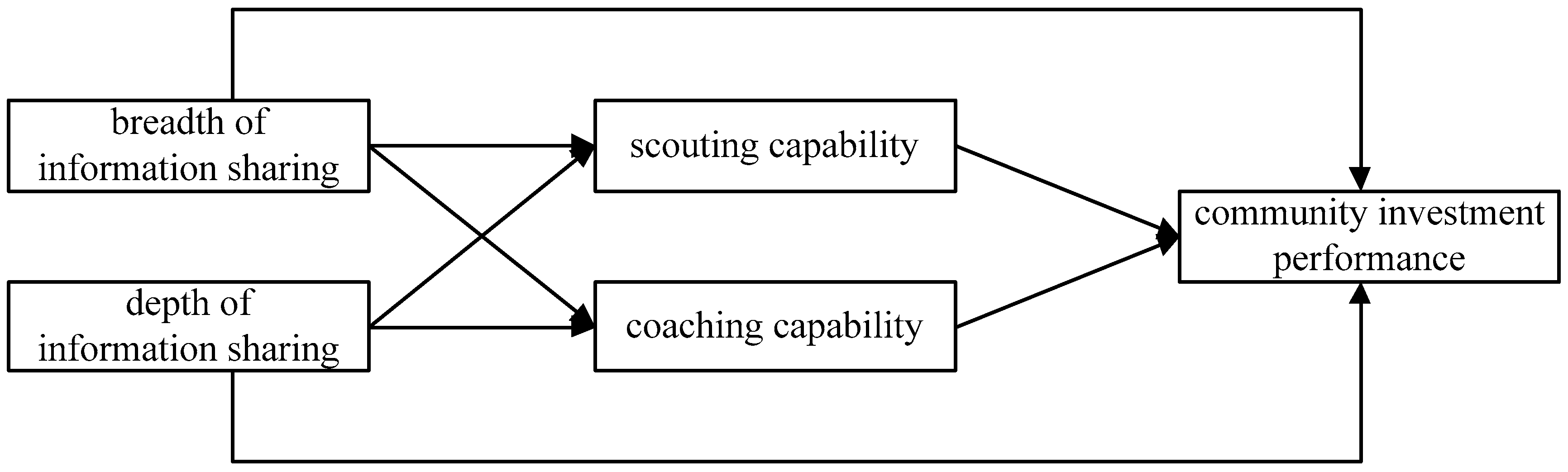

3.4.1. Impact of Community Information Sharing on Investment Performance

Based on the research of Hwang and Lee [

13] and Bubna et al. [

14], this paper divides VC network community information sharing into two dimensions: information sharing breadth and information sharing depth, and the study investigates its impact on investment performance.

First, the higher the breadth of information sharing in the VC network community, the more information the community members obtain and the broader is the scope of investment ESG start-ups, which helps them to select better quality ESG start-ups and improve investment performance. Bygrave [

20] suggests that VCs can learn whether start-ups are rejected by other members through the network, which will speed up the project screening of VCs. Cumming [

21] found that VCs share information through syndicated investment to reduce the information asymmetry of investment start-ups and the information sharing between VCs on investment start-ups helps to reduce the possibility of investing in “lemon” start-ups. Beshears [

22] found that information sharing among members of the Gulf of Mexico Oil and Gas Drilling Company help member companies find large-scale drilling, thereby improving their financial performance. Therefore, we believe that the higher the breadth of information sharing in the VC network community, the more information the community members can obtain about ESG start-ups, and the more it can help reduce the time of project screening and select higher quality ESG start-ups, thus improving investment performance.

Second, the higher the breadth of information sharing in the VC network community is, the more experience information the members of the community obtain, and the more skills they use in monitoring business management. These advantages enable the community members to provide better value-added services for ESG start-ups and improve investment performance after investment. Hopp [

23] believes that industry investment experience provides legitimacy for leading VCs, and more industry experience can bring more syndicated investment. Huang et al. [

24] found that if a company’s directors have experience in investment banking, the possibility of making merger decisions on the board is higher, and the M&A events show higher long-term performance. Similarly, Field and Mkrtchyan [

25] also believe that companies will hire directors to gain acquisition experience that is positively related to subsequent acquisition performance. Therefore, we believe that the higher the breadth of information sharing in the VC network community, the more experience information members can obtain, and the more comprehensive value-added services can be provided to ESG start-ups, and thus, the investment performance can be improved.

Based on the above analysis, this paper believes that the breadth of information sharing in the VC network community about ESG start-ups can increase the amount of information of community members and facilitate project screening and value-added services, thereby improving investment performance. Therefore, we propose the following hypothesis:

H1. The breadth of information sharing in the venture capital network community has a positive impact on investment performance.

First, the deeper the VC network community information sharing is, the more frequent the information sharing among the members of the community is, and the more trust that can be generated between them, which helps to obtain “second opinion” on investment ESG start-ups and reduce opportunistic behavior. Lee [

26] argues that information sharing through repeated transactions reduces information asymmetry among participants and the opportunistic behavior of partners. Therefore, we believe that the higher is the depth of information sharing in VC network community, the higher the trust among community members. This trust will help to provide real and effective “second-party opinions” for syndicated investment ESG start-ups and reduce opportunistic behavior in the process of cooperation, thereby improving the performance of community investment.

Second, when the information sharing depth of the VC network community is large, the information sharing among community members will be more frequent; thus, the relationship between members is intimate, making the community partners form reciprocal behavior. Ritter [

27] found that when institutional investors pay more transaction commissions to the main underwriters of the IPO, institutional investors can obtain more IPO share placements. Ferrary [

28] believes that the VC participating in the first round of investment is regarded as an internal investor who understands the private information of the start-ups in the subsequent round of financing. This study shares the private information of the start-ups with its familiar partners in exchange for the return of other VCs on the investment project. Therefore, we believe that the deeper the information sharing of VC network community is, the more frequent the reciprocal behavior among members of the community and the greater the pool of ESG start-ups resources that can be formed within the community, which will help to invest in more high-quality ESG start-ups, thereby improving the performance of community investment.

Based on the above analysis, we have the following hypothesis:

H2. The depth of information sharing in the venture capital network community has a positive impact on investment performance.

3.4.2. Impact of Community Information Sharing on Investment Capability

The greater the breadth of information sharing is, and the greater the number of information channels is, the larger the information set collected by VC is, which helps to identify external opportunities, perceive investment opportunities and initiate investment activities earlier than other online communities. Ozmel et al. [

10] shows that network-centric VCs have a wider access to information, which helps to understand the service needs of the start-ups. In the area of VCs, Sorenson and Stuart [

11] finds that information about potential investment opportunities typically circulates within geographic and industrial spaces that limit the flow of information and allow VCs to make local investments in geography and industry. However, the syndicated investment network between VCs allows information to be shared across space boundaries, thereby reducing the spatial constraints on economic exchanges and affecting investment decisions such as VC investment regions and investment industries. Hopp [

23] believes that new partners joining the syndicated investment network can be an important source of new knowledge or information. The new partners provide more heterogeneous knowledge and information for the syndicated investment network, which helps the members of the original investment network to expand investment areas and investment industries.

The greater the breadth of information sharing, and the more members or channels in the community for start-ups project information or postinvestment experience information, the higher is the information heterogeneity among community members, which helps the VC network community allocate resources such as information according to the characteristics of the start-ups. Henderson and Cockburn [

29] argues that new heterogeneous information or knowledge is necessary for solving unconventional problems. In addition, the more information sources or channels community members have, the more complementary the information among community members. As a result, the community has a greater chance of reorganizing or utilizing a variety of information, which helps the VC community to create new information or new knowledge and to allocate resources for information such as new investment opportunities. The study by Fleming and Sorenson [

30] confirms that the greater the breadth of knowledge sharing, the greater are the chances of reorganizing and integrating knowledge, which will drive new product development activities.

Therefore, we believe that the greater the breadth of information sharing, and the greater the number of information collections shared by the VC community, the more it can identify external investment opportunities in more investment areas about ESG start-ups, thereby improving its scouting capability. At the same time, the greater the breadth of information sharing, the higher is the information heterogeneity and information complementarity of VC network communities in relation to VC investment projects, which is conducive to resource allocation and utilization for solving conventional or unconventional problems. It also facilitates the allocation of resources for acquiring new investment opportunities, which will improve its utilization of configuration, thereby improving its coaching capability. In summary, this paper proposes the following hypotheses:

H3. The breadth of information sharing in the VC network community has a positive impact on the community’s investment capability.

H3a. The breadth of information sharing in the VC network community has a positive impact on the scouting capability.

H3b. The breadth of information sharing in the VC network community has a positive impact on the coaching capability.

The depth of information sharing affects the authenticity of information and the value of information, thereby affecting the scouting capability. The greater the depth of information sharing is, the more frequent or repeated the communication and sharing between ESG start-ups project information or experience information among community members are, which will strengthen the community’s capability to perceive investment opportunities. For the VC network community, the higher is the depth of information sharing, the more frequent the information sharing among community members, and the more trust that they can generate between each other, which helps to obtain “second-party opinions” about investment ESG start-ups and reduce opportunistic behavior. Cumming [

21] believes that “second-party opinions” can be obtained in the VC network, which is the information of other VCs on the start-ups, which is beneficial to reduce the possibility of investing in the “lemon” start-ups. Similarly, Lee [

26] holds that the information sharing accumulated through repeated transactions reduces the information asymmetry between participants and reduces the opportunistic behavior of partners.

Information sharing has a deep impact on information communication, information understanding and information reorganization, which affects the coaching capability. According to Levinthal and March [

31], on the one hand, the depth of knowledge sources can effectively reduce the mismatch of information at the communication level and reduce the cost of information communication. On the other hand, the depth of knowledge sources can deepen the concept of this information or knowledge and thus is conducive to the development of more valuable information or knowledge, that is, information reorganization. For the VC field, the experience information is particularly professional, and VCs often focus on investing in specific industries and at specific stages to accumulate specialized investment experience. The depth of the sharing of investment experience information can facilitate the reorganization of investment experience and the formation of new investment experience.

Therefore, we believe that the greater the depth of information sharing, the easier it is for the VC network community to obtain more authentic or valuable information, such as “second-party opinions” on ESG start-ups, which can strengthen the VC network community’s ability to grasp the investment opportunities and the perception of partner selection, thereby improving the scouting capability. At the same time, the greater the depth of information sharing, the more the VC network community can reduce the cost of information communication, and the more conducive it is to information reorganization, thereby improving the coaching capability.

H4. The depth of information sharing in the VC network community has a positive impact on the community’s investment capability.

H4a. The depth of information sharing in the VC network community has a positive impact on the scouting capability.

H4b. The depth of information sharing in the VC network community has a positive impact on the coaching capability.

3.4.3. Mediating Role of Community Investment Capability

This paper believes that the breadth of information sharing and the depth of information sharing influence the performance of community investment through the intermediary path of scouting capability and coaching capability. The construction of scouting capability and coaching capability is based on community information sharing. The stronger the community-sensing initiative is, the better the quantity and quality of information about investment opportunities. This is also the reflection of the breadth and depth of information sharing. At the same time, a network community with strong scouting capability can better screen and evaluate ESG start-ups and guarantee the improvement of investment performance in the quality of ESG start-ups. The stronger is the utilization of the configuration, the richer or more professional the resources such as the mastery and the information that can be controlled. Moreover, a network community with strong coaching capability can also mobilize, utilize, and reorganize the information and other resources for value-added services such as supervision and corporate governance, and promote the rapid and sustainable development of the ESG start-ups, ensuring that it has better investment performance.

Therefore, the scouting capability and coaching capability establish a bridge between community information sharing and investment performance. The difference in the breadth and depth of information sharing will result in different scouting capability and coaching capability. The scouting capability and coaching capability directly determine the project screening and value-added service quality of the ESG start-ups, which in turn affects its investment performance. Based on the above analysis, this paper proposes the following hypotheses:

H5. Community investment capability plays a mediating role in the relationship between information sharing and investment performance.

H5a. The scouting capability plays a mediating role in the relationship between the breadth of information sharing and investment performance.

H5b. The scouting capability plays a mediating role in the relationship of investment performance in the depth of information sharing.

H5c. The coaching capability plays a mediating role in the investment performance relationship in the breadth of information sharing.

H5d. The coaching capability plays a mediating role in the relationship of investment performance in the depth of information sharing.

{kind=link}