Lambda Value at Risk and Regulatory Capital: A Dynamic Approach to Tail Risk

Abstract

:1. Introduction

2. Method

2.1. Current Risk Measures and

2.2. The Proposal of Estimation: A Dynamic Benchmark Approach

2.3. Backtesting Method

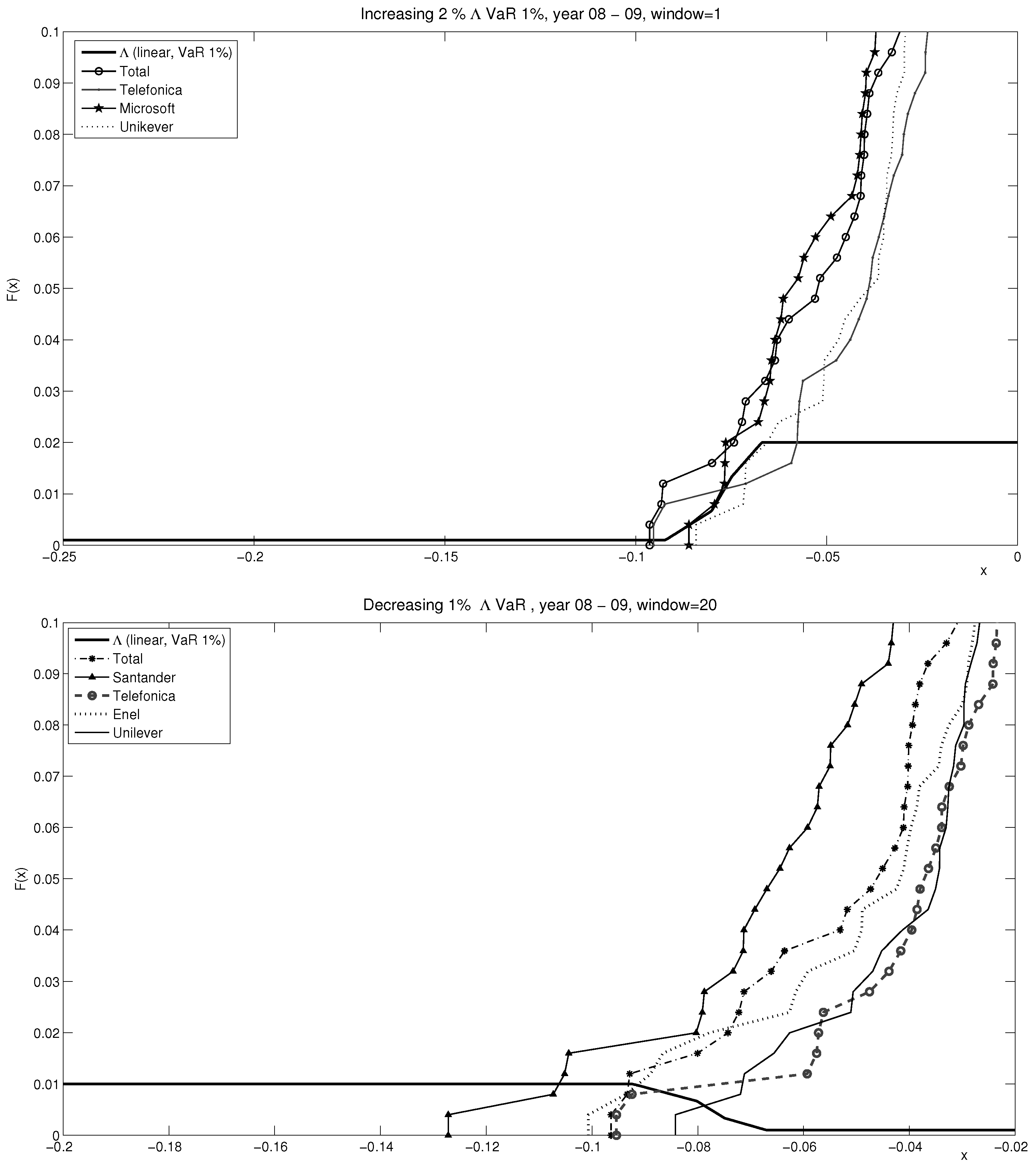

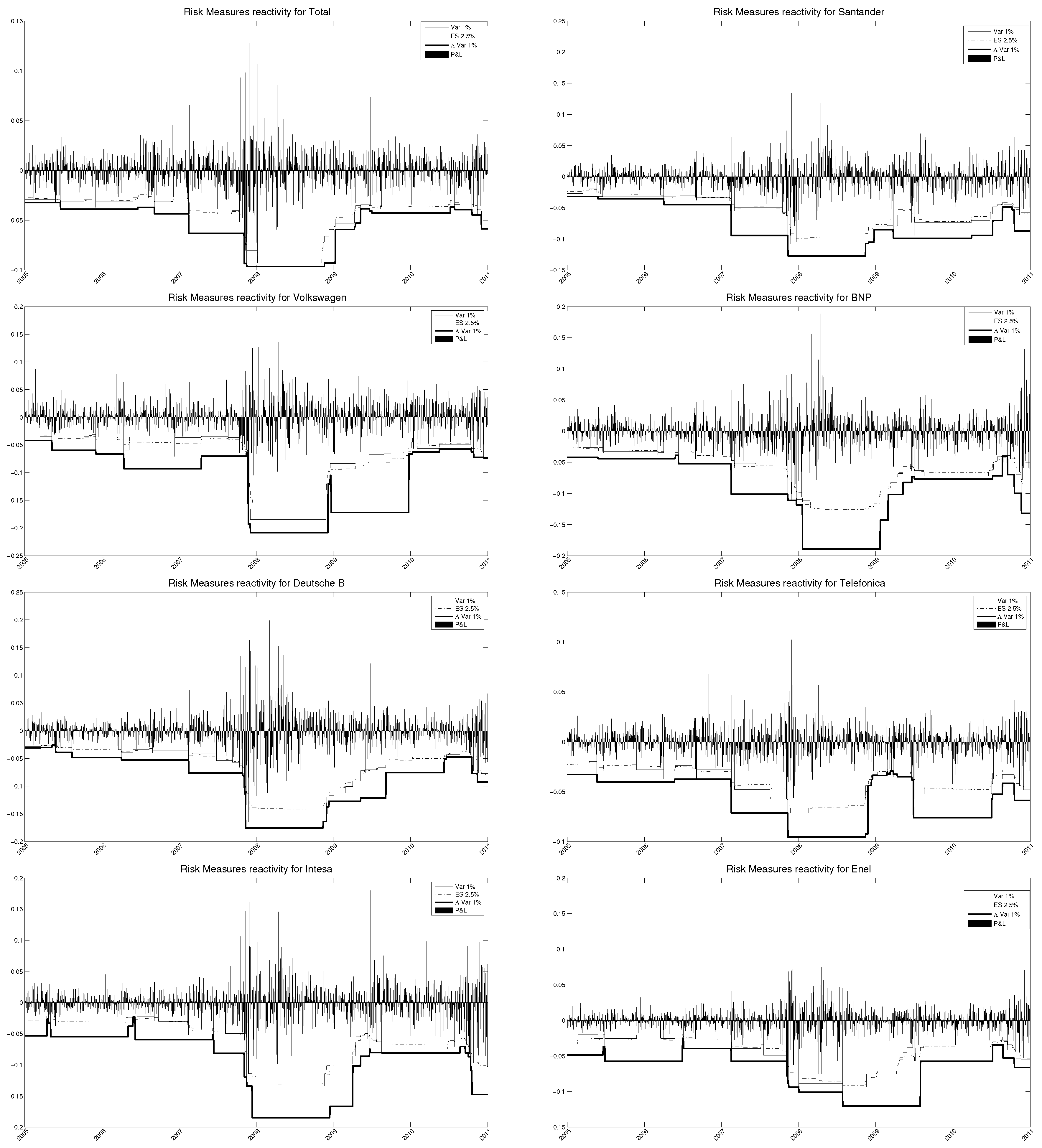

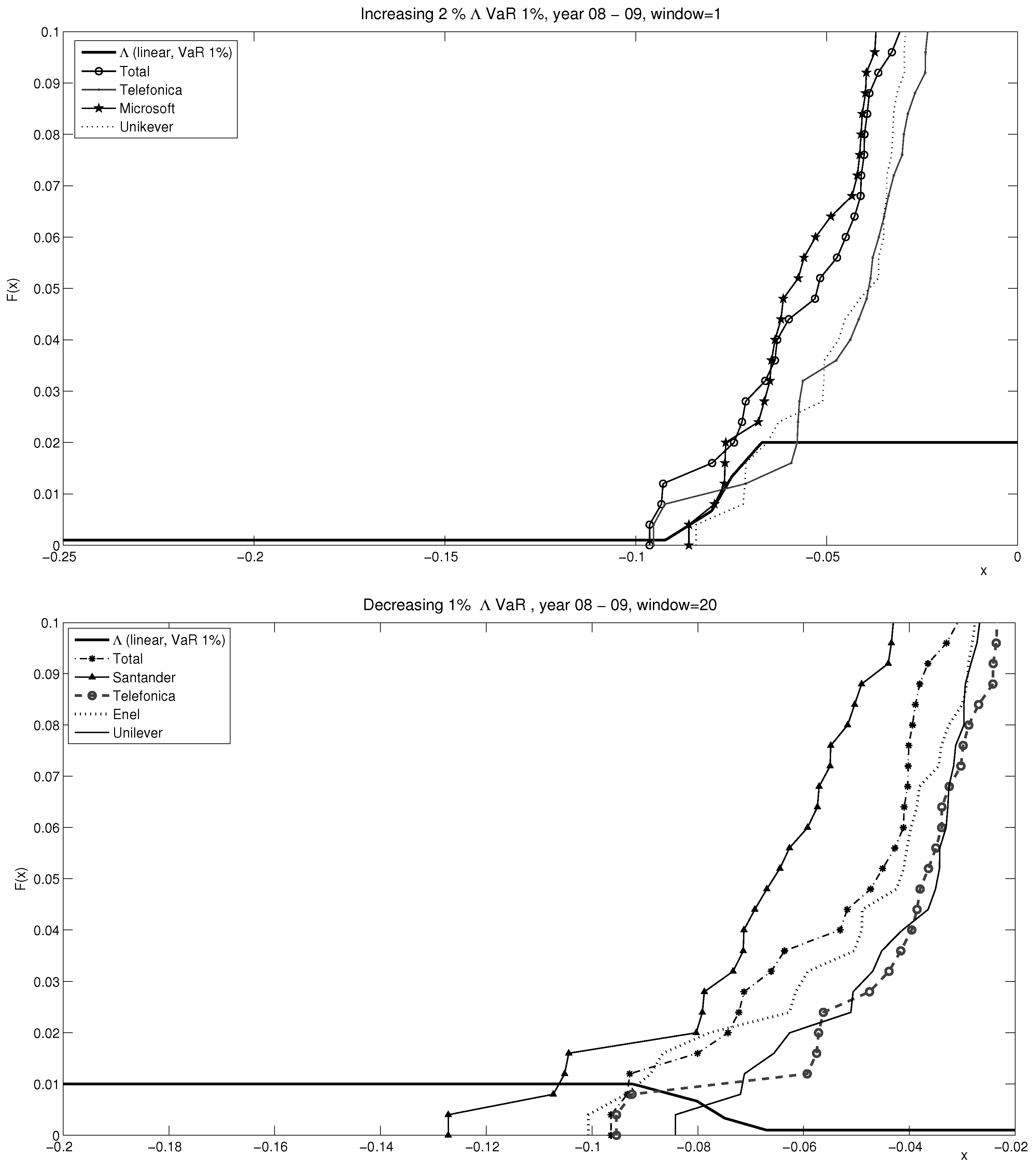

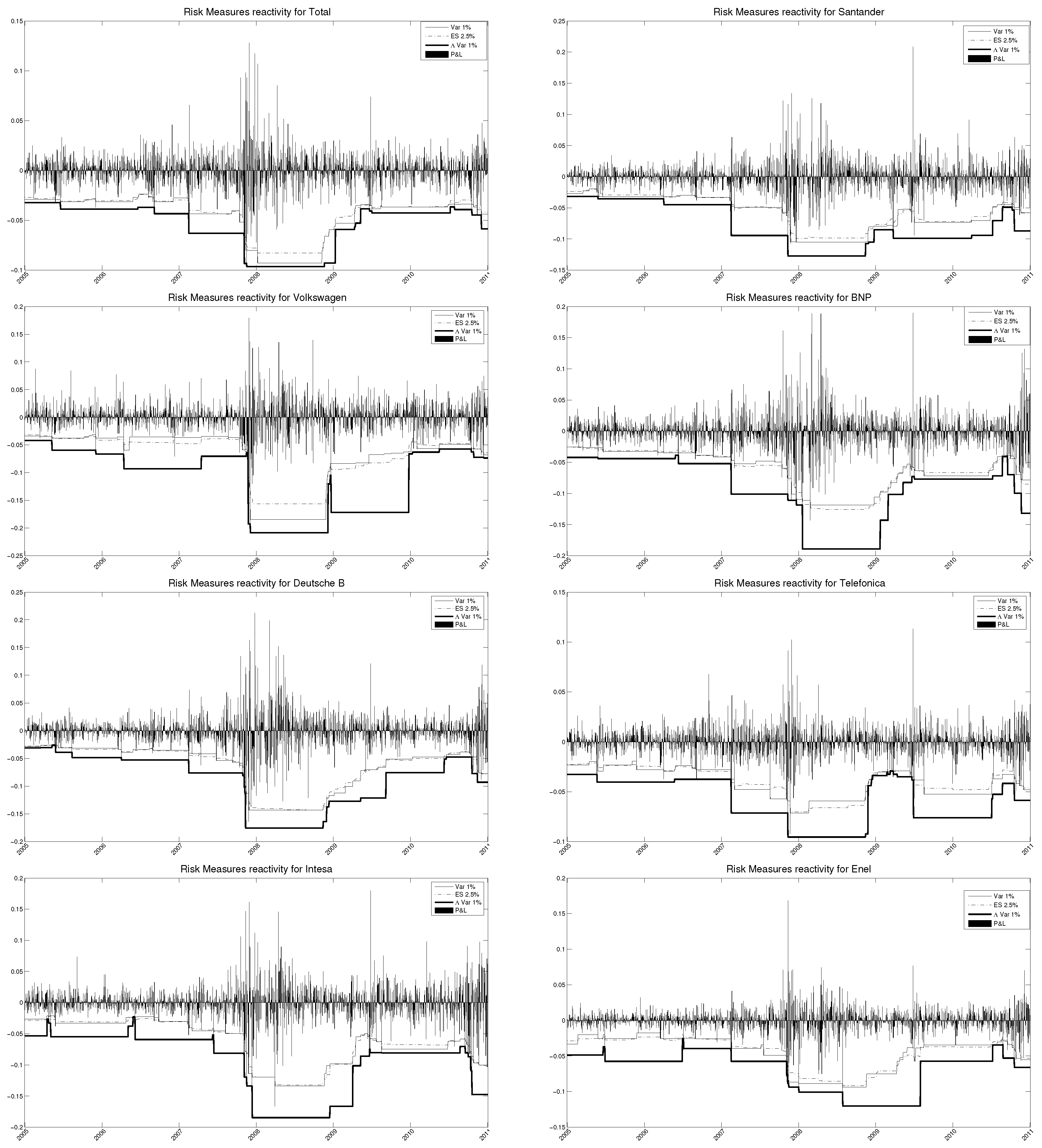

3. Empirical Analysis

Risk Measures Computation, Backtesting, and Comparison

4. Conclusions

Author Contributions

Conflicts of Interest

Appendix A. Descriptive Statistics of the Dataset

{kind=link}

{kind=link}

| 2006 | 2007 | |||||||||||||||||

| Min Daily Return | Max Daily Return | Annual Mean | Annual std | Skewness | Kurtosis | JB | H | p-Value | Min Daily Return | Max Daily Return | Annual Mean | Annual std | Skewness | Kurtosis | JB | H | p-Value | |

| FP FP | 0.0334 | 0.0326 | 0.1807 | 3.6305 | 10.8004 | R | 0.0119 | 0.0458 | 0.0131 | 0.2053 | 0.1085 | 3.6228 | 4.5312 | A | 0.0828 | |||

| SAN SQ | 0.0340 | 0.2265 | 0.1764 | 3.6016 | 8.8246 | R | 0.0194 | 0.0407 | 0.0157 | 0.2112 | 3.7085 | 5.5288 | A | 0.0540 | ||||

| VOW3 GY | 0.0875 | 0.5331 | 0.2884 | 0.6285 | 6.8101 | 167.6764 | R | 0.0010 | 0.0775 | 0.6116 | 0.3010 | 6.7672 | 148.0897 | R | 0.0010 | |||

| BNP FP | 0.0411 | 0.1838 | 0.2157 | 3.2898 | 1.2895 | A | 0.4873 | 0.0501 | 0.2649 | 0.0604 | 3.7158 | 5.4897 | A | 0.0548 | ||||

| DBK GY | 0.0416 | 0.2132 | 0.2055 | 3.7980 | 12.4206 | R | 0.0084 | 0.0419 | 0.2347 | 0.0817 | 3.8776 | 8.3019 | R | 0.0222 | ||||

| TEF SQ | 0.0362 | 0.2387 | 0.1532 | 4.6203 | 29.3396 | R | 0.0010 | 0.0675 | 0.3186 | 0.2018 | 0.3926 | 5.8767 | 92.6257 | R | 0.0010 | |||

| ISP IM | 0.0733 | 0.1883 | 0.2139 | 0.4339 | 6.5060 | 135.8837 | R | 0.0010 | 0.0328 | 0.1891 | 5.0088 | 44.2408 | R | 0.0010 | ||||

| ENEL IM | 0.0323 | 0.1554 | 0.1322 | 12.4250 | 978.7849 | R | 0.0010 | 0.0243 | 0.0257 | 0.1501 | 4.3647 | 30.6449 | R | 0.0010 | ||||

| C UN | 0.0300 | 0.0146 | 0.1619 | 5.0078 | 48.6896 | R | 0.0010 | 0.0680 | 0.3012 | 6.1061 | 101.4809 | R | 0.0010 | |||||

| MSFT UW | 0.0560 | 0.0305 | 0.2274 | 27.9181 | 6714.7750 | R | 0.0010 | 0.0849 | 0.1039 | 0.2299 | 0.6769 | 7.4973 | 229.7779 | R | 0.0010 | |||

| RBS LN | 0.0400 | 0.1195 | 0.1571 | 0.3047 | 4.3665 | 23.3198 | R | 0.0014 | 0.0879 | -0.8447 | 0.5197 | 94.7552 | 90038.2373 | R | 0.0010 | |||

| ULVR LN | 0.0453 | 0.1291 | 0.1714 | 7.4596 | 218.1719 | R | 0.0010 | 0.0568 | 0.2977 | 0.2086 | 0.5671 | 4.4899 | 36.5219 | R | 0.0010 | |||

| Indexes’ Statistics | Indexes’ Statistics | |||||||||||||||||

| SPX Index | 0.0220 | 0.0215 | 0.1234 | 3.5449 | 5.5002 | A | 0.0545 | 0.0313 | 0.1644 | 4.9352 | 53.5407 | R | 0.0010 | |||||

| SX5E Index | 0.0264 | 0.1389 | 0.1461 | 4.2074 | 24.3246 | R | 0.0013 | 0.0289 | 0.0622 | 0.1591 | 3.4765 | 4.1959 | A | 0.0965 | ||||

| UKX Index | 0.0237 | 0.1210 | 0.1225 | 4.0389 | 12.6325 | R | 0.0080 | 0.0326 | 0.1830 | 4.3609 | 26.6163 | R | 0.0010 | |||||

| 2008 | 2009 | |||||||||||||||||

| Min Daily Return | Max Daily Return | Annual Mean | Annual std | Skewness | Kurtosis | JB | H | p-Value | Min Daily Return | Max Daily Return | Annual Mean | Annual std | Skewness | Kurtosis | JB | H | p-Value | |

| FP FP | 0.1279 | 0.4800 | 0.5332 | 6.8048 | 162.6412 | R | 0.0010 | 0.0854 | 0.0904 | 0.2942 | 0.1161 | 5.1276 | 47.7145 | R | 0.0010 | |||

| SAN SQ | 0.1339 | 0.5410 | 0.1200 | 6.0451 | 97.1911 | R | 0.0010 | 0.1257 | 0.5008 | 0.4566 | 0.2267 | 5.6305 | 74.2226 | R | 0.0010 | |||

| VOW3 GY | 0.1797 | 0.6583 | 10.4683 | 609.7016 | R | 0.0010 | 0.1397 | 0.4458 | 0.5869 | 5.3791 | 60.8111 | R | 0.0010 | |||||

| BNP FP | 0.1613 | 0.6240 | 6.3064 | 115.3370 | R | 0.0010 | 0.1887 | 0.5602 | 0.6176 | 0.8090 | 8.0523 | 293.1566 | R | 0.0010 | ||||

| DBK GY | 0.2125 | 0.7341 | 0.2452 | 7.3222 | 197.1055 | R | 0.0010 | 0.1986 | 0.5447 | 0.6598 | 0.4548 | 5.8678 | 94.2840 | R | 0.0010 | |||

| TEF SQ | 0.1022 | 0.3750 | 0.0187 | 6.6780 | 140.9284 | R | 0.0010 | 0.0570 | 0.1916 | 0.2015 | 0.1586 | 4.1838 | 15.6458 | R | 0.0045 | |||

| ISP IM | 0.1614 | 0.5905 | 8.4487 | 309.9411 | R | 0.0010 | 0.1460 | 0.2049 | 0.5107 | 7.3550 | 204.0519 | R | 0.0010 | |||||

| ENEL IM | 0.1682 | 0.4222 | 0.5062 | 11.0113 | 679.2366 | R | 0.0010 | 0.0743 | 0.3460 | 7.6000 | 249.7127 | R | 0.0010 | |||||

| C UN | 0.4290 | 1.1321 | 0.4480 | 10.2519 | 556.1805 | R | 0.0010 | 0.3188 | 1.2630 | 11.0411 | 688.1444 | R | 0.0010 | |||||

| MSFT UW | 0.1665 | 0.4995 | 0.7136 | 6.7986 | 171.5222 | R | 0.0010 | 0.0887 | 0.3860 | 0.3617 | 9.2412 | 417.0772 | R | 0.0010 | ||||

| RBS LN | 0.2773 | 1.0237 | 18.3559 | 2574.4868 | R | 0.0010 | 0.3050 | 1.4588 | 80.8619 | 64901.8805 | R | 0.0010 | ||||||

| ULVR LN | 0.0717 | 0.3922 | 4.0791 | 12.5204 | R | 0.0082 | 0.0936 | 0.2483 | 0.2625 | 0.5203 | 6.9602 | 174.6435 | R | 0.0010 | ||||

| Indexes’ Statistics | Indexes’ Statistics | |||||||||||||||||

| SPX Index | 0.1104 | 0.4304 | 0.1654 | 5.6222 | 72.7629 | R | 0.0010 | 0.0656 | 0.1518 | 0.2494 | 0.2158 | 5.2018 | 52.4405 | R | 0.0010 | |||

| SX5E Index | 0.1044 | 0.3899 | 0.3188 | 6.5992 | 139.1742 | R | 0.0010 | 0.0588 | 0.1536 | 0.2799 | 3.9723 | 10.9097 | R | 0.0116 | ||||

| UKX Index | 0.0962 | 0.4000 | 0.3106 | 6.6233 | 140.7746 | R | 0.0010 | 0.0443 | 0.2303 | 0.2622 | 3.9021 | 10.6280 | R | 0.0124 | ||||

| 2010 | 2011 | |||||||||||||||||

| Min Daily Return | Max Daily Return | Annual Mean | Annual std | Skewness | Kurtosis | JB | H | p-Value | Min Daily Return | Max Daily Return | Annual Mean | Annual std | Skewness | Kurtosis | JB | H | p-Value | |

| FP FP | 0.0737 | 0.2254 | 0.1622 | 5.7403 | 79.3164 | R | 0.0010 | 0.0476 | 0.2457 | 3.7736 | 8.7549 | R | 0.0197 | |||||

| SAN SQ | 0.2088 | 0.4453 | 1.4085 | 15.3195 | 1663.5904 | R | 0.0010 | 0.0913 | 0.3823 | 0.1693 | 4.0687 | 13.4584 | R | 0.0068 | ||||

| VOW3 GY | 0.0745 | 0.7057 | 0.3498 | 3.2736 | 0.7800 | A | 0.5000 | 0.0994 | 0.4342 | 0.1226 | 3.5902 | 4.3738 | A | 0.0893 | ||||

| BNP FP | 0.1898 | 0.4181 | 1.1895 | 13.1948 | 1141.6031 | R | 0.0010 | 0.1564 | 0.5922 | 0.2772 | 5.8701 | 91.5016 | R | 0.0010 | ||||

| DBK GY | 0.1210 | 0.3301 | 0.4727 | 7.2044 | 193.4445 | R | 0.0010 | 0.1428 | 0.4869 | 0.3426 | 6.0348 | 103.6490 | R | 0.0010 | ||||

| TEF SQ | 0.1131 | 0.2619 | 0.5956 | 13.1055 | 1078.5520 | R | 0.0010 | 0.0497 | 0.2695 | 4.2022 | 16.7312 | R | 0.0037 | |||||

| ISP IM | 0.1796 | 0.4205 | 1.0616 | 11.3222 | 768.4168 | R | 0.0010 | 0.0980 | 0.6431 | 4.4557 | 34.7431 | R | 0.0010 | |||||

| ENEL IM | 0.0767 | 0.2226 | 0.1074 | 6.9702 | 164.6747 | R | 0.0010 | 0.0703 | 0.3213 | 4.7037 | 41.0263 | R | 0.0010 | |||||

| C UN | 0.0731 | 0.4268 | 0.3605 | 3.7236 | 5.7664 | R | 0.0494 | 0.1290 | 0.4876 | 8.0922 | 289.8362 | R | 0.0010 | |||||

| MSFT UW | 0.0388 | 0.0029 | 0.2103 | -0.2385 | 3.7083 | 7.5948 | R | 0.0272 | 0.0433 | 0.2129 | 4.5799 | 28.7242 | R | 0.0010 | ||||

| RBS LN | 0.1200 | 0.2371 | 0.5011 | 9.3214 | 425.4745 | R | 0.0010 | 0.0958 | 0.5344 | 3.7965 | 7.9866 | R | 0.0241 | |||||

| ULVR LN | 0.0611 | 0.0314 | 0.2176 | 9.8276 | 505.4270 | R | 0.0010 | 0.0366 | 0.1324 | 0.1687 | 0.1154 | 3.3345 | 1.7682 | A | 0.3672 | |||

| Indexes’ Statistics | Indexes’ Statistics | |||||||||||||||||

| SPX Index | 0.0348 | 0.2020 | 0.1642 | 4.4570 | 25.6590 | R | 0.0011 | 0.0457 | 0.0300 | 0.1969 | 7.5329 | 237.5537 | R | 0.0010 | ||||

| SX5E Index | 0.0985 | 0.2363 | 0.7062 | 10.4500 | 598.9229 | R | 0.0010 | 0.0590 | 0.2885 | 4.5356 | 27.7334 | R | 0.0010 | |||||

| UKX Index | 0.0471 | 0.1329 | 0.1748 | 4.6341 | 27.9268 | R | 0.0010 | 0.0379 | 0.2004 | 4.3841 | 26.2260 | R | 0.0010 | |||||

Appendix B. Violations and Kupiec’s Portion of Failure Test 2008

| Violations and Kupiec’s POF-Test 2008 | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FP FP | SAN SQ | VOW3 GY | BNP FP | DBK GY | TEF SQ | ISP IM | ENEL IM | C UN | MSFT UW | RBS LN | ULVR LN | |||

| VaR | 1% | LR | 9.711 | 15.210 | 15.210 | 15.210 | 24.852 | 7.297 | 18.253 | 7.297 | 43.847 | 28.383 | 18.253 | 9.711 |

| H0 | R | R | R | R | R | R | R | R | R | R | R | R | ||

| VIOL | 9 | 11 | 11 | 11 | 14 | 8 | 12 | 8 | 19 | 15 | 12 | 9 | ||

| 2% | LR | 10.439 | 17.230 | 17.230 | 17.230 | 22.401 | 5.016 | 19.756 | 14.830 | 30.998 | 22.401 | 14.830 | 6.653 | |

| H0 | R | R | R | R | R | R | R | R | R | R | R | R | ||

| VIOL | 14 | 17 | 17 | 17 | 19 | 11 | 18 | 16 | 22 | 19 | 16 | 12 | ||

| 3% | LR | 13.864 | 35.598 | 22.612 | 13.864 | 25.038 | 6.860 | 35.598 | 18.039 | 27.553 | 27.553 | 13.864 | 4.132 | |

| H0 | R | R | R | R | R | R | R | R | R | R | R | R | ||

| VIOL | 20 | 29 | 24 | 20 | 25 | 16 | 29 | 22 | 26 | 26 | 20 | 14 | ||

| VaR 1% (decreasing) | linear (VaR 5%) | LR | 3.280 | 7.297 | 0.654 | 7.297 | 12.356 | 0.654 | 3.280 | 5.141 | 7.297 | 5.141 | 12.356 | 3.280 |

| H0 | A | R | A | R | R | A | A | R | R | R | R | A | ||

| VIOL | 6 | 8 | 4 | 8 | 10 | 4 | 6 | 7 | 8 | 7 | 10 | 6 | ||

| linear (VaR 1%) | LR | 0.654 | 3.280 | 0.059 | 7.297 | 9.711 | 0.152 | 0.654 | 3.280 | 7.297 | 1.762 | 12.356 | 0.654 | |

| H0 | A | A | A | R | R | A | A | A | R | A | R | A | ||

| VIOL | 4 | 6 | 3 | 8 | 9 | 2 | 4 | 6 | 8 | 5 | 10 | 4.000 | ||

| VaR 1% (increasing) | linear (VaR 5%) | LR | 0.059 | 0.152 | 0.059 | 0.654 | 1.762 | 0.152 | 0.654 | 3.280 | 1.762 | 0.654 | 1.762 | 0.654 |

| H0 | A | A | A | A | A | A | A | A | A | A | A | A | ||

| VIOL | 3 | 2 | 3 | 4 | 5 | 2 | 4 | 6 | 5 | 4 | 5 | 4 | ||

| linear (VaR 1%) | LR | 0.059 | 0.152 | 0.059 | 0.654 | 1.762 | 0.152 | 0.654 | 3.280 | 1.762 | 0.654 | 1.762 | 0.654 | |

| H0 | A | A | A | A | A | A | A | A | A | A | A | A | ||

| VIOL | 3 | 2 | 3 | 4 | 5 | 2 | 4 | 6 | 5 | 4 | 5 | 4 | ||

| VaR 1.5% (decreasing) | linear (VaR 5%) | LR | 3.361 | 8.811 | 4.955 | 8.811 | 15.990 | 2.027 | 8.811 | 2.027 | 30.880 | 13.431 | 11.033 | 3.361 |

| H0 | A | R | R | R | R | A | R | A | R | R | R | A | ||

| VIOL | 8 | 11 | 9 | 11 | 14 | 7 | 11 | 7 | 19 | 13 | 12 | 8 | ||

| linear (VaR 1%) | LR | 0.987 | 6.779 | 0.289 | 4.955 | 11.033 | 0.229 | 0.289 | 2.027 | 30.880 | 3.361 | 11.033 | 0.987 | |

| H0 | A | R | A | R | R | A | A | A | R | A | R | A | ||

| VIOL | 6 | 10 | 5 | 9 | 12 | 3 | 5 | 7 | 19 | 8 | 12 | 6 | ||

| VaR 1.5% (increasing) | linear (VaR 5%) | LR | 0.229 | 1.143 | 0.229 | 0.003 | 0.289 | 1.143 | 0.003 | 0.987 | 0.289 | 0.003 | 0.289 | 0.003 |

| H0 | A | A | A | A | A | A | A | A | A | A | A | A | ||

| VIOL | 3 | 2 | 3 | 4 | 5 | 2 | 4 | 6 | 5 | 4 | 5 | 4 | ||

| linear (VaR 1%) | LR | 0.229 | 1.143 | 0.229 | 0.003 | 0.289 | 1.143 | 0.003 | 0.987 | 0.289 | 0.003 | 0.289 | 0.003 | |

| H0 | A | A | A | A | A | A | A | A | A | A | A | A | ||

| VIOL | 3 | 2 | 3 | 4 | 5 | 2 | 4 | 6 | 5 | 4 | 5 | 4 | ||

References

- Artzner, Philippe, Freddy Delbaen, Jean-Marc Eber, and David Heath. 1997. Thinking Coherently. Risk 10: 68–71. [Google Scholar]

- Artzner, Philippe, Freddy Delbaen, Jean-Marc Eber, and David Heath. 1999. Coherent Measures of Risk. Mathematical Finance 9: 203–28. [Google Scholar] [CrossRef]

- Basel Committee on Banking Supervision. 1996a. Amendment to the Capital Accord to Incorporate Market Risks. Basel: Bank for International Settlements. [Google Scholar]

- Basel Committee on Banking Supervision. 1996b. Supervisory Framework for the Use of Backtesting in Conjunction with the Internal Models Approach to Market Risk Capital Requirements. Basel: Bank for International Settlements. [Google Scholar]

- Basel Committee on Banking Supervision. 2016. Minimum Capital Requirements for Market Risk. Basel: Bank for International Settlements. [Google Scholar]

- Berkowitz, Jeremy, Peter Christoffersen, and Denis Pelletier. 2011. Evaluating Value at Risk Models with Desk Level Data. Management Science 57: 2213–27. [Google Scholar] [CrossRef]

- Burzoni, Matteo, Ilaria Peri, and Chiara M. Ruffo. 2017. On the Properties of the Lambda Value at Risk: Robustness, Elicitability and Consistency. Quantitative Finance 17: 1735–43. [Google Scholar] [CrossRef]

- Campbell, Sean D. 2005. A Review of Backtesting and Backtesting Procedures. Finance and Economics Discussion Series. Washington: Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board. [Google Scholar]

- Casella, George, and Roger L. Berger. 2002. Statistical Inference. Duxbury: Duxbury Press. [Google Scholar]

- Christoffersen, Peter. 2010. Encyclopedia of Quantitative Finance—Backtesting. West Sussex: John Wiley and Sons. [Google Scholar]

- Corbetta, Jacopo, and Ilaria Peri. 2017. Backtesting Lambda Value at Risk. European Journal of Finance. [Google Scholar] [CrossRef]

- Embrechts, Paul, and Marius Hofert. 2014. Statistics and Quantitative Risk Management for Banking and Insurance. Annual Review of Statistics and Its Application 1: 493–514. [Google Scholar] [CrossRef]

- Engle, Robert. 2001. GARCH 101: The use of ARCH/GARCH models in applied econometrics. Journal of Economic Perspectives 15: 157–68. [Google Scholar] [CrossRef]

- Engle, Robert F., Sergio M. Focardi, and Frank J. Fabozzi. 2008. ARCH/GARCH models in applied financial econometrics. In Handbook of Finance. Hoboken: John Wiley & Sons, Inc. [Google Scholar]

- Frittelli, Marco, Marco Maggis, and Ilaria Peri. 2014. Risk Measures on P(R) and Value at Risk with Probability/Loss Function. Mathematical Finance 24: 442–63. [Google Scholar] [CrossRef]

- Gneiting, Tilmann. 2011. Making and Evaluating Point Forecasts. Journal of the American Statistical Association 106: 746–62. [Google Scholar] [CrossRef]

- Jorion, Philippe. 2007. Value at Risk, The New Benchmark for Managing Financial Risk. New York: McGraw-Hill. [Google Scholar]

- Kupiec, Paul. 1995. Techniques for Verifying the Accuracy of Risk Measurement Models. Journal of Derivatives 3: 73–84. [Google Scholar] [CrossRef]

- Samitas, Aristeidis, and Elias Kampouris. 2017. Financial Illness and Political Virus: The Case of Contagious Crises in the Eurozone. International Review of Applied Economics. [Google Scholar] [CrossRef]

| 1 | See Corbetta and Peri (2017) for a detailed study on the backtesting of the . The authors improved on the backtesting of the and based their empirical findings on the estimation proposal introduced in the current paper. |

| Violations (Historical Simulation) | Kupiec’s POF-Test (Historical Simulation) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2006 (T = 261) | 2007 (T = 259) | 2008 (T = 260) | 2009 (T = 261) | 2010 (T = 263) | 2011 (T = 264) | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||

| VaR | 1% | 3.42 | 5.33 | 11.58 | 0.75 | 3.08 | 6.83 | 100% | 83% | 0% | 100% | 92% | 50% |

| 2% | 5.25 | 9.17 | 16.50 | 1.17 | 5.50 | 10.25 | 100% | 83% | 0% | 67% | 92% | 50% | |

| 3% | 9.33 | 15.42 | 22.58 | 2.92 | 7.58 | 14.83 | 92% | 50% | 0% | 50% | 83% | 42% | |

| 6 | 9.97 | 16.89 | 1.61 | 5.39 | 10.64 | 97% | 72% | 0% | 72% | 89% | 47% | ||

| (decr) | linear (VaR 5%) | 2.25 | 3.67 | 7.00 | 0.67 | 2.00 | 4.25 | 100% | 83% | 42% | 100% | 100% | 83% |

| linear (VaR 1%) | 2.17 | 2.33 | 5.75 | 0.67 | 1.58 | 4.00 | 100% | 83% | 67% | 100% | 100% | 83% | |

| 2.21 | 3.00 | 6.38 | 0.67 | 1.79 | 4.13 | 100% | 83% | 54% | 100% | 100% | 83% | ||

| (incr) | linear (VaR 5%) | 1.17 | 1.00 | 3.92 | 0.42 | 0.92 | 2.75 | 100% | 100% | 100% | 100% | 100% | 100% |

| linear (VaR 1%) | 1.17 | 1.00 | 3.92 | 0.42 | 1.00 | 2.75 | 100% | 100% | 100% | 100% | 100% | 100% | |

| 1.17 | 1.00 | 3.92 | 0.42 | 0.96 | 2.75 | 100% | 100% | 100% | 100% | 100% | 100% | ||

| (decr) | linear (VaR 5%) | 3.33 | 5.00 | 10.83 | 0.75 | 3.00 | 6.67 | 100% | 83% | 33% | 100% | 100% | 58% |

| linear (VaR 1%) | 2.92 | 3.67 | 8.50 | 0.67 | 2.33 | 5.92 | 100% | 83% | 58% | 100% | 100% | 67% | |

| 3.13 | 4.33 | 9.67 | 0.71 | 2.67 | 6.29 | 100% | 83% | 46% | 100% | 100% | 63% | ||

| (incr) | linear (VaR 5%) | 1.17 | 1.00 | 3.92 | 0.42 | 0.92 | 2.75 | 100% | 100% | 100% | 100% | 100% | 100% |

| linear (VaR 1%) | 1.17 | 1.00 | 3.92 | 0.42 | 1.00 | 2.83 | 100% | 100% | 100% | 100% | 100% | 100% | |

| 1.17 | 1.00 | 3.92 | 0.42 | 0.96 | 2.79 | 100% | 100% | 100% | 100% | 100% | 100% | ||

| Violations (Montecarlo Normal) | Kupiec’s POF-Test (Montecarlo Normal) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||

| VaR | 1% | 4.42 | 6.92 | 15.17 | 1.5 | 4.25 | 9.5 | 83% | 50% | 0% | 100% | 83% | 25% |

| 2% | 6.92 | 10 | 19.58 | 3 | 5.92 | 13.58 | 100% | 50% | 0% | 83% | 83% | 33% | |

| 3% | 9.08 | 12.5 | 22.67 | 3.92 | 8 | 17.17 | 83% | 58% | 0% | 58% | 75% | 25% | |

| 6.81 | 9.81 | 19.14 | 2.81 | 6.06 | 13.42 | 89% | 53% | 0% | 81% | 81% | 28% | ||

| (decr) | linear (VaR ) | 4.33 | 6.58 | 14.33 | 1.5 | 3.83 | 9.08 | 92% | 50% | 0% | 100% | 83% | 25% |

| linear (VaR ) | 4.17 | 5.5 | 13 | 1.17 | 3.33 | 8.75 | 92% | 83% | 0% | 100% | 92% | 33% | |

| 4.25 | 6.04 | 13.67 | 1.33 | 3.58 | 8.92 | 92% | 67% | 0% | 100% | 88% | 29% | ||

| (incr) | linear (VaR ) | 1.83 | 2.67 | 8.33 | 0.75 | 1.58 | 5.17 | 100% | 92% | 25% | 100% | 100% | 58% |

| linear (VaR 1%) | 1.92 | 3.83 | 10.17 | 1.08 | 2 | 5.58 | 100% | 75% | 8% | 100% | 92% | 58% | |

| 1.88 | 3.25 | 9.25 | 0.92 | 1.79 | 5.38 | 100% | 83% | 17% | 100% | 96% | 58% | ||

| (decr) | linear (VaR ) | 5 | 7.92 | 16.17 | 2.17 | 4.75 | 11.08 | 92% | 58% | 0% | 100% | 92% | 33% |

| linear (VaR ) | 4.83 | 6.67 | 13.67 | 1.75 | 4.08 | 10.42 | 92% | 83% | 8% | 100% | 100% | 33% | |

| 4.92 | 7.29 | 14.92 | 1.96 | 4.42 | 10.75 | 92% | 71% | 4% | 100% | 96% | 33% | ||

| (incr) | linear (VaR ) | 1.83 | 3.25 | 8.67 | 0.75 | 1.67 | 5.25 | 100% | 92% | 58% | 100% | 100% | 92% |

| linear (VaR 1%) | 2.42 | 4.92 | 11.58 | 1.08 | 2.5 | 5.83 | 100% | 75% | 33% | 100% | 92% | 83% | |

| VaR | 1% | 3 | 6.83 | 15.17 | 0.25 | 0.75 | 4.17 | 100% | 75% | 0% | 100% | 100% | 67% |

| 2% | 5 | 11.17 | 19.58 | 0.92 | 2.08 | 7.83 | 83% | 58% | 0% | 75% | 92% | 67% | |

| 3% | 7.5 | 14.08 | 22.67 | 1.92 | 3.08 | 12.08 | 100% | 58% | 0% | 50% | 75% | 67% | |

| 5.17 | 10.69 | 19.14 | 1.03 | 1.97 | 8.03 | 94% | 64% | 0% | 75% | 89% | 67% | ||

| (decr) | linear (VaR ) | 2.83 | 5.58 | 14.33 | 0.25 | 0.33 | 4.08 | 100% | 83% | 0% | 100% | 100% | 75% |

| linear (VaR ) | 2.67 | 4.75 | 13 | 0.17 | 0.17 | 3.75 | 100% | 83% | 0% | 100% | 100% | 75% | |

| 2.75 | 5.17 | 13.67 | 0.21 | 0.25 | 3.92 | 100% | 83% | 0% | 100% | 100% | 75% | ||

| (incr) | linear (VaR ) | 0.5 | 0.75 | 8.33 | 0 | 0.25 | 0.58 | 100% | 100% | 25% | 100% | 100% | 100% |

| linear (VaR 1%) | 0.5 | 1.17 | 10.17 | 0 | 0.5 | 0.75 | 100% | 100% | 8% | 100% | 100% | 100% | |

| 0.5 | 0.96 | 9.25 | 0 | 0.38 | 0.67 | 100% | 100% | 17% | 100% | 100% | 100% | ||

| (decr) | linear (VaR ) | 3.92 | 7.58 | 16.17 | 0.5 | 0.92 | 5.75 | 100% | 75% | 0% | 100% | 100% | 75% |

| linear (VaR ) | 3.33 | 5.83 | 13.67 | 0.25 | 0.5 | 5.42 | 100% | 83% | 8% | 100% | 100% | 83% | |

| 3.63 | 6.71 | 14.92 | 0.38 | 0.71 | 5.58 | 100% | 79% | 4% | 100% | 100% | 79% | ||

| (incr) | linear (VaR ) | 0.5 | 0.83 | 8.67 | 0 | 0.5 | 0.67 | 100% | 100% | 58% | 100% | 100% | 100% |

| linear (VaR 1%) | 0.5 | 1.58 | 11.58 | 0 | 0.67 | 0.83 | 100% | 100% | 33% | 100% | 100% | 100% | |

| 0.5 | 1.21 | 10.13 | 0 | 0.58 | 0.75 | 100% | 100% | 46 % | 100% | 100% | 100% | ||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hitaj, A.; Mateus, C.; Peri, I. Lambda Value at Risk and Regulatory Capital: A Dynamic Approach to Tail Risk. Risks 2018, 6, 17. https://doi.org/10.3390/risks6010017

Hitaj A, Mateus C, Peri I. Lambda Value at Risk and Regulatory Capital: A Dynamic Approach to Tail Risk. Risks. 2018; 6(1):17. https://doi.org/10.3390/risks6010017

Chicago/Turabian StyleHitaj, Asmerilda, Cesario Mateus, and Ilaria Peri. 2018. "Lambda Value at Risk and Regulatory Capital: A Dynamic Approach to Tail Risk" Risks 6, no. 1: 17. https://doi.org/10.3390/risks6010017

APA StyleHitaj, A., Mateus, C., & Peri, I. (2018). Lambda Value at Risk and Regulatory Capital: A Dynamic Approach to Tail Risk. Risks, 6(1), 17. https://doi.org/10.3390/risks6010017