The Nexus between Energy Consumption, Biodiversity, and Economic Growth in Lancang-Mekong Cooperation (LMC): Evidence from Cointegration and Granger Causality Tests

Abstract

1. Introduction

2. Literature Review

2.1. Four Hypotheses

2.2. Proxy Variables

2.3. Methodology

3. Methodology and Data

3.1. Four Hypotheses

3.2. Data

4. Empirical Analysis

4.1. Unit Root Test

4.2. The Panel Cointegration Test

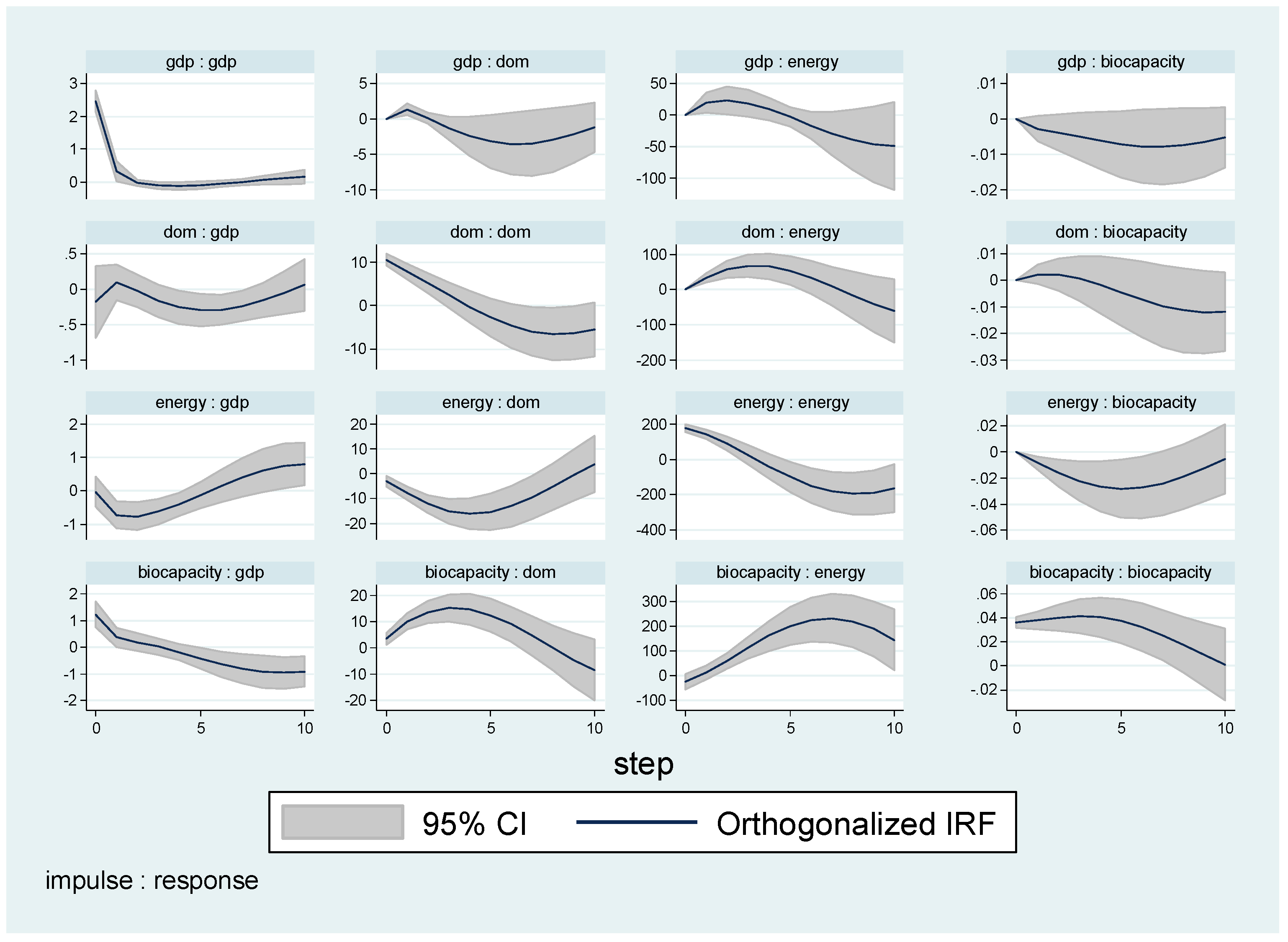

4.3. IRF Test

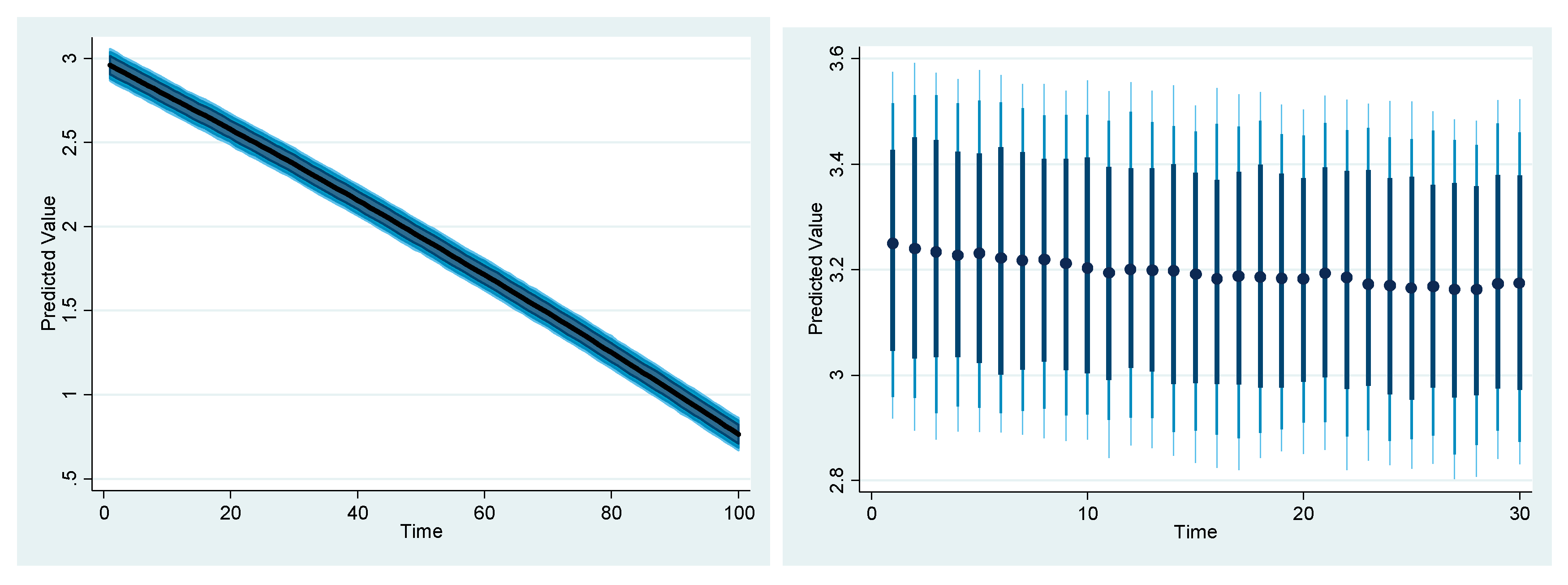

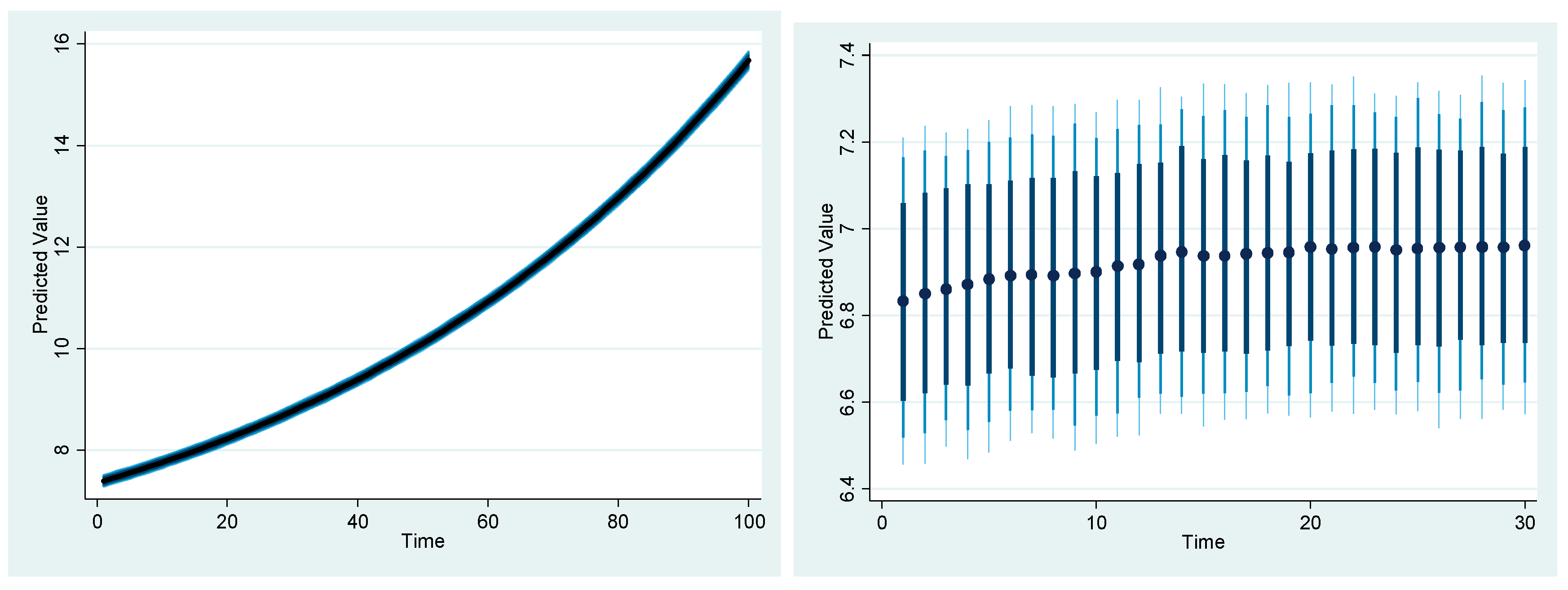

4.4. Empirical Results

5. Discussion and Policy Implications

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

Appendix A

References

- Zhang, C.; Zhou, K.; Yang, S.; Shao, Z. On electricity consumption and economic growth in China. Renew. Sustain. Energy Rev. 2017, 76, 353–368. [Google Scholar] [CrossRef]

- Xing, W. Lancang-Mekong River Cooperation and Trans.-Boundary Water Governance: A Chinese Perspective. China Q. Int. Strateg. Stud. 2017, 03, 377–393. [Google Scholar] [CrossRef]

- Liu, N. Lancang-Mekong Cooperation Injects New Momentum into Regional Development. China Foreign Trade (Engl. Ed.) 2018, 39, 39–41. [Google Scholar]

- Middleton, C.; Allouche, J. Watershed or Powershed? Critical Hydropolitics, China and the Lancang-Mekong Cooperation Framework. Int. Spect. 2016, 51, 100–117. [Google Scholar] [CrossRef]

- Arellano, M.; Bond, S. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef]

- Shahbaz, M.; Van Hoang, T.H.; Mahalik, M.K.; Roubaud, D. Energy consumption, financial development and economic growth in India: New evidence from a nonlinear and asymmetric analysis. Energy Econ. 2017, 63, 199–212. [Google Scholar] [CrossRef]

- Guangsheng, L.U. Lancang-Mekong Cooperation: How Did It Emerge from All Multilateral Mechanism? Contemp. World 2016, 6, 20–23. [Google Scholar]

- Menegaki, A.N.; Tugcu, C.T. The sensitivity of growth, conservation, feedback & neutrality hypotheses to sustainability accounting. Energy Sustain. Dev. 2016, 34, 77–87. [Google Scholar]

- Musa, S.D.; Zhonghua, T.; Ibrahim, A.O.; Habib, M. China’s energy status: A critical look at fossils and renewable options. Renew. Sustain. Energy Rev. 2018, 81, 2281–2290. [Google Scholar] [CrossRef]

- Lin, L.; Cunshan, Z.; Vittayapadung, S.; Xiangqian, S.; Mingdong, D. Opportunities and challenges for biodiesel fuel. Appl. Energy 2011, 88, 1020–1031. [Google Scholar] [CrossRef]

- Gregg, J.S.; Andres, R.J.; Marland, G. China: Emissions pattern of the world leader in CO2 emissions from fossil fuel consumption and cement production. Geophys. Res. Lett. 2008, 35, 1020–1031. [Google Scholar] [CrossRef]

- Dong, K.Y.; Sun, R.J.; Li, H.; Jiang, H.D. A review of China’s energy consumption structure and outlook based on a long-range energy alternatives modeling tool. Pet. Sci. 2016, 14, 214–227. [Google Scholar] [CrossRef]

- Li, R.; Leung, G.C.K. Coal consumption and economic growth in China. Energy Policy 2012, 40, 438–443. [Google Scholar] [CrossRef]

- Lean, H.H.; Smyth, R. Multivariate Granger causality between electricity generation, exports, prices and GDP in Malaysia. Energy 2010, 35, 3640–3648. [Google Scholar] [CrossRef]

- Stern, D.I. A multivariate cointegration analysis of the role of energy in the US macroeconomy. Energy Econ. 2000, 22, 267–283. [Google Scholar] [CrossRef]

- Ghali, K.H.; El-Sakka, M.I.T. Energy use and output growth in Canada: A multivariate cointegration analysis. Energy Econ. 2004, 26, 225–238. [Google Scholar] [CrossRef]

- Shahbaz, M.; Zeshan, M.; Afza, T. Is energy consumption effective to spur economic growth in Pakistan? New evidence from bounds test to level relationships and Granger causality tests. Econ. Mod. 2012, 29, 2310–2319. [Google Scholar]

- Omri, A.; Daly, S.; Rault, C.; Chaibi, A. Financial development, environmental quality, trade and economic growth: What causes what in MENA countries. Energy Econ. 2015, 48, 242–252. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. Renewable energy consumption and economic growth: Evidence from a panel of OECD countries. Energy Polic 2010, 38, 656–660. [Google Scholar] [CrossRef]

- Menegaki, A.N. Growth and renewable energy in Europe: A random effect model with evidence for neutrality hypothesis. Energy Econ. 2011, 33, 257–263. [Google Scholar] [CrossRef]

- Tugcu, C.T.; Ozturk, I.; Aslan, A. Renewable and non-renewable energy consumption and economic growth relationship revisited: Evidence from G7 countries. Energy Econ. 2012, 34, 1942–1950. [Google Scholar] [CrossRef]

- Ouedraogo, N.S. Energy consumption and human development: Evidence from a panel cointegration and error correction model. Energy 2013, 63, 28–41. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. A dynamic panel study of economic development and the electricity consumption-growth nexus. Energy Econ. 2011, 33, 770–781. [Google Scholar] [CrossRef]

- Abbas, F.; Choudhury, N. Electricity consumption-economic growth Nexus: An aggregated and disaggregated causality analysis in India and Pakistan. J. Policy Mod. 2013, 35, 538–553. [Google Scholar]

- Tang, C.F.; Shahbaz, M. Sectoral analysis of the causal relationship between electricity consumption and real output in Pakistan. Energy Policy 2013, 60, 885–891. [Google Scholar] [CrossRef]

- Al-mulali, U.; Fereidouni, H.G.; Lee, J.Y.M. Electricity consumption from renewable and non-renewable sources and economic growth: Evidence from Latin American countries. Renew. Sustain. Energy Rev. 2014, 30, 290–298. [Google Scholar] [CrossRef]

- Carfora, A.; Pansini, R.V.; Scandurra, G. The causal relationship between energy consumption, energy prices and economic growth in Asian developing countries: A replication. Energy Strategy Rev. 2019, 23, 81–85. [Google Scholar] [CrossRef]

- Shahbaz, M.; Lean, H.H. The dynamics of electricity consumption and economic growth: A revisit study of their causality in Pakistan. Energy 2012, 39, 146–153. [Google Scholar] [CrossRef]

- Wolde-Rufael, Y. Disaggregated industrial energy consumption and GDP: The case of Shanghai, 1952–1999. Energy Econ. 2004, 26, 69–75. [Google Scholar] [CrossRef]

- Ang, J.B. CO2 emissions, energy consumption, and output in France. Energy Policy 2007, 35, 4772–4778. [Google Scholar] [CrossRef]

- Soytas, U.; Sari, R.; Ewing, B.T. Energy consumption, income, and carbon emissions in the United States. Ecol. Econ. 2007, 62, 482–489. [Google Scholar] [CrossRef]

- Lin, S.; Wang, S.; Marinova, D.; Zhao, D.; Hong, J. Impacts of urbanization and real economic development on CO2 emissions in non-high income countries: Empirical research based on the extended STIRPAT model. J. Clean. Prod. 2017, 166, 952–966. [Google Scholar] [CrossRef]

- Destek, M.A.; Aslan, A. Renewable and non-renewable energy consumption and economic growth in emerging economies: Evidence from bootstrap panel causality. Renew. Energy 2017, 111, 757–763. [Google Scholar] [CrossRef]

- Brini, R.; Amara, M.; Jemmali, H. Renewable energy consumption, International trade, oil price and economic growth inter-linkages: The case of Tunisia. Renew. Sustain. Energy Rev. 2017, 76, 620–627. [Google Scholar] [CrossRef]

- Pinzón, K. Dynamics between energy consumption and economic growth in Ecuador: A granger causality analysis. Econ. Anal. Policy 2018, 57, 88–101. [Google Scholar] [CrossRef]

- Bakirtas, T.; Akpolat, A.G. The relationship between energy consumption, urbanization, and economic growth in new emerging-market countries. Energy 2018, 147, 110–121. [Google Scholar] [CrossRef]

- Owusu Appiah, M. Investigating the multivariate Granger causality between energy consumption, economic growth and CO2 emissions in Ghana. Energy Policy 2017, 112, 198–208. [Google Scholar] [CrossRef]

- Wang, Q.; Su, M.; Li, R.; Ponce, P. The effects of energy prices, urbanization and economic growth on energy consumption per capita in 186 countries. J. Clean. Prod. 2019, 225, 1017–1032. [Google Scholar] [CrossRef]

- Sims, C.A. Macroeconomics and reality. Econ. J. Econ. Soc. 1980, 48, 1–48. [Google Scholar] [CrossRef]

- Liu, H.; Kim, H. Ecological Footprint, Foreign Direct Investment, and Gross Domestic Prod.: Evidence of Belt & Road Initiative Countries. Sustainability 2018, 10, 3527. [Google Scholar] [CrossRef]

- Wolde-Rufael, Y. Electricity consumption and economic growth: A time series experience for 17 African countries. Energy Policy 2006, 34, 1106–1114. [Google Scholar] [CrossRef]

- Fotis, P.; Karkalakos, S.; Asteriou, D. The relationship between energy demand and real GDP growth rate: The role of price asymmetries and spatial externalities within 34 countries across the globe. Energy Econ. 2017, 66, 69–84. [Google Scholar] [CrossRef]

- Omri, A. An international literature survey on energy-economic growth nexus: Evidence from country-specific studies. Renew. Sustain. Energy Rev. 2014, 38, 951–959. [Google Scholar] [CrossRef]

- Oh, W.; Lee, K. Causal relationship between energy consumption and GDP revisited: The case of Korea 1970–1999. Energy Econ. 2004, 26, 51–59. [Google Scholar] [CrossRef]

- Shiu, A.; Lam, P.-L. Electricity consumption and economic growth in China. Energy Policy 2004, 32, 47–54. [Google Scholar] [CrossRef]

- Liu, Y.; Hao, Y. The dynamic links between CO2 emissions, energy consumption and economic development in the countries along the Belt and Road. Sci. Total Environ. 2018, 645, 674–683. [Google Scholar] [CrossRef]

- Granger, C.W. Investigating causal relations by econometric models and cross-spectral methods. Econ. J. Econ. Soc. 1969, 37, 424–438. [Google Scholar] [CrossRef]

- Granger, C.W.J. Development in the Study of Co-Integrated Economic Variables. Oxf. Bull. Econ. Stat. 1986, 48, 213–228. [Google Scholar] [CrossRef]

- Engle, R.F.; Granger, C.W. Co-integration and error correction: Representation, estimation, and testing. Econ. J. Econ. Soc. 1987, 55, 251–276. [Google Scholar] [CrossRef]

- Diebold, F.X. Elements of Forecasting, 2nd ed.; University of Pennsylvania Press: Philadelphia, PA, USA, 2007. [Google Scholar]

- Haile, M.G.; Wossen, T.; Tesfaye, K.; von Braun, J. Impact of Climate Change, Weather Extremes, and Price Risk on Global Food Supply. Econ. Disasters Clim. Change 2017, 1, 55–75. [Google Scholar] [CrossRef]

- Johansen, S. Statistical analysis of cointegration vectors. J. Econ. Dyn. Control. 1988, 12, 231–254. [Google Scholar] [CrossRef]

- Granger, C.W.J.; Newbold, P. Spurious regressions in econometrics. J. Econ. 1974, 2, 111–120. [Google Scholar] [CrossRef]

- Liu, H.; Kim, H.; Choe, J. Export diversification, CO2 emissions and EKC: Panel data analysis of 125 countries. Asia-Pac. J. Reg. Sci. 2018, 3, 361–393. [Google Scholar] [CrossRef]

- Lee, J.; Strazicich, M.C. Minimum LM unit root test with one structural break. Econ. Bull. 2013, 33, 2483–2492. [Google Scholar]

- Friedl, B.; Getzner, M. Determinants of CO2 emissions in a small open economy. Ecol. Econ. 2003, 45, 133–148. [Google Scholar] [CrossRef]

- Elliot, B.; Rothenberg, T.; Stock, J. Efficient tests of the unit root hypothesis. Econometrica 1996, 64, 13–36. [Google Scholar]

- Choi, I. Unit root tests for panel data. J. Int. Mon. Finance 2001, 20, 249–272. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, M.H.; Shin, Y. Testing for unit roots in heterogeneous panels. J. Econ. 2003, 115, 53–74. [Google Scholar] [CrossRef]

- Gengenbach, C.; Palm, F.C.; Urbain, J.-P. Panel unit root tests in the presence of cross-sectional dependencies: Comparison and implications for modelling. Econ. Rev. 2009, 29, 111–145. [Google Scholar] [CrossRef]

- Levin, A.; Lin, C.F.; Chu, C.S.J. Unit root tests in panel data: Asymptotic and finite-sample properties. J. Econ. 2002, 108, 1–24. [Google Scholar] [CrossRef]

- Jordan, S.; Philips, A.Q. Cointegration Testing and Dynamic Simulations of Autoregressive Distributed Lag Models. St. J. Promot. Commun. Stat. St. 2019, 18, 902–923. [Google Scholar] [CrossRef]

- Neal, T. Panel cointegration analysis with xtpedroni. St. J. 2014, 14, 684–692. [Google Scholar] [CrossRef]

- Pesaran, H.H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econ. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Pesaran, M.H. A simple panel unit root test in the presence of cross-section dependence. J. Appl. Econ. 2007, 22, 265–312. [Google Scholar] [CrossRef]

- Lee, C.-C. Energy consumption and GDP in developing countries: A cointegrated panel analysis. Energy Econ. 2005, 27, 415–427. [Google Scholar] [CrossRef]

- Magazzino, C.; Giolli, L.; Mele, M. Wagner’s Law and Peacock and Wiseman’s Displacement Effect in European Union Countries: A Panel Data Study. Int. J. Econ. Financ. Issues 2015, 5, 812–819. [Google Scholar]

- Perman, R.; Stern, D.I. Evidence from panel unit root and cointegration tests that the environmental Kuznets curve does not exist. Aust. J. Agric. Res. Econ. 2003, 47, 325–347. [Google Scholar] [CrossRef]

- Ghosh, S. Electricity supply, employment and real GDP in India: Evidence from cointegration and Granger-causality tests. Energy Policy 2009, 37, 2926–2929. [Google Scholar] [CrossRef]

- Swanson, N.; Granger, C.J. Impulse Response Functions Based on a Causal Approach to Residual Orthogonalization in Vector Autoregressions. Publ. Am. Stat. Assoc. 1997, 92, 357–367. [Google Scholar] [CrossRef]

- Liu, H.; Kim, H.; Liang, S.; Kwon, O.S. Export Diversification and Ecological Footprint: A Comparative Study on EKC Theory among Korea, Japan, and China. Sustainability 2018, 10, 3657. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author | Country | Time Period | Methodology | Conclusion |

|---|---|---|---|---|

| Hooi Hooi Lean, Russell Smyth [14] | Malaysia | 1970–2008 | ARDL (autoregressive distributed lag); TYDL (Toda and Yamanoto and Dolado and Lutkepohl) | Economic growth→Electricity generation |

| David Stern [15] | US | 1945–1995 | Multivariate cointegration | Energy→GDP |

| Khalifa H. Ghali [16] | Canada | 1961–1997 | Vector error-correction | Output growth→Energy use |

| Muhammad Shahbaz [17] | Pakistan | 1972–2011 | VECM Granger causality | Renewable energy consumption→Economic growth;nonrenewable energy consumption→Economic growth |

| Chi Zhang, Kaile Zhou [1] | China | 1978–2016 | Vector error correction model | Energy consumption→Economic growth; |

| Author | Country Group | Time Period | Methodology | Conclusion |

|---|---|---|---|---|

| Anis Omri, etc. [18] | MENA (Middle East and North Africa Countries) countries | 1990–2011 | Dynamic simultaneous equation | CO2 emission→GDP |

| Nicholas Apergis, James Payne [19] | EOCD countries | 1985–2005 | Panel Cointegration, error correction model | Renewable energy consumption→Economic growth |

| Angeliki N. Menegaki [20] | 27 European countries | 1997–2007 | Random effect model for cointegration | Neutrality hypothesis |

| Can Tansel Tugcu, etc. [21] | G7 countries | 1980–2009 | Autoregressive distributed lag (ARDL) | No causal relationship |

| Variable | Observations | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|

| GDP | 144 | 6.35 | 7.70 | −34.81 | 14.23 |

| Broad money | 144 | 63.73 | 50.59 | 4.89 | 190.75 |

| Domestic money | 144 | 53.38 | 50.35 | 2.37 | 166.50 |

| Fossil energy consumption | 144 | 62.35 | 62.35 | 17.92 | 96.95 |

| Renewable energy consumption | 144 | 41.26 | 28.57 | 3.82 | 88.11 |

| Total biocapacity | 144 | 1.56 | 0.68 | 0.72 | 3.74 |

| Variables | Breitung | Fisher-ADF | Hadri |

|---|---|---|---|

| GDP growth | −1.61 (0.05) | 24.26 (0.02) | 12.91 (0.00) |

| Broad money | 3.32 (0.99) | 1.91 (0.99) | 26.73 (0.00) |

| Domestic money | 3.32 (0.99) | 5.40 (0.94) | 15.28 (0.00) |

| Fossil energy consumption | 3.18 (0.99) | 25.13 (0.01) | 16.53 (0.00) |

| Renewable energy consumption | 3.49 (0.99) | 22.21 (0.04) | 17.62 (0.00) |

| Total biocapacity | 1.91 (0.97) | 4.64 (0.97) | 26.02 (0.00) |

| Observations: 144 Number of Panel Units: 6 | |

|---|---|

| Test Name | Test Statistics |

| Panel v-statistics | 0.06428 |

| Panel rho-statistics | 0.04571 |

| Panel t-statistics | −0.5923 |

| Panel ADF-statistics | 0.1192 |

| Group rho-statistics | 0.689 |

| Group v-statistics | −0.3259 |

| Group ADF-statistics | 0.615 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, H.; Liang, S. The Nexus between Energy Consumption, Biodiversity, and Economic Growth in Lancang-Mekong Cooperation (LMC): Evidence from Cointegration and Granger Causality Tests. Int. J. Environ. Res. Public Health 2019, 16, 3269. https://doi.org/10.3390/ijerph16183269

Liu H, Liang S. The Nexus between Energy Consumption, Biodiversity, and Economic Growth in Lancang-Mekong Cooperation (LMC): Evidence from Cointegration and Granger Causality Tests. International Journal of Environmental Research and Public Health. 2019; 16(18):3269. https://doi.org/10.3390/ijerph16183269

Chicago/Turabian StyleLiu, Hongbo, and Shuanglu Liang. 2019. "The Nexus between Energy Consumption, Biodiversity, and Economic Growth in Lancang-Mekong Cooperation (LMC): Evidence from Cointegration and Granger Causality Tests" International Journal of Environmental Research and Public Health 16, no. 18: 3269. https://doi.org/10.3390/ijerph16183269

APA StyleLiu, H., & Liang, S. (2019). The Nexus between Energy Consumption, Biodiversity, and Economic Growth in Lancang-Mekong Cooperation (LMC): Evidence from Cointegration and Granger Causality Tests. International Journal of Environmental Research and Public Health, 16(18), 3269. https://doi.org/10.3390/ijerph16183269