A Survey of the Accounting Industry on Holdings of Cryptocurrencies in Xiamen City, China

1

Xiamen National Accounting Institute, Xiamen 361005, China

2

School of Management, Xiamen University, Xiamen 361009, China

3

Department of Accounting, Finance and Economics, Griffith University, Nathan 4111, Australia

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2022, 15(4), 175; https://doi.org/10.3390/jrfm15040175

Submission received: 11 January 2022

/

Revised: 4 April 2022

/

Accepted: 6 April 2022

/

Published: 11 April 2022

(This article belongs to the Special Issue Emerging Markets)

Abstract

:This is the first survey conducted in China on the holding of cryptocurrencies. Although cryptocurrencies have existed in the world for more than a decade, because the exchange of cryptocurrencies is banned in China, there is no guidance on the holding of cryptocurrencies in China’s accounting standards. Moreover, although the exchange of cryptocurrencies is prohibited by the Chinese government, holdings of cryptocurrencies by Chinese entities and individuals cannot be prevented. Thus, we conducted a survey in investors’ attitudes towards cryptocurrencies in Xiamen City, a special economic zone (SEZ) and a pilot free trade zone (FTZ) in China. The survey respondents commonly defined cryptocurrencies as investments (45%), inventories (19%), and intangible assets (36%). A total of 84% of respondents stated that the value of a cryptocurrency should be represented by a fair value. These results are similar to those obtained in a survey by The Digital Assets Accounting Consortium (DAAC), but different to the tentative agenda decision of the International Financial Reporting Standards Interpretations Committee (IFRSIC). Additionally, 65% of respondents stated that they prefer to accept cryptocurrencies as cash equivalent currencies, and these cash equivalent currencies were considered to have two main functions: a medium of exchange (56%) and a monetary unit for pricing goods and services (52%).

1. Introduction

Since Bitcoin was invented in 2008 (Nakamoto 2008), more than 10,707 new cryptocurrencies (Investing 2022) have been created (as of March 2022). Generally, a cryptocurrency is a digital currency that is designed to work as a medium of intermediate exchange. Cryptocurrencies are decentralized digital currencies that are not issued by any jurisdictional authority. All transactions of cryptocurrencies are written in a big, distributed ledger that can be copied by every participant assigned to a node of the blockchain network. Cryptocurrencies are secured by encryption hash algorithms, signed with a digital signature, timestamped, and verified by participants to ensure security and prevent fraud (Silvia 2019).

Blockchain technology is the supporting technology that underlies cryptocurrencies. Cryptocurrencies are crypto assets, which are digitized by blockchain technology. Crypto assets are the most important financial assets in modern financial markets. Crypto assets impact elements of modern finance including highways, mobile phones, and the Internet. Blockchain technology has led to a revolutionary change to potentially many service industries, including finance and banking. Blockchain technology has become an innovative medium and transaction system with high value (Boring 2019).

On 5–6 March 2019, in London, the International Financial Reporting Standards (IFRS) Interpretations Committee (IFRSIC) held a meeting and discussed how the IFRS standards could apply to the holding of cryptocurrencies. A tentative agenda decision on holdings of cryptocurrencies was published. According to the tentative agenda decision, the IFRSIC (2019a) noted that cryptocurrencies are crypto assets.

A cryptocurrency is a digital currency that is recorded on a distributed ledger. For security, it is encrypted by a mathematical cryptography algorithm. A cryptocurrency is not as legal as a fiat currency issued by a jurisdictional authority or a central bank. Most cryptocurrencies are issued by private companies, which do not have any issuing permissions from the central government. The holders of cryptocurrencies do not have any legal contracts as they usually do in traditional financial markets (IFRSIC 2019a).

Based on the tentative agenda decision, IFRSIC (2019a) proposed that the IAS 2 Inventories accounting standard is the accounting rule that best fits the holding of cryptocurrencies. As in the ordinary course of business, when holders want to sell their crypto assets, the best accounting rule is the IAS 2 Inventories. The IFRSIC (2019a) also proposed that if the IAS 2 Inventories accounting standard is not appropriate for holdings of cryptocurrencies, another good choice is the IAS 38 Intangible Assets accounting standard. In most cases, IAS 38 will be the best accounting standard for holdings of cryptocurrencies.

After the tentative agenda decision was published by the IFRSIC (2019a), many accounting bodies worldwide, including accounting firms and accountants, made comments to the IFRSIC. As of 15 May 2019, at least 20 comment letters had been received by the IFRSIC (2019b, Comment letters). These comments represent the major opinions of the accounting industry on holdings of cryptocurrencies. This was the first time that the issue of cryptocurrency holding had been a focus of accounting bodies.

However, there have not been any comments from Mainland China. Do the Chinese accounting bodies not care about the issues of cryptocurrency holding?

Actually, since Bitcoin was created in 2008, the trend of cryptocurrency holding by private companies and individuals has been rapidly increasing in China. However, in contrast to the enthusiasm from private companies and individuals about cryptocurrency holding, the Chinese government has set up a number of regulations to prevent the widespread purchase of cryptocurrencies in China. The conflict between the private holding of cryptocurrencies and the government regulations means that no Chinese accounting body has made a statement on the suggestions of the IFRSIC (2019a). Although the exchange of cryptocurrencies is prohibited by the Chinese government, holdings of cryptocurrencies by Chinese entities and individuals cannot be prevented. Although there are a number of governmental regulations to prevent the exchange of cryptocurrencies in China, when dealt with as a technical problem, it is necessary to consider how to record the holdings of cryptocurrencies in financial statements. As long as some Chinese entities and individuals still hold cryptocurrencies, this will continuously be a question related to accounting standards. On the other hand, even if Chinese accounting bodies do not care about this issue, many international accounting bodies do. If the Chinese accounting bodies do not consider the implications of this issue in China now, it will be a continuous issue in the future. Thus, the motivation of this study was to investigate this issue now in relation to the situation in China.

On 3 December 2013, five Chinese central government regulators, including The People’s Bank of China (PBOC), jointly issued a governmental document named A Circular on Preventing Risks Related to Bitcoin (CSRC 2013) in which the Chinese central government regulators warn that no Chinese financial institution can offer its services to Bitcoin. The Chinese central government regulators noted that Bitcoin may be defined as a special virtual commodity in nature, but because it does not have any legal status as fiat currencies do, it must not be used or circulated in circulation markets as a currency in China. The Chinese central government regulators stated that Bitcoin has no central issuer, a limited total volume, no territory restrictions for its use, and anonymous users. In China, Bitcoin is not seen as a real currency although it is called a currency. Because it is not issued by monetary authorities, it does not have the characteristics of currency in terms of legal compensation and mandatory payment. For these reasons, the Chinese central government regulators have asked that the national financial institutions do not provide any bitcoin-related businesses or services. The Chinese central government regulators also require online Bitcoin exchanges to be filed as trading records, and measures must be taken to prevent speculative trading and money-laundering risks associated with bitcoin. The Chinese central government regulators have warned that if individuals use Bitcoin, then any risks related to Bitcoin will be taken by themselves (Zhu 2013).

Although Bitcoin-related business is prohibited by the Chinese regulators, many cryptocurrencies were used in China. Along with the development of cryptocurrencies in China, further regulations were published by the Chinese government.

On 4 September 2017, seven Chinese central government regulators, including the PBOC (CSRC 2017), again jointly issued a governmental document, named The Announcement on Preventing Financial Risks from Initial Coin Offerings (ICO Rules). Its purpose is to protect investors from financial risks. Under the ICO Rules, ICOs that raise cryptocurrencies are illegal in China. Cryptocurrencies, such as Bitcoin, Ethereum, and others, are considered illegal cryptocurrencies, and their issue and trading are prohibited in China by the Chinese government. If an investor tries to raise money by issuing cryptocurrencies on the black market or selling cryptocurrencies through an irregular trading channel, his or her illegal behavior is prohibited by the Chinese government. Because cryptocurrencies involved in ICOs are not issued by the Chinese official authorities, they are not legally accepted as a fiat currency in China (LLC 2018).

On 3 September 2021, eleven top Chinese economic regulators, including the National Development and Reform Commission (NDRC 2021), jointly issued a tightened regulation named the Notice on Regulating the Activities of Virtual Currency Mining. According to the notice, because virtual currency mining has many negative impacts on the economy, such as energy wastage and the creation of carbon emissions, which do not promote industrial development or technological improvements, industrial entities will be strictly punished if they engage in mining Bitcoin or other virtual currencies. The main punitive measures are the imposition of high electricity prices on state-owned and private companies undertaking virtual currency mining activities that would otherwise pay household electricity prices.

On 24 September 2021, ten Chinese central government regulators, including the PBOC (2021), jointly issued a more tightened regulation on virtual-currency trading and speculation, which is named The Notice on Further Preventing and Disposing of the Risk of Hype in Virtual Currency Trading. Based on the new notice, cryptocurrency trading in China was totally cracked down on. Because there was a concern that financial transactions of cryptocurrencies will have big negative impacts on the Chinese economic and financial order, these kinds of activities were made illegal and were banned in the country. According to the notice of the PBOC (2021), the main negative activities that may result from financial transactions of cryptocurrencies include financial gambling, illegal fund-raising, commercial fraud, pyramid scheme investments, money laundering, and serious threats to the safety of people’s property. Immediately, all cryptocurrency-related business activities were defined as illegal and strictly banned in China.

Although the mining of virtual currency and the trading of cryptocurrencies are banned based on the regulations announced by the Chinese government, in fact, some individuals and companies do hold cryptocurrencies in China. It is thus necessary to do a survey on holdings of cryptocurrencies in China. Except for the regulations, technically, it is necessary to discuss how transactions of cryptocurrencies should be recorded in financial statements. As China’s central bank is developing a digital currency electronic payment (DCEP) system (Xinhua 2020), a survey of holdings of cryptocurrencies will provide some useful suggestions for policy makers.

Generally, under the reform and opening up policy, the Chinese government usually prefers to operate and test its new business policies in a special economic zone (SEZ) or in a pilot free trade zone (FTZ). For example, according to the 2020 annual report (Meitu 2021), during the year ended 31 December 2021, the company of Meitu1 had invested 940.88523 units of Bitcoin and 31,000 units of Ethereum, and were accounted as intangible assets approximately US$45.1 million and US$117.3 million when revaluated by using the prevailing market prices of fair values (Meitu 2022). Moreover, on 12 October 2020, the PBOC issued CNY 10 million (about USD 1.47 million) of its first digital currency, known as Digital Renminbi, in Shenzhen (Xinhua 2020). These were the first SEZs and FTZs in China. Because the Digital Renminbi is not a cryptocurrency like Bitcoin, we do not discuss it in this paper. However, if a cryptocurrency is used as a reference to the Digital Renminbi, the survey on cryptocurrencies can provide some reference suggestions for the government.

Since the first pilot free trade zone was set up in 2013, China has established 18 pilot FTZs (CGTN 2019). Setting up new pilot FTZs is a strategic policy to improve the degrees of the Chinese reform and opening up in the new era. In China, the pilot FTZs are meant to serve as pioneers of the country’s reform and opening up. For better integration of the domestic economy with international practices, the Chinese government has given some special policies to the pilot FTZs. Before a new opening up policy is implemented in the country, it can be firstly implemented and tested in the pilot FTZs.

Xiamen City became a special economic zone (SEZ) in 1980 and a pilot free trade zone (FTZ) in 2015. Based on the support from the Xiamen City Federation of Social Science Associations (XMSK 2020), we conducted survey focusing on the issue of whether it would be possible for the Chinese government to allow people within the SEZ and FTZ of Xiamen City to trade cryptocurrencies. If this is possible, how do we deal with holdings of cryptocurrencies in accounting? To answer these questions, we conducted a survey in Xiamen City. We discuss the majority opinions from the global accounting industry and present the results of the survey conducted in Xiamen City.

2. Literature Review

2.1. Are Cryptocurrencies Intangible Assets, as Defined in IAS 38?

The IFRSIC (2019a) stated that the cryptocurrencies are intangible assets, as defined in IAS 38. If a cryptocurrency is an intangible asset, the basic assessment is that it must meet the requirements of an intangible asset defined in IAS 38. An asset is intangible if it can be separated, sold, or transferred from the holder individually, and it cannot be seen as a monetary item that can give the holder a contractual right to obtain a number of units of currency.

Some accounting bodies have noted that the application of IAS 38 may not be relevant for investors. Because a cryptocurrency is mostly held by investors for the purpose of investment, they have suggested that it is inappropriate to apply IAS 38 to holdings of cryptocurrencies.

Although a cryptocurrency meets the definition in paragraph 8 of IAS 38 for classification as an intangible asset, the purposes of holding a traditional intangible asset and holding a crypto asset for investment are totally different (Kim 2019).

Regarding the tentative agenda decision made by the IFRSIC (2019a) on the application of IAS 38 to holdings of cryptocurrencies, only a few accounting bodies agreed with this conclusion. Many other accounting bodies did not agree with the conclusion of the IFRSIC (2019a). For example, The Digital Assets Accounting Consortium (DAAC) conducted an industry survey for the period from February to April 2019 and found that only 19% of respondents carrying cryptocurrencies answered that holdings of cryptocurrencies are considered intangible assets, whereas as many as 64% of respondents answered no to this question (Boring 2019).

The Taiwan Accounting Research and Development Foundation (ARDF Taiwan) stated that the application of IAS 38 to holdings of cryptocurrencies may not generate relevant information for the investors. When comparing the characteristics and nature of cryptocurrencies and intangible assets, they are not exactly as the same as defined in IAS 38, because cryptocurrencies produce economic benefits through being sold or invested, while general intangible assets produce economic benefits through business operation (Liu 2019).

The Securities and Exchange Commission of Brazil (CVM) stated that if a cryptocurrency is bought for the purposes of investment, trading, or use as a medium of exchange, it can clearly not be considered within the scope of IAS 38 Intangible assets, because the nature of an intangible asset is related to the maintenance of operational activities (Ferreira and Silva 2019).

Generally, intangible assets are usually defined as goodwill or non-liquid assets. When a cryptocurrency is treated as an intangible asset, its true nature may not be easily separated from other intangible assets in financial statements (Boring 2019).

The information produced based on IAS 38 may not be the most useful information for investors, because under IAS 38, the value of holdings of cryptocurrencies might be estimated by a cost-based valuation method that measures the crypto assets’ value in financial statements. If the cost-based method is implemented, then values may be assigned to holdings of cryptocurrencies and recorded in financial statements as historical costs, but this will not provide relevant information about their current market value to investors. If the cost-based revaluation method is implemented, the real value of holding the cryptocurrency in terms of profit or loss will not be reflected when an active market exists and the cost-based revaluation method will need to change (Hait et al. 2019).

The Mexican Financial Reporting Standards Board (CINIF) stated that based on IAS 38, a cryptocurrency might be revalued at its purchased cost or at its fair value, because the purchased cost does not reflect the economic value of a cryptocurrency. If the revaluation method is applied to cryptocurrencies, which should be revaluated at fair value, the result of the revaluation should be confirmed as an integrated income. Because the purpose of cryptocurrency holding is speculative in nature, for revaluating in the short term, it might be inappropriate to revalue cryptocurrencies in terms of historical costs and the best revaluation method may be to measure the profit or loss using the fair value (Cervantes 2019).

The Canadian Accounting Standards Board (AcSB) noted that the IAS 38 was introduced much earlier than when cryptocurrencies were created. When the paragraphs of the IAS 38 were written, the nature of cryptocurrencies was never considered. When IAS 38 is applied to measure whether holdings of cryptocurrencies are intangible assets, the measurement result will be inappropriate and a fair value will not be achieved (Mezon 2019).

The Canadian Securities Administrators Chief Accountants Committee (CSACAC) explained that intangible assets, as defined in paragraph 9 of IAS 38, are generally held to help an entity to operate its business. However, cryptocurrencies are generally held to help an entity with investment, mostly to produce future profits from sale. Again, the prices of cryptocurrencies are volatile in the market, and cryptocurrencies are often held for speculative purposes in the short-term when they are used for the exchange for goods or services. Based on this analysis, it is inappropriate to see holdings of cryptocurrencies as intangible assets (Hait et al. 2019).

The Chamber of Digital Commerce stated that, in general, the application of the IAS 38 Intangible Assets accounting standard for holdings of cryptocurrencies is not appropriate, because the purposes of cryptocurrency holding should be considered when assessing which IFRS accounting standards should be applied (Boring 2019). Usually, the purposes of cryptocurrency holding are very different depending on whether the holders are broker-traders or cryptocurrency miners. While a cryptocurrency miner may take out a loan to mine crypto assets and repay this through selling crypto assets, another company’s treasury department may hold cryptocurrencies with a long-term investment objective and sell the remaining cryptocurrencies as a short-term liquid requirement (Boring 2019). Because the purposes are different, the accounting standard IAS 38 may not reflect the purposes appropriately.

2.2. Are Cryptocurrencies Inventories, as Defined in IAS 2?

The IFRSIC (2019a) concluded that if cryptocurrencies are held for sale during the ordinary course of business, it is appropriate to apply the IAS 2 Inventories accounting standard. If an entity holds cryptocurrencies for sale during the ordinary course of business, the held cryptocurrencies will be the same as inventories defined in the IAS 2. Conversely, if an entity holds cryptocurrencies that are not for sale in the ordinary course of business, the held cryptocurrencies can be considered intangible assets as described in IAS 38.

The IFRSIC (2019a) also concluded that when an entity acts as a broker-trader of cryptocurrencies and considers cryptocurrencies to be inventory assets similar to the description of commodities in the broker-traders act, it is appropriate to apply paragraph 3(b) of the IAS 2. In these circumstances, it is better to measure the value of inventories at fair value and calculate the profit less costs from the selling prices.

Many accounting bodies have agreed to accept the tentative agenda decision of the IFRSIC (2019a) by applying IAS 2 to holdings of cryptocurrencies so that they are considered inventories.

The Digital Assets Accounting Consortium (DAAC) conducted an industry survey from February to April 2019 and found that 39% of respondents who had crypto assets considered their cryptocurrencies to be inventories (Boring 2019).

The Accounting Standards Board of Japan (ASBJ) stated that because cryptocurrencies do not have any inherent value, their value usually comes from market exchange, if an entity wants to generate cash flow from its holdings of cryptocurrencies, the only way is to sell the cryptocurrencies on the cryptocurrency market. In this situation, it is appropriate to apply IAS 2 (Kogasaka 2019).

Hardidge (2019) suggested that cryptocurrencies held by broker-traders can be seen as inventories. Under IAS 2, a broker-trader holds cryptocurrencies for the purpose of generating a benefit by selling cryptocurrencies at high prices and buying them at low prices. The price fluctuations are the first consideration for holdings of cryptocurrencies.

Generally, a broker-trader holds cryptocurrencies in an ordinary business to sell them to customers. In some cases, these cryptocurrencies are bought from customers to satisfy the dealers’ sell orders. In other cases, cryptocurrencies are bought from miners to meet customers’ buy orders. In both cases, the cryptocurrencies are bought and sold to generate marginal profits. The characteristics of cryptocurrency holding in this case fits the definition of the IAS 2 inventory; accordingly, these digital assets are held as part of the inventory on the entities’ distributed ledger account (Boring 2019).

Some accounting bodies have noted that it is inappropriate to accept the tentative agenda decision of the IFRSIC (2019a) by applying IAS 2 to the holdings of cryptocurrencies as part of the inventory.

The Taiwan Accounting Research and Development Foundation (ARDF Taiwan) stated that the application of IAS 2 to holdings of cryptocurrencies may not provide relevant information to investors, because when cryptocurrencies are seen as inventory, their value may be estimated based on the purchased cost, and when they are valued using their historical cost, this will not exactly reflect their market economic value (Liu 2019).

Different to cryptocurrency holding by broker-traders, cryptocurrencies held by miners cannot be seen as inventories. When miners get a cryptocurrency reward from mining, the cryptocurrency cannot be seen as inventories under IAS 2 (Hardidge 2019).

2.3. Are Cryptocurrencies Cash, as Defined in IAS 32?

The IFRSIC (2019a) concluded that cryptocurrencies are not cash, because the nature of cryptocurrencies is not currently the same as the nature of cash.

Some accounting bodies prefer to accept that cryptocurrencies are not cash, as concluded by IFRSIC.

Although a cryptocurrency can be used as a medium for exchanging particular goods and services, it is not widely accepted as cash, as defined in the accounting standard IAS 32 Financial Instruments: Presentation. Additionally, although a cryptocurrency can be used as a monetary unit to price goods or services, it is also not widely accepted as cash in terms of the measurement and recording of transactions in financial statements, as defined in IAS 32.

Why are cryptocurrencies not accepted as cash, as defined in IAS 32? Many people are concerned that the prices of cryptocurrencies are highly volatile. Because the prices of cryptocurrencies undergo large fluctuations, they cannot be accepted as a medium or a monetary unit to measure the prices of other goods and services on the market. Conversely, the prices of cryptocurrencies have to be measured by other fiat currencies (Blockchain 2020). Based on this, cryptocurrencies’ functions are not the same as those of fiat currencies, because fiat currencies are usually used to measure the prices of goods and services. Moreover, considering their volatile pricing, cryptocurrencies are poorly stored as store value (Silvia 2019).

Some other accounting bodies prefer to accept that cryptocurrencies can be considered cash, as defined in IAS 32.

In the first quarter of 2021, Tesla (2021) purchased an aggregate amount of USD 1.50 billion Bitcoin. This cryptocurrency was firstly accepted as a type of payment for sales and was considered non-cash in accordance with the non-cash consideration guidance included in The US Accounting Standards Codification (ASC) 606 and as intangible asset as defined in ASC 805. Later, in 2022, Tesla (2022) reassessed the aggregate amount of USD 1.50 billion Bitcoin purchased in 2021 and reclassified it as an investment and also as a liquid alternative to cash in the long term.

The Securities and Exchange Commission of Brazil (CVM) stated that cryptocurrencies are not currently accepted as currency because cryptocurrencies were not entirely considered when the AG3 of IAS 32 was created; however, in some transactions, cryptocurrencies have to be considered cash, because, in fact, cryptocurrencies have been implemented as a medium of exchange and used as monetary units for transactions in some markets (Ferreira and Silva 2019).

The Mexican Financial Reporting Standards Board (CINIF) stated that, in general terms, it is inappropriate for cryptocurrencies to receive accounting recognition according to IAS 2 Inventories or IAS 38 Intangible. Conversely, it is appropriate to define a cryptocurrency as cash, because a cryptocurrency is a digital record that is based on encrypted algorithms and used as a form of payment, and its transfer can only be carried out via electronic means (Cervantes 2019).

Bitcoin, Ethereum, and other cryptocurrencies, although not widely accepted as electronic cash, are accepted by many commercial entities as a payment tool and used to pay for exchanges worldwide. More and more people are preferring to use cryptocurrencies to exchange goods and services, and this trend will continue to accelerate in the future (Rowland 2019). As the most popular cryptocurrency today, Bitcoin was created in a peer-to-peer network as an electronic form of cash, which permits payments to be directly transferred from one party to another through the blockchain network. It is targeted to act as a medium of exchange and monetary unit for pricing goods and services and is defined as having the basic function of cash according to IAS 32.

The International Air Transport Association’s (IATA) Industry Accounting Working Group (IAWG) suggested that cryptocurrencies should be treated as cash. Generally, cash has three basic functions: a medium of exchange, a monetary unit for pricing goods and services, and a store value of currency. Although the exchange medium function is an essential element for an asset that acts as cash, it is not essential for an asset acting as cash to have the other two basic functions. Although many sovereign currencies are widely accepted as cash, they cannot be converted into a normal fiat currency and are not able to be widely used as a medium of exchange in the international market. Functional currencies and foreign notes and coins held by an entity are generally reported as cash in accounting statements. Thus, if cryptocurrencies are widely used as a medium of exchange in the market by entities, they should be treated as cash (Nevo and Cahalan 2019).

The Taiwan Accounting Research and Development Foundation (ARDF Taiwan) stated that the fundamental function of a cryptocurrency is to act as a medium of exchange, usually for the purpose of exchanging goods, services, or fiat currencies. Although cryptocurrencies do not have any inherent or intrinsic value, entities that hold cryptocurrencies can receive market benefits from their subsequent exchange or sale. This is quite different to the description of intangible assets by IAS 38 or inventories by IAS 2 (Liu 2019).

Different to some accounting bodies that directly agree or disagree that cryptocurrencies are not cash, as concluded by the IFRSIC, some accounting bodies are focused on future trends.

Deloitte agrees that although the conclusion that cryptocurrencies are not cash is accepted now, this will not be the case in the future. While existent accounting standards, such as IAS 38, have been used to assess whether cryptocurrencies act as cash now, this conclusion will be reassessed if the accounting standards catch up with the development of cryptocurrencies in the future. Accordingly, in the future, it will be essential to develop a more robust definition for the accounting standards of cash (Poole 2019).

The Fintech company Brane stated that it is necessary to review and develop the definition of cash in the IFRS standards. There are five ways to assess whether an asset is as a financial asset according to IAS 32. Only Paragraph AG3 of IAS 32 defines the function of cash as being a medium of exchange. This is an incomplete definition for cash, because it does not sufficiently explain the widespread function of an exchange medium when assessing whether a given asset can be considered cash (Rowland 2019).

2.4. Are Cryptocurrencies a Financial Instrument, as Defined in IAS 32?

The IFRSIC (2019a) noted that cryptocurrencies are not monetary items and do not give the holder legal rights as monetary items usually do. Generally, a monetary item can give a holder a contractual right to get a fixed number of units of currency. Based on the tentative agenda decision on holdings of cryptocurrencies of the IFRSIC (2019a), a cryptocurrency is not a financial equity instrument because it cannot give the holder a legal contractual right to receive a fixed interest.

Some accounting bodies accept the conclusion of the IFRSIC (2019a) that a cryptocurrency is not a monetary item.

Rowland (2019) noted that a smart contract is embedded on the blockchain network for cryptocurrencies. When assessing whether a cryptocurrency is a financial asset, it is very important to consider whether the contractual rights and obligations utilize a consensus protocol coordinated between the holder and the blockchain network of cryptocurrencies.

A financial instrument is defined in IAS 32 as a contract that can give a holder the right to receive a fixed benefit. Silvia (2019) stated that a cryptocurrency is not a financial instrument because the holders of cryptocurrencies generally do not have any legal contractual right to receive cash or another financial asset as occurs with a traditional financial instrument.

Some accounting bodies do not accept the conclusion of the IFRSIC (2019a) that a cryptocurrency is not a financial instrument, as defined in IAS 32, based on the issuance of cryptocurrencies, because cryptocurrencies do involve a contract between the holder and the blockchain network.

Actually, it is not true that the holder of a cryptocurrency does not have any contract. The truth is that the holder of a cryptocurrency has an electronic contract with the blockchain system through a distributed ledger. The difference between a cryptocurrency and a traditional financial instrument, as defined in IAS 32, is that the contract of the cryptocurrency holder does not contain a legal contractual right to receive a fixed unit of money. This means that the electronic contract does not have any guarantee from the jurisdictional authority.

The Fintech company Brane noted that it is necessary for the IFRSIC to consider the technical attributes of the proof-of-stake consensus protocol (PoS) in the blockchain network when assessing whether a cryptocurrency can or cannot be considered a financial asset (Rowland 2019). It is not correct for the IFRSIC to state that the holder of a cryptocurrency does not have any contractual right to receive a number of units of money (Rowland 2019). For example, the Bitcoin blockchain network is addressed in a proof-of-work (POW) consensus protocol. Similarly, the Ethereum blockchain network is addressed in a proof-of-stake (POS) consensus protocol. Under both the POW and POS consensus protocol networks, all participants in the blockchain networks are required to agree with these consensus protocols and the related rules when they intend to hold Bitcoin and Ethereum and conduct business on the networks. If an entity decides to participate in the Bitcoin or Ethereum blockchain networks, they accept the network consensus protocols and receive financial reward from holdings of Bitcoin and Ethereum. If an entity enters into the networks, the POW and POS consensus protocols become obligations that the entity has to obey. The POW and POS consensus protocols and their related rules are usually embedded in a smart contract. As soon as the entity accesses the typical networks, the smart contract between the entity and the network is automatically signed. Consequently, every participant’s activities, responsibilities, and obligations on the network are regulated by the smart contract. Similar to the cryptocurrencies of Bitcoin and Ethereum, the consensus protocols of POW and POS are applied by more than 80% of all cryptocurrencies (Rowland 2019). It is significant that the smart contracts can be accepted as general contracts, as defined in IAS 32 for financial instruments.

Some accounting bodies suggested that different methods should be used to assess whether a cryptocurrency can be seen as an intangible asset, cash, inventory, or financial instrument in different situations.

The Chamber of Digital Commerce stated that it is more appropriate to use different accounting standards to assess the characteristics of cryptocurrencies based on the purpose of their holding. When the intent is to resell the cryptocurrency, it is appropriate to apply the inventory accounting standard, IAS 2; however, when the intent is to use a cryptocurrency as a financial instrument, then it is appropriate to apply both IAS 32 and IAS 39 (Boring 2019).

2.5. How to Disclose Holdings of Cryptocurrencies in Accounting?

The IFRSIC (2019a) concluded that an entity may apply the disclosure requirements of the IFRS standards to determine the amount to be recorded in accounting financial statements in three ways. If an entity holds cryptocurrencies for sale in the ordinary course of business, it is appropriate to apply paragraph 36–39 of the IAS 2 Inventory to determine the amount to be displayed in the financial statement. Otherwise, it is appropriate to apply paragraph 118–128 of IAS 38 intangible assets to determine the amount to be displayed in the financial statement. In both cases, because the cost-based method can only measure the historical value of holdings of cryptocurrencies but cannot provide any relevant information for making investment decisions, it is essential to apply paragraphs 91–99 of IFRS 13 Fair Value Measurement to disclose the value of holdings of cryptocurrencies.

The IFRSIC (2019a) noted that when an entity applies paragraph 122 of IAS 1 Presentation of Financial Statements to holdings of cryptocurrencies in accounting, it is necessary to disclose judgements that significantly affect the amounts confirmed in the financial statements.

The IFRSIC (2019a) also noted that if an entity is applying paragraph 21 of IAS 10 Events to holdings of cryptocurrencies in accounting after the reporting period, it is necessary to disclose any relevant non-adjusting events, including information related to the nature of the event and value of the financial effects. For example, if an entity holds cryptocurrencies and intends to sell them for liquidity, because the disclosed events in the financial statement may influence the decisions of investors, based on the IFRS 13 Fair Value Measurement requirement, it is necessary to disclose significant changes to the fair value that have occurred after the reporting period.

Many accounting bodies agree that the fair value is a good way to measure value when an entity holds cryptocurrencies.

Because a cryptocurrency is usually used as a payment tool or stored for sale, the fair value is the best way to reflect the economic value of holdings of cryptocurrencies (Cervantes 2019).

The Accounting Standards Board of Japan (ASBJ) stated that the best way of revaluating the holdings of cryptocurrencies is to use their fair value through profit or loss (FVTPL), because the FVTPL provides the most relevant information to investors in financial statements (Kogasaka 2019).

Grant Thornton International Ltd. noted that if an entity is not a broker-trader and its holdings of cryptocurrencies are not for sale in the short-run, because the accounting standard defined by the IFRSIC cannot sufficiently reveal the performance of its businesses, FVTPL is the best choice to provide relevant information for investors (Haygarth 2019).

The Mexican Financial Reporting Standards Board (CINIF) stated that the historical cost and net realizable value may not reflect the actual value of holdings of cryptocurrencies, because only the FVTPL can reflect the market value of holdings of cryptocurrencies (Cervantes 2019).

When Tesla (2021) revaluated its aggregate of USD 1.50 billion Bitcoin purchased in 2021, the sales revenue from contracts with customers was recorded based on the fair value according to current quoted market prices.

The Canadian Securities Administrators Chief Accountants Committee (CSACAC) conducted a survey of 41 Canadian entities with cryptocurrency holdings and/or undergoing related activities and summarized that although there are different accounting practices that can be applied to holdings of cryptocurrencies, most respondents (76%) stated that they prefer to disclose the values of cryptocurrencies in financial statements using fair value through profit and loss (Hait et al. 2019).

In most cases, if an entity holding cryptocurrencies is considered to be a commodity broker-trader, as defined in IAS 2, the alternative accounting standard that can be used is paragraph 11 of IAS 8, which may provide a framework for assessing the concepts of assets, liabilities, income, and expenses (Hait et al. 2019).

Similarly, the Digital Assets Accounting Consortium (DAAC) conducted an industry survey from February to April 2019 and found that 75% of respondents holding cryptocurrencies treated changes in events related to cryptocurrencies at fair value when revaluing their earnings or liquidity from holdings of cryptocurrencies (Boring 2019).

2.6. What Proposals Were Put Forward by Accounting Bodies?

Some accounting bodies suggested that it is essential to change the definition of cryptocurrency from that proposed by the IFRSIC (2019a).

As a Fintech company, Brane stated that the birth of cryptocurrencies was a shock to the traditional financial market. Clearly, cryptocurrencies emerged much later than the formation of IAS 38, and while the blockchain distributed ledger technology and encryption algorithms are rapidly evolving in the accounting area, the IAS 38 only provides a very limited solution to the estimation of the fair value of cryptocurrency holdings. When IAS 38 is applied to holdings of cryptocurrencies, considering the nature of cryptocurrencies, IAS 38 cannot provide a perfect solution and therefore does not appropriately represent the nature of the crypto assets when attempting to accounted for them in financial statements (Rowland 2019).

The International Air Transport Association’s (IATA) Industry Accounting Working Group (IAWG) questioned the definition presented by the IFRSIC. Although cryptocurrencies are considered by the IFRSIC as not being issued by a jurisdictional authority, the IAWG confirmed that this is not true. Although cryptocurrencies are not issued by a jurisdictional authority at the moment, they can be transferred to a fiat currency and used as a medium of payment clearing. It is easy to solve this problem if a contract between the holder of cryptocurrencies and the clearing parties is created through the blockchain network. For this reason, the IAWG suggested that the definition of cryptocurrency should be changed (Nevo and Cahalan 2019).

Some accounting bodies suggested that it is essential to revise the current IFRS standards.

The IFRS Technical Committee of Chile (TCC) suggested that although holdings of cryptocurrencies are intangible assets, as defined in IAS 38, because this is an implicit assumption but not an explicit assumption, there is a requirement for the accounting standard of IAS 38 to be updated when explicitly defining holdings of cryptocurrencies as intangible assets (Torres 2019).

The Securities and Exchange Commission of Brazil (CVM) stated that an IFRS standard revision of cryptocurrencies is essential. As a new category of asset, when the majority of IFRS standards were created, no cryptocurrencies had been created. Cryptocurrencies are directly constrained by the scope of the current IFRS standards and explained by a tentative agenda decision by IFRSIC (2019a). If the standards of the IFRS are not revised and updated, some new characteristics of cryptocurrencies will probably be far beyond the scope of the current IFRS standards, meaning that the current IFRS standards will probably not be able to correctly reflect new financial trends related to cryptocurrencies (Ferreira and Silva 2019).

The Accounting Standards Committee of Germany (ASCG) noted that the outcome of the tentative agenda decision of the IFRSIC (2019a) on holdings of cryptocurrencies has led to inappropriate results under all facts and circumstances. Some cryptocurrencies, such as Bitcoin, are accepted as mediums of exchange, which implies that these cryptocurrencies have the basic function of cash. Some cryptocurrencies, such as utility tokens, have limited use within a very specific scope of service, which means that these cryptocurrencies may or may not have the basic function of cash. Some cryptocurrencies may not have any functions of cash at all, which means that these cryptocurrencies do not have any cash functions. To record the holdings of all categorized cryptocurrencies in financial statements appropriately, it is essential to revise and update the standards of the IFRS, including IAS 2 and IAS 38. It is necessary to consider all possible scenarios, as the standard make more sense in some scenarios than in others (Barckow 2019).

Some accounting bodies suggested that it is essential to add new projects to the current IFRS standards.

Rowland (2019) suggested that the IFRSIC should create a new project and add some new paragraphs to the current IFRS standards for holdings of cryptocurrency, because the application of IAS 38 already lags the application of blockchain technology. Applying IAS 38 based on the tentative agenda decisions of the IFRSIC will only be a temporary measure before IFRS standards can catch up to the application of today’s technologies. If the IFRS fails to provide more appropriate guidance to the holdings of cryptocurrencies and if no new IFRS standard is added to fit cryptocurrencies, the IFRS will not be considered just or fair for the profession. Consequently, the presentation of cryptocurrencies in financial statements will fall further behind and suffer from a lack of appropriateness in the IFRS standards.

The Mexican Financial Reporting Standards Board (CINIF) suggested that it is necessary to issue a new standard for cryptocurrencies. Cryptocurrencies are a new kind of asset. They are completely different to the traditional assets explained in the existing accounting standards of the IFRS, including IAS 2 and IAS 38. When the accounting standards of the IFRS were issued, cryptocurrencies had not been created. As cryptocurrencies were created a long time later, the existing accounting standards of the IFRS do not reflect the fair value of cryptocurrencies presented in financial statements. Accordingly, it is necessary to develop the standards of the IFRS and issue new specific paragraphs within the IFRS for cryptocurrencies (Cervantes 2019).

3. A Survey of the Accounting Industry on Holdings of Cryptocurrencies

3.1. Survey Results from the Xiamen City, China

In order to provide meaningful feedback on how to deal with holdings of cryptocurrencies in accounting, we conducted a survey of the industry in Xiamen City, China, from April to September 2020.

First, basic information of the respondents was collected.

During the survey, a total of 1013 valid questionnaires were collected. About 60% of the respondents were male, and the other 40% of the respondents were female (Table A1).

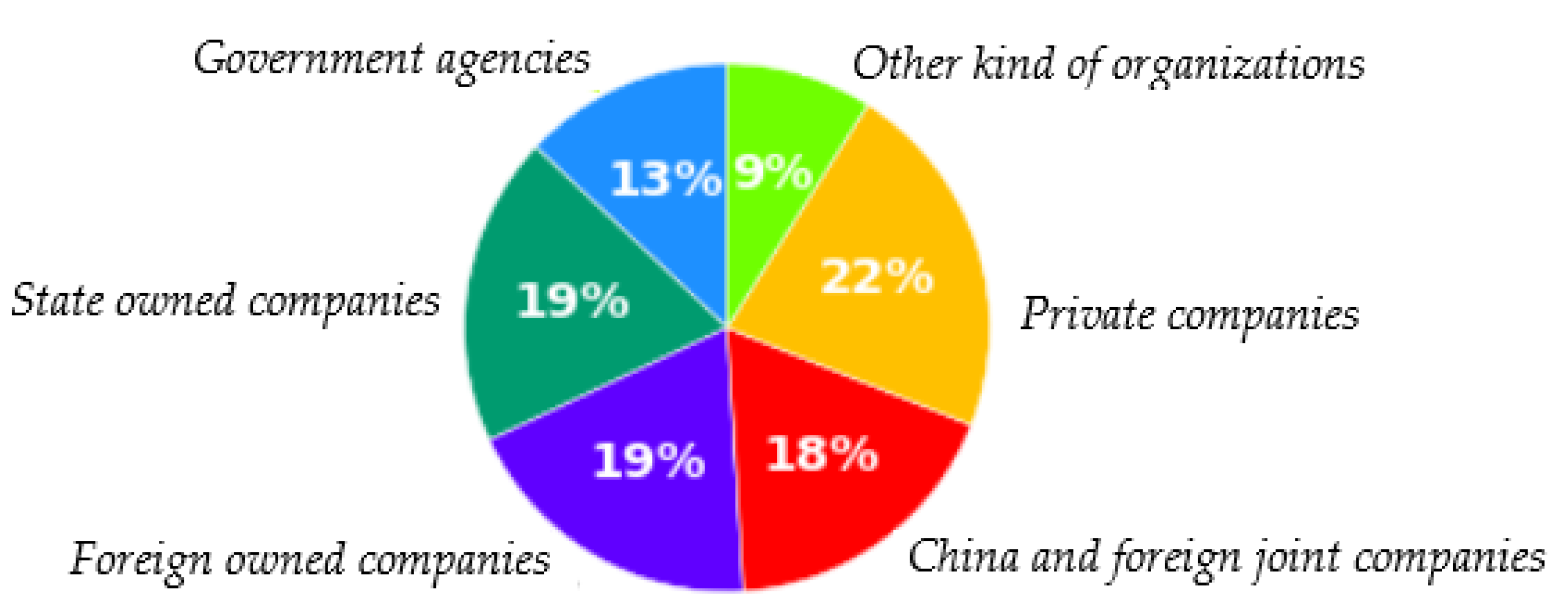

The total of 1013 respondents could be distributed into six different areas (Figure 1): 13% were from government agencies and affiliated institutions, 19% were from state-owned companies, 19% were from foreign-owned companies, 18% were from China and foreign joint companies, 22% were from private companies, and 9% were from other organizations (Table A2).

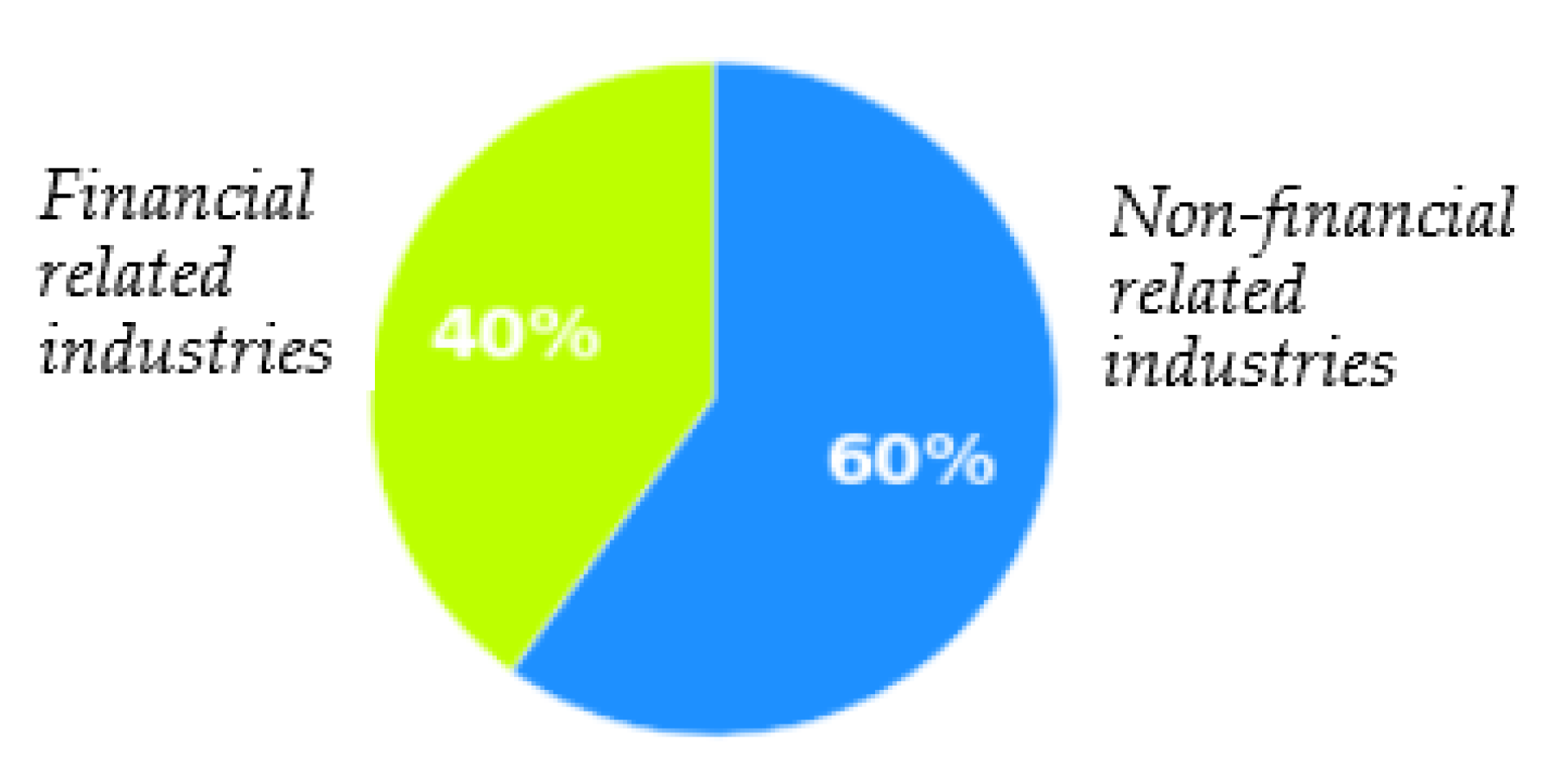

About 40% of the respondents were from financial-related industries, and the other 60% were from other industries (Figure 2, Table A3).

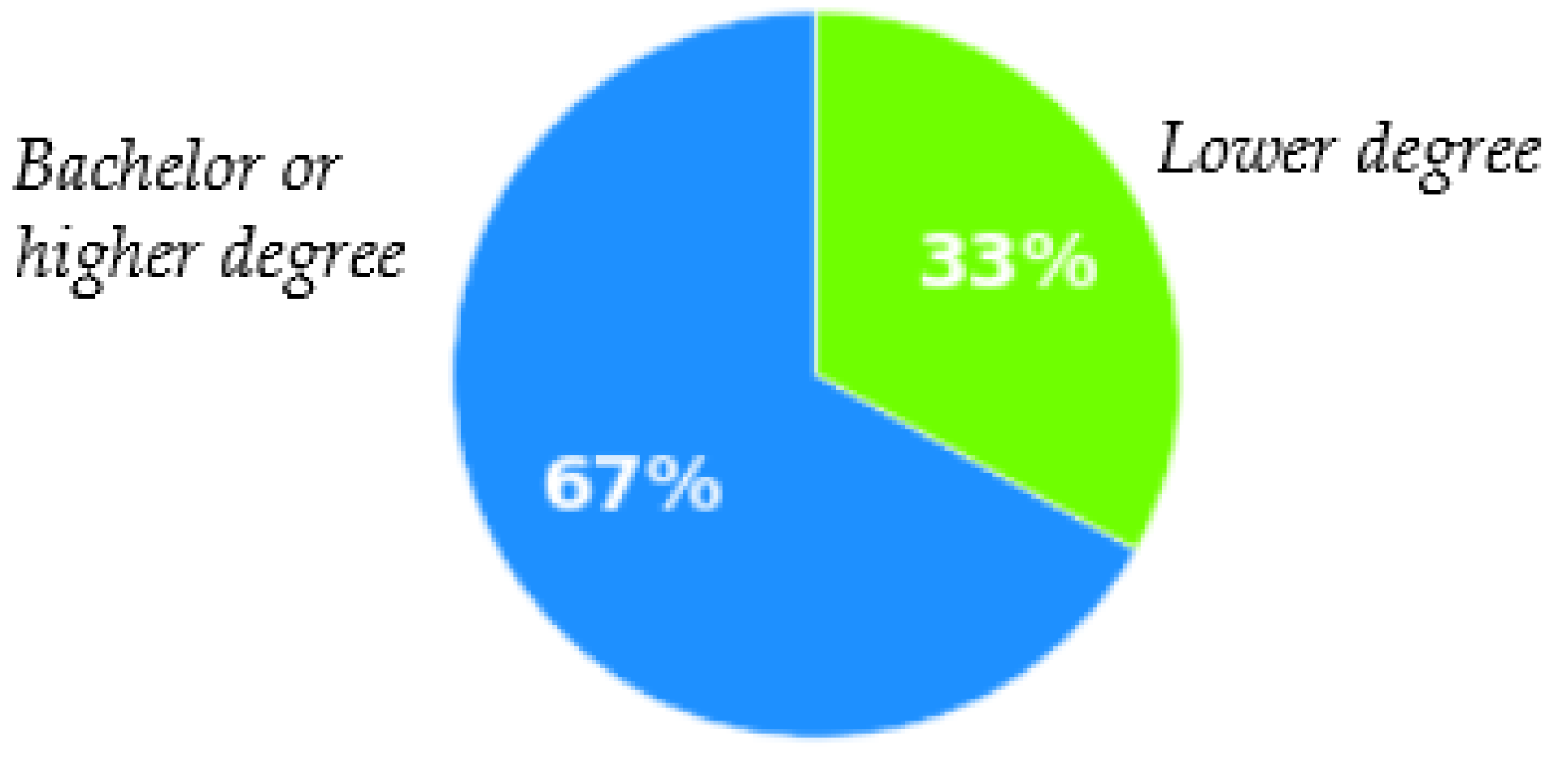

A total of 67% of the respondents held a bachelor’s degree or higher, while the other 33% held a lower degree (Figure 3, Table A4).

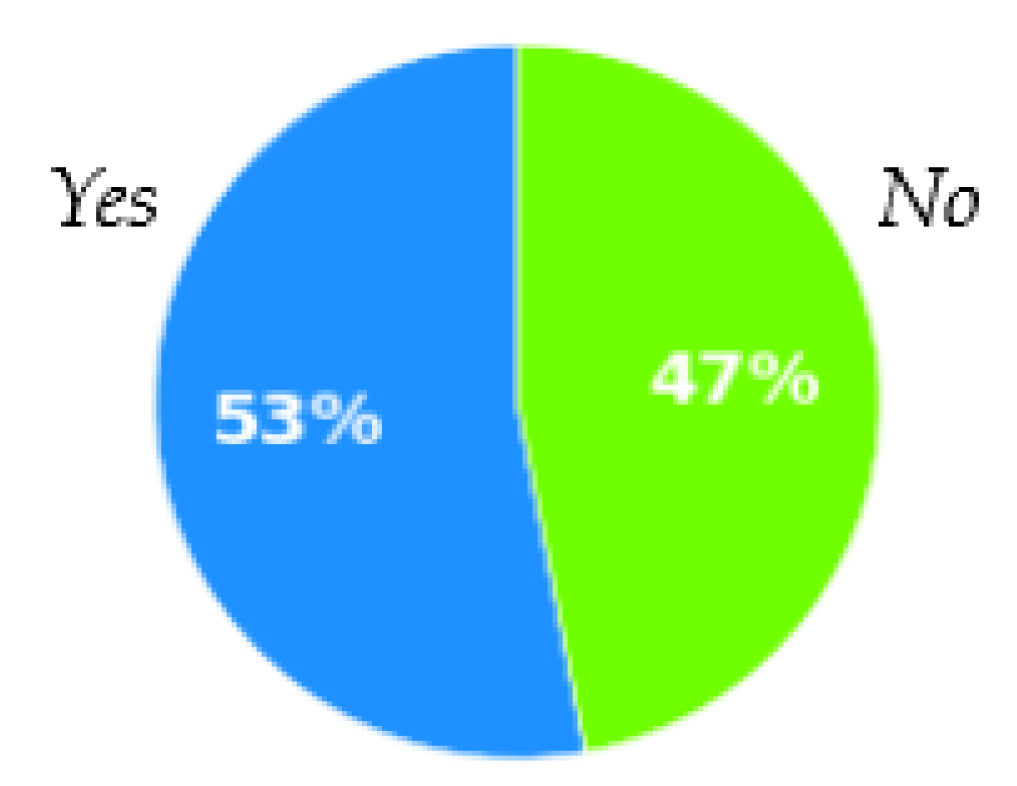

A total of 53% of the respondents have experience with operating financial derivatives, including stocks and options, while 47% of the respondents did not have this experience (Figure 4, Table A5).

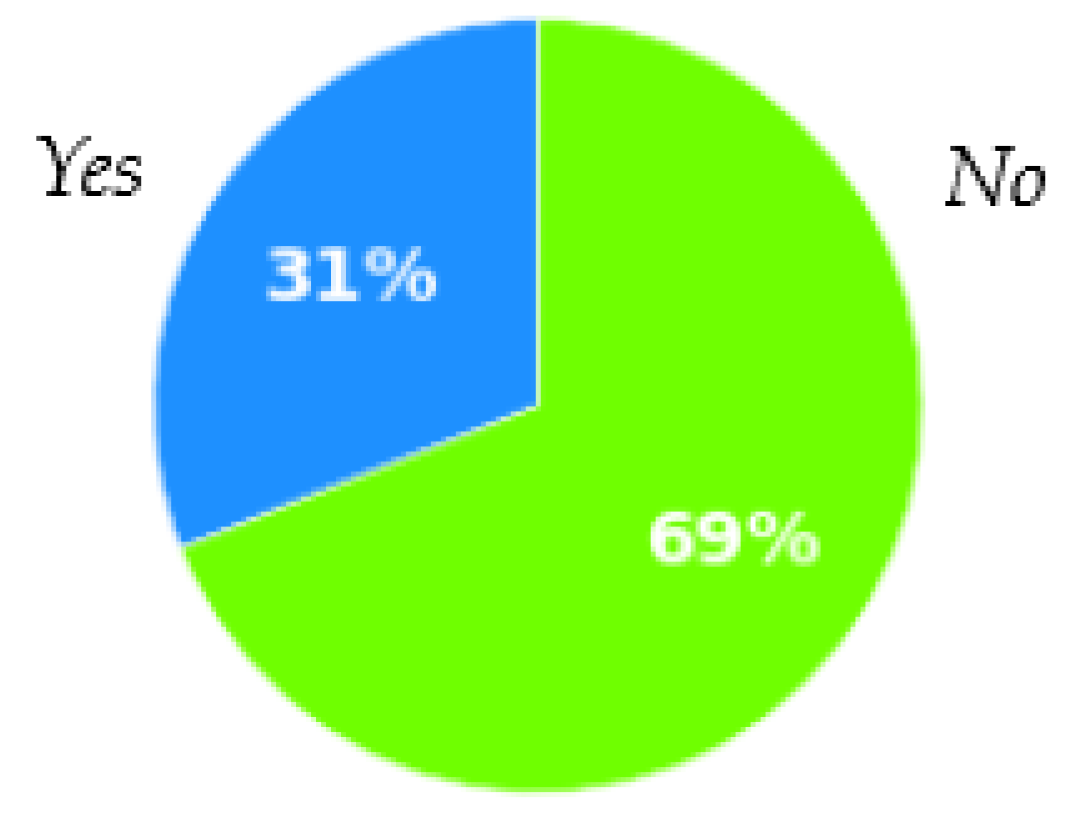

Only 31% of the respondents had experience with holdings of cryptocurrencies, while the other 69% did not (Figure 5, Table A6).

While 100% of the respondents already knew that Bitcoin is the first-ranking cryptocurrency in the world (Table A7), only 38% of the respondents knew that the Ethereum is the second-ranking cryptocurrency in the world (Table A8).

Second, the survey investigated the characteristics of holdings of cryptocurrencies in China.

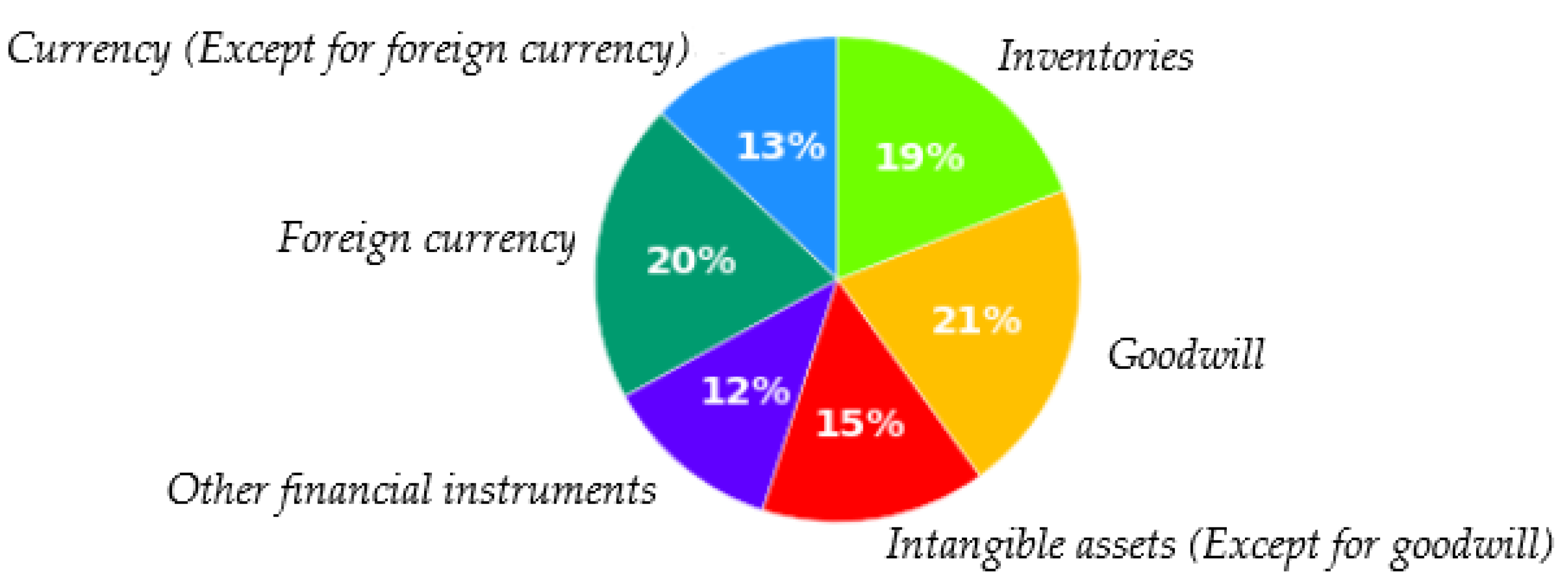

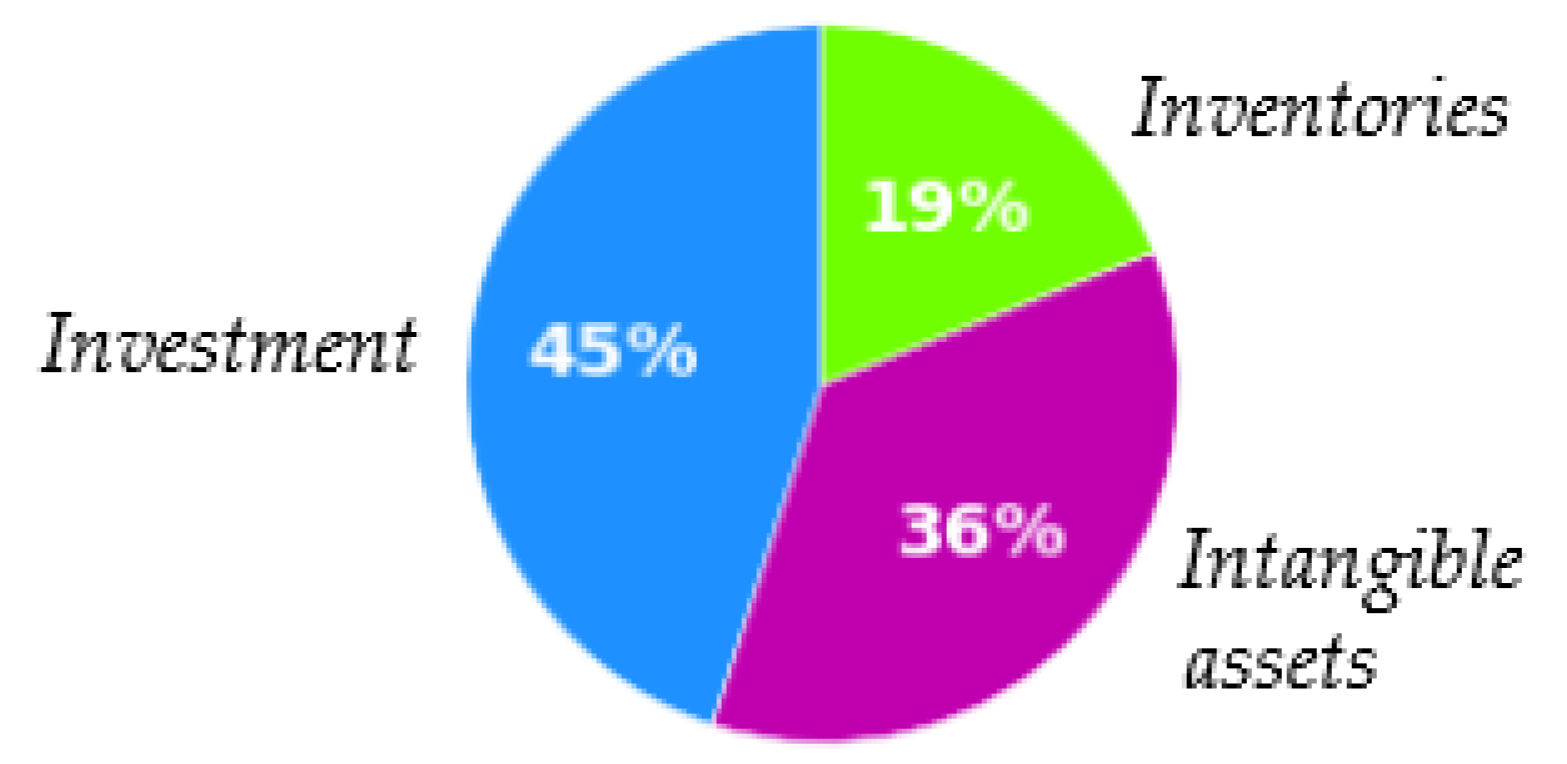

In answer to the question of how companies currently account for holdings of cryptocurrencies, 45% of the respondents stated that entities carry crypto assets as investments (13% as cash, 20% as foreign currencies, and 12% as other financial instruments), 36% of the respondents stated that entities carry crypto assets as intangible assets (15% as intangible assets except for goodwill, and 21% as goodwill), and 19% of the respondents stated that entities carry crypto assets as inventories (Figure 6 and Figure 7, Table A9).

This survey result is similar to that of the DAAC, where 50% of the respondents answered that entities carry crypto assets as investments, 39% as inventories, and 19% as intangible assets (Boring 2019). However, this result differs from the tentative agenda decision of the IFRSIC, because the conclusion of the IFRSIC does not include investments.

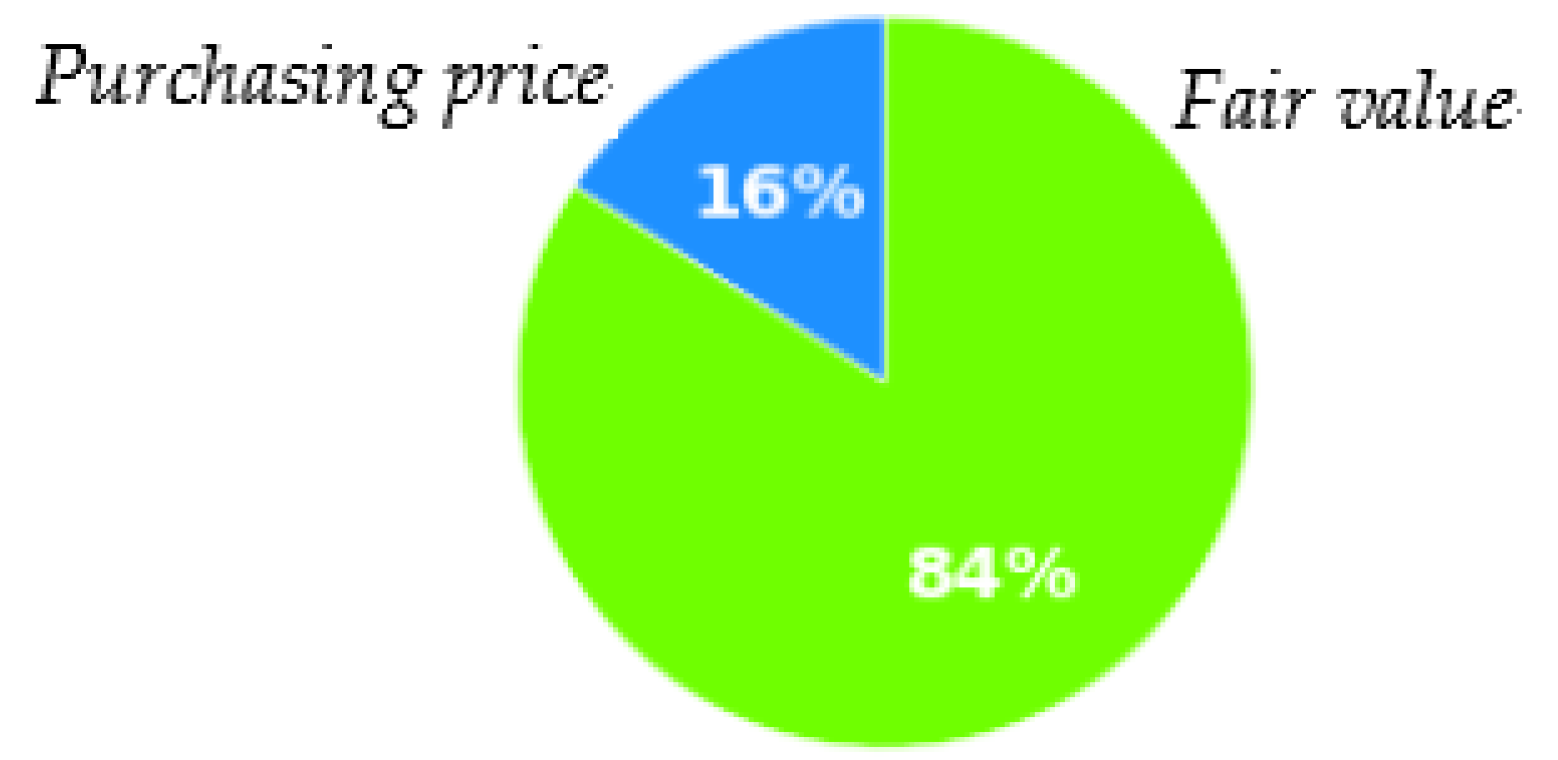

In answer to the question of how to disclose the value of the crypto assets held by entities in accounting, 84% of the respondents stated that entities holding cryptocurrencies should revaluate them at fair value through profit and loss (FVTPL) (Figure 8, Table A10).

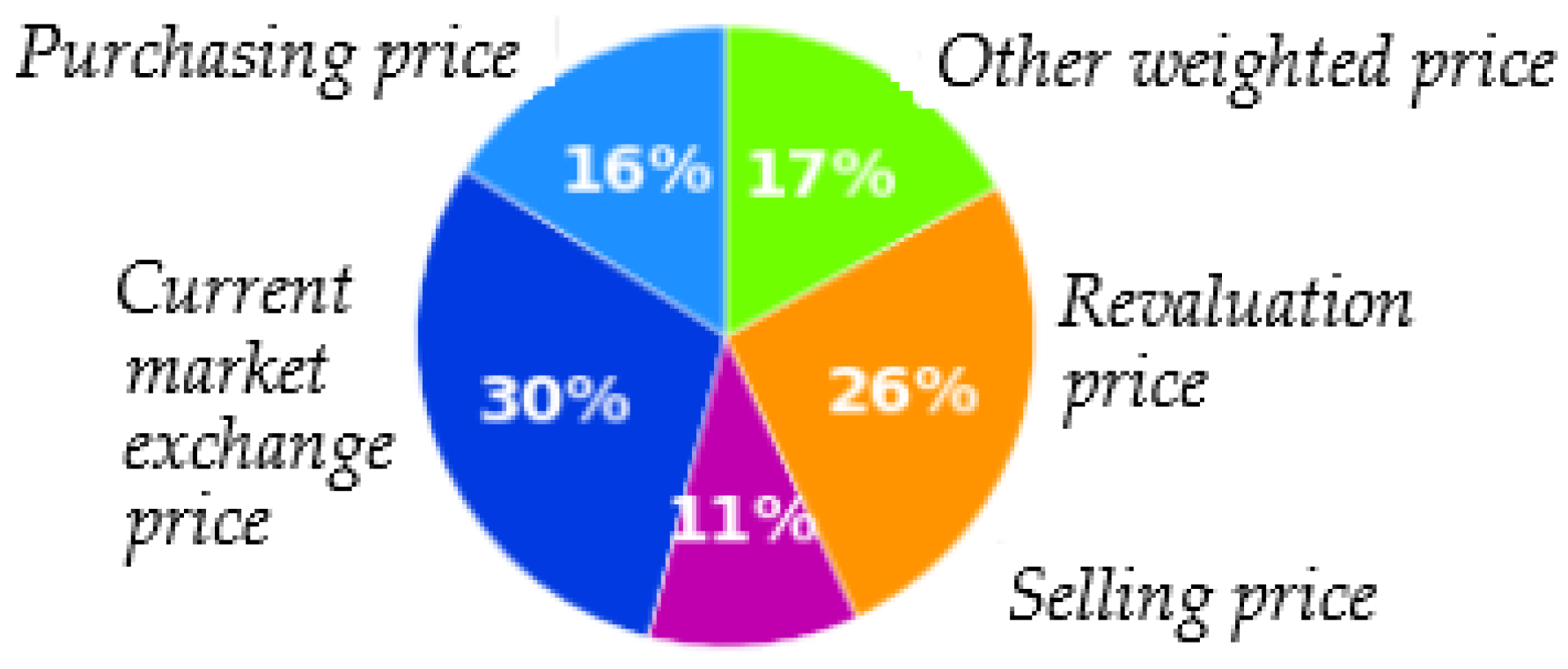

This survey result has also revealed that the 84% of fair value is composed by four different types of fair value, including 30% of current market exchange price, 11% of selling price, 26% of revaluation price and 17% or other weighted price (Figure 9, Table A10).

This percentage of the respondents stated that entities holding cryptocurrencies should revaluate them at FVTPL is much higher than those obtained in the Canadian Securities Administrators Chief Accountants Committee (76%) (Hait et al. 2019) and the DAAC (75%) (Boring 2019).

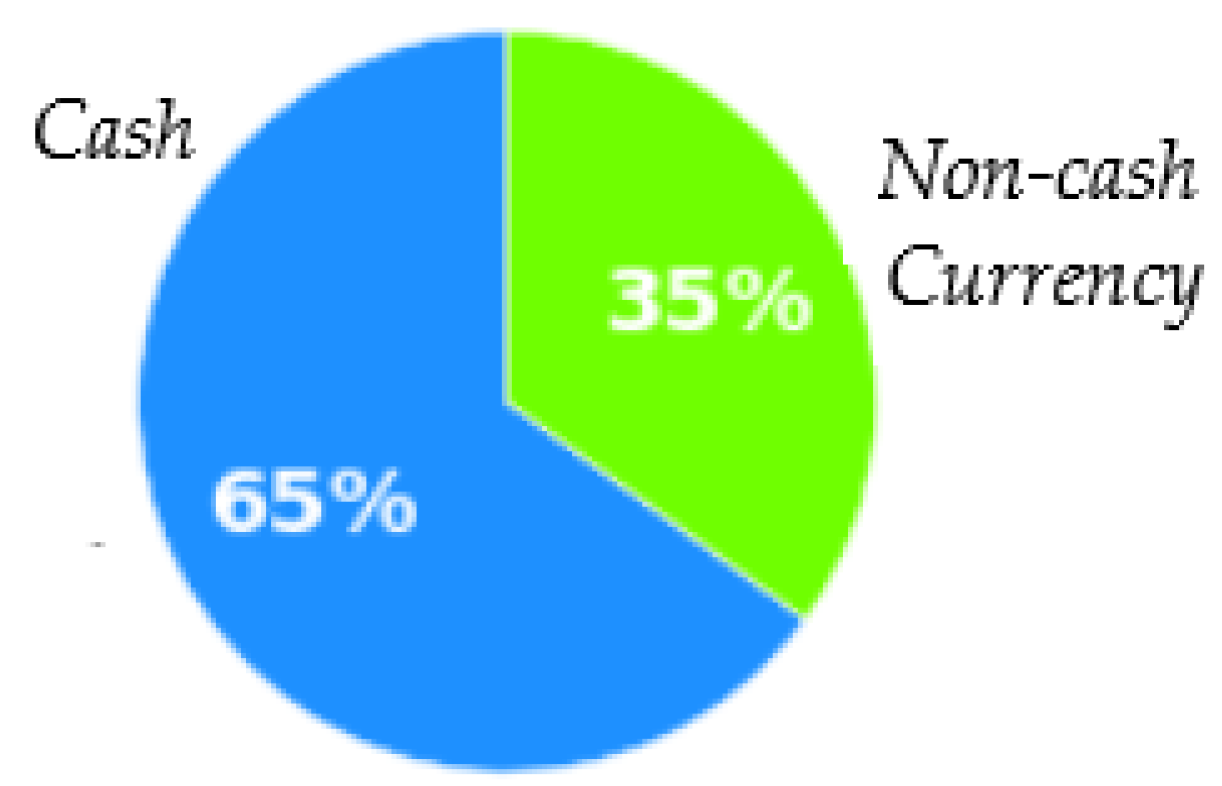

In answer to the question of whether cryptocurrencies are considered cash (currencies), 65% of the respondents stated that cryptocurrencies are cash, whereas 35% of the respondents stated that cryptocurrencies are not cash (Figure 10, Table A11).

This result is different to that of the tentative agenda decision of the IFRSIC, because the conclusion of the IFRSIC was that cryptocurrencies are not cash.

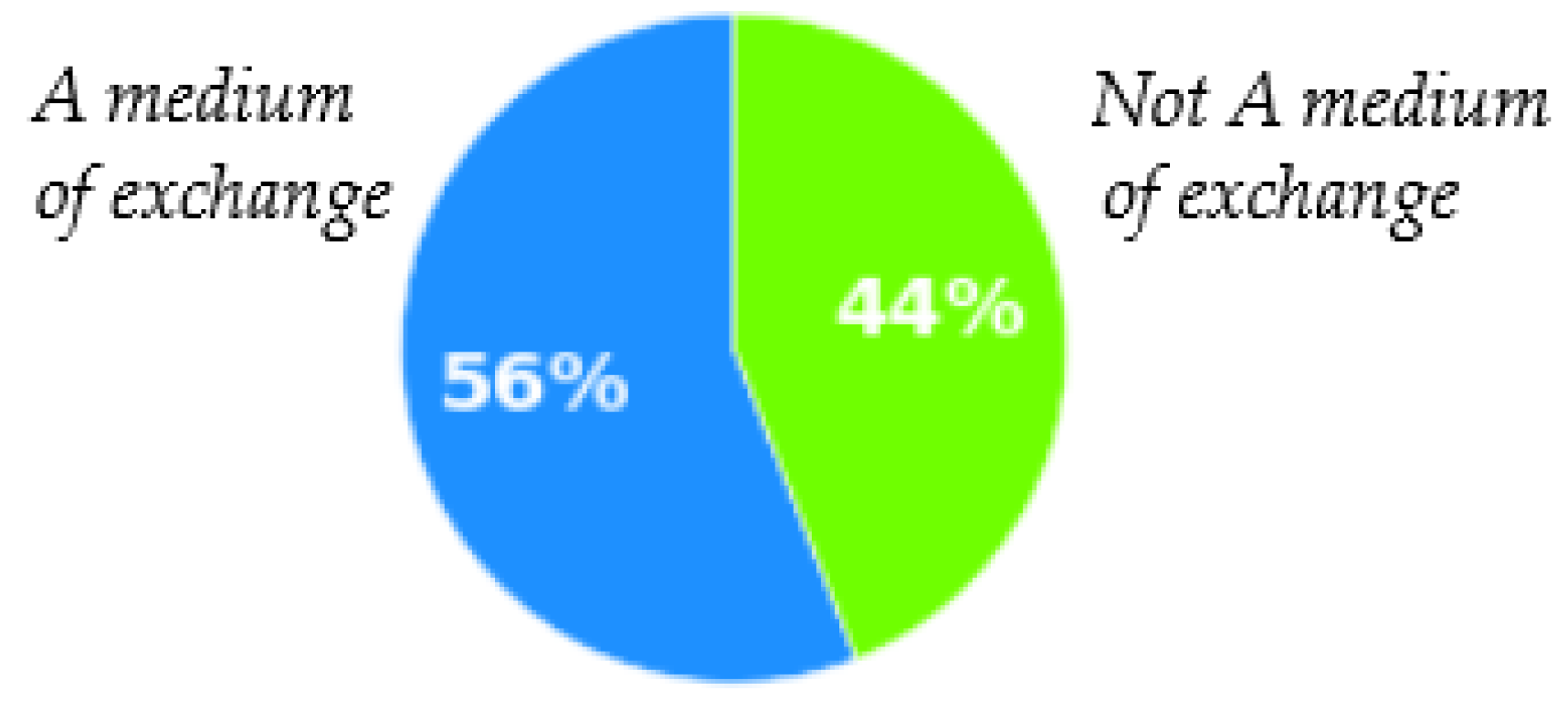

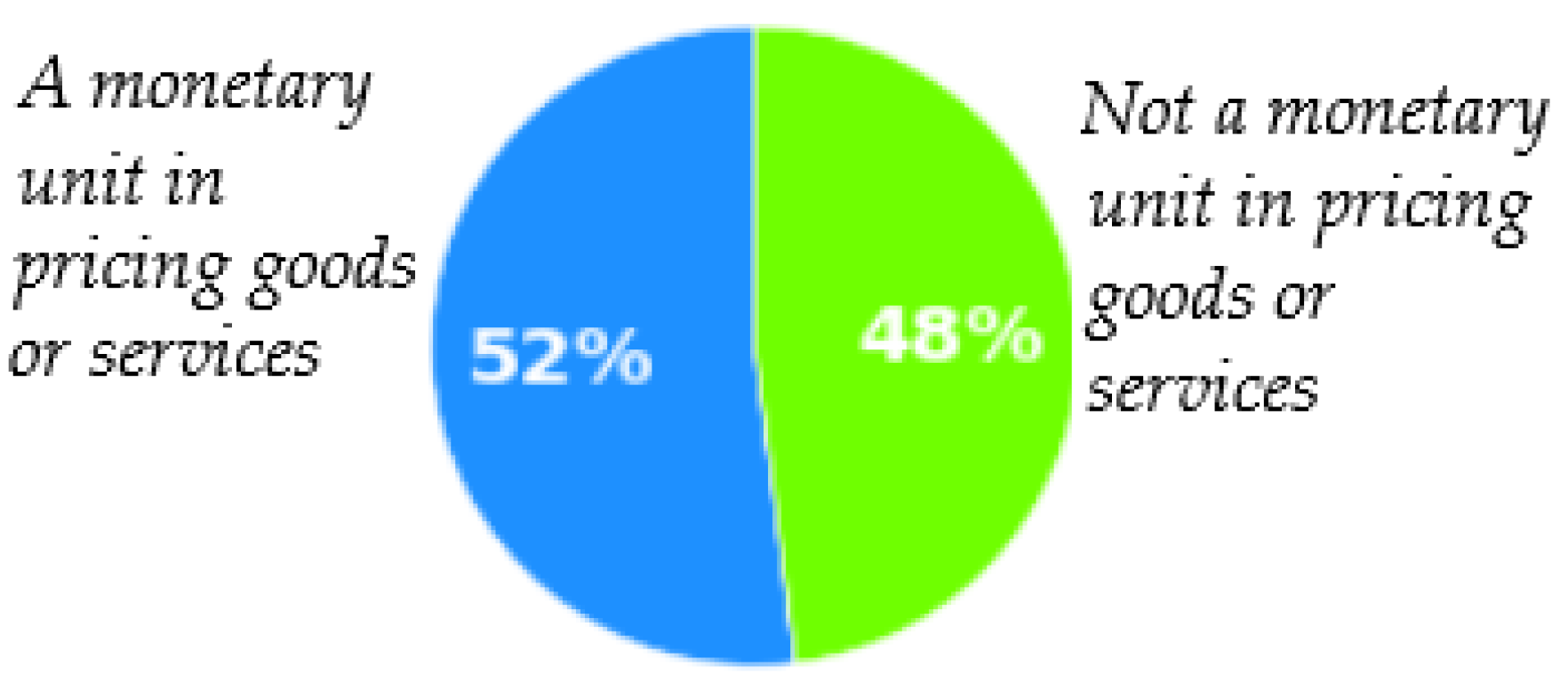

In answer to the question of what functions of a currency that cryptocurrencies have (if the respondent considers cryptocurrencies to be currencies), 56% of the 1013 respondents stated that cryptocurrencies can be used as a medium of exchange (Figure 11), 52% stated that cryptocurrencies can be used as a monetary unit for pricing goods or services (Figure 12), 36% stated that cryptocurrencies can be used to store currency value, and 18% stated that cryptocurrencies can be used as world currencies (Table A12).

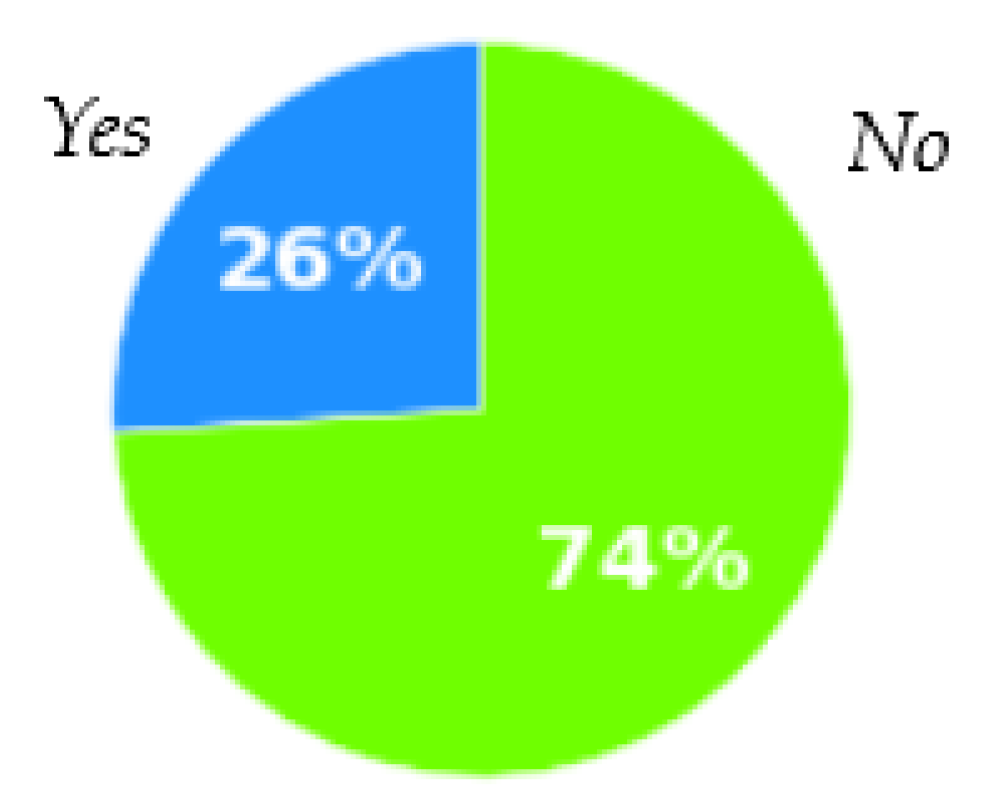

In answer to the question of whether the current accounting standards of the IFRS are appropriate for entities’ holdings of cryptocurrencies, 74% of the respondents answered no, and only 26% of the respondents answered yes (Figure 13, Table A13).

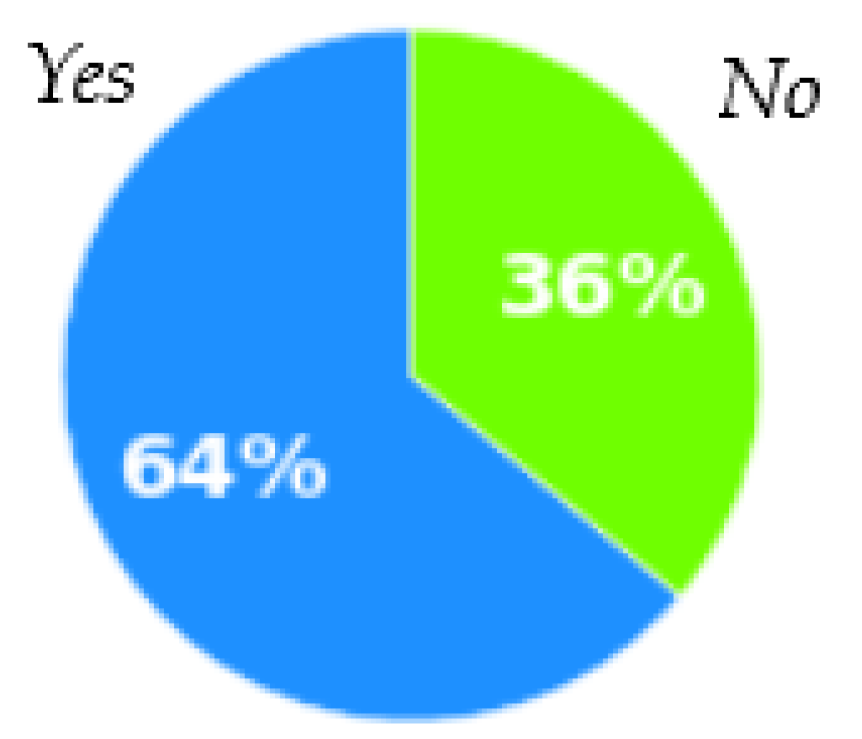

In answer to the question of whether it is essential to make additions to the current standards of the IFRS for holdings of cryptocurrencies, 64% of the respondents answered yes, and 36% of the respondents answered no (Figure 14, Table A14).

In answer to the question of whether the distribution ledger recording the trading of cryptocurrencies has greater advantages than the central ledger recording the trading of traditional currencies, 61% of the respondents answered yes, and 39% of the respondents answered no (Table A15).

In answer to the question of whether the distribution ledger in the blockchain will become a trend that substitutes the central ledger in the future, 54% of the respondents answered yes, and 46% of the respondents answered no (Table A16).

In answer to the question of whether the respondent would accept the use of cryptocurrencies by their partners when doing business with them, 58% of the respondents answered yes, while 42% of the respondents answered no (Table A17).

Third, the survey asked questions about the future trends for holdings of cryptocurrencies in China.

In answer to the question of whether the respondent considered exchange platforms of cryptocurrencies on the Internet to be legal in China, 37% answered yes and 63% answered no (Table A18).

In answer to the question of whether the respondent considered that the trading of cryptocurrencies, including Bitcoin, should be legally permitted in China, 52% answered yes and 48% answered no (Table A19).

In answer to the question of whether the respondent thought holdings of cryptocurrencies would become legal in China in the future, 60% answered yes and 40% answered no (Table A20).

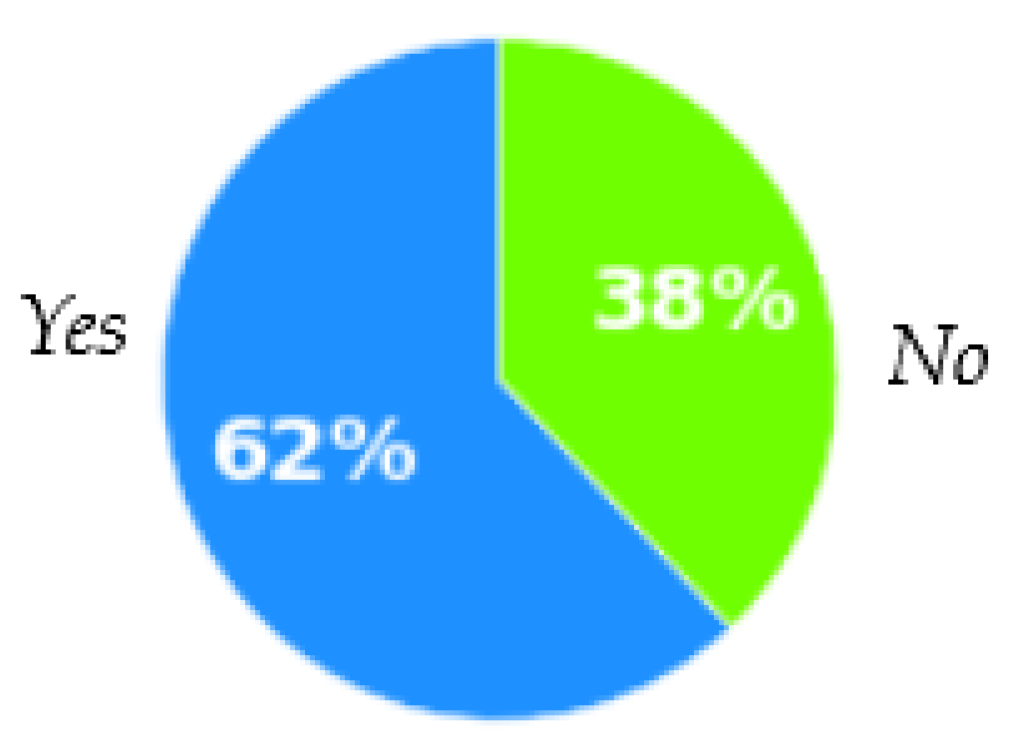

In answer to the question of whether the respondent considered it essential for legal exchange platforms to be set for cryptocurrencies and the management of these platforms to be enhanced in China, 62% answered yes and 38% answered no (Figure 15, Table A21).

Fourth, the survey asked questions about future trends for holdings of cryptocurrencies in China’s Xiamen pilot FTZs.

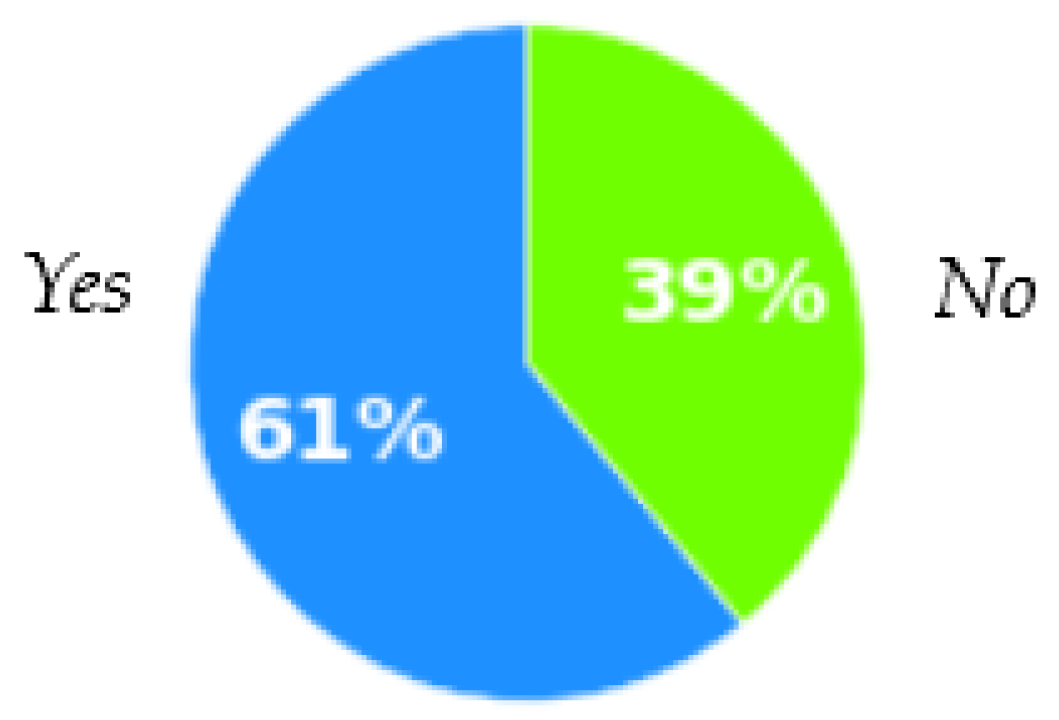

In answer to the question of whether the respondent thought that the legal trade of cryptocurrencies should first be operated and tested in China’s pilot FTZs, 61% answered yes and 39% answered no (Figure 16, Table A22).

In answer to the question about the areas that the legal trade of cryptocurrencies should be first operated and tested in China’s Xiamen pilot FTZs, 59% stated that this should occur and agreed to encourage the setup of platforms for the trading of cryptocurrencies, 55% suggested that the government should give permission to entities to hold and use cryptocurrencies, 51% stated that cryptocurrencies should become legal, and 50% stated that cryptocurrencies should be freely traded (Table A23).

In answer to the question of which industry should be selected as the first to use cryptocurrencies in the pilot FTZs, 58% of the respondents chose the financial industry (Table A24).

3.2. Analysis of the Survey Results and Policy Suggestions

When considering all respondents, this survey tended to collect questionnaires from people with higher educational degrees who had already learned about cryptocurrencies, particularly about the first-ranking cryptocurrency, Bitcoin. This survey is tended to collect questionnaires from people who had work experience in government agencies, state-owned companies, financial organizations, and Internet-related companies.

Because the first contractors and holders of cryptocurrencies preferred to access them via the Internet, and because the questionnaire was focused on the concepts of currency and accounting, it was reasonable to target the questionnaire to people with Internet experience and higher educational degrees in computing, banking, accounting, and some other majors.

Regarding the total number questionnaires received and the industries of the respondents, we consider the survey results to be representative in terms of both quantity and quality. Because the respondents were from many different industries, held higher educational degrees, and had good understanding of cryptocurrencies, including Bitcoin, the survey results give a good idea of the real situation of cryptocurrencies in China.

The survey results fit with the enthusiasms of private companies and individuals with holdings of cryptocurrencies in China. Most respondents responded positively when asked about the developing trend of cryptocurrencies and supported the legal operation and testing of holdings in China’s Xiamen pilot free trade zone.

Nearly one-third of the respondents had experience with holdings of cryptocurrencies, despite there being no legal exchange market or policy support in China.

Most of the respondents stated that they define holdings of cryptocurrencies as investments, inventories, or intangible assets and believe that the value of a cryptocurrency holding is best represented by its market fair value. Most of the respondents stated that they consider cryptocurrencies are currencies with two main functions: a medium of exchange and a monetary unit for pricing goods and services. Most of the respondents confirmed that the current IFRS standards do not satisfy the accounting requirements for holdings of cryptocurrencies. Thus, it is necessary to add to current IFRS standards to make them appropriate for holdings of cryptocurrencies. Most respondents stated the distributed decentralized ledger based on blockchain technology recording the transactions of cryptocurrencies has more advantages than the centralized ledger, which records the transactions of traditional currencies and believe that, in the future, the distributed ledger will replace the centralized ledger.

Although most of the respondents already knew that the trade of cryptocurrencies in China is illegal and strictly prohibited by the Chinese government, they still stated that, in the future, the trade of cryptocurrencies is likely to become legal and be permitted by the government; platforms for the exchange of cryptocurrencies will be set up and regulated by the government; and cryptocurrencies will be accepted and used by firms for business.

One-third of the respondents stated that, in Xiamen city, there are a few firms that record cryptocurrencies as assets in financial statements and use them as monetary units in business contracts to price goods and services. Most respondents estimated that, in Xiamen city, there are about 50–100 firms that are focused on doing business related to the development of cryptocurrencies.

Most respondents supported the setting up of exchange platforms for cryptocurrencies in the Xiamen pilot free trade zone, the holding and use of cryptocurrencies by entities, the trading of cryptocurrencies in a legal mode, and the initial operation and testing of legal trading in the financial industry.

From the survey results, we can see that although most respondents presented an optimistic attitude toward the holding, use, and trading of cryptocurrencies, a few respondents presented a negative attitude. This means that for an opening up policy for cryptocurrencies to be developed, namely, the operation and test exchange of cryptocurrencies in the Xiamen pilot FTZ, it is necessary to maintain a prudent attitude and conduct a complete analysis of policies, environments, and risks to avoid financial risks from the trading of cryptocurrencies.

4. Summary

According to the conclusion of the IFRSIC in March 2019, cryptocurrencies can be seen as inventories, as defined in IAS 2, when an entity holds them for sale in the ordinary course of business; otherwise, cryptocurrencies can be seen as intangible assets, as defined in IAS 38. Because the trade of cryptocurrencies is strictly prohibited by the Chinese government, there have been no comments from Mainland China. However, according to our survey, many private companies and individuals are very keen to do business in the area of cryptocurrencies. Generally, under the reform and opening up policy, the Chinese government has preferred to operate and test its new business policies in a special economic zone (SEZ) or a pilot free trade zone (FTZ). Xiamen City became a special economic zone in 1980 and a pilot free trade zone in 2015. Based on support from the Xiamen City Federation of Social Science Associations (XMSK 2020), we conducted a survey in Xiamen City on holdings of cryptocurrencies in China.

The results represents that, the respondents defined holdings of cryptocurrencies as investments (45%), inventories (36%), or intangible assets (19%) and stated that the value of cryptocurrencies can be better represented by the fair value (Table A9 and Table A10). This result is similar to that of DAAC (Boring 2019), but different to the tentative agenda decision of the IFRSIC, as the conclusion of the IFRSIC does not include investment in its definition. More than half of respondents stated that cryptocurrencies are currencies with two main functions: a medium of exchange (56%) and a monetary unit for pricing goods and services (52%) (Table A12). This differs from the tentative agenda decision of the IFRSIC, which concluded that cryptocurrencies can be considered cash. 74% of the respondents stated that the current IFRS standards do not satisfy the accounting requirements of cryptocurrency holding (Table A13). Thus, it is necessary to discuss the current IFRS standards for holdings of cryptocurrencies. 62% respondents stated that they support the setting up of legal exchange platforms for cryptocurrencies in the Xiamen pilot free trade zone in China (Table A21). Our suggestion is to initially support the operation and testing exchange of cryptocurrencies in the Xiamen pilot FTZ but to be careful to avoid financial risks associated with the trading of cryptocurrencies.

Author Contributions

Conceptualization H.Y.; methodology, H.Y.; software, H.Y.; validation, H.Y.; formal analysis, H.Y. and K.Y.; investigation, H.Y.; resources, H.Y.; data curation, H.Y.; writing—original draft preparation, H.Y. and K.Y.; writing—review and editing, H.Y. and K.Y.; visualization, H.Y. and K.Y.; supervision, K.Y. and R.G.; project administration, H.Y. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by [Xiamen City Federation of Social Science Associations] grant number [2020-16].

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Statistics of the Valid Questionnaires on Holdings of Cryptocurrencies in Accounting

Appendix A.1. Statistics from the Questions Related to the Basic Information of the Respondents

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Are you male or female (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Male | 612 | 60% |

| Female | 401 | 40% |

| Sum | 1013 | 100% |

Table A2.

Which industry are you from (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Government agencies | 131 | 13% |

| State owned companies | 195 | 19% |

| Foreign owned companies | 197 | 19% |

| China and foreign joint companies | 187 | 18% |

| Private companies | 217 | 22% |

| Other kind of organizations | 86 | 9% |

| Sum | 1013 | 100% |

Table A3.

Are you working in the financial related industries (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Financial related industries | 405 | 40% |

| Non-financial related industries | 608 | 60% |

| Sum | 1013 | 100% |

Table A4.

Do you hold a bachelor or higher degree (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Bachelor or higher degree | 676 | 67% |

| Lower degree | 337 | 33% |

| Sum | 1013 | 100% |

Table A5.

Do you have any experiences on operating financial derivatives (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 535 | 53% |

| No | 478 | 47% |

| Sum | 1013 | 100% |

Table A6.

Do you have any experiences on holdings of cryptocurrencies (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 318 | 31% |

| No | 695 | 69% |

| Sum | 1013 | 100% |

Table A7.

Have you already learned Bitcoin (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 1013 | 100% |

| No | 0 | 0% |

| Sum | 1013 | 100% |

Table A8.

Which cryptocurrency have you already learned (multiple-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Digital Renminbi (DCEP) | 345 | 34% |

| Ethereum (ETH) | 380 | 38% |

| EOS (EOS) | 90 | 9% |

| Litecoin (LTC) | 90 | 9% |

| XRP (XRP) | 79 | 8% |

| Tether (USDT) | 64 | 6% |

| TRON (TRX) | 78 | 8% |

| Monero (XMR) | 92 | 9% |

| Others | 77 | 8% |

| No (except for Bitcoin) | 288 | 28% |

Appendix A.2. Statistics from the Questions of the Characteristics on Holdings of Cryptocurrencies in China

Table A9.

How companies to account for holdings of cryptocurrencies (multiple-choice question)?

| Selections | Number of the Respondents | Percentages | Weight Average | Sum | |

|---|---|---|---|---|---|

| Investments | Currency (Except for foreign currency) | 241 | 24% | 13% | 45% |

| Foreign currency | 354 | 35% | 20% | ||

| Other financial instruments | 210 | 21% | 12% | ||

| Intangible assets | Intangible assets (Except for goodwill) | 264 | 26% | 15% | 36% |

| Goodwill | 384 | 38% | 21% | ||

| Inventories | Inventories | 341 | 34% | 19% | 19% |

| Sum (The valid questionnaires are 1013) | 100% | 100% | |||

Table A10.

How to disclose the values of cryptocurrencies in accounting (multiple-choice question)?

| Selections | Number of the Respondents | Percentages | Weight Average | Sum | |

|---|---|---|---|---|---|

| Purchasing price | Purchasing price | 279 | 28% | 16% | 16% |

| Fair value | Current market exchange price | 513 | 51% | 30% | 84% |

| Selling price | 186 | 18% | 11% | ||

| Revaluation price | 436 | 43% | 26% | ||

| Other (Except for purchasing price) | 293 | 29% | 17% | ||

| Sum (The valid questionnaires are 1013) | 100% | 100% | |||

Table A11.

Do you think that cryptocurrencies are cash or non-cash currency (single-choice question)?

Table A11.

Do you think that cryptocurrencies are cash or non-cash currency (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Cash | 661 | 65% |

| Non-cash Currency | 352 | 35% |

| Sum | 1013 | 100% |

Table A12.

What functions of currency do you think that cryptocurrencies have (multiple-choice question)?

Table A12.

What functions of currency do you think that cryptocurrencies have (multiple-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| A medium of exchange | 576 | 56% |

| A monetary unit in pricing goods or services | 534 | 52% |

| A store of value | 375 | 36% |

| A world currency | 185 | 18% |

Table A13.

Are the current IFRS standards satisfied holdings of cryptocurrencies (single-choice question)?

Table A13.

Are the current IFRS standards satisfied holdings of cryptocurrencies (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 266 | 26% |

| No | 747 | 74% |

| Sum | 1013 | 100% |

Table A14.

Is it necessary to add new projects to current IFRS standards for holdings of cryptocurrencies (single-choice question)?

Table A14.

Is it necessary to add new projects to current IFRS standards for holdings of cryptocurrencies (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 646 | 64% |

| No | 367 | 36% |

| Sum | 1013 | 100% |

Table A15.

Do you think that the distribution ledger in blockchain will become a trend and substitute the central ledger in the future (single-choice question)?

Table A15.

Do you think that the distribution ledger in blockchain will become a trend and substitute the central ledger in the future (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 621 | 61% |

| No | 392 | 39% |

| Sum | 1013 | 100% |

Table A16.

Do you think that the distribution ledger recording the trading of cryptocurrencies has higher advantages than the central ledger in the future (single-choice question)?

Table A16.

Do you think that the distribution ledger recording the trading of cryptocurrencies has higher advantages than the central ledger in the future (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 543 | 54% |

| No | 470 | 46% |

| Sum | 1013 | 100% |

Table A17.

Will you accept that your partners use cryptocurrencies in the business when you are doing business with them (single-choice question)?

Table A17.

Will you accept that your partners use cryptocurrencies in the business when you are doing business with them (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 592 | 58% |

| No | 421 | 42% |

| Sum | 1013 | 100% |

Appendix A.3. Statistics from the Questions of the Future Trend of Holdings of Cryptocurrencies in China

Table A18.

Do you think that exchange platforms of cryptocurrencies existed on the Internet are legal in China (single-choice question)?

Table A18.

Do you think that exchange platforms of cryptocurrencies existed on the Internet are legal in China (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 379 | 37% |

| No | 634 | 63% |

| Sum | 1013 | 100% |

Table A19.

Do you think that the trading of cryptocurrencies including Bitcoin in China should be legally permitted (single-choice question)?

Table A19.

Do you think that the trading of cryptocurrencies including Bitcoin in China should be legally permitted (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 529 | 52% |

| No | 484 | 48% |

| Sum | 1013 | 100% |

Table A20.

Do you think that holdings of cryptocurrencies will become legal in the future in China (single-choice question)?

Table A20.

Do you think that holdings of cryptocurrencies will become legal in the future in China (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 607 | 60% |

| No | 406 | 40% |

| Sum | 1013 | 100% |

Table A21.

Do you think that in China it is essential to set legal exchange platforms of cryptocurrencies and enhance platforms’ management (single-choice question)?

Table A21.

Do you think that in China it is essential to set legal exchange platforms of cryptocurrencies and enhance platforms’ management (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 624 | 62% |

| No | 389 | 38% |

| Sum | 1013 | 100% |

Appendix A.4. Statistics from the Questions Related to the Future Trend of Holdings of Cryptocurrencies in China’s Xiamen Pilot FTZs

Table A22.

Do you think that the legal trade of cryptocurrencies should be firstly permitted to operate and test in China’s Xiamen pilot FTZs (single-choice question)?

Table A22.

Do you think that the legal trade of cryptocurrencies should be firstly permitted to operate and test in China’s Xiamen pilot FTZs (single-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Yes | 615 | 61% |

| No | 398 | 39% |

| Sum | 1013 | 100% |

Table A23.

What do you think that the legal trade of cryptocurrencies should be firstly permitted to operate and test in China’s Xiamen pilot FTZs (multiple-choice question)?

Table A23.

What do you think that the legal trade of cryptocurrencies should be firstly permitted to operate and test in China’s Xiamen pilot FTZs (multiple-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| To set up platforms for the trading of cryptocurrencies | 599 | 59% |

| To allow entities holding and using cryptocurrencies | 554 | 55% |

| To support that cryptocurrency will become legality | 516 | 51% |

| To support that cryptocurrencies will be freedom traded | 505 | 50% |

Table A24.

Do you think which industry can be selected as the first industry to use cryptocurrencies in the pilot FTZs (multiple-choice question)?

Table A24.

Do you think which industry can be selected as the first industry to use cryptocurrencies in the pilot FTZs (multiple-choice question)?

| Selections | Number of the Respondents | Percentages |

|---|---|---|

| Financial industry | 589 | 58% |

| Foreign trade industry | 499 | 49% |

| IT related industry | 449 | 44% |

| Medicine industry | 135 | 13% |

| Commercial industry | 277 | 27% |

| Other | 272 | 27% |

| 1 | Meitu Inc. is the biggest company that holds cryptocurrencies in Xiamen city. It is an artificial intelligence (AI) driven technology company with a total of 246 million monthly active users in the field of computer vision, deep learning, and computer graphics. The Company’s two main subsidiaries are Xiamen Meitu Networks Technology Co., Ltd. and Xiamen MeituEve Networks Services Co., Ltd. From the example of Meitu Inc., we can see that the survey of holdings of cryptocurrencies in accounting is very important in Xiamen city, China. The survey results will really provide some supports to companies when they assess the holdings of cryptocurrencies in accounting. |

References

- Barckow, Andreas. 2019. Comments on the Tentative Agenda Decision Relating to Holdings of Cryptocurrencies from Accounting Standards Committee of Germany (ASCG). Comment Letters on Holdings of Cryptocurrencies, IFRS Interpretations Committee Meeting, June 2019. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap13-ias-19-plan-classification.pdf (accessed on 15 May 2020).

- Blockchain. 2020. Bitcoin. Blockchain. October 16. Available online: https://www.blockchain.com/explorer (accessed on 15 May 2020).

- Boring, Perianne. 2019. Comments on the Tentative Agenda Decision Relating to Holdings of Cryptocurrencies from the Chamber of Digital Commerce, Washington, DC. Comment Letters on Holdings of Cryptocurrencies, IFRS Interpretations Committee Meeting, June 2019. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12a-comment-letters.pdf (accessed on 15 May 2020).

- Cervantes, Felipe Perez. 2019. Comments on the Tentative Agenda Decision Relating to Holdings of Cryptocurrencies from the Mexican Financial Reporting Standards Board, Consejo Mexicano de Normas de Información Financiera (CINIF). Comment Letters on Holdings of Cryptocurrencies, IFRS Interpretations Committee Meeting, June 2019. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12a-comment-letters.pdf/ (accessed on 15 May 2020).

- CGTN. 2019. China Announces Master Plan for Six New Pilot Free Trade Zones. China Global Television Network (CGTN). August 26. Available online: https://news.cgtn.com/news/2019-08-26/China-announces-a-master-plan-for-six-new-pilot-free-trade-zones-JthIPT32bm/index.html (accessed on 18 September 2020).

- CSRC. 2013. Circular on Preventing Risks Related to Bitcoin. The People’s Bank of China (PBOC), Ministry of Industry and Information Technology (MIIT), China Banking Regulatory Commission (CBRC), China Securities Regulatory Commission (CSRC), China Insurance Regulatory Commission (CIRC), December 3. Available online: http://www.csrc.gov.cn/pub/newsite/flb/flfg/bmgf/zh/gfxwjfxq/201401/t20140122_242972.html (accessed on 17 September 2020).

- CSRC. 2017. Announcement on Preventing Financial Risks from Initial Coin Offerings. People’s Bank of China (PBOC), Cyberspace Administration of China (CAC), Ministry of Industry and Information Technology (MIIT), State Administration for Industry and Commerce (SAIC), China Banking Regulatory Commission (CBRC), China Securities Regulatory Commission (CSRC), China Insurance Regulatory Commission (CIRC), September 4. Available online: http://www.csrc.gov.cn/pub/newsite/zjhxwfb/xwdd/201709/t20170904_323047.html (accessed on 17 September 2020).

- Ferreira, Paulo Roberto Gonçalves, and José Carlos Bezerra da Silva. 2019. Comments on the Tentative Agenda Decision Relating to Holdings of Cryptocurrencies from the Securities and Exchange Commission of Brazil (CVM). Comment Letters on Holdings of Cryptocurrencies, IFRS Interpretations Committee Meeting, June 2019. May 15. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12a-comment-letters.pdf/ (accessed on 5 September 2020).

- Hait, Carla-Marie, Lara Gaede, Cameron McInnis, and Nicole Parent. 2019. Comments on the Tentative Agenda Decision—Holdings of Cryptocurrencies from The Canadian Securities Administrators (CSA) Chief Accountants Committee. Comment Letters on Holdings of Cryptocurrencies, IFRS Interpretations Committee Meeting, June 2019. May 2. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12a-comment-letters.pdf (accessed on 5 September 2020).

- Hardidge, David. 2019. Comments on the Tentative Agenda Decision—Holdings of Cryptocurrencies. Comment Letters on Holdings of Cryptocurrencies, IFRS Interpretations Committee Meeting, June 2019. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12a-comment-letters.pdf (accessed on 8 May 2020).

- Haygarth, Edward. 2019. Comments on the Tentative Agenda Decision Relating to Holdings of Cryptocurrencies from Global IFRS Team, Grant Thornton International Ltd. Comment Letters on Holdings of Cryptocurrencies, IFRS Interpretations Committee Meeting, June 2019. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12a-comment-letters.pdf (accessed on 15 May 2020).

- IFRSIC (IFRS Interpretations Committee). 2019a. Committee’s Tentative Agenda Decisions on Holdings of Cryptocurrencies. Update March. Available online: https://www.ifrs.org/news-and-events/updates/IFRSIC-updates/march-2019/#1 (accessed on 9 September 2020).

- IFRSIC (IFRS Interpretations Committee). 2019b. Comment letters on Holdings of Cryptocurrencies. June. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12a-comment-letters.pdf (accessed on 5 September 2020).

- Investing. 2022. Today’s Cryptocurrency Prices. Available online: https://cn.investing.com/crypto/currencies (accessed on 18 February 2022).