Available online: http://www.h2moves.eu/ (accessed on 14 January 2013).

- Chiarimonti, D.; Tondi, G. Stationary Applications of Liquid Biofuels; PTA contract NNE5-PTA-2002-006; ETA Renewable Energies: Firenze, Italy, 2003; Available online: http://ec.europa.eu/energy/res/sectors/doc/bioenergy/pta_biofuels_final_rev2_1.pdf (accessed on 14 January 2013).

- Febiac. Evolution of Registrations of New Vehicles Per Fuel Type. Available online: http://www.febiac.be/public/statistics.aspx?FID=23&lang=NL (accessed on 11 January 2013).

- De Borger, B. Discrete choice models and optimal two-part tariffs in the presence of externalities: Optimal taxation of cars. Region. Sci. Urban Econ. 2001, 31, 471–504. [Google Scholar] [CrossRef]

- European Commission. Proposal for a Council Directive Amending Directive 92/81/EEC and Directive 92/82/EEC to Introduce Special Tax Arrangements for Diesel Fuel Used for Commercial Purposes and to Align the Excise Duties on Petrol and Diesel Fuel. COM(2002) 410 Final; European Commission: Brussels, Belgium, 2002. [Google Scholar]

- Mayeres, I.; Proost, S. Should Diesel Cars in Europe be Discouraged; Katholieke Universiteit Leuven: Leuven, Belgium, 2000. [Google Scholar]

- Johnstone, N.; Karousakis, K. Economic incentives to reduce pollution from road transport: The case for vehicle characteristics taxes. Transp. Policy 1999, 6, 99–108. [Google Scholar] [CrossRef]

- Crawford, I.; Smith, S. Fiscal instruments for air pollution abatement in road transport. J. Transp. Econ. Policy 1995, 29, 33–51. [Google Scholar]

- Innes, R. Regulating automobile pollution under certainty competition, and imperfect information. J. Environ. Econ. Manag. 1996, 31, 219–239. [Google Scholar] [CrossRef]

- Santos, G.; Behrendt, H.; Maconi, L.; Shirvani, T.; Teytelboym, A. Part I: Externalities and economic policies in road transport. Res. Transp. Econ. 2010, 28, 2–45. [Google Scholar] [CrossRef]

- Timmermans, J.-M. A Contribution to Cleaner Vehicle Technologies. Ph.D. Dissertation, Vrije Universiteit Brussel, Brussels, Belgium, 2010. [Google Scholar]

- Boureima, F.-S.; Wynen, V.; Sergeant, N.; Heijke, R.; Messagie, M.; van Mierlo, J. Clever: Clean Vehicle Research: LCA and Policy Options; LCA Report for Belgian Science Policy: Brussels, Belgium, 2011. [Google Scholar]

- Maibach, M.; Schreyer, C.; Sutter, D.; van Essen, H.P.; Boon, B.H.; Smokers, R.; Schroten, A.; Doll, C.; Pawlowska, B.; Bak, M. Handbook on Estimation of External Costs in the Transport Sector: Internalisation Measures and Policies for all External Cost of Transport (IMPAC); Commissioned by the European Commission (DG TREN): Brussels, Belgium, 2008. [Google Scholar]

- Turcksin, L. Stimulating the Purchase of Environmentally Friendlier Cars—A Socio-Economic Evaluation. Ph.D. Dissertation, Vrije Universiteit Brussel, Brussels, Belgium, 2011. [Google Scholar]

- Chamber of Belgian Representatives. Proposition of a Resolution with Respect to the Introduction of an Ecoscore-Vignette for Vehicles; Doc 52 (0764/001); Chamber of Belgian Representatives: Brussels, Belgium, 2008. [Google Scholar]

- Macharis, C.; Turcksin, L.; Sergeant, N.; van Mierlo, J.; Denys, T.; Jourquin, B. Modalities of the Reformation of the Traffic and Registration Tax Based on the Environmental Performance of Vehicles; Final Report of the Project Commissioned by the Brussels Capital Region: Brussels, Belgium, 2007. [Google Scholar]

- Mobimix, Flemish Circulation Tax and/or Road Pricing. Available online: http://www.mobimix.be (accessed on 12 January 2013).

- Macharis, C.; Turcksin, L. Calculation of Behavioural Change as a Result of a Tax Reformation Based on the Euro Standard and CO2 Emissions of the Vehicle. Report of Project Commissioned by the LNE: Brussels, Belgium, 2010. [Google Scholar]

- Greene, D.L. Uncertainty, loss aversion, and markets for energy efficiency. Energy Econ. 2011, 33, 608–616. [Google Scholar] [CrossRef]

- Greene, D.L.; Patterson, P.D.; Singh, M.; Li, J. Feebates, rebates and gas-guzzler taxes: A study of incentives for increased fuel economy. Energy Policy 2005, 33, 757–775. [Google Scholar] [CrossRef]

- De Haan, P.; Mueller, M.G.; Scholz, R.W. How much do incentives affect car purchase? Agent-based microsimulation of consumer choice of new cars—Part II: Forecasting effects of feebates based on energy-efficiency. Energy Policy 2009, 37, 1083–1094. [Google Scholar] [CrossRef]

- Liebermann, Y.; Ungar, M. Efficiency of consumer intertemporal choice under life cycle cost conditions. J. Econ. Psychol. 2002, 23, 729–748. [Google Scholar] [CrossRef]

- Van Bree, B.; Verbong, G.P.J.; Kramer, G.J. A multi-level perspective on the introduction of hydrogen and battery-electric vehicles. Technol. Forecast. Soc. Chang. 2010, 77, 529–540. [Google Scholar] [CrossRef]

- Heffner, R.; Kurani, K.S.; Turrentine, T. Symbolism in California’s early market for hybrid electric vehicles. Transp. Res. Part D 2007, 12, 396–413. [Google Scholar] [CrossRef]

- Turrentine, T.S.; Kurani, K.S. Car buyers and fuel economy? Energy Policy 2007, 35, 1213–1223. [Google Scholar] [CrossRef]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Turcksin, L.; Mairesse, O.; Macharis, C.; Mierlo, J.V. Encouraging Environmentally Friendlier Cars via Fiscal Measures: General Methodology and Application to Belgium. Energies 2013, 6, 471-491. https://doi.org/10.3390/en6010471

Turcksin L, Mairesse O, Macharis C, Mierlo JV. Encouraging Environmentally Friendlier Cars via Fiscal Measures: General Methodology and Application to Belgium. Energies. 2013; 6(1):471-491. https://doi.org/10.3390/en6010471

Chicago/Turabian StyleTurcksin, Laurence, Olivier Mairesse, Cathy Macharis, and Joeri Van Mierlo. 2013. "Encouraging Environmentally Friendlier Cars via Fiscal Measures: General Methodology and Application to Belgium" Energies 6, no. 1: 471-491. https://doi.org/10.3390/en6010471

APA StyleTurcksin, L., Mairesse, O., Macharis, C., & Mierlo, J. V. (2013). Encouraging Environmentally Friendlier Cars via Fiscal Measures: General Methodology and Application to Belgium. Energies, 6(1), 471-491. https://doi.org/10.3390/en6010471