What Is the Effect of Oil and Gas Markets (Spot/Futures) on Herding in BRICS? Recent Evidence (2007–2022)

School of Business & Management, Royal Holloway, Egham TW20 0EX, UK

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2023, 16(11), 466; https://doi.org/10.3390/jrfm16110466

Submission received: 16 September 2023

/

Revised: 14 October 2023

/

Accepted: 19 October 2023

/

Published: 27 October 2023

(This article belongs to the Special Issue Financial Assets as Profit-Makers in Inflationary Periods)

Abstract

:We investigate the effect of gas/oil markets (spot/futures) on herding in stock markets in BRICS over 15 years (2007–2022). We consider the effect(s) of crises (Global financial, European debt, COVID-19, and Russia–Ukraine war), bull/bearish energy markets, volatility, and speculation. The effect of gas and oil markets on herding in stock markets is minimal, and investors herd selectively during crises. Even during the ongoing Russia–Ukraine war, the effect of energy markets on herding in BRICS is minimal. Causality tests show that oil (spot/futures) Granger causes CSAD during COVID-19 only. Gas (spot/futures) has no effect. We also find that energy (spot/futures) market states (bearish/bullish) have no effect on herding in stock markets. Low volatility in energy markets can trigger herding (consistent with previous research in US, China) in all BRICS. Speculative activities during (non)crises appear to have minimal impact on herding. However, as the degree of intensity (volatility) in speculative activities increases in oil/gas, it causes herding in all countries (India is affected mostly), except Brazil. It is not the speculation activity per se in (non)crises that causes herding, but the intensity/volatility in speculation activity. Overall, oil/gas markets (especially gas markets) appear to have a smaller impact on herding than expected, contrary to public belief; however, as the intensity/volatility in speculative activities increases, then herding also increases, which is expected given the uncertainty that speculation causes.

JEL Classifications:

G14; G15; G411. Introduction

Over the past century, behaviour finance, as a subfield of behaviour economics, has been concerned with psychological and bias effects on financial markets and the economic environment, especially on investment decisions. This subfield can be traced back over 150 years and has begun to attract more interest from researchers, practitioners, and policymakers since the recent experiencing of several crises (such as the 1997 Asian Crisis, the 2000 dotcom crash, and the 2008 global financial crisis). Within the massive ‘heuristics’ and ‘cognitive effects’ sector of this field, the topic of herding is one of the most active areas in behaviour research, which is defined as a form of regret aversion and a collective behaviour where participants adopt actions and make decisions depending solely on others’ choices rather than on their own judgements and analysis (Liao et al. 2011). Moreover, herding, as one of the representatives of emotional bias, can be utilised to explain certain anomalies (such as the occurrence of bubbles and low-beta anomaly) and somewhat indicates the failure of the efficient market hypothesis, because investors are bounded-rational subjects who use rules of thumb and acquire imperfect information instead of applying their reasoning when making decisions (Ivanov et al. 2009; Baddeley et al. 2012). As a result, herding may somewhat trigger excessive market volatility and convergence in investment directions.

Previous studies have primarily concentrated on the herding effect itself in single asset markets (such as equity or bond markets), but have ignored the effect of external factors on herding or the spillover effect between equity markets and other markets. Therefore, we will introduce a new perspective of herding research in this study. We will explore how energy markets can exert influence on investors’ behaviour in equity markets. This investigation will be carried out from a global perspective and will include five emerging markets, namely, Brazil, Russia, India, China, and South Africa (BRICS).

When it comes to the rationale behind the selection of the sample markets and this topic, there are several motivations. In the first place, a large and growing body of literature pays particular attention to the crucial role of the commodity market (especially the oil and gas market). As noted by Wang et al. (2022) and Rapier (2020), oil, as a core raw material of modern industries, remains on top, accounting for almost 33% of total energy consumption.

The second motivation for this study is the close link between the equity market(s) and the commodity market(s), from both theoretical and practical points of view (Meyer 2022; Degiannakis et al. 2018; Gatfaoui 2016; Bashir 2022; Acaravci et al. 2012). Oil can be seen as playing an important strategic and political role in the equity market and the economic cycle. To date, the literature concerning the effect of oil on the stock market has heightened. For example, Apergis and Miller’s (2009) work on the importance of oil is complemented by BenMabrouk and Litimi’s (2018) study, which emphasised that oil not only possesses an ability to predict the real economy—such as GDP, exchange rate, and CPI—but can also have great repercussions for stock prices and various sectors, including transportation, heating, and financial. On the other hand, studies have suggested that different markets present diverse behaviour when facing price fluctuations or speculative activities regarding crude oil, such as significant herding in the Gulf Arab stock market (Balcilar et al. 2014), but anti-herding in Turkey (Cakan et al. 2019a). In terms of the other side of the coin, it is fitting to discuss the connection between natural gas and the stock market. Indeed, there exist many published studies that have discussed the impact of natural gas price shocks and volatility on the equity market for developed and emerging markets (Acaravci et al. 2012; Dai and Zhu 2022; Wadhwa and Darad 2022; Cliffe 2022).

In terms of the reason for selecting the BRICS countries as the sample, it is the crucial role of BRICS in the global energy market. According to Nasir et al. (2018), BRICS countries consist of both oil-exporting countries (Russia and Brazil) and oil-importing countries (India, China, and South Africa). In 2021, Russia and Brazil were the second and tenth largest oil exporters in the world, respectively (Workman 2022a). Considering growth rates, Brazil can be regarded as one of the fastest growing crude oil exporters since 2020. Moreover, China and India can be ranked as the first and third largest economies importing crude oil in 2021, respectively (Workman 2022b). As for natural gas, all of the BRICS markets, apart from Russia, can be regarded as natural gas importers. Brazil, China, India, and South Africa’s imported gas accounts for a relatively large proportion of total natural gas consumption, specifically 50% for Brazil, 45% for China, 37% for India, and 78% for South Africa (de Oliveira 2022; Kemp 2022; Worldometer 2015a, 2015b). In addition to this, Russia is the leading country and one of the largest natural gas producers; for instance, approximately 45% of the natural gas in the European Union came from Russia (Pistilli 2022; Staff 2022). Therefore, in order to extend our current knowledge about the role of energy in BRICS countries, the issue regarding the relationship between the energy market (oil and gas) and herding will be examined.

Additionally, it is now well established, based on a variety of studies, that there exists a spillover effect between the energy market(s) and the equity markets in BRICS (Sadraoui et al. 2022; Boubaker and Larbi 2022). More specifically, Boubaker and Larbi (2022) echoed Sadraoui et al. (2022), suggesting that stock markets in BRICS are undeniably affected by risk spillovers from energy markets and such a relationship can enhance impulsiveness in stock markets, which can make investors further increase hedging. Moreover, evidence provided by Hashmi et al. (2022) served to illustrate a positive effect of oil price on the stock market, as well as an impact of volatility of the stock market on the volatility of crude oil in China. To further demonstrate the relationship between oil and the stock market, Ono (2011) utilised a VAR model and concluded that stock returns positively respond to changes in oil prices in three BRICS member markets, except for Brazil, between 1999 and 2009. With respect to the relationship between natural gas and the stock market, a weaker co-movement can be reported in BRICS countries compared to that seen in the crude oil market (Mensi et al. 2021). The relationship between energy market(s) and stock market(s) has been widely examined and investigated considering price, return, and volatility. However, there is limited evidence to explain and analyse the relationship between investors’ behaviour when it comes to trading (e.g., herding) and commodities, including oil and gas. Therefore, our study will choose the BRICS countries as sample markets, which can provide additional evidence in this field. The purpose of this work is to allow investors to better understand the commodity market’s effect on the BRICS stock markets and make it possible for those investors to select a more suitable time to invest in, or withdraw from, the BRICS equity markets.

The last motivation behind selecting the BRICS countries as the sample can be ascribed to the characteristics of their stock markets. According to statistical data from Büge et al. (2013), four members of the BRICS group have a high percentage of state (national)-owned companies (NOCs)—96% in China (ranked 1st), 81% in Russia (ranked 3rd), 59% in India (ranked 7th), and 50% in Brazil (ranked 8th). NOCs play key roles in global energy, especially for the oil and gas industry in developing markets. According to reports and predictions of the International Energy Agency (IEA), NOCs have become dominant forces in the global energy industry and are expected to account for approximately 80% of the total rise in global oil and gas production (IEA 2008). As significant players in energy projects, NOCs are estimated to provide a large proportion of oil reserves, ranging from 80% to 90%, and are more likely to become the main source of all new oil suppliers achieving a 90% share, which will dominate the markets. (The Economist 2011; Austin 2009). As energy prices rise and geopolitical crises increase, NOCs can gain more advantage over private companies due to more diplomatic and financial support acquired from home governments (Chen and Jaffe 2007). Additionally, in order to control and stabilise the domestic energy market, NOCs sometimes have to sacrifice some part of their profits due to price caps set by government(s) (Austin 2009). This measure can somewhat protect the domestic energy market from international pressures. However, NOCs are also subject to criticism for their low transparency and inefficiency, human capital, capital accumulation, and tax burden (Victor 2007). Despite some limitations and criticism, NOCs will still dominate the market, and this tendency will be intensified. Therefore, in a study that investigates the effect of energy markets on stock market herding, selecting BRICS is quite suitable due to the fact that their markets are mainly composed of NOCs. On the other hand, although the BRICS countries have made important progress in opening their markets, there remain some restrictions on investments and transactions for foreign investors, such as short selling bans in India (Segal et al. 2022), as well as A-shares for domestic investors and B-shares for foreign investors in China (Segal and Scott 2021). The energy sector can be regarded as the first industry in which Foreign Direct Investment (FDI) occurred and is welcomed on a large scale globally based on considerations of market(s) liberalisation and increased supply security (Fleischmann et al. 2022). China has relaxed some parts of investment restrictions and has allowed investment in oil and gas since 2022 (Fleischmann et al. 2022). Despite some changes and policy reformation, there are still a considerable number of restrictions that are not abolished. Due to their specific FDI characteristics, the effect of energy markets on investor behaviour in equity market(s) may be different compared to Western countries or the rest of the world. Moreover, a seminal piece of work from Konradsson and Porss (2019) suggested that the BRICS countries can share similar systematic risk factors, whilst the work further reported that the BRICS countries can present fewer long-run co-movements with each other, which can satisfy the needs of diversification and risk management for international investors. Bouoiyour and Selmi (2016) showed that BRICS equity markets tend to embody heterogenous responses to oil prices using the frequency domain approach and causality analysis. Short-run causality is reported in India and South Africa, but a long-term effect is reported in the Chinese stock market. In the meantime, Bouoiyour and Selmi (2016) view different industrial production measures, financial system efficiency, market share distribution, tax policy, and regulation effectiveness as the most important factors that cause different degrees of impact of oil on stock return in BRICS. In light of the individual characteristics of BRICS equity markets, energy market(s) are more likely to exert a diverse impact on every BRICS market. Therefore, the relationship between BRICS and energy markets is an important and meaningful topic to be examined. Additionally, Adu et al. (2015) demonstrated that there are distinctively different patterns of stock returns between mature markets and emerging markets, such as high volatility and autocorrelated observable returns, as well as long-term return predictability. In other words, the BRICS countries can be considered as candidates and alternatives when investors try to construct global portfolio(s). The reason for this may well be that portfolios consisting of BRICS countries can achieve the goal of minimising risks without sacrificing adjusted and expected portfolio returns.

The main focus of this study will be the relationship between energy markets (including oil and gas) and herding in BRICS countries, whilst it will also compare differences and/or similarities in investors’ behaviour within these five sample markets after considering energy markets as an influence medium. Since they are representatives of emerging markets, the selection of BRICS countries can serve the purpose of gaining a relatively comprehensive understanding of the behaviour patterns of emerging markets under the influence of world energy markets. Nevertheless, much of the published research concerning this issue focuses on the developed markets or Gulf Cooperation Council (GCC) countries, such as the cases of the United States (BenMabrouk and Litimi 2018; Brunetti et al. 2013; Youssef and Mokni 2020), GCC markets (Balcilar et al. 2014, 2017; Ulussever and Demirer 2017), and Saudi Arabia (Gabbori et al. 2020), or on just one or two markets of the BRICS group, such as the cases of Brazil and Russia (Cakan et al. 2019a) and Chinese Stock Exchanges (Loang 2023). Most importantly, currently, there seems to exist a variety of published literature shedding light on the influence of global energy on the local stock market, which can be divided into two categories: (1) the effect of fluctuation in various energy indicators (energy price, return, volatility, speculative activities in either spot or futures market) on the performance of the equity market (Ross et al. 2021; Bernanke 2016; Alamgir and Amin 2021; Antonakakis and Filis 2013; Gatfaoui 2016); (2) the relationship between the energy market and investment behaviour (herding or trading preferences) (Cliffe 2022; Cattlin 2021; BenMabrouk and Litimi 2018; Cakan et al. 2019a; Ghorbel et al. 2014). The following cases can be regarded as a good illustration and summary, which makes it possible to capture previous research achievement and clearly clarify differences between our study and previous literature. Important work on the US herding phenomenon was undertaken by BenMabrouk and Litimi (2018), who showed that herding is more intense in the Capital Goods and Consumer Services as a result of a falling oil market. During an investigation into herding in Saudi Arabia, Gabbori et al. (2020) observed that herding in Saudi Arabia tends to be independent of oil volatility, but not of OPEC meetings—the stock market in Saudi Arabia is reported to herd on and around the days of OPEC meetings. With regard to BRICS, Youssef and Mokni’s (2023) work was complemented by Loang’s (2023) study, which agreed that the crude oil market causes herding in China (only in the Shanghai Stock Exchange) due to its high degree of globalisation and development. Cakan et al. (2019b) confirmed that a high-volatility regime can be regarded as the only driver of investors’ herding in the real estate investment market in South Africa. When considering the degree of integration between energy markets and BRICS stock markets, previous research has concentrated on a single market or just two markets, rather than including all BRICS members in a single study. The purpose of this study is to research how commodities (oil and gas) affect investors’ behaviour and to examine whether or not investors in the BRICS countries respond differently to energy markets when those markets are in different states. Additionally, this study will raise a question pertaining to whether the spot market and the future market of energy markets have a similar impact on investor behaviour in the stock markets of the BRICS countries. In other words, this study will be the first one to compare the effects of the spot market and the futures market for all BRICS in a single study. This can, in turn, offer those interested in investing in these countries or who set the rules a good opportunity to consider the similarities and uniqueness of the BRICS countries.

Cakan et al. (2019a) identified speculative activity as the major cause of herding, and highlighted, by utilising firm-level data, more prevalent herding in Russia and Brazil when the two emerging countries were experiencing a high degree of speculative activity in the oil market. In comparison to Cakan et al. (2019a), our study will take other possible influential elements into account besides speculative activities, including volatility and different market states of the oil and gas market. Unlike Cakan et al. (2019a), Balcilar et al. (2017) argued that speculative activities can be considered as positive signals to drive investment decisions away from market consensus, which can trigger anti-herding behaviour in oil-rich Gulf Arab stock markets; indeed, they formulated this argument after employing firm-level data and the Markov switching time-varying parameter herding model. More specifically, Balcilar et al. (2017) claimed that “speculative activities in the oil market, rather than oil price movements, are positively correlated with anti-herding in the stock markets of major exporters” and further explained that “traders take the speculative signals from the oil market as a sign of positive expectation and try to generate superior profits by going against the crowd in their local market”. As regards the effect of volatility, there exist many published studies describing the role of volatility in the stock market itself, rather than focusing on the importance of the volatility of the commodity market (e.g., Balcilar et al. (2014, 2017), Huang et al. (2015), Blasco et al. (2012), and Messis and Zapranis (2014)). In other words, research studies have not addressed, in detail, the different or similar influences of the spot market and the futures market on the stock market for BRICS countries during the past decade. Finally, the current study will examine the effect of the Russia–Ukraine war on the commodity market and further clarify the nature of the relationship between the commodity market (oil market vs. natural gas market) and investors’ behaviour in the BRICS countries during this period. According to a survey by GEP (2022), the Russia–Ukraine war suddenly changed the mode of supply chains and economies by affecting the price of global oil and gas. The price of oil skyrocketed from USD 76 per barrel in January 2022 to over USD 110 per barrel on 4th March 2022 (GEP 2022). Unsurprisingly, Henry Hub natural gas spot prices surged from USD 4.38 per million btu in January 2022 to USD 5.66 per million btu in October 2022, peaking at USD 8.81 per million btu in August 2022 (EIA 2022). That is to say, the sudden fluctuation of the oil and gas market may exert influence on the stock market, which could have an effect on investors’ confidence and sentiment, whilst also subsequently leading to a change in investors’ behaviour.

To prompt the results (most important findings), herding, appears to be unconnected to crises, contrary to public belief. Only China and India appear to herd responding to the oil market at different points in time (crises). South Africa herds to gas futures. Secondly, energy markets (and, specifically, different states of those markets (up/down)) exert no influence on investors’ behaviour—no herding reported for the whole sample in the stock markets. Remarkably herding in the stock markets appears enhanced in a low volatile environment (for gas/oil, mainly when volatility is less than 25% of the total distribution) for all BRICS countries. Investors are indifferent to herding as a result of speculation during (non)crises. Finally, Brazil is immune to speculative activities in the energy markets. Conversely, the rest of the countries exhibit herding when the volatility of speculative activities increases. It is not the speculation activity per se in (non)crises that causes herding, but the intensity/volatility in speculation activity.

This work has been organised in the following way. The next section will present a brief overview of the previous studies. Subsequently, we will present the data and methodology, before then going on to discuss, in detail, results produced by quantitative analysis. The conclusion will provide a brief summary, critique of the findings, and implications.

2. Literature Review

2.1. Relationship between Stock Markets and Commodity Markets

Numerous studies and reports have attempted to explain the association between the stock market and the commodity market. According to Motilal Oswal (2018), commodity markets can exert great influence on equity prices through two different channels due to different characteristics of equities, and these are commodity companies/stocks themselves and input-sensitive companies/stocks. More specifically, “commodity companies” can be defined as “output-sensitive stocks” and refer to entities that directly produce and sell related commodity products or services, such as copper producers, oil extractors, and gold mining. These companies’ business performance tends to directly rely on the price of commodities (Motilal Oswal 2018; DailyBulls 2023), whereas the second set of companies—“input-sensitive stocks”—is used to refer to organisations that are heavily impacted by changes of commodities’ price via the channel of costs. In other words, these companies are usually not commodity-related entities, but utilise commodities as input (Motilal Oswal 2018). For example, oil is an essential input for the paint industry or automobile industry. They can be affected by changes in the price of energy. In other words, the profitability of these companies tends to reduce in periods of increased ‘input’ prices due to higher transportation and manufacturing costs, but they outperform other industries when the price of commodities is on a downswing (DailyBulls 2023). Pinho and Maldonado’s (2022) cross-market analysis revealed that there are spillover effects between commodity markets (including oil, gold, copper, and agriculture) and stock markets, whilst it also showed that the return connection is stronger in the short run than in the long term. Most importantly, commodities can be regarded as a recommended hedge investment tool against inflation that can be used by investors due to their low or even negative correlation with traditional assets (Banton et al. 2022).

In detail, oil and natural gas, as two of the hard commodities, can have a close link with the equity market. Theoretically, oil price is a significant component of the value of output products, which can change production cost(s) and increase the price of the final outputs. In a randomised controlled study of the relationship between oil prices and the stock market, Groww (2022) agreed with Jones and Kaul (1996), pointing out that an increase in oil price can increase costs (e.g., transportation, equipment maintenance, and production costs) due to more expensive fuel, which can thus result in higher prices of products and, in turn, can reduce consumption. This, in turn, tends to somewhat affect demand for, and supply of, products, thus causing declines in companies’ profits and changes in the shares of firms. Therefore, such changes can lower profit margins and have adverse impacts on the stock market (Groww 2022). Similarly, a report/survey of Monthly Bulletin (2004) analysed data of the Dow Jones EURO STOXX index and turned out that a hike in oil price triggers a decrease in the expected rate of economic growth and also drives up inflation expectation, which further lowers firms’ earnings expectations, leading to a dampening effect on stock prices. This can be explained by the psychology of investors’ uncertainty towards the future outlook of corporate profitability, which, in turn, possibly results in relatively higher risk premia, exerting additional downward pressure on stock prices (Monthly Bulletin 2004). From another point of view, a marked rise in oil prices tends to contribute to a higher inflation level (named as “cost-push inflation”) and imbalance between demand and supply, resulting in higher prices for numerous goods and services, as well as an increase in households’ budgets (Federal Reserve Bank of San Francisco (FRB) 2007). Conversely, Ross et al. (2021) forwarded the perspective that whether oil prices can affect stock markets and economic status depends on the different industries being focused on. Meanwhile, they claimed that there seems to be a weak linkage between oil prices and the stock market on account of increasingly sophisticated methods with which to forecast future movements of oil prices. Therefore, firms can implement a sufficient number of measures to compensate for added fuel costs and switch operating strategies. Nandha and Faff (2008) showed that oil price indeed exerts great influence on equity markets for all 35 sample industries, but the degree and direction of influence is different, such as a positive effect of high oil price on the mining, oil, and gas sector, but a negative effect/association between high oil price and the other 32 industries. Likewise, by investigating 38 industries, Scholtens and Yurtsever’s (2012) comparative study found that the majority of industries tend to benefit from negative oil price shocks (that is, descending oil price), except mining, oil, and gas. Commenting on the sectoral effect, Elyasiani et al. (2011) provided similar evidence and underscored that there tends to be a quite different effect of oil prices for oil-substitute industries and oil-using industries, such as a positive relationship between increasing oil price and oil-substitute sectors (i.e., coal, oil refineries, and electric-gas service), whereas a negative and indirect effect of positive oil price changes on oil-using sectors (i.e., metal, building, and air transportation).

Compared to the crude oil market, fewer researchers have been able to draw on any systematic research into the correlation between natural gas and the stock market. It is believed that hikes of natural gas can create pressure in the economy and increase the possibilities of inflation, especially for the electricity sector (Wadhwa and Darad 2022). In another major study, Acaravci et al. (2012) collected quarterly data for 15 European Union countries and underlined that the long-run relationship between natural gas and the stock market would vary with different sample countries; their results were obtained by means of the Granger causality models between 1990 and 2008. They discovered the existence of a long-term equilibrium relationship in Austria, Denmark, Finland, Germany, and Luxembourg, but found that this disappeared in the 10 remaining European Union sample countries. Overall, the relationship is not particularly straightforward.

2.2. Energy Market and Herding

Only in the past 20 years has research on herding directly addressed how the commodity market can influence investors’ behaviour, especially for energy market(s). In the context of equity markets in three oil-exporting countries (Saudi Arabia, Canada, and Russia) and three oil-importing countries (US, Japan, and China), Youssef and Mokni (2023) acknowledged that herding differed across all sample markets due to a negative correlation between oil-exporting countries and oil-importing countries. Simultaneously, the authors confirmed that a dynamic herding pattern existed by means of a time-varying parameter model, especially for China, and also supported that stronger herding occurred under the circumstance of increasing oil prices in Russia, Japan, and China. In the same vein, Balcilar et al. (2013) discovered that investors reacted by herding in oil-rich frontier markets (GCC countries), and oil price increases seemed to be associated with a movement out of ‘low’- into ‘high’-volatility states, during which herding behaviour was observed, pointing out that GCC markets tended to be well integrated with oil markets and can be easily impacted by global factors. Also, for the GCC countries, using the traditional CCK model and the Markov switching time-varying parameter model (MS-TVP), Balcilar et al. (2017) evaluated the effect of the crude oil market on investors’ behaviour in five Gulf Corporation Council (GCC) stock exchanges over the span of 10 years and identified that herding was only reported in volatile periods, disappearing during calm periods. This finding is in line with the result of a study by Balcilar et al. (2014), who highlighted that herding can also be recognised as a dynamic phenomenon and varies with changes in market states in GCC stock markets, and oil shocks can be regarded as a significant factor governing the transition to herding states.

In addition to research in oil-rich developing countries (GCCs), there is also research on renewable energy sources and herding. Trueck and Yu (2016) set out to solely investigate the renewable energy sector in the US between 2000 and 2015 and pointed out that the renewable sector seemed to switch back and forth between herding and anti-herding, given changes in oil price and investors’ beliefs. More specifically, the authors concluded that a dramatic drop in oil price can stimulate herding in the renewables sector, while “anti-herding” is more pronounced during long periods of increasing oil price, which can be explained by the belief that investors are more likely to interpret and react differently towards “good news” or “positive oil return” for renewable energy stocks. Compared to crude oil, there is limited evidence to evaluate the effect of natural gas on investors’ behaviour, especially in the field of herding.

2.3. Geopolitics, Energy Market, and Herding

2.3.1. The Effect of Geopolitics on Energy Market

To date, several studies have assessed the nature of the relationship between geopolitics and commodities. For instance, Noguera-Santaella (2016) looked into a considerable number of global geopolitical events over the span of nearly 150 years (from 1861 to 2011) and the highly sensitive oil market. Noguera-Santaella (2016) documented that geopolitical risks occurring before 2000 can exert greater influence on actual oil prices. Recently, nearly all commodities reached a peak in the weeks following the Russia–Ukraine conflict, especially natural gas and crude oil; the two commodities simultaneously experienced greater volatility compared to stock markets (Costola and Lorusso 2022; Alam et al. 2022; Boubaker et al. 2022). In an investigation regarding the price and exports of natural gas and oil after the Russia–Ukraine war, Nadig (2022) reported an increase of 54% in European costs since the second half of 2021, tripled growth in the natural gas price, and a peak of USD 105 per barrel in crude oil price for the first time since 2014. In their analysis, the energy market is one of the most affected markets due to the conflict between Russia and Ukraine. They also report a relatively high-risk contagion between the metal market and the energy market. This finding is consistent with the perspective of Sansarlioglu (2022), who supported the notion that the Russia–Ukraine war can be regarded as a driver to trigger increased volatility and rapid fluctuation in commodities prices due to an imbalance between supply and demand. Both Olayele (2015) and Siapartners (2022) highlighted that geopolitics may overshadow the market and exert great influence on economic activities via affecting policies, consumer needs, and transmission, with an example being records of a new high in oil and natural gas, especially in Europe. Additionally, a detailed examination of geopolitics effects by Bricout et al. (2022) showed that geopolitics can still contribute to triggering fluctuations of European international oil companies (IOCs), but the influence has gradually diminished due to increasing awareness of the lowering usage of oil. However, the above-mentioned authors (Bricout et al. 2022) also emphasised that the influence of geopolitics on gas can still be strong due to the fact that it is indispensable at the moment.

2.3.2. The Effect of Geopolitics on Herding

The existing literature on the relationship between geopolitics and herding has been extensive and focused particularly on the degree of the effect. Historically speaking, geopolitical risks can somewhat lead to rising volatilities in financial markets and fluctuations of economic activities due to increased uncertainty and decreased investors’ confidence; examples in this regard are the average 6.2% sell-off in the S&P 500 during various geopolitical events, as well as longer-lasting negative economic impacts and disruption of energy markets after the Arab oil embargo in 1973 (Abrahamian 2022). In a study conducted by Krishna and Suresha (2022), it was shown that herding intensified during the India–China geopolitical conflicts of 2020, with the Hurst exponent/coefficient (a representative indicator of herding behaviour) reaching 0.72 throughout the overall intensified geopolitical conflicts event window, and was prevalent in the three major National Stock Exchange sectoral indices (Auto, Energy, and Pharma) on account of high reliance on Chinese supplies and trade linkages with China.

Since the beginning of 2022, the eruption of the Russia–Ukraine crisis has rapidly become a popular topic and grabbed the whole world’s attention. In such a context, Bougatef and Nejah (2023) utilised the CSAD model to describe investors’ behaviour pattern before and during the war by selecting 40 firms listed in the Moscow stock exchange as a sample between 16 June 2021 and 30 November 2022. In their analysis of the relationship between herding and geopolitical risk, Bougatef and Nejah (2023) highlighted that the outbreak of the Russia–Ukraine tension prompted herding. This evidence seems to corroborate the psychological theory, which suggested that investors are inclined to put aside their beliefs and, in turn, herd towards the crowd when they sense a danger or face a great degree of market uncertainty (Christie and Huang 1995; Devenow and Welch 1996).

Unlike the above studies, Espinosa-Méndez (2022) reported reverse herding in Chile during civil unrest, which can be explained by the psychological factor that investors and agents start to distrust and become suspicious of the decisions made by the most informed and professional specialists when facing future uncertain market volatility. This can be explained by the ‘relative deprivation’ theory, which suggests that economic inequality and dissociation between expectations and actual experience makes people dismiss objective information and engage in subjective consideration, leading to the appearance of reverse herding (Power 2018).

This view is similar to Mertzanis and Allam’s (2018) evidence indicating the existence of anti-herding in emerging markets when investors face periods of political instability. To determine the presence of (anti-)herding in Egypt, Mertzanis and Allam (2018) employed both daily and monthly returns of the EGX30 index as a proxy from 2 January 2003 until 15 April 2014 as the sample period including the 2011 revolution. One unanticipated finding was the anti-herding phenomenon in the Egyptian stock market after the revolution, regardless of the normal/bullish/bearish market. This rather contradictory result may be due to the control of daily price fluctuation limits and the absence of short-selling, which can be regarded as the most important factors to discourage excessive herding and even preclude speculators or irrational investors re-entering the stock market (Mertzanis and Allam 2018). Another possible explanation for this result might be that investors are better aware of the true idiosyncratic risks of stocks and become more prudent regarding their future investment positions, leading to the appearance of more rational investors (Mertzanis and Allam 2018).

2.4. Speculative Activities, Energy Market, and Herding

The Effect of Speculation in Energy Market on Herding

Apart from a close connection between speculative activities and the energy market, there are a few studies that shed light on the impact of speculation in energy markets on herding. Balcilar et al. (2017) can be considered as one of the representative cases in this field. Balcilar et al. (2017), in their study, noted that speculative activities in the oil market can cause anti-herding to occur amongst major oil exporters, particularly in Saudi Arabia and Qatar. The observed anti-herding behaviour between the oil market and GCC stock markets can be explained in the following way. The speculative signal from the oil market can be interpretated as a sign of positive oil price movement, and, therefore, traders expect to generate superior profits by making independent investment decisions and trading away from the market consensus after their analysis of acquired information (Balcilar et al. 2017). However, another seminal article was published in 2019, which pointed out that a higher degree of speculative activities in the global oil market triggered more intensive herding in Russia and Brazil (Cakan et al. 2019a). There is one likely cause for the association between a high level of speculative activities and a great degree of herding, that is, investors are apt to view frequent speculative activities in the oil market as signals of increasing uncertainty towards the oil market itself, the local stock market, and future global economic expectations, which leads to a greater level of willingness to follow the crowd and mimic others’ trading behaviour instead of believing in their own judgement and confidently diagnosing acquired private information in order to gain a sense of security (Cakan et al. 2019a; Devenow and Welch 1996). Obviously, there is no consensus regarding the effect of speculative activities in the oil market on herding. Commenting on herding, Pompian (2017) summarised that herding, as a reactive phenomenon, indicates convergence of behaviour and participating in the crowd’s behaviour, which can trigger the occurrence of speculative bubbles in different markets (such as the stock market and real estate market) and result in irrational asset prices, which can stimulate numerous capital inflows into specific asset classes, creating a tsunami-like effect. A similar study by Brunetti et al. (2013) could not find strong evidence to support a connection between herding by speculative traders and the crude oil market for either swap dealers or hedge funds.

2.5. Volatility in Energy Markets, Stock Markets, and Herding

2.5.1. The Effect of Volatility in Energy Market(s) on the Stock Market(s)

It is now well established, based on a variety of studies, that there exists a spillover effect between the volatility of the oil and gas market and the volatility of the stock market. As indicated by Sadorsky (1999), there are asymmetric effects between oil price shocks and the equity market and economic activity, meaning that there is a one-way influence path from oil price shock(s) to stock returns and the economy, but there is limited impact reported on the opposite direction. More specifically, it is suggested that positive oil price shocks are very likely to depress real stock returns (Sadorsky 1999). Joo and Park (2021) and Jones and Kaul (1996) outlined that oil price shocks and uncertainty can have a negative effect on trading in global stock markets and stock returns. Their test confirmed that oil prices fluctuation has a detrimental impact on real stock returns and output in the US, Canada, and Japan during the post-war period. Additionally, Pindyck (2004) shows that crude oil volatility, to a certain degree, has predictive power when it comes to natural gas, but not the other way around. As noted by Hampton (2022) and Groves (2022), natural gas can be considered a financial instrument, and sharp swings in natural gas can bring about investment opportunities for traders, accompanied by high risks. On the other hand, a huge surge in natural gas leads to increased market volatility (Chandler 2022).

2.5.2. The Effect of Energy Market Volatility on Herding

In recent years, the issue pertaining to the association between herding and the volatility of commodities has attracted increasing interest from practitioners and policymakers. In a comprehensive study of herding, Gabbori et al. (2020) surprisingly found that herding was independent of oil market volatility in the Saudi Arabia Stock Market. Similarly, BenMabrouk and Litimi (2018) selected, as a sample, all domestic US firms listed on the equity market over the span of 17 years and divided all sample companies into 12 sectors. An interesting finding emerged, i.e., that there was a significant linkage between the oil market and herding within the Capital Goods and Consumer Services sector for the whole sample period, but the volatility of the oil market can reduce herding and even generate anti-herding for all other sectors.

2.6. Relationship between Energy Market, Stock Market, and Herding in BRICS

2.6.1. Relationship between the Energy Markets and the Stock Markets in BRICS

There exist many published studies describing the role of oil and gas and their connection with financial stock markets in BRICS countries. Brazil, as one of the largest oil exporters, has surprisingly experienced growth of 30% in the equity market, which is due to rises in oil prices since the beginning of 2022 (Mellow 2022). Surveys, such as that conducted by Ferreira et al. (2020), have shown that the Brazilian financial sector has greater exposure to oil returns, which can provide some considerations and implications for both investors and authorities. This finding is similar to the perspective put forth by de Salles (2019), who highlighted a close linkage between crude oil fluctuation and the Brazilian stock market. Taking the case of India, Mahunta (2011) focused on the long-term effect of the international crude oil price on the Indian stock market, and Granger causality results revealed the existence of a unidirectional causality just from the crude oil market to the stock market. This view is supported by Yadav et al. (2020), who underlined that crude oil is a driver that leads to price discovery in the Indian equity market using a VAR model—a finding that can benefit investors who seek to diversify portfolios and offers a new insight to regulators who formulate related economic policies to balance the relationship between energy market(s) and the financial world. With respect to South Africa, Sanusi and Kapingura (2022) drew on an extensive range of sources to assess the interaction between the equity market and oil price. They subscribe to the view that changes in equity market performance stem from erratic oscillation in oil prices (using a time-varying approach and Markov regime switching VAR model) due to its heavy reliance on oil imports. Taking the above as their main focus, Hashmi et al. (2022) used a VAR-DCC-GARCH model to test the interaction between crude oil and the Chinese stock market over the span of 19 years. In detail, they proved that there tended to be a positive spillover effect between the crude oil fluctuations and equities in both directions, whilst they noted that the effect was stronger for mining, chemical, nonferrous metals, and steel. Wen et al. (2019) show that there is a significant bilateral nonlinear causality between oil prices and the Chinese equity markets due to increased demand and high dependence on oil imports. Conversely, Cong et al. (2008) illustrated that there seemed to be no significant interaction between oil price shocks and most Chinese equity indices, excluding the manufacturing index and some oil companies. Mensi et al.’s (2021) cross-country analysis utilising the wavelet method showed that there is a relation between oil and the BRICS stock market, and that the observed co-movement could have reached its peak during the 2008 global financial crisis. In a comparative study, Bouoiyour and Selmi (2016) proposed that the impact of oil price on stock returns in BRICS tends not to be uniform, but heterogeneous. Oil prices have a medium- and long-term potential effect on Brazilian, Russian, and Chinese shares, but a short-run effect on India and South Africa due to their different characteristics, such as oil dependence, financial system efficiency, securities regulation effectiveness, and market share distribution. Specifically, South Africa and India showed short-run causality running from real oil prices to stock returns. On the other hand, long-run causality can be reported in the other countries, which can be attributed to their high concentration on oil sectors and high dependence on oil importing—more than 50% of shares in Brazil and 60% of shares in Russia belong to oil-related companies; likewise, dependence on oil imports and oil intensity of China accounts for 32.8% and 23%, respectively (Bouoiyour and Selmi 2016). To conclude, oil exerts influence on these countries in different ways.

Relative to oil, less attention seems to be paid to issues regarding the relationship between natural gas and the equity market. According to Mensi et al. (2021), natural gas has the highest systematic risks compared to the stock market and crude oil. With respect to the influence of natural gas on equity markets in BRICS, Sadraoui et al.’s (2022) comparative study found significant evidence of a dynamic spillover effect between natural gas and the stock market in the BRICS countries, thus signifying higher prediction of impulsiveness in the equity market after investors have acquired information relative to gas prices. Kumar et al. (2019) mentioned that there seems to be no long-run causality between energy futures and the Indian stock market, but they also emphasised that investing in natural gas futures can have better hedge effects when investors consider establishing comprehensive and diversified portfolios in the Indian stock market on account of their characteristic of sometimes exhibiting abrupt movement with the stock market. Using the variance decomposition approach, Costola and Lorusso (2022) did conclude that increased uncertainty in Russian geopolitical conflicts may prompt a significantly positive spillover connectedness of future energy commodities volatility, including oil and gas. Last, but not least, they did report that Russian energy industries can be regarded as net shock transmitters to energy commodities.

2.6.2. Relationship between Energy Markets and Herding in BRICS

With respect to the relationship between herding and oil, more attention has been drawn on this field in recent years. Cakan et al. (2019a) provided an in-depth analysis for emerging markets, showing more prevalent herding in the case of Russia. In their seminal article, they identified that speculative activities in the global oil market can be significantly associated with investors’ herding behaviour in Russia and Brazil. The reason for this can be attributed to the investors’ psychology, i.e., that a high level of speculative activities in the oil market can be deemed a sign of increased uncertainty in terms of the direction of global demand, thus causing a greater tendency to follow the market consensus, so as to avoid investment mistakes. In addition, Chang et al. (2020) extended the current understanding of oil’s impact on the stock market and demonstrated a stronger herding tendency during extreme low oil prices, especially for fossil fuel energy sectors. This surprising and interesting result can be explained by the fact that extreme low or negative returns can be regarded as bad news in the oil market, which can have direct effects on energy sectors. In other words, investors’ behaviour in the energy sector seems to be sensitive to dynamic changes in the oil market (Arjoon and Bhatnagar 2017; Balcilar et al. 2013). Simultaneously, it is worth noting that there tends to be strong cross-sector herding and risk spillover effects from the US fossil fuel energy market to any renewable energy markets in normal periods. This is prevalent in the US market, but disappeared in European and Asian markets during the SARS epidemic (Chang et al. 2020). In a case study of herding in Indian energy commodity futures, Dewan and Dharni (2022) observed the absence of herding amongst energy commodity futures, except for downward market states, but reported a higher degree of herding behaviour for energy commodities during more volatile periods.

Given the literature above, our research hypotheses are as follows:

Hypothesis 1 (H1):

Energy markets have an impact on herding in stocks markets (‘rejected’).

Hypothesis 2 (H2):

Energy markets have an impact on herding in stocks markets during crises (‘rejected’, no unanimity, investors herd selectively at different points in time/crises).

Hypothesis 3 (H3):

Returns performance in energy markets Granger cause CSAD (‘rejected’, limited evidence).

Hypothesis 4 (H4):

A bullish energy market has an impact on herding in stock exchanges (‘rejected’).

Hypothesis 5 (H5):

High volatility in energy markets has an impact on herding in stock exchanges (‘rejected’).

Hypothesis 6 (H6):

Speculation in energy markets during crises has an impact on herding in stock exchanges (‘rejected’).

Hypothesis 7 (H7):

An increase in intensity/volatility in speculative activities in energy markets during crises has an impact on herding in stock exchanges (‘not rejected’).

3. Methodology and Data

3.1. Data and Sample(s)

The stock indices covered include Brazilian IBOVESPA, Russian MOEX Index, Chinese CSI 300, Indian S&P BSE SENSEX, and South African FTSE/JSE Africa All Share Index1. All data were collected from Bloomberg.

In addition, the Henry Hub Natural Gas Index2 and Brent Oil Index3 were selected as proxies to capture gas and oil price movements. The data were collected from the US Energy Information Administration. Secondly, in order to achieve the research goal of detecting similarities/differences regarding the impact of the energy spot and futures markets on the stock markets in BRICS, two different futures contracts, namely, Generic 1st “CO” Futures and Generic 1st “NG” Futures, will be selected as the research basis4; data on these contracts were collected from Bloomberg.

The whole sample period will cover 15 years, from 17 May 2007 to 13 May 2022. Several important events will also be taken into account. Our sub-periods analysis includes the following events: (1) “Global Financial Crisis (15 September 2008–31 March 2009)” (Lin et al. 2013; Aït-Sahalia et al. 2012); (2) “European Debt Crisis (1 April 2010–31 January 2012” (Dos Santos and Lagoa 2017); (3) “COVID-19 Crisis (31 December 2019 to 13 May 2022” (World Health Organization (WHO) 2020); and (4) “Russia–Ukraine War (24 February 2022–13 May 2022) (Psaropoulos 2022)”. The aim of this division/sample splitting is to establish whether event effects exist and whether investors tend to behave in different ways when there are sudden changes in market conditions, especially the occurrence of crises.

3.2. The Basic Model

We employ daily closing prices of market indices and individual stocks in BRICS countries to calculate market returns and individual stocks’ returns, respectively, via the following formula: . All empirical or statistical herding models can be divided into two categories: (1) based on holding and transaction data; and (2) based on returns data. Our research will adopt the second method and focus on returns’ dispersion or convergence. Compared to the other methods, the approaches utilising returns data can be more suitable when it comes to detecting and tracing time-variation herding in the context of emerging markets, because these methods take securities into account. Therefore, the returns’ dispersion is measured using the cross-sectional absolute deviation, as follows (Chang et al. 2000):

where

- (1)

- —Cross Sectional Absolute Deviation at Time t;

- (2)

- —Market Return at Time t;

- (3)

- —Return of Individual Stock at Time t;

- (4)

- N—the Number of Sample Stocks.

The model will become the benchmark for all the following models. Model (2) can serve as a valid model with which to detect herding. The CSAD indicator is not a measure of herding, but rather the parameter calculated by regressing CSAD on squared market return captures herding behaviour. The presence of herd behaviour is confirmed if is significantly negative.

3.3. Models for Detecting Herding between Energy Markets and Stock Markets

After introducing the basic herding model, the effect of energy markets on investors’ behaviour will be tested. To establish whether there are herding effects between energy markets and the behaviour of stock markets in BRICS countries, the return of crude oil and natural gas will be added to the regression model (Equation (2)) as one of the variables. Most importantly, spot markets and futures markets will be taken into account in this part. The model will be modified as follows:

where

- (1)

- —Daily Return of Brent Oil Index;

- (2)

- —Daily Return of Oil Generic 1st “CO” Futures;

- (3)

- —Daily Return of Henry Hub Natural Gas Index;

- (4)

- Daily Return of Natural Gas Generic 1st “NG” Futures.

A significantly negative captures herding behaviour, which means that the crude oil market or natural gas market can cause herding.

According to Hoque et al. (2020), oil and gas can be considered significant risk factors in terms of exerting influence on stock returns for oil and gas sub-industries, and this effect varies across sub-industries. In the previous sections, it was noted that an increasing number of articles have examined the effects of crude oil on the equity market compared to natural gas and the equity market. To extend understanding in this area, Kouchaksaraei et al. (2016) examined the relationship between gas prices and the performance of the stock exchange. In their research, there tended to be a two-way causality relationship between natural gas prices and the equity market in Russia and Norway—a relationship that was established via use of the Granger causality test. Therefore, prior literature has provided pieces of evidence to support the notion that natural gas prices can be considered a risk factor in terms of causing movements in the equity market. However, so far, to the best of our knowledge, no studies have considered how fluctuations in gas prices influence investment decisions and investor psychology, causing changes of behaviour. In order to bridge the research gap in this field, the current study will become the first empirical study to focus on the relationship between the natural gas market and the behaviour of stock markets in BRICS countries.

Aside from the spot market, which will certainly be considered, the futures market will become one of the significant elements to be introduced into this study. Therefore, the current study will become the first piece of work to incorporate both the spot market and the futures market into one research study. The aim is to observe whether the spot market and the futures market tend to have similar directions in terms of exerting influence on investors’ behaviour in the stock market; the degree of the effect will also be tested.

3.4. Crisis Events and Herding

3.4.1. Regression Model

In addition to the effects of energy markets on the stock market during the complete sample period, several important events will be added as distinct periods in order to determine changes in markets. According to Joo et al. (2020), it can be shown that an economic recession, such as that brought on by the 2008 Global Financial Crisis, can trigger rises in crude oil price, but it can also be found—interestingly—that the identified tendency can eventually revert to its original state. The Russia–Ukraine conflict could bring about or exacerbate an existing energy crisis. It could drive up prices of natural gas and even slow economic growth on account of high inflation rate and fuel shortages (IEA 2022). Therefore, the current study will consider both the effect of economic crisis and the effect of geopolitics, whilst the effect of a public health crisis (COVID-19) will also be addressed. The reason for this is that COVID-19 can somewhat impact economic development and disrupt supply chains. After taking the effect of crises events into account, the herding model will be modified as follows:

Crisis events stand for periods of Global Financial Crisis, European Debt Crisis, COVID-19 Crisis, and the Russia–Ukraine war. If is significant and negative, then this indicates the presence of herding. Most importantly, a greater value of can signal a stronger herding tendency.

3.4.2. Granger Causality Test

In addition to the regression model(s), a method known as the Granger causality test will be applied to further test the connection/causality between CSAD and energy markets returns during the four crisis periods. The Granger causality test was first put forward by Granger (1969) with the aim of identifying causality between time series data. It does not imply that one variable causes the other. It means that one variable contains info about the other. This is similar to the approach used in Galariotis et al. (2016) between CSAD and liquidity, while, in this study, we use CSAD and energy market performance, as stated above.

3.5. Different States for Energy Markets and Herding in Stock Markets

Regression Model

Equation (3) can be regarded as the model to detect the effect of energy markets on investors’ behaviour in the equity market during the complete sample period. In addition to the traditional model, the current study will also consider whether the effects will remain constant or will change with the altering of market conditions; in this way, the present study will be more comprehensive. In other words, this study will examine whether increased periods or decreased periods will trigger more of a herding phenomenon compared to normal states of energy markets. The purpose is to distinguish how fluctuations of the oil/gas market can result in a change of investors’ behaviour. Therefore, on the basis of the model (Equations (2) and (3), page 370) proposed by Galariotis et al. (2016), the variable named ‘energy market returns’ will be added to the model in order to establish a connection/relation between behaviour in the stock market and the performance of the energy market(s). The new modified model is presented below:

‘Up periods’ represent returns of oil and gas markets (including both the spot and futures markets) that are positive—greater than zero, while ‘downward periods’ capture negative returns of energy markets. According to the above models, a significantly negative indicates the occurrence of herding behaviour.

3.6. Volatility in Energy Markets and Herding in Stock Markets

The impact of volatility on herding behaviour has been well documented in the literature, with examples including Huang et al. (2015) and Balcilar et al. (2013). However, these articles have focused solely on the volatility of the equity market itself, whilst limited work has attempted to address the issue pertaining to the relationship between the volatility of energy markets and behaviour in stock markets. The current study will provide a new approach, so as to shed light on the connection between the volatility of energy markets and investors’ behaviour in BRICS countries.

3.6.1. Spot Market Volatility

Risk, as a crucial element of financial analysis, has always received much attention, both for risk management and for regulatory purposes. To date, various methods have been developed and introduced to measure volatility, which are classified into three types: implied volatility, conditional volatility, and historical volatility. Schwert (1989) has shown that higher average volatility is more likely to occur in recession periods. Studies concerning volatility contribute to understanding the fluctuation of financial markets, which may extend the understanding of investors’ behaviour due to swings of psychology and emotion.

More specifically, the GARCH model will be utilised to examine volatility of the spot market; indeed, this model was put forward by Bollerslev (1986) and Taylor (1987) and allows the conditional variance to depend on previous lag(s) on the basis of Engle’s (1982) ARCH model. Compared to the ARCH model, the advantage of the GARCH model is that it has better prediction ability with fewer variables and simultaneously avoids overfitting due to its characteristic of negativity constraints (Akgiray 1989; Brooks 2014). To examine the possibility of a relationship between GARCH volatility of the spot price/returns in energy markets and investors’ behaviour in equity markets, the GARCH model5 is presented in the following equations (the herding model is presented separately in the sections that follow further down):

where

- (1)

- : Daily Return of Brent Oil Index or Henry Hub Natural Gas Index at Time t;

- (2)

- : Daily Return of Brent Oil Index or Henry Hub Natural Gas Index at Time t − 1;

- (3)

- : GARCH Volatility of Crude Oil or Natural Gas Spot Market at Time t.

To determine whether different levels of volatility (and methods of calculating it) can trigger similar effects (of various degrees), a second method will be introduced to calculate volatility, namely, the EWMA model. The EWMA model is an acronym of exponentially weighted moving average and plays a fundamental role in computing return volatility in the area of risk management; the model was established by J.P. Morgan/Reuters (1996), who have teamed up to enhance RiskMetrics (also known as exponential smoother). Compared to the GARCH model, its strength is computation simplicity and its ability to better capture autocorrelation of the squared return; it also has greater forecasting capacity with regard to real data on account of its characteristic of dependency on the decay parameter (Ding and Meade 2010; Araneda 2021). Therefore, the EWMA model is as follows:

where

- (1)

- : EWMA Volatility of Oil or Natural Gas Spot Market at Time t;

- (2)

- : First-ordered Lagged Volatility.

3.6.2. Futures Market Volatility

In addition to considering the spot market, the futures market will also be taken into account in the current study. The aim in this regard is to offer a chance to compare the difference between the two types of energy markets in terms of effects on investors’ behaviour in equity markets. There exists a considerable amount of literature illustrating that volatility can trigger more speculation activity (Algieri and Leccadito 2019; Brunetti et al. 2016). Moreover, some studies have found that volatility increased herding tendency (Mandaci and Cagli 2022; Bouzid 2022; Bekiros et al. 2017). However, the majority of these studies investigated the effect of volatility on return performance and investors’ behaviour within the same financial market, rather than across different markets (such as the effect of volatility in the stock market on herding behaviour in the stock market). Additionally, few studies have focused on the relationship between volatility in the futures market and herding in the equity market. Therefore, the present study will devote itself to researching this aspect. The range-based method (RS volatility model) proposed by (Rogers and Satchell 1991; Rogers et al. 1994) will be employed as the basis for calculating the volatility of the futures market using the following equation:

where

- (1)

- —RS Volatility of Oil or Natural Gas Futures at Time t;

- (2)

- Ot—Opening Oil or Natural Gas Futures Price at Time t;

- (3)

- Ct—Closing Oil or Natural Gas Futures Prices at Time t;

- (4)

- Ht—High Oil or Natural Gas Futures Prices at Time t;

- (5)

- Lt—Low Oil or Low Natural Gas Futures Prices at Time t.

To ascertain whether different volatility models yield the same results, another extra model, namely, the GK model, will be introduced in this study. Under the guidance of Parkinson’s (1980) model, Garman and Klass (1980) put forward a new method to calculate historical volatility via incorporating intraday variability information. The benefit is that this estimator takes advantage of commonly available price information, and the application of high-frequency data can make it a more precise model when it comes to testing volatility. In light of this, the GK model is presented below (the herding model follows in the next section):

where

- (1)

- GK Volatility of Oil or Gas Futures Market at Time t;

- (2)

- ;

- (3)

- .

3.6.3. The Effect of Energy Volatility on Herding in BRICS’ Stock Market

As mentioned in the previous paragraph, there is a consensus among practitioners and scholars that there is a close link (and cross effect) between market volatility and herding (e.g., Huang et al. 2015; Balcilar et al. 2013; Fei and Zhang 2023). Nevertheless, there is an ambiguous relationship between energy market volatility and equity herding in the current literature. In other words, there is lack of enough empirical research to expound on how fluctuation of the energy markets (including the spot and futures markets) can exert influence on herding in BRICS.

In this study, the purpose is to illustrate the connection between different levels of energy volatility and behaviour in BRICS. Therefore, three interactive dummies will be employed in this study, which will represent different degrees of volatility. The model is presented below:

where

- (1)

- —Captures Volatility in the Second Quartile (25% of Distribution < σ < 50% of Distribution) and gets the value of 1, otherwise 0;

- (2)

- —Captures Volatility in the Third Quartile (50% of Distribution < σ < 75% of Distribution) and gets the value of 1, otherwise 0;

- (3)

- —Captures Volatility in the Forth Quartile (σ > 75% of Distribution) and gets the value of 1, otherwise 0;

- (4)

- —Represents GARCH and EWMA Volatility of Oil and Gas Spot Market, as well as RS and GK Volatility of Oil and Gas Futures Market;

- (5)

- Note that captures the first quartile.

In terms of the above model, the basic model is divided into four sub-models based on different volatility distributions (such as high volatility or low volatility of energy prices). There are four states of the world (or four quartiles), so that we create three dummies to capture the second, third, and fourth quartile of volatility levels. If , and are significantly negative, this indicates that the corresponding level of volatility level will induce herding. Again, to clarify, the first quartile (<25% of the distribution) is captured by . No dummy is created for the first quartile, otherwise we would be introducing multicollinearity. This is similar to Equation (5), page 145, in Galariotis et al. (2016).

3.7. Speculative Activity in Futures Market and Herding in Stock Market

In this study, the issue pertaining to the effect of speculation in the energy market on herding in the equity market will be examined. The present work will select the speculation ratio introduced by Chan et al. (2015), who showed that the speculation ratio can be calculated as “trading volume to open interest” for Brent oil futures contracts. According to the definition, a lower ratio indicates lower speculation activity. All data are collected from Bloomberg. Unlike the above models in our study, this part will focus solely on the futures market. Therefore, the modified model, which includes the speculation ratio as its main characteristic, is presented in the following equations:

where

- (1)

- : Speculation Ratio of Oil or Natural Gas Futures Market at Time t;

- (2)

- : Speculation Ratio of Oil or Natural Gas Futures during crisis and non-crisis periods (division method is the same as previous model);

- (3)

- Equation (14) captures any relationship between CSAD and SR if present during the whole period;

- (4)

- Equation (15) captures any relationship between CSAD and SR if present during different crisis events;

- (5)

- Equation (16) employs a quartile model to capture any relationship between CSAD and SR if present based on different levels of speculation activities via the introduction of dummy variables;

- (5a)

- captures the effect of the Speculation Ratio on CSAD when it lies in the Lower 25% of the SR Distribution;

- (5b)

- = 1 when the Speculation Ratio lies between 25% and 50% of the SR Distribution, otherwise = 0;

- (5c)

- = 1 when the Speculation Ratio lies between 50% and 75% of the SR Distribution, otherwise = 0;

- (5d)

- = 1 when the Speculation Ratio lies in the Upper 25% of the SR Distribution (Greater than 75% of Distribution), otherwise = 0.

If the coefficient in Equation (14) is significantly negative, this implies that a higher speculation ratio results in a lower market deviation. That is to say, a negative coefficient signifies that higher speculation in the futures market leads to convergence, which can be regarded as a sign of herding. Moreover, a significantly negative in Equation (15) implies a herding tendency during different crisis events. Finally, in Equation (16), significantly negative α3, α5, and α6 points to the occurrence of herding behaviour under a different level of speculation activities.

4. Discussion and Findings

4.1. Herding in Stock Markets and the Effect of Energy Markets (Oil/Gas–Spot/Futures)

The Augmented Dickey–Fuller (ADF) is a unit root test designed to test for stationarity of time series data. It can be seen from Table 1A,B, that all values of the ADF test are significant, thus indicating that all variables are stationary. Table 2 presents summary statistics for herding indicators and market returns of BRICS countries. It is apparent, from this table, that CSAD somewhat tends to change with market return. For instance, India reports the highest average and median values of the two variables, whilst Russia reports relatively lower values of these indicators. Russia also exhibits the greatest fluctuation and range in both of the two variables. The results obtained from the preliminary test of herding in equity markets are shown in Table 3. Chang et al.’s (2000) model suggests that a significant negative coefficient of Rmt2 indicates a herding tendency for sample markets. Strong evidence of herding in China and Russia is found between 2007 and 2022. Moreover, China seems to report a higher degree of herding than does Russia due to the greater value of the coefficient number.

4.2. Crisis Event Effects

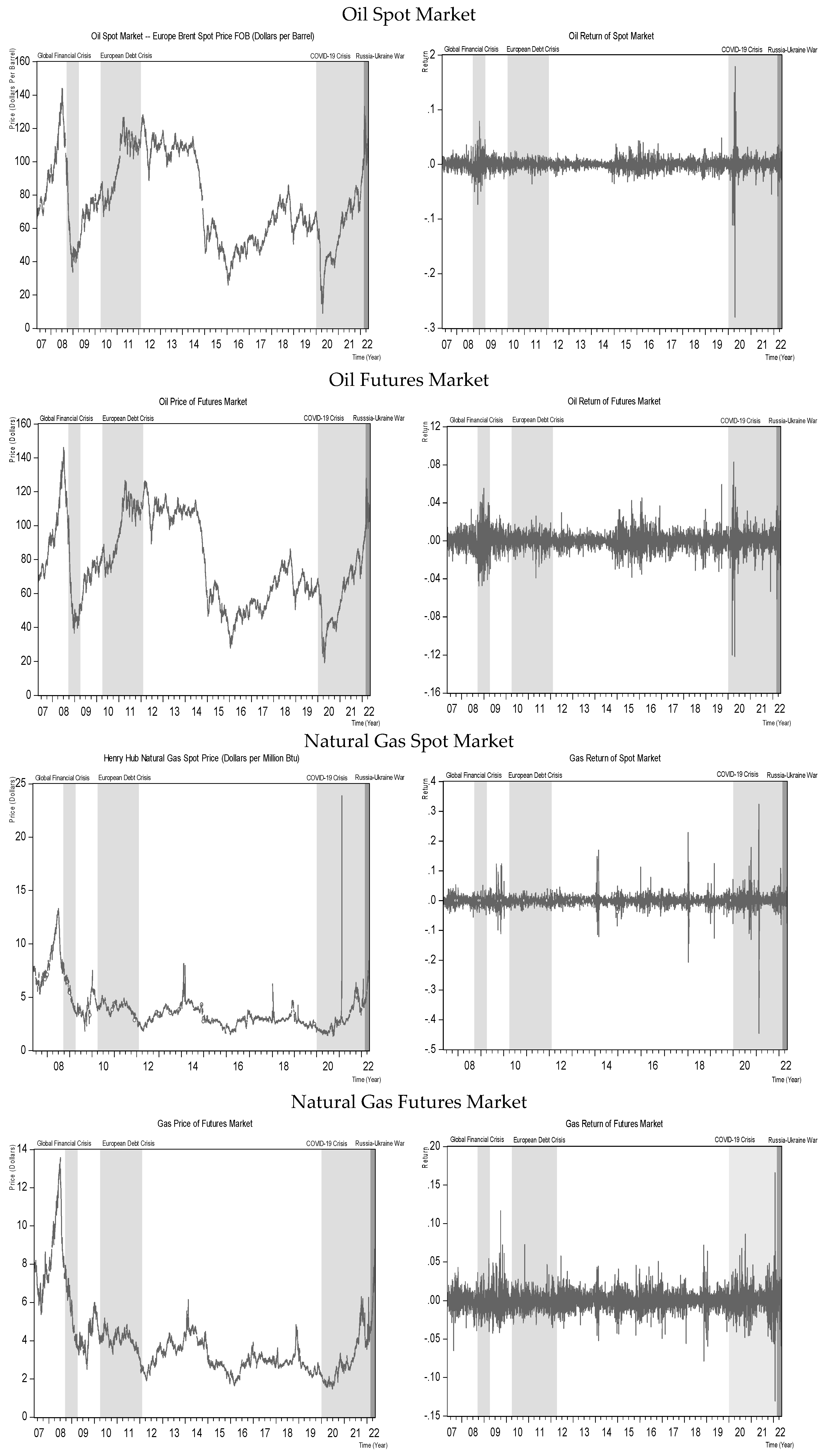

Figure 1 presents prices and returns in both the oil market and the natural gas market; the figure incorporates the spot market and the futures market. Specifically, shaded areas in the graphs capture the different crisis periods, namely, the Global Financial Crisis, the European Debt Crisis, the COVID-19 Crisis, and the Russia–Ukraine War. The COVID-19 Crisis and the Russia–Ukraine War are captured by a single shaded area. It can be seen that prices and returns have experienced great fluctuation over the span of 15 years from 2007 to 2022. Figure 1 confirms that a crisis event can be regarded as a driver that triggers a higher degree of changes in the two variables, as indicated in the shaded areas. This finding is consistent with the standpoint of Rogoff (2022), who pointed out that the occurrence of crises can somewhat lead to greater price volatility in the oil and natural gas market via changes in short-term demand and decreased investment in production. For instance, the oil price suffered a large drop from its normal price of USD 68/barrel at the end of 2019 to USD 14/barrel in April 2020, as a result of the outbreak of COVID-19. However, the price recovered quickly, and even rose to USD 133/barrel in March 2022 due to the occurrence of the Russia–Ukraine war (Rogoff 2022). Similarly, The Investopedia Team et al. (2022) stressed that the 2008 Global Financial Crisis did not lead to contraction in credit, but did decimate prices in the oil and natural gas sector.

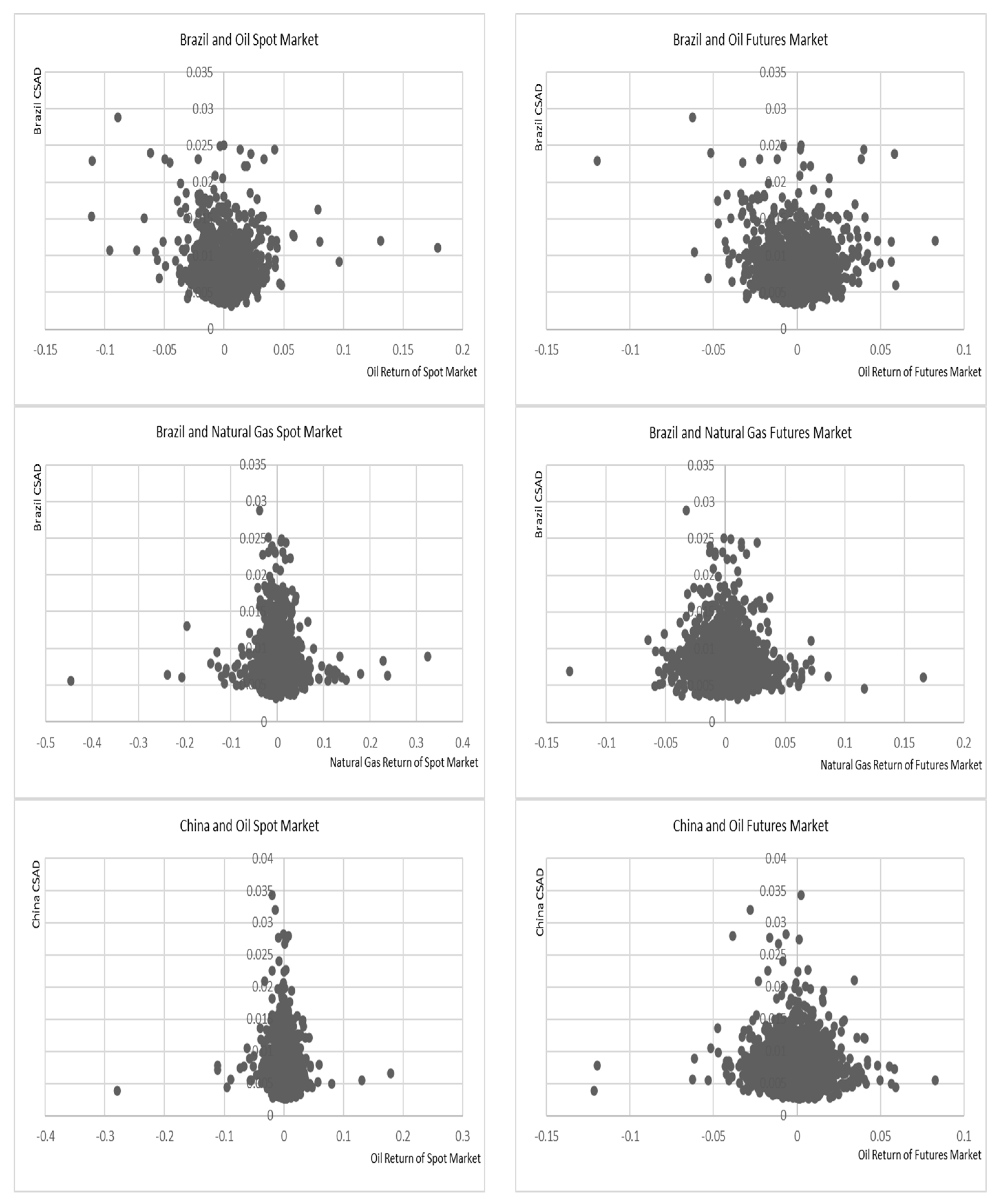

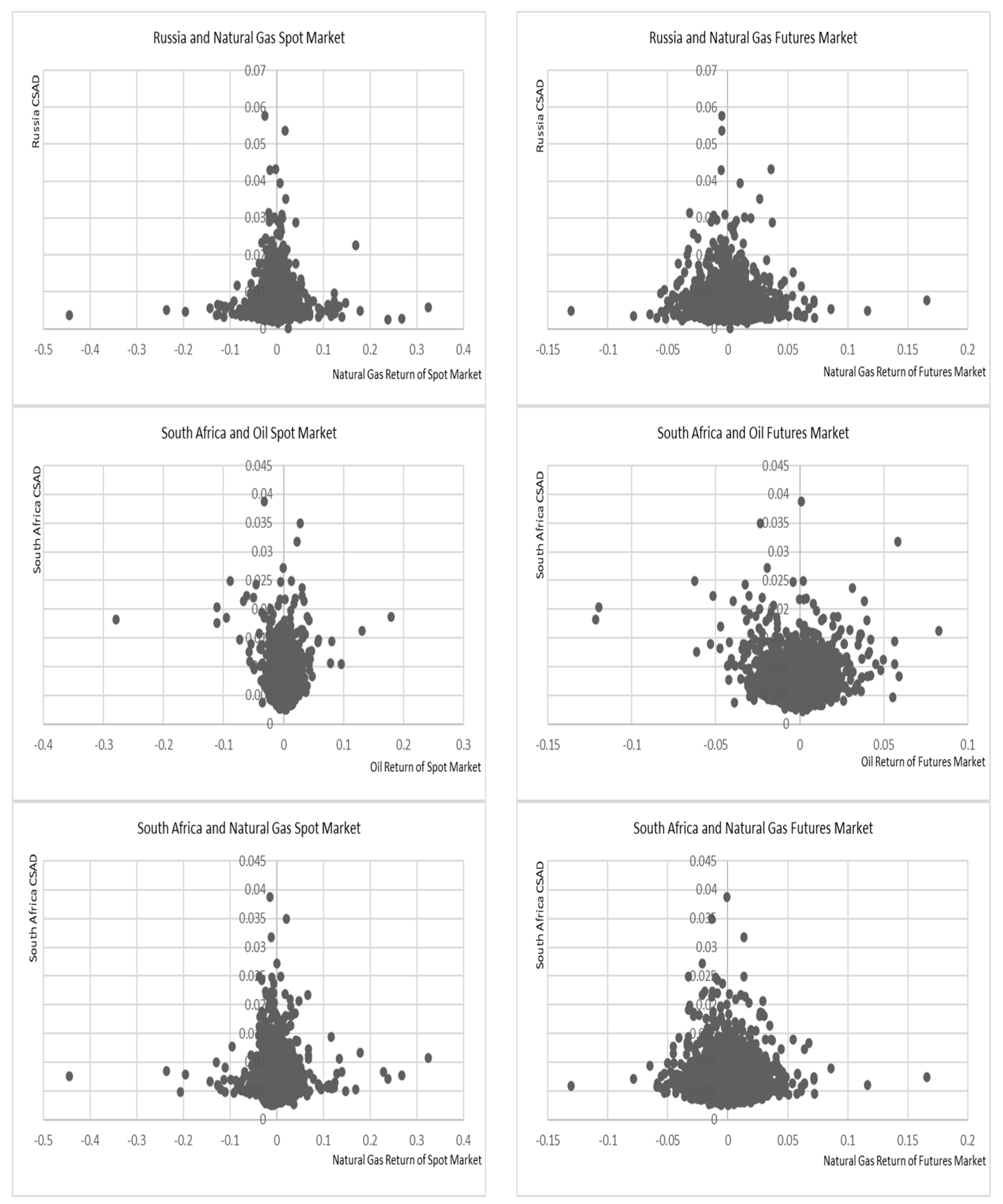

A scatter diagram was used to determine the relation between CSAD in BRICS and returns of energy markets, including the spot market and the futures market, in the oil and natural gas market. As Figure 2 shows, there is a non-linear relationship between the two indicators, which is confirmed by the existence of a data cluster instead of a straight line. In other words, such a relationship shows that the CCK model put forward by Chang et al. (2000) is appropriate for our study.

Table 5 presents the results obtained from the preliminary analysis of the relationship between investors’ behaviour in BRICS and the global financial crisis, as well as different crisis events; the findings were produced using the CCK model. What stands out from Table 5 is that a crisis event can trigger a very limited herding phenomenon when energy markets (oil/gas–spot/futures) are considered. There are very few negative and significant values (in bold) in Table 5. It is worth noticing that even during the Russia–Ukraine war, only one country (South Africa) appears to herd as a result of gas futures. Obviously, crises do not have the same effect on herding as one would think. Herding as a result of changes in energy markets during crises is ‘very much country and period’ dependent. There is no such thing as universality for herding in BRICS resulting from energy markets. When the whole period is considered (as already shown in Table 4), energy markets have zero influence on investors’ behaviour. The reason for this may be that BRICS countries seem to face less pressure, in terms of an energy crisis, induced by the Russia–Ukraine war compared to other countries (such as Europe), even though energy prices, production, and demand have been experiencing great fluctuation during the period.

Now, from a country’s point of view, Table 5 shows that Brazil and Russia seem to be economic entities that are clearly independent of the oil and natural gas markets compared to the other sample countries during the majority of sub-periods; no herding phenomenon is reported for Russia during any periods (Russia is a major producer and exporter of oil and gas, so a smaller or no effect is expected on its equity market), while for Brazil (which is also a producer/exporter of oil), herding behaviour is reported in the equity market as a result of gas futures market changes only during the pre-European Debt Crisis. Conversely, India can be regarded as the most susceptible market, which herds as a result of changes in energy markets (during crisis or not). All results are significant at the 5% or 10% level.

Finally, Table 5 also allows us to compare the effect(s) that oil and natural gas markets have on herding. During periods of crisis, the oil market tends to exert greater influence on investors’ behaviour in BRICS. For instance, the oil spot market can trigger herding in China and India. Nevertheless, South Africa is the only country whose behaviour is affected by gas futures during the Global Financial Crisis and the Russia–Ukraine War period, rather than being influenced by the oil market. The main reason for this is its heavy reliance on importing natural gas due to limited domestic natural gas resources—the second largest gas importer in Africa, with 3.6 billion standard cubic meters in 2020 (Washington and Gupte 2021; Halsey et al. 2022; Statista 2023). Another possible reason for the above result could be policy changes in South Africa. By putting forward the Integrated Resource Plan, South Africa intends to strengthen the role of Liquefied Natural Gas and plans to create an additional 8100 MW gas and diesel-fired generation capacity by 2030, with the purpose of ensuring energy security and filling the energy shortfall caused by the delays in the establishment of the country’s mega coal-fired power stations (Ross 2020). Such policy changes may urge investors to pay more attention to the global natural gas futures market(s) and to adjust their portfolios and decisions.