New Zealand’s Drug Development Industry

Abstract

:1. Introduction

- To develop a theoretical framework for evaluating the drug development industry in NZ

- To critically evaluate the expertise of this industry in NZ

- To identify the enablers and barriers to the use and/or development of NZ expertise and the factors that have allowed this industry to arise

- To assess the potential economic benefits to NZ of policies supporting the drug discovery and development industry

2. Methods

2.1. Revenue fromthe Successful Development of a NZ-Discovered Medicine

2.2. Revenue from Clinical Research

{kind=link}

| Parameter | Assumption | Basis of the assumption |

|---|---|---|

| Timing of out-license deal | Pre-clinical (i.e., without clinical data) | N/A |

| Local ownership when deal agreed | 100% | N/A |

| Upfront payment | $6.5 million | Research by Kessel and Frank [17] |

| Projected global peak sales | $350 million | N/A |

| Time of global peak sales | Year 10 after product launch | Data from Danzon and Kim [18], Grabowski [19] and Hoyle [20] |

| Duration of sales | 20 years | Data from Danzon and Kim [18], Grabowski [19] and Hoyle [20] |

| Sales for Year 1 to Year 20 as a percentage of peak sales | Bell-shaped curve, as described in Table 2 | Data from Rasmussen [21] and Cook [22] |

| Probability that a self-originated compound is approved for sale | 16% | Research by DiMasi and Feldman [23] |

| Average gross profit on sales | 50% | Data from Rasmussen [21] |

| Royalty payments on sales profit | 10% | Research by Kessel and Frank [17] |

3. Results and Discussion

3.1. Revenue from the Successful Development of a NZ-discovered Medicine

| Out-license deal after pre-clinical stage | Percent probability of successful completion | Project sales as percent of peak global sales (%) | Projected sales/milestone payment per year ($ million) | Projected profit (50% of sales) | Projected profit multiplied by percent probability of success | Probability based payments to NZ ($ million) |

|---|---|---|---|---|---|---|

| Upfront Payment | 100 | N/A | 6.500 | N/A | 6.500 | 6.500 |

| Successful Phase I | 71 | N/A | 0 | N/A | 0 | 0 |

| Successful Phase II | 31.95 | N/A | 0 | N/A | 0 | 0 |

| Successful Phase III and registration dossier submitted | 20.45 | N/A | 0 | N/A | 0 | 0 |

| Approval of registration dossier | 19.02 | N/A | 0 | N/A | 0 | 0 |

| Year 1 sales | 16 | 30 | 105.000 | 52.500 | 8.400 | 0.840 |

| Year 2 sales | 16 | 40 | 140.000 | 70.000 | 11.200 | 1.120 |

| Year 3 sales | 16 | 50 | 175.000 | 87.500 | 14.000 | 1.400 |

| Year 4 sales | 16 | 60 | 210.000 | 105.000 | 16.800 | 1.680 |

| Year 5 sales | 16 | 70 | 245.000 | 122.500 | 19.600 | 1.960 |

| Year 6 sales | 16 | 80 | 280.000 | 140.000 | 22.400 | 2.240 |

| Year 7 sales | 16 | 85 | 297.500 | 148.750 | 23.800 | 2.380 |

| Year 8 sales | 16 | 90 | 315.000 | 157.500 | 25.200 | 2.520 |

| Year 9 sales | 16 | 95 | 332.500 | 166.250 | 26.600 | 2.660 |

| Year 10 sales | 16 | 100 | 350.000 | 175.000 | 28.000 | 2.800 |

| Year 11 sales | 16 | 90 | 315.000 | 157.500 | 25.200 | 2.520 |

| Year 12 sales | 16 | 80 | 280.000 | 140.000 | 22.400 | 2.240 |

| Year 13 sales | 16 | 75 | 262.500 | 131.250 | 21.000 | 2.100 |

| Year 14 sales | 16 | 70 | 245.000 | 122.500 | 19.600 | 1.960 |

| Year 15 sales | 16 | 60 | 210.000 | 105.000 | 16.800 | 1.680 |

| Year 16 sales | 16 | 50 | 175.000 | 87.500 | 14.000 | 1.400 |

| Year 17 sales | 16 | 40 | 140.000 | 70.000 | 11.200 | 1.120 |

| Year 18 sales | 16 | 35 | 122.500 | 61.250 | 9.800 | 0.980 |

| Year 19 sales | 16 | 30 | 105.000 | 52.500 | 8.400 | 0.840 |

| Year 20 sales | 16 | 25 | 87.500 | 43.750 | 7.000 | 0.700 |

| Total ($ million) | 4,399.000 | 2,196.250 | 357.900 | 41.640 |

| Sensitivity analysis | Detail and total revenue to NZ ($ million) | |||||

|---|---|---|---|---|---|---|

| Lower end of the range | Original calculation | Upper end of the range | ||||

| Analysis detail | Revenue to NZ ($ million) | Analysis detail | Revenue to NZ ($ million) | Analysis detail | Revenue to NZ ($ million) | |

| Later out licence deal | N/A | N/A | Pre-clinical | 41.640 | Post ph I Post ph II | 68.347 140.599 |

| Value of peak sales | $50 million | 11.520 | $350 million | 41.640 | $1,000 million | 106.900 |

| Level of royalty payments | 8% of sales profit | 33.572 | 10% of sales profit | 41.640 | 12% of sales profit | 47.608 |

| Percent probability of approval of registration dossier | 10.0% | 28.463 | 16.0% | 41.640 | 30.0% | 72.388 |

| Sales profitability | 40% of sales value | 33.312 | 50% of sales value | 41.640 | 60% of sales value | 49.968 |

| Cummulative sales | $3,294.4 million | 32.894 | $4,399.0 million | 41.640 | $5,278.8 million | 48.730 |

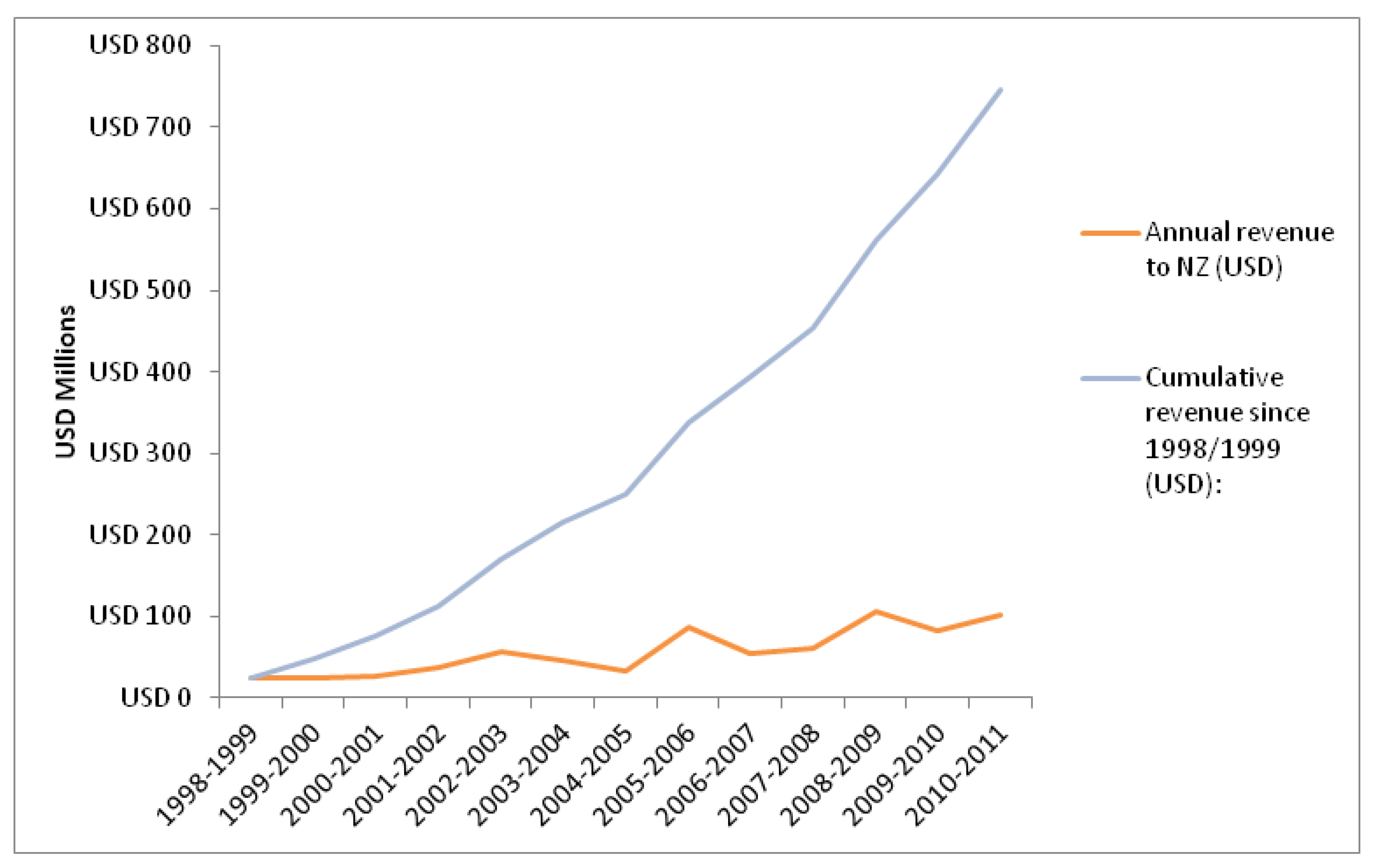

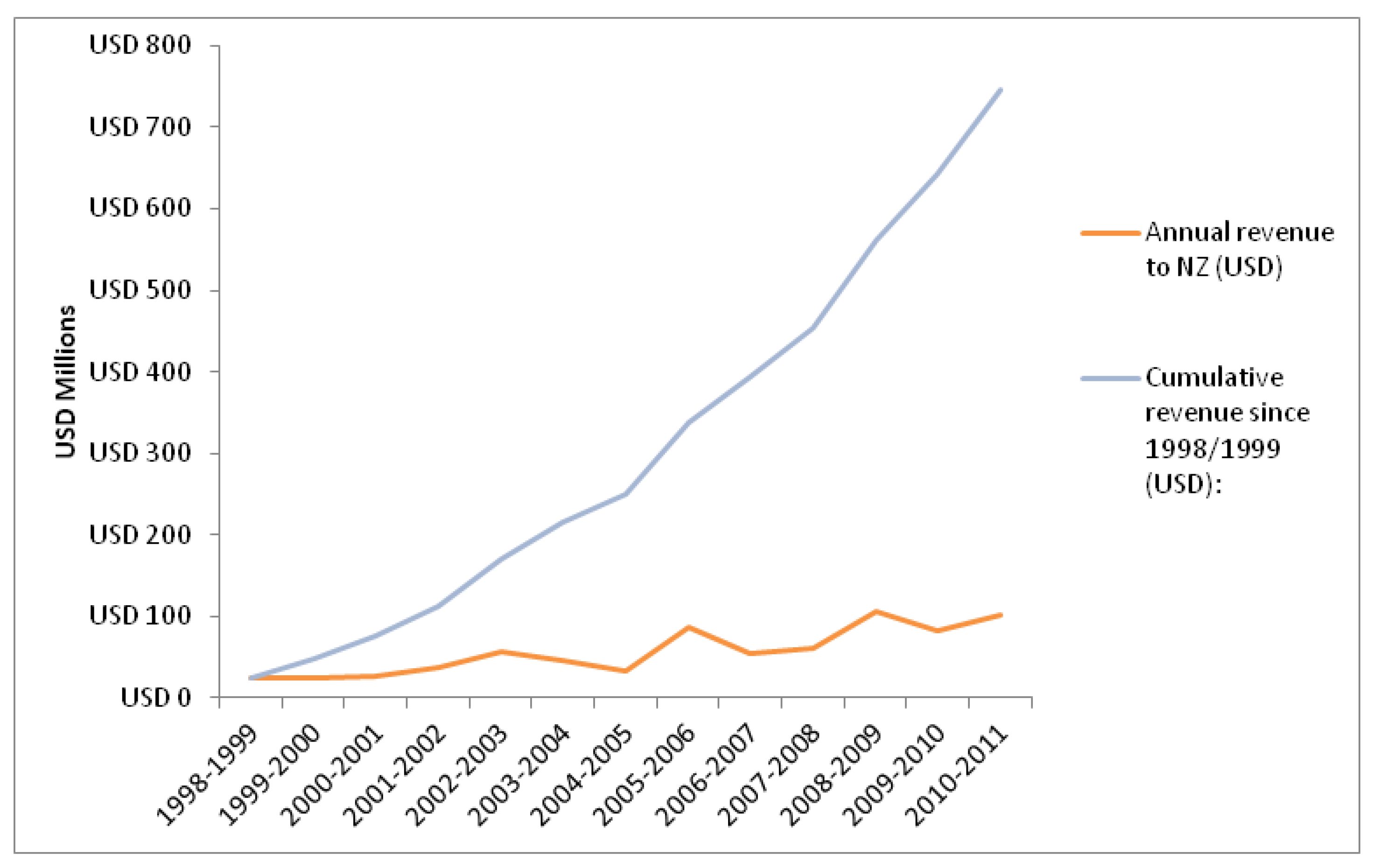

3.2. Revenue from Clinical Research

3.3. Discussion

4. Conclusions

Acknowledgements

Conflicts of Interest

References

- Garofolo, W.; Garofolo, F. Global outsourcing. Bioanalysis 2010, 2, 149–152. [Google Scholar] [CrossRef]

- Tralau-Stewart, C.J.; Wyatt, C.A.; Kleyn, D.E.; Ayad, A. Drug discovery: New models for industry-academic partnerships. Drug Discov. Today 2009, 14, 95–101. [Google Scholar] [CrossRef]

- Bennani, Y.L. Drug discovery in the next decade: Innovation needed ASAP. Drug Discov. Today 2011, 16, 779–792. [Google Scholar] [CrossRef]

- Kaitin, K.I. Deconstructing the drug development process: The new face of innovation. Clin. Pharmacol. Ther. 2010, 87, 356–361. [Google Scholar] [CrossRef]

- Garnier, J.P. Rebuilding the R&D engine in big pharma. Harv. Bus. Rev. 2008, 86, 68–76. [Google Scholar]

- Schweitzer, S.O. Pharmaceutical Economics and Policy, 2nd ed.; Oxford University Press: New York, NY, USA, 2007. [Google Scholar]

- Branston, J.R.; Rubini, L.; Sugden, R.; Wilson, J.R. Healthy Governance: Economic Policy and the Health Industry Model. In Health Policy and High-Tech Industrial Development; di Tommaso, M.R., Schweitzer, S.O., Eds.; Edward Elgar Publishing Limited: London, UK, 2005; pp. 45–58. [Google Scholar]

- Frew, S.E.; Sammut, S.M.; Siu, W.W.; Daar, A.S.; Singer, P.A. The role of the domestic private sector in developing countries for addressing local health needs. Int. J. Biotechnol. 2006, 8, 91–102. [Google Scholar]

- Al-Bader, S.; Masum, H.; Simiyu, K.; Daar, A.S.; Singer, P.A. Science-based health innovation in sub-Saharan Africa. BMC Int. Health Hum. Rights 2010, 10. [Google Scholar] [CrossRef]

- Sloan, F.A.; Hsieh, C.-R. Conclusions and Policy Implications. In Pharmaceutical Innovation: Incentives, Competition, and Cost-Benefit Analysis in International Perspective; Sloan, F.A., Hsieh, C.-R., Eds.; Cambridge University Press: New York, NY, USA, 2007. [Google Scholar]

- Rosenberg-Yunger, Z.R.S.; Daar, A.S.; Singer, P.A.; Martin, D.K. Healthcare sustainability and the challenges of innovation to biopharmaceuticals in Canada. Health Policy 2008, 87, 359–368. [Google Scholar] [CrossRef]

- Vernon, J.A.; Golec, J.H. Correctly measuring drug development risk: A public policy imperative. Expert Rev. Pharmacoecon. Outcomes Res. 2011, 11, 1–3. [Google Scholar] [CrossRef]

- Organisation for Economic Co-Operation and Development, Reviews of Innovation Policy— New Zealand; Organisation for Economic Co-Operation and Development: Paris, France, 2007.

- Ministry of Research Science and Technology, New Zealand. Roadmaps Science—Biotechnology Research: A Guide for New Zealand Science Activity; Ministry of Research Science and Technology: Wellington, New Zealand, 2007; pp. 1–74.

- Ministry of Research Science and Technology, New Zealand, Our Strategy 2008–2011. MoRST; Ministry of Research Science and Technology: Wellington, New Zealand, 2008.

- Denny, W. Conversation Regarding the Costs per Year for a Medicinal Chemist or Biologist, Including Salary, Rent, Equipment and Consumables. Personal communication, University of Auckland: New Zealand, 2011. [Google Scholar]

- Kessel, M.; Frank, F. A better prescription for drug-development financing. Nat. Biotechnol. 2007, 25, 859–866. [Google Scholar] [CrossRef]

- Danzon, P.M.; Kim, J.D. The Life-Cycle of Pharmaceuticals: A Cross-National Persective; Office of Health Economics: London, UK, 2002. [Google Scholar]

- Grabowski, H.; Vernon, J.; DiMasi, J.A. Returns on research and development for 1990s new drug introductions. Pharm. Econ. 2002, 20 (Suppl. 3), 11–29. [Google Scholar] [CrossRef]

- Hoyle, M. Accounting for the drug life cycle and future drug prices in cost-effectiveness analysis. Pharm. Econ. 2011, 29, 1–15. [Google Scholar] [CrossRef]

- Rasmussen, B. Innovation and Commercialisation in the Biopharmaceutical Industry; Edward Elgar Publishing Limited: Cheltenham, UK, 2010; pp. 1–326. [Google Scholar]

- Cook, A.G. Forecasting for the Pharmaceutical Industry: Models for New Product and in-Market Forecasting and How to Use Them; Gower Publishing Company: Aldershot, UK, 2006; pp. 1–141. [Google Scholar]

- DiMasi, J.A.; Feldman, L.; Seckler, A.; Wilson, A. Trends in risks associated with new drug development: Success rates for investigational drugs. Clin. Pharmacol. Ther. 2010, 87, 272–277. [Google Scholar] [CrossRef]

- Tuunainen, J. High-tech hopes: Policy objectives and business reality in the biopharmaceutical industry. Sci. Public Policy 2011, 38, 338–348. [Google Scholar] [CrossRef]

- Enzing C, Reiss T. The effectiveness of biotechnology policies in Europe. Int. J. Biotechnol. 2008, 10, 327–340. [Google Scholar] [CrossRef]

- March-Chordà, I.; Yagüe-Perales, R.M. Biopharma business models in Canada. Drug Discov. Today 2011, 16, 54–58. [Google Scholar]

- Malik, T. Real option as strategic technology uncertainty reduction mechanism: Inter-firm investment strategy by pharmaceuticals. Technol. Anal. Strateg. Manag. 2011, 23, 489–507. [Google Scholar] [CrossRef]

- Marks, A.R. Repaving the road to biomedical innovation through academia. Sci. Transl. Med. 2011, 3, 1–3. [Google Scholar] [CrossRef]

- Handen, J.S. Drug Discovery in the Modern Age: How We Got Here and What Does it Mean? In Industrialisation of Drug Discovery, 1st ed.; Handen, J.S., Ed.; CRC Press: Boca Raton, FL, USA, 2005; pp. 1–12. [Google Scholar]

- Teague, S.J. Learning lessons from drugs that have recently entered the market. Drug Discov. Today 2011, 16, 398–411. [Google Scholar] [CrossRef]

- Swinney, D.C.; Anthony, J. How were new medicines discovered? Nat. Rev. Drug Discov. 2011, 10, 507–519. [Google Scholar] [CrossRef]

- NZBIO, The Importance of New Zealand’s Human Therapeutics Sector in Future Economic Growth; NZBIO: Wellington, New Zealand, 2009.

- Karlberg, J.P.E. Trends in disease focus of drug development. Nat. Rev. Drug Discov. 2008, 7, 639–640. [Google Scholar] [CrossRef]

- Arrowsmith, J. A decade of change. Nat. Rev. Drug Discov. 2012, 11, 17–18. [Google Scholar] [CrossRef]

- Lockhart, M.; Babar, Z.-U.-D.; Garg, S. Evaluation of policies to support drug development in New Zealand. Health Policy 2010, 96, 108–117. [Google Scholar] [CrossRef]

- Kaitin, K.I.; DiMasi, J.A. Pharmaceutical innovation in the 21st century: New drug approvals in the first decade, 2000–2009. Clin. Pharmacol. Ther. 2011, 89, 183–188. [Google Scholar] [CrossRef]

- Health Committee, Inquiry into Improving New Zealand’s Environment to Support Innovation through Clinical Trials; New Zealand Parliament: Wellington, New Zealand, 2011.

- Clinical Trials Action Group, Clinically Competitive: Boosting the Business of Clinical Trials in Australia; National Libraries of Australia: Canberra, Australia, 2011.

- Lockhart, M.M.; Babar, Z.-U.-D.; Garg, S. Clinical trials in New Zealand: Progress, people, and policies. Drug Dev. Res. 2010, 72, 229–304. [Google Scholar]

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Lockhart, M.M.; Babar, Z.-U.-D.; Carswell, C.; Garg, S. New Zealand’s Drug Development Industry. Int. J. Environ. Res. Public Health 2013, 10, 4339-4351. https://doi.org/10.3390/ijerph10094339

Lockhart MM, Babar Z-U-D, Carswell C, Garg S. New Zealand’s Drug Development Industry. International Journal of Environmental Research and Public Health. 2013; 10(9):4339-4351. https://doi.org/10.3390/ijerph10094339

Chicago/Turabian StyleLockhart, Michelle Marie, Zaheer-Ud-Din Babar, Christopher Carswell, and Sanjay Garg. 2013. "New Zealand’s Drug Development Industry" International Journal of Environmental Research and Public Health 10, no. 9: 4339-4351. https://doi.org/10.3390/ijerph10094339