Does Short-Termism Influence the Market Value of Companies? Evidence from EU Countries

Department of International Finance and Investments, Faculty of Economics and Sociology, University of Lodz, Rewolucji 1905 Street 41, 90-255 Lodz, Poland

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2020, 13(11), 272; https://doi.org/10.3390/jrfm13110272

Submission received: 13 October 2020

/

Revised: 31 October 2020

/

Accepted: 3 November 2020

/

Published: 6 November 2020

(This article belongs to the Special Issue International Trends and Economic Sustainability on Emerging Markets)

Abstract

:This paper fits into the stream of current research on the concept of short-termism and its importance for economic sustainability, especially sustainable finance. Short-termism focuses on short time horizons by both corporate managers and the financial markets, and prioritizes short-time shareholder return over the long-term growth of the company’s value. This study engages the short-termism discussion by examining the effect of quarterly reporting on the long-term market value of listed companies. The aim of the article is to determine whether European companies experience the negative effects of short-termism, precisely, whether public companies that prepare quarterly reports, and which focus mainly on achieving the short-term goals of stock exchange investors, are seeing a decline in their market value in the long-term. We have not proven the existence of such a dependence, the increase in reporting frequency of public companies does not contribute to a decline in their long-term market value. In the case of the EU-15 the results of regression model estimation indicate a positive and statistically significant impact of the time of regular quarterly reporting on the buy-and-hold rates of return, in the “new” EU member states this relationship is not observed.

1. Introduction

The degradation of the natural environment caused by human economic activity has become one of the key reasons for the concept of sustainable economic development. The financial sector is a part of the economic system that acts as an intermediary in the distribution of funds in the economy. The challenges of sustainable development require reforming the financial system, investment funds should be allocated to the projects that fit into the idea of a sustainable economy—“sustainability is the theme of our time—and the financial system has a key role to play in delivering that set of ambitions” (Final Report 2018, p. 3). As a result of combining sustainable development with the activities of the financial sector, the concept of “sustainable finance” was created, which is perceived mainly in the context of the transmission of funds to projects that take into account the environmental, social, and governance factors1—ESG (USSIF).

Such an interpretation of the term “sustainable finance” does not seem accurate—these investments are mainly part of the so-called “green finance”, as investments in low-emission projects are defined. The G20 Green Finance Study Group (2016) defines green finance as financing investments that provide environmental benefits in the broader context of environmentally sustainable development. Sustainable finance includes green finance, but it is a much broader concept and relates to the functioning of the entire financial system, not only the issue of the final destination of investment funds. Proenvironmental investments require the long-term commitment of financial resources (Final Report 2018), which is associated with an increase in investment risk.

The instability of the contemporary world economy and changes taking place on the international financial markets have contributed to changes in investors’ behavior. Investors increasingly prefer shorter periods of financial commitment due to, inter alia, growing risk aversion (Yanovski et al. 2020). Currently, investments with a horizon of more than 3 (Atherton et al. 2007) or 6 years (ESMA 2019) are seen to be long-term. The shortening of the investment horizon has direct consequences for the enterprises’ functioning as they are forced to redefine their long-term plans.

The financial markets, on which companies are looking for investment capital, are characterized by an asymmetry of information (Grossman and Stiglitz 1980; Greenwald et al. 1984; Hubbard 1998), where the capital takers, i.e., enterprises, are privileged entities (Thakor 1990; Healy and Palepu 2001). In order to counteract the negative consequences of information asymmetry for investors, countries take measures to ensure that they have access to information on publicly traded companies that is cyclical and as exhaustive as possible. It is customary for companies to publish annual and semiannual reports (European Parliament and of the Council 2013), while in some countries, the requirement to publish quarterly reports has been introduced (Link 2012).

Theoretically, the greater frequency of publishing information about companies should help reduce the scale of information asymmetry on the financial markets and have a positive impact on the performance of both the investors and the companies (Goldstein and Yang 2017). In practice, the introduction of quarterly reporting contributed to the emergence of a highly unfavorable phenomenon—investors (capital providers) exerting pressure on company management boards (capital takers) to maximize profits in the short term (Yongtae et al. 2017). Consequently, the decrease in the scale of information asymmetry in the investor-company relationship contributed to a potential increase in the asymmetry of benefits of these two groups—an increase in investor benefits and a decrease in corporate benefits.

On the other hand, some authors argue that disclosing too much information is not always good for stock investors. A unique experiment conducted by Abudy and Shust (2020), in which a regulator limited voluntary disclosure of oil and gas firms, showed that after the new regulation came into effect, studied firms generated less unexplained trading volume than before the regulation. Authors explained it by a decline in investor disagreement following the rule. Furthermore, research concerning what happens to trading volume when the regulator bans voluntary disclosure was conducted by Friedman et al. (2020), who studied how the potential for discretionary disclosure affects the way a firm designs its reporting system. They argue that companies’ primary but nonexclusive concern is to induce beliefs that exceed a threshold.

However, the remedy for the information asymmetry proved to have unexpected side effects. The forced change of corporate strategy, which resulted from market pressure (i.e., investors) to achieve quick profits at the expense of achieving long-term goals, was called “short-termism”. Short-termism means focusing on short time horizons by both the corporate managers and the financial markets, and prioritizing near-time shareholder interest over the long-term growth of the companies (Reilly et al. 2016). Alternatively, corporate stakeholders—investors, managers, board members, and auditors—show a preference for strategies that add less value but have an earlier payoff relative to strategies that would add more value in the long run (Jackson and Petraki 2011b).

Short-termism, seen, for example, through the prism of the short-term reporting of companies, has become the subject of severe criticism in the context of meeting the challenges of sustainable development. Due to the necessity to incur capital expenditures on pro-environmental activities, companies may show a deterioration of financial results in the short term reflected in their financial reports. Companies face a dilemma—whether to pursue long-term goals in line with their (and the economy’s) interests, or focus on short-term goals that are in line with investors’ expectations. As Souder et al. (2016) noticed, the most positive returns occur when long-horizon investments are aligned with investor patience. Consequently, a paradox appears—investors, i.e., the owners of an enterprise, prefer to achieve short-term goals at the expense of its future development (Haldane 2011). This paradox results from the fact that short-term investors, who do not participate in managing the enterprise due to the scale of capital involvement and/or the investment strategy, are mainly interested in its current financial results. If one takes into account these two groups with conflicting interests—capital providers and capital buyers—it is crucial which group will be supported by the state, representing the interests of the broadly understood economy.

The original assumption was that on the financial markets, the negative effects of information asymmetry significantly deteriorate the position of investors (capital providers) in relation to enterprises (capital takers). Thus, capital providers should be protected by legal regulations that reduce the level of this asymmetry. For this reason, in 2004, the EU adopted a directive (European Parliament and of the Council 2004) pursuant to which public companies were obliged to publish quarterly reports. It was intended to increase the transparency of the activities of entities operating in the public space and to provide investors with accurate and up-to-date information on those activities. However, as far back as 2007, a discussion on the validity of the adopted solutions began, pointing to the fact that the decrease in information asymmetry, which was favorable for investors, contributed to an increase in short-termism, which was unfavorable for enterprises.

According to Calcagno and Heider (2007), short-termism also proved to be unprofitable for investors, as it makes the stock price less informative about management performance and weakens market-based incentives. Net benefits to economies began to decline as companies focused on short-term goals rather than pursuing long-term strategies that are aligned with the long-term development goals of the national economies. As a result, the EU formally lifted the requirement for public companies to publish quarterly reports in 2014 (European Parliament and of the Council 2013), leaving the Member States a choice as to the solutions applied in this area. In 2018, the EU adopted Action Plan: Financing Sustainable Growth (European Commission 2018), which considered short-termism harmful and recommended its elimination.

The impact of short-term reporting on the functioning of public companies (vide Cheng et al. (2005)) is currently being discussed in scientific and business circles. This article is a part of this discussion. The aim of the article is to determine whether the European companies experience negative effects of short-termism, precisely, whether public companies that prepare quarterly reports, and which focus mainly on achieving the short-term goals of stock exchange investors, are seeing a decline in their market value in the long term. In order to achieve the goal the empirical research will be conducted whether the consistency of the quarterly reporting by public companies domiciled in selected EU member states is connected with buy-and-hold abnormal returns (BHAR). Thus, the authors want to answer whether public companies that prepare quarterly reports, and which focus mainly on achieving the short-term goals of stock exchange investors, are seeing a decline in their market value in the long term. According to studies that promote long-termism, low long-term rates of return of companies that implement a quarterly reporting strategy should be a natural consequence of the actions of management boards of companies that focus mainly on achieving short-term (quarterly) profits, not on achieving long-term financial goals and strategies. That would result in a decline in market value in the long run. The research hypothesis in the article is as follows: there is a negative relationship between regularly quarterly reporting in the public companies domiciled in EU member states and long-term rates of return on the company’s shares.

The direct reason for which we undertook our study was a lack of research in the literature on the role of short-termism as a concept to advance the knowledge of the theory and practice of sustainable finance. The conclusions of our research are both theoretical and applicative in character. In the theoretical aspect, they are part of expanding knowledge in the area of finance (especially corporate finance), in the applicative aspect they allow to state that short-termism is difficult to consider as the feature of financial markets that negatively affects the long-term value of public enterprises and, consequently, EU activities aimed at fighting the negative effects of short-termism seems to be an artificial problem compared to other challenges related to sustainable finance.

2. Sustainable Development, Sustainable Finance, and Short-Termism

2.1. The Concepts of Sustainable Development and Sustainable Finance

The idea of sustainable development appeared in the world economy at the turn of the 1980s and 1990s as a response to the negative effects of the extensive economic development model that was contributing to the degradation of the natural environment (Ionescu 2020). It was pointed out that natural resources are not only exhaustible (crude oil, coal), but they also have a limited regenerative capacity (water, air). The progressive impoverishment and degradation of the natural environment may, therefore, lead to an imbalance of the ecosystem and the loss of its ability to self-regenerate. In 1987, the definition of the term “sustainable development” was formulated, according to which it is a development that enables the current needs of societies to be met without limiting this possibility for future generations (World Commission on Environment and Development 1987). With the passage of time, the concept of sustainable development has evolved, and it has been extended to the aforementioned ESG factors. Sustainable development has been recognized as a complementary process that covers more than just strictly environmental factors.

In September 2015, in its “2030 Agenda for Sustainable Development”, the United Nations laid down 17 Sustainable Development Goals (SDGs) to guide international action on economic, social, and environmental targets (United Nations 2015). One of them (goal 8: Decent Work and Economic Growth) refers to macroeconomic issues, but it does not refer directly to finance and the financial system. Analyzing the SDGs leads to the conclusion that the financial system per se was not identified as crucial to achieving the set goals. Therefore, it should be explicitly assumed that it was considered a complement to a sustainable economy. This approach not only contributed to the marginalization of finances in the process of restructuring economies towards sustainable development, but it also proved to be wrong2. Since the amount of money necessary to finance the reconstruction process significantly exceeded the capacity of the public sector3, it became necessary to mobilize private capital via financial markets. This was one of the reasons why the European Union adopted the Action Plan on Building a Capital Markets Union (European Commission 2015), in which the sustainable development goals have become one of the priorities: “It is a prominent building block of the renewed Capital Markets Union (CMU) 2.0 project to unlock public and private investments to support the transition towards a low-carbon, circular and resource-efficient economy.” (Lannoo and Thomadakis 2020).

The concept of sustainable development is relatively coherently defined; sustainable finance is not. Experts from the High-Level Expert Group on Sustainable Finance (EU) indicate that sustainable finance is about two imperatives (Final Report 2018, p. 6): (1) improving the contribution of finance to sustainable and inclusive growth, as well as the mitigation of climate change; (2) strengthening financial stability by incorporating environmental, social, and governance factors into investment decision-making. And further—sustainable finance means a commitment to the longer term, as well as patience and trust in the value of investments that need time for their value to materialize (Final Report 2018, p. 9).

The Expert Panel on Sustainable Finance defines sustainable finance as finance that comprises capital flows, risk management activities, and financial processes that assimilate ES factors as a means of promoting sustainable economic growth and the long-term stability of the financial system (Final Report of the Expert Panel on Sustainable Finance 2019, p. 2). Some definitions more closely reflect the broad meaning of the concept and link it to the functioning of enterprises and financial markets. Such an approach is seen in the World Bank study, in which sustainable finance is understood as a strong commitment from owners and managers to make sustainability considerations a primary component of business strategy. It incorporates sustainability strategies into the process to allocate resources—both the firms’ own capital and intermediated resources—in support of creating new sustainable business lines, fostering the growth of existing ones, and moving away from activities not aligned with sustainability (World Bank Group Initiative 2017, p. 11).

Summarizing the different approaches, in a broad sense, the concept of “sustainable finance” mainly refers to strengthening financial stability in the economy by considering ESG factors and preferring long-term investments in the decision-making process on the financial markets. In the narrow sense, it refers to reallocating funds for low-carbon investments that positively affect the environment. The phenomenon of short-termism, which is examined in this article, is part of a broader concept.

Following the adoption of the above-mentioned plan to build a capital markets union, Action Plan: Financing Sustainable Growth (European Commission 2018) was created, which focused on implementing three goals: reorienting capital flows towards sustainable investment to achieve sustainable and inclusive growth; managing financial risks that stem from climate change, resource depletion, environmental degradation, and social issues; and fostering transparency and long-termism in financial and economic activity.

For our research, the key objective is the third one, which includes two more specific objectives: strengthening sustainability disclosure and accounting rule-making, and fostering sustainable corporate governance and attenuating short-termism in capital markets. In this article, we focus on the consequences of short-termism for the long-term operation of public companies in the context of value creation, including, in particular, their valuation by the capital markets. The short-term nature, which is increasingly present in contemporary financial markets, is inconsistent with the direction of changes taking place in domestic economies that implement sustainable, inclusive economy solutions.

2.2. Short-Termism Concept and Its Effect on the Capital Market

The ongoing process of the globalization of the financial markets (Lane and Milesi-Ferretti 2008; Carp 2014; Broner and Ventura 2016) has led to a break in the relationship between the levels of domestic investment and savings (Feldstein and Horioka 1980; Sachsida and Abi-Ramia Caetano 2000). As a result of the liberalization of financial flows, capital moves among countries, searching for investments with the highest rates of return. The availability of companies’ short-term financial results, resulting from the shorter reporting period, is conducive to the pressure exerted by short-term investors on their management boards (Bhojraj and Libby [2005] 2015). Companies begin to focus more on the short-term meeting of investors’ expectations than on long-term development prospects, e.g., they abandon long-term pro-development investments (Ladika and Sautner 2019). Short-termism results in insufficient attention being paid to a firm or an institution’s strategy, fundamentals, and long-term value creation (EY Poland Report 2014). It is a suboptimal state that prevents companies from fully using their potential in the long term or achieving sustainable development goals.

Such an approach adversely changes the way enterprises operate and negatively affects the economy, which aims to maximize the welfare of the whole of society, not a group of stakeholders. According to Rappaport (2005), there is no greater impediment to good corporate governance, long-term value creation, and stock market allocative efficiency than earnings obsession. If we assume that, as a result of short-term corporate policy related to short-term reporting, the value of the company decreases in the long term (which is the subject of our study), it can be concluded that the pressure from investors has not only a negative effect on the company, but it also harms the investors themselves. This is another short-termism paradox.

As Jackson and Petraki argue, “short-termism is not an isolated phenomenon. Rather it reflects the complex interactions between the incentives and orientations of different stakeholders” (Jackson and Petraki 2011a, p. 217). In particular, we should point out many complex interactions and relationships between managers and shareholders. Therefore, short-termism should be considered in the context of agency theory (Gryglewicz et al. 2020) regarding the diverse goals of the agents and principals that lead to the agency conflict between them.

This is also the view of Sappideen, who claims that short-termism should be seen as “the result of structural changes brought about by agency theory based managerial compensation”. As a reason for short-termism, he indicates endogenous and exogenous factors such as short-term managerial employment contracts, stock-based compensation, and high-risk investment implemented in a company to achieve high short-term earnings, as well as the market pressure to deliver high stock price (Sappideen 2011, p. 412).

Opinions on whether short-termism is a consequence of market pressure (an exogenous factor) or results from actions taken by the company’s management board, whose remuneration is related to the financial results achieved (an endogenous factor), are divided. The effects of managers’ myopic decisions are indicated by Shleifer and Vishny (1990), Laverty (2004), Edmans et al. (2013), and Marinovic and Varas (2019), while the consequences of market pressure (investors) are given by Barton et al. (2016) and Hackbarth et al. (2018). Regardless of which opinion is closer to the actual state of play, there is no doubt that the key is to answer the question: Does short-termism, perceived in our article through the prism of the requirement for public companies to publish quarterly reports, contribute to the decline in their value in the long-term period? The negative assessment of short-termism should result from the negative effects it brings to companies, and, consequently, to economies, and not only from the shortening of the average period of financial commitment of most stock exchange investors, which is now becoming an inherent feature of financial markets.

According to the economic literature, the problem of short-termism and its effect on firm market value leads to the focus of several channels, i.e., information asymmetry, cost of capital, earnings timeliness, liquidity, compliance cost, and managers’ business decisions (myopic investment and real activities manipulation).

Under agency theory (Jensen and Meckling 1976), the principle-agent conflict and information asymmetry should be minimized by higher disclosure frequency, in particular, when capital market pressure is high. Interim financial reporting (e.g., quarterly reporting) provides more timely information, increases transparency, and reduces the information asymmetry (Cuijpers and Peek 2010). Using a sample of the US firms that underwent voluntary and mandatory changes from annual to semiannual between 1951 and 1973, Fu et al. (2012) confirmed a significant correlation between shorter reporting intervals, lower information asymmetry, and a lower cost of capital. In the study by Butler et al. (2007), the voluntary semi-annual and quarterly financial statements are related to an improvement in earnings timeliness (firms that are required to report quarterly do not experience this increase).

A higher disclosure frequency might improve a firm’s information environment and increase liquidity on the capital market (Glosten and Milgrom 1985). On the other hand, liquidity is connected with information transparency (Amihud and Mendelson 1986), which influences cash flow and the cost of capital (components of the company’s market value) (Lang and Maffett 2010). As a result, transparency helps market participants better monitor managers’ decisions and better assess a firm’s performance (Stulz 2009). Additionally, McNichols and Manegold (1983) documented that more frequent reporting is associated with lower surprise in annual earnings announcements, which have a significant effect on real investment decisions (Badertscher et al. 2013).

Meanwhile, Gigler et al. (2014) openly stated that higher reporting frequency, principally mandatory quarterly reporting, is associated with short-term management behavior and increases the focusing one’s attention on short-term earnings. The high market pressure created by higher disclosure frequency induces managers to select investment projects, which are not related to a long-term perspective and long-term company’s market value.

Consistent with these arguments, Kanodia and Lee (1998) evidenced that more frequent reporting increases the probability of managerial short-termism and disciplines managers’ investment choices. In the survey of more than 400 CFOs by Graham et al. (2005), almost 80 percent of managers would decrease R&D expenses, and more than 55 percent would delay starting a new project to meet quarterly earnings targets. Thus, Kraft et al. (2018) documented that higher reporting frequency is associated with a massive decline in investments. Another adverse effect of short-termism on the capital market is managers’ tendency for real earnings management. Ernstberger et al. (2017), who examined European companies, reported that firms increasingly use real activities manipulation (RAM) to meet earnings targets after they are required to present quarterly statements.

Among policymakers and regulators, no consensus exists on whether quarterly reporting is desirable from a regulatory perspective. Despite the numerous efforts by US and EU regulators to address the problem of voluntary and mandatory quarterly reporting, it has not been eliminated. While accounting standards have many arguments that timeliness is a fundamental characteristic of practical financial reporting, there is a discussion about the problem of voluntary and mandatory quarterly reporting.

In the US, quarterly reporting has been a central component of the US equity markets since 1970. The requirement to disclose quarterly financial information is consistently maintained, but there have been several arguments recently regarding loosening these restrictions. In 2018, as suggested by President Donald Trump, the US Securities and Exchange Commission (SEC) commented on the cost and benefits of a reduction in reporting frequency. Due to the many arguments against focusing on the short-term, the SEC is considering loosening quarterly reporting requirements for some firms and mandating only semiannual reports. If US corporations report semiannually, investors will have fewer open resources to analyze their performance, increasing the difficulty for them to make investment decisions (Securities and Exchange Commission (SEC) 2018). On the other hand, corporations need time to get used to filing semiannual reports, and they would also like to reveal their financials to show their growth potential and strengthen the confidence of stockholders (Zhou 2018).

In contrast to the US, the EU has historically presented an unstable policy regarding the obligation for public companies to publish quarterly reports. As a result of the debate on the initial “Transparency Directive” in 2004 (implementation date: 2007), public companies were obliged to publish quarterly reports (Directive 2004/109/EC). However, the requirement to disclose quarterly financial information was subsequently abolished in 2013 (Directive 2013/50/EU). Although the EU mandates only annual and semiannual financial reporting, some EU-members retained quarterly reporting obligations for public companies listed on the main markets. Additionally, many firms voluntarily report quarterly financial information. As a consequence, there is a significant variation in companies’ reporting choices within the EU.

3. Materials and Methods

3.1. The Institutional Setting—Quarterly Reporting in the EU

To provide evidence on the consequences of short-termism for the capital market, we used the institutional setting of the EU. It constitutes a suitable and relevant laboratory to test for 2 reasons. Firstly, accounting principles, reporting regulations, financial disclosure, and reporting frequency are strongly harmonized in the EU. This setting allows for a comparative study across the EU countries, principally on whether abolishing the quarterly reporting requirement resulted in companies withdrawing from publishing quarterly reports. Secondly, for historical reasons, the EU countries have different national reporting regulations and reporting frequency regimes. The obligation for firms to publish quarterly reports stems from the national regulatory authorities, and it usually concerns public companies listed on the main markets. This diversity makes it possible to isolate the effect of interim reporting frequency on a company’s market value.

Table 1 and Table 2 present data on the specific requirements in each EU country before and after the “Transparency Directive” implemented in 2007 (Directive 2004/109/EC), under which public companies were obliged to publish quarterly reports. For most EU-15 members, this requirement has been respected partially. For example, in Greece, Finland, Portugal, and Sweden, the national regulatory authorities require public companies to publish full quarterly financial statements. In Germany and Austria, public companies listed in selected segments (“Prime Standard” in Germany and “Prime Market” in Austria) are also obliged to publish full quarterly financial information (Austria abolished this requirement for the “Prime Market” only in 2019). The transposition of EU regulations into national systems in the new EU member states (which joined in 2004 and later) was heterogeneous, too, and some countries (Bulgaria, Croatia, and Poland) retained reporting obligations for companies listed on the main markets.

In order to conduct the study, we created a research sample consisting of companies listed on European exchanges, focusing only on those stock markets that are regulated by the European Union. The largest and most liquid companies listed on EU-regulated markets were used for 2 reasons. Firstly, according to the corporate governance rules, as well as the International Accounting Standards or national codes of best practice, the largest listed companies are required by many formal rules and laws, in particular, to publish detailed interim reports. Secondly, the costs and benefits of quarterly reporting for market participants are different for small companies compared with larger firms. In particular, voluntary quarterly reporting seems to be costly and unprofitable for small listed companies. The additional benefits of interim reporting frequency for market participants might be more pronounced in the largest and most liquid companies, which are often followed by financial analysts (“buy, hold, and sell” recommendation).

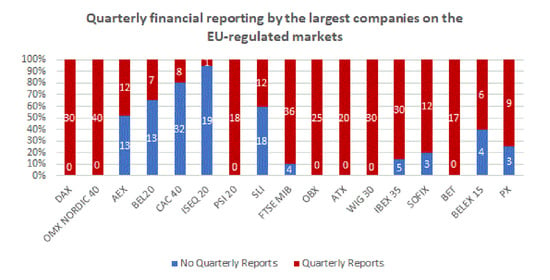

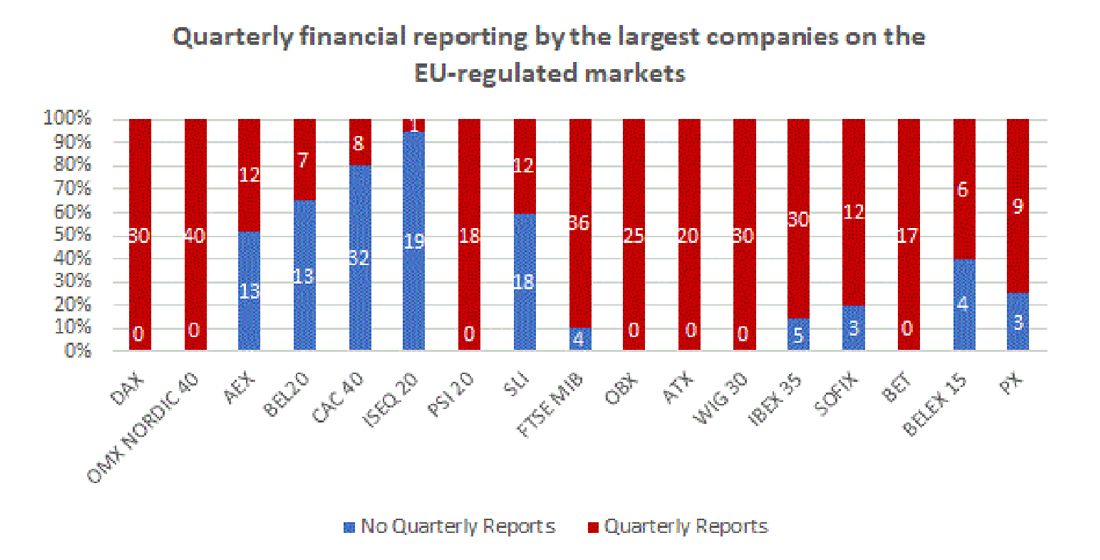

Table 3 gives an overview of the practical publication of quarterly financial statements by the companies listed on 13 selected European regulated markets on 21 May 2020, which we compiled from the websites of individual companies4. A sample of 427 companies from 17 indexes was assembled. The period of analysis spanned 13 years, from 2007 to 2019. This specific period was caused by the “Transparency Directive” implemented in 2007, under which public companies were originally obliged to publish quarterly reports. Additionally, data for earlier years were very limited in most companies.

As followed from national reporting regulations in EU-15 (compare Table 1), in Germany (DAX) and Austria (ATX), all listed companies were obliged to publish full quarterly reports on their websites in each year between 2007 and 2019. In the case of the main markets of Nasdaq Nordic (OMX NORDIC 40), Oslo Bors & Oslo Axess (OBX), and one of the Euronext indices—PSI 20—the practice of quarterly financial reporting was the same too. These results are strongly correlated with quarterly reporting rules presented in the national law. An interesting case is that in 2 markets—Italy and Spain—where quarterly reporting is not obligatory, ca. 90 percent of companies presented quarterly statements on their websites in any given year.

Based on the research results in the new EU member states (which joined in 2004 and later), it can be stated that some observations are consistent with previous findings regarding quarterly reporting rules in individual countries (compare Table 2). For example, in the stock exchange located in Poland, all companies from the WIG 30 index published quarterly financial information. By contrast, for Bulgarian companies, the mandatory quarterly reporting was not fully respected. Additionally, the results did not correspond to the rules for listed companies on Prague’s “Prime Market”. A very unexpected case is the Bucharest Stock Exchange. Despite the lack of obligation to report quarterly, all 17 Romanian companies presented quarterly financial statements. Thus, the diversity of mandatory and voluntary quarterly reporting on the EU-regulated markets is related to the lack of EU policy and national regulations in individual member states. This EU setting allows us to examine the real capital market effects of short-termism and to provide evidence on how this effect depends on different institutional settings.

3.2. Research Sample—Characteristics

In terms of the main empirical research, which is aimed at finding answers to the question regarding the influence of short-termism on the market value of European companies, both from the EU-15 and new EU member states, we focused only on those market indices for which the share of companies regularly reporting quarterly results represents no less than 75% of total companies in the index portfolio (see Table 3). This was done so that the research sample would be representative and so that the conclusions would not be distorted by one-time or short-term disclosures of quarterly reports. Therefore, our research sample included 11 European stock indices (i.e., DAX, OMX NORDIC 40, PSI 20, FTSE MIB, OBX, ATX, IBEX 35, WIG 30, SOFIX, BET, and PX).

In order to conduct a long-term study and to manage the analysis of the impact of quarterly reporting on the long-term rates of return, we decided to limit the research sample to companies included in the indices portfolios for which we were able to obtain financial data for at least 5 subsequent years. As a result, our research sample consisted of 227 European listed companies, which required us to examine 10,275 quarterly financial reports. A detailed specification of the research sample is presented in Table 4.

The data for the study were obtained from the Thompson Reuters Eikon database. However, in the case of deficiencies, data were hand-collected. Furthermore, the closing rate of the WIG30 index before 2013 was retrieved from the financial portal Stooq.pl. The main calculations were performed using the Statistica 13.3 package.

3.3. Research Methods

Our research was conducted taking into consideration 2 areas. First, we examined the impact of short-termism on the market value of European companies broken down into the old member states of the European Union (i.e., those belonging to the EU-15) and the new ones (i.e., those that joined in 2004 and later). Then, we examined whether the regular disclosure of quarterly financial reports affected a company’s market value depending on the capital market on which it was listed. For this purpose, our study considered selected European market indices.

In order to achieve the research purpose, we employed the methodology of buy-and-hold abnormal returns. We assumed that a stock investor purchases shares at the closing price on the last trading day of the quarter preceding the first quarter in which the company presents its quarterly financial report and then holds the shares for subsequent periods (quarters). In order to eliminate the impact of the stock market, we adjusted the obtained results by the rate of return on the market portfolio using selected market indices on a given trading day as a benchmark. The long-term stock returns resulting from the adopted investment strategy and market-adjusted model are given by the following formulas:

where is the buy-and-hold return on shares the of i-th company reporting quarterly in period T; denotes the rate of return on shares of the i-th company on the t-th day; is the buy-and-hold return on the stock index corresponding to the i-th company during the observation period T; denotes the rate of return on the stock index on the t-th day.

The market-adjusted model refers to the abnormal changes in the market share price of companies that report their financial results quarterly. The rates of return that result from the buy-and-hold investment strategy are given as follows (Barber and Lyon 1997, p. 344; Badshah et al. 2019, p. 3):

where indicates the buy-and-hold abnormal return on shares of the i-th company that reports the financial results quarterly in period T; other markings as above.

In accordance with the aim of our study and in order to find the answer to the question of whether short-termism affects the market value of companies listed on the European stock markets, we studied the existence of the relationship between the length of the quarterly reporting of companies in the portfolios of European stock indices and the long-term stock returns. To verify our hypothesis, which states that the longer a company follows the policy of regular quarterly reporting, the lower the long-term rates of return on its shares, we estimated the Ordinary Least Squares (OLS) regression models presented by the following formula:

where QUARTERT,i is the number of quarters in period T in which the i-th company follows the policy of regular quarterly reporting. Furthermore, 6 control variables were considered as determinants of buy-and-hold abnormal return, i.e., ΔROAT,i denotes the growth rate of return on total assets of the i-th company in period T, ΔROET,i refers to the growth rate of return on equity of the i-th company in period T, Δ(D/E)T,i is the growth rate of the debt-to-equity ratio of the i-th company in period T, Δ(P/E)T,i stands for the growth rate of the price-to-earnings ratio of the i-th company in period T, Δln(ASSETS)T,i stands for the growth rate of the i-th company’s size in period T measured as a natural logarithm of total assets, and Δ(MV/BV) T,i means the growth rate of the market-to-book ratio of the i-th company in period T; other markings as above.

4. Results

4.1. Quarterly Reporting and the Market Value of European Companies—The Case of the EU-15 and the New Member States of the EU

The results of research concerning the impact of the length of the company’s quarterly reporting policy on the long-term rates of return, carried out using the multiple regression model, divided into the EU-15 and the new EU member states, are different in each of these two analyzed groups. In the case of the EU-15, the results of the regression model estimation indicate a positive and statistically significant impact of the number of quarters with the regular disclosure of quarterly reports at the level of rates of return related to implementing the buy-and-hold investment strategy. The parameter value for the QUARTER independent variable is 0.019 and is statistically significant at the significance level α = 0.01. Therefore, for the EU-15, it should be noted that by extending regular quarterly reporting by one quarter, the value of buy-and-hold abnormal returns increases by 0.019 percentage points (see Table 5).

Furthermore, the study of the EU-15 shows that the value of the β parameter for the control variables is statistically significant in most of the analyzed cases. An increase in the long-term buy-and-hold abnormal returns occurs as a result of an increase in the growth rate of return on equity (β = 0.025), the growth rate of the company’s size (β = 0.159), and the growth rate of the market-to-book ratio (β = 0.638). On the other hand, a decrease in BHAR is observed with an increase in the growth rate of both the return on total assets (β = −0.009) and the debt-to-equity ratio (β = −0.026). However, it should be pointed out that in the analyzed model, the coefficient of determination is low, which means that only 15.5% of the total variability of the dependent variable is explained by the independent variables.

In turn, in the group that includes the new member states, the research results concerning the impact of the length of quarterly reporting on the long-term rates of return are different. The estimation results of multiple regression model indicate that for the new EU member states, the parameter value for the variable specifying the number of quarters in period T is negative, but statistically insignificant at the adopted significance level (β = −0.017).

The analysis of the model’s control variables showed that the parameter values for two of them are statistically significant at the significance level α = 0.01. In the new EU member states, the buy-and-hold abnormal returns decrease along with an increase in the growth rate of return on equity increases (β = −1.765), and they increase when the company’s growth rate increases (β = 6.661). As with estimating the parameters of the model developed for the EU-15, in this model, the coefficient of determination is also low (R2 = 26.8% and R2 adj. = 26.4%).

Considering the above, the empirical research on the impact of the length of the company’s quarterly reporting policy on the long-term rates of return, broken down into the EU-15 and the new member states, does not allow us to confirm the research hypothesis. There are differences between the “old” and “new” EU states observed in how regular quarterly reporting impacts the shaping of companies’ market value—as well as the low coefficient of determination values obtained in both models. This made us take a closer look at the research problem and undertake in-depth and more detailed empirical research on the impact of disclosing quarterly financial reports on buy-and-hold abnormal returns, considering the individual capital markets of the EU member states.

4.2. The Disclosure of Quarterly Financial Reports and Long-Term Rates of Return—Evidence from European Stock Exchanges

The empirical research concerning the impact of quarterly reporting policy on the market value of companies on individual European stock exchanges allows us to conclude that on the stock markets of the “old” EU member states, the length of the quarterly reporting period has a positive impact on the long-term rates of return. For the majority of the EU-15 stock exchanges, the parameter value for the QUARTER variable is positive and statistically significant at the significance level α = 0.01. Therefore, along with the extension of the disclosure period of quarterly financial reports on stock exchanges such as the pan-regional Nordic Stock Exchange, Euronext Lisbon, the Italian Exchange, the Oslo Stock Exchange, the Vienna Stock Exchange, and the Madrid Stock Exchange, the growth of buy-and-hold abnormal returns is observed (the value of the β parameter is 0.019, 0.021, 0.024, 0.005, 0.007, and 0.006, respectively). The only exception is the Frankfurt Stock Exchange. In the case of the DAX index, the estimated parameter value for the QUARTER variable is negative (β = −0.001), but the achieved result is not statistically significant (see Table 6).

Furthermore, taking into account the control variables of our regression model, it should be noted that for all of the analyzed EU-15 stock exchanges, an increase in the growth rate of the company’s size and the growth rate of the market-to-book ratio results in an increase in buy-and-hold abnormal returns (all values of the β parameter for these variables are positive and statistically significant at the significance level α = 0.01). The impact of the other control variables on the dependent variable differs, depending on the stock exchange. However, it is worth paying attention to the variables that show the growth rate of return on equity, as well as the growth rate of the debt-to-equity ratio. For the first indicated variable, the values of the β parameter are positive in all models built for the EU-15 stock exchanges. Thus, on these capital markets, an increase in the growth rate of return on equity results in an increase in buy-and-hold abnormal returns. However, it should be emphasized that the results are not always statistically significant. For the second of the indicated variables (the growth rate of debt-to-equity ratio), the value of the β parameter is negative and statistically significant on most of the EU-15 stock exchanges. Thus, an increase in the growth rate of the debt-to-equity ratio results in a decline in long-term rates of returns.

Based on the results, it should be stated that the models we built for the EU-15 stock exchanges explain from approx. 40% to 84% of the variability of the dependent variable, depending on the model (details are presented in Table 6). Moreover, the value of the F statistic and its corresponding p test probability level confirm a statistical significance of the estimated models.

In turn, in the case of the stock indices of the “new” EU member states, the research results are not homogeneous, which may be related to their high heterogeneity, degree of market development, as well as different information efficiency. Our study confirms the research hypothesis only for the Bucharest Stock Exchange. The analysis carried out for the BET index shows that as the period of quarterly financial reporting lengthens, a decline in long-term rates of return is observed. For this stock exchange index, the value of the parameter for the QUARTER variable was equal to −0.054 and was statistically significant at the level of significance α = 0.01. For the other indices, i.e., the WIG30 index, the SOFIX index, and the PX index, the test results are different. The value of the parameter for this independent variable that shows the length of quarterly reporting is positive but not statistically significant for the Warsaw Stock Exchange (β = 0.004), while for the Bulgarian Stock Exchange, it is positive and statistically significant at the adopted significance level (β = 0.016), whereas for the Prague Stock Exchange it is negative but not statistically significant (β = −0.002).

Referring to the control variables, it should be noted that their impact on the buy-and-hold abnormal return variable varies depending on the stock exchange. Therefore, the research results cannot be generalized, and it is impossible to clearly indicate the positive or negative impact of the control variables on the changes in the long-term rates of return on all the stock exchanges of the “new” EU member states that were studied (see Table 6).

It is worth emphasizing that the models developed for different stock exchanges of the “new” EU member states explain the variability of the dependent variable to a different extent. For the SOFIX index, it is approximately 76%, the WIG30, approximately 69%, the PX index, approximately 34%, while for the BET index, it is approximately 14%. The value of the F statistic and its corresponding p-value confirm the statistical significance of the estimated models.

5. Conclusions

The purpose of our research was to determine whether, in public companies that pursue a policy of regular quarterly reporting, a decline in the market value of these companies is observed in the long-term research perspective.

As a result of the empirical research conducted on selected capital markets of the European Union Member States, the existence of such a dependence has not been proven. Thus, the research hypothesis adopted in the article, i.e., there is a negative relationship between regularly quarterly reporting and long-term rates of return on the company’s shares, has not been positively verified. Thus, it cannot be concluded that an increase in reporting frequency by public companies contributes to a decline in their long-term value.

At the same time, it should be emphasized that the establishment of regulations at the EU level (i.e., the adoption of the quarterly reporting requirement in 2004, and then the abolition of this obligation in 2014) did not result in the full transposition of the adopted solutions into the legal systems of EU Member States. Consequently, the de jure situation concerning this requirement in individual countries differs significantly from the de facto one. It constitutes a significant obstacle in conducting research. In several countries of the EU-15 (i.e., the “old” countries), the observed practice of quarterly financial reporting of public companies was strictly harmonized with national regulations in this regard (e.g., DAX, ATX, OMX NORDIC 40, OBX, or PSI-20 companies). On the Italian and Spanish markets, where quarterly reporting is not legally required, most companies presented this information voluntarily. There are also ambiguous reporting practices in the “new” EU Member States. While in Poland and the Czech Republic, for example, public companies presented quarterly reports in accordance with national regulations, in Bulgaria, they did not. In contrast, all Romanian companies surveyed published quarterly financial information despite the lack of an obligation to do so.

Another obstacle in conducting the research was the significant heterogeneity of financial markets in EU countries. We researched two groups of countries—the “old” EU countries (Germany, Sweden, Denmark, Finland, Portugal, Italy, Austria, Spain, and additionally Norway) and the “new” EU countries (Poland, Bulgaria, Romania, Czech Republic). We applied this procedure deliberately, assuming that both groups’ financial markets are characterized by significant differences, which are mainly a derivative of different conditions for their development. The new EU countries that gained membership after 2004 previously belonged to the Eastern Bloc, with a centrally controlled economy. System changes and the building of a market economy (including the capital market) began only in the 1990s. As a result, the level of development of the financial markets of “old” and “new” countries, both in terms of quality and quantity, is significantly different, which allows for a natural division of these financial markets into developed (“old” countries) and developing (“new” countries). The consequences of these differences were reflected in the results of our research.

In the “old” EU countries, quarterly reporting by public companies was positively related to their long-term market value. If we consider the requirement of quarterly reporting as a proxy for reducing the level of information asymmetry on the financial market, it can be concluded that on the developed financial markets, we observed a positive relationship—reduction of information asymmetry has a positive effect on the long-term value of public companies. Therefore, there is no justification for eliminating quarterly reporting using the argument that such reporting promotes the negative consequences of short-termism. In a certain sense, our results are consistent with the findings that were done by proponents of short-termism, which argued that interim reports provide more timely information, increase transparency and liquidity on the capital market, reduce the information asymmetry and cost of capital, and help market participants better monitor managers’ decisions and better assess a firm’s performance (Glosten and Milgrom 1985; Stulz 2009; Cuijpers and Peek 2010; Fu et al. 2012).

In the case of the “new” EU member states, submitting quarterly reports by public companies did not have a statistically significant relationship with their long-term value. A few previous empirical studies also failed to find a relationship between higher reporting frequency and benefits for market participants. Van Buskirk (2012) established a negative association between reporting frequency and information asymmetry. Additionally, there may be more powerful adverse effects on the capital market if investors overreact to timelier financial information (Thomas and Zhang 2008). According to some authors, higher disclosure frequency might harm investors due to compliance cost and the short-term perspective of managers’ business decisions (cf. (Gigler et al. 2014; Ernstberger et al. 2017; Kajuter et al. 2018; Kraft et al. 2018)). If firms are required to disclose interim financial statements (in Q1 and Q3), managers will shift numerous resources to the preparation, review, and auditing of quarterly reports.

It is worth emphasizing that the capital markets (or more precisely, the stock markets) of these “new” EU countries diverge from the developed markets in terms of their quantitative (number of companies, capitalization, and turnover) and qualitative (number of financial intermediaries, available financial products) development. If quarterly reporting does not affect the long-term value of public companies listed in these markets, there is no justification for its liquidation. At the early stage of development, capital markets even require such reporting due to the relatively low level of investor confidence in the reliability and completeness of the information presented by companies. In developing markets, reducing information asymmetry seems to be one of the key elements that influence market development.

6. Recommendations and Limitations

The research goal of this article was formulated due to an eagerness to analyze a new and empirically unrecognized research area, and to fill the research gap in the area of broadly understood sustainable finance. The existence of the dependence between regular quarterly reporting and long-term market value of companies would confirm the existence of negative consequences of short-termism on the capital markets, understood as the focus of public companies to implement short-term goals, in particular, short-term results regularly presented in their quarterly reports.

Contrary to our assumptions, the decrease in the asymmetry of information in the investor-company relationship did not contribute to the increase in the asymmetry of benefits of these two groups. On the contrary—there was an increase in the benefits of both investors and enterprises. The results of our analysis, therefore, open a new research field and raise a number of important questions, including those regarding the validity of implementing short-termism, understood as a market-forced (i.e., investors) change of corporate strategy in order to achieve quick profits at the expense of achieving long-term goals.

The results of our study are based on a limited sample, which includes 11 European stock indices, so they should not be used as a basis for general reflections and conclusions about all EU companies, EU members, or EU countries. However, they can unquestionably be useful as a foothold for innovative theoretical and empirical research on the influence of short-termism on market value of companies. A wider use of quantitative research and, for instance, qualitative methods, would certainly help better assess the usefulness of quarterly reporting for designing effective EU plans, which are connected with short-termism and sustainable finance.

It is also worth adding that the impact of short-termism on the functioning of public companies is a subject of debate not only in the EU but also in the USA, where most investment funds in the economy are transmitted via the capital market. However, the main thread of the discussions on the American market is different from those conducted in the EU, as it concerns not so much the legitimacy of publishing quarterly reports by public companies as projections. The problem arises from investors putting pressure on companies to then reflect their published financial forecasts in the actual financial results achieved5. This situation does not have much to do with the publication of financial results achieved by companies in the last quarter, which are only informative for investors.

As previously indicated, short-termism should be negatively assessed due to the negative effects it brings to companies, and consequently to economies, and not as a derivative of the shortening of the average period of financial involvement of stock exchange investors. Our research does not provide clear grounds to support the thesis that short-termism has a negative impact on the company’s long-term market value, and thus on the management board’s long-term investment decisions that affect the creation of this value. Thus, there is no reason to indicate short-termism as a feature of capital markets, which negatively affects companies’ ability to undertake long-term investments necessary from the point of view of sustainable development. In this situation, it is worth considering whether short-termism, which is present on contemporary capital markets, is the main reason for the insufficient value of proenvironmental investments undertaken by companies, or whether the sources of this shortage should be sought elsewhere.

The conclusions drawn from our research allow for the formulation of a clear recommendation addressed primarily to the European Commission: short-termism perceived as a requirement for public companies to publish quarterly reports does not seem to have a negative impact on the operations and valuation of public companies. Contrary to the concerns formulated in the reports and the arguments cited above in the article, the publication of short-term reports by public companies does not mean that these companies focus on achieving short-term goals, which would have a negative impact on their long-term value. For this reason, it is worth considering giving up the fight against short-termism as one of those features of the financial market that negatively affects sustainable development and sustainable finance. In consequence, personal and financial resources of the EU can be shifted to other, much more important activities from the point of view of sustainable finance and the future of the European sustainable economy.

Author Contributions

Conceptualization, M.J., A.P.-B. and A.S.; methodology, A.P.-B.; software, A.P.-B.; validation, M.J., A.P.-B. and A.S.; formal analysis, M.J., A.P.-B. and A.S.; investigation, A.P.-B.; resources, A.S.; data curation, A.P.-B. and A.S.; writing—original draft preparation M.J., A.P.-B. and A.S.; writing—review and editing, M.J., A.P.-B. and A.S.; visualization, A.S.; supervision, M.J.; project administration, M.J.; funding acquisition, M.J. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abudy, Menachen, and Efrat Shust. 2020. What Happens to Trading Volume When the Regulator Bans Voluntary Disclosure? European Accounting Review 29: 555–80. [Google Scholar] [CrossRef]

- Amihud, Yakov, and Haim Mendelson. 1986. Asset pricing and the bid-ask spread. Journal of Financial Economics 17: 223–49. [Google Scholar] [CrossRef]

- Atherton, Alison, James Lewis, and Roel Plant. 2007. Causes of short-termism in the finance sector. In Discussion Paper Institute for Sustainable Futures. Ultimo: University of Technology Sidney, p. 2. [Google Scholar]

- Badertscher, Brad, Nemit Shroff, and Hal D. White. 2013. Externalities of public firm presence: Evidence from private firms’ investment decisions. Journal of Financial Economics 109: 682–706. [Google Scholar] [CrossRef] [Green Version]

- Badshah, Ihsan, Hardjo Koerniadi, and James Kolari. 2019. Testing the information-based trading hypothesis in the option market: Evidence from share repurchases. Journal of Risk and Financial Management 12: 1–11. [Google Scholar] [CrossRef] [Green Version]

- Barber, Brad M., and John D. Lyon. 1997. Detecting long-run abnormal stock returns: The empirical power and specification of test statistics. Journal of Financial Economics 43: 341–72. [Google Scholar] [CrossRef] [Green Version]

- Barton, Dominic, Jonathan Bailey, and Joshua Zoffer. 2016. Rising to the Challenge of Short-Termism. Report FCLT Global. Available online: https://www.fcltglobal.org/wp-content/uploads/fclt-global-rising-to-the-challenge.pdf (accessed on 29 September 2020).

- Bhojraj, Sanjeev, and Robert Libby. 2015. Retraction: Capital market pressure, disclosure frequency-induced earnings/cash flow conflict, and managerial myopia. The Accounting Review 90: 1715. First published 2005. [Google Scholar] [CrossRef]

- Broner, Fernando, and Jaume Ventura. 2016. Rethinking the effects of financial globalization. The Quarterly Journal of Economics 131: 1497–542. [Google Scholar] [CrossRef] [Green Version]

- Butler, Marty, Arthur Kraft, and Ira S. Weiss. 2007. The effect of reporting frequency on the timeliness of earnings: The cases of voluntary and mandatory interim reports. Journal of Accounting and Economics 43: 181–217. [Google Scholar] [CrossRef]

- Calcagno, Riccardo, and Florian Heider. 2007. Market based Compensation, Price Informativeness and Short-Term Trading. Working Paper Series 735; Frankfurt am Main, Germany: European Central Bank, p. 27. [Google Scholar]

- Carp, Lenuţa. 2014. Financial globalization and capital flows volatility effects on economic growth. Procedia Economics and Finance 15: 350–56. [Google Scholar] [CrossRef] [Green Version]

- Cheng, Mei, K. R. Subramanyam, and Yuan Zhang. 2005. Earnings Guidance and Managerial Myopia. Available online: https://ssrn.com/abstract=851545 (accessed on 29 September 2020).

- Cuijpers, Rick, and Erik Peek. 2010. Reporting frequency, information precision and private information acquisition. Journal of Business Finance & Accounting 37: 27–59. [Google Scholar] [CrossRef]

- Edmans, Alex, Vivian W. Fang, and Katharina A. Lewellen. 2013. Equity Vesting and Managerial Myopia. NBER Working Paper No. 19407. Cambridge, MA, USA: NBER, Available online: http://www.nber.org/papers/w19407 (accessed on 29 September 2020).

- Ernstberger, Jürgen, Benedikt Link, Michael Stich, and Oliver Vogler. 2017. The real effects of mandatory quarterly reporting. The Accounting Review 92: 33–60. [Google Scholar] [CrossRef]

- Escrig-Olmedo, Elena, María Jesús Muñoz-Torres, and María Ángeles Fernández-Izquierdo. 2013. Sustainable development and the financial system: Society’s perceptions about socially responsible investing. Business Strategy and the Environment 22: 410–28. [Google Scholar] [CrossRef]

- ESMA. 2019. Report Undue Short-Term Pressure on Corporations. ESMA30-22-762. Paris: ESMA, p. 9. [Google Scholar]

- European Commission. 2015. 30.9.2015 COM(2015) 468 Final Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions Action Plan on Building a Capital Markets Union {SWD(2015) 183 Final} {SWD(2015) 184 Final}. Brussels: European Commission. [Google Scholar]

- European Commission. 2018. 8.3.2018r. COM(2018) 97 Final Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions Action Plan: Financing Sustainable Growth. Brussels: European Commission. [Google Scholar]

- European Commission. 2020. Brussels Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee of the Regions. Sustainable Europe Investment. Plan European Green Deal Investment Plan. 14.1.2020 COM(2020) 21 Final. Brussels: European Commission, p. 4. [Google Scholar]

- European Parliament and of the Council. 2004. On the Harmonisation of Transparency Requirements in Relation to Information about Issuers Whose Securities Are Admitted to Trading on a Regulated Market and Amending Directive 2001/34/EC, Directive 2004/109/EC. December 15. Available online: https://eur-lex.europa.eu/legal-content/GA/TXT/?uri=CELEX:32004L0109 (accessed on 28 September 2020).

- European Parliament and of the Council. 2013. Amending Directive 2004/109/EC of the European Parliament and of the Council on the Harmonisation of Transparency Requirements in Relation to Information about Issuers Whose Securities are Admitted to Trading on a Regulated Market. Directive 2013/50/EU. October 22. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=celex%3A32013L0050 (accessed on 28 September 2020).

- EY Poland Report. 2014. Short-Termism in Business: Causes, Mechanisms and Consequences. p. 7. Available online: https://www.ey.com/Publication/vwLUAssets/EY_Poland_Report/%24FILE/Short-termism_raport_EY.pdf (accessed on 29 September 2020).

- Feldstein, Martin, and Charles Horioka. 1980. Domestic saving and international capital flows. The Economic Journal 90: 314–29. [Google Scholar] [CrossRef]

- Final Report. 2018. Financing a Sustainable European Economy. Brussels: The High-Level Expert Group on Sustainable Finance, the European Commission. [Google Scholar]

- Final Report of the Expert Panel on Sustainable Finance. 2019. Mobilizing Finance for Sustainable Growth. Gatineau: Environment and Climate Change Canada, Public Inquiries Centre, ISBN 978-0-660-30986-6. [Google Scholar]

- Friedman, Henry L., John S. Hughes, and B. Michaeli. 2020. Optimal reporting when additional information might arrive. Journal of Accounting and Economics 69: 1–52. [Google Scholar] [CrossRef]

- Fu, Renhui, Arthur Kraft, and Huai Zhang. 2012. Financial reporting frequency, information asymmetry, and the cost of equity capital. Journal of Accounting and Economics 54: 132–49. [Google Scholar] [CrossRef]

- Gigler, Frank, Chandra Kanodia, Haresh Sapra, and Raghu Venugopalan. 2014. How frequent financial reporting can cause managerial short-termism: An analysis of the costs and benefits of increasing reporting frequency. Journal of Accounting Research 52: 357–87. [Google Scholar] [CrossRef]

- Glosten, Lawrence R., and Paul R. Milgrom. 1985. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics 14: 71–100. [Google Scholar] [CrossRef] [Green Version]

- Goldstein, Itay, and Liyan Yang. 2017. Information disclosure in financial markets. Annual Review of Financial Economics 9: 101–25. [Google Scholar] [CrossRef]

- Graham, John R., Campbell R. Harvey, and Shiva Rajgopal. 2005. The economic implications of corporate financial reporting. Journal of Accounting and Economics 40: 3–73. [Google Scholar] [CrossRef] [Green Version]

- Greenwald, Bruce, Joseph E. Stiglitz, and Andrew Weiss. 1984. Informational imperfections on the capital market and macro-economic fluctuations. The American Economic Review 74: 194–99. [Google Scholar]

- Grossman, Sanford J., and Joseph E. Stiglitz. 1980. On the impossibility of informationally efficient markets. American Economic Review 70: 393–408. [Google Scholar] [CrossRef]

- Gryglewicz, Sebastian, Simon Mayer, and Erwan Morelec. 2020. Agency Conflicts and Short- vs. Long-Termism in Corporate Policies. Journal of Financial Economics 163: 718–42. [Google Scholar] [CrossRef]

- Hackbarth, Dirk, Alejandro Rivera, and Tak-Yuen Wong. 2018. Optimal Short-Termism (29 October 2018). Finance Working Paper No. 546, Asian Finance Association (AsianFA) 2018 Conference. Brussels, Belgium: European Corporate Governance Institute (ECGI). Available online: https://ssrn.com/abstract=3060869 (accessed on 29 September 2020).

- Haldane, Andrew G. 2011. Executive Director, Financial Stability and Richard Davies. The short long. Paper presented at Speech Delivered during 29th Société Universitaire Européene de Recherches Financières Colloquium, Brussels, Belgium, May 11; Available online: https://www.tradinggame.com.au/wp-content/uploads/2011/05/here.pdf (accessed on 29 September 2020).

- Healy, Paul M., and Krishna G. Palepu. 2001. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31: 405–40. [Google Scholar] [CrossRef]

- Hubbard, R. Glenn. 1998. Capital-market imperfections and investment. Journal of Economic Literature 36: 193–225. [Google Scholar]

- Ionescu, Luminița. 2020. Pricing Carbon Pollution: Reducing Emissions or GDP Growth? Economics, Management, and Financial Markets 15: 37–43. [Google Scholar] [CrossRef]

- Jackson, Gregory, and Anastasia Petraki. 2011a. How does corporate governance lead to short-termism? In The Sustainable Company: A New Approach to Corporate Governance. Edited by Sigurt Vitols and Norbert Kluge. Brussels: European Trade Union Institute, pp. 199–226. [Google Scholar]

- Jackson, Gregory, and Anastasia Petraki. 2011b. Understanding Short-Termism: The Role of Corporate Governance. Report to the Glasshouse Forum. Stockholm: Glasshouse Forum, pp. 9–10. [Google Scholar]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Kajuter, Peter, Florian Klassmann, and Martin Nienhaus. 2018. The effect of mandatory quarterly reporting on firm value. The Accounting Review 94: 251–77. [Google Scholar] [CrossRef]

- Kanodia, Chandra, and Deokheon Lee. 1998. Investment and disclosure: The disciplinary role of periodic performance reports. Journal of Accounting Research 36: 33–55. [Google Scholar] [CrossRef]

- Kraft, Arthur G., Rahul Vashishtha, and Mohan Venkatachalam. 2018. Frequent financial reporting and managerial myopia. The Accounting Review 93: 249–75. [Google Scholar] [CrossRef]

- Ladika, Tomislav, and Zacharias Sautner. 2019. Managerial Short-Termism and Investment: Evidence from Accelerated Option Vesting. Available online: https://ssrn.com/abstract=2286789 (accessed on 29 September 2020).

- Lane, Philip R., and Gian Maria Milesi-Ferretti. 2008. The drivers of financial globalization. American Economic Review: Papers & Proceedings 98: 327–32. [Google Scholar] [CrossRef] [Green Version]

- Lang, Mark, and Mark Maffett. 2010. Economic effects of transparency in international equity markets: A review and suggestions for future research. Foundations and Trends in Accounting 5: 175–241. [Google Scholar] [CrossRef]

- Lannoo, Karel, and Apostolos Thomadakis. 2020. Derivatives in Sustainable Finance. CEPS-ECMI Study. Brussels: Centre for European Policy Studies, p. 3. [Google Scholar]

- Laverty, Kevin J. 2004. Managerial myopia or systemic short-termism? The importance of managerial systems in valuing the long term. Management Decision 42: 949–62. [Google Scholar] [CrossRef]

- Link, Benedikt. 2012. The struggle for a common interim reporting frequency regime in Europe. Accounting in Europe 9: 191–226. [Google Scholar] [CrossRef]

- Marinovic, Ivan, and Feliepe Varas. 2019. CEO horizon, optimal pay duration, and the escalation of short-termism. The Journal of Finance 74: 2011–53. [Google Scholar] [CrossRef]

- McNichols, Maureen, and James G. Manegold. 1983. The effect of the information environment on the relationship between financial disclosure and security price variability. Journal of Accounting and Economics 5: 49–74. [Google Scholar] [CrossRef]

- Park, James J. 2020. Do the securities laws promote short-termism? UC Irvine Law Review 10: 991–1044. [Google Scholar]

- Rappaport, Alfr. 2005. The economics of short-term performance obsession. Financial Analyst Journal 61: 65–79. [Google Scholar] [CrossRef]

- Reilly, Greg, David Souder, and Rebecca Ranucci. 2016. Time horizon of investments in the resource allocation process: Review and framework for next steps. Journal of Management 42: 1169–94. [Google Scholar] [CrossRef]

- Sachsida, Adolfo, and Marcelo Abi-Ramia Caetano. 2000. The Feldstein–Horioka puzzle revisited. Economics Letters 68: 85–88. [Google Scholar] [CrossRef]

- Sappideen, Razzen. 2011. Focusing on Corporate Short-termism. Singapore Journal of Legal Studies 53: 412–31. [Google Scholar]

- Securities and Exchange Commission (SEC). 2018. Request for Comment on Earnings Releases and Quarterly Reports. Release No. 33-10588; 34-84842. Washington, DC: SEC. [Google Scholar]

- Shleifer, Andrei, and Robert W. Vishny. 1990. Equilibrium short horizons of investors and firms. American Economic Review 80: 148–53. [Google Scholar]

- Souder, David, Greg Reilly, Philip Bromiley, and Scott Mitchell. 2016. A behavioral understanding of investment horizon and firm performance. Organization Science 27: 1065–341. [Google Scholar] [CrossRef]

- Stulz, René M. 2009. Securities laws, disclosure, and national capital markets in the age of financial globalization. Journal of Accounting Research 47: 349–90. [Google Scholar] [CrossRef] [Green Version]

- Thakor, Anjan V. 1990. Investment myopia and the internal organization of capital allocation decisions. Journal of Law, Economics, and Organization 1: 129–54. [Google Scholar] [CrossRef]

- The G20 Green Finance Study Group. 2016. G20 Green Finance Synthesis Report. p. 3. Available online: http://unepinquiry.org/g20greenfinancerepositoryeng (accessed on 29 September 2020).

- Thomas, Jacob, and Frank Zhang. 2008. Overreaction to intra-industry information transfers? Journal of Accounting Research 46: 909–40. [Google Scholar] [CrossRef]

- United Nations. 2015. Transforming our World: The 2030 Agenda for Sustainable Development. Available online: https://sustainabledevelopment.un.org/post2015/transformingourworld (accessed on 29 September 2020).

- Van Buskirk, Andrew. 2012. Disclosure frequency and information asymmetry. Review of Quantitative Finance and Accounting 38: 411–40. [Google Scholar] [CrossRef]

- World Bank Group Initiative. 2017. Roadmap for a Sustainable Financial System. Nairobi: UN Environment. [Google Scholar]

- World Commission on Environment and Development. 1987. Report of the World Commission on Environment and Development: Our Common Future. Available online: https://sustainabledevelopment.un.org/content/documents/5987our-common-future.pdf (accessed on 29 September 2020).

- Yanovski, Boyan, Lessmann Kai, and Tahri Ibrahim. 2020. The Link between Short-Termism and Risk: Barriers to Investment in Long-Term Projects. Available online: https://ssrn.com/abstract=3550501 (accessed on 29 September 2020).

- Yongtae, Kim, Lixin Su, and Xindong Zhu. 2017. Does the cessation of quarterly earnings guidance reduce investors’ short-termism? Review of Accounting Studies 22: 715–52. [Google Scholar] [CrossRef]

- Zhou, Mengchen. 2018. Potential consequences of U.S. Securities and Exchange Commission’s Replacement of the Quarterly Reporting Requirement for Semi-Annual Reporting. Accounting Undergraduate Honors Theses. Available online: https://scholarworks.uark.edu/acctuht/37 (accessed on 22 September 2020).

| 1 | Currently ESG investments are equated with Socially Responsible Investment (SRI), although this was not always the case. SRI has its origins in what was termed ethical investment with moral screening (Escrig-Olmedo et al. 2013). |

| 2 | “Given the complexity of the financial system and its policy and regulatory framework, there is no single lever to achieve these ambitions and ‘switch’ the financial system to sustainability.” (Final Report 2018, p. 5). |

| 3 | “As the investment pillar of the European Green Deal, the Sustainable Europe Investment Plan will mobilize at least EUR 1 trillion of sustainable investments over the next decade. This amount of financing for the green transition is achieved through spending under the EU’s long-term budget, a quarter of which will go to climate-related purposes, and including estimated EUR 39 billion for environmental expenditures. Moreover, the Plan will crowd in additional private funding through leveraging the EU’s budget guarantee under the InvestEU Programme.” (European Commission 2020, p. 4). |

| 4 | We have ignored the London Stock Exchange in our research for two reasons. Firstly, the UK is no longer a member of the EU. Secondly, the UK has adopted the Anglo–American model of corporate governance, while our study focuses on countries, which has adopted the Continental Model as the most appropriate. To provide a broader view of the practical publication of quarterly financial statements by European companies, we additionally included the Swiss Stock Exchange and the Oslo Bors & Oslo Axess (similar accounting principles, reporting regulations, financial disclosure, and reporting frequency to the rest of the EU countries). |

| 5 | “The evidence most clearly points to projections as the main source of pressure on public companies. Public companies reported quarterly earnings for decades without feeling the pressure of short-termism. It was not until quarterly projections became widely distributed that short-termism became an issue” (Park 2020, p. 996). |

{kind=link}

Table 1.

Quarterly reporting environment in the EU-15 after the “Transparency Directive” implemented in 2007.

Table 1.

Quarterly reporting environment in the EU-15 after the “Transparency Directive” implemented in 2007.

| Member of the EU | Quarterly Financial Reporting Mandatory? | Quarterly Reporting Rules? |

|---|---|---|

| Belgium | No—only IMS | No |

| Denmark | No—only IMS | No |

| Germany | No—only IMS | No—except companies listed in the “Prime Standard” |

| Greece | Yes | Obligatory for all listed firms |

| Spain | No—only IMS | No |

| France | No—only IMS | No |

| Ireland | No—only IMS | No |