The Subjective Well-Being Challenge in the Accounting Profession: The Role of Job Resources

,

,  ,

,

Abstract

:1. Introduction

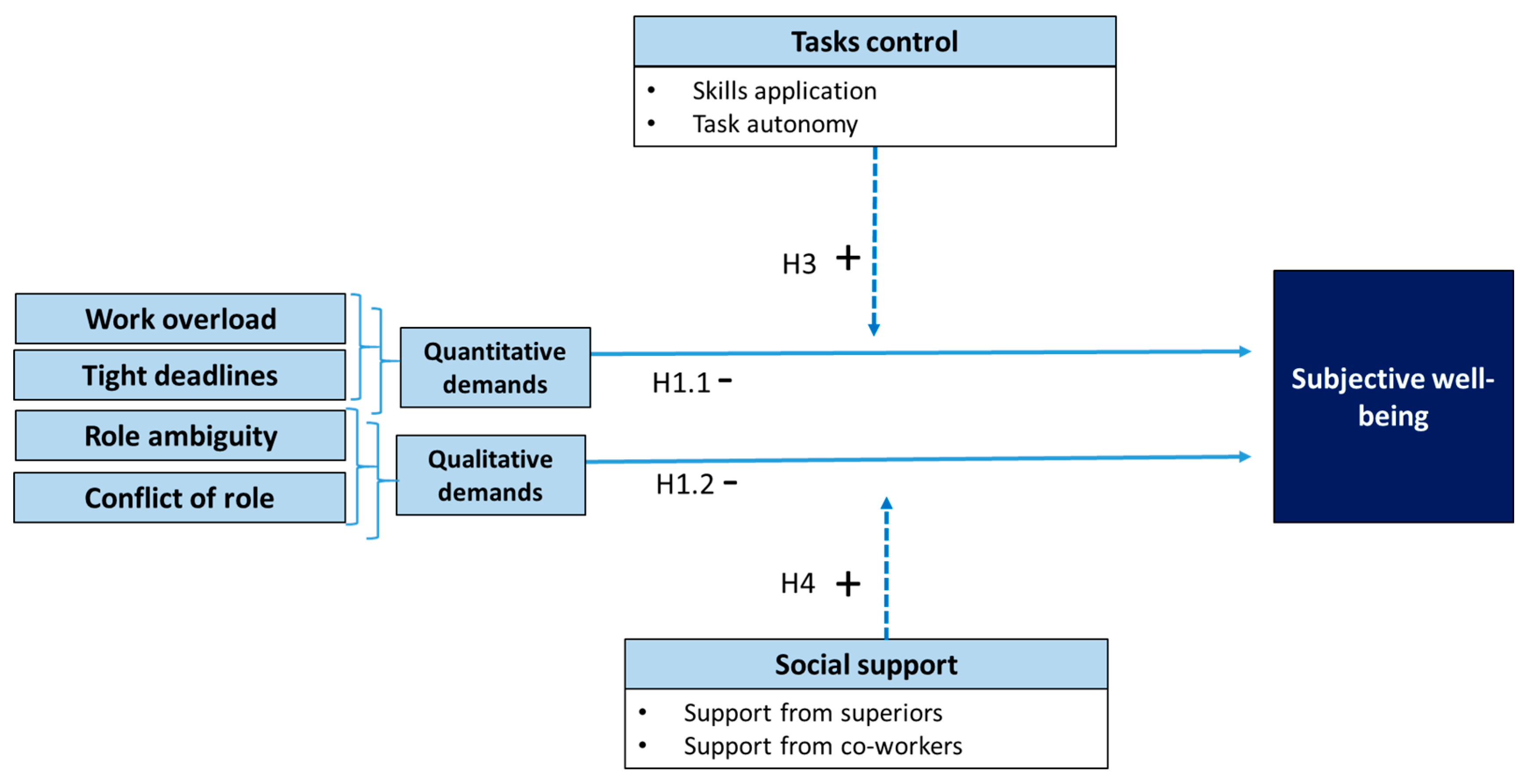

1.1. Job Demands on Accountants

1.2. Job Resources: Task Control and Social Support

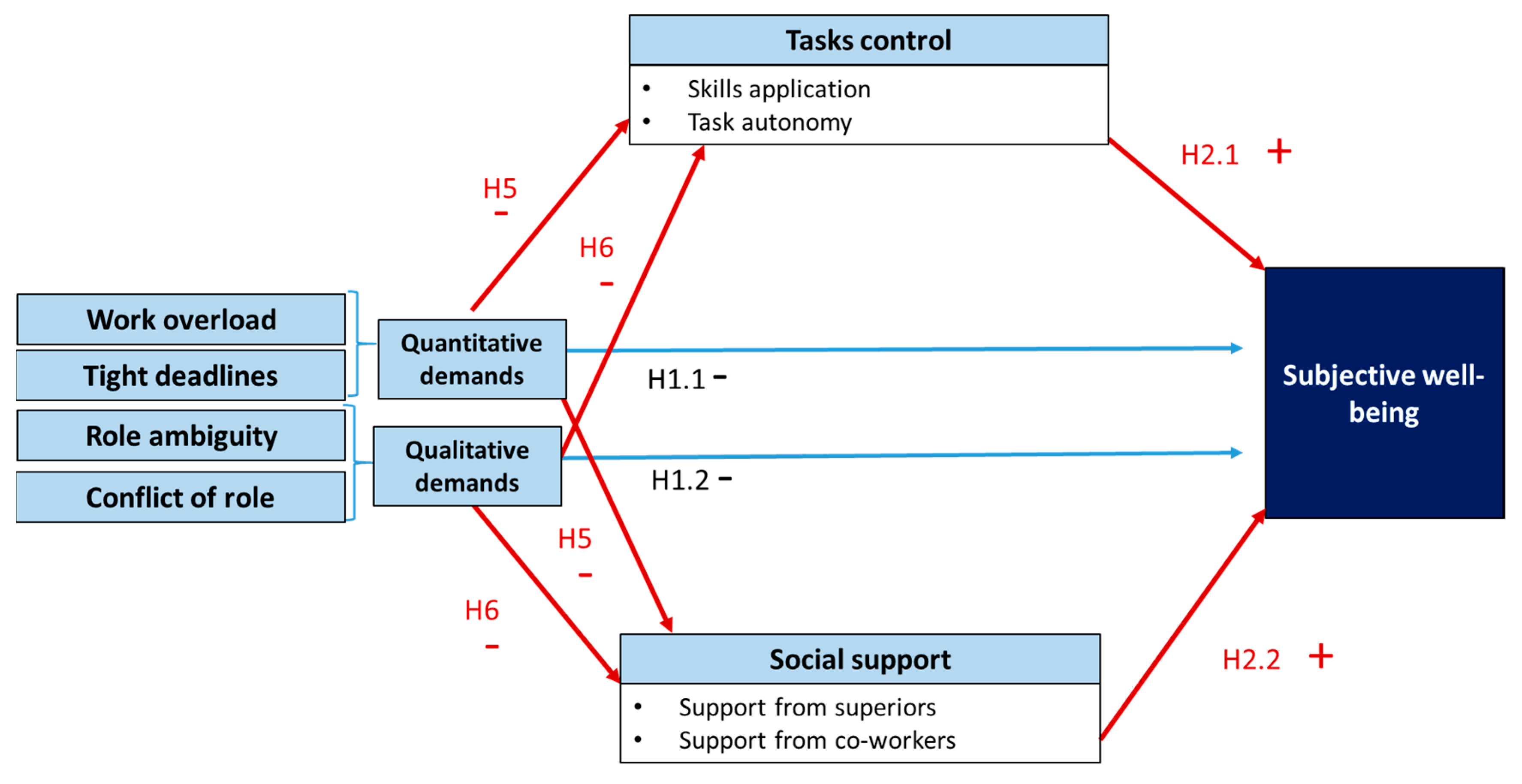

1.3. The Buffer or Mediating Role of Job Resources in the Relationship between Job Demands and Subjective Well-Being

2. Materials and Methods

2.1. Sample

2.2. Measures

2.3. Methodology

3. Results

3.1. Measurement Model

3.2. Structural Model

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Diener, E.; Tay, L. A Scientific Review of the Remarkable Benefits of Happiness for Successful and Healthy Living. Report to the United Nations General Assembly, Well-Being and Happiness: A New Development Paradigm 2012. Available online: http://www.researchgate.net/profile/Louis_Tay/publication/236272980_A_scientific_review_of_the_remarkable_benefits_of_happiness_for_successful_and_healthy_living/links/54a2e7830cf267bdb90 (accessed on 2 August 2019).

- Diener, E.; Chan, M. Happy people live longer: Subjective well-being contributes to health and longevity. Appl. Psychol. Health Well Being 2011, 3, 1–43. [Google Scholar] [CrossRef]

- Diener, E.; Wirtz, D.; Tov, W.; Kim-Prieto, C.; Dong-won, C.; Oishi, S. New well-being measures: Short scales to assess flourishing and positive and negative feelings. Soc. Indicat. Res. 2010, 97, 143–156. [Google Scholar] [CrossRef]

- Fogarty, T.J.; Singh, J.; Rhoads, G.K.; Moore, R.K. Antecedents and Consequences of Burnout in Accounting: Beyond the Role Stress Model. Behav. Res. Account. 2000, 12, 31–68. [Google Scholar]

- Johnson, J.V.; Hall, E.M. Job strain, work place social support, and cardiovascular disease: A cross-sectional study of a random sample of the Swedish working population. Am. J. Public Health 1988, 78, 1336–1342. [Google Scholar] [CrossRef]

- Karasek, R.A.; Theorell, T. Healthy Work: Stress, Productivity and the Reconstruction of Working Life; Basic Books: New York, NY, USA, 1990. [Google Scholar]

- Neffa, J.C. Los Riesgos Psicosociales en el Trabajo: Contribución a su Studio; Universidad Metropolitana para la Educación y el Trabajo. Centro de Innovación para los Trabajadores: Buenos Aires, Argentina, 2015; Available online: http://biblioteca.clacso.edu.ar/Argentina/fo-umet/20160212070619/Neffa.pdf (accessed on 19 August 2019).

- Rebele, J.E.; Michaels, R.E. Independent Auditors’ Role Stress: Antecedents, Outcome, and Moderating Variables. Behav. Res. Account. 1990, 2, 124–153. [Google Scholar]

- Sweeney, J.T.; Summers, S.L. The effect of busy season workload on public accountants’ job burnout. Behav. Res. Account. 2002, 14, 223–245. [Google Scholar] [CrossRef]

- Buchheit, S.; Dalton, D.W.; Harp, N.L.; Hollingsworth, C.W. A Contemporary Analysis of Accounting Professionals’ Work-Life Balance. Account. Horiz. 2016, 30, 41–62. [Google Scholar] [CrossRef]

- Umans, T.; Broberg, T.; Schmidt, M.; Nilsson, P.; Olsson, E. Feeling well by being together: Study of Swedish auditors. Work 2016, 54, 79–86. [Google Scholar] [CrossRef] [PubMed]

- Demerouti, E.; Bakker, A.B.; Nachreiner, F.; Schaufeli, W.B. The job demands–resources model of burnout. J. Appl. Psychol. 2001, 86, 499–512. [Google Scholar] [CrossRef]

- Schaufeli, W.B.; Bakker, A.B. Job demands, job resources, and their relationship with burnout and engagement: A multi-sample study. J. Organiz. Behav. 2004, 25, 293–315. [Google Scholar] [CrossRef]

- Asif, F.; Javed, U.; Janjua, S.Y. The Job Demand-Control-Support Model and Employee Well-being: A Meta-Analysis of Previous Research. Pak. J. Psychol. Res. 2018, 33, 203–221. [Google Scholar]

- Schaufeli, W.B.; Taris, T.W. A Critical Review of the Job Demands-Resources Model: Implications for Improving Work and Health. In Bridging Occupational, Organizational and Public Health: A Transdisciplinary Approach; Bauer, G.F., Hämmig, O., Eds.; Springer: Dordrecht, The Netherlands, 2014; Chapter 4; pp. 43–68. [Google Scholar] [CrossRef]

- Bakker, A.B.; Demerouti, E. The Job Demands—Resources model: State of the art. J. Manag. Psychol. 2007, 22, 309–328. [Google Scholar] [CrossRef]

- Häusser, J.A.; Mojzisch, A.; Niesel, M.; Schulz-Hardt, S. Ten years on: A review of recent research on the Job Demand–Control (-Support) model and psychological well-being. Work Stress 2010, 24, 1–35. [Google Scholar] [CrossRef]

- Ibrahim, R.; Ohtsuka, K. Review of the job demand-control and job demand-control-support models: elusive moderating predictor effects and cultural implications. South East Asia Psychol. J. 2014, 1, 10–21. [Google Scholar]

- Wolfe, D.M.; Snoek, J.D. A study of tension and adjustment under role conflict. J. Soc. Issues 1962, 18, 102–121. [Google Scholar] [CrossRef]

- Senatra, P. Role conflict, role ambiguity and organizational climate in a public accounting firm. Account. Rev. 1980, 55, 594–603. [Google Scholar]

- Beehr, T.A.; Walsh, J.T.; Taber, T.D. Relationship of stress to individually and organizationally valued states: Higher order needs as a moderator. J. Appl. Psychol. 1976, 61, 41–47. [Google Scholar] [CrossRef]

- Bennett, G.B.; Hartfield, R.C. Do Approaching Deadlines Influence Auditors’ Materiality Assessments? Audit. J. Pract. Theory 2017, 36, 29–48. [Google Scholar] [CrossRef]

- Bagley, P.L. Negative Affect: A Consequence of Multiple Accountabilities in Auditing. Audit. J. Pract. Theory 2010, 29, 141–157. [Google Scholar] [CrossRef]

- DeAngelo, L. Auditor size and audit quality. J. Account. Econ. 1981, 3, 189–199. [Google Scholar] [CrossRef]

- Chong, V.K.; Monroe, G.S. The impact of the antecedents and consequences of job burnout on junior accountants’ turnover intentions: A structural equation modelling approach. Account. Financ. 2015, 55, 105–132. [Google Scholar] [CrossRef]

- Nelson, M.W. A model and literature review of professional skepticism in auditing. Audit. J. Pract. Theory 2009, 28, 1–34. [Google Scholar] [CrossRef]

- Smith, K.J.; Derrick, P.L.; Koval, M.R. Stress and its antecedents and consequences in accounting settings: An empirically derived theoretical model. In Advances in Accounting Behavioral Research; Emerald Group Publishing Limited: Bingley, UK, 2010; Volume 13, pp. 113–142. [Google Scholar] [CrossRef]

- Janssen, O. Fairness perceptions as a moderator in the curvilinear relationships between job demands, and job performance and job satisfaction. Acad. Manag. J. 2001, 44, 1039–1050. [Google Scholar] [CrossRef]

- Ohly, S.; Sonnentag, S.; Pluntke, F. Routinization, work characteristics and their relationships with creative and proactive behaviors. J. Organ. Behav. 2006, 27, 257–279. [Google Scholar] [CrossRef] [Green Version]

- Baer, M.; Oldham, G.R. The Curvilinear Relation Between Experienced Creative Time Pressure and Creativity: Moderating Effects of Openness to Experience and Support for Creativity. J. Appl. Psychol. 2006, 91, 963–970. [Google Scholar] [CrossRef]

- Khedhaouria, A.; Montani, F.; Thurik, R. Time pressure and team member creativity within R&D projects: The role of learning orientation and knowledge sourcing. Int. J. Proj. Manag. 2015, 35, 942–954. [Google Scholar] [CrossRef]

- Maruping, L.M.; Venkatesh, V.; Thatcher, S.M.N.; Patel, P.C. Folding under pressure or rising to the occasion? Perceived time pressure and the moderating role of team temporal leadership. Acad. Manag. J. 2015, 58, 1313–1333. [Google Scholar] [CrossRef]

- Glover, S.M. The Influence of Time Pressure and Accountability on Auditors’ Processing of Nondiagnostic Information. J. Account. Res. 1997, 35, 213–226. [Google Scholar] [CrossRef]

- Guénin-Paracini, H.; Marsch, B.; Marché Paillé, A. Fear and risk in the audit process. Account. Organ. Soc. 2014, 39, 264–288. [Google Scholar] [CrossRef]

- Bakker, A.B.; Demerouti, E. Job Demands—Resources Theory: Taking Stock and Looking Forward. J. Occup. Health Psychol. 2017, 22, 273–285. [Google Scholar] [CrossRef]

- Law, D.; Sweeney, J.; Summers, S. An examination of the influence of contextual and individual variables on public accountants’ exhaustion. In Advances in Accounting Behavioral Research; Arnold, V., Clinton, B., Lillis, A., Roberts, R., Wolfe, C., Wright, S., Eds.; Emerald Group Publishing Limited: Bingley, UK, 2016; Volume 11, pp. 129–153. [Google Scholar] [CrossRef]

- Pierce, B.; Sweeney, J. Cost-Quality Conflict in Audit Firms: An Empirical Investigation. Eur. Account. Rev. 2004, 13, 415–441. [Google Scholar] [CrossRef]

- McNamara, S.M.; Liyanatachchi, G.A. Time Budget pressure and auditor dysfunctional behaviour within an occupational stress model. Account. Bus. Public Interest 2008, 7, 1–43. [Google Scholar]

- Nehme, R.; Al Mutawa, A.; Jizi, M. Dysfunctional Behavior of External Auditors. The collision of time budget and time deadline. Evidence from developing country. J. Dev. Areas 2016, 50, 373–388. [Google Scholar] [CrossRef]

- Baldacchino, P.J.; Tabone, N.; Agius, J.; Bezzina, F. Organizational Culture, Personnel Characteristics and Dysfunctional Audit Behavior. IUP J. Account. Res. Audit Pract. 2016, 15, 34–63. [Google Scholar]

- Sayed Hussin, S.A.H.; Iskandard, T.M.; Saleh, N.M.; Jaffar, R. Professional Skepticism and Auditors’ Assessment of Misstatement Risks: The Moderating Effects of Experience and Time Budget Pressure. Econ. Sociol. 2017, 10, 225–250. [Google Scholar] [CrossRef]

- Umar, M.; Sitorus, S.M.; Surya, R.L.; Shauki, E.R.; Diyanti, V. Pressure, Dysfunctional Behavior, Fraud Detection and Role of Information Technology in the Audit Process. Australas. Account. Bus. Financ. J. 2017, 11, 102–115. [Google Scholar] [CrossRef]

- Larson, L.L.; Meier, H.H.; Poznanski, P.J.; Murff, E.J.T. Concepts and Consequences of Internal Auditor Job Stress. J. Account. Financ. Res. 2004, 12, 35–46. [Google Scholar]

- Larson, L.L.; Tipton Murff, E.J. An Analysis of Job Stress Outcomes among Bank Internal Auditors. Bank Account. Financ. 2006, 19, 39–43. [Google Scholar]

- Lepine, J.A.; Podsakoff, N.P.; Lepine, M.A. A meta-analytic test of the challenge stressor-hindrance stressor framework: An explanation for inconsistent relationships among stressors and performance. Acad. Manag. J. 2005, 48, 764–775. [Google Scholar] [CrossRef]

- Jones, A.; Strand, C.; Wier, B. Healthy Lifestyle as a Coping Mechanism for Role Stress in Public Accounting. Behav. Res. Account. 2010, 22, 21–41. [Google Scholar] [CrossRef]

- Pearsall, M.J.; Ellis, A.P.J.; Stein, J.H. Coping with challenge and hindrance stressors in teams: Behavioral, cognitive, and affective outcomes. Organ. Behav. Hum. Decis. Process. 2009, 109, 18–28. [Google Scholar] [CrossRef]

- Crawford, E.R.; LePine, J.A.; Rich, B.L. Linking job demands and resources to employee engagement and burnout: A theoretical extension and meta-analytic test. J. Appl. Psychol. 2010, 95, 834–848. [Google Scholar] [CrossRef]

- Halbesleben, J.R.B. A meta-analysis of work engagement: Relationships with burnout, demands, resources, and consequences. In Work Engagement: A Handbook of Essential Theory and Research; Bakker, A.B., Leiter, M.P., Eds.; Psychology Press: New York, NY, USA, 2010; pp. 102–117. [Google Scholar]

- Wadsworth, L.L.; Owens, B.P. The effects of social support on work-family enhancement and work-family conflict in the public sector. Public Adm. Rev. 2007, 67, 75–87. [Google Scholar] [CrossRef]

- Kalbers, L.A.; Fogarty, T. Antecedents to Internal Auditor Burnout. J. Manag. Issues 2005, 17, 101–118. [Google Scholar]

- Mock, T.; Wright, A.M. Are Audit Program Plans Risk-Adjusted? Audit. J. Pract. Theory 1999, 18, 55–74. [Google Scholar] [CrossRef]

- Mock, T.; Turner, J.L. Auditor Identification of Fraud Risk Factors and their Impact on Audit Programs. Int. J. Audit. 2005, 9, 59–77. [Google Scholar] [CrossRef]

- Fazli, S.; Muhammaddun, Z.; Ahmad, A. The Effects of Personal Organizational Factors on Role Ambiguity amongst Internal Auditors. Int. J. Audit. 2014, 18, 105–114. [Google Scholar] [CrossRef]

- Gul, F.A.; Ma, S.; Lai, K. Busy Auditors, Partner-Client Tenure, and Audit Quality. Evidence from an Emerging Market. J. Int. Account. Res. 2017, 16, 83–105. [Google Scholar] [CrossRef]

- Herda, D.N.; Lavelle, J.J. The Auditor-Audit Firm Relationship and Its Effect on Burnout and Turnover Intention. Account. Horiz. 2012, 26, 707–723. [Google Scholar] [CrossRef]

- Cannon, N.H.; Herda, D.N. Auditors’ Organizational Commitment, Burnout, and Turnover Intention: A Replication. Behav. Res. Account. 2016, 28, 69–74. [Google Scholar] [CrossRef]

- Hakanen, J.; Bakker, A.B.; Demerouti, E. How dentists cope with their job demands and stay engaged: The moderating role of job resources. Eur. J. Oral Sci. 2005, 113, 479–487. [Google Scholar] [CrossRef]

- Bakker, A.B.; Hakanen, J.J.; Demerouti, E.; Xanthopoulou, D. Job resources boost work engagement particularly when job demands are high. J. Educ. Psychol. 2007, 99, 274–284. [Google Scholar] [CrossRef]

- Xanthopoulou, D.; Bakker, A.B.; Demerouti, E.; Schaufeli, W.B. Reciprocal relationships between job resources, personal resources, and work engagement. J. Vocat. Behav. 2009, 74, 235–244. [Google Scholar] [CrossRef] [Green Version]

- Espinosa-Pike, M.; Barrainkua, I. El efecto de los valores profesionales y la cultura organizativa en la respuesta de los auditores a las presiones de tiempo. Span. J. Financ. Account. 2017, 46, 507–534. [Google Scholar] [CrossRef]

- Pratt, J.; Jiambalvo, J. Relationships between leader behaviors and audit team performance. Account. Organ. Soc. 1981, 6, 133–142. [Google Scholar] [CrossRef]

- Nelson, M.W.; Proell, C.A.; Randel, A.E. Team-Oriented Leadership and Auditors’ Willingness to Raise Audit Issues. Account. Rev. 2016, 91, 1781–1805. [Google Scholar] [CrossRef]

- Yang, L.; Brink, A.G.; Wier, B. The impact of emotional intelligence on auditor judgement. Int. J. Audit. 2018, 22, 83–97. [Google Scholar] [CrossRef]

- Hobfoll, S.E. The influence of culture, community, and the nested-self in the stress process: Advancing conservation of resources theory. Appl. Psychol. 2001, 50, 337–370. [Google Scholar] [CrossRef]

- Driskell, J.E.; Salas, E.; Johnston, J. Does Stress Lead to a Loss of Team Perspective? Group Dyn. Theory Res. Pract. 1999, 3, 291–302. [Google Scholar] [CrossRef]

- Bakker, A.B.; Demerouti, E.; Verbeke, W. Using the Job Demands—Resources model to predict burnout and performance. Hum. Resour. Manag. 2003, 43, 83–104. [Google Scholar] [CrossRef]

- Bakker, A.B.; Demerouti, E.; de Boer, E.; Schaufeli, W.B. Job demands and job resources as predictors of absence duration and frequency. J. Vocat. Behav. 2003, 62, 341–356. [Google Scholar] [CrossRef]

- Jansen in de Wal, J.A.; Van den Beemt, A.; Martens, R.L.; Den Brok, P.J. The relationship between job demands, job resources and teachers’ professional learning: Is it explained by self-determination theory? Stud. Contin. Educ. 2018. [Google Scholar] [CrossRef]

- Van Woerkom, M.; Bakker, A.B.; Nishi, L.H. Accumulative Job Demands and Support for Strength Use: Fine-Tuning the Job Demands-Resources Model Using Conservation of Resources Theory. J. Appl. Psychol. 2016, 101, 141–150. [Google Scholar] [CrossRef]

- De Clercq, D.; Dimov, D.; Belausteguigoitia, I. Perceptions of adverse work conditions and innovative behavior: The buffering roles of relational resources. Entrep. Theory Pract. 2016, 40, 515–542. [Google Scholar] [CrossRef]

- Wright, T.A.; Cropanzano, R. Psychological Well-Being and Job Satisfaction as Predictors of Job Performance. J. Occup. Health Psychol. 2000, 5, 84–94. [Google Scholar] [CrossRef]

- Wright, T.A.; Cropanzano, R.; Bonnet, D.G. The Moderating Role of Employee Positive Well Being on the Relation Between Job Satisfaction and Job Performance. J. Occup. Health Psychol. 2007, 12, 93–104. [Google Scholar] [CrossRef]

- Oswald, A.J.; Proto, E.; Sgroi, D. Happiness and productivity. J. Labor Econ. 2015, 33, 789–822. [Google Scholar] [CrossRef]

- Bryson, A.; Forth, J.; Stokes, L. Does Worker Well-Being Affect Workplace Performance? Department for Business Innovation and Skills. UK. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/366637/bis-14-1120-does-worker-well-being-affect-workplace-performance-final.pdf (accessed on 2 August 2019).

- Eurofound. European Working Conditions Survey Integrated Data File; UK Data Service: Colchester, UK, 2017. [CrossRef]

- Bech, P.; Olsen, L.R.; Kjoller, M.; Rasmussen, N.K. Measuring well-being rather than the absence of distress symptoms: A comparison of the SF-36 Mental Health subscale and the WHO-Five Well-Being Scale. Int. J. Methods Psychiatr. Res. 2003, 12, 85–91. [Google Scholar] [CrossRef]

- Roldán, J.L.; Sánchez-Franco, M.J. Variance-based structural equation modelling: Guidelines for using partial least squares in information systems research. In Research Methodologies, Innovations and Philosophies in Software Systems Engineering and Information Systems; Mora, M., Gelman, O., Steenkamp, A.L., Raisinghani, M., Eds.; IGI Global: Hershey, PA, USA, 2012; pp. 193–221. [Google Scholar]

- Barroso, C.; Carrión, G.C.; Roldán, J.L. Applying maximum likelihood and PLS on different sample sizes: Studies on SERVQUAL model and employee behavior model. In Handbook of Partial Least Squares Concepts, Methods and Applications; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer: Berlin/Heidelberg, Germany, 2010; pp. 427–447. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.M. SmartPLS 3; SmartPLS: Boenningstedt, Germany, 2015. [Google Scholar]

- Chin, W.W. How to write up and report PLS analyses. In Handbook of Partial Least Squares Concepts, Methods and Applications; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer: Dordrecht, The Netherlands, 2010; pp. 645–689. [Google Scholar]

- Carmines, E.G.; Zeller, R.A. Reliability and Validity Assessment; Sage Publications: California, CA, USA; London, UK; New Delhi, India, 1979. [Google Scholar]

- Nunnally, J.C.; Bernstein, I.H.; Berge, J.M.T. Psychometric Theory; McGraw-Hill: New York, NY, USA, 1967. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Market. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modelling. J. Acad. Market. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Kline, R.B. Principles and Practice of Structural Equation Modelling; Guilford Publications: New York, NY, USA, 2015. [Google Scholar]

- Petter, S.; Straub, D.; Rai, A. Specifying formative constructs in information systems research. MIS Q. 2007, 31, 623–656. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modelling. In Modern Methods for Business Research; Marcoulides, G.A., Ed.; Lawrence Erlbaum Associates Publisher: Mahwah, NJ, USA, 1998; Volume 10, pp. 295–336. [Google Scholar]

- Hair, J.F., Jr.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V. Partial least squares structural equation modeling (PLS-SEM). An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- NIOSH. Fundamentals of Total Worker Health Approaches: Essential Elements for Advancing Worker Safety, Health, and Well-Being; Department of Health and Human Services, Centers for Disease Control and Prevention, National Institute for Occupational Safety and Health: Cincinnati, OH, USA, 2017. Available online: https://www.cdc.gov/niosh/docs/2017-112/pdfs/2017_112.pdf?id=10.26616/NIOSHPUB2017112. (accessed on 12 September 2018).

- Van der Doef, M.; Maes, S. The job demand-control (-support) model and psychological well-being: A review of 20 years of empirical research. Work Stress 1999, 13, 87–114. [Google Scholar] [CrossRef]

- Bakker, A.B.; Demerouti, E. J Multiple levels in job demands-resources theory: Implicationsfor employee well-being and performance. In Handbook of Well-Being; Diener, E., Oishi, S., Tay, L., Eds.; DEF Publishers: Salt Lake City, UT, USA, 2018. [Google Scholar]

{kind=link}

{kind=link}

| Variable | Loads | Weights | VIF 1 | |||

|---|---|---|---|---|---|---|

| 1 | Quantitative demands | n/a | n/a | |||

| Your job involves working at very high speed | 0.067 | 1.600 | ||||

| Your job involves working with tight deadlines | 0.054 | 1.571 | ||||

| Enough time to get the job done | 0.964 | ** | 1.086 | |||

| 2 | Qualitative demands | n/a | n/a | |||

| Emotionally disturbing situations | 0.432 | ** | 1.061 | |||

| You know what is expected of you at work | 0.854 | ** | 1.010 | |||

| Your work requires you to hide your feelings | 0.041 | 1.052 | ||||

| 3.1 | Application of personal skills | 0.186 | 1.014 | |||

| Short repetitive tasks of less than 10 minutes | 0.234 | 1.044 | ||||

| Solving unforeseen problems on your own | 0.419 | 1.150 | ||||

| Monotonous tasks | 0.889 | 1.058 | ||||

| Learning new things | −0.027 | 1.149 | ||||

| 3.2 | Autonomy in planning activities | 0.961 | ** | 1.014 | ||

| Ability to choose your order of tasks | 0.045 | 1.426 | ||||

| Ability to choose your methods of work | −0.120 | 1.469 | ||||

| Ability to choose your speed or rate of work | 0.435 | 1.327 | ||||

| You are consulted before objectives are set for your work | 0.175 | 1.373 | ||||

| You have a say in the choice of your work colleagues | −0.081 | 1.291 | ||||

| You are able to apply your own ideas in your work | 0.543 | ** | 1.545 | |||

| You can influence decisions that are important to your work | 0.334 | * | 1.712 | |||

| 4.1 | Support and guidance from superiors | 0.871 | ** | 1.097 | ||

| Your manager helps and supports you | 0.131 | 1.457 | ||||

| Your boss respects you as a person | 0.530 | ** | 1.748 | |||

| Your boss gives you recognition | 0.293 | 1.897 | ||||

| Your boss is successful in getting people to work together | 0.004 | 2.123 | ||||

| Your boss is helpful in getting the job done | −0.065 | 1.779 | ||||

| Your boss provides useful feedback | 0.192 | 2.047 | ||||

| Your boss encourages and supports your development | 0.148 | 2.667 | ||||

| 4.2 | Support from other colleagues | 0.297 | 1.097 | |||

| Your colleagues help and support you | 1.000 | ** | 1.000 | |||

| 5 | Subjective well-being | n/a | ||||

| I have felt cheerful and in a good mood | 0.848 | ** | ||||

| I have felt calm and relaxed | 0.857 | ** | ||||

| I have felt active and vigorous | 0.857 | ** | ||||

| I woke up feeling fresh and rested | 0.844 | ** | ||||

| My daily life has been filled with things that interest me | 0.778 | ** | ||||

| Variables | Cronbach’s Alpha 1 | rho_A 1 | Composite Reliability 1 | Average Variance Extracted (AVE) 2 | |||

|---|---|---|---|---|---|---|---|

| Subjective well-being | 0.893 | 0.894 | 0.921 | 0.701 | |||

| Discriminant validity | |||||||

| Heterotrait–Monotrait Ratio HTMT3 | |||||||

| Skills application | Co-workers support | Superiors support | Task autonomy | Subjective well-being | Qualitative demands | Quantitative demands | |

| Skills application | |||||||

| Co-workers support | 0.191 | ||||||

| Superiors support | 0.130 | 0.501 | |||||

| Task autonomy | 0.369 | 0.266 | 0.460 | ||||

| Subjective well-being | 0.174 | 0.168 | 0.345 | 0.277 | |||

| Qualitative demands | 0.498 | 0.327 | 0.389 | 0.520 | 0.491 | ||

| Quantitative demands | 0.388 | 0.131 | 0.241 | 0.227 | 0.366 | 0.622 | |

| R2 Subjective Well-Being: 0.223 Relationship | Original Sample (O) | T Statistics | P Value | 2.5% | 97.5% | Significative | |

|---|---|---|---|---|---|---|---|

| Direct effects | |||||||

| Quantitative demands -> Subjective well-being | −0.221 | 5.695 | 0.000 | *** | −0.292 | −0.141 | Sig. |

| Qualitative demands -> Subjective well-being | −0.098 | 2.494 | 0.013 | * | −0.170 | −0.015 | Sig. |

| Task control -> Subjective well-being | 0.123 | 3.284 | 0.001 | *** | 0.049 | 0.194 | Sig. |

| Social support -> Subjective well-being | 0.248 | 6.073 | 0.000 | *** | 0.166 | 0.325 | Sig. |

| Task control*Qualitative demands. -> Subjective well-being | 0.020 | 0.429 | 0.668 | −0.077 | 0.110 | No Sign. | |

| Task control*Quantitative demands. -> Subjective well-being | −0.002 | 0.050 | 0.960 | −0.095 | 0.092 | No Sign. | |

| Social support*Qualitative D. -> Subjective well-being | 0.025 | 0.645 | 0.519 | −0.055 | 0.097 | No Sign. | |

| Social support*Quantitative D. -> Subjective well-being | −0.047 | 1.135 | 0.257 | −0.129 | 0.032 | No Sign. |

| R2 Subjective Well-Being: 0.203; R2 Task Control: 0.116; R2 Social Support: 0.077 Relationship | Original Sample (O) | T Statistics | P Value | 2.5% | 97.5% | Significative | |

|---|---|---|---|---|---|---|---|

| Direct Effects | |||||||

| Quantitative demands -> Subjective well-being | −0.269 | 6.057 | 0.000 | *** | −0.349 | −0.171 | Sig. |

| Quantitative demands -> Task control | −0.193 | 5.183 | 0.000 | *** | −0.263 | −0.116 | Sig. |

| Quantitative demands -> Social support | −0.179 | 4.003 | 0.000 | *** | −0.265 | −0.090 | Sig. |

| Qualitative demands -> Subjective well-being | −0.157 | 3.570 | 0.000 | *** | −0.236 | −0.062 | Sig. |

| Qualitative demands -> Task control | −0.223 | 5.870 | 0.000 | *** | −0.291 | −0.146 | Sig. |

| Qualitative demands -> Social support | −0.165 | 3.298 | 0.001 | *** | −0.258 | −0.058 | Sig. |

| Task control -> Subjective well-being | 0.108 | 2.629 | 0.009 | ** | 0.026 | 0.188 | Sig. |

| Social support -> Subjective well-being | 0.239 | 5.586 | 0.000 | *** | 0.156 | 0.322 | Sig. |

| Indirect Effects | |||||||

| Quantitative demands -> Subjective demands | −0.064 | 4.002 | 0.000 | *** | −0.098 | −0.036 | Sig. |

| Qualitative demands -> Subjective demands | −0.064 | 3.748 | 0.000 | *** | −0.098 | −0.033 | Sig. |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Molina-Sánchez, H.; Ariza-Montes, A.; Ortiz-Gómez, M.; Leal-Rodríguez, A. The Subjective Well-Being Challenge in the Accounting Profession: The Role of Job Resources. Int. J. Environ. Res. Public Health 2019, 16, 3073. https://doi.org/10.3390/ijerph16173073

Molina-Sánchez H, Ariza-Montes A, Ortiz-Gómez M, Leal-Rodríguez A. The Subjective Well-Being Challenge in the Accounting Profession: The Role of Job Resources. International Journal of Environmental Research and Public Health. 2019; 16(17):3073. https://doi.org/10.3390/ijerph16173073

Chicago/Turabian StyleMolina-Sánchez, Horacio, Antonio Ariza-Montes, Mar Ortiz-Gómez, and Antonio Leal-Rodríguez. 2019. "The Subjective Well-Being Challenge in the Accounting Profession: The Role of Job Resources" International Journal of Environmental Research and Public Health 16, no. 17: 3073. https://doi.org/10.3390/ijerph16173073