Use of Bayesian Estimates to determine the Volatility Parameter Input in the Black-Scholes and Binomial Option Pricing Models

Abstract

:1. INTRODUCTION

2. PRIOR RESEARCH

3. DATA

4. MATHEMATICAL FRAMEWORK

4.1 A Bayes estimate using a conjugate prior

4.2 An empirical Bayesian approach

4.3 Measurement of estimation error

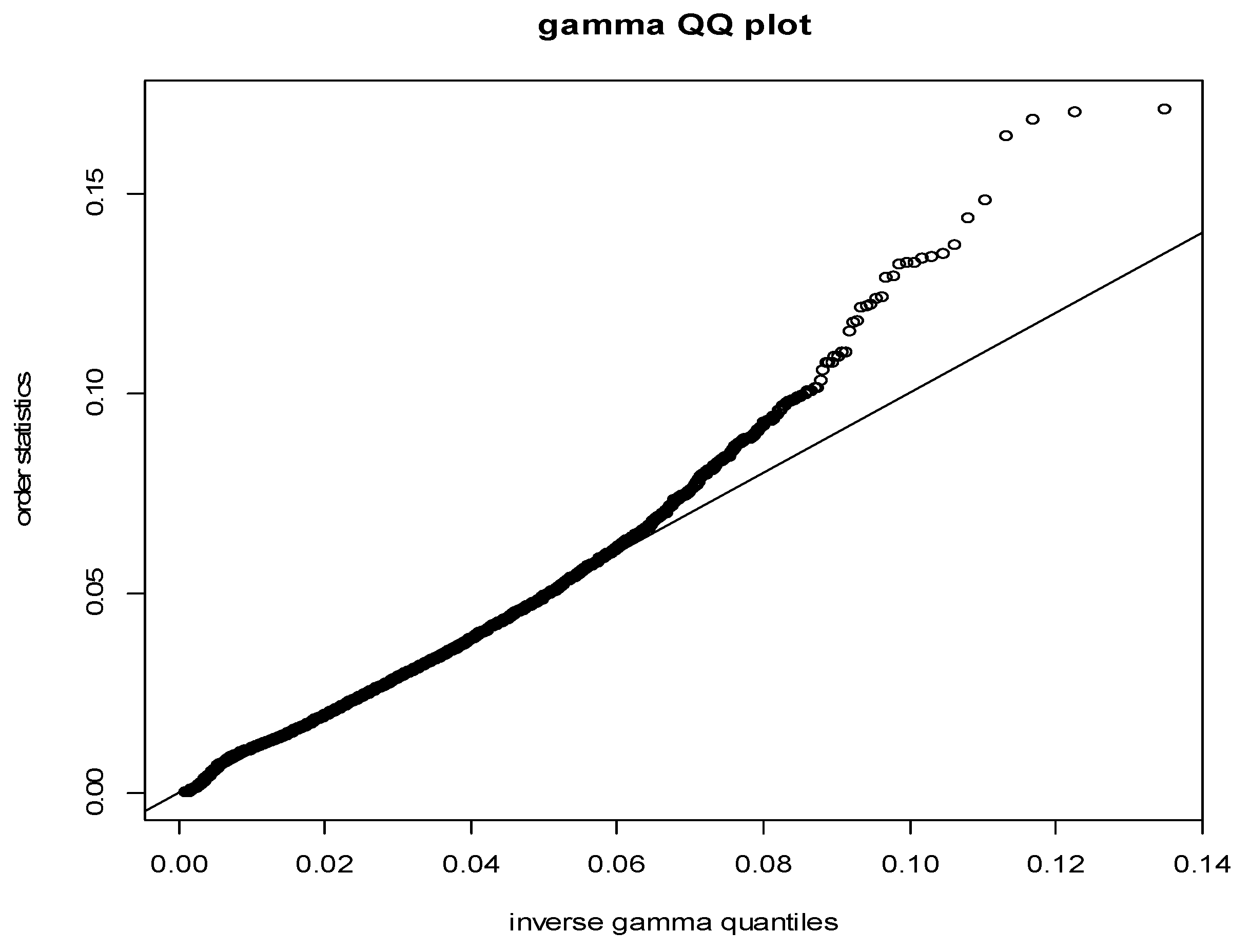

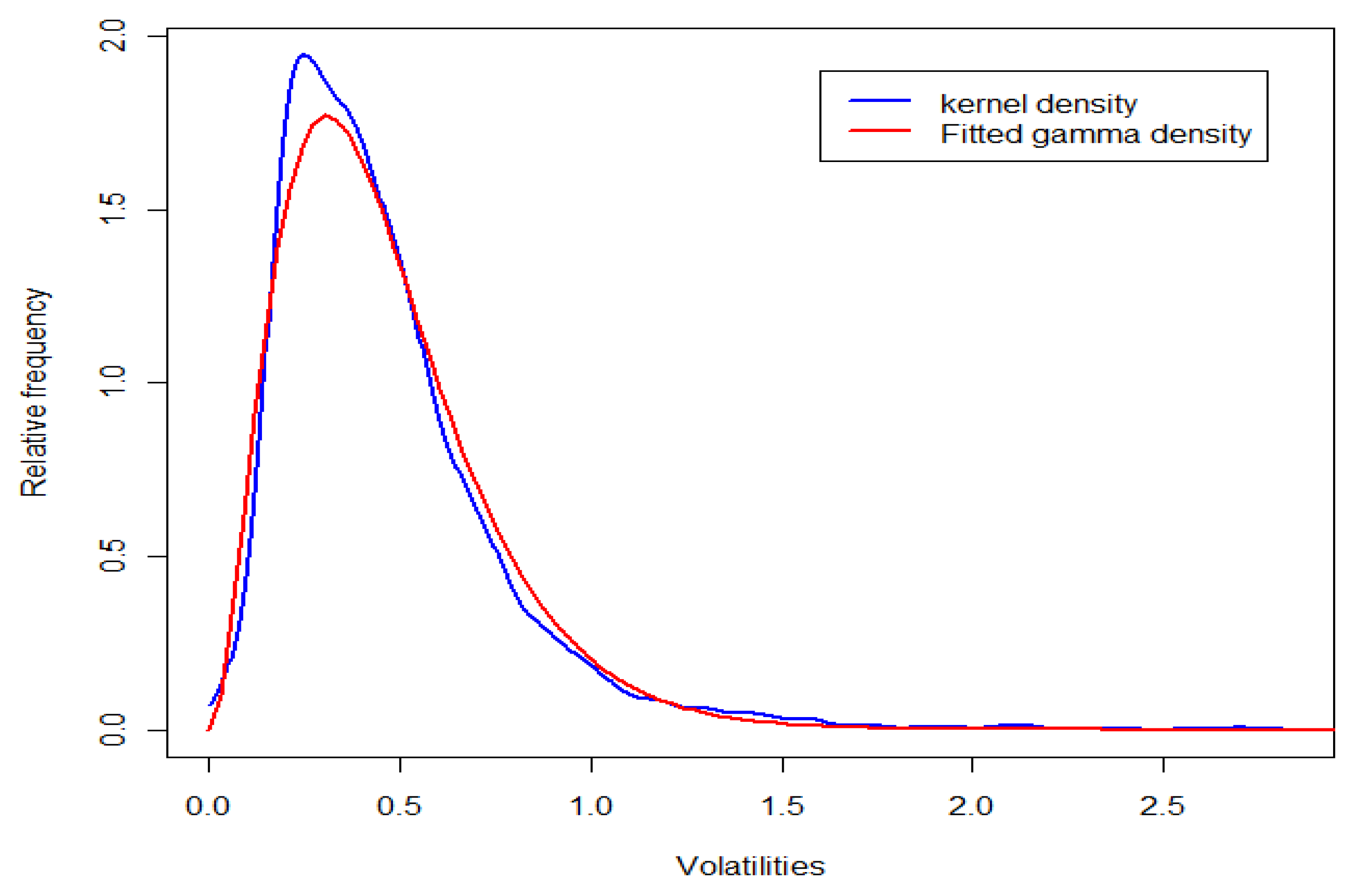

5. EMPIRICAL RESULTS

6. CONCLUSION

References

- S. Balsam, S. O’Keefe, and M. Weidemer. “Frontline reaction to FASB 123-12.” Journal of Accounting 203 No. 4. (2007): 54–56. [Google Scholar]

- G. Barone-Adesi, and R.E. Whaley. “The valuation of American call options and the expected ex-dividend stock price decline.” Journal of Financial Economics 17 (1986): 58–91. [Google Scholar] [CrossRef]

- G. Barone-Adesi, and R.E. Whaley. “Efficient analytic approximation of American Option Values.” Journal of Finance 42 (1987): 301–320. [Google Scholar] [CrossRef]

- L. Bauwens, and M. Lubrano. “Bayesian option pricing using asymmetric GARCH models.” Journal of Empirical Finance 9 (2002): 321–342. [Google Scholar] [CrossRef]

- S. Beckers. “Standard deviation implied in option prices as predictors of future stock price variability.” Journal of Banking and Finance 5, 3 (1981): 363–381. [Google Scholar] [CrossRef]

- “BIS Quarterly Review, 2011, Dec.” http://www.bis.org/publ/qtrpdf/r_qs1112.pdf.

- F. Black, and M. Scholes. “The valuation of options and corporate liabilities.” Journal of Political Economy 81 (1973): 637–654. [Google Scholar] [CrossRef]

- M.E. Blume. “Betas and their regression tendencies.” Journal of Finance 30 No. 3. (1975): 785–795. [Google Scholar] [CrossRef]

- L. Canina, and S. Figlewski. “The informational content of implied volatility.” Review of Financial Studies 6 (1993): 659–681. [Google Scholar] [CrossRef]

- D.P. Chiras, and S. Manaster. “The information content of prices and a test of market efficiency.” Journal of Financial Economics 6 (1978): 213–234. [Google Scholar] [CrossRef]

- P. Choudhary. “Evidence on differences between recognition and disclosure: A comparison of inputs to estimate fair value of employee stock options.” Journal of Accounting and Economics 51 (2011): 77–94. [Google Scholar] [CrossRef]

- B.J. Christensen, and N.R. Prabhala. “The relation between implied realized volatility.” Journal of Financial Economics 50 No. 2. (1998): 125–150. [Google Scholar] [CrossRef]

- J.C. Cox, and S.A. Ross. “The valuation of options for alternative stochastic processes.” Journal of Financial Economics 3 (1976): 145–166. [Google Scholar] [CrossRef]

- J.C. Cox, S.A. Ross, and M. Rubenstein. “Option pricing: A simplified approach.” Journal of Financial Economics 7 (1979): 229–264. [Google Scholar] [CrossRef]

- T. Darsinos, and S. Satchell. “Bayesian analysis of the Black-Scholes option price.” In Forecasting Expected Returns in the Financial Markets. Edited by S. Satchel. NY: Academic Press, 2007, pp. 117–150. [Google Scholar]

- A.P. Dempster, N.M. Laird, and D.B. Rubin. “Maximum Likelihood from Incomplete Data via the EM Algorithm.” Journal of the Royal Statistical Society 39 (1977): 1–38. [Google Scholar]

- E.J. Elton, M.J. Gruber, and T.J. Urich. “Are Betas Best? ” Journal of Finance 33 No. 5. (1978): 1375–1384. [Google Scholar] [CrossRef]

- A. Eubank Jr., and J.K. Zumwalt. “An Analysis of the Forecast Error Impact of Alternative Beta Adjustment Techniques and Risk Classes.” Journal of Finance 34 No. 3. (1979): 761–776. [Google Scholar] [CrossRef]

- J. Fleming. “The quality of market volatility forecasts implied by S&P 100 Index option prices.” Journal of Empirical Finance 5 (1998): 317–345. [Google Scholar]

- D.B. Flynn, S.D. Grose, G.M. Martin, and V.L. Martin. “Pricing Australian S&P 200 options: A Bayesian approach based on general distributional forms.” Australian and New Zealand Journal of Statistics 47 (2005): 101–17. [Google Scholar]

- C.S. Forbes, G.M. Martin, and J. Wright. “Inference for a class of stochastic volatility models using option and spot prices: application of a bivariate Kalman filter.” Econometric Reviews 26 (2007): 387–418. [Google Scholar] [CrossRef]

- M.B. Garman, and S.W. Kohlhagen. “Foreign currency option values.” Journal of International Money and Finance 2 (1983): 231–237. [Google Scholar] [CrossRef]

- J.C. Hull. Options, Futures and Other Derivatives, Eight Edition ed. 2011, Pearson Education Limited. [Google Scholar]

- J.C. Jackwerth, and M. Rubinstein. “Recovering probability distributions from option prices.” Journal of Finance 51 (1996): 1611–1631. [Google Scholar] [CrossRef]

- E. Jacquier, and R. Jarrow. “Bayesian analysis of contingent claim model error.” Journal of Econometrics 94 (2000): 145–180. [Google Scholar] [CrossRef]

- P. Jorion. “Predicting volatility in the foreign exchange market.” Journal of Finance 50 (1995): 507–528. [Google Scholar] [CrossRef]

- G.A. Karolyi. “A Bayesian approach to modelling stock return volatility for option valuation.” Journal of Financial and Quantitative Analysis 28 (1993): 579–594. [Google Scholar] [CrossRef]

- R.C. Klemkosky, and J.D. Martin. “The adjustment of beta forecasts.” Journal of Finance 30 No. 4. (1975): 1123–1128. [Google Scholar] [CrossRef]

- H. Latane, and R.J. Rendleman. “Standard deviations of stock price ratios implied in option prices.” Journal of Finance 31 No. 2. (1976): 369–381. [Google Scholar] [CrossRef]

- M. le Roux. “A long-term model of the dynamics of the S&P 500 implied volatility surface.” North American Actuarial Journal 11, 4 (2005): 61–75. [Google Scholar]

- K. Li. “Long-memory versus option-implied volatility prediction.” Journal of Derivatives Vol. 9 No. 3 Spring. (2002): 9–25. [Google Scholar] [CrossRef]

- S. Li, and Q. Yang. “The relationship between implied and realized volatility: evidence from the Australian stock index option market.” Review of Quantitative Finance and Accounting 32 (2009): 405–419. [Google Scholar] [CrossRef]

- G.M. Martin, C.S. Forbes, and V.L. Martin. “Implicit Bayesian inference using option prices.” Journal of Time Series Analysis 26 (2005): 437–462. [Google Scholar] [CrossRef]

- R.C. Merton. “Theory of rational option pricing.” Bell Journal of Economics and Management Science 4 Spring. (1973): 141–183. [Google Scholar] [CrossRef]

- R.C. Merton. “Option pricing when underlying stock returns are discontinuous.” Journal of Financial Economics 3 (1976): 125–144. [Google Scholar] [CrossRef]

- S. Poon, and C. Granger. “Practical issues in forecasting volatility.” Financial Analysts Journal 61 (2005): 45–56. [Google Scholar] [CrossRef]

- J. Shu, and J.E. Zhang. “The relationship between implied volatility and realised volatility of S&P 500 index.” Technical Article 4. WILMOTT Magazine, 2003, 83–91. [Google Scholar]

- A. Szakmary, E. Ors, J.K. Kim, and W.N. Davidson. “The predictive power of implied volatility: evidence from 35 futures markets.” Journal of Banking and Finance 27 (2003): 2151–2175. [Google Scholar] [CrossRef]

- O.A. Vasicek. “A Note on Using Cross-Sectional Information in Bayesian Estimation of Security Betas.” Journal of Finance 28 No. 5. (1973): 1233–1239. [Google Scholar] [CrossRef]

- 1See Jackwerth and Rubinstein (1996) and Hull (2011) for evidence on volatility smiles for equity stock options.

- 2CRSP stands for Center for Research in Security Prices and is a provider for historical stock data.

- 3Poon and Granger (2005) note that outliers can have a big impact on volatility estimation and suggest outliers might be separately examined with the use of a crisis model or using extreme value theories.

- 4IVolatility and OptionMetrics are the two most widely used databases for options as pointed out in le Roux (2005).

- 5See equation 5 for details of this calculation.

{kind=link}

{kind=link}

{kind=link}

| End Date | CRSP sample Size (prior to deletion of outliers) | Ivolatility sample size |

|---|---|---|

| August 16, 2007 | 6,031 | 243 |

| October 1, 2007 | 5,912 | 249 |

| November 13, 2007 | 5,942 | 255 |

| December 28, 2007 | 5,961 | 252 |

| February 13, 2008 | 6,018 | 253 |

| March 31, 2008 | 5,899 | 250 |

| May 13, 2008 | 5,816 | 259 |

| June 26, 2008 | 5,889 | 258 |

| August 11, 2008 | 5,751 | 263 |

| September 24, 2008 | 5,739 | 256 |

| November 6, 2008 | 5,750 | 247 |

| December 22, 2008 | 5,637 | 248 |

| February 24, 2009 | 5,462 | 245 |

| April 8, 2009 | 5,557 | 256 |

| May 22, 2009 | 5,557 | 266 |

| July 8, 2009 | 5,573 | 267 |

| August 20, 2009 | 5,577 | 270 |

| October 5, 2009 | 5,674 | 272 |

| November 17, 2009 | 5,671 | 275 |

| Sample | N | Minimum | First quartile | Mean | Median | Third quartile | Maximum |

|---|---|---|---|---|---|---|---|

| Historical volatility of entire sample on CRSP | 5,671 | 0.0030 | 0.2614 | 0.4604 | 0.3985 | 0.5756 | 2.720 |

| Historical volatility of stocks of interest | 275 | 0.0850 | 0.2907 | 0.4258 | 0.4053 | 0.5205 | 1.2650 |

| Implied volatility (call) | 275 | 0.0954 | 0.3353 | 0.4750 | 0.4423 | 0.5756 | 1.3190 |

| Implied volatility (put) | 275 | 0.1042 | 0.3437 | 0.4785 | 0.4371 | 0.5744 | 1.2980 |

| Panel A | Call Options | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Conjugate | Gamma | Mixture | |||||||

| End date | Difference of medians | Wilcoxon P-value | Historical percentgreater | Difference of medians | Wilcoxon P-value | Historical percentgreater | Difference of medians | Wilcoxon P-value | Historical percentgreater |

| August 16, 2007 | -0.00123 | 0.8988 | 46 | 0.00382 | 0.0000 | 63 | 0.00299 | 0.0000 | 62 |

| October 1, 2007 | -0.00032 | 0.0018 | 37 | 0.00450 | 0.0000 | 71 | 0.00460 | 0.0000 | 71 |

| November 13, 2007 | -0.00023 | 0.0264 | 38 | -0.00001 | 0.0000 | 73 | 0.00053 | 0.0000 | 72 |

| December 28, 2007 | -0.00089 | 0.0855 | 50 | 0.00006 | 0.0000 | 64 | 0.00153 | 0.0000 | 66 |

| February 13, 2008 | 0.00269 | 0.0000 | 61 | -0.00454 | 0.0755 | 46 | -0.00395 | 0.2807 | 47 |

| March 31, 2008 | -0.00048 | 0.0522 | 40 | 0.00336 | 0.0000 | 64 | 0.00391 | 0.0000 | 68 |

| May 13, 2008 | 0.00132 | 0.8680 | 45 | 0.00489 | 0.0000 | 63 | 0.00540 | 0.0000 | 64 |

| June 26, 2008 | -0.00309 | 0.0000 | 12 | 0.01130 | 0.0000 | 88 | 0.00970 | 0.0000 | 83 |

| August 11, 2008 | 0.00247 | 0.0000 | 64 | -0.00240 | 0.0015 | 41 | -0.00119 | 0.0200 | 43 |

| September 24, 2008 | -0.00184 | 0.0286 | 51 | 0.00042 | 0.0000 | 62 | -0.00113 | 0.6299 | 53 |

| November 6, 2008 | 0.00765 | 0.0000 | 84 | -0.02174 | 0.0000 | 32 | -0.02939 | 0.0000 | 16 |

| December 22, 2008 | 0.00857 | 0.0000 | 93 | -0.03283 | 0.0000 | 21 | -0.03563 | 0.0000 | 9 |

| February 24, 2009 | -0.00037 | 0.0636 | 41 | 0.00239 | 0.0000 | 66 | 0.00100 | 0.0000 | 60 |

| April 8, 2009 | 0.00051 | 0.0000 | 73 | -0.00715 | 0.0000 | 29 | -0.00754 | 0.0000 | 26 |

| May 22, 2009 | 0.00165 | 0.0000 | 66 | -0.00285 | 0.0004 | 39 | -0.00260 | 0.0022 | 41 |

| July 8, 2009 | -0.00330 | 0.0000 | 12 | 0.00907 | 0.0000 | 88 | 0.00988 | 0.0000 | 88 |

| August 20, 2009 | -0.00194 | 0.0000 | 28 | 0.00520 | 0.0000 | 73 | 0.00512 | 0.0000 | 72 |

| October 5, 2009 | -0.00372 | 0.0000 | 9 | 0.01221 | 0.0000 | 94 | 0.01560 | 0.0000 | 95 |

| November 17, 2009 | -0.00021 | 0.0000 | 31 | 0.00095 | 0.0000 | 65 | 0.00109 | 0.0000 | 66 |

| All periods | 0.00020 | 0.0007 | 45 | 0.00217 | 0.0000 | 60 | 0.00193 | 0.0000 | 58 |

| Panel B | Put options | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Conjugate | Gamma | Mixture | |||||||

| End date | Difference of medians | Wilcoxon P-value | Historical percent greater | Difference of medians | Wilcoxon P-value | Historical percent greater | Difference of medians | Wilcoxon P-value | Historical percent greater |

| August 16, 2007 | -0.00102 | 0.6806 | 44 | 0.00136 | 0.0000 | 63 | 0.0002 | 0.0000 | 61 |

| October 1, 2007 | -0.00211 | 0.0000 | 32 | 0.00455 | 0.0000 | 79 | 0.0020 | 0.0000 | 77 |

| November 13, 2007 | -0.00207 | 0.0048 | 36 | 0.00466 | 0.0000 | 73 | 0.0050 | 0.0000 | 72 |

| December 28, 2007 | 0.00041 | 0.0416 | 49 | 0.00078 | 0.0000 | 66 | 0.0013 | 0.0000 | 67 |

| February 13, 2008 | 0.00097 | 0.0000 | 59 | -0.00424 | 0.7031 | 49 | -0.0046 | 0.7632 | 51 |

| March 31, 2008 | -0.00134 | 0.0341 | 40 | 0.00131 | 0.0000 | 66 | 0.0013 | 0.0000 | 68 |

| May 13, 2008 | -0.00072 | 0.4641 | 43 | 0.00408 | 0.0000 | 66 | 0.0039 | 0.0000 | 68 |

| June 26, 2008 | -0.00272 | 0.0000 | 12 | 0.00666 | 0.0000 | 87 | 0.0070 | 0.0000 | 83 |

| August 11, 2008 | 0.00118 | 0.0000 | 65 | 0.00053 | 0.0344 | 44 | 0.0006 | 0.2023 | 46 |

| September 24, 2008 | -0.00002 | 0.0398 | 51 | 0.00382 | 0.0000 | 62 | 0.0023 | 0.4593 | 54 |

| November 6, 2008 | 0.00382 | 0.0000 | 84 | -0.02300 | 0.0000 | 30 | -0.0264 | 0.0000 | 15 |

| December 22, 2008 | 0.00801 | 0.0000 | 93 | -0.03216 | 0.0000 | 22 | -0.0385 | 0.0000 | 10 |

| February 24, 2009 | -0.00086 | 0.0098 | 39 | 0.00513 | 0.0000 | 69 | 0.0038 | 0.0000 | 62 |

| April 8, 2009 | 0.00152 | 0.0000 | 68 | -0.00580 | 0.0000 | 32 | -0.0059 | 0.0000 | 28 |

| May 22, 2009 | -0.00040 | 0.0000 | 67 | -0.00656 | 0.0002 | 38 | -0.0067 | 0.0013 | 40 |

| July 8, 2009 | -0.00336 | 0.0000 | 12 | 0.00873 | 0.0000 | 87 | 0.0096 | 0.0000 | 88 |

| August 20, 2009 | -0.00217 | 0.0000 | 25 | 0.00437 | 0.0000 | 76 | 0.0037 | 0.0000 | 75 |

| October 5, 2009 | -0.00418 | 0.0000 | 9 | 0.01328 | 0.0000 | 94 | 0.0160 | 0.0000 | 95 |

| November 17, 2009 | -0.00048 | 0.0000 | 27 | 0.00453 | 0.0000 | 69 | 0.0048 | 0.0000 | 71 |

| All periods | 0.00000 | 0.14635 | 46 | 0.00233 | 0.0000 | 62 | 0.00227 | 0.0000 | 60 |

| End date | Count | N | Percent |

|---|---|---|---|

| August 16, 2007 | 86 | 243 | 35 |

| October 1, 2007 | 39 | 249 | 16 |

| November 13, 2007 | 80 | 255 | 31 |

| December 28, 2007 | 42 | 252 | 17 |

| February 13, 2008 | 62 | 253 | 25 |

| March 31, 2008 | 51 | 250 | 20 |

| May 13, 2008 | 84 | 259 | 32 |

| June 26, 2008 | 57 | 258 | 22 |

| August 11, 2008 | 71 | 263 | 27 |

| September 24, 2008 | 72 | 256 | 28 |

| November 6, 2008 | 54 | 247 | 22 |

| December 22, 2008 | 25 | 248 | 10 |

| February 24, 2009 | 38 | 245 | 16 |

| April 8, 2009 | 27 | 256 | 11 |

| May 22, 2009 | 68 | 266 | 26 |

| July 8, 2009 | 47 | 267 | 18 |

| August 20, 2009 | 81 | 270 | 30 |

| October 5, 2009 | 60 | 272 | 22 |

| November 17, 2009 | 71 | 275 | 26 |

| All periods | 1,115 | 4,884 | 23 |

Share and Cite

Ho, S.W.; Lee, A.; Marsden, A. Use of Bayesian Estimates to determine the Volatility Parameter Input in the Black-Scholes and Binomial Option Pricing Models. J. Risk Financial Manag. 2011, 4, 74-96. https://doi.org/10.3390/jrfm4010074

Ho SW, Lee A, Marsden A. Use of Bayesian Estimates to determine the Volatility Parameter Input in the Black-Scholes and Binomial Option Pricing Models. Journal of Risk and Financial Management. 2011; 4(1):74-96. https://doi.org/10.3390/jrfm4010074

Chicago/Turabian StyleHo, Shu Wing, Alan Lee, and Alastair Marsden. 2011. "Use of Bayesian Estimates to determine the Volatility Parameter Input in the Black-Scholes and Binomial Option Pricing Models" Journal of Risk and Financial Management 4, no. 1: 74-96. https://doi.org/10.3390/jrfm4010074

APA StyleHo, S. W., Lee, A., & Marsden, A. (2011). Use of Bayesian Estimates to determine the Volatility Parameter Input in the Black-Scholes and Binomial Option Pricing Models. Journal of Risk and Financial Management, 4(1), 74-96. https://doi.org/10.3390/jrfm4010074