Developing an Impact-Focused Typology of Socially Responsible Fund Providers

Abstract

:1. Introduction

2. Conceptual Foundation

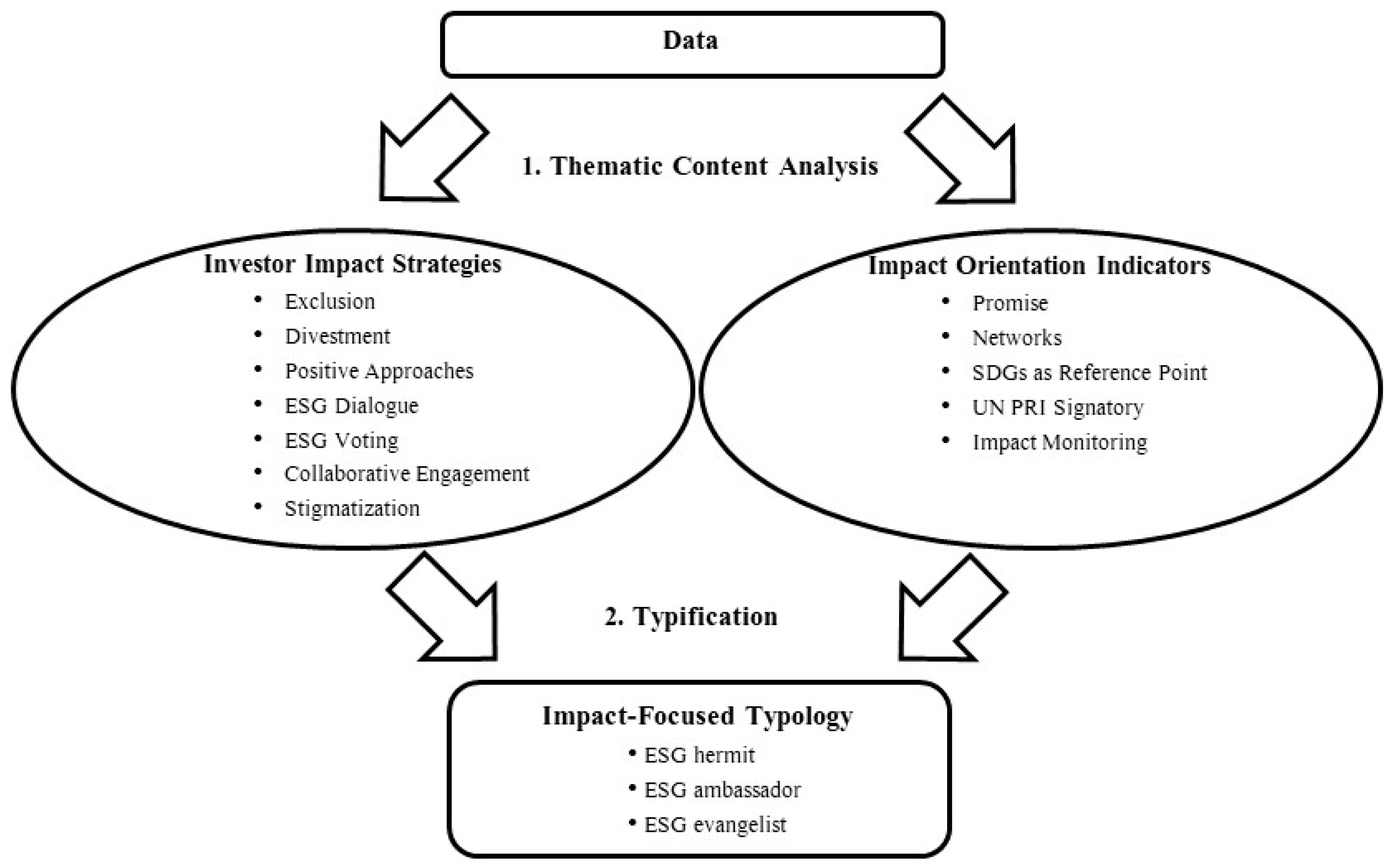

3. Data and Method

3.1. Thematic Content Analysis

3.1.1. Description of the Impact Orientation Indicators

3.1.2. Description of the Investor Impact Strategies

3.2. Typification

4. Results

4.1. ESG Hermit

“Investors no longer need to choose between sacrificing the opportunity for strong risk adjusted returns or their integrity.”(fund provider from the USA)

“Our staff reassess the company to verify or refute the accusation. We can’t go on what someone else has said.”(fund provider from the USA)

“We will not invest a single penny into any company that violates our filters.”(fund provider from the USA)

4.2. ESG Ambassador

“Investments designed for performance and a better world.”(fund provider from the USA)

“It is taken into account whether companies counteract the negative effects, compensate for them or prevent them completely.”(fund provider from Germany)

“From the outset, they wanted to go beyond a pure do-no-harm approach, i.e. not only exclude the most questionable companies and countries, but also invest specifically in securities that make a positive contribution to sustainable development.”(fund provider from Germany)

4.3. ESG Evangelist

“The Bank’s active ownership approach is to support long-term, sustainable development. As an active owner, we incorporate environmental, social and governance (ESG) issues into our investment ownership policies and practices and seek to reduce the negative impact on society and the environment and to promote sustainable growth.”(fund provider from Switzerland)

“In a few cases, exceptions are made for companies with which we are engaged in productive shareholder dialogue or that are making notable progress on areas that concern us.”(fund provider from the USA)

“It is only through engagement that the vision of an often postulated “double return” is credibly pursued.”(fund provider from Austria)

“This means that, unless otherwise agreed, the content of the majority of our meetings is kept confidential between the company and us as an investor. However, we recognise the importance of the media as a tool for delivering change and are not afraid to comment on poor practice (as a method of escalating our engagement) or to engage with the press to raise the profile of important issues and initiatives.”(fund provider from the United Kingdom)

5. Discussion and Future Research

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | There is an ongoing discussion about the ambiguity associated with rating a firm’s impact; see for example Li and Polychronopoulos (2020) or Fish et al. (2019). |

| 2 |

References

- Bailey, Kenneth D. 1972. Polythetic Reduction of Monothetic Property Space. Sociological Methodology 4: 83–111. [Google Scholar] [CrossRef]

- Baker, Malcolm P., Daniel B. Bergstresser, George Serafeim, and Jeffrey A. Wurgler. 2018. Financing the Response to Climate Change: The Pricing and Ownership of U.S. Green Bonds (Working Paper No. 2514). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Barber, Brad M., Adair Morse, and Ayako Yasuda. 2021. Impact investing. Journal of Financial Economics 139: 162–85. [Google Scholar] [CrossRef]

- Barko, Tamas, Martijn Cremers, and Luc Renneboog. 2017. Shareholder Engagement on Environmental, Social, and Governance Performance. Journal of Business Ethics forthcoming forthcoming. [Google Scholar] [CrossRef]

- Bauer, Rob, Ruof Tobias, and Smeets Paul. 2019. Get Real! Individuals Prefer More Sustainable Investments. Working Paper; SSRN. Available online: https://papers.ssrn.com/abstract=3287430 (accessed on 5 March 2022).

- Berry, Thomas C., and Joan C. Junkus. 2013. Socially Responsible Investing: An Investor Perspective. Journal of Business Ethics 112: 707–20. [Google Scholar] [CrossRef]

- Brest, Paul, and Kelly Born. 2013. Unpacking the impact in impact investing. Stanford Social Innovation Review 11: 22–31. [Google Scholar]

- Brest, Paul, Ronald J. Gilson, and Mark A. Wolfson. 2018. How Investors Can (and Can’t) Create Social Value. Amsterdam: Elsevier. [Google Scholar] [CrossRef]

- Busch, Timo, Bauer Rob, and Orlitzky Marc. 2016. Sustainable Development and Financial Markets: Old Paths and New Avenues. Business & Society 55: 303–29. [Google Scholar] [CrossRef]

- Busch, Timo, Bruce-Clark Peter, Derwall Jeroen, Eccles Robert, Hebb Tessa, Hoepner Andreas, Klein Christian, Krueger Philipp, Paetzold Falko, Scholtens Bert, and et al. 2021. Impact investments: A call for (re)orientation. SN Business and Economics 1: 33. [Google Scholar] [CrossRef]

- Campbell, John L., Quincy Charles, Osserman Jordan, and Pedersen Ove K. 2013. Coding in-depth semistructured interviews: Problems of unitization and intercoder reliability and agreement. Sociological Methods & Research 42: 294–320. [Google Scholar] [CrossRef]

- Chen, Tao, Dong Hui, and Lin Chen. 2020. Institutional shareholders and corporate social responsibility. Journal of Financial Economics 135: 483–504. [Google Scholar] [CrossRef]

- Cialdini, Robert B., and Melanie R. Trost. 1998. Social influence: Social norms, conformity and compliance. In The Handbook of Social Psychology, 4th ed. Edited by Daniel T. Gilbert, Susan T. Fiske and Gardner Lindzey. New York City: McGraw-Hill, pp. 151–92. [Google Scholar]

- Clementino, Ester, and Richard Perkins. 2020. How do companies respond to environmental, social and governance (ESG) ratings? Evidence from Italy. Journal of Business Ethics 171: 379–97. [Google Scholar] [CrossRef]

- Dawkins, Cedric E. 2018. Elevating the role of divestment in socially responsible investing. Journal of Business Ethics 153: 465–78. [Google Scholar] [CrossRef]

- DellaVigna, Stefano, John A. List, and Ulrike Malmendier. 2012. Testing for altruism and social pressure in charitable giving. Quarterly Journal of Economics 127: 1–56. [Google Scholar] [CrossRef] [PubMed]

- Derwall, Jeroen, Koedijk Kees, and Ter Horst Jenke. 2011. A tale of values-driven and profit-seeking social investors. Journal of Banking and Finance 35: 2137–47. [Google Scholar] [CrossRef]

- Diener, Joel, and André Habisch. 2021. A plea for a stronger role of non-financial impact in the socially responsible investment discourse. Corporate Governance 21: 294–306. [Google Scholar] [CrossRef]

- Dillenburg, Stephen J., Greene Timothy, and Erekson Homer. 2003. Approaching socially responsible investment with a comprehensive ratings scheme: Total social impact. Journal of Business Ethics 43: 167–77. [Google Scholar] [CrossRef]

- Dimson, Elroy, Karakaş Oğuzhan, and Li Xi. 2015. Active ownership. Review of Financial Studies 28: 3225–326. [Google Scholar] [CrossRef]

- Dimson, Elroy, Karakaş Oğuzhan, and Li Xi. 2018. Coordinated Engagements. Available online: https://papers.ssrn.com/abstract=3209072 (accessed on 17 April 2022).

- Dimson, Elroy, Kreutzer Idar, Lake Rob, Sjo Hege, and Starks Laura. 2013. Responsible Investment and the Norwegian Government Pension Fund Global. Oslo: Norwegian Ministry of Finance. [Google Scholar]

- Dyck, Alexander, Lins Karl, Roth Lukas, and Hannes F. Wagner. 2019. Do institutional investors drive corporate social resposnbility? International evidence. Journal of Financial Economics 131: 693–714. [Google Scholar] [CrossRef]

- European Commission. 2018. Action Plan: Financing Sustainable Growth. COM/2018/097 final. Brussels: European Commission. [Google Scholar]

- European Commission. 2021. Study on Sustainability-Related Ratings, Data and Research: Executive Summary. Directorate-General for Financial Stability, Financial Services and Capital Markets Union, Publications Office. Available online: https://data.europa.eu/doi/10.2874/52845 (accessed on 7 December 2021).

- European Parliament. 2020. Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the Establishment of a Framework to Facilitate Sustainable Investment, and Amending Regulation (EU) 2019/2088. Brussels: Official Journal of the European Union L 198/13. [Google Scholar]

- Eurosif. 2018. European SRI Study 2018. Brussels: European Sustainable Investment Forum. [Google Scholar]

- Fish, Alexander, Dong Hyun Kim, and Shankar Venkatraman. 2019. The ESG Sacrifice. Working Paper. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3488475 (accessed on 12 April 2022).

- Friede, Gunnar, Busch Timo, and Bassen Alexander. 2015. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance and Investment 5: 10–233. [Google Scholar] [CrossRef]

- GAO. 2010. United States Government Accountability Office: Testimony Before the Subcommittee on International Monetary Policy and Trade on Sudan Divestment. Available online: https://www.gao.gov/assets/gao-11-245t.pdf (accessed on 2 February 2022).

- Gifford, E. James M. 2010. Effective Shareholder Engagement: The Factors that Contribute to Shareholder Salience. Journal of Business Ethics 92: 79–97. [Google Scholar] [CrossRef]

- Global Sustainable Investment Alliance (GSIA). 2020. GLOBAL SUSTAINABLE INVESTMENT REVIEW 2020. Available online: http://www.gsi-alliance.org/wp-content/uploads/2021/08/GSIR-20201.pdf (accessed on 20 November 2021).

- Goodman, Jennifer, Louche Céline, Katinka C. van Cranenburgh, and Daniel Arenas. 2014. Social Shareholder Engagement: The Dynamics of Voice and Exit. Journal of Business Ethics 125: 193–210. [Google Scholar] [CrossRef]

- Gutsche, Gunnar, and Bernhard Zwergel. 2016. Information barriers and SRI market participation–Can sustainability and transparency labels help? In MAGKS Discussion Paper No. 24. Marburg: School of Business and Economics, Philipps-University Marburg. [Google Scholar]

- Häßler, Rolf D., and Ines Markmiller. 2013. Der Einfluss nachhaltiger Kapitalanlagen auf Unternehmen. München: Oekom Research. [Google Scholar]

- Heeb, Florian, Kölbel Julian, Paetzold Falko, and Zeisberger Stefan. 2021. Do Investors Care About Impact? Available online: https://ssrn.com/abstract=3765659 (accessed on 22 January 2022).

- Hiller, Jennifer, and Svea Herbst-Bayliss. 2021. Engine No. 1 Extends Gains with a Third Seat on Exxon Board. London: Reuters. [Google Scholar]

- Hoepner, Andreas, Laura T. Starks, Sautner Zacharias, Zhou Xiao, and Oikonomou Ioannis. 2022. ESG Shareholder Engagement and Downside Risk. AFA 2018 paper, European Corporate Governance Institute–Finance Working Paper No. 671/2020. Brussels: European Corporate Governance Institute. [Google Scholar]

- Husson-Traore, Anne-Catherine, and Sarah Meller. 2013. Controversial Companies: Do Investor Blacklist Make A Difference? Paris: Novethic. [Google Scholar]

- Kinder, Peter D., and Amy L. Domini. 1997. Social Screening: Paradigms Old and New. The Journal of Investing 6: 12–19. [Google Scholar] [CrossRef]

- King, Brayden G., and Sarah A. Soule. 2007. Social movements as extra-institutional entrepreneurs: The effect of protests on stock price returns. Administrative Science Quarterly 52: 413–42. [Google Scholar] [CrossRef]

- Kolbe, Richard H., and Melissa S. Burnett. 1991. Content-analysis research: An examination of applications with directives for improving research reliability and objectivity. Journal of Consumer Research 18: 243–50. [Google Scholar] [CrossRef]

- Kölbel, Julian F., Heeb Florian, Paetzold Falko, and Busch Timo. 2020. Can Sustainable Investing Save the World? Reviewing the Mechanisms of Investor Impact. Organization and Environment 33: 554–74. [Google Scholar] [CrossRef]

- Kuckartz, Udo. 2016. Qualitative Inhaltsanalyse. In Methoden, Praxis, Computerunterstützung. 3., überarbeitete Auflage. Weinheim: Beltz Juventa. [Google Scholar]

- Kuckartz, Udo. 2022. Qualitative Inhaltsanalyse. In Methoden, Praxis, Computerunterstützung. 5., überarbeitete Auflage. Weinheim: Beltz Juventa. [Google Scholar]

- Landier, Augustin, and Stefano Lovo. 2020. ESG Investing: How to Optimize Impact? In HEC Paris Research Paper No. FIN-2020-1363. Available online: http://dx.doi.org/10.2139/ssrn.3508938 (accessed on 28 March 2022).

- Landis, J. Richard, and Gary G. Koch. 1977. The measurement of observer agreement for categorical data. Biometrics 33: 159–74. [Google Scholar] [CrossRef] [PubMed]

- Lee, Darren D., Jacquelyn E. Humphrey, Karen L. Benson, and Jason Y. K. Ahn. 2010. Socially responsible investment fund performance the impact of screening intensity. Accounting and Finance 50: 351–70. [Google Scholar] [CrossRef]

- Li, Feifei, and Ari Polychronopoulos. 2020. What a Difference an ESG Ratings Provider Makes. Newport Beach: Research Affiliates Publication. [Google Scholar]

- Louche, Céline. 2015. CSR and Shareholders. In Corporate Social Responsibility, 1st ed. Edited by Esben Rahbek and Gjedrum Pedersen. London: Sage Publishing, pp. 205–39. [Google Scholar]

- Luo, Arthur H., and Ronald J. Balvers. 2017. Social screens and systematic investor boycott risk. Journal of Financial and Quantitative Analysis 52: 365–99. [Google Scholar] [CrossRef]

- Markman, Gideon D., Theodore L. Waldron, and Andreas Panagopoulos. 2016. Organizational hostility: Why and how nonmarket players compete with firms. Academy of Management Perspectives 30: 74–92. [Google Scholar] [CrossRef]

- Moore, David, Cranston Gemma, Reed Anders, and Galli Alessandro. 2012. Projecting future human demand on the Earth’s regenerative capacity. Ecological Indicators 16: 3–10. [Google Scholar] [CrossRef]

- OECD. 2017. Investment Governance and the Integration of Environmental, Social and Governance Factors. Available online: https://www.oecd.org/finance/Investment-Governance-Integration-ESG-Factors.pdf (accessed on 3 March 2022).

- Pástor, Lubos, Robert F. Stambaugh, and Lucian A. Taylor. 2021. Sustainable investing in equilibrium. Journal of Financial Economics 142: 550–71. [Google Scholar] [CrossRef]

- Peifer, Jared L. 2011. Morality in the financial market? A look at religiously affiliated mutual funds in the USA. Socio-Economic Review 9: 235–59. [Google Scholar] [CrossRef]

- Pérez-Gladish, Blanca, Paz Méndez, and Bouchra M’Zali. 2012. A decision support tool for environmentally conscious investors. Journal of Financial Decision Making 7. [Google Scholar]

- Principles of Responsible Investment (PRI). 2017. Aligning Responsible Investment with the UN Sustainable Development Goals. Available online: https://www.commoninterests.com/wp-content/uploads/2017/07/Aligning-investment-with-the-SDGs.pdf (accessed on 2 September 2021).

- Renneboog, Luc, Ter Horst Jenke, and Zhang Chendi. 2008. Socially responsible investments: Institutional aspects, performance, and investor behavior. Journal of Banking and Finance 32: 1723–42. [Google Scholar] [CrossRef]

- Richardson, Benjamin J. 2009. Climate Finance and its Governance: Moving to a Low Carbon Economy through Socially Responsible Financing? International and Comparative Law Quarterly 58: 597–626. [Google Scholar] [CrossRef]

- Robinson, Lynn D. 2002. Doing Good and Doing Well: Shareholder Activism, Responsible Investment, and Mainline Protestantism. In The Quiet Hand of God: Faith-Based Activism and the Public Role of Mainline Protestantism. Edited by Robert Wuthnow and John H. Evans. Berkeley: University of California Press. [Google Scholar]

- Sandberg, Joakim, and Jonas Nilsson. 2011. Conflicting intuitions about ethical investment: A survey among Individual investors. In Sustainable Investment and Corporate Governance Working Papers. Sustainable Investment Research Platform, SIRP WP 10–16. Sustainable Investment Research Platform. [Google Scholar]

- Schwirplies, Claudia, and Andreas Ziegler. 2016. Offset carbon emissions or pay a price premium for avoiding them? A cross-country analysis of motives for climate protection activities. Applied Economics 48: 746–58. [Google Scholar] [CrossRef]

- Shang, Jen, and Rachel Croson. 2009. A field experiment in charitable contribution: The impact of social information on the voluntary provision of public goods. Economic Journal 119: 1422–39. [Google Scholar] [CrossRef]

- Slager, Rieneke, and Wendy Chapple. 2015. Carrot and stick? The role of financial market intermediaries in corporate social performance. Business and Society 55: 398–426. [Google Scholar] [CrossRef]

- Sorkin, Andrew R. 2015. A new tack in the war on mining mountains. The New York Times, March 9. [Google Scholar]

- Tang, Dragon Yongjun, and Yupu Zhang. 2018. Do Shareholders Benefit from Green Bonds? Working Paper. Available online: https://ssrn.com/abstract=3259555 (accessed on 27 May 2022).

- Teoh, Siew, Welch Ivo, and C. Paul Wazzan. 1999. The effect of socially activist investment policies on the financial markets: Evidence from the South African boycott. Journal of Business 72: 35–89. [Google Scholar] [CrossRef]

- The Economist. 2022. The Truth about Dirty Assets. Available online: https://www.economist.com/leaders/2022/02/12/the-truth-about-dirty-assets (accessed on 21 June 2022).

- The Financial Reporting Council (FRC). 2020. The UK Stewardship Code. Review of Early Reporting. Available online: https://www.frc.org.uk/getattachment/975354b4-6056-43e7-aa1f-c76693e1c686/The-UK-Stewardship-Code-Review-of-Early-Reporting.pdf (accessed on 5 April 2022).

- UN Principles for Responsible Investment (UN PRI). 2018. PRI Brochure. UNEP Finance Initiative and UN Global Compact. Available online: https://www.unpri.org/pri/about-the-pri (accessed on 15 July 2019).

- UN Principles for Responsible Investment (UN PRI). 2020. PRI REPORTING FRAMEWORK Overview and Structure. UNEP Finance Initiative and UN Global Compact. Available online: https://dwtyzx6upklss.cloudfront.net/Uploads/w/h/f/overview_and_guidance_reporting_framework_structure3_584160.pdf (accessed on 21 August 2021).

- UN Principles for Responsible Investment (UN PRI). 2021. PRI Brochure. UNEP Finance Initiative and UN Global Compact. Available online: https://www.unpri.org/download?ac=10948 (accessed on 22 August 2021).

- United Nations General Assembly. 2015. Transforming our World: The 2030 Agenda for Sustainable Development, A/RES/70/1. New York: UN General Assembly. [Google Scholar]

- VERBI Software. 2020. MAXQDA 2022 [Computer Software]; Berlin: VERBI Software. Available online: maxqda.com (accessed on 5 August 2020).

- Waldron, Theodore L., Chad Navis, and Fisher Greg. 2014. Explaining differences in firms’ responses to activism. Academy of Management Review 38: 397–417. [Google Scholar] [CrossRef]

- Waldron, Theodore L., Chad Navis, Olivia Aronson, Jeffrey G. York, and Desiree F. Pacheco. 2019. Values-Based Rivalry: A Theoretical Framework of Rivalry Between Activists and Firms. Academy of Management Review 44: 800–18. [Google Scholar] [CrossRef]

- Waygood, Steve. 2011. How do the capital markets undermine sustainable development? What can be done to correct this? Journal of Sustainable Finance & Investment 1: 81–87. [Google Scholar] [CrossRef]

- Weber, Max. 1978. Economy and Society: An Outline of Interpretive Sociology. Berkeley and Los Angeles: University of California Press. First published 1922. [Google Scholar]

- WEF. 2020. Measuring Stakeholder Capitalism: Towards Common Metrics and Consistent Reporting of Sustainable Value Creation. White Paper. Geneva: WEF. [Google Scholar]

- Wendt, Karen. 2021. Theory of Change: Defining the Research Agenda. In Theories of Change: Change Leadership Tools, Models and Applications for Investing in Sustainable Development. Edited by Karen Wendt. Cham: Springer International Publishing, pp. 383–89. [Google Scholar] [CrossRef]

- Wins, Anett, and Bernhard Zwergel. 2016. Comparing those who do, might and will not invest in sustainable funds: A survey among German retail fund investors. Business Research 9: 51–99. [Google Scholar] [CrossRef]

- WWF, Zoological Society of London, and Global Footprint Network. 2016. Living Planet Report 2016: Risk and Resilience in a New Era. London: World Wide Fund for Nature. [Google Scholar]

- Zerbib, Olivier David. 2019. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking and Finance 98: 39–60. [Google Scholar] [CrossRef]

{kind=link}

| ESG Hermits | ESG Ambassadors | ESG Evangelists | |

|---|---|---|---|

| 1. Indicators for Impact Orientation | |||

| Promise | purity | investor impact | investor impact |

| Networks | None | Sustainability networks | Sustainability networks |

| + normative networks | |||

| SDGs as Reference Point | No | Yes | Yes |

| UN PRI Signatory | No | Yes | Yes |

| Impact Monitoring | None | None | yes |

| 2. Investor Impact Strategies | |||

| Exclusion | yes | yes | yes |

| Divestment | divestment as first | divestment as first | first engage, then divest |

| option in controversies | option in controversies | in controversies | |

| Positive Approaches | no | yes | yes |

| ESG Dialogue | no | no | yes |

| ESG Voting and Shareholder Proposals | no | no | yes |

| Collaborative Engagement | no | no | yes |

| Stigmatization | If used, only to confront | None | If used as last step of escalation in |

| and pressure | engagement strategy |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Diener, J.; Habisch, A. Developing an Impact-Focused Typology of Socially Responsible Fund Providers. J. Risk Financial Manag. 2022, 15, 298. https://doi.org/10.3390/jrfm15070298

Diener J, Habisch A. Developing an Impact-Focused Typology of Socially Responsible Fund Providers. Journal of Risk and Financial Management. 2022; 15(7):298. https://doi.org/10.3390/jrfm15070298

Chicago/Turabian StyleDiener, Joel, and André Habisch. 2022. "Developing an Impact-Focused Typology of Socially Responsible Fund Providers" Journal of Risk and Financial Management 15, no. 7: 298. https://doi.org/10.3390/jrfm15070298